US Cold Storage Market Size, Trends and Insights By Warehouse Type (Private and Semi-Private Warehouses, Public Warehouses), By Construction Type (Bulk Storage, Production Stores, Ports), By Temperature Type (Chilled (Above 0°C), Frozen (-18°C to -25°C)), By Application (Food and Beverages, Fruits and Vegetables, Meat and Poultry, Seafood, Dairy Products, Frozen Foods, Bakery Products, Pharmaceuticals, Vaccines, Biologics, Blood Products, Chemicals, Other Applications), and By Region - Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 10.66%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | USA |

| Largest Market: | USA |

Major Players

- Lineage Logistics Holdings, LLC

- Americold Realty Trust Inc.

- S. Cold Storage Inc.

- Agro Merchants Group LLC

- Others

Reports Description

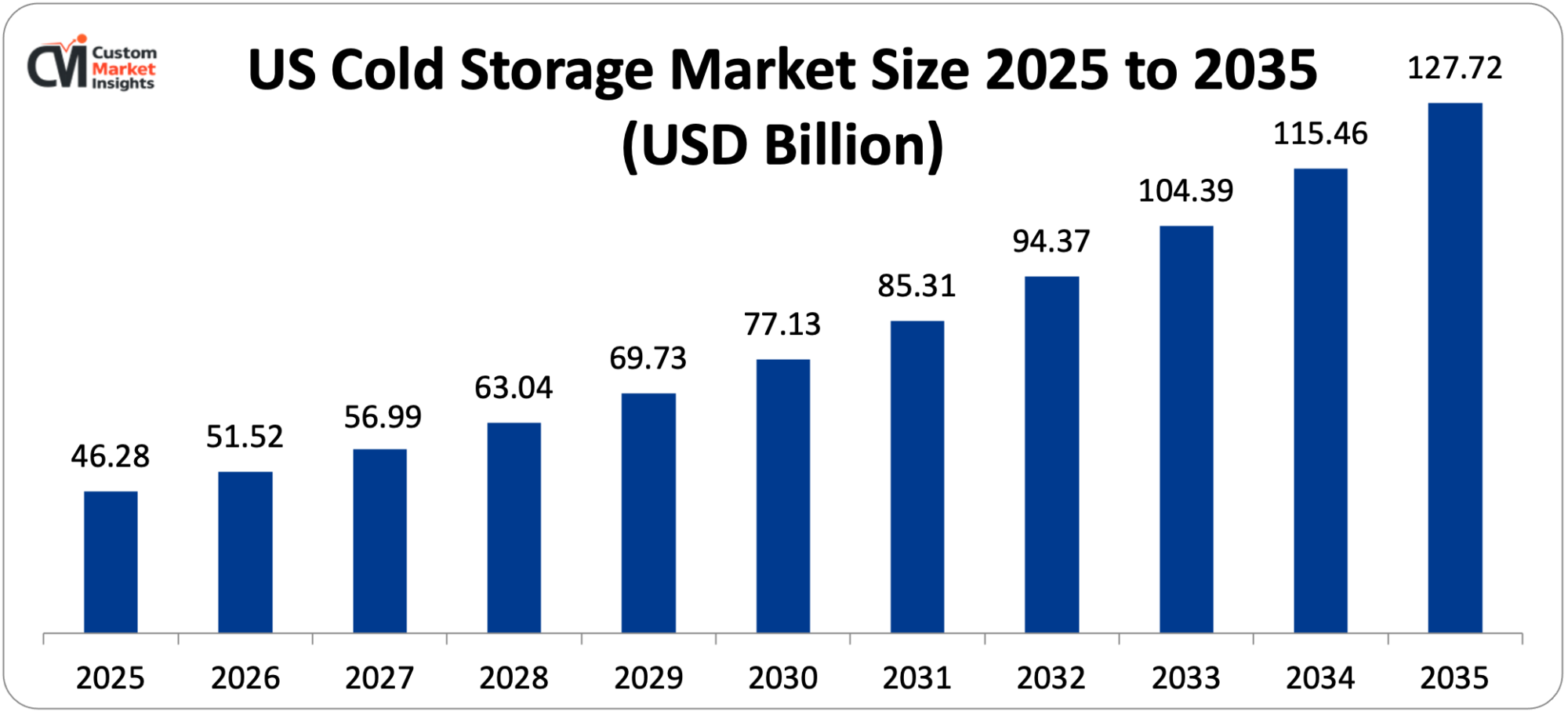

The market size of cold storage in the US is estimated at USD 46.28 billion in 2025 and its market growth is expected to rise from between USD 51.52 billion and USD 127.72 billion between 2026 and 2035 with a CAGR of 10.66%. The increasing sales in e-commerce groceries and meal kit delivery services, increasing pharmaceutical cold chain needs to distribute biologics and deliver vaccines, the mass use of automation technologies, strict food safety standards, the growing demand for fresh and frozen goods, the proliferation of food waste reduction efforts, and technological developments in refrigeration systems promote the growth of the market.

Market Highlight

- In 2025, the US has been estimated to possess a 34.1% market share in the global cold storage market, which is the largest single country market in the world in terms of temperature controlled warehousing.

- By type of warehouse, the refrigerated warehouse segment had a market share of about 59.3% in 2025 with centralized storage needs of perishable goods.

- Regarding the type of warehouses, the area with the highest CAGR of 12.94% in 2026-2035 is the public warehouse segment due to the growth of third-party logistics and the rise in e-commerce demand.

- Application The food and beverages segment is projected to provide the highest market share of 77% in 2025, whereas the pharmaceuticals segment is projected to grow at a CAGR of 13.82% within the potential time frame of 2026-35.

- By type of storage, frozen storage owned 62% of the market in 2025, at which frozen vegetables, meat, seafood, and prepared frozen foods were stored at -18°C to -25°C.

- Infrastructure capacity to accommodate market growth: Market Leading suppliers such as Lineage logistics and Americold have increased their cold storage capacity by more than 18 million square feet since 2019 and reflect the significant infrastructure development.

Significant Growth Factors

The US Cold Storage Market Trends present significant growth opportunities due to several factors:

- Explosive E-Commerce Grocery Growth and Last-Mile Delivery Transformation:

The underlying force behind the cold storage market growth is the exponential rise of e-commerce grocery purchases and online food delivery services, with retailers and third-party logistics providers developing urban micro-fulfillment centers, building refrigerated distribution systems, and investing in the last-mile delivery systems to satisfy the consumer need to have fresh and frozen products delivered to their doorsteps.

The online grocery sales in the United States have grown by over USD 1 billion in two consecutive months of 2025 as per Brick Meets Click and Mercatus data, reflecting the growth of consumers using e-grocery stores because of the temperature-controlled storage needs. E-commerce grocery sales hit an apocalyptic high of about USD 9.8 billion every month in April 2025, a 15% year-over-year growth, and May 2025 sales had reached USD 27.0 billion, 27% annually, as the online grocery penetration accelerated with unparalleled urgency, demanding cold storage capacity at membership levels never attempted or experienced before.

Online grocery has grown to over 20% and is now the new reality with a penetration rate of more than 13% in 2021, and this represents the radical change in consumer shopping behavior that has led retailers and logistics providers to invest billions of dollars in cold chain infrastructure to support the fulfillment of e-commerce. It is estimated that online grocery will take 21.5% of all grocery sales in the US by 2025 and that this will prompt retailers and logistics providers to remodel current facilities or construct specific micro-fulfillment centers in the urban centers to reduce the lead time of last-mile operations and allow retailers to deliver perishable goods in the same-day or next-day timeframe.

The onset of fast-commerce formats with sub-60-minute delivery times puts an even greater strain on high-throughput refrigerated and frozen areas, located near consumers, which spreads cold storage space to dense urban centers and outlying markets, which the traditional warehouse model had not previously served. Delivery of meal kits such as Blue Apron, HelloFresh and Home Chef needs advanced cold chain logistics with recipe ingredients staying fresh in central commissaries to the end destination, which prompts special cold storage facilities to support assembly, use of multiple temperature stages, and quick turnaround order delivery. Shuttle automation, robotic picking, click and collect bays, and hybrid facilities that blur the line between store and warehouse operations are being introduced to establish temperature-controlled fulfillment centers that can handle thousands of orders each day whilst having a high level of strict temperature controls that protect the quality of products and food safety during both the process of ordering and dispatching products.

- Escalating Food Waste Crisis and Cold Chain Infrastructure Imperative:

The sheer volume of food waste in the United States at 30-40% of the food supply each year is both a challenge and critical opportunity for cold storage expansion, and an improved temperature-controlled infrastructure is a must for extending the shelf life, reducing food spoilage, preserving food quality, and food waste reduction programs aimed at achieving the 2030 target of cutting waste by 50%. ReFED data state that in 2024 the United States would permit 29% of the 240 million tons of food supply to remain unsold or uninvolved in any way as surplus food, and that one-fourth of all food, 63 million tons with a total value of USD 384 billion, would go to waste destinations, such as landfills, incineration, or disposal, equating to nearly 115 billion meals of food wasted each year or 1.3% of the United States GDP. Food waste exists at every step of the supply chain and EPA estimates show that in 2019, 66 million tons of wasted food were produced in food retail, food service, and residential sectors, most of which (approximately 60 million tons) was sent to landfills, with another 40 million tons produced in food and beverage manufacturing and processing sectors, showing how widespread the problem is in the system and requiring all-solutions cold chain efforts.

The amount of food that the United States throws in the trash every year is 60 million tons, or 120 billion pounds, about 40% of the total food supply, and it is equivalent to 325 pounds of waste per capita, with food being the greatest of all, with 22% of the total of municipal solid waste being constituted by food, which causes an environmental crisis that cold storage is able to resolve by improving food preservation. Among the groceries that are not eaten in the house and the plate waste in restaurants, consumers discard nearly USD 261 billion in food annually (equivalent to 35 million tons) with an economic incentive of better cold storage to decrease spoilage, and food producers and businesses lose USD 108 billion in revenue at the point of the plate (equivalent to 21.5 million tons). Perceived or real food spoilage is one of the largest causes of food being thrown away in the US, with over 80% disposing of perfectly edible food that can still be consumed due to poor understanding of edible date labels such as sell by, use by, and best before dates, which implies that improved cold storage with improved inventory control will increase the lifespan of edible products.

The USDA and EPA have set the goal of a 50% reduction of food waste in the country by 2030 with states such as California, Connecticut, Massachusetts, New York, Rhode Island and Vermont passing state laws to limit food waste to landfills and Vermont passing the Universal Recycling Law which outlawed food scrap waste, leading to 40% growth in food donation across the state showing regulatory drivers to support cold storage investments. The cold storage infrastructure is a direct answer to food waste in the form of extending the shelf life of perishable food which allows processing seasonal inventory, facilitates distribution across geographic locations between production and consumption regions, and ensures the quality of food during extended supply chains to prevent spoilage of otherwise edible foods before they go to waste.

- Pharmaceutical Cold Chain Revolution Driven by Biologics and Vaccine Distribution:

The ever-growing pharmaceutical cold chain needs, especially of temperature-sensitive biologics, cell and gene therapies, and vaccine distribution, can be seen as a transformational growth driver that generates demand for ultra-low temperature storage facilities, temperature monitoring systems that are validated, redundant cooling, and specialized logistics networks that support the integrity of pharmaceutical products. Pharmaceuticals that are sensitive to temperature such as refrigerated products that need 2°C to 8°C storage or ultra-low temperature vaccinations that need -80°C to -60°C storage, are rapidly growing in the cold chain logistics sector, and pharmaceutical shippers are now outsourcing temperature-regulated storage to third-party logistics firms that provide audited quality management systems and demonstrated data recording capabilities.

The pharmaceutical cold storage products provided by logistics providers include centralised automated ultra-low temperature chambers with backup cooling, twenty-four-hour temperature control and real-time notifications, approved Standard Operating Procedures, GMP-based process workflows, and disaster recovery plans ensuring the protection of pharmaceutical products worth hundreds of millions of dollars. The companies involved in pharmaceuticals are shifting to out-of-house cold storage with third-party vendors with certified infrastructure, avoiding capital outlay in owning warehousing, accessing scalable capacity during demand changes, capitalizing on provider experience in compliance with regulations, and having established transportation networks that provide seamless delivery of these temperature-sensitive pharmaceuticals to the health organizations, pharmacies and patients in need.

What are the Major Advances Changing the US Cold Storage Market Today?

- Automation and Robotics Integration Revolutionizing Operations:

The most radical technology change in cold storage operations is the widespread use of automation technologies such as automated storage and retrieval systems (AS/RS), autonomous forklifts, robot palletizers, AI-powered inventory management platforms, and integrated warehouse management systems which can help address chronic labor shortages, increase operational efficiency, and optimize space utilization as well as energy consumption without compromising on temperature control.

The use of automation technologies to solve the long-term labor shortages that affect the operations of the warehouse is in the acceleration phase by cold storage operators nationwide, and automated systems are allowing 24/7 operation to occur without any reliance on human labor due to the harsh environment in the refrigerated warehouse and the high turnover and productivity is being enhanced through the consistent handling of products by an automated system that eliminates fatigue-related errors. In October 2025, Tjoapack improved its sterile packaging and cold chain storage systems in the United States and Europe, investing in infrastructure at its plant in Clinton, New York, whereby two new packaging lines were installed, inclusive of a fully automated high-speed vial packaging line that was commissioned in the second quarter of 2025 and had an annual production capacity of up to 20 million units, reflecting the pharmaceutical cold storage automation trends.

In April 2025, Agile Cold storage of Georgia will celebrate the opening of their first plant in Joliet, Illinois with this semi-automated, multi-temperature facility of more than 200,000 square feet and will provide employment to a large number of people and also will offer value-added services such as case picking, loading/unloading containers, blast freezing, and tempering operation through automated systems. Robot systems optimize the use of space in temperature controlled facilities; they provide high density storage arrangements, narrow aisles through autonomous vehicles, high bay storage arrangements up to 100 plus feet and enhanced cube space by 30-40% over conventional layouts, which offer capacity growth without expanding the footprint of the facility. Automated systems also help goals of sustainability by minimizing use of energy consumption through optimization of door operation minimizing of temperature changes, controlling temperatures, eliminating overcooling wastes, automated light systems that are only on demand, and efficient movement routines that minimize equipment operational hours compared to that of manual operations where the system requires forklifts to continually move around.

AI-based inventory management systems offer real-time inventory location tracking, FIFO/FEFO rotation automation which ensures an inventory is being correctly turned over, prediction of demand trends to allow capacity planning ahead of time, improved picking paths and therefore less travel distance and time, and analytics to show which operations are operating inefficiently to support continuous improvement efforts to improve throughput and lower the cost. High-tech warehouse management systems are linked to transportation management, order management systems, and enterprise resource planning allowing seamless information flow within the supply chain partners, automated order processing leading to shorter fulfillment lead times, real time inventory balancing ensuring stock out, and decision making based on available data enhancing the overall supply chain responsiveness and customer satisfaction.

- Sustainable Refrigeration Technologies and Energy Efficiency Solutions:

The introduction of sustainable refrigeration technologies such as the use of natural refrigerants, energy efficient cooling systems, integration of renewable energy, introduction of LED lighting systems, building envelopes, and waste heat recovery systems are critical improvement areas in terms of the cost of operation and environmental sustainability with electricity making up 50-70% of cold warehouse operating expenses creating major investments in energy reducing technologies. Renewable energy integration in advanced energy management systems is assisting cold storage operators in putting downward pressure on electricity expenses, and solar panel installations on warehouse roofs produce on-site power to eliminate grid reliance, battery storage systems store surplus solar generation to use during peak demand situations and utility-scale renewable energy contracts provide certainty in electricity prices against volatile electricity prices.

New and retrofitted plants are using natural refrigerants such as ammonia, carbon dioxide and propane to replace high-global-warming-potency refrigerants, enhance energy efficiency due to high thermodynamic factors, lower regulatory compliance liabilities due to HFC phase-down acceleration, and promote corporate sustainability pledges to climate change issues. Variable frequency drives on refrigeration compressors, fans and pumps adjust equipment operation to best match actual load needs as opposed to operating at a maximum capacity, which will save 20-40% of energy usage and extend equipment life due to reduced operating stress, decreased maintenance needs, and decreased equipment wear due to smoother operation and less cycling.

LED lighting systems have been implemented in cold storage facilities at the expense of metal halide and fluorescent lighting systems and save 50-70% of the lighting energy, generate no heat to add to cooling loads, increase light quality and visibility to enhance worker safety, and offer a longer service life that reduces maintenance costs and operational losses experienced as a result of lighting failures. Improvements to the building envelope such as high-performance insulation panels with an R-value of more than R-40, door systems that are airtight and minimise infiltration, vestibules and air curtains at dock doors that reduce temperature loss, and reflective roof materials that reduce solar heat gain minimise the amount of energy needed to maintain target temperatures in refrigerated and frozen areas. Waste heat recovery systems exploit the thermal energy produced by the refrigeration system condenser operations and redirect waste heat to serve the office heating, domestic hot water heating, and ice and snow melting systems or even resell it to other nearby facilities and using the operational byproduct to enhance the overall energy efficiency and reduce the operating costs of the facility.

- Geographic Expansion and Strategic Location Development:

The extensive location development of cold storage facilities in major geographic markets, such as port cities that support international trade, food production areas that support farm-to-warehouse locations, urban areas that serve population centers and sunbelt states that have grown exponentially in population are indicative of significant market evolution with the facility location decision-making being influenced by the optimization of supply chains, cost reduction in transportation, and proximity to the location of demand centers.

The booming tourism business and online grocery markets in the State of Florida are considered major demand factors that underline decentralized cold storage because of the short to medium run in the growth of the online grocers in the Florida market attributed to the introduction of continuous cold storage facilities over the next five years to boost demand by market players and the construction of more cold storage facilities around Miami and Orlando in the state responsive to the demand and supply side of the business. California is the largest food producer in America and thus the top destination of cold storage development with an estimate of about 396 million square feet of industrial cold space which proves to be very promising due to the e-grocery and fresh produce logistics converging in Los Angeles and the Central Valley presenting intense concentration of cold storage needs.

The New Orleans Cold storage Company of Louisiana has a total of four output port-based facilities of more than 15 million cubic feet with a blast-freezing capacity of over one point two million pounds per day, which is essential in meat and seafood imports that are sent through the Port of New Orleans and the Gulf Coast facilities which act as entry points to international trade and which the company is required to refrigerate immediately after clearance at customs before being distributed locally. The cold storage market competition is shifting towards a phase of consolidation where major market players are expanding their capacity with large scale capacity expansion by major industry players who are also implementing strategic acquisition of smaller sized companies with cold storage facilities (capacity) as well as associated assets to the tune of USD 247 Million as announced by Lineage Logistics in April 2025 to acquire four existing cold storage warehouses totaling approximately 49 million cubic feet capacity and associated assets in a deal with Tyson Foods.

The regional differences in cold storage adoption result in different market characteristics with the Northeast exhibiting the highest level of practice concentration of 54% using remote patient monitoring technologies to serve aging population, the South with low levels of telemedicine adoption of 28% citing patient preference of face-to-face visits, and the Midwest with moderate levels of technology integration demonstrating varying levels of market maturity.

Category Wise Insights

By Warehouse Type

Why Refrigerated Warehouses Lead the Market?

The largest segment comprises refrigerated warehouses, which will have a share of about 59.3 in 2025. This is a dominance that is based on the need to have consistency in the quality of products throughout the cold chain with goods stored in large, professionally operated refrigerated facilities that help maintain consistent temperature conditions between production and distribution limits to reduce spoilage, ensure a good fit in quality parameters of the goods on reaching the retailer and consumers, and improve the optimization of loads and transport to the suppliers. Fridge warehouses offer centralized storage, which allows economies of scale in the refrigeration business, and large facilities are more energy efficient per cubic foot than distributed smaller facilities, professionally managed, with specialized equipment such as loading docks, staging areas, and material handling equipment that is optimized to handle perishable products.

The marketability of refrigerated warehouses is informed by the fact that the issues of food safety and waste are on the rise, and professionally managed warehouses offer a reliable cold storage that allows extending shelf life, ensures the maintenance of safety standards, the proper rotation of inventory, and well-organized record-keeping with traceability and regulatory compliance needs that are ongoing in the food industry. The large retailers, distributors, and food processing companies require consolidated refrigerated warehouses, which are used to store the inventory of various suppliers, to consolidate the operations of cross-docking, to store the seasonal products, to provide the buffer inventory against disruptions in the supply chains, and to produce the continuous demand of third-party cold storage facilities of flexible capacity with specialized services.

The quickest growth is in public warehouses with a projected CAGR of 12.94% between 2026 and 2035 due to a surge in growth in cold storage networks by 3PLs to meet the growing demand of e-commerce and grocery delivery, retailers and food companies outsourcing operations to 3PLs with temperature-controlled warehouses minimizing capital exposure, and leading providers such as Lineage and Americold developing extensive networks adding an additional 18 million square feet of space since 2019.

The trend of outsourcing is undeniable as retailers and manufacturers hire the services of the public 3PL to provide multi-temperature footprints, flexible capacity to meet seasonal demands, and geographic coverage to support the national distribution networks, as well as expertise in cold chain management, food safety compliance, and regulatory demands that the company can hardly achieve in distributed facilities. Public warehousing allows firms to transform fixed capital investments into variable operating costs, have capacity during peak seasons without incurring idle capacity during other seasons, scale the economy of the provider, which results in lower per-unit costs, and concentrate internal resources on core competencies and not warehousing activities, which produces powerful economic rationales that justify outsourcing of the growth of the public warehouse segment.

By Application

Why Food and Beverages Dominate Cold Storage Applications?

The biggest area of application is the food and beverages segment which will amount to about 77% of all market share in 2025. This leadership is in regard to the core role played by cold storage in the food supply chain, whereby temperature controlled warehousing is vital in preserving perishable goods such as meat, poultry, seafood, dairy products, fruits, and vegetables in the distribution of products between production facilities and retail outlets or food service facilities.

The increasing use of perishable foods such as dairy products, fruits and vegetables, meat and seafood creates a high demand for temperature-regulated warehousing and transportation products that allow the smooth flow of perishable products from farm gates to processing, distribution, retailing and finally to the consumer tables without the destruction of quality and safety. The increase in consumer demands in terms of product availability all year round, fresh food demand irrespective of the season of the year, year-round availability of a wide range of proteins, and year-round availability of dairy products require the construction of cold storage facilities that support imports and exports by the global community, seasonal maintenance of inventory, and buffer stocks to avert supply shocks which guarantee the non-disruption of product supply.

The increasing food processing industry and increasing demand for convenient, pre-cooked food products such as frozen foods, prepared salads, meal kits, and processed food products with added value provide growing cold storage capacity to serve the manufacturing industries, finished goods storage, and distribution to retail and food service outlets where convenience foods are gaining an ever-increasing market share. Strict food safety laws such as those in the FDA Food Safety Modernization Act, USDA inspection regulations, and state/local health codes that require proper temperature control along food supply chains, cold storage facilities with validated temperature control systems, comprehensive record keeping, employee training, and preventive controls to ensure adherence to stringent food safety laws to protect the health of the population and prevent expensive recalls.

Pharmaceuticals is the fastest growing with a projected CAGR of 13.82% in the period 2026-2035 due to the expanding biologics and cell-and-gene therapy pipeline requiring ultra-low temperature storage, the increasing vaccine distribution needs following COVID-19 pandemic infrastructure investment, increasing pharmaceutical outsourcing to specialized third-party providers offering validated systems, and the growing demand of temperature-controlled distribution to protect high-value pharmaceutical investments throughout the supply chains.

The US cell therapy market that may reach USD 3.9 billion in 2024 and is expected to grow at a high rate creates a high cold storage demand, because such treatments need the lowest possible temperatures of -80: -196 o C to preserve the cellular activity, specialised handling protocols to avoid contamination and product degradation, a validated chain of custody to ensure regulatory compliance, and backup systems to prevent temperature outliers from destroying entire batches worth millions of dollars. Drugs and other products that are sensitive to temperatures such as vaccines, biologics, insulin, blood products, diagnostic reagents, and specialty drugs should be kept at a definite temperature, usually between 2°C and 8°C, where anything below or above this could render that product ineffective or unsafe, posing a liability risk, damaging patients, and costing pharmaceutical companies significant financial losses this makes validated cold storage with strict quality requirements.

By Temperature Type

Why Frozen Storage Dominates the Market?

The biggest segment is frozen storage with an estimated market share of around 62% in 2025. This dominance is associated with the capacity of frozen storage to maintain the quality of products over a long period, facilitate international trade of frozen foods, control seasonal inventory, and provide a variety of frozen food products such as vegetables, fruits, meat, seafood, prepared meals, and ice cream that consumers have been enjoying due to their convenience and year-round availability. Frozen storage stores the products at temperatures between -10F and -20F (-23C and -29C) to preserve frozen vegetables, fish, meat, seafood, ice cream, frozen prepared meals, and other items that demand sub-zero conditions to prevent any bacterial growth or enzymatic activity, keeping the product in texture and nutritional state and enabling the frozen products to last a few months or even years rather than days or weeks when other products are kept in refrigeration.

The increasing preference for frozen foods motivated by convenience, extended shelf life, less food waste, variety of products, and enhanced quality perceptions as food technologies due to flash-freezing allow the preservation of flavor and nutrition is generating a persistent need for frozen storage capacity to support retail frozen food sales and distribution of food services and provision of ingredients to food producers using frozen foods. Frozen goods that are imported and exported such as seafood, Midwest processing plants and plants in agricultural regions, meat, and other specialty items that are traded internationally demand frozen storage facilities in ports, distribution centers and staging facilities that support import/export operations, customs processing and domestic distribution that provide geographic diversity in frozen storage demand. Agricultural products that are harvested in certain seasons and consumed all year round are practiced in frozen storage to manage inventory in seasons but processing at optimal levels and then freezing preserves their quality, and they are stored all year and then released to the market to provide a consistent supply without changes in the production cycle depending on the season, reducing fluctuation in prices.

The chilled storage market is undergoing consistent growth to support fresh produce delivery, store dairy products, fresh meat, and poultry prior to processing or retail sale, prepared salads and meal kits that need refrigeration but not freezing, and pharmaceutical goods that require 2°C to 8°C storage, with this segment enjoying consumer preference of fresh against frozen products in some segments and retail trends of expanded fresh food offerings.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 51.52 billion |

| Projected Market Size in 2035 | USD 127.72 billion |

| Market Size in 2025 | USD 46.28 billion |

| CAGR Growth Rate | 10.66% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Warehouse Type, Construction Type, Temperature Type, Application and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Economic Impact Analysis

How Significant is the Industry’s Economic Contribution?

The US cold storage industry is a strong economic industry with a value of USD 46.28 billion in 2025, and USD 127.72 billion in 2035, thus exhibiting strong growth that facilitates food distribution networks, pharmaceutical supply chains, and global trade activities by enabling workforces in warehouse activities, movement, maintenance, and administrative operations throughout the temperature-controlled logistics systems. Major cold storage operators such as Lineage Logistics and Americold have already increased capacity by over 18 million square feet since 2019, which is a capital investment of billions of dollars in land purchase, facility building, refrigeration and automation, and technological infrastructure to support the modern cold chain operation of its domestic and international markets. Cold storage businesses directly employ warehouse workers, forklift operators, inventory managers, quality assurance people, maintenance technicians and administrative staff, with the Agile Cold Storage 200,000 square foot Joliet facility providing many jobs to the surrounding population showing job creation effects especially in areas where cold storage companies are developing around food production areas, ports, or large population centers.

The indirect economic effects spread across the supply chains, cold storage facilities buy electricity, refrigeration equipment, building materials, automation technologies, and services of professionals in engineering, environmental compliance, and information technology, which has multiplier effects that create jobs and economic activity in several industries other than direct warehouse activities. Benefits of the cold storage market to food security.

The cold storage market helps maintain food security through the availability of perishable goods all year round, through minimizing post-harvest losses due to inadequate preservation, through international trade to market goods sensitive to temperature fluctuations, and through providing buffer capacity to prevent supply shock caused by weather conditions, transportation delays, and production issues that may result in shortages or spikes in food supplies to consumers. Cold storage facilities provide property tax revenues to local governments to budget for schools, infrastructure, and other government services, and facilities usually reflect large property values, generating large tax revenues, and employment provides wage income to local economies through worker spending in retail stores, restaurants, residential buildings, and services.

What is the Industry’s Infrastructure Investment and Technology Development?

Cold storage business exhibits a high level of infrastructure capital where market players have invested billions of dollars on building facilities, capacity building, automation, and technology upgrades to meet an ever-increasing demand of e-commerce, pharmaceutical distribution, food industry consolidation, and consumer preference of fresh and frozen goods that receive temperature-controlled warehousing across supply chains.

The CBRE forecasts of 100 million square feet of new cold storage in the country in 5 years are an indication of unprecedented growth in the industry and this development is bound to incur capital investments of USD 10-20 billion based on the estimated building cost of USD 100-200/per square foot for building refrigerator warehouses including specialized refrigeration systems, building insulation, loading infrastructure, and automation equipment that is very high in comparison with the traditional warehouse construction costs.

AS/RS systems, autonomous vehicles, robotic palletizers, and AI software platform investments are major expenditures with capital investments of USD 10-50 million individually based on the size of the facility and automation level, and the payback of these investments is generated by labor savings, productivity gains, space savings and operational efficiencies in 5-7 years of payback. The upgrades on energy efficiency, such as LED lighting, natural refrigerants, building envelopes, solar installations, and waste heat recovery systems demand a high initial cost bearing savings in the form of lower electricity usage, better equipment durability, longer equipment shelf life, regulatory compliance, and achievement of corporate sustainability goals, supporting environmental commitments and management of operational costs.

The consolidation of activities as noted by Lineage Logistics purchasing the cold storage assets of Tyson Foods in April 2025 of USD 247 million, is an indication of industry maturity, with the major players seeking to grow by getting access to existing customer relationships, geographic growth, immediate capacity additions and operational synergies available to justify higher valuations, and concentrate market consolidation trends into fewer operators with the capital resources to support further growth.

Top Players in the Market

- Lineage Logistics Holdings LLC

- Americold Realty Trust Inc.

- S. Cold Storage Inc.

- Agro Merchants Group LLC

- Cloverleaf Cold Storage Company

- Kloosterboer USA

- VersaCold Logistics Services

- NewCold Advanced Cold Logistics

- Burris Logistics

- Interstate Cold Storage Inc.

- Others

Key Developments

The market has experienced a lot of developments as the players in the industry strive to increase its capabilities and improve on service offerings.

- In October 2025: Tjoapack is expanding on its sterile packaging and cold chain storage infrastructure in the United States and Europe and have invested in infrastructure at its United States plant in Clinton, New York, including a high speed vial packaging line that is completely automated and has an annual capacity of up to 20 million units, as examples of automation in pharmaceutical cold storage.

- In April 2025: Lineage Logistics, the largest cold storage company in the US and overall market, declared it would acquire and assume the business of four current cold storage warehouses with a combined cumulative capacity of about 49 million cubic feet and other assets of Tyson Foods, indicating the strategies of industry consolidation and expansion of capacity.

- In March 2025: Agile Cold Storage in Georgia held the opening of the first facility in Joliet, Illinois, this multi-temperature semi-automated facility, more than 200,000 square feet, offered a variety of value-added services, including case picking, blast freezing, and tempering services, controlled with automated systems.

These strategic actions have enabled the firms to consolidate the market base, increase the geographical reach, and seize technological advances and growth opportunities in the fast-growing market.

The US Cold Storage Market is segmented as follows:

By Warehouse Type

- Private and Semi-Private Warehouses

- Public Warehouses

By Construction Type

- Bulk Storage

- Production Stores

- Ports

By Temperature Type

- Chilled (Above 0°C)

- Frozen (-18°C to -25°C)

By Application

- Food and Beverages

- Fruits and Vegetables

- Meat and Poultry

- Seafood

- Dairy Products

- Frozen Foods

- Bakery Products

- Pharmaceuticals

- Vaccines

- Biologics

- Blood Products

- Chemicals

- Other Applications

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. US Cold Storage by Segments

- 2.1.2. US Cold Storage by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. US Cold Storage Market Attractiveness Analysis, By Warehouse Type

- 2.2.3. US Cold Storage Market Attractiveness Analysis, By Construction Type

- 2.2.4. US Cold Storage Market Attractiveness Analysis, By Temperature Type

- 2.2.5. US Cold Storage Market Attractiveness Analysis, By Application

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Explosive E-Commerce Grocery Growth and Last-Mile Delivery Transformation

- 3.1.2. Escalating Food Waste Crisis and Cold Chain Infrastructure Imperative

- 3.1.3. Pharmaceutical Cold Chain Revolution Driven by Biologics and Vaccine Distribution

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. US Cold Storage Market – By Warehouse Type

- 4.1. Warehouse Type Market Overview, By Warehouse Type Segment

- 4.1.1. US Cold Storage Market Revenue Share, By Warehouse Type, 2025 & 2035

- 4.1.2. Private and Semi-Private Warehouses

- 4.1.3. US Cold Storage Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Public Warehouses

- 4.1.7. US Cold Storage Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Warehouse Type Market Overview, By Warehouse Type Segment

- Chapter 5. US Cold Storage Market – By Construction Type

- 5.1. Construction Type Market Overview, By Construction Type Segment

- 5.1.1. US Cold Storage Market Revenue Share, By Construction Type, 2025 & 2035

- 5.1.2. Bulk Storage

- 5.1.3. US Cold Storage Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Production Stores

- 5.1.7. US Cold Storage Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Ports

- 5.1.11. US Cold Storage Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Construction Type Market Overview, By Construction Type Segment

- Chapter 6. US Cold Storage Market – By Temperature Type

- 6.1. Temperature Type Market Overview, By Temperature Type Segment

- 6.1.1. US Cold Storage Market Revenue Share, By Temperature Type, 2025 & 2035

- 6.1.2. Chilled (Above 0°C)

- 6.1.3. US Cold Storage Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Frozen (-18°C to -25°C)

- 6.1.7. US Cold Storage Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Temperature Type Market Overview, By Temperature Type Segment

- Chapter 7. US Cold Storage Market – By Application

- 7.1. Application Market Overview, By Application Segment

- 7.1.1. US Cold Storage Market Revenue Share, By Application, 2025 & 2035

- 7.1.2. Food and Beverages

- 7.1.3. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Fruits and Vegetables

- 7.1.7. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Meat and Poultry

- 7.1.11. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Seafood

- 7.1.15. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Dairy Products

- 7.1.19. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Frozen Foods

- 7.1.23. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1.26. Bakery Products

- 7.1.27. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.29. Key Market Trends, Growth Factors, & Opportunities

- 7.1.30. Pharmaceuticals

- 7.1.31. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.33. Key Market Trends, Growth Factors, & Opportunities

- 7.1.34. Vaccines

- 7.1.35. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.36. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.37. Key Market Trends, Growth Factors, & Opportunities

- 7.1.38. Biologics

- 7.1.39. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.40. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.41. Key Market Trends, Growth Factors, & Opportunities

- 7.1.42. Blood Products

- 7.1.43. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.44. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.45. Key Market Trends, Growth Factors, & Opportunities

- 7.1.46. Chemicals

- 7.1.47. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.48. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.49. Key Market Trends, Growth Factors, & Opportunities

- 7.1.50. Other Applications

- 7.1.51. US Cold Storage Share Forecast, By Region (USD Billion)

- 7.1.52. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.53. Key Market Trends, Growth Factors, & Opportunities

- US Cold Storage Market – Regional Analysis

- 7.2. US Cold Storage Market Overview, By Region Segment

- 7.2.1. US Cold Storage Market Revenue Share, By Region, 2025 & 2035

- 7.2.2. US Cold Storage Market Revenue, By Region, 2025 – 2035 (USD Billion)

- 7.2.3. US Cold Storage Market Revenue, By Warehouse Type, 2025 – 2035

- 7.2.4. US Cold Storage Market Revenue, By Construction Type, 2025 – 2035

- 7.2.5. US Cold Storage Market Revenue, By Temperature Type, 2025 – 2035

- 7.2.6. US Cold Storage Market Revenue, By Application, 2025 – 2035

- 7.1. Application Market Overview, By Application Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. US Cold Storage Market: Company Market Share, 2025

- 8.2. US Cold Storage Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. Lineage Logistics Holdings LLC

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Americold Realty Trust Inc.

- 9.3. U.S. Cold Storage Inc.

- 9.4. Agro Merchants Group LLC

- 9.5. Cloverleaf Cold Storage Company

- 9.6. Kloosterboer USA

- 9.7. VersaCold Logistics Services

- 9.8. NewCold Advanced Cold Logistics

- 9.9. Burris Logistics

- 9.10. Interstate Cold Storage Inc.

- 9.11. Others.

- 9.1. Lineage Logistics Holdings LLC

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Custom Market Insights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

List Of Figures

Figures No 1 to 33

List Of Tables

Tables No 1 to 2

FAQs

The key players in the market are Lineage Logistics Holdings LLC, Americold Realty Trust Inc., U.S. Cold Storage Inc., Agro Merchants Group LLC, Cloverleaf Cold Storage Company, Kloosterboer USA, VersaCold Logistics Services, NewCold Advanced Cold Logistics, Burris Logistics, Interstate Cold Storage Inc., Others.

Regulatory frameworks have a major impact on the cold storage market, with the FDA Food Safety Modernization Act requiring preventive measures and monitoring temperatures in food facilities, USDA inspections required on meat and poultry storage facilities, state and local health codes requiring refrigeration standards and sanitation practices and environmental regulations requiring refrigerant phase-outs and emissions and building codes stipulating insulation requirements, fire prevention systems and structural standards of refrigerated warehouses. The FDA has added some additional regulations on pharmaceutical cold storage that need to include validated temperature control, chain of custody records, alternate power, and GMP compliance that safeguard product integrity. Compliance regulations can demand expensive investments in monitoring and employee education, record keeping technology, and facility improvements, as well as provide obstacles to the market entry of new market entrants who do not have the regulatory knowledge and capital base to meet compliance needs.

Energy use contributes greatly to cold storage profitability and competitiveness with electricity taking up 50-70% of operating expense making energy efficiency a business priority thus investment in LED lighting which reduces energy use by 50-70%, natural refrigerants which enhance thermodynamic performance, variable frequency drives, which adjust equipment operation and minimize energy use by 20-40%, solar panel installations which also generate power on site, building envelope buildings which reduce cooling needs, and waste heat recovery which takes refrigeration by product and converts them to valuable resource. The energy management strategies allow the operators to save on expenses, enhance their sustainability performance, fulfill their corporate environmental commitments and remain competitive in a market where customers are more than ever demanding cost-effective solutions.

According to the current analysis, the US cold storage market is expected to be estimated at USD 127.72 billion by 2035 and is projected to grow at a CAGR of 10.66% between 2026 and 2035, as a result of the transformation in the e-commerce grocery chains requiring the establishment of urban micro-fulfillment centers, food waste management initiatives necessitating a better supply chain of preservation systems, the expansion of pharmaceutical cold chains to support biologics distribution, automation to enhance operational efficiency, geographic expansion in high-growth regions including Florida and California, energy efficiency investments reducing operating costs, and multi-temperature facility development supporting diverse customer requirements.

Refrigeration warehouses will continue to dominate the industry with about 59.3% market share attributed to the dominance of centralized storage needs that guarantee the same temperature level between production and distribution, professional management that makes sure that food safety is being followed, economies of scale that prevail based on better energy consumption per cubic foot, specialized infrastructure that is suited to perishable product handling, and food safety issues that demand the presence of reliable cold storage that will enhance longer shelf lives and guarantee that all standards of product quality will be maintained in the supply chains that serve the needs of retailers, foodservice establishments, and consumers.

The fastest growing is the pharmaceuticals segment with the projected CAGR of 13.82% between 2026 and 2035 due to growing biologics and cell and gene therapy pipelines that require ultra-low temperature storage at -80°C to -196°C, the growth in vaccine distribution needs due to COVID-19 investment in infrastructure, increasing demand on pharmaceutical outsourcing to specialized third-party providers with validated 2°C to 8°C storage requirements, and the rise in the requirement to safeguard high-value pharmaceutical investments across supply chains where temperature excursions could destroy batches valued at millions of dollars.

It is expected that the US Cold Storage Market will grow massively because of the e-commerce groceries that are growing exponentially, with online sales expected to hit USD 9.8 billion each month, which is a 15% increase over the years, and penetration expected to rise to 20% by 2025; the crisis in food waste, which is expected to reach USD 30-40 billion of food waste annually, and infrastructure imperative, the revolution in pharmaceutical cold chains with the biologics and cell therapy market to reach USD 3.9 billion, heavy adoption addressing labor shortages, stringent food safety regulations mandating temperature control, and sustainable refrigeration technologies reducing operating costs representing 50-70% of warehouse expenses.