Battery Chemicals Market Size, Trends and Insights By Chemical Type (Cathode Battery Chemicals, Electrolyte Battery Chemicals, Anode Battery Chemicals), By Battery Type (Nickel Cadmium Batteries, Lithium Ion Batteries, Lead Acid Batteries, Zinc Carbon Batteries, Alkaline Batteries, Others), By End Use (Automotive Industry, Household Appliances, Consumer Electronics, Security & Monitoring Systems, Utilities & Backup Power), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 8.6%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Europe |

| Largest Market: | Asia-Pacific |

Major Players

- Albemarle Corporation

- Umicore SA

- BASF SE

- Sumitomo Metal Mining Co. Ltd.

- Others

Reports Description

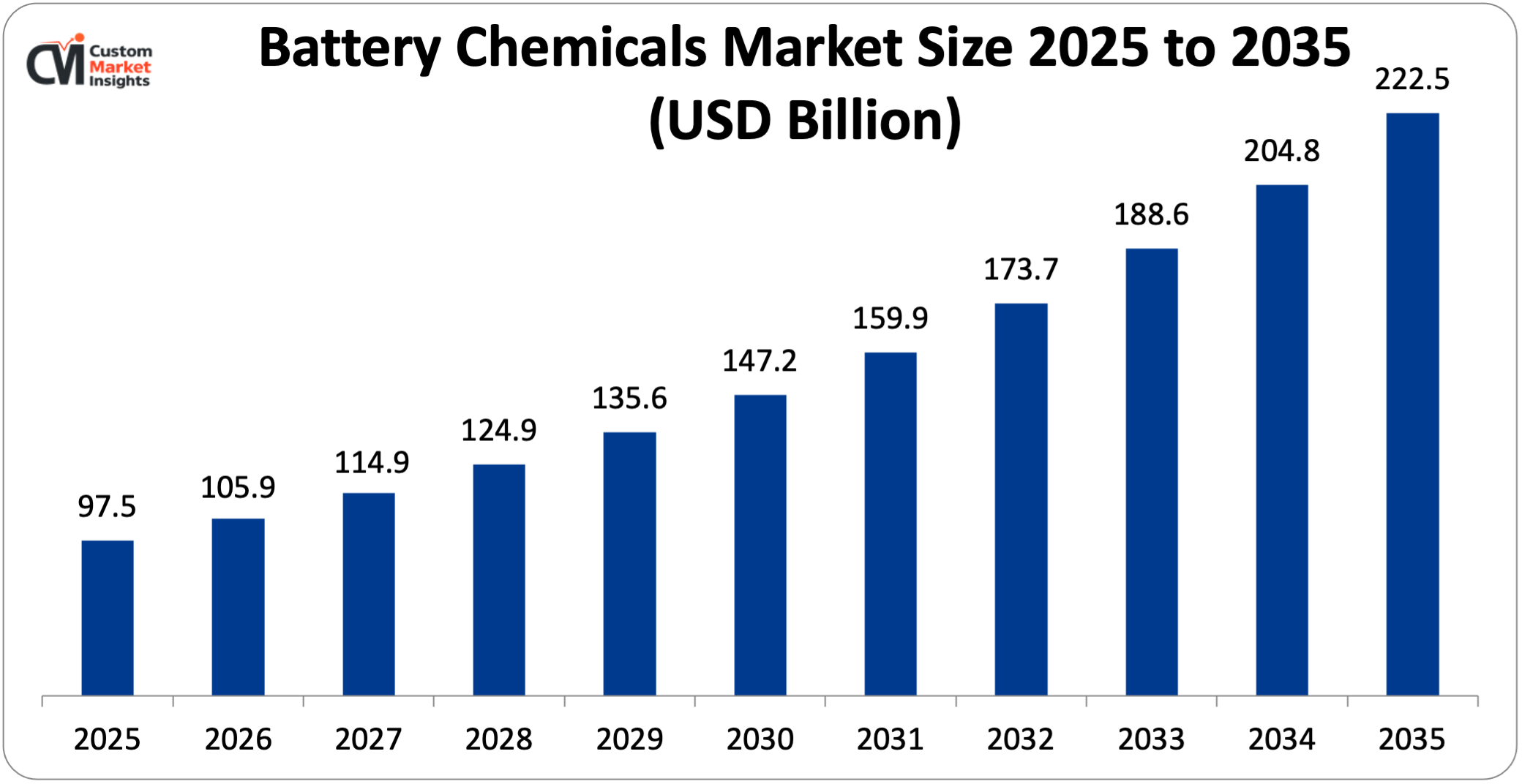

The market size of global battery chemicals will be estimated at USD 97.5 billion in 2025 and is expected to grow to between USD 105.9 billion in 2026 and about USD 222.5 billion by 2035, with a current CAGR (compound annual growth rate) of 8.6% during the period of 2026 to 2035. Battery chemicals are the raw chemicals/compounds used in battery manufacturing to facilitate energy storage, electrochemical reactions, etc.

They mainly comprise various lithium chemicals, such as Lithium carbonate, lithium hydroxide, etc.; nickel; cobalt; manganese; graphite; electrolyte; and battery additives forming cathodes & anodes, etc. They are also relevant to the capacity, state of charge, charge rate, safety & service life of batteries. Battery chemicals have a broad application in electric vehicles, electronics (eg. Cell phones, laptops), energy storage, etc.

Market Highlight

- In 2025, the Asia Pacific will dominate the global market with an estimated market share of 52%. The presence of major players and continuous product launches in the region drives the market growth.

- Europe is growing at the highest CAGR over the analysis period. The increasing emphasis on renewable energy.

- By chemical type, the cathode battery chemicals segment dominated the industry in 2025.

- By battery type, the lithium ion batteries segment captures the largest market share in 2025.

- By end user, the automotive industry segment held the largest market share in 2025.

Significant Growth Factors

The battery chemicals market trends present significant growth opportunities due to several factors:

- Rising Energy Storage Needs: The ever-growing demand for energy storage systems is one of the drivers of the battery chemicals market, which is substantially supported by government and other institutional data that shows an aggressive and rapid growth of energy storage systems. The International Energy Agency states that the global battery storage capacity is growing at an unprecedented rate; over 40 GW were added in 2023 alone, more than double 2022, making it the fastest-growing energy technology. The total installed battery storage capacity has also increased from 1 GW in 2012 to 85 GW, reinforcing the trend of growth in the energy storage sector. Other data put forward by agencies like the CEA has energy storage requirements in India proposed to grow from 82.37 GWh in 2026–27 to 411.4 GWh in 2031–32, and the world spends to see a net zero world by 2070 in the energy storage segment. According to the IEA, the world‘s battery storage capacity will have to increase sixfold by 2030 to achieve these climate goals and enable the expansion of clean energy on the scale needed, which surely will affect the acceleration of the demand for battery chemicals such as electrolytes and cathode and anode precursors, as these are necessary for battery cell manufacturing for an energy storage system.

- Government Policies & Incentives: Government schemes and incentives are having a positive influence in 2025 by promoting EVs and planning to support local battery manufacturing and develop infrastructure. For instance, in India there was the PLI Auto scheme for Advanced Chemistry Cells (ACC), which announced an investment of 18,100 crore (~USD 2.08 billion) for the construction of 50 GWh batteries. This demonstrates an opportunity for the lithium, nickel, and electrolyte market. This investment was supported by a recording of 35,657 crore and 13.6 lakh EVs by this PLI-Auto investment scheme in November 2025, until which there is a clear trend of scaled-up EV manufacturing and, consequently, battery demand. More generally, the government-initiated PLI schemes in India received 1.76 lakh crore (~USD 21 billion) in 2025 resulting in 1.2 million new jobs, showing the overall benefit to manufacturing and economic growth, including batteries and all other electrical automotive parts. Therefore, decreases in tax benefits, in the form of GST falling from 12 to 5 percent on EV production, together with other incentives offered by the government, are reducing the costs and thereby increasing the demand. Furthermore, infrastructure schemes will also play a fundamental role in supporting growth. Currently, there are plans to increase the number of public EV charging stations from 75,000 in 2024 to around 375,000 by 2030. Fifty billion (~USD 240 million) will be invested in the charging infrastructure, directly impacting demand and second-life battery use. All these issues regarding government incentives and schemes will promote the boom in EV and energy storage by increasing battery chemical demand across the entire value chain.

What are the Major Advances Changing the Battery Chemicals Market Today?

- Shift Toward LFP (Lithium Iron Phosphate) Chemistry: Achieving lithium iron phosphate (LFP) chemistry is one of the biggest innovations in the battery chemicals market today, due to its lower costs, safer chemistry, and reduced need for costly critical minerals like cobalt and nickel. This is reflected in global businesses pouring billions into this transition and demonstrates how LFP is dramatically reshaping demand for the leading battery chemicals, including lithium iron phosphate, electrolyte, and phosphate chemicals, for example: First, Tesla and LG Energy Solution, in partnership with other investors, have announced a $4.3 billion (2026) investment into an LFP battery manufacturing facility in the USA to supply batteries needed for energy storage systems and to build the country‘s battery supply chain. This shows LFP‘s growth inside EVs and energy storage systems at a large scale. Second, CATL and Stellantis have committed approximately $4.7 bn (2025) to the development of a large-scale LFP battery plant in Spain (approximately 50 GWh capacity), further balancing the increasing LFP production across the continent. Lastly, Ford has committed an investment of $3.5 billion for an LFP battery plant in Michigan to help reduce costs for EVs and bring down the barrier to entry for the mass-market vehicle. Overall, this proves how the chemical cluster will evolve greatly as the number of LFP chemistry investments continues to grow from Ford, Tesla, CATL and Stellantis while moving away from costly and rare materials and increasing demand for cost-efficient phosphate-based chemicals.

- Advanced Electrolytes & Additives: Innovations in advanced electrolytes and functional additives have been identified as the most significant technological breakthrough in the battery chemicals sector. These innovations have been identified to positively influence battery safety, efficiency, and mechanical life. Electrolytes have traditionally been used as a conducting medium for transporting battery ions between cathode and anode. Development of high-voltage electrolytes, solid- and gel-based versions, and flame-retardant electrolytes has greatly enhanced the degree of high energy density achievable in batteries while considerably reducing risks related to overheating, deterioration, and other hazards. Simultaneously, functional additives like film formers or binders, stabilizers, and conductance enhancers have been increasingly used for enhancing cycle life, fast-charging capabilities, and thermal stability in the next generation of solid-state and lithium-ion batteries. This trend is aided by increasing industry spending on advanced batteries and innovation. For instance, Liebherr-Transportation Systems (LTS), BASF SE and Solvay SA are working on advanced electrolyte compositions for high-performance electric vehicle (EV) batteries. Also, Tinci Materials Technology, along with American companies like Chemetall and Toray, is expanding its large-scale production of electrolyte solutions and additives to meet the growing market demand. The rising emphasis on fast-charging EVs, efficient high-energy batteries, and safer replacements has led to a phenomenal rise in the demand for advanced electrolytes, making this one of the most promising segments in the battery chemicals industry.

Category Wise Insights

By Chemical Type

Why Cathode Battery Chemicals Hold a Prominent Position in the Market?

The cathode battery chemicals segment dominated the industry in 2025. This market is primarily driven by the rapid growth of electric vehicles (EVs), renewable energy storage, etc. Cathode materials account for a considerable percentage of overall battery cost and constitute a significant value-generating segment in the batteries. With the high-performance chemistry trends flowing in, high-nickel cathodes and low-cost LFP chemistry are leading to the growth of lithium, nickel, cobalt, and iron phosphate chemistry demand. Also, the continuous technology developments in cathodes for the improvement of power density, safety, and cycle life of the batteries are positively influencing the market size. Rising investments in gigafactories, localization of supply chains, and government subsidies in favor of local cell manufacturing are resulting in more cathode chemical consumption.

The electrolyte battery chemicals segment is growing at the highest CAGR over the analysis period. The demand for high-performance lithium-ion batteries (LIBs) for use in electric vehicles (EVs), consumer electronics, and energy storage will continue to rise. It is well established that the electrolyte, which conducts ions within the cell, is an essential element of every cell, and from the determination of efficiency and safety through to cycle life, the electrolyte defines the performance of the battery. The inexorable drive toward higher-value batteries, including specialist models with fast-charging and high-energy-density properties, will characterize increased demand for higher-purity lithium salts such as LiPF and advanced solvents and functional additives. The increase in manufacturing capacity, as well as the advent of many gigafactories worldwide, will act as a catalyst for rising electrolyte raw material consumption. However, further developments in electrolytes and the introduction of solid-state and gel variants for safety and performance reasons will further drive the electrolyte market, giving it the best growth in the battery chemicals market.

By Battery Type

Why Lithium Ion Batteries Capture the Highest Market Share the Battery Chemicals Market?

The lithium ion batteries segment captures the largest market share in 2025. This growth is primarily driven by their broad adoption range, best-in-class price-to-performance ratio, and increasing use of Electric Vehicles (EVs), Energy Storage Systems (ESS), and Consumer Electronics. The Li-ion battery is the largest competitor in the market owing to its high energy densities, long life cycles, and light weight. Product enhancements of the Li-ion batteries, attributed to ongoing improvements in cell configurations/chemistries (NMC, LFP) and electrolyte technologies to provide increased efficiencies, continue to accelerate the growth in the use of battery chemicals. Accelerating the uptake of large Lithium-ion batteries for renewable energy storage to stabilize the grid is also a positive driver for the battery chemicals market. The primary growth factor for the Lithium-ion segment is the continuous iterative improvements on cell chemistry and design, which have increased the energy density and durability of modern cell chemistries (chemistry improvements in LFP, LMO, and NMC cells).

The lead-acid batteries segment is growing at a steady rate over the projected period. The requirement for lead (acid) battery chemicals is primarily when lead (acid) batteries are used in car starter batteries (SLI), uninterruptible power supplies (UPS), and, to a lesser extent, for backup power storage. Although lithium-ion and other advanced battery chemistries are emerging, lead-acid batteries are still relevant because they are inexpensive and highly reliable, and the recycling systems are mature with recycling efficiencies of above 95% in a number of markets. Growing energy and power requirements for backup power for IT data centers, telecom infrastructure, and industrial installations in the developing economies and the ever-increasing automotive fleet (e.g. Internal combustion engine (ICE) and hybrid) are ensuring a consistent stream of demand for lead, sulfuric acid, and other battery chemicals. Improving battery technology (more advanced flooded batteries (EFB) and AGM) is enhancing battery life and performance and subjecting earnings to further growth.

By End User

Why Automotive Industry Capture the Highest Market Share the Battery Chemicals Market?

The automotive industry segment held the largest market share in 2025. Market growth is mainly driven by the rapid shift to electric mobility and the increase of electrification in vehicles. The increase in the production and markets for Electric Vehicles (EVs) is fueling demand for key battery chemicals such as lithium, nickel, cobalt, electrolytes, and advanced cathode materials for batteries, despite government incentives, emissions regulations, and environmental awareness. Market growth is also driven by more hybrid usage and advanced electronics, which are increasing battery demand further; automakers are investing heavily in battery manufacture and continue to vertically integrate the supply chain in order to meet the demand increase and result in higher demand for base and specialty chemicals. Overall, the development of high-performance batteries with longer range, faster charging times, and improved safety performance is enhancing battery demand further.

The consumer electronics segment is growing at a rapid rate over the projected period. The increasing demand for consumer electronics such as smartphones, laptops, PCs and others drives the industry growth.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 105.9 billion |

| Projected Market Size in 2035 | USD 222.5 billion |

| Market Size in 2025 | USD 97.5 billion |

| CAGR Growth Rate | 8.6% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Chemical Type, Battery Type, End Use and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Battery Chemicals Market Size?

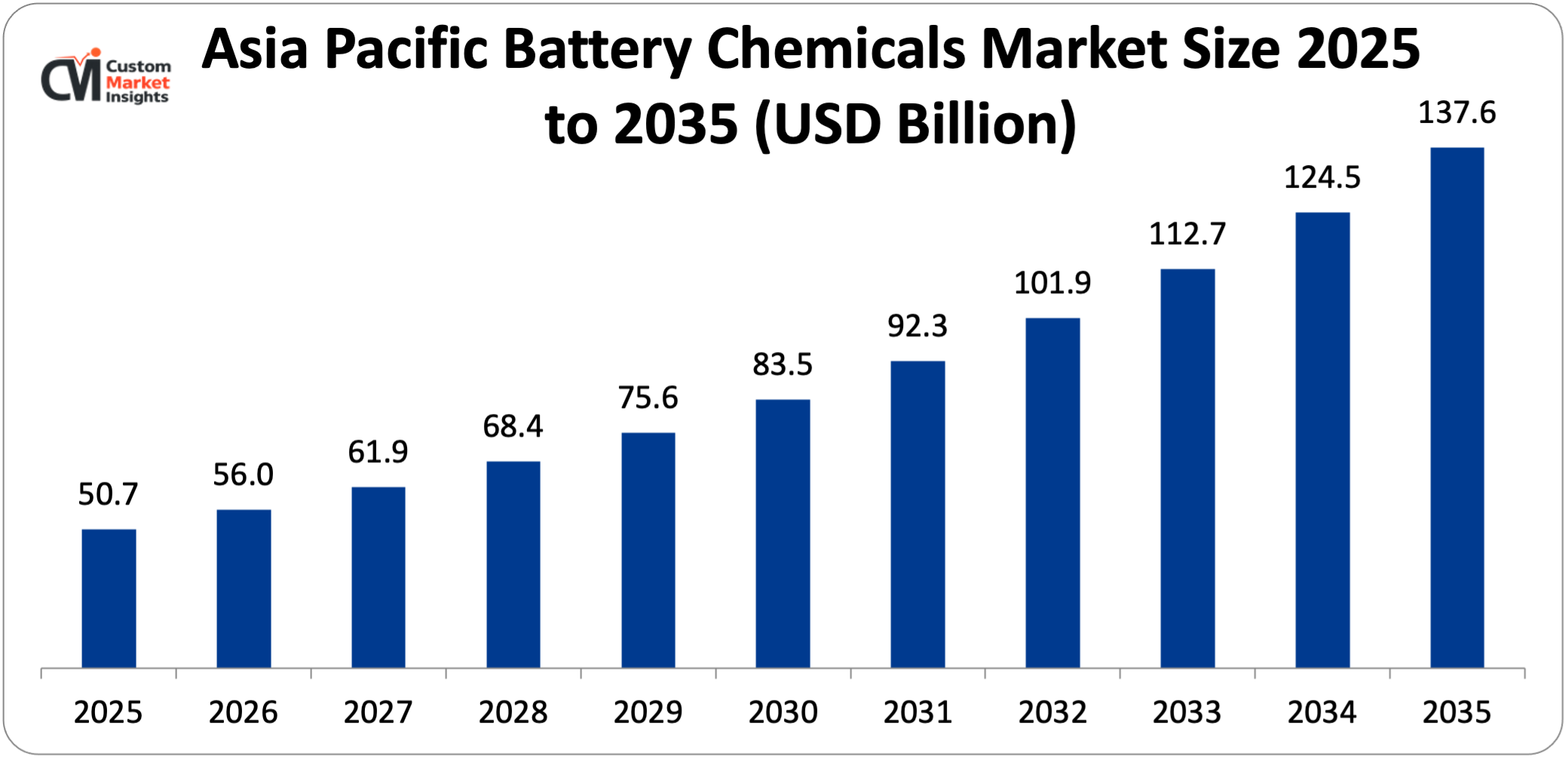

Its market size, in terms of the Asia Pacific battery chemicals, is projected to be USD 50.7 billion in 2025 with a growth to about USD 137.6 billion in 2035 with a CAGR of 10.5% between 2026 and 2035.

Why did the Asia Pacific Dominate the Battery Chemicals Market in 2025?

In 2025, the Asia Pacific will dominate the global market with an estimated market share of 52%. The region’s deep hold on battery manufacturing and raw material processing will largely underpin its growth. Lithium-ion battery production is focused in a handful of countries, in particular China, Japan, South Korea, and India, where large gigafactories and supply chains exist for the supply of finished batteries. Rapid take-up of electric vehicles (EVs), which are already led by China (the world‘s largest EV market), and large-scale government policies, subsidies, and investment in domestic battery manufacturing are boosting demand for battery chemicals, especially lithium, nickel, cobalt, and electrolytes.

China Battery Chemicals Market Trends

In the Asia Pacific region, China leads the industry expansion over the projected period. Widespread utilization of renewable generation and energy storage systems in the region is also leading to increased demand for sophisticated battery materials. Additionally, a strong base of top chemical and battery-producing companies, along with ongoing innovations and affordable production methods, is expected to generate revenue, particularly as these advancements enable the production of more efficient and sustainable battery technologies that meet the growing market needs.

Why is Europe Experiencing Significant Growth in the Battery Chemicals Market?

Europe holds a significant market share in 2025. Market growth is driven by both ambitious decarbonization targets and the rapidly growing adoption of electric vehicles (EVs). The EU‘s rigorous emission standards and policy to achieve climate neutrality are urging OEMs to start manufacturing electric vehicles at a higher pace, driving higher demand for battery chemicals such as lithium, nickel, cobalt, and advanced cathode compounds.

UK Battery Chemicals Market Trends

The UK held the dominant position in the market in 2025. Government-funded projects and grants are supporting the research and development of next-generation battery technologies (including solid-state batteries and sustainable materials).

Why is North America Growing at a Steady Rate in the Battery Chemicals Market?

North America is expected to grow at a steady rate over the projected period. The growth is owing to the increasing emphasis on renewable energy and increasing government support for sustainability.

US Battery Chemicals Market Trends

The US is in a dominant position in the battery chemical market. The US is aiming to become less reliant on imports by investing more in domestic mining, refining, and gigafactory build-out, which results in more purchases of battery chemicals. The speed at which the development of renewable energy projects and grid-scale energy storage systems is increasing is also leading to higher demand for high-end battery materials. Furthermore, collaborations between car manufacturers and chemical producers, as well as developments in battery chemicals, will likely grow the market. The US is thus surfacing as a dominant region for revenue growth.

Why is the Middle East & Africa Region is growing rapidly in the Battery Chemicals?

The MEA region is growing at a steady rate over the projected period. This region has been drawing increasing attention for its minerals, such as cobalt and other critical materials, which are vital for the manufacture of batteries, and for the sizable investment it is witnessing in mineral excavation and processing from a host of countries. Efforts to diversify the economy from its oil reliance and to encourage the use of clean energy are further factors that are buoying up the market, as they create new opportunities for investment in renewable energy technologies and sustainable practices that align with global environmental goals.

UAE Battery Chemicals Market Trends

The UAE is growing at the highest CAGR during the forecast period. The increasing investment in renewable energy is expected to drive industry growth.

Top Players in the Battery Chemicals Market and Their Offerings

- Albemarle Corporation

- Umicore SA

- BASF SE

- Sumitomo Metal Mining Co. Ltd.

- Mitsubishi Chemical Group

- Johnson Matthey Plc

- Solvay SA

- Asahi Kasei Corporation

- Eastman Chemical Company

- 3M Company

- SSRL Battery Chemicals Pvt. Ltd.

- GFCL EV Products Limited

- Hitachi High-Tech Corporation

- LOTTE Chemical Corporation

- Himadri Speciality Chemical Ltd

- Mitra Chem

- Tata Chemicals

- Others

Key Developments

Battery chemicals market has experienced considerable changes in the last two years as the market players are trying to diversify their technological aspects and develop product portfolios using strategic approaches.

- In August 2025, BASF Battery Materials, through its joint venture BASF Shanshan Battery Materials Co., Ltd. (BSBM), has achieved a major milestone in next-generation battery technology. In collaboration with Beijing WELION New Energy Technology Co., Ltd., BASF has successfully delivered its first batches of mass-produced Cathode Active Materials (CAM) for Semi-Solid-State batteries – marking a significant step towards industrializing Solid-State batteries. (https://www.basf.com/global/en/media/news-releases/2025/08/p-25-168)

- In November 2025, diversified global manufacturer Asahi Kasei and German battery manufacturer EAS Batteries signed a license agreement for the use of Asahi Kasei’s acetonitrile-containing electrolyte technology. The electrolyte will be used in EAS’ novel ultra-high-power lithium-ion battery cell using a lithium iron phosphate (LFP) cathode. The electrolyte’s high ionic conductivity contributes to reduced internal cell resistance and enhanced rate capability, even under demanding temperature conditions. The market launch of EAS Batteries’ new cell utilizing this technology is in line with Asahi Kasei’s commercialization plans, with the product scheduled to be released no later than March 2026. (https://www.asahi-kasei.com/news/2025/e251104.html)

These strategic measures have enabled the companies to reinforce their competitive positions, increase the product line, boost their technological competencies, and also seize growth opportunities in the fast-growing battery chemicals market.

The Battery Chemicals Market is segmented as follows:

By Chemical Type

- Cathode Battery Chemicals

- Electrolyte Battery Chemicals

- Anode Battery Chemicals

By Battery Type

- Nickel Cadmium Batteries

- Lithium Ion Batteries

- Lead Acid Batteries

- Zinc Carbon Batteries

- Alkaline Batteries

- Others

By End Use

- Automotive Industry

- Household Appliances

- Consumer Electronics

- Security & Monitoring Systems

- Utilities & Backup Power

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Battery Chemicals by Segments

- 2.1.2. Battery Chemicals by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Battery Chemicals Market Attractiveness Analysis, By Chemical Type

- 2.2.3. Battery Chemicals Market Attractiveness Analysis, By Battery Type

- 2.2.4. Battery Chemicals Market Attractiveness Analysis, By End Use

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Rising Energy Storage Needs

- 3.1.2. Government Policies & Incentives

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Battery Chemicals Market – By Chemical Type

- 4.1. Chemical Type Market Overview, By Chemical Type Segment

- 4.1.1. Battery Chemicals Market Revenue Share, By Chemical Type, 2025 & 2035

- 4.1.2. Cathode Battery Chemicals

- 4.1.3. Battery Chemicals Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Electrolyte Battery Chemicals

- 4.1.7. Battery Chemicals Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Anode Battery Chemicals

- 4.1.11. Battery Chemicals Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Chemical Type Market Overview, By Chemical Type Segment

- Chapter 5. Battery Chemicals Market – By Battery Type

- 5.1. Battery Type Market Overview, By Battery Type Segment

- 5.1.1. Battery Chemicals Market Revenue Share, By Battery Type, 2025 & 2035

- 5.1.2. Nickel Cadmium Batteries

- 5.1.3. Battery Chemicals Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Lithium Ion Batteries

- 5.1.7. Battery Chemicals Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Lead Acid Batteries

- 5.1.11. Battery Chemicals Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Zinc Carbon Batteries

- 5.1.15. Battery Chemicals Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Alkaline Batteries

- 5.1.19. Battery Chemicals Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Others

- 5.1.23. Battery Chemicals Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Battery Type Market Overview, By Battery Type Segment

- Chapter 6. Battery Chemicals Market – By End Use

- 6.1. End Use Market Overview, By End Use Segment

- 6.1.1. Battery Chemicals Market Revenue Share, By End Use, 2025 & 2035

- 6.1.2. Automotive Industry

- 6.1.3. Battery Chemicals Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Household Appliances

- 6.1.7. Battery Chemicals Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Consumer Electronics

- 6.1.11. Battery Chemicals Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Security & Monitoring Systems

- 6.1.15. Battery Chemicals Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Utilities & Backup Power

- 6.1.19. Battery Chemicals Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End Use Market Overview, By End Use Segment

- Chapter 7. Battery Chemicals Market – Regional Analysis

- 7.1. Battery Chemicals Market Overview, By Region Segment

- 7.1.1. Global Battery Chemicals Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Battery Chemicals Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Battery Chemicals Market Revenue, By Chemical Type, 2026 – 2035

- 7.1.4. Global Battery Chemicals Market Revenue, By Battery Type, 2026 – 2035

- 7.1.5. Global Battery Chemicals Market Revenue, By End Use, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Battery Chemicals Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Battery Chemicals Market Revenue, By Chemical Type, 2026 – 2035

- 7.2.3. North America Battery Chemicals Market Revenue, By Battery Type, 2026 – 2035

- 7.2.4. North America Battery Chemicals Market Revenue, By End Use, 2026 – 2035

- 7.2.5. U.S. Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Battery Chemicals Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Battery Chemicals Market Revenue, By Chemical Type, 2026 – 2035

- 7.3.3. Europe Battery Chemicals Market Revenue, By Battery Type, 2026 – 2035

- 7.3.4. Europe Battery Chemicals Market Revenue, By End Use, 2026 – 2035

- 7.3.5. Germany Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Battery Chemicals Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Battery Chemicals Market Revenue, By Chemical Type, 2026 – 2035

- 7.4.3. Asia Pacific Battery Chemicals Market Revenue, By Battery Type, 2026 – 2035

- 7.4.4. Asia Pacific Battery Chemicals Market Revenue, By End Use, 2026 – 2035

- 7.4.5. China Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Battery Chemicals Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Battery Chemicals Market Revenue, By Chemical Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Battery Chemicals Market Revenue, By Battery Type, 2026 – 2035

- 7.5.4. The Middle-East and Africa Battery Chemicals Market Revenue, By End Use, 2026 – 2035

- 7.5.5. Saudi Arabia Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Battery Chemicals Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Battery Chemicals Market Revenue, By Chemical Type, 2026 – 2035

- 7.6.3. Latin America Battery Chemicals Market Revenue, By Battery Type, 2026 – 2035

- 7.6.4. Latin America Battery Chemicals Market Revenue, By End Use, 2026 – 2035

- 7.6.5. Brazil Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Battery Chemicals Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Battery Chemicals Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Battery Chemicals Market: Company Market Share, 2025

- 8.2. Global Battery Chemicals Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. Albemarle Corporation

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Umicore SA

- 9.3. BASF SE

- 9.4. Sumitomo Metal Mining Co. Ltd.

- 9.5. Mitsubishi Chemical Group

- 9.6. Johnson Matthey Plc

- 9.7. Solvay SA

- 9.8. Asahi Kasei Corporation

- 9.9. Eastman Chemical Company

- 9.10. 3M Company

- 9.11. SSRL Battery Chemicals Pvt. Ltd.

- 9.12. GFCL EV Products Limited

- 9.13. Hitachi High-Tech Corporation

- 9.14. LOTTE Chemical Corporation

- 9.15. Himadri Speciality Chemical Ltd

- 9.16. Mitra Chem

- 9.17. Tata Chemicals

- 9.18. Others.

- 9.1. Albemarle Corporation

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Healthcare Foresights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

- Chapter 12. List Of Figures

- 12.1. Figures No 1 to 30

- Chapter 13. List Of Tables

- 13.1. Tables No 1 to 46

Prominent Player

- Albemarle Corporation

- Umicore SA

- BASF SE

- Sumitomo Metal Mining Co. Ltd.

- Mitsubishi Chemical Group

- Johnson Matthey Plc

- Solvay SA

- Asahi Kasei Corporation

- Eastman Chemical Company

- 3M Company

- SSRL Battery Chemicals Pvt. Ltd.

- GFCL EV Products Limited

- Hitachi High-Tech Corporation

- LOTTE Chemical Corporation

- Himadri Speciality Chemical Ltd

- Mitra Chem

- Tata Chemicals

- Others

FAQs

The key players in the market are Albemarle Corporation, Umicore SA, BASF SE, Sumitomo Metal Mining Co. Ltd., Mitsubishi Chemical Group, Johnson Matthey Plc, Solvay SA, Asahi Kasei Corporation, Eastman Chemical Company, 3M Company, SSRL Battery Chemicals Pvt. Ltd., GFCL EV Products Limited, Hitachi High-Tech Corporation, LOTTE Chemical Corporation, Himadri Speciality Chemical Ltd., Mitra Chem, Tata Chemicals, Others.

Government policy will be critical in demand generation, safety, and setting industry standards to ensure the supply of battery chemicals. As demand for batteries and battery chemicals increases, this will be directly proportional to the growth of electric vehicles and renewable energy generation, and legislation to lower carbon emissions and safety and performance standards set by regulators will be a key driver in new innovation and product development in the industry while also helping to guarantee the supply of key battery materials such as lithium and cobalt.

Price is an important factor in battery chemical market growth, as an increase in the price of important battery chemicals, lithium, cobalt, and nickel, would increase the overall price of the battery and could hinder battery adoption (especially for mass-market electric vehicles and energy storage in markets where cost is king), whereas a decrease in the price of battery chemicals (through better technology, economies of scale, and the mass adoption of cheaper chemistries such as LFP) would allow for a quicker adoption and broader growth.

According to the present analysis and forecast modeling, the market of battery chemicals will witness a significant growth of about USD 222.5 billion in the year 2035 with the growing innovative product launch, increasing collaboration, and rising demand for EVs with a CAGR of 8.6% between the years 2026 and 2035.

It is projected that the Asia Pacific will hold the largest market share in the battery chemicals market in the forecast period, with a share of about 52% of the global market share, which is attributed to the region’s presence of major players and high production of EVs.

Europe is expected to grow at a significant rate during the forecast period. The growth in the region is owing to the growing decarbonization aim.

The main factors boosting growth in the battery chemicals market are the exponential growth of electric cars, higher demand for energy storage systems to accommodate renewable energy, and the proliferation of consumer electronic products. Moreover, government incentives and growing investment in battery development technology and the manufacturing supply chain within the country are helping boost the battery chemicals market further.