US Biostimulants Market Size, Trends and Insights By Active Ingredient (Acid-Based (Humic Acid, Fulvic Acid), Seaweed Extracts, Protein Hydrolysates , Microbial Amendments, Amino Acids, Other Ingredients), By Application (Foliar Treatment, Soil Treatment, Seed Treatment), By Form (Liquid, Dry/Powder), By Crop Type (Row Crops (Corn, Soybeans, Wheat), Horticultural Crops (Fruits, Vegetables), Turf & Ornamentals), By End User (Farmers, Agricultural Distributors, Commercial Growers), and By Region - Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 7.6%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | USA |

| Largest Market: | USA |

Major Players

- BASF SE

- Bayer AG

- Syngenta

- UPL Limited

- Others

Reports Description

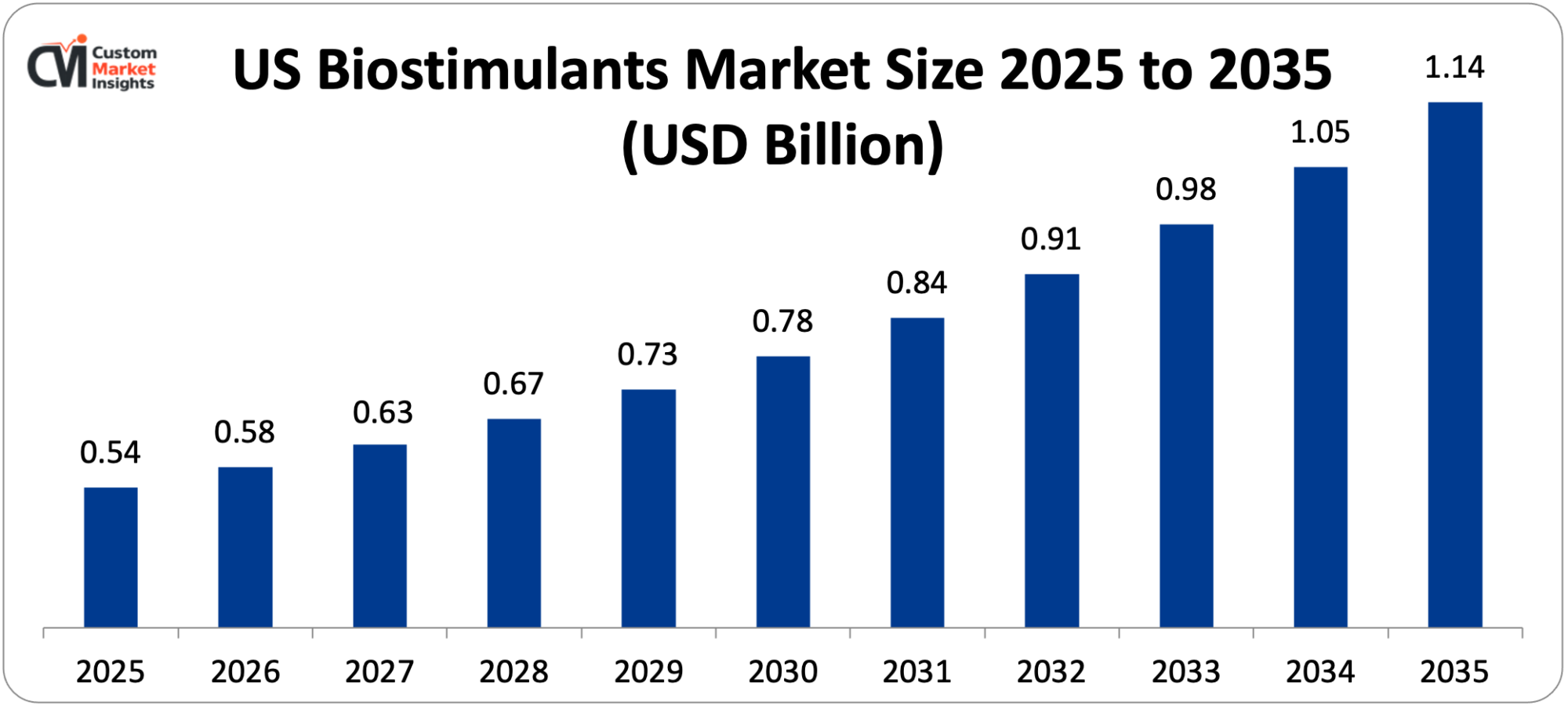

The market size of US biostimulants is estimated at USD 0.54 billion in 2025 and is forecasted to grow to between USD 0.58 billion in 2026 and USD 1.14 billion in 2035 at a CAGR of 7.6% between the years 2026 and 2035.

The market is expanding due to the rising demand for sustainable agricultural practices, the increase in organic farming acreage reaching 5.6 million acres in 2024, the federal cost-share incentive through the USDA Climate-Smart Commodities Initiative of up to 75% of the application cost, the growing demand for residue-free produce by retailers, technological progress in system formulation and delivery systems, and the evidence linking biostimulants with yield stability.

Market Highlight

- The US is estimated to have 17.0% market share of worldwide biostimulants in 2025 which is the second largest market in the world after Europe.

- By active ingredient, acid-based biostimulants will have a revenue share of 49.86% in 2025, whereas seaweed extracts will have the highest growth in the same period of the forecast.

- Through application, foliar treatment had 71.2% market share in 2024 as it gets absorbed quickly through the leaves.

- By type of crop, the market share of row crops in 2025 was 70.95%, whereas the market share of horticultural crops was 13.74% CAGR in 2031.

- Certified organic farmland grew 2.7% in 2024 to 5.6 million acres after the imposition of synthetic input limits by the USDA National Organic Program.

- The US market had protein hydrolysates that commanded the largest revenue share, 37.05% in 2025 based on the ability to develop yield and quality characteristics in farm crops.

Significant Growth Factors

The US Biostimulants Market Trends present significant growth opportunities due to several factors:

- Sustainable Agriculture Transition and Organic Farming Expansion:

The underlying trend of sustainable agricultural production is the key driving factor behind the US biostimulants business, as farmers are growing more interested in using biological inputs in their production that would reduce their reliance on synthetic chemical fertilizers and pesticides and promote healthy soil, increase nutrient efficacy, and provide crop resistance to environmental stresses in line with consumer demands of sustainably produced foods and corporate sustainability requirements. In 2024, the USDA National Organic Program increased certification of organic farmland from 2.7 to 5.6 million acres as synthetic input restrictions are tightened and non-synthetic amino-acid biostimulants are ruled to retain organic eligibility eliminating regulatory ambiguity and attracting quicker conversion into organic operations in search of inputs that can be used synthetically without violating organic eligibility criteria and remain essential to organic eligibility as needed for premium prices.

In 2024, organic price premiums were at USD 0.40 per pound on corn and USD 2.10 per pound on soybeans which comprised a 15-30% cost premium of biological inputs such as biostimulants and allowed farmers to capture values of environmentally conscious consumers who were willing to pay premiums on certified organic products. California has the highest rate of growth in organic acreage at 1.1 million and the USDA Organic Transition Initiative gives USD 300 million in 2027 to offset the cost of transition-period and when farmers switch to an organic system they have to endure reduced yield and complex management systems till they are certified and attract higher prices, biostimulants are the tools that sustain productivity throughout the conversion period when transition is needed.

The rising consumer consciousness on the environmental effects of traditional farming is fueling the demand of sustainably produced foodstuff, as surveys have shown that more than 70% of consumers would choose to buy food produced through sustainably sourced farming techniques, which creates market push all along the supply chain, as retailers, food manufacturers and restaurants chain set sustainability sourcing policies requiring suppliers to adopt practices such as the use of biostimulants that minimize the use of synthetic chemicals. Federal and state programs such as the USDA Climate-Smart Commodities Partnership program that provides significant funding to support the adoption of climate-friendly farming practices offset up to 75% of the application expenses of biostimulants used in the field, which radically changes the economics and provides data to prove that the practice has benefits for the environment such as decreased greenhouse gas emissions, increased carbon sequestration, and improved water quality that help to develop policy and expand programs. There are new revenue streams in the agricultural sustainability certifications and carbon credit programs and new carbon markets with soil carbon sequestration credits where biostimulants enhancing root development and soil organic matter help yield a set of payments to supplement farm income to help encourage the adoption of sustainable inputs.

- Climate Resilience and Abiotic Stress Management:

The growing intensity and frequency of weather extremes such as drought, heat stress, flooding, and changes in temperature demand assistance in agricultural inputs that increase crop resistance, biostimulants have been shown to have proven effectiveness in increasing tolerance to abiotic stresses in plants by a variety of reactions including bolstering antioxidant systems, water use efficiency, nutrient uptake under stressful environments, and post-stress recovery.

The effects of climate change on agriculture are increasing with the rise in temperature, changing patterns of precipitations and extreme weather occurrence which is expected to result in further warming posing a challenge to the conventional crop production system and necessitating adaptation measures in which biostimulants can be considered as viable means farmers can use to handle the challenge of production risks caused by climate change whilst retaining output and profitability. Drought is an especially important issue throughout large agricultural areas, as the lack of water constrains the access to the irrigation system even in previously well-endowed areas, and the use of biostimulants enhancing the efficiency of water use by improving root development, more efficient stomata, and higher drought tolerance are the key factors that allow crops to remain productive in water-stressed conditions and ensure production sustainability in water-restricted regions.

Heat stress at key stages of reproductive development may significantly decrease the yields of several important crops such as corn and soybeans and biostimulants that include certain compounds such as amino acids and seaweed extracts have shown the potential to alleviate heat stress by protecting the cellular structures and sustaining photosynthetic activity and pollen viability amid heat stress that is becoming increasingly frequent during the growing periods in the US agricultural regions. The efficiency in nutrient use benefits that biostimulants offer are especially useful under stress-induced situations where nutrient absorption and utilization are impaired and nutrient solubility as a result of biostimulants elevates the growth of roots, activates useful microorganisms in the soil and contributes to the growth of crops in declining environments where environmental conditions inhibit the efficacy of conventional fertility programs. Combined stress management strategies that integrate biostimulants with precision agriculture technologies such as soil moisture sensors, weather services, and variable rate application can be used to implement targeted interventions maximizing benefits and reducing costs through maximizing the right time and place by digital technology which may provide decision support, linking field level measurements to product suggestions on the choice of biostimulant and application response depending on individual crop needs and stress conditions.

What are the Major Advances Changing the US Biostimulants Market Today?

- Advanced Formulation Technologies and Multi-Ingredient Synergies:

The technological change from simple single-ingredient products to complex multi-component formulations exemplifies a big technological change of the manufacturers that produce synergistic blends of amino acids, humic substances, seaweed extracts, and beneficial microorganisms that provide a better performance due to multiple modes of action that can be coordinated to act in a complementary way, i.e. Multi-action. Current biostimulant formulations take advantage of scientific knowledge of plant stress physiology, root-soil relationships, and microbial ecology to develop accurate formulae to fit a particular agricultural problem, and development programs develop ingredient combinations by research through controlled trials and field validation establishing efficacy claims to support marketing position and adoption by farmers. Long-lasting biostimulant release technologies enhance efficiency by reducing frequency of application and increasing duration of activity of nutrient and bioactive compounds by using encapsulation, granulation, and polymer coating technologies that allow gradual release of the compound to mimic patterns of plant uptake and minimizing losses through leaching or degradation of water-soluble formulations through longer-acting release systems.

The compatibility enhancements that allow biostimulant tank-mixing with fertilizers, pesticides, and other crop inputs without chemical breakdown or physical segregation lead to lower application costs due to consolidated field activities as well as enhanced adoption by being seamlessly integrated into the existing agronomic programs instead of treating biostimulants as special applications which raise application costs and may cause cost-sensitive farmers to shy away. Application-related formulation advancements such as foaming, nozzle plugging, and spray drift improve the user experience and boost field performance and technical service enhances the maximization of application parameters such as timing, carrier volumes, and environmental conditions to maximize product performance without application errors that can limit performance and erode the confidence of the farmer in using biological technologies. The incorporation of surfactants, pH regulating agents and anti-foaming agents in formulations enhances foliar uptake, spray coverage and tank stability of products that have a user-friendly aspect that works in a variety of application scenarios from ground boom sprayers to aerial application and preserves the biological activity of living organisms or complex organic molecules that might otherwise be destroyed by severe chemical conditions or improper handling.

- Microbial Consortium Development and Soil Health Focus:

The development of microbial biostimulant technologies that utilize specific bacterial and fungal species that offer many plant benefits such as N fixation, phosphorous solubilization, growth hormone production and disease suppressions are rapidly expanding segments that are expected to have the highest CAGR in the foreseeable future due to the focus on soil health and knowledge of plant-microbe symbioses. Nutrient acquisition, water uptake, and stress-tolerance-enhancing beneficial relationships between plant growth-promoting rhizobacteria and mycorrhizal fungi colonizing root systems, and commercial products provide a proven strain of rhizobacteria and mycorrhizal fungi that has shown consistent field efficacy across a wide range of soils, cropping systems and environmental conditions.

The soil health movement that focuses on biological activity, building of organic matter and cycles of nutrients gives good ground to the microbial biostimulant supporting regenerative agriculture ideals, wherein increasing the diversity and functionality of the soil microbiome is the basis of sustainable production and lessening dependence on external inputs and increasing resiliency to environmental changes and economic instability. Multi-strain consortia of complementary microbial species show improved functionality over any single strain product in terms of functional diversity, where multiple organisms respond to different needs of the plant or environmental conditions, and well-selected microbial communities show synergistic interaction with improved colonization, persistence, and overall efficacy when used compared to single strain uses.

The challenges of scaling up in production such as viability during production, formulation, storage, and use in the field have been solved with the development of better fermentation technology, advanced protective carrier technology, and formulation science that allows the production of commercially viable microbial products that have a long shelf life and field activity that satisfies farmers at an affordable cost compared to synthetic products. Collaborations between agricultural firms, higher education institutions, and government research laboratories have been used to expedite the discovery of microbial biostimulants by using highly developed screening regimens to select promising microbes, genomic characterization to understand how they work, field experiments to validate efficacy, and regulatory pathways to support innovations by ensuring environmental safety and efficacy of the product.

- Precision Application Technologies and Digital Integration:

Combining biostimulants with precision agricultural technologies such as GPS-controlled application, variable rate controllers, sensor-based monitoring systems, and data analytics applications optimize product deployment to crop areas based on the specific field area, growth status or stress conditions require benefits to outweigh costs by applying products precisely and at the appropriate time in place of blanket applications which waste product on areas that have a limited response potential. Digital advisory systems that include weather data, soil analytics, satellite imagery, and crop modelling deliver decision support based on what the algorithms are capable of computing via myriads of data streams that prescribe optimal application timing and rate of biostimulants depending on specific conditions of the field, the soil, and previous management history, which offer greater returns on investment than blanket prescriptions that do not take into account local environmental conditions, soil, and past management history. Variable rate application technology allows setting of biostimulant rates per field based on yield potential, soil characteristics or stress sensors, and controllers can automatically adjust application rates in real-time based on prescription maps or sensor feeds ensuring the correct distribution of products with regard to spatial variability within fields to maximize benefits and contain input costs that are especially relevant in the face of expensive biological products that need economically justified application.

Drone and robot application systems have spot treatment-specific delivery capabilities, high-density canopies, and inaccessible locations that the conventional ground equipment would need a great deal of time to reach, with unmanned aerial vehicles being able to be deployed across large acreage nearly instantly and being able to be highly flexible in responding to arising stress situations or responding to short time windows when soil conditions are unfavorable to the use of more conventional equipment. Smartphone applications that link farmers to manufacturers, agronomists and research tools are useful in the transfer of knowledge, technical assistance and performance monitoring, whereby databases of application dates, rates, weather conditions and crop responses are documented to promote continuous improvement and the realization of product value necessary to justify premium prices and promote purchasing again in a competitive market environment.

- Retailer Requirements and Premium Market Access:

The increasing retailer and processor demands of residue-free produce or certified sustainable production practices provide a high market push of biostimulants, and the high level of market demand of major food companies and grocery chains is to set biological programs and establish supplier standards to support valuable contract relationships. Fresh produce distributors report that crops sprayed with biostimulants are found to have 23 times lower residue detection rates and extended shelf life reducing after harvest losses, and these quality benefits are especially important to specialty crops of high value where appearance, shelf life and food safety directly correlate with marketability and premium prices paid to growers compared to conventional growers restricted by residue limits and inaccessible to high-value markets. In addition to the higher pricing, secure contracts will enable growers to have terms of better financing and have the stability of long-term planning that facilitates future investment in biological inputs, where markets can be confident enough to spend money on the products to improve quality and sustainability without having to worry much about the risks of price fluctuations which will make the premium inputs economically unsustainable.

California is the pioneer in the implementation of the residue reduction requirements: organic production has attained 1.1 million acres, and the conventional growers serving in retail contracts have adopted the biological programs with high standards of testing, as other states progressively move in the same direction with food safety concerns, environmental regulations, and market preferences contributing to the transformation of the industry to less chemical dependency where the biostimulants are essential tools in the production process and where they meet the stringent requirements of the regulatory and market factors. Independent testing that gives third-party confirmation of biostimulant activity and university validation programs fosters grower confidence and helps support marketing claims, and cooperative extension services undertaking replicated trials under a wide range of conditions generate unbiased information that shows that the technology is effective and justifies its adoption by risk-averse farmers who need credible evidence before they can make investments in new technologies, especially biological products where performance may depend on environmental conditions and application strategies require education and technical support to ensure success.

Category Wise Insights

By Active Ingredient

Why Acid-Based Leads While Seaweed Shows Fastest Growth?

The highest revenue share of 49.86 was obtained by acid-based biostimulants in 2025, and the humic and fulvic acids were the most popular because of their demonstrated benefits of improving soil structure, enhancing nutrient availability, root growth, and water retention, which were especially important in row crop systems, where the basis of soil health ensures a consistent yield despite changing weather conditions. Protein hydrolysates were the leaders in terms of share in revenue in select product categories, which were valued because they achieve agronomic objectives in building crop vigor, stimulation of nutrient uptake, and tolerance to environmental stresses, and growers have observed agronomic benefits in the growth of crops.

Seaweed extracts denote the emerging market segment with a broad range of positive effects on plant growth, stress tolerance and soil microbial processes and growing evidence of success in a wide range of crops and production systems with many researchers willing to find value in use beyond conventional purposes.

By Application

Why Foliar Treatment Dominates Market?

In 2024, foliar treatment controlled 71.2% of the market share and is projected to grow at a 10.4% CAGR with the dominance due to the rapid uptake of nutrients and bioactive substances via leaves and fast responses in plants, especially in times of stress or in correcting deficiencies where soil applications may not achieve sufficiently quick responses. Compared to other types of application methods, foliar treatments that are sprayed onto the leaf surface of plants can be effectively absorbed within a short time with minimal fixation of nutrients and biostimulants by soil or root-based blocking of leached nutrients and facilitated direct absorption of the treatment to any part of the plant where it is needed, as opposed to soil treatments, which may have little or no effect on plants because of fixation or root-related uptake restrictions. Foliar applications are used to meet nutrient requirements, enhance growth and increase stress resistance against abiotic stresses such as drought, heat, flooding and salinity that are posing more and more severe challenges to crop production in the US agricultural regions subjected to climate variability and the need to employ adaptive management equipment to maintain yields in the challenging conditions.

Seed treatment exhibits high growth potential as a viable and economical application technique that gives advantages of early season through coating the seeds with biostimulants before planting so that the young seedlings can gain the benefits of better germination and good root system growth and also tolerance to stress in adverse early establishment conditions that determine overall yield potential.

By Crop Type

Why Row Crops Lead While Horticulture Shows Fastest Growth?

In 2025, Row crops had a market share of 70.95%, indicating that the production of corn, soybean and wheat dominated the US agricultural landscape with expansive acreages, mechanization application capability, and federal subsidies in the form of crop insurance and commodity payments to make biostimulants a favourable choice for the major field crops that define the production of agriculture in the country and food security. The US biostimulant use in row crops is dominated by the north, with biostimulant application based on the cold resistance and nutrient efficiency of the crops during the shorter growing periods and the maximization of yield potential in the productive agricultural areas such as the Corn Belt states where intensive production systems and progressive farmer adoption of innovative technologies provide favorable environment for integrating the biological inputs.

Horticultural crops are estimated to increase at a 13.74% CAGR to 2031 due to the technologies of producing high-value, specialty crop production where the growers are willing to pay more input prices to secure better premium contracts, superior quality, and meet the stringent marketing demand, such as appearance, shelf life, sugar levels and post-harvest qualities, which are directly related to biostimulants in terms of their ability to improve fruit set, color intensification, increase sugar levels and lengthen post-harvest quality characteristics that directly influence marketability and the pricing.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 0.58 billion |

| Projected Market Size in 2035 | USD 1.14 billion |

| Market Size in 2025 | USD 0.54 billion |

| CAGR Growth Rate | 7.6% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Active Ingredient, Application, Form, Crop Type, End User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Top Market Players and Their Offerings

- BASF SE

- Bayer AG

- Syngenta

- UPL Limited

- Yara International

- FMC Corporation

- Novozymes

- Acadian Seaplants Limited

- Haifa Group

- Koppert Biological Systems

- Others

Key Developments

- In July 2025: Yara North America established a biostimulant demonstration farm in Saskatoon, highlighting sustainable crop solutions, assessing performance under practical conditions supporting regenerative agriculture practices.

- In April 2025: Bayer AG released the high-activity seaweed biostimulant product An Hai Long that deals with soil degradation, nutrient absorption barriers, and extreme climates.

- In May 2024: UPM Biochemicals opened a new product line of bio-based plant stimulants UPM Solargo™, and joined the venture in the agriculture industry.

The US Biostimulants Market is segmented as follows:

By Active Ingredient

- Acid-Based (Humic Acid, Fulvic Acid)

- Seaweed Extracts

- Protein Hydrolysates

- Microbial Amendments

- Amino Acids

- Other Ingredients

By Application

- Foliar Treatment

- Soil Treatment

- Seed Treatment

By Form

- Liquid

- Dry/Powder

By Crop Type

- Row Crops (Corn, Soybeans, Wheat)

- Horticultural Crops (Fruits, Vegetables)

- Turf & Ornamentals

By End User

- Farmers

- Agricultural Distributors

- Commercial Growers

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. US Biostimulants by Segments

- 2.1.2. US Biostimulants by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. US Biostimulants Market Attractiveness Analysis, By Active Ingredient

- 2.2.3. US Biostimulants Market Attractiveness Analysis, By Application

- 2.2.4. US Biostimulants Market Attractiveness Analysis, By Form

- 2.2.5. US Biostimulants Market Attractiveness Analysis, By Crop Type

- 2.2.6. US Biostimulants Market Attractiveness Analysis, By End User

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Sustainable Agriculture Transition and Organic Farming Expansion

- 3.1.2. Climate Resilience and Abiotic Stress Management

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. US Biostimulants Market – By Active Ingredient

- 4.1. Active Ingredient Market Overview, By Active Ingredient Segment

- 4.1.1. US Biostimulants Market Revenue Share, By Active Ingredient, 2025 & 2035

- 4.1.2. Acid-Based (Humic Acid, Fulvic Acid)

- 4.1.3. US Biostimulants Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Seaweed Extracts

- 4.1.7. US Biostimulants Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Protein Hydrolysates

- 4.1.11. US Biostimulants Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Microbial Amendments

- 4.1.15. US Biostimulants Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Amino Acids

- 4.1.19. US Biostimulants Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Other Ingredients

- 4.1.23. US Biostimulants Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Active Ingredient Market Overview, By Active Ingredient Segment

- Chapter 5. US Biostimulants Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. US Biostimulants Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Foliar Treatment

- 5.1.3. US Biostimulants Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Soil Treatment

- 5.1.7. US Biostimulants Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Seed Treatment

- 5.1.11. US Biostimulants Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. US Biostimulants Market – By Form

- 6.1. Form Market Overview, By Form Segment

- 6.1.1. US Biostimulants Market Revenue Share, By Form, 2025 & 2035

- 6.1.2. Liquid

- 6.1.3. US Biostimulants Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Dry/Powder

- 6.1.7. US Biostimulants Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Form Market Overview, By Form Segment

- Chapter 7. US Biostimulants Market – By Crop Type

- 7.1. Crop Type Market Overview, By Crop Type Segment

- 7.1.1. US Biostimulants Market Revenue Share, By Crop Type, 2025 & 2035

- 7.1.2. Row Crops (Corn, Soybeans, Wheat)

- 7.1.3. US Biostimulants Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Horticultural Crops (Fruits, Vegetables)

- 7.1.7. US Biostimulants Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Turf & Ornamentals

- 7.1.11. US Biostimulants Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Crop Type Market Overview, By Crop Type Segment

- Chapter 8. US Biostimulants Market – By End User

- 8.1. End User Market Overview, By End User Segment

- 8.1.1. US Biostimulants Market Revenue Share, By End User, 2025 & 2035

- 8.1.2. Farmers

- 8.1.3. US Biostimulants Share Forecast, By Region (USD Billion)

- 8.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.5. Key Market Trends, Growth Factors, & Opportunities

- 8.1.6. Agricultural Distributors

- 8.1.7. US Biostimulants Share Forecast, By Region (USD Billion)

- 8.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.9. Key Market Trends, Growth Factors, & Opportunities

- 8.1.10. Commercial Growers

- 8.1.11. US Biostimulants Share Forecast, By Region (USD Billion)

- 8.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.13. Key Market Trends, Growth Factors, & Opportunities

- 8.1. End User Market Overview, By End User Segment

- Chapter 9. US Biostimulants Market – Regional Analysis

- 9.1. US Biostimulants Market Overview, By Region Segment

- 9.1.1. US Biostimulants Market Revenue Share, By Region, 2025 & 2035

- 9.1.2. US Biostimulants Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 9.1.3. US Biostimulants Market Revenue, By Active Ingredient, 2026 – 2035

- 9.1.4. US Biostimulants Market Revenue, By Application, 2026 – 2035

- 9.1.5. US Biostimulants Market Revenue, By Form, 2026 – 2035

- 9.1.6. US Biostimulants Market Revenue, By Crop Type, 2026 – 2035

- 9.1.7. US Biostimulants Market Revenue, By End User, 2026 – 2035

- 9.1. US Biostimulants Market Overview, By Region Segment

- Chapter 10. Competitive Landscape

- 10.1. Company Market Share Analysis – 2025

- 10.1.1. US Biostimulants Market: Company Market Share, 2025

- 10.2. US Biostimulants Market Company Market Share, 2024

- 10.1. Company Market Share Analysis – 2025

- Chapter 11. Company Profiles

- 11.1. BASF SE

- 11.1.1. Company Overview

- 11.1.2. Key Executives

- 11.1.3. Product Portfolio

- 11.1.4. Financial Overview

- 11.1.5. Operating Business Segments

- 11.1.6. Business Performance

- 11.1.7. Recent Developments

- 11.2. Bayer AG

- 11.3. Syngenta

- 11.4. UPL Limited

- 11.5. Yara International

- 11.6. FMC Corporation

- 11.7. Novozymes

- 11.8. Acadian Seaplants Limited

- 11.9. Haifa Group

- 11.10. Koppert Biological Systems

- 11.11. Others.

- 11.1. BASF SE

- Chapter 12. Research Methodology

- 12.1. Research Methodology

- 12.2. Secondary Research

- 12.3. Primary Research

- 12.3.1. Analyst Tools and Models

- 12.4. Research Limitations

- 12.5. Assumptions

- 12.6. Insights From Primary Respondents

- 12.7. Why Custom Market Insights

- Chapter 13. Standard Report Commercials & Add-Ons

- 13.1. Customization Options

- 13.2. Subscription Module For Market Research Reports

- 13.3. Client Testimonials

List Of Figures

Figures No 1 to 32

List Of Tables

Tables No 1 to 2

FAQs

The key players in the market are BASF SE, Bayer AG, Syngenta, UPL Limited, Yara International, FMC Corporation, Novozymes, Acadian Seaplants Limited, Haifa Group, Koppert Biological Systems, Others.

Market regulatory schemes have substantial effects on the market of biostimulants (regulation), with the EPA oversight under a pesticide law in most states raising compliance expenses, the USDA National Organic Program defining eligibility as organic necessary to certify operations, the Association of American Plant Food Control Officials model law unevenly implemented across states resulting in complexity in compliance, and supportive policies, such as the USDA Climate-Smart Commodities funding, Regional Agricultural Promotion Program incentives, and a proposed Plant Biostimulant Act, to encourage sustainable agricultural practices. California will need multi-ingredient product registrations whereas Texas has single ingredient product registrations, representing regulatory differences manufacturers must consider when it comes to the cost of commercialization and the cost of market access schedules.

Pricing of biostimulants is very high and depends on the active ingredient and the complexity of the formulation and application rate, with a range of USD 5-20 per acre for simple products up to USD 50-100+ per acre for high quality formulations, although organic price premiums, federal cost-share reimbursement (up to 75% of costs), and premium market access subsidies offset costs. Although the initial costs have been more expensive than synthetic products, the market has been growing due to the proven value of stability of yields under stress of up to 5-15% on average, quality improvement that attracts price-value, fewer synthetic products required by the soil, health benefits of the soils, and the potential revenue in the form of carbon credits that support economic justification beyond direct yield.

This is projected to grow to about USD 1,135.8 million by 2033 with consistent growth due to organic farming growth, support programs by the federal government, the need to adapt to the climate, the sustainability of retailers, the development of the carbon market, the integration of precision agriculture, the future development of microbial technology, building farmer confidence through university validation programs, and the harmonization of regulations through EPA-USDA-FDA coordination to bring about better clarity in the market, with a CAGR of 7.6% between 2026 and 2033.

Horticultural crops will experience an increase of 13.74% CAGR through 2031 due to the production of high-value specialty crops (where the growers receive higher input costs on the premium contracts) and the resulting high quality that meets market standards, lack of residues (where fresh produce is required), and post-harvest quality enhancement (23% better shelf life is reducing losses). Fruits, vegetables, and other specialty crops that are used have a premium rate that justifies the use of biological inputs that have the ability to provide quantifiable quality improvement.

Seaweed extracts: Fastest-growing category due to various positive effects of multiple compounds in the extract, such as plant hormones, trace minerals, and complex carbohydrates, which reduce global seaweed production by supplying it, proven benefits to improve soil fertility and crop yield, and research demonstrating its efficacy against various crops. Microbial amendments with the largest CAGR are expected due to the focus on soil health, the adoption of regenerative agriculture, and the knowledge of the positive relationships between plants and microbes.

The US Biostimulants Market is growing steadily as there is sustained growth in the agricultural sector, which is transitioning to sustainable agriculture with over 5.6 million acres of corn and soybean farms as organic farms in 2024, federal cost-share assistance through the USDA programs that reimburse up to 75% of the application expenses, organic price premiums of USD 0.40/lb on corn and USD 2.10/lb on soybean where 15-30% of the input cost premium is covered, retailer requirements based on residue-free produce with biostimulant-treated crops showing 23% lower residue detection, climate resilience needs addressing drought and heat stress, the USDA Organic Transition Initiative allocating USD 300 million through 2027, emerging carbon credit programs rewarding soil health practices, and technological advancements in formulation and precision application optimizing product deployment and return on investment.