Data Center Colocation Market Size, Trends and Insights By Type (Retail Colocation, Wholesale Colocation, Hybrid Colocation), By Tier Level (Tier 1, Tier 2, Tier 3, Tier 4), By Enterprise Size (Large Enterprises, SMEs), By End Use (Retail, IT & Telecom, BFSI, Healthcare, Media & Entertainment, Others), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 14.5%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia-Pacific |

| Largest Market: | North America |

Major Players

- Digital Realty Trust

- Zayo Group LLC

- CoreSite

- CyrusOne

- Others

Reports Description

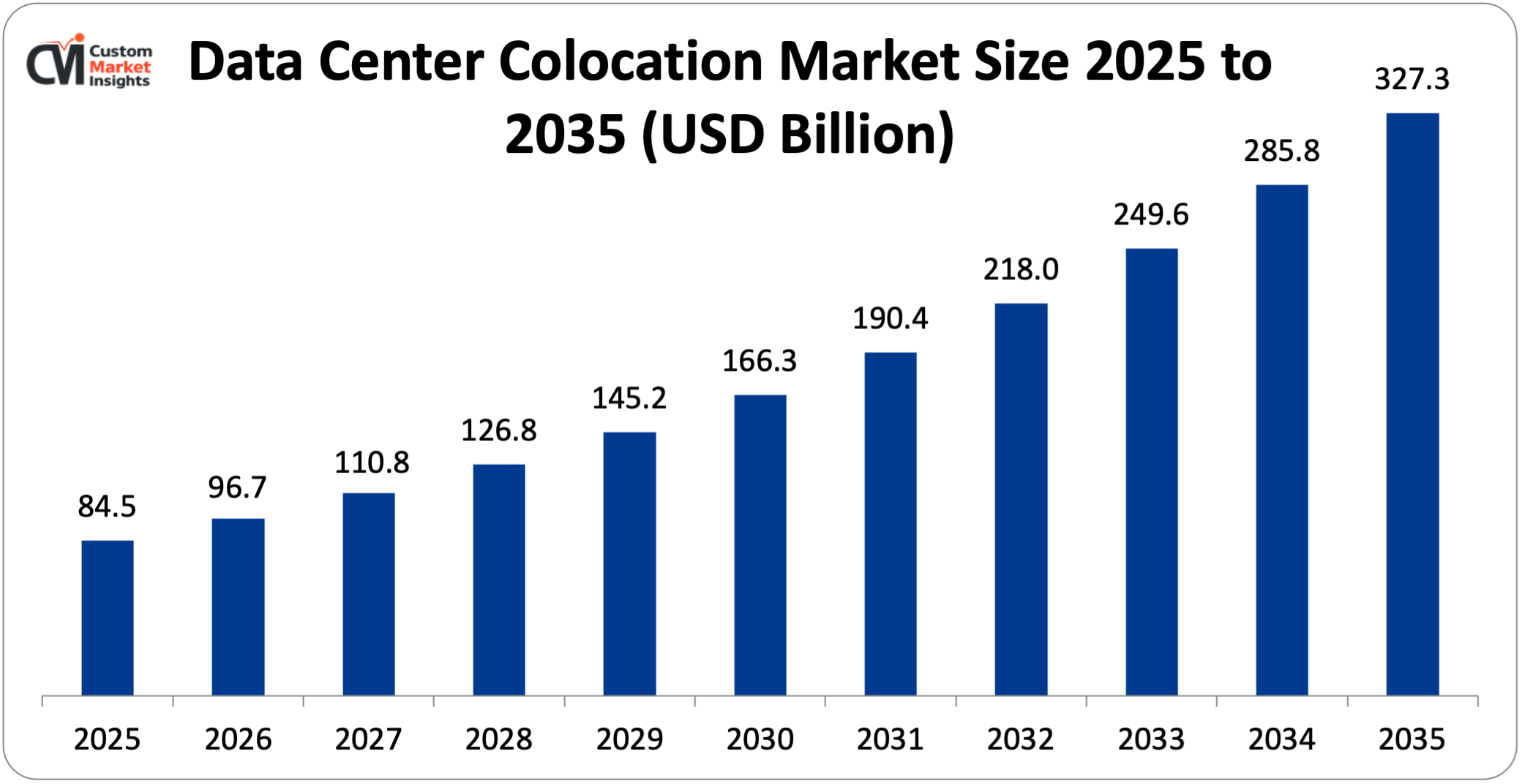

The market size of global data center colocation will be estimated at USD 84.5 billion in 2025 and is expected to grow to between USD 96.7 billion in 2026 and about USD 327.3 billion by 2035, with a current CAGR (compound annual growth rate) of 14.5% during the period of 2026 to 2035. Data Center Colocation is an off-site facility that companies lease space in, purchasing power, cooling, and connectivity resources from an external data center floor to use for their servers and other hardware.

It provides a service of providing an onsite data center without the costs of building, designing, and managing it by providing their hardware with the facilities of a data center with full availability, security, and redundancy; the colocation facility brings ‘additional infrastructure such as backup power stations, the latest cooling technology, physical security, and high-speed interconnected networks.

Market Highlight

- In 2025, North America will dominate the global market with an estimated market share of 39%. The presence of major players and continuous product launches in the region drives the market growth.

- The Asia Pacific is growing at the highest CAGR over the analysis period. The increasing digital transformation in countries like India and China.

- By type, the retail colocation segment dominated the industry in 2025 with a market share of over 70%.

- By tier level, the tier 3 segment captures the largest market share in 2025 of over 55%.

- By end use, the IT & telecom segment captures the highest revenue share of 30% in 2025.

Significant Growth Factors

The data center colocation market trends present significant growth opportunities due to several factors:

- Growing Adoption of Cloud Computing & Hybrid IT: The surge in usage of cloud computing and hybrid IT is a significant factor for the rapid growth in the data center colocation market. As more companies migrate to cloud-based services but continue to deploy some workloads on physical hardware, hybrid IT environments are emerging as the preferred model. Colocation facilities offer an optimal link between on-premise data center environments and traditional private and public clouds, significantly enhancing workload flexibility and visibility and numerous benefits associated with cost reduction and control management. The needs of enterprises for flexible, cost-effective, and high-speed access to compute resources are consequently boosting the colocation demand.

- Cost Efficiency & Operational Flexibility: Cost efficiencies and flexibility are cited among the key drivers behind the rise of the Data Center Colocation market. The colocation business model provides ‘scaled’ access, as either a dedicated or shared service, to all data center infrastructure, including power, cooling, and security, while reducing maintenance and consumption costs in return. As well as cost efficiencies, it provides much increased flexibility, as ‘it is a much more agile way of provisioning and de-provisioning data processing power in response to changing market conditions and IT requirements.

What are the Major Advances Changing the Data Center Colocation Market Today?

- Advanced Cooling Technologies (Liquid & Immersion Cooling): Advanced Cooling Technologies (Liquid & Immersion Cooling) are some of the most disruptive innovations changing the Data Center Colocation Market, especially with the advent of AI, HPC and the formation of high-density server environments. Conventional air-cooling solutions become logistically impractical and increasingly ineffective in reigning in the production of heat in high-density server environments. Liquid cooling (delivering coolant directly to the heat producer) and immersion cooling (making part of the server get entirely immersed in a thermally conductive, yet nonconductive fluid) provide much more efficient heat dissipation, optimized energy efficiency, and minimized physical space usage. This not only lowers the Power Usage Effectiveness (PUE) but also equips colocation providers with the ability to support the next phases of high-performance, high-density workloads. Product innovation within the liquid cooling space has seen Vertiv (formerly Liebert) introducing liquid cooling product lines such as the Liebert(R) XDU coolant distribution units, which help in effectively removing heat from high-density racks. However, Schneider Electric has also launched comprehensive liquid cooling and rear-door heat exchanger solutions that can be easily integrated into existing colocation infrastructure. In the immersion cooling market, Submer introduced their modular SmartPod systems that fully immersed high-performance servers in dielectric fluid for strong cost savings and ultra-high-density server deployments.

- Rise of Edge Computing & Distributed Infrastructure: Emergence of edge computing & distributed infrastructure is a key development that is revolutionizing the data center colocation industry. Digital applications, including IoT, autonomous systems, video streaming, and 5G-enabled services, require the processing of large volumes of data in real time. Require processing of large volumes of data in real time; a single centralized data center is not enough to meet the bandwidth and latency needs. Advanced colocation service providers are transforming the industry by deploying multiple smaller data centers with distributed architecture across geographies, which are clustered in the proximity of the end-users, application requests, or users. Edge computing ensures improved application performance and customer experience by minimizing the latency. This is expected to be adopted at a faster rate in industrial segments such as telecom, healthcare, manufacturing, and smart cities. Operators are building edge-ready colocation centers by working on the default architecture of data, power, cooling, and security. For example, colocation giants like Equinix are constantly increasing their edge infrastructure by application of their Network Edge platform that is capable of deploying virtual network services near endpoints without requiring substantial investment in hardware. It is also launching Digital Realty-PlatformDIGITAL(R), which helps in transferring data at a rapid pace between core, edge, and cloud environments. Similarly, American Tower is using its ubiquitous tower base to establish colocation data centers that help applications to operate in 5G and low-latency settings. These innovations are significantly changing the colocation industry by shifting focus from traditional nodes to dynamic distributed ecosystems, which enable faster functioning, high bandwidth, and ease of establishing new services.

Category Wise Insights

By Type

Why Retail Colocation Hold a Prominent Position in the Market?

The retail colocation segment dominated the industry in 2025 with a market share of over 70%. Retail colocation has the option for businesses to rent smaller areas within a data center—this is suitable if the amount of data is smaller and the infrastructure needed is not as enormous. The fact that this is cheaper has led to a large take-up by SMEs, as it offers them secure, reliable, and scalable IT infrastructure at a low cost, without the need to build data centers themselves. The overall low-budget aspect is appealing to SMEs, and so this model has proven popular.

The wholesale colocation segment is growing at the highest CAGR of 18.6% over the analysis period. The main cloud giants like Google and Amazon are also coming into the wholesale storage sector to cater to their enterprise customers, who require a very high amount of storage and infrastructure. Big businesses have millions of customers who all require large-sized sites that can be expanded to sizable limits and require secure sites for their servers—the size of their digital requirements is what makes large companies such as these a major contributor to the success of the wholesale colocation sector and thus the market.

By Tier Level

Why Tier 3 Capture the Highest Market Share in the Data Center Colocation Market?

The tier 3 segment captures the largest market share in 2025 of over 55%. Enterprises, CSPs, financial service institutions, and technology companies drive this growth by demanding high reliability, scalability, and redundancy. Tier 3 data center specifications cater to up to 99.982% uptime hours (~ 1.6 hours of outage annually) with N+1 redundancy for power and cooling. As such, most Tier 3 and Tier 3-equivalent facilities cater to hybrid cloud for the most critical use cases, such as Mission Critical workloads, virtualization, digital transformation, and large enterprise data centers.

The tier 4 segment is growing at the highest rate over the projected period. The proliferation of hyperscale cloud providers, driven by artificial intelligence (AI) and high-performance computing (HPC), is accelerating the need for Tier 4 colocation facilities. High-performance workloads and the heavy computing power requirements of data-intensive applications and deep learning models demand the advanced data center infrastructure that Tier 4 colocation centers can provide.

By Enterprise Size

Why Does Large Enterprise Dominate the Data Center Colocation Market?

The large enterprises segment held the largest market share in 2025 of more than 48%. Maintaining high availability of one‘s business is a key concern for large organizations, particularly for those with mission-critical applications like financial transactions, cloud SaaS applications, or government operations. In a colocation data center, redundant power sources, generator backup, disaster recovery facilities, and geographically diverse equipment can guarantee 99.999% uptime, with an extremely low Downtime risk, which makes enterprises’ business continuity plans easier, whether time replication, failover, or real-time data recovery.

The SMEs segment is growing at a rapid rate over the projected period. Continuing rapid increase of the number of software-as-a-service startups, fintech companies, and digital-first SMEs leads to demands in the infrastructure-as-a-service environment for safe, reliable, and high-performance colocation services. These companies need flexible IT infrastructure to support 24/7 programming and use of cloud-native applications and real-time FX-based transactions. Colocation provides enterprise-grade infrastructure that can quickly innovate these startups and technology-smart SMEs.

By End Use

Why Does IT & Telecom Hold a Prominent Share in the Data Center Colocation Market?

The IT & telecom segment captures the highest revenue share of 30% in 2025. Global rollout of 5G is one of the main reasons for colocation data centers, with telecom operators demanding the connection to be closer and deliver low-latency infrastructure to enable such high-speed networks. They anticipate that more than 60% of the world‘s population will be covered by 5G networks by 2027; that would drive the need for net edge data centers to host data closer to people. Colocation facilities provide high-speed fiber connections, neutral ecosystems, and edge computing, enabling telecom players to relieve congested networks, deliver far better performance for mobile broadband, and support new applications such as IoT, smart cities, and self-driving vehicles.

The healthcare segment is growing at a rapid rate over the projected period. The healthcare industry is experiencing a digital revolution using EHRs, telemedicine, AI-enabled diagnostics, and medical IoT (IoMT). Large volumes of patient data, real-time applications, and regulatory requirements demand high-performance, reliable, and scalable IT infrastructure.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 96.7 billion |

| Projected Market Size in 2035 | USD 327.3 billion |

| Market Size in 2025 | USD 84.5 billion |

| CAGR Growth Rate | 14.5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Tier Level, Enterprise Size, End Use and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is North America Data Center Colocation Market Size?

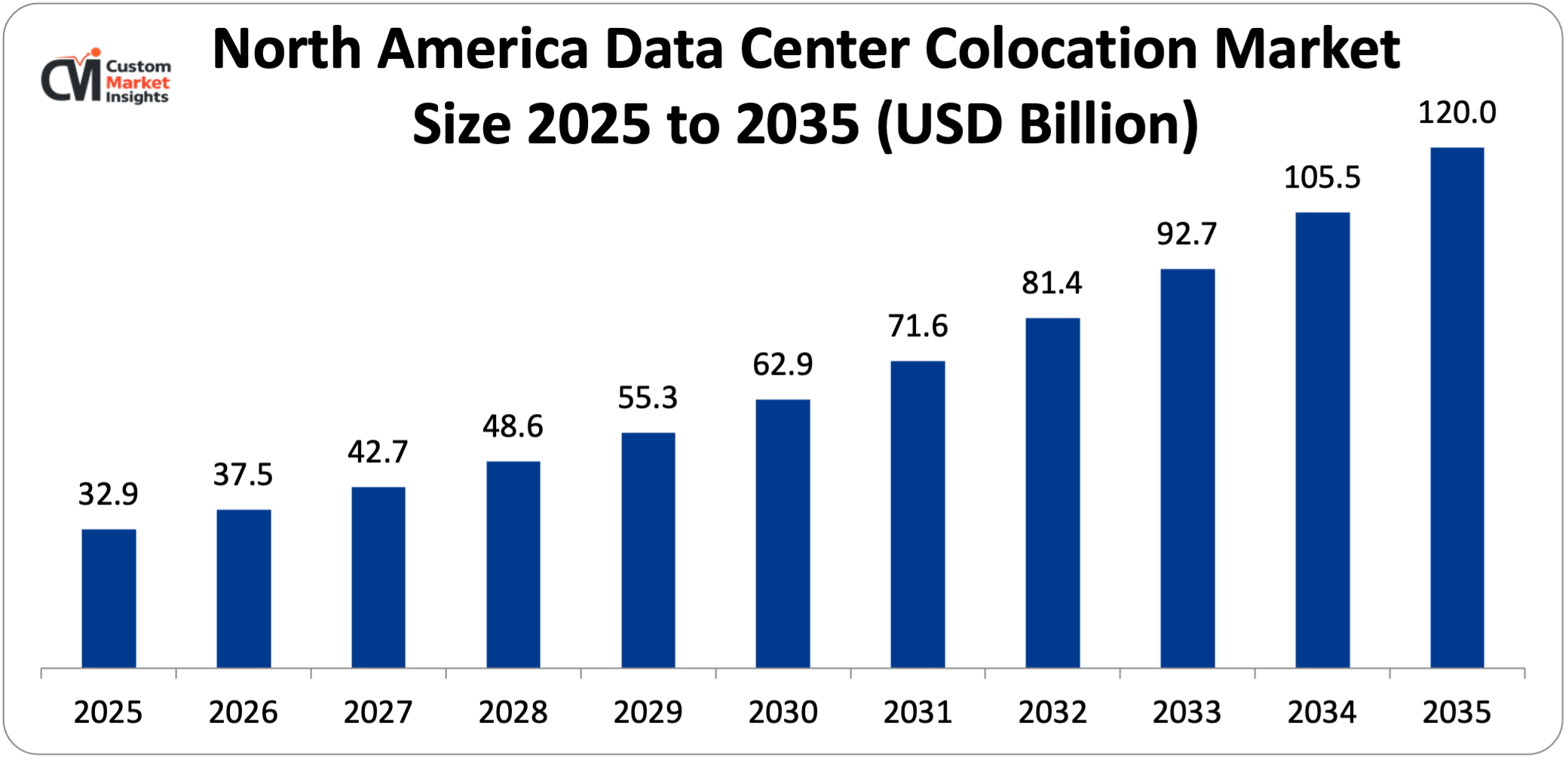

Its market size, in terms of North American data center colocation, is projected to be USD 32.9 billion in 2025 with a growth of about USD 120.0 billion in 2035 with a CAGR of 13.8% between 2026 and 2035.

Why did North America Dominate the Data Center Colocation Market in 2025?

In 2025, North America will dominate the global market with an estimated market share of 39%. The growth reflects the rapid growth of the cloud computing industry, artificial intelligence workloads, and enterprise digitalization. The large hyperscale presence in the region (AWS, Microsoft Azure, and Google Cloud) ensures constant demand for high-performance, interconnected colocation facilities. The rise of 5G, IoT, and edge computing is also growing a large ecosystem of edge colocation in the dominant markets of Northern Virginia, Dallas, and Silicon Valley.

US Data Center Colocation Market Trends

In the North American region, the US leads the industry expansion over the projected period. The growth in the region is due to the increasing collaboration among the key market players. For instance, in March 2026, Fidium, a leading provider of high-capacity fiber solutions for networks, announced an increased partnership with Flexential, a leading provider of data center colocation and hybrid IT solutions. By utilizing the Flexential Marketplace, a channel within the recently announced FlexAnywhere(R) platform, Fidium will improve its reach and prominence in Flexential data centers located in Dallas and Plano, Texas, and Minneapolis–St. Paul, Minnesota, allowing enterprises, carriers, and hyperscalers to accelerate connectivity in ways never before seen. The pact capitalizes on Fidium’s ever-expanding national data center footprint and strategic alliances, providing the backbone for enterprises’ AI, cloud, and edge processing needs with direct access to 100G and 800G Wavelength services, Ethernet, Dark Fiber, and Construction-as-a-Service (CaaS) packages.

Why is Europe Experiencing Significant Growth in the Data Center Colocation Market?

Europe holds a significant market share in 2025. Europe is growing due to increasing cloud adoption, strict data protection regulations (GDPR), and enterprise IT modernization. Countries like Germany, UK and the Netherlands are prime colocation markets thanks to mature connectivity infrastructure and a business-friendly environment. Increasing adoption of AI ready, high-density colocation space is expected to drive the market further.

UK Data Center Colocation Market Trends

The UK held the dominant position in the market in 2025. The country’s growth is mainly led by the growth of the hybrid cloud revolution, AI investments, and the financial services sector that needs the secure and high-performance colocation facilities. London is still a top-tier colocation hub, with direct connections to Western cloud providers and many large financial institutions. The new post-Brexit data sovereignty post also makes more and more companies store their data within the country, driving the request for Tier 3/4 colocation.

Why is the Asia Pacific Growing at the Highest CAGR in the Data Center Colocation Market?

The Asia Pacific is expected to grow at the highest CAGR over the projected period. The market is growing rapidly, underpinned by the accelerating digital economies and AI operated businesses and the deployment of cloud computing services. Hyperscale colocation hosting investment is pouring into major Asian cities—Singapore, Tokyo, and Sydney—targeting the rapidly growing internet penetration and e-commerce economic activities, as well as the adoption of 5G networks and smart city projects, which brings in more colocation demand.

Japan Data Center Colocation Market Trends

Japan holds the prominent market share in the industry. The rapid development of AI, IoT, and digitization enabled by 5G has made Tokyo and Osaka significant colocation locations in their own right. As key access points for cloud computing, gaming, and financial services, Japan’s colocation industry requires ultra-low latency and a resilient data center facility environment. Growing demand for data privacy regulations (APPI) and escalating cyberattacks will also drive colocation investment.

Why is the Middle East & Africa Region is growing rapidly in the Data Center Colocation?

The MEA region is growing at a steady rate over the projected period. The region has experienced unprecedented growth, fuelled by accelerated digitalization, growing internet adoption, and increasing investments into smart infrastructure. Countries like the UAE, Saudi Arabia, and South Africa are established hubs, as they are paving the way to becoming digital economies with increased regional demand for scalable and secure data storage and colocation requirements through government-driven initiatives like the smart city rollouts and national digital strategies, which are aimed at increasing digital adoption. Increasing cloud adoption, Fintech groups and e-commerce and cloud companies is translating into growing colocation demands from enterprises looking for latency-sensitive and reliable hosting options. The region has seen increased investment from the global cloud providers and colocation players in improving infrastructure capacity.

UAE Data Center Colocation Market Trends

The UAE is growing at the highest CAGR during the forecast period. This growth is mainly driven by the growth of hyperscale cloud providers, increasing adoption of AI, IoT, 5G, etc. Favorable government policies are being implemented to support the development of smart cities and digital economies in locations such as Dubai, Abu Dhabi, and others.

Top Players in the Data Center Colocation Market and Their Offerings

- Digital Realty Trust

- Zayo Group LLC

- Colt Technology Services Group Limited

- CoreSite

- CyrusOne

- Centersquare

- China Telecom Corporation Limited

- Equinix Inc.

- Flexential

- Iron Mountain Inc.

- NTT Ltd. (NTT DATA)

- QTS Realty Trust LLC

- Rackspace Technology

- Telehouse (KDDI CORPORATION)

- Cologix

- Others

Key Developments

Data center colocation market has experienced considerable changes in the last two years as the market players are trying to diversify their technological aspects and develop product portfolios using strategic approaches.

- In March 2026, HIVE Digital Technologies Ltd., a global leader in sustainable digital infrastructure and AI compute, through its wholly owned subsidiary BUZZ High Performance Computing (“BUZZ”), announced a 4x expansion of its liquid-cooled AI data center capacity through its previously announced strategic data center partner in Canada, growing the existing 4 megawatts (“MW”) in Manitoba to 16.6 MW of critical IT load across two Canadian provinces (all figures referenced herein are in critical IT load), expanding HIVE’s BUZZ HPC Sovereign AI Compute offering in Canada (all amounts in US dollars, unless otherwise indicated). (https://www.tradingview.com/news/tmx_newsfile:a8afc7ef6094b:0-hive-s-buzz-hpc-expands-data-center-footprint-into-british-columbia-with-4-times-growth-in-liquid-cooled-ai-data-center-capacity/)

- In April 2025, Apollo announced that Apollo-managed infrastructure funds (the “Apollo Funds”) have agreed to acquire the European colocation business developed and managed by STACK Infrastructure, a portfolio company of Blue Owl Digital Infrastructure Advisors LLC (“BODI”) in a carve-out transaction. (https://www.apollo.com/insights-news/pressreleases/2025/04/apollo-funds-to-acquire-pan-european-highly-interconnected-colocation-data-center-business-from-stack-infrastructure-a-portfolio-company-of-blue-owl-digital-infrastructure-3069871)

These strategic measures have enabled the companies to reinforce their competitive positions, increase the product line, boost their technological competencies and also seize growth opportunities in the fast-growing data center colocation market.

The Data Center Colocation Market is segmented as follows:

By Type

- Retail Colocation

- Wholesale Colocation

- Hybrid Colocation

By Tier Level

- Tier 1

- Tier 2

- Tier 3

- Tier 4

By Enterprise Size

- Large Enterprises

- SMEs

By End Use

- Retail

- IT & Telecom

- BFSI

- Healthcare

- Media & Entertainment

- Others

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Data Center Colocation by Segments

- 2.1.2. Data Center Colocation by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Data Center Colocation Market Attractiveness Analysis, By Type

- 2.2.3. Data Center Colocation Market Attractiveness Analysis, By Tier Level

- 2.2.4. Data Center Colocation Market Attractiveness Analysis, By Enterprise Size

- 2.2.5. Data Center Colocation Market Attractiveness Analysis, By End Use

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Growing Adoption of Cloud Computing & Hybrid IT

- 3.1.2. Cost Efficiency & Operational Flexibility

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Data Center Colocation Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Data Center Colocation Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Retail Colocation

- 4.1.3. Data Center Colocation Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Wholesale Colocation

- 4.1.7. Data Center Colocation Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Hybrid Colocation

- 4.1.11. Data Center Colocation Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Data Center Colocation Market – By Tier Level

- 5.1. Tier Level Market Overview, By Tier Level Segment

- 5.1.1. Data Center Colocation Market Revenue Share, By Tier Level, 2025 & 2035

- 5.1.2. Tier 1

- 5.1.3. Data Center Colocation Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Tier 2

- 5.1.7. Data Center Colocation Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Tier 3

- 5.1.11. Data Center Colocation Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Tier 4

- 5.1.15. Data Center Colocation Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Tier Level Market Overview, By Tier Level Segment

- Chapter 6. Data Center Colocation Market – By Enterprise Size

- 6.1. Enterprise Size Market Overview, By Enterprise Size Segment

- 6.1.1. Data Center Colocation Market Revenue Share, By Enterprise Size, 2025 & 2035

- 6.1.2. Large Enterprises

- 6.1.3. Data Center Colocation Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. SMEs

- 6.1.7. Data Center Colocation Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Enterprise Size Market Overview, By Enterprise Size Segment

- Chapter 7. Data Center Colocation Market – By End Use

- 7.1. End Use Market Overview, By End Use Segment

- 7.1.1. Data Center Colocation Market Revenue Share, By End Use, 2025 & 2035

- 7.1.2. Retail

- 7.1.3. Data Center Colocation Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. IT & Telecom

- 7.1.7. Data Center Colocation Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. BFSI

- 7.1.11. Data Center Colocation Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Healthcare

- 7.1.15. Data Center Colocation Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Media & Entertainment

- 7.1.19. Data Center Colocation Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Others

- 7.1.23. Data Center Colocation Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End Use Market Overview, By End Use Segment

- Chapter 8. Data Center Colocation Market – Regional Analysis

- 8.1. Data Center Colocation Market Overview, By Region Segment

- 8.1.1. Global Data Center Colocation Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Data Center Colocation Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Data Center Colocation Market Revenue, By Type, 2026 – 2035

- 8.1.4. Global Data Center Colocation Market Revenue, By Tier Level, 2026 – 2035

- 8.1.5. Global Data Center Colocation Market Revenue, By Enterprise Size, 2026 – 2035

- 8.1.6. Global Data Center Colocation Market Revenue, By End Use, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Data Center Colocation Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Data Center Colocation Market Revenue, By Type, 2026 – 2035

- 8.2.3. North America Data Center Colocation Market Revenue, By Tier Level, 2026 – 2035

- 8.2.4. North America Data Center Colocation Market Revenue, By Enterprise Size, 2026 – 2035

- 8.2.5. North America Data Center Colocation Market Revenue, By End Use, 2026 – 2035

- 8.2.6. U.S. Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Data Center Colocation Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Data Center Colocation Market Revenue, By Type, 2026 – 2035

- 8.3.3. Europe Data Center Colocation Market Revenue, By Tier Level, 2026 – 2035

- 8.3.4. Europe Data Center Colocation Market Revenue, By Enterprise Size, 2026 – 2035

- 8.3.5. Europe Data Center Colocation Market Revenue, By End Use, 2026 – 2035

- 8.3.6. Germany Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Data Center Colocation Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Data Center Colocation Market Revenue, By Type, 2026 – 2035

- 8.4.3. Asia Pacific Data Center Colocation Market Revenue, By Tier Level, 2026 – 2035

- 8.4.4. Asia Pacific Data Center Colocation Market Revenue, By Enterprise Size, 2026 – 2035

- 8.4.5. Asia Pacific Data Center Colocation Market Revenue, By End Use, 2026 – 2035

- 8.4.6. China Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Data Center Colocation Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Data Center Colocation Market Revenue, By Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Data Center Colocation Market Revenue, By Tier Level, 2026 – 2035

- 8.5.4. The Middle-East and Africa Data Center Colocation Market Revenue, By Enterprise Size, 2026 – 2035

- 8.5.5. The Middle-East and Africa Data Center Colocation Market Revenue, By End Use, 2026 – 2035

- 8.5.6. Saudi Arabia Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Data Center Colocation Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Data Center Colocation Market Revenue, By Type, 2026 – 2035

- 8.6.3. Latin America Data Center Colocation Market Revenue, By Tier Level, 2026 – 2035

- 8.6.4. Latin America Data Center Colocation Market Revenue, By Enterprise Size, 2026 – 2035

- 8.6.5. Latin America Data Center Colocation Market Revenue, By End Use, 2026 – 2035

- 8.6.6. Brazil Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Data Center Colocation Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Data Center Colocation Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Data Center Colocation Market: Company Market Share, 2025

- 9.2. Global Data Center Colocation Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Digital Realty Trust

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Zayo Group LLC

- 10.3. Colt Technology Services Group Limited

- 10.4. CoreSite

- 10.5. CyrusOne

- 10.6. Centersquare

- 10.7. China Telecom Corporation Limited

- 10.8. Equinix Inc.

- 10.9. Flexential

- 10.10. Iron Mountain Inc.

- 10.11. NTT Ltd. (NTT DATA)

- 10.12. QTS Realty Trust LLC

- 10.13. Rackspace Technology

- 10.14. Telehouse (KDDI CORPORATION)

- 10.15. Cologix

- 10.16. Others.

- 10.1. Digital Realty Trust

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 33

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Digital Realty Trust

- Zayo Group LLC

- Colt Technology Services Group Limited

- CoreSite

- CyrusOne

- Centersquare

- China Telecom Corporation Limited

- Equinix Inc.

- Flexential

- Iron Mountain Inc.

- NTT Ltd. (NTT DATA)

- QTS Realty Trust LLC

- Rackspace Technology

- Telehouse (KDDI CORPORATION)

- Cologix

- Others

FAQs

The key players in the market are Digital Realty Trust, Zayo Group LLC, Colt Technology Services Group Limited, CoreSite, CyrusOne, Centersquare, China Telecom Corporation Limited, Equinix Inc., Flexential, Iron Mountain Inc., NTT Ltd. (NTT DATA), QTS Realty Trust LLC, Rackspace Technology, Telehouse (KDDI CORPORATION), Cologix, Others.

Government mandates expected to influence the colocation data center industry include data sovereignty and localization laws that require data to be stored within the country, creating greater demand for local facilities, and data security rules that make colocation more attractive.

Data center colocation pricing is vital to market growth and service adoption. The more attractive and flexible the pricing models are (pay-as-you-grow plan, subscriptions, etc.), the more likely small and medium businesses will be inclined toward this service. The lower investments needed for a data center will be strongly appealing to businesses that prefer to adopt these services faster. The pricing structure must be transparent (power, space, and bandwidth) since this is the most important factor in a business’s IT budget. On the other hand, premium locations or very high-density infrastructures might be a limiting factor to adoption.

According to the present analysis and forecast modeling, the market of Data Center Colocation will witness a significant growth of about USD 327.3 billion in the year 2035 with the growing innovative product launch, increasing collaboration, and rising digital transformation across industries with a CAGR of 14.5% between the years 2026 and 2035.

It is projected that North America will hold the largest market share in the data center colocation market in the forecast period, with a share of about 34% of the global market share, which is attributed to the region’s presence of major players and the growing product launch.

The Asia Pacific is expected to grow at the highest CAGR during the forecast period. The growth in the region is owing to the growing number of data centers and increasing investment in advanced technology.

Data Center Colocation market is mainly influenced by the rapid adoption of cloud computing and hybrid IT infrastructure, which accelerates the demand for scalable infrastructure solutions. The significant cost benefits obtained by adopting a capex to opex model of service adoption are also known to be a key growth driver for the colocation industry. Other factors that are influencing the colocation industry’s growth are rising data flows generated by the growth in usage of digitized services and data-boomed AI and IoT; the need for latency-sensitive digital services driven by technologies like edge computing, and growing government regulation for data localization.