Butyl Rubber Market Size, Trends and Insights By Type (Regular Butyl Rubber (IIR), Chlorobutyl Rubber (CIIR), Bromobutyl Rubber (BIIR), Partially Cross-linked Butyl Rubber, Other Types), By Grade (Industrial Grade, Pharmaceutical Grade, Specialty/High-Performance Grade), By Application (Tire & Automotive (Inner Liners, Innertubes, Vibration Dampeners, Seals), Pharmaceutical Packaging (Stoppers, Plungers, Septa), Construction & Sealants, Industrial (Hoses, Belts, Tank Linings, Chemical-Resistant Products), Other Applications), By End-Use (Automotive OEM, Replacement Tire Market, Healthcare & Pharmaceutical Manufacturers, Industrial End-Users, Others), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 5.6%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- ExxonMobil Chemical Company

- LANXESS AG

- Arlanxeo (Saudi Aramco / LANXESS JV)

- Nizhnekamskneftekhim PJSC (NKNK)

- Others

Reports Description

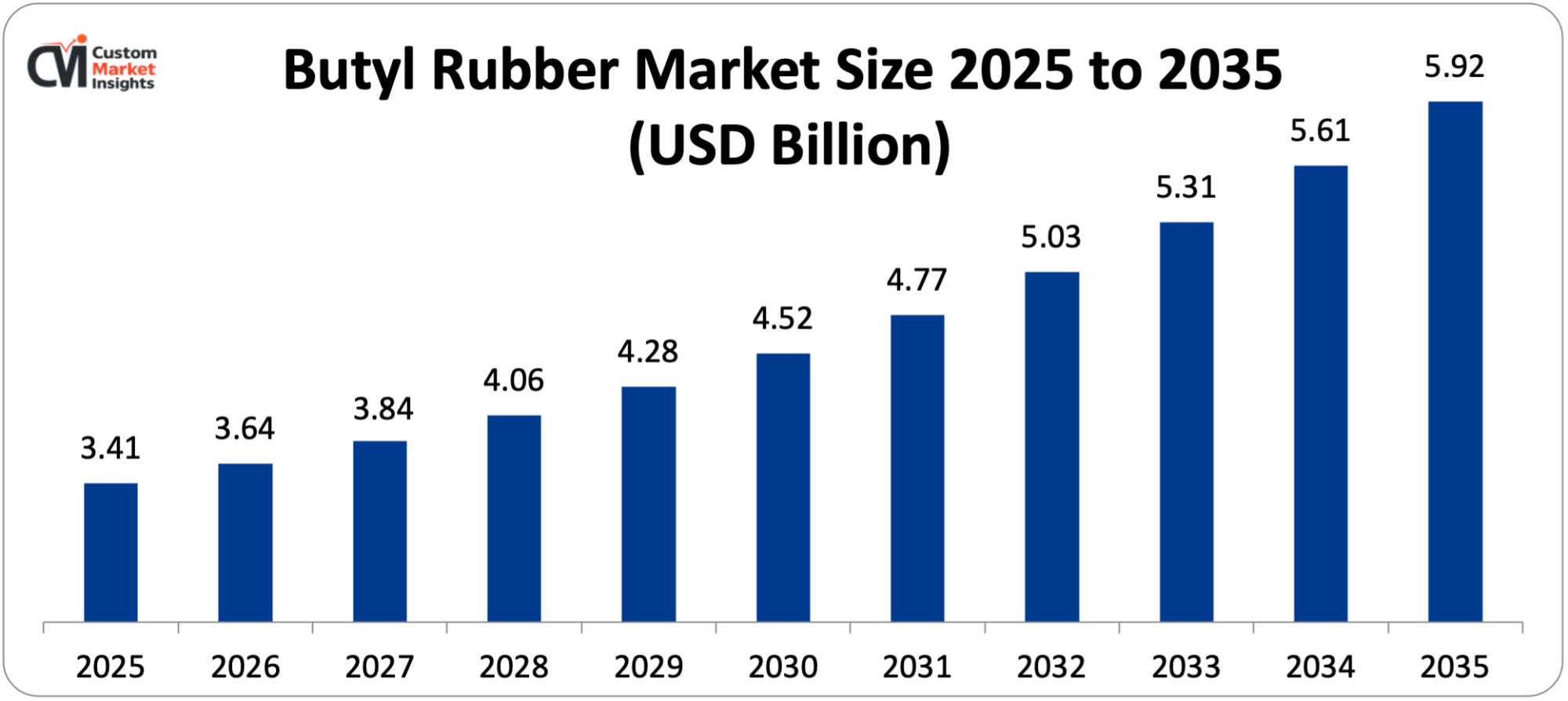

The size of the global butyl rubber market is estimated at USD 3.64 billion in 2026 and it will grow by 5.6% during the period of 2026 to 2035 to reach USD 5.92 billion. Market growth is motivated by increasing automotive industry demands for low-permeability, fuel saving tire components, the escalating pharmaceutical packaging requirements; the increased construction activities worldwide and the progress of halobutyl rubber formulations.

Market Highlight

- Asia Pacific is dominating the butyl rubber market with a 46% market share in 2025.

- North America will grow at a rate of CAGR 4.9% in the period 2026 to 2035.

- By type, the regular butyl rubber segment was found to have about 38% of the market share in 2025.

- By type, the bromobutyl rubber segment is increasing at the highest CAGR of 7.1% between 2026 and 2035.

- By application, the tire and automotive application had the largest market share of 54% in 2025, whereas the pharmaceutical application segment is likely to increase the CAGR at the highest rate of 8.3% during the forecast period of 2026 to 2035.

- By grade, industrial grade segment had 61% market share by the year 2025.

- Butyl rubber: in 2024, the company controlled over a quarter of the total market share of synthetic rubber at 28.4%.

Significant Growth Factors

The Butyl Rubber Market Trends present significant growth opportunities due to several factors:

- Rising Automotive Production and Fuel Efficiency Standards Globally: It is the unremitting quest of the global auto industry toward fuel efficiency and lower emissions, which is the major driving force behind the demand of butyl rubber, especially as both tire inner liner and innertube the material has unrivalled gas impermeability compared with any other commercial elastomer. The International Organization of Motor Vehicle Manufacturers (OICA) records that the world automobile manufacturing industry has already reached 93.5 million vehicles in the year 2024 and it is expected to exceed 100 million vehicles per annum by the year 2030 which is directly associated with the consumption of robust butyl rubber. Chlorobutyl rubber (including chlorobutyl and bromobutyl forms) is now a necessary production ingredient in the construction of tires of tubeless types, and an average passenger car tire inner liner uses about 800-1200 grams of halobutyl rubber. Butyl is used, and halobutyl is used in nearly 95% of the total number of tires made worldwide that use tubeless pneumatic tires. The regulatory forces, such as the compulsory CO₂ emissions of the European Union, 95 g/km, in passenger vehicles; the U.S. CAFE standards, which demand fleet averages of 49 mpg by 2026 are pushing the automakers to spend big on low rolling-resistance tire technologies that focus on the development of precision halobutyl inner liner formulations. The transition of radial tire manufacturing in the new markets, especially in India, Southeast Asia, and some parts of Africa, is increasing the radical change from tube-type to tubeless designs, with demand reaching significant incremental butyl rubber demand. Moreover, a rapidly rising electric vehicle (EV) influx (with the world EV sales expected to reach 14 million vehicles in 2023 and 40 million vehicles, according to the International Energy Agency (IEA)) is also intensifying butyl rubber use because EV tires come with a heavier vehicle weight, and more complex inner liner formulations are needed to be able to maintain the tire pressure at optimum levels over extended durations without driver intervention.

- Expanding Pharmaceutical Packaging Requirements and Healthcare Sector Growth: The use of Butyl rubber in pharmaceutical closures, vial stoppers, syringe plungers, and injectable drug packaging is a high-value, high-growth application segment based on the high regulatory standards and the increasing spending on healthcare worldwide. According to IQVIA data, the global pharmaceutical market is expected to increase at a CAGR of 6.5 to USD 2.3 trillion by 2030, and it currently has a value of USD 1.48 trillion in 2023. This growth is a direct catalyst to the need to utilize pharmaceutical grade bromobutyl and chlorobutyl rubber compounds that are more chemically inert, have low extractables and have excellent sterilization compatibility that is vital to drug packaging integrity. About 1216 billion pharmaceutical rubber stoppers are produced every year in the world market with half the market dominated by halobutyl rubber owing to its high performance over the natural rubber or other manmade alternatives. The COVID-19 pandemic visibly revealed the strategic significance of pharmaceutical rubber chains, and vaccine rollouts in 2021-2022 had devoured up to 23 billion rubber vial stoppers and syringe plungers around the world in just 18 months. The USP Class VI, ISO 8871, and EU GMP regulatory standards require the utilisation of pharmaceutical grade halobutyl rubber in the packaging of parenteral drugs, which establishes stiff barriers against other material substitutes. This has been driven by the constant growth of the biopharmaceutical industry with the global biologics market set to surpass USD 600 billion by 2030, which is creating premium demand in specialty butyl compounds that are designed to be compatible with protein-based drugs, monoclonal antibodies, and cell and gene therapies, which are particularly susceptible to container-closure interactions.

What are the Major Advances Changing the Butyl Rubber Market Today?

- Development of High-Performance Halobutyl Rubber Compounds for Next-Generation Tires: The most impactful technological breakthrough in the butyl rubber industry is the development of the halobutyl rubber formulations, which remain one of the technologies that allow a tire manufacturer to attain better rolling resistance, better air retention, and durability at the same time. Next-generation bromobutyls – especially those with polymer structures with functional branches and with controlled branching and narrow molecular weight distribution – provide inner liners that are 1015% thinner than traditional formulations and air impermeable at the same level or better and lower tire overall weight and fuel economy. Industry statistics suggest that a 10% decrease in tire rolling resistance boosts vehicle fuel consumption by about 112%, which means that over time, there would be a substantial CO₂ savings in the lifecycle of the automotive fleet. High-performance halobutyl compounds with reactive cure systems to improve adhesion to adjacent rubber components and minimize gauge variation are the Bromobutyl 2222 and 2030 series of ExxonMobil and the Baytubes series of LANXESS. The combination of these cutting-edge compounds with the state of the art tire erection materials has enabled tire fabricators to cut down on the total bulk of the inner liner by an average of 150-200 grams per passenger car tire, a major engineering breakthrough at annual production amounts of over 2 billion tires worldwide. Also, self-sealing tire technologies, whereby butyl rubber-based adhesive layers in the form of sealants are built into tire structures, are becoming commercially popular and the self-sealing tire market is predicted to increase at 9.2% CAGR up to 2030 as manufacturers aim to do away with spare tires and vehicle weight.

- Green and Bio-Based Butyl Rubber Research and Sustainability Initiatives: The growing demand associated with automotive OEM sustainability requirements, EU Circular Economy Action Plan requirements, and corporate ESG requirements are driving the current research on bio-based isobutylene feedstocks and more sustainable butyl rubber production processes. Conventional butyl making is based on isobutylene found in petroleum based C4 feeds in either steam cracking or refinery catalytic cracking – processes, both of which are linked to a high carbon footprint. The other companies working on research programs that explore fermentation-based bio-isobutylene routes are Lanxess, ExxonMobil, and Arlanxeo with Gevo and others proving the technical viability of the production of bio-isobutylene using sugars and lignocellulosic biomass feedstocks. The bio-based butyl rubber production routes, according to the life cycle analysis, have the potential to cut cradle-to-gate CO₂ emissions by 30–50% relative to petroleum-based production, which is of great interest to tire manufacturers with the aim of decarbonizing the supply chain. Industry estimates suggest that the global market of green rubber is set to increase at a rate of 8.7% CAGR between 2025 and 2032 including bio-based and sustainably produced synthetic rubbers. Furthermore, advancements in butyl rubber vulcanization chemistry, especially the replacement of sulfur based systems with more efficient peroxides and phenolic resin cure systems, are also consuming less energy in rubber processing and increasing compound shelf life, increasing the sustainability profile of butyl rubber use, albeit in small steps.

- Smart Manufacturing and Process Digitalization in Butyl Rubber Production: The introduction of Industry 4.0 technologies in butyl rubber polymerization and compounding processes is generating significant improvements in the efficiency of the production process, the quality of products, and the safety of the operations. Polymerization of butyl rubber is done at very low temperatures (around -90/-100°C) with liquid ethylene as a diluent and aluminum chloride catalysts a technically challenging process in which the ratio of the monomers and the injection of catalysts directly affect the molecular weight distribution and the quality of the product. Manufacturers are reducing the level of batch-to-batch variation on viscosity with the use of advanced distributed control systems (DCS) with AI-assisted process optimization algorithms, which has a direct effect on downstream processability at tire and pharmaceutical manufacturers that require batching of compound materials. The use of predictive maintenance systems that check the mechanical integrity of specialized low-temperature reactors, compressors, and heat exchangers, equipment used in severe service conditions, is also minimizing unplanned outages by 25–35% in most major production facilities, according to available industry implementation records. Using digital quality management systems with real-time Mooney viscosity, molecular weight monitoring with an inline GPC sensor, and automatic certificate of analysis generation are reducing quality release cycles formerly achieved in days and allowing just-in-time delivery models that are becoming more and more demanded by automotive tier-1 customers. Such manufacturing technology investments are especially large considering the fact that the production of butyl rubber is highly capital intensive and there are only a few manufacturers in the world, where efficiency in operations directly leads to competitive distinction and margin growth.

- Advanced Pharmaceutical Closure Technologies and Drug Delivery Integration: Novelty in the pharmaceutical-grade butyl rubber compounds and in designs of the closure system is forming higher-value points of application in injectable drug delivery, combination products and higher-value drug-device interfaces. Pharmaceutical closure manufacturers such as Datwyler, West Pharmaceutical Services and Aptar are coming up with coated closure technologies – in which PTFE or fluoropolymer films are coated onto bromobutyl rubber stoppers – that reduce drug-rubber interactions, extractables and leachables many times over and also do not siliconize stoppers and raise concerns of particulate formation. These are high-end coated closures that sell at 3-5 times the cost of uncoated bromobutyl closures, however, these high-end coated closures are required to meet the most critical drug stability and patient safety concerns of biologics and protein-based pharmaceuticals. The biologic drug pipeline and home healthcare trends that will increase the prefillable syringe market to USD 8.2 billion in 2024 and 10.1% CAGR through 2030 are entirely dependent on pharmaceutical-grade bromobutyl rubber plunger stoppers. Also, wearable injector devices, auto-injector devices, and on-body drug delivery devices are another high-growth application segment with wearable injector market expected to grow to USD 11.4 billion by 2030, with their applications demanding precision-engineered butyl rubber components with specific dimensional tolerances and drug compatibility requirements.

Category Wise Insights

By Type

Why Does Regular Butyl Rubber Lead the Market?

Regular butyl rubber (IIR) is the most prevalent type segment, which controls approximately 38⎻ per cent of the entire market in 2025. It is dominating since it is widely used in cost-effective industrial processes like tire inner tubes on commercial vehicles, curing bladders during tire production, and general-purpose sealing and hose purposes where the extra price of halobutyl is not worth the extra expense. According to industry data, the global regular butyl rubber production capacity is estimated as approximately 1.1 million metric tons per year in 2024, with significant capacity located at major plants of ExxonMobil (Baton Rouge, USA; Notre Dame de Gravenchon, France), LANXESS (Zwijndrecht, Belgium; Jhagadia, India), and Nizhnekamskneftekhim (Russia). The low gas permeability of regular butyl rubber (approximately 8-10 times less than natural rubber) and outstanding resistance to ozone and heat are the reasons why this material is preferable in curing bladders. They are inflatable membranes that are used in tire vulcanization presses, are reusable, and 50,000 -100,000 curing bladders manufactured in a single tire manufacturing plant produce a high captive demand stream. Lower processing temperatures are also needed to make regular butyl compared to halobutyl grades and energy consumption is saved when mixing and molding compounds, and halobutyl grades need higher processing temperatures, which in turn favor their cost competitiveness in large volume industrial use.

The most rapidly expanding category of rubber is bromobutyl rubber at a 7.1% CAGR between 2026 and 2035. Its benefits are a high compatibility to cure with both natural as well as diene rubber, high rate of cure compared to chlorobutyl, and high tire air pressure retention with time. These are some of the traits that enable bromobutyl to dominate passenger car and SUV tire inner liners that are a growing market with the growth of light-vehicle production in the world. In 2025, the segment is estimated to have a value of approximately USD 1.02billion and the figure will stand at USD 1.78 billion in 2035. A major trend is the development of coextruded and multilayer inner liner designs which include bromobutyl in very fine gauges; manufacturers of major tires are thinning liner gauge to about 0.8 to 0.9 mm while at the same time achieving the same air-retention properties with much higher-performing bromobutyl formulations.

By Application

Why Does Tire & Automotive Dominate Butyl Rubber Applications?

Regular butyl rubber (IIR) is the biggest type segment and it holds an amount of about 38% of the total market share in 2025. This hegemony is due to its extensive use in low-end industrial markets such as tire inner tubes in commercial vehicles, curing bladders in tire production and in general-purpose sealing and hose markets where the high price of halobutyl-based versions does not justify itself. The industry data showed that the total world capacity of regular butyl rubber was about 1.1 million metric tons per year in 2024, with large facilities owned by ExxonMobil (Baton Rouge, USA and Notre Dame de Gravenchon, France), LANXESS (Zwijndrecht, Belgium and Jhagadia, India), and Nizhnekamskneftekhim (Russia). The low gas permeability of regular butyl rubber, about 810 times less than natural rubber, and its high ozone and heat resistance give butyl rubber the preferred choice in curing bladders a reusable inflatable membrane used in tire vulcanization presses. Each tire manufacturing plant can require 50,000-100,000 curing bladders every year, and this is a big source of captive demand. The processing temperatures being relatively lower in regular butyl rubber than the halobutyl grades also lowered the energy usage in the mix of the compound and molding processes which conserved energy, which supports its price competitiveness in high-volume industrial usage.

Bromobutyl rubber is growing at the highest CAGR rate of 7.1% between 2026 and 2035 due to its high cure compatibility with natural and diene rubbers, higher cure rate than chlorobutyl and higher ability to retain tire air pressure over time. These characteristics render bromobutyl the material of choice in passenger car and SUV tire inner liners, a business that is expanding in tandem with light vehicle manufacturing in the world. In 2025, the bromobutyl rubber part was estimated to have a USD 1.02 billion value, and the value is supposed to increase to USD 1.78 billion in 2035. The move towards coextruded and multilayer inner liner constructions using bromobutyl rubber in thin-gauge applications is one of the trends with leading tire manufacturers shrinking liner gauge by about 0.8mm to 0.9mm whilst maintaining the same air retention characteristics by using superior performance bromobutyl formulations.

By Grade

Why Does Industrial Grade Dominate the Market?

The greatest percentage of grade portions in the market share are in industrial-grade butyl and halobutyl rubber, which is about 61% in 2025 because of the high volume of tire, automotive, and general industrial applications that do not need pharmaceutical levels of purity. Industrial grade butyl rubber is made to specifications including Mooney viscosity (usually ML 1 + 8 at 125 o C in the range 3275 depending on use), isoprene content ( 0.52.5 mol + ), halogen content (halobutyl grade 1.820 ml bromine; chlorine 1.1–1.3 ml chlorine), and ash, moisture, and antioxidant content. The industrial grade market is expected to increase at a rate of 5.1, to USD 2.08 billion in 2025 and USD 3.35 billion in 2035. Though a smaller volume share, pharmaceutical-grade butyl rubber does sell at a much higher price and a much better margin, with pharmaceutical-grade bromobutyl stoppers selling at USD 0.08-0.25 a unit versus commodity rubber of USD 1.6-2.2/kg in large bulk form.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 3.64 billion |

| Projected Market Size in 2035 | USD 5.92 billion |

| Market Size in 2025 | USD 3.41 billion |

| CAGR Growth Rate | 5.6% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Grade, Application, End-Use and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

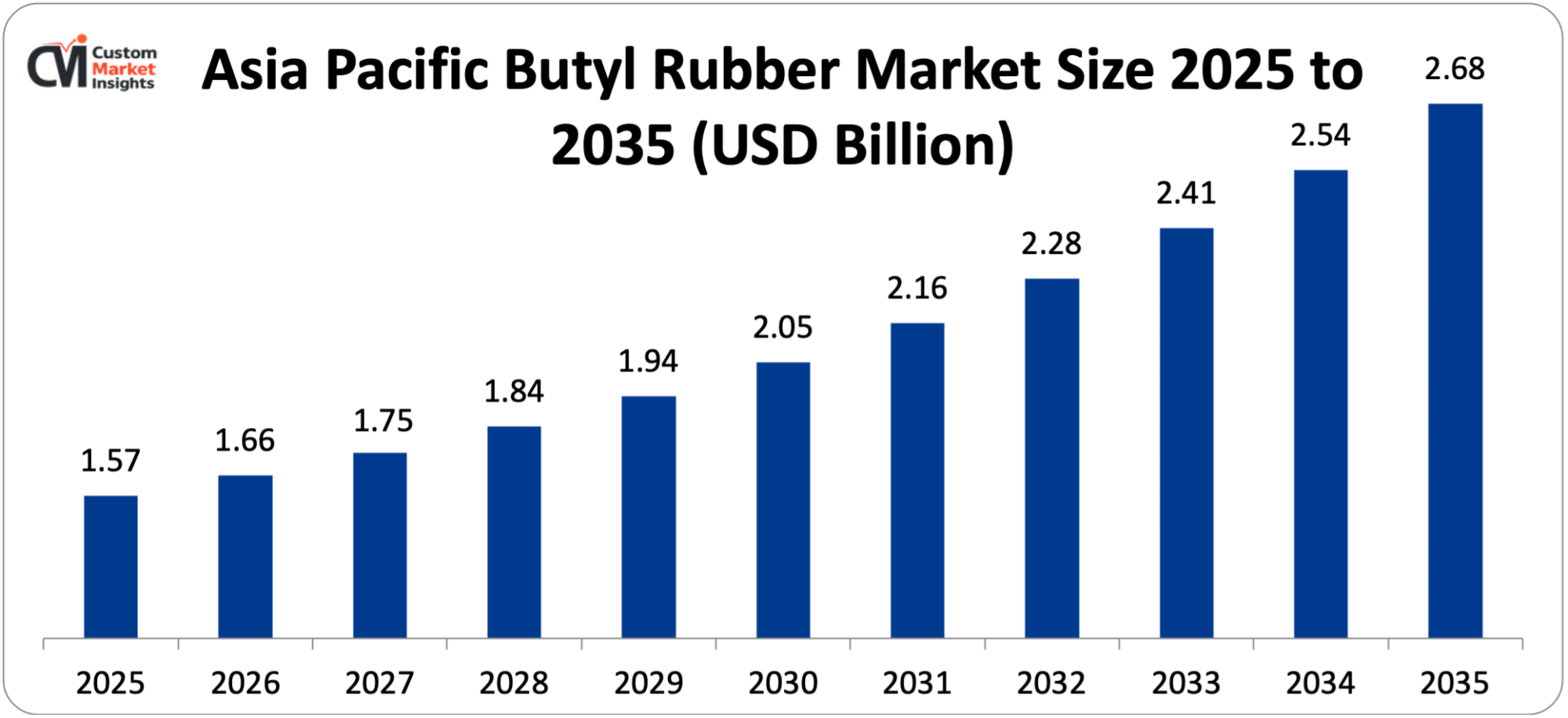

The Asia Pacific butyl rubber market size is estimated at USD 1.57 billion in 2025 and is projected to reach approximately USD 2.68 billion by 2035, with a 6.1% CAGR from 2026 to 2035.

Why Did Asia Pacific Dominate the Market in 2025?

By 2025, Asia Pacific controls a total of about 46% of the world butyl rubber market share, as it is the largest tire producing region in the world, fast growing automobile production, rising pharmaceutical manufacture base, and rising domestic capacity of production of halobutyl rubber compounds. China alone makes an estimated 650-700 million tires each year which is around 35% of the world tire production, its domestic butyl rubber consumption is the largest single national market in the world at an estimated USD 620 million in 2025. The tire industry of India, which is estimated to manufacture about 200 million tires as of 202324 by the Automotive Tyre Manufacturers Association (ATMA), has been rapidly growing due to the rise in domestic vehicle sales of 78% per annum and an increase in its export to Europe and the Americas. The countries of Japan and South Korea have had technologically advanced butyl rubber consuming industries and the companies of Bridgestone, Sumitomo Rubber, Hankook, and Kumho tire manufacture have been using the best halobutyl consuming compounds of the world and the region in high-performance and ultra-high-performance tire products. The domestic capacity of halobutyl in China has been growing at an impressive rate over the recent ten years, with Sinopec Yanhua and Zhejiang Xintao Polymer appearing to be the significant regional producers, though the consistency and quality of Chinese halobutyl manufacturing into high-end tire applications in the outer liner remains a competitive edge in favour of traditional global players.

China Market Trends

China boasts the largest butyl rubber market in Asia Pacific, with its status as the largest vehicle manufacturer in the world and with its huge tire manufacturing industry serving both domestic and export markets, the booming pharmaceutical manufacturing industry with CXMO activity and domestic drug production, and its policies of promoting domestic production of major petrochemical intermediates such as butyl rubber. The pharmaceutical industry of China has been expanding the use of locally produced pharmaceutical grade rubber closures for local drug manufacturing, but the high value biologics manufacturers are still reluctant to use non-validated local domestic domestically produced pharmaceutical grade rubber closures because they want regulatory assurance.

Why is North America Experiencing Steady Growth?

North America is steadily growing with a forecasted CAGR of 4.9% in the 2026-2035 period, and the region has an established but technologically advanced automotive industry, it is the home base of the major manufacturing of butyl rubber by ExxonMobil, it is home to a large pharmaceutical manufacturing industry, and due to the construction and the industrial use, the demand is growing steadily. Replacement tires in the United States are also a key player in the demand that has led to high world replacement tire sales of about 18%. The trend of higher tire specifications in the U.S. market, which results in light truck tires, which demand heavier and more aggressive inner liners than passenger car tires, taking up a disproportionately large portion of vehicle sales, is advantageous to the consumption of North American butyl rubber.

What is the Size of the U.S. Market?

The U.S. butyl rubber market size is calculated at approximately USD 532 million in 2025 and is expected to reach nearly USD 848 million in 2035, advancing at a CAGR of 4.9% between 2026 and 2035.

U.S. Market Trends

The U.S. market has a sophisticated downstream customer base of premium tire manufacturers, world class pharmaceutical companies and advanced industrial users. The USD 1.2 trillion infrastructure investment commitment in the Bipartisan Infrastructure Law is also underpinning the expansion of construction sealant and waterproofing applications using butyl rubber, and roofing membranes and waterproofing sealants are one of the increasing segments of demand. The high level of application of the standards of pharmaceutical packaging by the FDA makes the pharmaceutical packaging a quality-differentiated market that favors the suppliers of premium-grade halobutyl.

Why is Europe Focusing on Sustainability and Circularity?

The European butyl rubber market has been defined by a very high regulatory impact on the sphere of supply and demand, the EU Tire Labelling Regulation requirements which promote the performance of low rolling resistance, which is also achieved through optimization of halobutyl inner liner formulations; the requirements of the EU REACH and the EU SVHC regulations which are currently seeking to reformulate rubber compounds to remove substances of concern and the EU Pharmaceutical Legislation reform which focuses on quality of drug packaging and resiliency in the supply chain. LANXESS has some large butyl rubber plants in Zwijndrecht, Belgium, and Europe as a large manufacturing site. The largest European national market is Germany, which is the headquarters of Continental, the second-largest tire organization in the world, and a leading pharmaceutical manufacturing center.

Why is the Middle East & Africa Region Experiencing Growth?

The LAMEA region demonstrates the increasing development of the market due to the increase in the number of automotive assembly activities in Morocco, South Africa, and Egypt, the development of the pharmaceutical industry in Saudi Arabia and the UAE through Vision 2030 industrial diversification programs, and the increase in the level of tire replacement needed in the expanding vehicle fleet in Sub-Saharan Africa. The ownership of Arlanxeo (a joint venture with LANXESS) gives Saudi Aramco strategic exposure to the manufacture of butyl rubber and the further development of the petrochemical industry in the Kingdom is investing in downstream synthetic rubber production.

Top Players in the Market and Their Offerings

- ExxonMobil Chemical Company

- LANXESS AG

- Arlanxeo (Saudi Aramco / LANXESS JV)

- Nizhnekamskneftekhim PJSC (NKNK)

- Sinopec Beijing Yanhua Petrochemical Co. Ltd.

- Sumitomo Chemical Co. Ltd.

- ZEON Corporation

- Sibur Holding PJSC

- Formosa Synthetic Rubber Corp.

- Versalis S.p.A. (Eni subsidiary)

- Others

Key Developments

The market has undergone significant developments as industry participants seek to expand capabilities and enhance product portfolios.

- In January 2025: ExxonMobil Chemical introduced Bromobutyl 2030XP, a new high-performance bromobutyl rubber grade designed and developed for use in ultra-thin EV tires as an inner liner. The new grade provides a 12% enhancement on the air impermeability compared to the previous product at the same gauge, which will allow the tire manufacturers to reduce the mass of the inner liner further and still achieve the EV-specific tire performance characteristics. ExxonMobil reported that the inner-liner performance specifications in EV tires, being influenced by increased load on heavy vehicles and the desire by the industry to do away with spare tires, were the main engineering design driver for the new product.

- In March 2025: Arlanxeo declared it is entering into a strategic alliance with a key biopharmaceutical manufacturer of closures to create next-generation coated bromobutyl based formulations that have been directly tailored to the requirements of the fast-growing pharmaceutical industry to improve the compatibility of coated elastomeric drug packaging with mRNA-based therapeutics and other protein biologics.

The strategic activities have enabled the companies to gain market strength, increase products, build technological strength, and capture growth opportunities in the growing market.

The Butyl Rubber Market is segmented as follows:

By Type

- Regular Butyl Rubber (IIR)

- Chlorobutyl Rubber (CIIR)

- Bromobutyl Rubber (BIIR)

- Partially Cross-linked Butyl Rubber

- Other Types

By Grade

- Industrial Grade

- Pharmaceutical Grade

- Specialty/High-Performance Grade

By Application

- Tire & Automotive (Inner Liners, Inner Tubes, Vibration Dampeners, Seals)

- Pharmaceutical Packaging (Stoppers, Plungers, Septa)

- Construction & Sealants

- Industrial (Hoses, Belts, Tank Linings, Chemical-Resistant Products)

- Other Applications

By End-Use

- Automotive OEM

- Replacement Tire Market

- Healthcare & Pharmaceutical Manufacturers

- Industrial End-Users

- Others

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Butyl Rubber by Segments

- 2.1.2. Butyl Rubber by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Butyl Rubber Market Attractiveness Analysis, By Type

- 2.2.3. Butyl Rubber Market Attractiveness Analysis, By Grade

- 2.2.4. Butyl Rubber Market Attractiveness Analysis, By Application

- 2.2.5. Butyl Rubber Market Attractiveness Analysis, By End-Use

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Rising Automotive Production and Fuel Efficiency Standards Globally

- 3.1.2. Expanding Pharmaceutical Packaging Requirements and Healthcare Sector Growth

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Butyl Rubber Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Butyl Rubber Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Regular Butyl Rubber (IIR)

- 4.1.3. Butyl Rubber Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Chlorobutyl Rubber (CIIR)

- 4.1.7. Butyl Rubber Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Bromobutyl Rubber (BIIR)

- 4.1.11. Butyl Rubber Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Partially Cross-linked Butyl Rubber

- 4.1.15. Butyl Rubber Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Other Types

- 4.1.19. Butyl Rubber Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Butyl Rubber Market – By Grade

- 5.1. Grade Market Overview, By Grade Segment

- 5.1.1. Butyl Rubber Market Revenue Share, By Grade, 2025 & 2035

- 5.1.2. Industrial Grade

- 5.1.3. Butyl Rubber Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Pharmaceutical Grade

- 5.1.7. Butyl Rubber Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Specialty/High-Performance Grade

- 5.1.11. Butyl Rubber Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Grade Market Overview, By Grade Segment

- Chapter 6. Butyl Rubber Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Butyl Rubber Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Tire & Automotive (Inner Liners, Innertubes, Vibration Dampeners, Seals)

- 6.1.3. Butyl Rubber Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Pharmaceutical Packaging (Stoppers, Plungers, Septa)

- 6.1.7. Butyl Rubber Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Construction & Sealants

- 6.1.11. Butyl Rubber Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Industrial (Hoses, Belts, Tank Linings, Chemical-Resistant Products)

- 6.1.15. Butyl Rubber Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Other Applications

- 6.1.19. Butyl Rubber Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Butyl Rubber Market – By End-Use

- 7.1. End-Use Market Overview, By End-Use Segment

- 7.1.1. Butyl Rubber Market Revenue Share, By End-Use, 2025 & 2035

- 7.1.2. Automotive OEM

- 7.1.3. Butyl Rubber Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Replacement Tire Market

- 7.1.7. Butyl Rubber Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Healthcare & Pharmaceutical Manufacturers

- 7.1.11. Butyl Rubber Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Industrial End-Users

- 7.1.15. Butyl Rubber Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Others

- 7.1.19. Butyl Rubber Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-Use Market Overview, By End-Use Segment

- Chapter 8. Butyl Rubber Market – Regional Analysis

- 8.1. Butyl Rubber Market Overview, By Region Segment

- 8.1.1. Global Butyl Rubber Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Butyl Rubber Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Butyl Rubber Market Revenue, By Type, 2026 – 2035

- 8.1.4. Global Butyl Rubber Market Revenue, By Grade, 2026 – 2035

- 8.1.5. Global Butyl Rubber Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Butyl Rubber Market Revenue, By End-Use, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Butyl Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Butyl Rubber Market Revenue, By Type, 2026 – 2035

- 8.2.3. North America Butyl Rubber Market Revenue, By Grade, 2026 – 2035

- 8.2.4. North America Butyl Rubber Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Butyl Rubber Market Revenue, By End-Use, 2026 – 2035

- 8.2.6. U.S. Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Butyl Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Butyl Rubber Market Revenue, By Type, 2026 – 2035

- 8.3.3. Europe Butyl Rubber Market Revenue, By Grade, 2026 – 2035

- 8.3.4. Europe Butyl Rubber Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Butyl Rubber Market Revenue, By End-Use, 2026 – 2035

- 8.3.6. Germany Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Butyl Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Butyl Rubber Market Revenue, By Type, 2026 – 2035

- 8.4.3. Asia Pacific Butyl Rubber Market Revenue, By Grade, 2026 – 2035

- 8.4.4. Asia Pacific Butyl Rubber Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Butyl Rubber Market Revenue, By End-Use, 2026 – 2035

- 8.4.6. China Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Butyl Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Butyl Rubber Market Revenue, By Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Butyl Rubber Market Revenue, By Grade, 2026 – 2035

- 8.5.4. The Middle-East and Africa Butyl Rubber Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Butyl Rubber Market Revenue, By End-Use, 2026 – 2035

- 8.5.6. Saudi Arabia Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Butyl Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Butyl Rubber Market Revenue, By Type, 2026 – 2035

- 8.6.3. Latin America Butyl Rubber Market Revenue, By Grade, 2026 – 2035

- 8.6.4. Latin America Butyl Rubber Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Butyl Rubber Market Revenue, By End-Use, 2026 – 2035

- 8.6.6. Brazil Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Butyl Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Butyl Rubber Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Butyl Rubber Market: Company Market Share, 2025

- 9.2. Global Butyl Rubber Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. ExxonMobil Chemical Company

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. LANXESS AG

- 10.3. Arlanxeo (Saudi Aramco / LANXESS JV)

- 10.4. Nizhnekamskneftekhim PJSC (NKNK)

- 10.5. Sinopec Beijing Yanhua Petrochemical Co. Ltd.

- 10.6. Sumitomo Chemical Co. Ltd.

- 10.7. ZEON Corporation

- 10.8. Sibur Holding PJSC

- 10.9. Formosa Synthetic Rubber Corp.

- 10.10. Versalis S.p.A. (Eni subsidiary)

- 10.11. Others.

- 10.1. ExxonMobil Chemical Company

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 36

List Of Tables

Tables No 1 to 51

Prominent Player

- ExxonMobil Chemical Company

- LANXESS AG

- Arlanxeo (Saudi Aramco / LANXESS JV)

- Nizhnekamskneftekhim PJSC (NKNK)

- Sinopec Beijing Yanhua Petrochemical Co. Ltd.

- Sumitomo Chemical Co. Ltd.

- ZEON Corporation

- Sibur Holding PJSC

- Formosa Synthetic Rubber Corp.

- Versalis S.p.A. (Eni subsidiary)

- Others

FAQs

The key players in the market are ExxonMobil Chemical Company, LANXESS AG, Arlanxeo (Saudi Aramco / LANXESS JV), Nizhnekamskneftekhim PJSC (NKNK), Sinopec Beijing Yanhua Petrochemical Co. Ltd., Sumitomo Chemical Co. Ltd., ZEON Corporation, Sibur Holding PJSC, Formosa Synthetic Rubber Corp., Versalis S.p.A. (Eni subsidiary), Others.

The government regulations have a pervasive impact in the butyl rubber value chain. Low rolling resistance tire performance requirements in the EU, U.S., China and India, which are required by automotive emission and fuel economy standards, are materially reliant on the use of advanced halobutyl inner liner technology, providing sustained regulatory-based demand. FDA, EMA and PMDA have regulation on compliance of drug packaging rubber closures with pharmacopeial standards, which establishes quality criteria that are not negotiable, and which favor established, proven suppliers of halobutyl. The European environmental laws such as the REACH and the emerging trends in Chinese chemical management policies are compelling reformulation investments in dropping some accelerators and processing aids in butyl rubber compounds. Investment in domestic butyl rubber production capacity (especially in China and India) is being supported by national strategic needs, especially with favourable financing and import tariff regimes, redefining the global competitive forces in the regional markets.

The prices of butyl rubber are directly related to the feedstock price of isobutylene which is further related to the economics of crude oil and C4 hydrocarbon streams. The past five years have been characterized by regular butyl rubber spot prices of USD 1.60- USD 2.80 per kilogram with harbor butyl premium grades fetching USD 2.20- USD 3.50 per kilogram according to grade specification and supply-demand forces. Pharmaceutical grade halobutyl compounds have a much higher realized prices after formulation and as manufactured into finished closures, pharmaceutical stoppers produce USD 80250 per kilogram of rubber equivalent value. The capital intensity of butyl rubber production; according industry estimates, a world-scale grassroots butyl rubber plant needs USD 400600 million in capital investment which poses high barriers to entry which moderate the threat of disruptive price competition by new entrants which promotes sustained price stability and margin discipline among existing producers.

According to the current analysis, the market is estimated to reach USD 5.92 billion by 2035, driven by the demand by the automotive industry to electrify their industries necessitating the use of high-quality tire materials, the pharmaceutical pipeline development that demand high-quality rubber closure product solutions, the growth in the construction sector in the emerging economies, the sustainability push to reformulate products, creating higher-value product growth, and the digitalization of the butyl rubber manufacturing process, enhancing the efficiency of production and ensuring consistency in the product.

It is predicted that Asia Pacific will have the largest share of revenue, with a share of about 46% of the total world market share during the forecast period, considering the regions monopoly in the concentration of tire manufacturing, China being the largest car maker globally, emerging Asian economies have been increasing their spending in pharmaceutical and health care, the state investment in the production of synthetic rubber, and consumption increase in line with the GDP growth in the various large economies all combined within the same period.

Asia Pacific is projected to grow at the strongest CAGR of 6.1% during the forecast period, driven by China and India’s dominant positions in global tire manufacturing with combined production representing approximately 45% of global output, rapidly expanding pharmaceutical manufacturing bases in both countries demanding pharmaceutical-grade halobutyl closures, growing automotive production in Southeast Asian countries including Thailand, Indonesia, and Vietnam, and increasing domestic butyl rubber production capacity in the region reducing dependence on imports.

The Global Butyl Rubber Market is projected to achieve high growth because there is global vehicle production of over 100 million vehicles in 2030 that will demand tire inner liners, the global pharmaceutical market is expected to expand to USD 2.3 trillion by 2030 that will demand premium-grade bromobutyl pharmaceutical packaging, EV market is expected to grow to 40 million vehicles in 2030 creating demand in high quality EV-optimized inner liner formulations, and construction investment is expected to drive the growth in sealant and waterproofing application growth.