Vinyl Toluene Market Size, Trends and Insights By Grade Type (Standard Grade, High-Purity Grade, Specialty Grade), By Isomer Composition (Meta-Vinyl Toluene, Para-Vinyl Toluene, Mixed Isomer Vinyl Toluene), By Formulation Type (Monomer Formulations, Modified Resin Systems, Copolymer Blends), By End-Use Industry (Paints & Coatings Industry, Adhesives & Sealants Industry, Printing Inks Industry, Composite Materials Industry, Chemical Intermediate Manufacturing), By Functionality (Reactive Diluent Applications, Crosslinking Agent Usage, Polymer Intermediate Applications), By Distribution Channel (Direct Manufacturer Supply, Specialty Chemical Distributors, B2B Chemical Procurement Platforms), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 5.9%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Europe |

| Largest Market: | Asia Pacific |

Major Players

- INEOS

- BASF

- Dow Inc.

- LyondellBasell

- Others

Reports Description

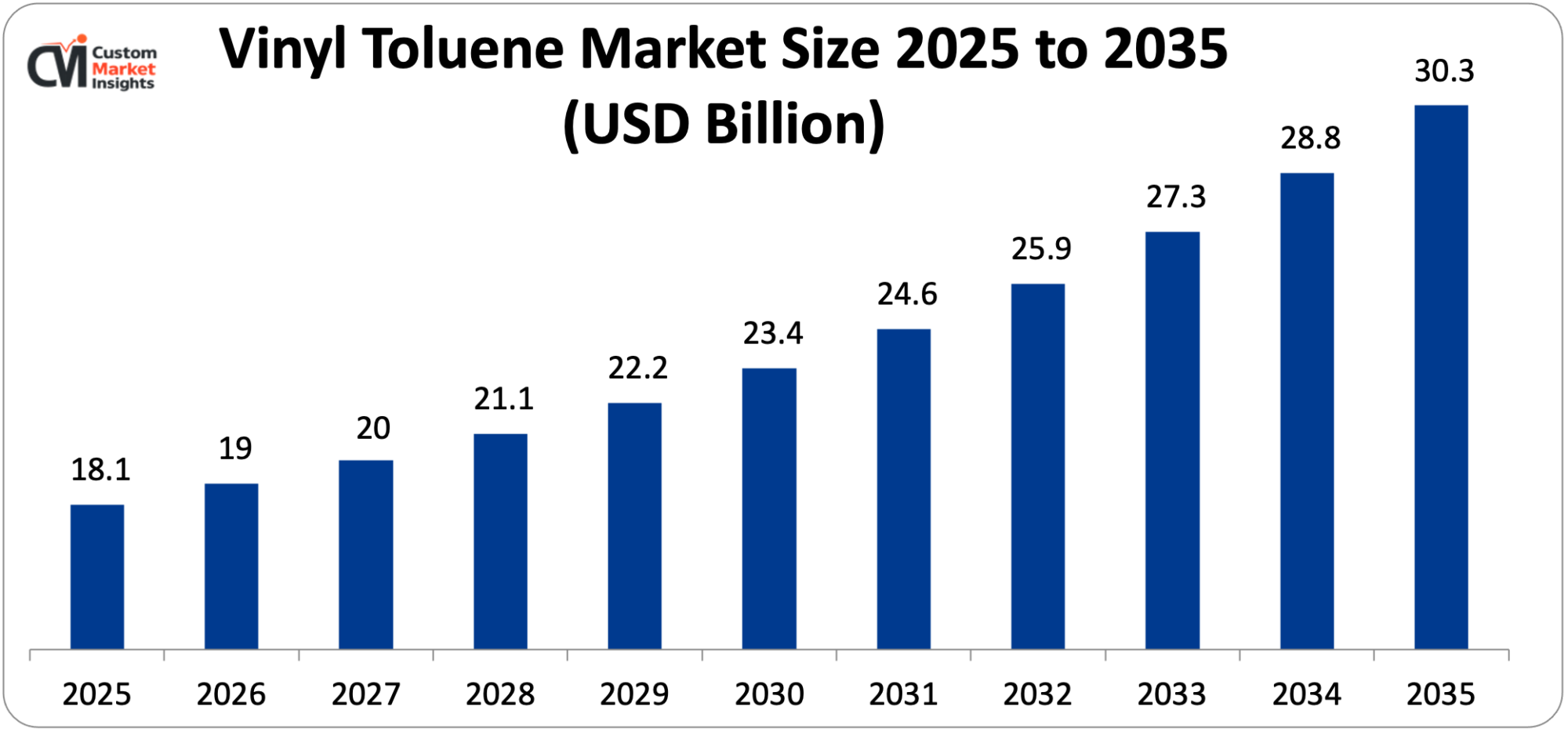

Vinyl Toluene market in the world is expected to hit USD 19 billion in 2026 and is projected to reach USD 30.3 billion in 2035 with a CAGR of 5.9% projected throughout the forecast period of 2026-35. The expansion of the market is mainly influenced by the increased demand for high-performance resins and polymers in the following uses; coating, construction material, automotive parts, and composite uses.

The growth of the industry is being further accelerated by increasing the use of vinyl toluene as a reactive diluent and crosslinking agent in unsaturated polyester and alkyd resin systems. A further reason is the increasing investments in modern polymer production technologies, infrastructure, and industrial developments in the emerging economies and migration to lightweight and durable materials, which are reinforcing momentum in the market. The factors that are also proving to be instrumental in facilitating the long-term growth of the vinyl toluene market include continuous product innovations, enhanced formulation effectiveness, and an increasing distribution network of the leading chemical manufacturers.

Market Highlight

- Asia Pacific will dominate the market share of Vinyl Toluene in 2025 with a market share of 41% with good growth in the construction chemicals business, increased polymer capacity production, and rising demand in the automotive and electronic products manufacturing centers in China, India, South Korea, and Japan.

- North America is expected to have the highest CAGR of 6.5% between 2026 and 2035 on the basis of increasing investments in high composite materials, increasing demand for specialty resins and technological improvement in high performance coatings.

- By Grade Type, industrial grade vinyl toluene will have 44% of the market share in 2025 because of the prevalence of these products in mass production of resin, and the high-purity products will experience the most growth through 2035 because of the growing use of these products in precision coating applications and specialty products.

- On the basis of Isomer Profile, mixed-isomer vinyl toluene will be the leader in 2025 with 52% of the market share owing to its affordability and wide industrial applicability, whereas para-rich compositions will steadily increase owing to enhanced reactivity and performance features.

- By Formulation Integration, the vinyl toluene employed in unsaturated polyester resin systems takes 47% of the market in 2025 as part of the fiberglass-reinforced products, with its general use in advanced copolymer systems expected to grow at a significant rate during the next decade.

- Under End-Use Applications, the paints and protective coating segment will dominate the market with 38% in 2025 due to the development of infrastructure and the use of non-corrosive industrial coating, and the composites sector will achieve a healthy growth of 13.5 percent because of the demand for lightweight materials.

- By Functional Role, its application as a reactive viscosity modifier holds 49% of the market in 2025 because it offers benefits of its application as formulation efficiency, but its application as a performance-enhancing polymer modifier will increase faster in the forecast period.

- On Supply Channel, direct manufacturer-to-industry supply will remain predominant with 57% in 2025 due to long-term procurement agreements but specialty chemical distributors are expected to increase gradually as small and middle scale manufacturers grow worldwide.

Significant Growth Factors

The high market growth in Vinyl Toluene is mainly attributed to market growth through an increase in high performance polymers, growth in the building and manufacturing of automobiles, adoption of superior composite materials, and the constant development of resins and specialty chemical technologies. The development of infrastructure investments in Asia Pacific and North America as well as the transition to durable, lightweight, and chemically resistant materials further boosts the growth of the market.

- Rising Demand for High-Performance Resins and Composites: The key driver of the business success is the growing use of vinyl toluene in unsaturated polyester resins and reinforced composite structures. In March 2023, INEOS declared growth plans in its styrenics and specialty monomers product range to satisfy the rising demand of industry resin. LyondellBasell has in May 2023 emphasized the investments in capacity optimization as a method of enhancing performance polymer production. Moreover, in September 2023, AOC improved its composite resin solutions to serve the wind energy and infrastructure uses. All these developments indicate an increasing need for high-strength and corrosion resistant materials that indirectly promote the use of vinyl toluene in polymer modification.

- Coatings and Polymer Innovation: Customary R&D in Coatings and special matter is yet another key growth driver. In July 2023, Allnes launched new high-end technologies of industrial coating resins to enhance their durability and effectiveness in performance. In addition, BASF declared more investments in performance materials and specialty monomers in November 2023 as an attempt to improve formulation sustainability and regulatory compliance. These strategic actions, coupled with the increase of purification processes and technologies of production on an industrial scale, are bolstering supply and the future prospects of the growth of the global vinyl toluene market in the long term.

The major Innovations that are transforming the Vinyl toluene market of the modern world.

The market of Vinyl Toluene is undergoing a rapidly changing technology due to the advancements in the chemistry of polymers, increased rate of production, sustainability in the production of specialty chemicals, and high level of performance resin in several businesses. The current research and development and long-term partnerships between chemical manufacturers and their final markets in the utilization of the product are rendering new advanced aromatic derivatives of vinyl to be quickly gaining commercial adoption.

- Specialty Monomer and Polymer Formulation Technologies: Companies are increasingly becoming specialized in monomer purification of high purity and polymer compatibility solutions. In January 2023, SABIC expanded its portfolio of specialty chemicals, which is beneficial to its customers in the construction and automotive composite market in the higher-performance polymers and resin segment. In April 2024, Evonik Industries initiated research projects in the fields of the development of performance additives and other resin stabilization technologies. The inventions are important to provide better control over the viscosity, thermal stability, and durability of toluene-based vinyl formulations that are to be utilized in the production of industrial coatings and composite materials in the upcoming generation.

- Smart Manufacturing and Process Optimization in Aromatic Chemical Production: In Aromatic Chemical Production, it is the production of vinyl aromatic Smart Manufacturing and Process Optimization in Aromatic Chemical Production that is increasing the efficiency and sustainability of the production process through digitalization and process automation. In August of 2023, Dow Inc. announced it was going to modernize its monomer production facilities that produced specialty materials to use less energy and generate more. In October 2024, Eastman Chemical Company expanded its capacity in process engineering to enable it to take on elaborate purification and low-emission chemistry processing technologies. Such inventions are helping manufacturers meet more difficult environmental compliance standards and also improve commercial boosts of vinyl toluene products.

- High-performance sustainable resin systems: Due to the growing interest in green materials, the resin systems based on bio-enhanced and low-emission vinyl toluene derivatives are developed. In May 2024, Arkema declared sustainability-focused polymer study programs and aimed to optimize the lifecycle functionality of materials and reduce the emissions of volatile organic compounds of industrial coatings. The vinyl toluene polymer solutions available in the international industrial markets are also improving the long-term competitiveness through sustainable chemical engineering strategic investments in R&D.

Category Wise Insights

By Grade Type

What is so Appealing about the Market of High-Purity Grade?

It is estimated that high-purity vinyl toluene will take over the market in 2025 as it is excellent in performance in specialty chemical and high-value polymer applications. High-purity grades are replacing blended coating and composite production requirements that are on the increase with advanced coating and composite manufacturing applications. Ordinary grade vinyl toluene still enjoys a high level of usage in large volume resin production because it is cost effective, whereas specialty grades will experience the greatest CAGR in the period 2026 to 2035 as industries move towards high performance or precision chemical formulations.

By Isomer Composition

Why Mixed Isomers Prefer Market?

Mixed isomer vinyl toluene will be the most popular in the market in 2025 because it is relatively cheap to produce and has wide industrial application in resin modification and polymer manipulation. Specialty chemical formulations The use of meta and para isomers is becoming increasingly popular due to their high chemical reactivity and thermal stability. The variants of para-isomers are likely to experience the highest growth in the forecast period because of the increasing demand for high-performance industrial coating.

By Formulation Type

How come Monomer Formulations are the best in the market?

Monomer based toluene formulations (vinyl) will rule in 2025 because of their widespread application in the manufacture of unsaturated polyester resin and processing of polymers. Another area where modified resin systems are becoming significant is in the enhancement of the mechanical strength and chemical resistance of resin systems by the manufacturers. The rate of growth in copolymer blends is expected to increase further between 2026 and 2035 because of the escalating demands of the advanced composite materials in automotive and construction.

By End-Use Industry

What is making Paints and Coatings Industry Conquer?

Vinyl toluene market will be dominated by the paints and coatings sector in 2025 because of the high rate of infrastructural development, industrial growth, and corrosion-proof coating materials. The sponge and sealants are likely to continue increasing because they are used in the building and food packaging systems. The printing inks and composite materials segments are projected to enjoy a high growth in terms of a boom in demand for high-performance industrial materials worldwide. Downstream production of polymers will also remain with chemical intermediate applications.

By Functionality

What is So Appealing about Reactive Diluent Applications?

It is expected that in 2025, the reactive diluent applications will have the highest share, as they will lower the resin viscosity and shorten processing time in the polymer system. Vinyl toluene as a polymer intermediate also has an upsurge in demand because of the growing specialty resin production. It is estimated that crosslinking application will experience continuous growth in 2026 -2035, owing to the technological innovations in high-strength polymer networks and industrial coating.

By Distribution Channel

The Reason Direct Supply Channels Win?

The long term procurement contracts and the high demand in industrial sectors are the reasons to expect dominance of direct supply by chemical manufacturers in 2025. The growth rate of specialty chemical distributors is anticipated to be higher in the forecast period due to the growth of small and medium-scale manufacturers in the international arena. B2B chemical procurement solutions are also getting increasingly popular as a result of industrial supply chains being digitalized and enhanced pricing transparency.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 19 billion |

| Projected Market Size in 2035 | USD 30.3 billion |

| Market Size in 2025 | USD 18.1 billion |

| CAGR Growth Rate | 5.9% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Grade Type, Isomer Composition, Formulation Type, End-Use Industry, Functionality, Distribution Channel and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How big is the Asia Pacific Market?

It is projected to make USD 7.40 billion in 2025 and further to USD 12.1 billion by 2035 with a CAGR of 5.8% between 2026 and 2035 in the Asia Pacific Vinyl Toluene market. The market is dominated by the region because it is highly industrialized, the construction and auto-manufacture sector is growing at a great pace, and the region needs performance polymers and specialty chemical formulations. The regional demand is also being augmented by increasing the capacity of production of downstream resin industries as well as the development of infrastructure in emerging economies.

Reasons Why Asia Pacific Squeezed the Market in 2025.

Asia Pacific was estimated to have about 41% market share in the world market in 2025 because of the robust chemical manufacturing ecosystems in China, India, South Korea and Japan. The region enjoys the advantages of large scale production facilities of polymer and resin, the availability of low cost sources of raw material, and the growing end use industries in the form of coatings, adhesives, and composites. The fast urbanization, industrialization export-oriented development and government support of high-tech manufacturing technologies are also increasing the demand for vinyl toluene. Also, there are alliances between chemical manufacturers and downstream manufacturers that are also supporting high volume specialty chemical applications.

China Market Trend

The dominant roles that China holds in the production of global chemicals and its large investments in specialty polymer technologies lead to its dominance in the Asia Pacific market. Vinyl toluene is being fuelled by the expansion of the construction materials production, automotive lightweight parts, and industrial coatings. The market expansion is also being reinforced by government initiated industrial modernization initiatives and investments in high performance chemical manufacturing units. The cooperation of chemical manufacturers, coating manufacturing organizations, and polymer technology firms is improving the competitive position of China in the global market.

What Is driving further North American Expansion?

The North American market will have a CAGR of 5.6% in the years 2026–2035 because there will be an increase in the high-performance industrial materials and specialty coatings. The growth of the market is being motivated by increased ESG commitments by manufacturing firms and investments in green technologies in chemical production that are sustainable. High levels of specialty chemical producers, aggressive research technology on polymers and increased demand on lasting construction materials are also playing a pivotal role in expanding the market.

How Big Is the U.S. Market?

The U.S. Vinyl Toluene market will have a projected future of USD 3.39 Billion in 2025 and projected growth of 5.7% CAGR between 2026 and 2035.

U.S. Market Trends

The American marketplace is motivated by rising regulatory attention to the reduction of industrial emissions and rising use of chemical manufacturing techniques that are environmentally friendly. The demand is also being facilitated by increased investment in specialty resin output and high quality coating technologies. Increase in infrastructure renovation, automotive manufacturing and industrial maintenance is also contributing to increased domestic consumption of the vinyl toluene-based polymer solutions.

What Is the Rational behind Europe being so concerned with Specialty Chemical Sustainability?

The market for the Vinyl Toluene in Europe has a huge portion of the world market because of the environmental policy and great attention to the sustainability of chemical production. The low-VOC coating materials and efficient polymer systems are being taken up under encouragement of carbon neutrality and chemical emission standards. Germany, France, and the Netherlands are making huge investments in research and development of specialty chemicals and green polymers. The growth of the regional market is being supported by high use of high-quality coating resins and industrial polymer technologies.

Germany Market Trends

Germany is an important part of Europe since it has developed a high-technology chemical engineering sector and is a powerful researcher in specialty materials. The German chemical producers are concentrating on high-performance polymer additives, new resin stabilization technologies, and chemical processing based on sustainability. Market opportunities are also being enhanced by the increasing demands of the automotive production and industrial machinery sectors.

What Propels Growth in Middle East and Africa?

The Middle East & Africa region has a moderate growth trend in the market, but it is steady because of the growing industrial diversification strategies and infrastructure modernization strategies. Specialized chemical production and chemical feedstocks based on renewable energy are being invested in by the Gulf region countries, Saudi Arabia, and the UAE. Growth in Africa is facilitated by increased construction activity, industrialization, and the supply of better chemical distribution networks. The development of additional international relationships in chemical supply chains should increase long-term acceptance of the market in the region.

Top Players in the Market and Their Offerings

- INEOS

- BASF

- Dow Inc.

- LyondellBasell

- Eastman Chemical Company

- Arkema

- Evonik Industries

- SABIC

- Formosa Plastics Corporation

- Mitsubishi Chemical Group

- Sumitomo Chemical

- LG Chem

- Others

Key Developments

The market of Vinyl Toluene is experiencing strategic events with the giant producers of chemicals expanding their production capacities, researching new polymer chemistry and improving specialty chemical supply chains to meet the rising demand within the coatings, resin, and composite industries. Companies are also working hard on improving the purification technologies of the monomers, establishing a superior resin performance capability, and expanding the international distribution systems.

- SABIC -August 2023: SABIC announced that it intends to increase its worldwide demand for specialty chemicals and performance polymer production plants in response to the growing worldwide demand for industrial resins and high-tech coating materials. This will strengthen the supply chain of derivatives of aromatic monomers.

- LG Chem -September 2024: LG Chem announced a strategic R&D on high-performance polymer materials and next-generation coating chemistry to enhance the longevity and heat resistance of their products in addition to their functionality in industrial use.

All these developments have indicated that the industry is well oriented towards specialty polymer development, improving production productivity and increasing the availability of supplies of the vinyl toluene chemical application across the globe.

The Vinyl Toluene Market is segmented as follows:

By Grade Type

- Standard Grade

- High-Purity Grade

- Specialty Grade

By Isomer Composition

- Meta-Vinyl Toluene

- Para-Vinyl Toluene

- Mixed Isomer Vinyl Toluene

By Formulation Type

- Monomer Formulations

- Modified Resin Systems

- Copolymer Blends

By End-Use Industry

- Paints & Coatings Industry

- Adhesives & Sealants Industry

- Printing Inks Industry

- Composite Materials Industry

- Chemical Intermediate Manufacturing

By Functionality

- Reactive Diluent Applications

- Crosslinking Agent Usage

- Polymer Intermediate Applications

By Distribution Channel

- Direct Manufacturer Supply

- Specialty Chemical Distributors

- B2B Chemical Procurement Platforms

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Vinyl Toluene by Segments

- 2.1.2. Vinyl Toluene by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Vinyl Toluene Market Attractiveness Analysis, By Grade Type

- 2.2.3. Vinyl Toluene Market Attractiveness Analysis, By Isomer Composition

- 2.2.4. Vinyl Toluene Market Attractiveness Analysis, By Formulation Type

- 2.2.5. Vinyl Toluene Market Attractiveness Analysis, By End-Use Industry

- 2.2.6. Vinyl Toluene Market Attractiveness Analysis, By Functionality

- 2.2.7. Vinyl Toluene Market Attractiveness Analysis, By Distribution Channel

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Rising Demand for High-Performance Resins and Composites

- 3.1.2. Coatings and Polymer Innovation

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Vinyl Toluene Market – By Grade Type

- 4.1. Grade Type Market Overview, By Grade Type Segment

- 4.1.1. Vinyl Toluene Market Revenue Share, By Grade Type, 2025 & 2035

- 4.1.2. Standard Grade

- 4.1.3. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. High-Purity Grade

- 4.1.7. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Specialty Grade

- 4.1.11. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Grade Type Market Overview, By Grade Type Segment

- Chapter 5. Vinyl Toluene Market – By Isomer Composition

- 5.1. Isomer Composition Market Overview, By Isomer Composition Segment

- 5.1.1. Vinyl Toluene Market Revenue Share, By Isomer Composition, 2025 & 2035

- 5.1.2. Meta-Vinyl Toluene

- 5.1.3. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Para-Vinyl Toluene

- 5.1.7. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Mixed Isomer Vinyl Toluene

- 5.1.11. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Isomer Composition Market Overview, By Isomer Composition Segment

- Chapter 6. Vinyl Toluene Market – By Formulation Type

- 6.1. Formulation Type Market Overview, By Formulation Type Segment

- 6.1.1. Vinyl Toluene Market Revenue Share, By Formulation Type, 2025 & 2035

- 6.1.2. Monomer Formulations

- 6.1.3. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Modified Resin Systems

- 6.1.7. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Copolymer Blends

- 6.1.11. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Formulation Type Market Overview, By Formulation Type Segment

- Chapter 7. Vinyl Toluene Market – By End-Use Industry

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 7.1.1. Vinyl Toluene Market Revenue Share, By End-Use Industry, 2025 & 2035

- 7.1.2. Paints & Coatings Industry

- 7.1.3. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Adhesives & Sealants Industry

- 7.1.7. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Printing Inks Industry

- 7.1.11. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Composite Materials Industry

- 7.1.15. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Chemical Intermediate Manufacturing

- 7.1.19. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 8. Vinyl Toluene Market – By Functionality

- 8.1. Functionality Market Overview, By Functionality Segment

- 8.1.1. Vinyl Toluene Market Revenue Share, By Functionality, 2025 & 2035

- 8.1.2. Reactive Diluent Applications

- 8.1.3. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 8.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.5. Key Market Trends, Growth Factors, & Opportunities

- 8.1.6. Crosslinking Agent Usage

- 8.1.7. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 8.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.9. Key Market Trends, Growth Factors, & Opportunities

- 8.1.10. Polymer Intermediate Applications

- 8.1.11. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 8.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.13. Key Market Trends, Growth Factors, & Opportunities

- 8.1. Functionality Market Overview, By Functionality Segment

- Chapter 9. Vinyl Toluene Market – By Distribution Channel

- 9.1. Distribution Channel Market Overview, By Distribution Channel Segment

- 9.1.1. Vinyl Toluene Market Revenue Share, By Distribution Channel, 2025 & 2035

- 9.1.2. Direct Manufacturer Supply

- 9.1.3. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 9.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 9.1.5. Key Market Trends, Growth Factors, & Opportunities

- 9.1.6. Specialty Chemical Distributors

- 9.1.7. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 9.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 9.1.9. Key Market Trends, Growth Factors, & Opportunities

- 9.1.10. B2B Chemical Procurement Platforms

- 9.1.11. Vinyl Toluene Share Forecast, By Region (USD Billion)

- 9.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 9.1.13. Key Market Trends, Growth Factors, & Opportunities

- 9.1. Distribution Channel Market Overview, By Distribution Channel Segment

- Chapter 10. Vinyl Toluene Market – Regional Analysis

- 10.1. Vinyl Toluene Market Overview, By Region Segment

- 10.1.1. Global Vinyl Toluene Market Revenue Share, By Region, 2025 & 2035

- 10.1.2. Global Vinyl Toluene Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 10.1.3. Global Vinyl Toluene Market Revenue, By Grade Type, 2026 – 2035

- 10.1.4. Global Vinyl Toluene Market Revenue, By Isomer Composition, 2026 – 2035

- 10.1.5. Global Vinyl Toluene Market Revenue, By Formulation Type, 2026 – 2035

- 10.1.6. Global Vinyl Toluene Market Revenue, By End-Use Industry, 2026 – 2035

- 10.1.7. Global Vinyl Toluene Market Revenue, By Functionality, 2026 – 2035

- 10.1.8. Global Vinyl Toluene Market Revenue, By Distribution Channel, 2026 – 2035

- 10.2. North America

- 10.2.1. North America Vinyl Toluene Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 10.2.2. North America Vinyl Toluene Market Revenue, By Grade Type, 2026 – 2035

- 10.2.3. North America Vinyl Toluene Market Revenue, By Isomer Composition, 2026 – 2035

- 10.2.4. North America Vinyl Toluene Market Revenue, By Formulation Type, 2026 – 2035

- 10.2.5. North America Vinyl Toluene Market Revenue, By End-Use Industry, 2026 – 2035

- 10.2.6. North America Vinyl Toluene Market Revenue, By Functionality, 2026 – 2035

- 10.2.7. North America Vinyl Toluene Market Revenue, By Distribution Channel, 2026 – 2035

- 10.2.8. U.S. Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.2.9. Canada Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.2.10. Mexico Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.2.11. Rest of North America Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.3. Europe

- 10.3.1. Europe Vinyl Toluene Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 10.3.2. Europe Vinyl Toluene Market Revenue, By Grade Type, 2026 – 2035

- 10.3.3. Europe Vinyl Toluene Market Revenue, By Isomer Composition, 2026 – 2035

- 10.3.4. Europe Vinyl Toluene Market Revenue, By Formulation Type, 2026 – 2035

- 10.3.5. Europe Vinyl Toluene Market Revenue, By End-Use Industry, 2026 – 2035

- 10.3.6. Europe Vinyl Toluene Market Revenue, By Functionality, 2026 – 2035

- 10.3.7. Europe Vinyl Toluene Market Revenue, By Distribution Channel, 2026 – 2035

- 10.3.8. Germany Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.3.9. France Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.3.10. U.K. Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.3.11. Russia Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.3.12. Italy Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.3.13. Spain Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.3.14. Netherlands Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.3.15. Rest of Europe Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.4. Asia Pacific

- 10.4.1. Asia Pacific Vinyl Toluene Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 10.4.2. Asia Pacific Vinyl Toluene Market Revenue, By Grade Type, 2026 – 2035

- 10.4.3. Asia Pacific Vinyl Toluene Market Revenue, By Isomer Composition, 2026 – 2035

- 10.4.4. Asia Pacific Vinyl Toluene Market Revenue, By Formulation Type, 2026 – 2035

- 10.4.5. Asia Pacific Vinyl Toluene Market Revenue, By End-Use Industry, 2026 – 2035

- 10.4.6. Asia Pacific Vinyl Toluene Market Revenue, By Functionality, 2026 – 2035

- 10.4.7. Asia Pacific Vinyl Toluene Market Revenue, By Distribution Channel, 2026 – 2035

- 10.4.8. China Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.4.9. Japan Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.4.10. India Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.4.11. New Zealand Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.4.12. Australia Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.4.13. South Korea Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.4.14. Taiwan Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.4.15. Rest of Asia Pacific Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.5. The Middle-East and Africa

- 10.5.1. The Middle-East and Africa Vinyl Toluene Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 10.5.2. The Middle-East and Africa Vinyl Toluene Market Revenue, By Grade Type, 2026 – 2035

- 10.5.3. The Middle-East and Africa Vinyl Toluene Market Revenue, By Isomer Composition, 2026 – 2035

- 10.5.4. The Middle-East and Africa Vinyl Toluene Market Revenue, By Formulation Type, 2026 – 2035

- 10.5.5. The Middle-East and Africa Vinyl Toluene Market Revenue, By End-Use Industry, 2026 – 2035

- 10.5.6. The Middle-East and Africa Vinyl Toluene Market Revenue, By Functionality, 2026 – 2035

- 10.5.7. The Middle-East and Africa Vinyl Toluene Market Revenue, By Distribution Channel, 2026 – 2035

- 10.5.8. Saudi Arabia Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.5.9. UAE Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.5.10. Egypt Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.5.11. Kuwait Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.5.12. South Africa Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.5.13. Rest of the Middle East & Africa Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.6. Latin America

- 10.6.1. Latin America Vinyl Toluene Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 10.6.2. Latin America Vinyl Toluene Market Revenue, By Grade Type, 2026 – 2035

- 10.6.3. Latin America Vinyl Toluene Market Revenue, By Isomer Composition, 2026 – 2035

- 10.6.4. Latin America Vinyl Toluene Market Revenue, By Formulation Type, 2026 – 2035

- 10.6.5. Latin America Vinyl Toluene Market Revenue, By End-Use Industry, 2026 – 2035

- 10.6.6. Latin America Vinyl Toluene Market Revenue, By Functionality, 2026 – 2035

- 10.6.7. Latin America Vinyl Toluene Market Revenue, By Distribution Channel, 2026 – 2035

- 10.6.8. Brazil Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.6.9. Argentina Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.6.10. Rest of Latin America Vinyl Toluene Market Revenue, 2026 – 2035 (USD Billion)

- 10.1. Vinyl Toluene Market Overview, By Region Segment

- Chapter 11. Competitive Landscape

- 11.1. Company Market Share Analysis – 2025

- 11.1.1. Global Vinyl Toluene Market: Company Market Share, 2025

- 11.2. Global Vinyl Toluene Market Company Market Share, 2024

- 11.1. Company Market Share Analysis – 2025

- Chapter 12. Company Profiles

- 12.1. INEOS

- 12.1.1. Company Overview

- 12.1.2. Key Executives

- 12.1.3. Product Portfolio

- 12.1.4. Financial Overview

- 12.1.5. Operating Business Segments

- 12.1.6. Business Performance

- 12.1.7. Recent Developments

- 12.2. BASF

- 12.3. Dow Inc.

- 12.4. LyondellBasell

- 12.5. Eastman Chemical Company

- 12.6. Arkema

- 12.7. Evonik Industries

- 12.8. SABIC

- 12.9. Formosa Plastics Corporation

- 12.10. Mitsubishi Chemical Group

- 12.11. Sumitomo Chemical

- 12.12. LG Chem

- 12.13. Others.

- 12.1. INEOS

- Chapter 13. Research Methodology

- 13.1. Research Methodology

- 13.2. Secondary Research

- 13.3. Primary Research

- 13.3.1. Analyst Tools and Models

- 13.4. Research Limitations

- 13.5. Assumptions

- 13.6. Insights From Primary Respondents

- 13.7. Why Custom Market Insights

- Chapter 14. Standard Report Commercials & Add-Ons

- 14.1. Customization Options

- 14.2. Subscription Module For Market Research Reports

- 14.3. Client Testimonials

List Of Figures

Figures No 1 to 42

List Of Tables

Tables No 1 to 61

Prominent Player

- INEOS

- BASF

- Dow Inc.

- LyondellBasell

- Eastman Chemical Company

- Arkema

- Evonik Industries

- SABIC

- Formosa Plastics Corporation

- Mitsubishi Chemical Group

- Sumitomo Chemical

- LG Chem

- Others

FAQs

The key players in the market are INEOS, BASF, Dow Inc., LyondellBasell, Eastman Chemical Company, Arkema, Evonik Industries, SABIC, Formosa Plastics Corporation, Mitsubishi Chemical Group, Sumitomo Chemical, LG Chem, Others.

The market of Vinyl Toluene is highly affected by government regulations. The environmental policies that favor the production of low-VOC chemicals and the standards of emission and sustainability programs are motivating manufacturers to use cleaner chemical processes. The chemical safety regulations and standards of transportation and manufacturing emissions to the industries are hastening the production of advanced polymer chemistry solutions. The use of green manufacturing and sustainable chemical production with government incentives is also contributing to the growth of markets in the long run.

Price positioning and production cost are important aspects of market adoption. Vinyl toluene materials of high purity and specialty grade demand rigorous purification and processing technology, which makes them more expensive than the typical ones. Nonetheless, the investment is warranted by industrial users because of long-term operating efficiency, better performance of the product, and more durability traits. Economies of scale in terms of mass production and streamlining of the supply chain are assisting in enhancing market accessibility.

The value of the global Vinyl Toluene market is likely to be about USD 30.3 billion in the year 2035 with a CAGR of 5.9% in the period 2026-2035. The growth of the market will be enabled by the growing needs in terms of specialty polymers, advanced resin systems, and high-performance coating materials. The long-term market development will be maintained by growth in construction activities, manufacturing in industries, and the use of composite material.

Asia Pacific will take over the global Vinyl Toluene market in terms of revenue share. The area has the advantage of a high capacity for chemical production, polymer production industries, and fast urban infrastructure development. The other major consumers comprise countries like China, South Korea, Japan, and India because of growth in automotive production, construction material, and industrial coatings production. The regional leadership is also being enhanced by the government promoting industrial modernization and growth in foreign investments in chemical production plants.

It is also anticipated that Europe will experience the greatest CAGR over the forecast period 2026 – 2035 because of the stringent environmental policies, high levels of sustainability efforts, and increasing demand for low-VOC coatings and specialty polymer materials. The Netherlands, Germany, and France are investing a great deal in new technology for manufacturing chemicals and sustainable resin. Market growth in the region is further increasing because of the strong R&D efforts in specialty materials and increasing use of high-performance industrial coatings.

The Vinyl Toluene market worldwide will be growing at a very fast rate since the demand is ever-growing for high-performance polymers, specialty coatings, and sophisticated composite materials in the industrial field. Consumption of vinyl toluene based resins and chemical intermediates is accelerated by rapid growth of construction, automotive manufacturing, and infrastructure development. Growing investments in the production of specialty chemicals, growth in technology to modify polymers, and growing demand for light and durable materials further contribute to the growth of the market. Market adoption is also accelerating because of increased industrialization among emerging economies and increased supply chains to support the global chemical industries.