Intravenous Infusion Pump Market Size, Trends and Insights By Product Type (Volumetric Infusion Pumps, Large Volume Pumps, Small Volume Pumps, Syringe Infusion Pumps, Ambulatory Infusion Pumps, Disposable Pumps, Chemotherapy Infusion Pumps, Patient-Controlled Analgesia (PCA) Pumps, Implantable Infusion Pumps, Insulin Infusion Pumps, Infusion Pump Accessories and Consumables), By Disease Indication (Chemotherapy, Diabetes, Gastroenterology, Analgesia/Pain Management, Pediatrics/Neonatology, Hematology, Other Applications), By End-User (Hospitals, Home Care Settings, Ambulatory Care Centers, Other End-Users), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 7.6%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- Braun Melsungen AG

- Fresenius Kabi AG

- ICU Medical Inc.

- Medtronic plc

- Others

Reports Description

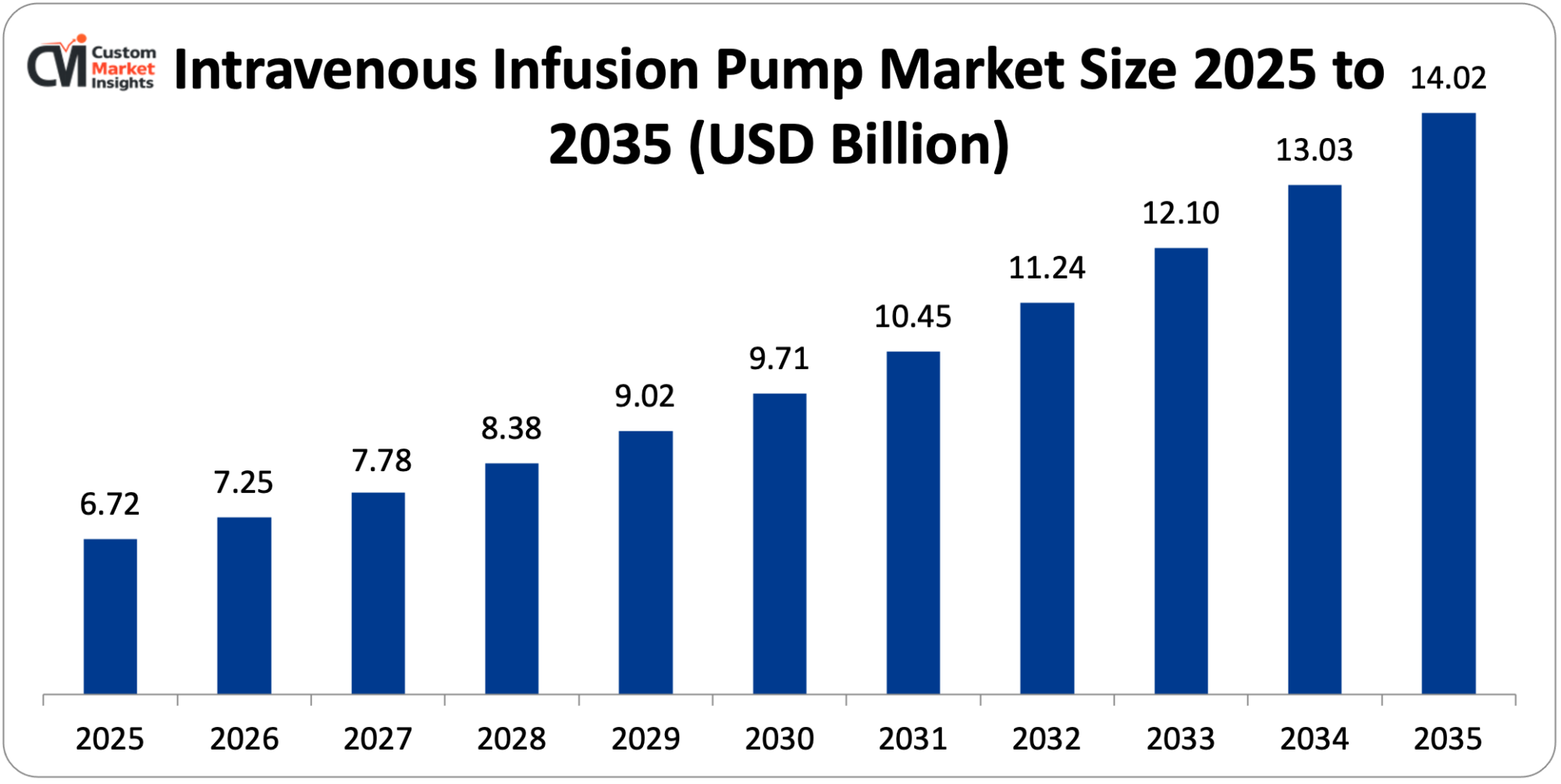

The market size of the global intravenous infusion pump is estimated at USD 6.72 billion in the year 2025 and is estimated to rise by USD 7.25 billion in 2026 to an estimate of USD 14.02 billion in 2035 at a CAGR of 7.6% between the years 2026 and 2035.

The market is being developed by the rising incidence of chronic diseases, the rising geriatric demographic, the rising demand for home health care services, and the development of smart pump technologies with improved safety measures.

Market Highlight

- North America controlled the market with a 51% market share of the intravenous infusion pump in 2025.

- Asia Pacific will also experience the highest CAGR of 9.3% from 2026 to 2035.

- By product type, the volumetric type infusion pump market segment had an approximate 17% market share in 2025.

- By product type, the ambulatory infusion pumps segment is with a robust CAGR of 8.9% between the years 2026 and 2035.

- By indication of the disease, it is chemotherapy segment with the highest market share of 29% in 2025, and, pediatrics/neonatology segment with the fastest rate of 9.7% CAGR during the estimated period between 2026 and 2035.

- By end-user, the segment of hospitals assumed 73% of market share in 2025.

Significant Growth Factors

The Intravenous Infusion Pump Market Trends present significant growth opportunities due to several factors:

- Rising Prevalence of Chronic Diseases and Medication Delivery Needs: The growing rate of chronic diseases worldwide is the key market force of the intravenous infusion pump where diseases that need constant and accurate medication provision establish a long-term need for sophisticated and refined infusion machines. As data published by the International Diabetes Federation indicate in 2025, 589 million adults (20-79 years) live with diabetes throughout the world, which is 11.1% of the adult population, and the numbers are expected to increase to 853 million in 2050. Equally, the prevalence and mortality rates of cardiovascular diseases will rise by 90 and 73.4% respectively by 2025 and 2050. The increasing number of chronic illnesses promotes the use of superior infusion pumps by healthcare providers that are safe, precise, and convenient to patients. Research published in 2024 estimated that in the United States, the American Cancer Society estimated more than 2 million new cases of cancer and 611,720 cancer-related deaths, and treatment with any chemotherapy would involve the use of infusion pumps to deliver precise intravenous drugs. There are about 4,000 avoidable injuries as a result of mistakes in the administration of medication each year and 3-7% of the doses given by nurses contain an error. The requirement of precise medication delivery among the various patients such as cancer patients, diabetics, cardiovascular patients and critically ill patients generates a high demand on complex infusion pump systems. Newer infusion pump systems include coinage features such as a dose error reduction system (DERS), having a drug library that has standard dosing limits, a wireless interface allowing interaction with electronic health records, and real-time monitoring capability that improves patient safety and decreases medication errors. The increasing number of patients requiring continuous therapy through medication, as well as more sophisticated therapeutic practices, is a long-term growth potential of infusion pump manufacturers and healthcare institutions with a comprehensive medication safety program.

- Technological Advancements and Smart Pump Integration with Healthcare IT: Market growth has increased very fast because of the evolution of technologies and the addition of artificial intelligence, internet of things sensors, and interoperability capabilities to infusion pump systems. Smart infusion pumps with two-way EHR integration to provide seamless data flow where infusion orders are sent to pumps and infusion data sent back to records, wireless connectivity and remote monitoring and remote programming, and cloud-based data management platforms that provide detailed analytics on usage are all examples of innovations. Smart infusion pumps will be utilized in more than 41% of the U.S. hospitals by 2025, with an increasing number of hospitals adopting this technology because they have found it to be an effective tool in patient safety. Contemporary smart pumps are characterized by pre-set clinical guidelines, extensive drug libraries that contain drug information, dose, volume, and flow rate, audiovisual alerts about problems such as air bubbles and occlusions, and preset dose limits that avoid dose errors. As an example, in June 2025, MEDITECH launched the two-way communication between its Expanse EHR and smart infusion pumps to facilitate the seamless exchange of data and automated records. In May 2025, Penlon introduced the HP TCi Syringe Pump, an intravenous production anesthesia device for critical care, with a touchscreen interface, AI-aided dose calculation, and real-time monitoring. Studies reveal that smart infusion pump interoperability can lower the errors committed during medication administration by 15.4-54.8%, and a health system has saved USD 531,891 in a year by avoiding 56 preventable adverse drug events caused by interoperability execution. In addition to this, medical technology in the field of batteries, miniaturized parts, ergonomics, and improved safety features has facilitated application in various care environments encompassing hospitals, ambulatory centers, and home-based healthcare facilities. The ongoing product development by major manufacturers such as BD, Baxter, B. Braun, and Fresenius Kabi keeps increasing product portfolios and enhancing the results of patients having a high demand of specific medication input.

What are the Major Advances Changing the Intravenous Infusion Pump Market Today

- AI-Powered Smart Pumps with EHR Integration: The most powerful technological development, which allows automated programming, removes errors in data entry by humans, and provides intelligent control over the parameters of infusion. Smart EHR-connected infusion pumps receive physician order entry systems via smart medication orders, automatically fill pump settings like drug choice, dosing rate, and other infusion rates, and transmit infusion data to patient records so that all infusion data can be fully documented. Research shows that interoperability can help decrease medication administration errors that are subject to technological influence by 15.4 to 54.8%, and that all medication administration errors are lowered after being implemented. AI-based systems process patient information in real time and suggest the most effective dosages and possible drug interactions as well as anticipate adverse events. These new technologies will solve the long-standing issue of errors in medication usage, which influence 2.15% of the inpatient hospitalizations and claim the lives of more than 18,000 every year due to adverse drug events that began during hospitalization.

- Wireless Connectivity and Remote Monitoring Capabilities: Wireless-enabled infusion pumps have led to the transformation of medication delivery through their ability to monitor remotely, manage centralized fleets and provide real-time performance data. Smart pumps are wireless and use the information about the usage, alert and performance to send it to central monitoring stations and enable clinical teams to monitor and control a large number of patients at once and to quickly respond to the alert of the pump or its malfunctions. Hospitals that use wireless pump networks claim to have better equipment utilization, less time to respond to patient needs, and the ability to monitor drug library compliance rates. The wireless connectivity as well makes updating of drug libraries in the air possible where all pumps in a healthcare system are kept up to date with all the dosing parameters without any human intervention. Wireless features facilitate new telemedicine functionality, allowing specialist consultation in complicated infusion control and logged over processes in home health care environments.

- Dose Error Reduction Systems and Advanced Safety Features: Sophisticated dose error reduction software is an important safety innovation and multi-layered safety checks that avoid programming errors and detect possible adverse events are incorporated in modern systems. The DERS technology applies versatile drug libraries which comprise institution-specific dosing records, hard and soft dose thresholds that raise compulsory notifications or advisory messages and context-driven programming that adjusts safety parameters according to patient weight, age, and clinical environment. It has been shown that even with the use of smart pumps, 60% of medication dispenses have one or more discrepancies, the most frequent ones being incorrect infusion rates and workarounds such as bypassing safety measures. Enhanced DERS implementations resolve all these issues by providing better user interfaces, simplified programming procedures and automated alertness mechanisms to reduce alarm fatigue without compromising on safety vigilance.

- Ambulatory and Portable Infusion Systems: The introduction of small battery-powered ambulatory infusion pumps facilitates the provision of medication beyond the conventional hospital care, which is the global transition to home-based care and the ambulatory model of care. The latest ambulatory pumps are designed to be very lightweight (less than one pound), have longer battery duration allowing them to be used over a period of many days, have low profiles that allow implantation beneath clothes and have easy-to-use interfaces that can be used by patients and caregivers. They are especially useful in the administration of chemotherapy, antibiotic therapy, pain management, and total parenteral nutrition so that a patient can continue with such portable systems under constant medication. In February 2025, the FDA authorized ONAPGO, an apomorphine infusion device that is placed subcutaneously to control motor fluctuation in advanced PD, which is an example of innovation in ambulatory infusion technology. The ambulatory infusion pumps market segment is recording strong growth of an expected CAGR of 8.9% between 2026 and 2035 due to the patient preference of home based care and the pressure of healthcare cost containment.

Category Wise Insights

By Product Type

Why Volumetric Infusion Pumps Lead the Market?

Volumetric infusion pumps in the year 2025 are a strong segment with about 17% of the entire market share. This high representation explains why volumetric pumps are vital to the need to provide large amounts of fluids, medications and nutrients with a specific flow rate control in various clinical settings. Volumetric infusion pumps are the workhorses of hospital based administration of medication delivery, which find wide use in the administration of IV fluids, antibiotics, chemotherapy, parenteral nutrition and other therapeutic solutions that may need precise volume regulation over a long period of infusion. The fluid delivery of such pumps is also delivered by volume and not by drops which makes them much more accurate and consistent than the conventional gravity-fed systems.

The wide range of applications of volumetric infusion pumps allows their implementation in all departments of hospitals, almost everywhere, such as intensive care units, medicine floors, emergency departments, cancer units, or operating rooms. Current volumetric pumps have many channels of infusion allowing the delivery of various medications using the same device, controllable dosing values that can fit a wide range of treatment regimens and connectivity with the hospital information system allowing automated documentation and control. Volumetric pumps become essential capabilities in dealing with complex patients who need several simultaneous treatments at any given time, due to the capacity to administer primary as well as secondary medication doses.

The other sizeable product segment is syringe infusion pumps that are mostly appreciated in needy situations where small doses of very strong output of medications need to be delivered with high levels of accuracy. Syringe pumps are particularly useful in neonatal intensive care, where small volume infusions are necessary with minute fine margins available to infants, critical care units giving the patient infusion of vasoactive drugs requiring a high degree of exactness and where the administration of sedatives and analgesics in anesthesia requires that extreme care be taken in its application. It is expected that the syringe infusion pumps market will reach USD 2.0 billion by 2032 due to the consistent demand for the precision delivery of medication in a variety of specialized clinical uses.

The most rapidly growing with the projected CAGR of 8.9% during 2026 to 2035 are the ambulatory infusion pumps that are fuelled by the growing home healthcare market and the desire of patients to be treated outside the institutions. Continuous medication administration is made possible by ambulatory pumps when patients are allowed to live regular lives, which are used in treatments such as home-based chemotherapy, chronic infections with long-term antibiotics, long-term pain treatments, and feeding patients with feeding tubes in case of gastrointestinal diseases. The COVID-19 pandemic increased the use of home infusion services, and healthcare systems and payers realized the benefits in cost savings and patient contentment of ambulatory infusion programs. The modern ambulatory pumps have user friendly interfaces, which patients can easily operate, wireless connectivity, which allows the healthcare provider to monitor the patient remotely, a compact design, which allows the pump to be hidden and easily carried around, and a long battery life, which allows the pump to work on a multiday basis before it is charged again.

By Disease Indication

Why Chemotherapy Dominates Infusion Pump Applications?

The highest disease indication market comes through chemotherapy applications, which are expected to take 29% of the total market share in 2025. Such a managerial role indicates the importance of infusion pumps in cancer therapy where high accuracy of cytotoxic drug delivery is necessary to achieve the highest degree of treatment efficiency and the lowest level of toxicity. The chemotherapy drugs usually possess a small range of therapeutic optimization that demands precise dosages and speedy infusion of the drugs to maximize the destruction of the tumor cells and minimize harm to normal tissues. Infusion pumps make possible constant infusion regimens that allow constant drug levels to be sustained, enhancing the efficacy of treatment of some types of cancer over the bolus route.

The growing cancer burden in the world continually creates the need to use chemotherapy infusion equipment. The American Cancer Society states that there were more than 2 million cases of new cancer cases in 2024, and most of the patients will need numerous sessions of intravenous chemotherapy that will be performed over months of treatment in the United States alone. An example of this continued innovation in chemotherapy regimens, now based on infusion accuracy, was a randomized clinical trial in November 2024 which found that high-dose intravenous vitamin C addition to chemotherapy doubled overall survival of late-stage metastatic pancreatic cancer patients from eight months to 16 months. The chemotherapy part is showing a strong growth with a projected CAGR of 9.7% in terms of growing cancer rates and growing the application of infusion based cancer treatment.

Chemotherapy infusion is done in a wide array of settings such as oncology units of hospitals, ambulatory infusion centers that have been designed specifically to treat cancer and at an increasing number of places such as home health care settings that use portable ambulatory pumps. The intricacy of chemotherapy regimens incorporating numerous agents given in sequence or in combination, pretake medications to cause adverse reactions, and supportive care medications demands complex infusion pump systems that can allow complex guidelines. Smart infusion pumps that have extensive chemotherapy drug libraries offer critical safety controls, such as dose capping depending on the calculation of the body surface area, checking on intricate dosing routines, and giving warnings on the likelihood of medication mistakes.

Another large area of application is the diabetes segment, where the insulin infusion pumps offer continuous subcutaneous insulin administration to diabetic patients with type 1 diabetes and a small number of type 2 diabetes patients who need intensive insulin therapy. Insulin delivery devices are in sustained demand because of the global number of 589 million adults with diabetes in the year 2025 which is set to rise to 853 million individuals in 2050. Insulin infusion pumps have been shown to be superior in glycemic control over multiple daily injections and include basal insulin delivery with adjustable rates that may fluctuate throughout the day, accuracy of bolus dosing of meals and glucose corrections, and the ability to be linked with continuous glucose monitoring systems to allow semi-automated delivery of insulin.

The most significant growth is observed in the pediatrics/neonatology segment, and its most forecastable CAGR is 9.7% in the period between 2026 and 2035, which is due to the specifics of medication delivery in infants and children. Pediatric and neonatal patients are extremely delicate when it comes to infusion because of their small bodies, underdeveloped organ systems that can be affected by the error of medication and weight-based dosing calculations that need high levels of accuracy. Pediatric dedicated infusion pumps have low volume accuracy delivery functions, weight-based dosing calculators incorporated within the programming of the pump, and safety measures tailored to vulnerable patient groups.

By End-User

Why Hospitals Dominate Infusion Pump Adoption?

The biggest end-user market is hospitals where they will occupy about 73% of the market share by 2025. Such dominance is indicative of the acute care medication delivery that is concentrated in hospital-based settings where critically ill patients are provided with constant infusion therapy and surgical patients with perioperative medication administration and a wide range of patient populations with treatments that could not be provided through other routes. Hospitals have the highest installed base of infusion pumps with extensive fleets of hundreds or even thousands of pumps in various units and specialties in large medical centers.

Smart pump technology that has high levels of safety in making procurement decisions, interoperability with hospital information systems, and enterprise-wide standardization of infusion pumps is becoming crucial in hospital infusion pump procurement decisions. Market statistics show that the majority of the market share was taken by hospitals in 2023 (46.4%) due to the growing geriatric population that needed special patient handling equipment and more stringent safety rules. Smart infusion pump networks with centralized fleet management, automatic drug library updates on all devices, and wireless connectivity which provides real time monitoring and extensive data analytics to initiate quality improvement efforts are costly investments by healthcare facilities. Patient safety, compliance with the law, and the minimization of medication errors are the primary motivators behind the focus of the hospital administrators on advanced infusion technology as an essential part of an infrastructure that can help hospitals provide high-quality care.

Home care environments are the most rapidly expanding end user market with the projected CAGR of 10.2% between 2026 and 2035 as the world moves towards in-home care delivery. Such fast growth is explained by the rising demand in the specially designed equipment that should be used in residential settings when patients have chronic conditions, need long-term antibiotic treatment, need constant pain medication, or undergo home chemotherapy. Home healthcare infusion services offer less but equally expensive options to hospital-based care where payors are increasingly paying for home infusion therapy and durable medical equipment. Safe home infusion programs can be realized with the help of the development of user-friendly ambulatory pumps that can be operated by patients and family caregivers with the assistance of telehealth platforms allowing remote monitoring and support.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 7.25 billion |

| Projected Market Size in 2035 | USD 14.02 billion |

| Market Size in 2025 | USD 6.72 billion |

| CAGR Growth Rate | 7.6% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Product Type, Disease Indication, End-User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the North America Market Size?

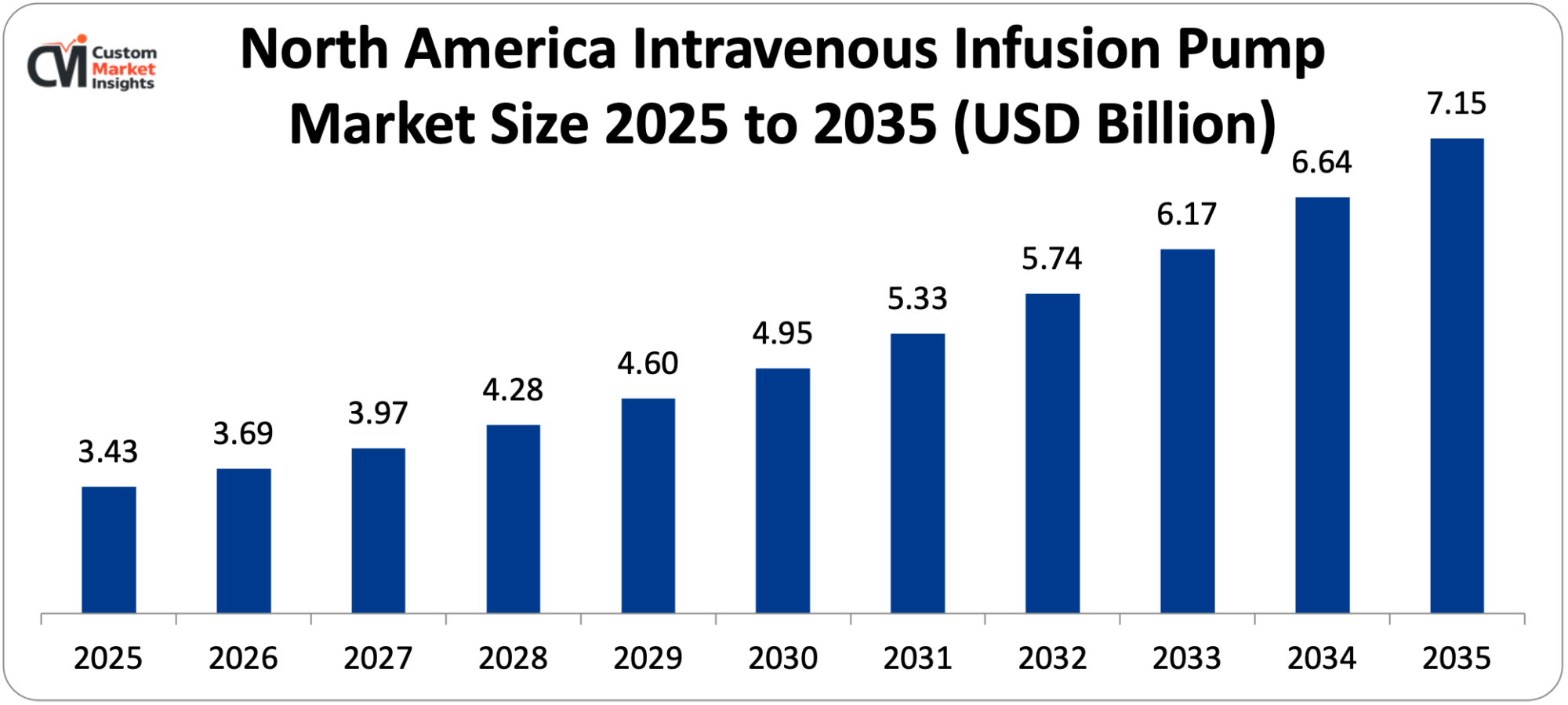

The North America intravenous infusion pump market size is estimated at USD 3.43 billion in 2025 and is projected to reach approximately USD 7.15 billion by 2035, with a 7.2% CAGR from 2026 to 2035.

Why did North America Dominate the Market in 2025?

The most influential worldwide with approximately 51% in 2025 is North America due to the developed healthcare facilities, the extensive use of the smart infusion pump, strict medication safety standards, the availability of developed reimbursement systems, and the existence of the best manufacturers. The largest contribution to the revenue of the region is the United States where more than 41% of the U.S. hospitals will have been equipped with smart infusion pumps by 2025. Technology is adopted by federal and state relationships that encourage patient safety, FDA regulations of advanced safety solutions in novice infusion pumps, and healthcare quality indicators linked to the decrease of medication errors.

What is the Size of the U.S. Market?

The intravenous infusion pump market size of the U.S. is estimated at USD 2.96 billion in the year 2025 and a projected 2035 of almost USD 6.15 million with a high CAGR of 7.5% during 2026-2035.

U.S. Market Trends

The US market is the biggest segment of the worldwide demand as a result of high healthcare expenditures, advanced hospital systems adopting extensive smart pump initiatives, rising focus on interoperability and health IT integration, broadening domestic healthcare provisions, and demographic aging rising the manifestation of chronic illnesses. The regulatory supervision of the FDA has ensured a steady enhancement of the safety of the infusion pump, recent clearances comprise the BD Alaris Infusion System with Guardrails Suite MX in April 2025 and 510(k) clearance for the Plum Solo precision IV pump manufactured by ICU Medical.

Why is Asia Pacific Experiencing the Fastest Growth?

It is expected that the Asia-Pacific region will show the highest growth, and its CAGR is estimated to be 9.3 between 2026 and 2035. The rapid growth indicates the rising healthcare expenditure, rising hospital infrastructures, rising prevalence of chronic conditions, rise in awareness of medication safety, and government programs that encouraged healthcare modernization. The biggest markets are China, India, and Japan, which between them make the majority of the regional demand.

China Market Trends

China boasts of a booming market owing to government healthcare reform efforts, huge investment in hospital infrastructure, rising numbers in the middle-class population who have more access to healthcare, and growing healthcare manufacturing capacities. The local manufacturers such as Shenzhen Mindray are coming up with competitive infusion pump systems, with international manufacturers setting up local production and distribution networks.

Why is Europe Entering a New Era?

The European market is large and developed with well-developed healthcare systems, detailed patient safety policies, high attention to minimization of medication errors, and well-developed hospital facilities. Europe has a large share in global markets with Germany taking 26.3% of European market share in 2025, the UK coming in with 21.8 and France with 18.5%.

Germany Market Trends

Advanced healthcare system, a wide network of hospitals, numerous insurances, and a robust regulatory framework that accentuates the safety and quality of medical devices are the factors that have made Germany have one of the largest markets in Europe. German healthcare institutions exhibit a high level of innovative technology intake as well as adherence to evidence-based practices.

Why is the Middle East & Africa Region Accelerating Adoption?

The markets of the LAMEA region are characterized by much heterogeneity and variable development. Healthcare infrastructure investment, development of specialized hospitals, and modernization of care standards have proven to be increasing the adoption of the Middle East and especially GCC countries. Africa is characterized by immature market and its growth is pegged to the expansion of the healthcare facilities.

Brazil Market Trends

The market development of Brazil is promoted by the development of the industry of the private healthcare sector, the greater access to the modern medical technologies, the larger burden of the chronic diseases, and government programs that enhance the accessibility to healthcare. Brazilian healthcare infrastructure is still at its developmental stage; hence, infusion pump adoption is expected to be optimistic.

Top Players in the Market and Their Offerings

- Becton Dickinson and Company (BD)

- Baxter International Inc.

- Braun Melsungen AG

- Fresenius Kabi AG

- ICU Medical Inc.

- Medtronic plc

- Terumo Corporation

- Tandem Diabetes Care Inc.

- Smiths Medical (ICU Medical)

- Shenzhen Mindray Bio-Medical Electronics Co. Ltd.

- Others

Key Developments

The market has undergone significant developments as industry participants seek to expand capabilities and enhance product portfolios.

- In April 2025: Becton, Dickinson and Company received FDA clearance for the BD Alaris Infusion System with Guardrails Suite MX, including modules like PC Unit, Pump, Syringe, PCA, EtCO2, Auto-ID, and System Manager, enhancing safety features for patients and representing the latest advancement in BD’s comprehensive infusion platform. (Source: https://www.accessdata.fda.gov/cdrh_docs/pdf24/K243855.pdf)

- In April 2025: Tandem Diabetes Care launched Control-IQ+ insulin delivery technology in the U.S., an automated system expanding accessibility to adults with type 2 diabetes and children aged two and older with type 1 diabetes, representing a significant advancement in diabetes management technology. (Source: https://investor.tandemdiabetes.com/news-releases/news-release-details/tandem-diabetes-care-launches-new-control-iq-automated-insulin)

These strategic activities have allowed companies to strengthen market positions, expand product offerings, and capitalize on growth opportunities within the expanding market.

The Intravenous Infusion Pump Market is segmented as follows:

By Product Type

- Volumetric Infusion Pumps

- Large Volume Pumps

- Small Volume Pumps

- Syringe Infusion Pumps

- Ambulatory Infusion Pumps

- Disposable Pumps

- Chemotherapy Infusion Pumps

- Patient-Controlled Analgesia (PCA) Pumps

- Implantable Infusion Pumps

- Insulin Infusion Pumps

- Infusion Pump Accessories and Consumables

By Disease Indication

- Chemotherapy

- Diabetes

- Gastroenterology

- Analgesia/Pain Management

- Pediatrics/Neonatology

- Hematology

- Other Applications

By End-User

- Hospitals

- Home Care Settings

- Ambulatory Care Centers

- Other End-Users

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Preface

- 1.1 Report Description and Scope

- 1.2 Research scope

- 1.3 Research methodology

- 1.3.1 Market Research Type

- 1.3.2 Market research methodology

- Chapter 2. Executive Summary

- 2.1 Global Intravenous Infusion Pump Market, (2026 – 2035) (USD Billion)

- 2.2 Global Intravenous Infusion Pump Market: snapshot

- Chapter 3. Global Intravenous Infusion Pump Market – Industry Analysis

- 3.1 Intravenous Infusion Pump Market: Market Dynamics

- 3.2 Market Drivers

- 3.2.1 Rising Prevalence of Chronic Diseases and Medication Delivery Needs

- 3.2.2 Technological Advancements and Smart Pump Integration with Healthcare IT

- 3.3 Market Restraints

- 3.4 Market Opportunities

- 3.5 Market Challenges

- 3.6 Porter’s Five Forces Analysis

- 3.7 Market Attractiveness Analysis

- 3.7.1 Market attractiveness analysis By Product Type

- 3.7.2 Market attractiveness analysis By Disease Indication

- 3.7.3 Market attractiveness analysis By End-User

- Chapter 4. Global Intravenous Infusion Pump Market- Competitive Landscape

- 4.1 Company market share analysis

- 4.1.1 Global Intravenous Infusion Pump Market: company market share, 2025

- 4.2 Strategic development

- 4.2.1 Acquisitions & mergers

- 4.2.2 New Product launches

- 4.2.3 Agreements, partnerships, collaborations, and joint ventures

- 4.2.4 Research and development and Regional expansion

- 4.3 Price trend analysis

- 4.1 Company market share analysis

- Chapter 5. Global Intravenous Infusion Pump Market – Product Type Analysis

- 5.1 Global Intravenous Infusion Pump Market overview: By Product Type

- 5.1.1 Global Intravenous Infusion Pump Market share, By Product Type, 2025 and 2035

- 5.2 Volumetric Infusion Pumps

- 5.2.1 Global Intravenous Infusion Pump Market by Volumetric Infusion Pumps, 2026 – 2035 (USD Billion)

- 5.3 Large Volume Pumps

- 5.3.1 Global Intravenous Infusion Pump Market by Large Volume Pumps, 2026 – 2035 (USD Billion)

- 5.4 Small Volume Pumps

- 5.4.1 Global Intravenous Infusion Pump Market by Small Volume Pumps, 2026 – 2035 (USD Billion)

- 5.5 Syringe Infusion Pumps

- 5.5.1 Global Intravenous Infusion Pump Market by Syringe Infusion Pumps, 2026 – 2035 (USD Billion)

- 5.6 Ambulatory Infusion Pumps

- 5.6.1 Global Intravenous Infusion Pump Market by Ambulatory Infusion Pumps, 2026 – 2035 (USD Billion)

- 5.7 Disposable Pumps

- 5.7.1 Global Intravenous Infusion Pump Market by Disposable Pumps, 2026 – 2035 (USD Billion)

- 5.8 Chemotherapy Infusion Pumps

- 5.8.1 Global Intravenous Infusion Pump Market by Chemotherapy Infusion Pumps, 2026 – 2035 (USD Billion)

- 5.9 Patient-Controlled Analgesia (PCA) Pumps

- 5.9.1 Global Intravenous Infusion Pump Market by Patient-Controlled Analgesia (PCA) Pumps, 2026 – 2035 (USD Billion)

- 5.10 Implantable Infusion Pumps

- 5.10.1 Global Intravenous Infusion Pump Market by Implantable Infusion Pumps, 2026 – 2035 (USD Billion)

- 5.11 Insulin Infusion Pumps

- 5.11.1 Global Intravenous Infusion Pump Market by Insulin Infusion Pumps, 2026 – 2035 (USD Billion)

- 5.12 Infusion Pump Accessories and Consumables

- 5.12.1 Global Intravenous Infusion Pump Market by Infusion Pump Accessories and Consumables, 2026 – 2035 (USD Billion)

- 5.1 Global Intravenous Infusion Pump Market overview: By Product Type

- Chapter 6. Global Intravenous Infusion Pump Market – Disease Indication Analysis

- 6.1 Global Intravenous Infusion Pump Market overview: By Disease Indication

- 6.1.1 Global Intravenous Infusion Pump Market share, By Disease Indication, 2025 and 2035

- 6.2 Chemotherapy

- 6.2.1 Global Intravenous Infusion Pump Market by Chemotherapy, 2026 – 2035 (USD Billion)

- 6.3 Diabetes

- 6.3.1 Global Intravenous Infusion Pump Market by Diabetes, 2026 – 2035 (USD Billion)

- 6.4 Gastroenterology

- 6.4.1 Global Intravenous Infusion Pump Market by Gastroenterology, 2026 – 2035 (USD Billion)

- 6.5 Analgesia/Pain Management

- 6.5.1 Global Intravenous Infusion Pump Market by Analgesia/Pain Management, 2026 – 2035 (USD Billion)

- 6.6 Pediatrics/Neonatology

- 6.6.1 Global Intravenous Infusion Pump Market by Pediatrics/Neonatology, 2026 – 2035 (USD Billion)

- 6.7 Hematology

- 6.7.1 Global Intravenous Infusion Pump Market by Hematology, 2026 – 2035 (USD Billion)

- 6.8 Other Applications

- 6.8.1 Global Intravenous Infusion Pump Market by Other Applications, 2026 – 2035 (USD Billion)

- 6.1 Global Intravenous Infusion Pump Market overview: By Disease Indication

- Chapter 7. Global Intravenous Infusion Pump Market – End-User Analysis

- 7.1 Global Intravenous Infusion Pump Market overview: By End-User

- 7.1.1 Global Intravenous Infusion Pump Market share, By End-User, 2025 and 2035

- 7.2 Hospitals

- 7.2.1 Global Intravenous Infusion Pump Market by Hospitals, 2026 – 2035 (USD Billion)

- 7.3 Home Care Settings

- 7.3.1 Global Intravenous Infusion Pump Market by Home Care Settings, 2026 – 2035 (USD Billion)

- 7.4 Ambulatory Care Centers

- 7.4.1 Global Intravenous Infusion Pump Market by Ambulatory Care Centers, 2026 – 2035 (USD Billion)

- 7.5 Other End-Users

- 7.5.1 Global Intravenous Infusion Pump Market by Other End-Users, 2026 – 2035 (USD Billion)

- 7.1 Global Intravenous Infusion Pump Market overview: By End-User

- Chapter 8. Intravenous Infusion Pump Market – Regional Analysis

- 8.1 Global Intravenous Infusion Pump Market Regional Overview

- 8.2 Global Intravenous Infusion Pump Market Share, by Region, 2025 & 2035 (USD Billion)

- 8.3. North America

- 8.3.1 North America Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.3.1.1 North America Intravenous Infusion Pump Market, by Country, 2026 – 2035 (USD Billion)

- 8.3.1 North America Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.4 North America Intravenous Infusion Pump Market, by Product Type, 2026 – 2035

- 8.4.1 North America Intravenous Infusion Pump Market, by Product Type, 2026 – 2035 (USD Billion)

- 8.5 North America Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035

- 8.5.1 North America Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035 (USD Billion)

- 8.6 North America Intravenous Infusion Pump Market, by End-User, 2026 – 2035

- 8.6.1 North America Intravenous Infusion Pump Market, by End-User, 2026 – 2035 (USD Billion)

- 8.7. Europe

- 8.7.1 Europe Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.7.1.1 Europe Intravenous Infusion Pump Market, by Country, 2026 – 2035 (USD Billion)

- 8.7.1 Europe Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.8 Europe Intravenous Infusion Pump Market, by Product Type, 2026 – 2035

- 8.8.1 Europe Intravenous Infusion Pump Market, by Product Type, 2026 – 2035 (USD Billion)

- 8.9 Europe Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035

- 8.9.1 Europe Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035 (USD Billion)

- 8.10 Europe Intravenous Infusion Pump Market, by End-User, 2026 – 2035

- 8.10.1 Europe Intravenous Infusion Pump Market, by End-User, 2026 – 2035 (USD Billion)

- 8.11. Asia Pacific

- 8.11.1 Asia Pacific Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.11.1.1 Asia Pacific Intravenous Infusion Pump Market, by Country, 2026 – 2035 (USD Billion)

- 8.11.1 Asia Pacific Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.12 Asia Pacific Intravenous Infusion Pump Market, by Product Type, 2026 – 2035

- 8.12.1 Asia Pacific Intravenous Infusion Pump Market, by Product Type, 2026 – 2035 (USD Billion)

- 8.13 Asia Pacific Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035

- 8.13.1 Asia Pacific Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035 (USD Billion)

- 8.14 Asia Pacific Intravenous Infusion Pump Market, by End-User, 2026 – 2035

- 8.14.1 Asia Pacific Intravenous Infusion Pump Market, by End-User, 2026 – 2035 (USD Billion)

- 8.15. Latin America

- 8.15.1 Latin America Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.15.1.1 Latin America Intravenous Infusion Pump Market, by Country, 2026 – 2035 (USD Billion)

- 8.15.1 Latin America Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.16 Latin America Intravenous Infusion Pump Market, by Product Type, 2026 – 2035

- 8.16.1 Latin America Intravenous Infusion Pump Market, by Product Type, 2026 – 2035 (USD Billion)

- 8.17 Latin America Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035

- 8.17.1 Latin America Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035 (USD Billion)

- 8.18 Latin America Intravenous Infusion Pump Market, by End-User, 2026 – 2035

- 8.18.1 Latin America Intravenous Infusion Pump Market, by End-User, 2026 – 2035 (USD Billion)

- 8.19. The Middle-East and Africa

- 8.19.1 The Middle-East and Africa Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.19.1.1 The Middle-East and Africa Intravenous Infusion Pump Market, by Country, 2026 – 2035 (USD Billion)

- 8.19.1 The Middle-East and Africa Intravenous Infusion Pump Market, 2026 – 2035 (USD Billion)

- 8.20 The Middle-East and Africa Intravenous Infusion Pump Market, by Product Type, 2026 – 2035

- 8.20.1 The Middle-East and Africa Intravenous Infusion Pump Market, by Product Type, 2026 – 2035 (USD Billion)

- 8.21 The Middle-East and Africa Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035

- 8.21.1 The Middle-East and Africa Intravenous Infusion Pump Market, by Disease Indication, 2026 – 2035 (USD Billion)

- 8.22 The Middle-East and Africa Intravenous Infusion Pump Market, by End-User, 2026 – 2035

- 8.22.1 The Middle-East and Africa Intravenous Infusion Pump Market, by End-User, 2026 – 2035 (USD Billion)

- Chapter 9. Company Profiles

- 9.1 Becton Dickinson and Company (BD)

- 9.1.1 Overview

- 9.1.2 Financials

- 9.1.3 Product Portfolio

- 9.1.4 Business Strategy

- 9.1.5 Recent Developments

- 9.2 Baxter International Inc.

- 9.3 B. Braun Melsungen AG

- 9.4 Fresenius Kabi AG

- 9.5 ICU Medical Inc.

- 9.6 Medtronic plc

- 9.7 Terumo Corporation

- 9.8 Tandem Diabetes Care Inc.

- 9.9 Smiths Medical (ICU Medical)

- 9.10 Shenzhen Mindray Bio-Medical Electronics Co. Ltd.

- 9.11 Others

- 9.1 Becton Dickinson and Company (BD)

List Of Figures

Figures No 1 to 38

List Of Tables

Tables No 1 to 77

Prominent Player

- Becton Dickinson and Company (BD)

- Baxter International Inc.

- Braun Melsungen AG

- Fresenius Kabi AG

- ICU Medical Inc.

- Medtronic plc

- Terumo Corporation

- Tandem Diabetes Care Inc.

- Smiths Medical (ICU Medical)

- Shenzhen Mindray Bio-Medical Electronics Co. Ltd.

- Others

FAQs

The key players in the market are Becton Dickinson and Company (BD), Baxter International Inc., B. Braun Melsungen AG, Fresenius Kabi AG, ICU Medical Inc., Medtronic plc, Terumo Corporation, Tandem Diabetes Care Inc., Smiths Medical (ICU Medical), Shenzhen Mindray Bio-Medical Electronics Co. Ltd., Others.

Government regulations play a major role in the market, such as FDA approval of medical devices such as premarket notification (510(k)) clearance, post-market surveillance to identify adverse events related to the device, mandatory safety features in new pump design, clinical practice guidelines to use smart pumps and drug libraries to comply with new technologies, reimbursement policies to cover the infusion therapy services, and patient safety programs such as Centers for Medicare and Medicaid Services quality measures which are based on the rate of medication errors, which make advanced infusion pumps an important necessity.

The cost of equipment is an adoption barrier especially in resource-constrained environments. Smart infusion pumps are generally between USD 3,000 and USD 15,000 per device based on features and a full hospital implementation (wireless infrastructure, central monitoring stations, and enterprise wide integration of Smart Infusion Pumps) costs millions of capital. Nevertheless, there are various considerations that enhance accessibility such as proven cost benefits in the form of fewer mistakes in medication administration with one health system saving USD 531,891 per year by avoiding 56 avoidable adverse drug events, enhanced charge capture by recovering lost billing revenue, leasing and rental equipment, and insurance reimbursement of home infusion therapy and durable medical equipment.

According to the present-day analysis, the market is expected to rise to about USD 14.02 billion by 2035 and experience solid growth due to the increased burden of chronic diseases, the aging demographic, the development of improving smart pump technology with AI and interoperability capabilities, increased use of home healthcare, and the sustained focus on medication safety and error reduction with a CAGR of 7.6% between 2026 and 2035.

It is projected that North America will control the largest market share in terms of revenue with an estimated market share of 51% of the total global market as a result of well-developed healthcare infrastructures, high take-up rates of smart infusion pumps (with 41% of hospitals in the U.S. currently using smart pumps), strict medication safety regulations, extensive reimbursement systems, and the industry having major industry players like BD, Baxter, and ICU Medical with a high healthcare expenditure on the use of advanced medical technologies.

It is assumed that the Asia-Pacific Region will have the greatest CAGR of about 9.3 in the forecast period because of the phenomenally growing healthcare spending, increasing hospital facilities, growing prevalence of chronic diseases, growing consciousness of medication safety standards, government actions of promoting healthcare modernization and huge population bases in such countries as China, India, Japan, and South Korea, which establish high absolute demand.

The Global Intravenous Infusion Pump Market is forecasted to grow at an enormous rate because of the rising prevalence of chronic diseases with 589 million adults worldwide living with diabetes and 853 million patients as the number rises to 2050, the aging population, the expansion of home care; technology development with AI-powered smart pumps and integration of EHRs to minimize medication errors by 15.4-54.8%; and strict safety requirements, with about 4,000 preventable injuries per hospital year caused by medication errors.