Carton Packaging Market Size, Trends and Insights By Product Type (Folding Cartons, Reverse Tuck End (RTE) Cartons, Straight Tuck End (STE) Cartons, Auto Bottom Cartons, Sleeve Cartons, Shelf-Ready Cartons, Gable Top Cartons, Standard Gable Top Cartons, Extended Shelf Life (ESL) Gable Top, Reclosable Gable Top Cartons, Brick Liquid Cartons, Standard Brick Cartons, Slim and Square Brick Variants, Aseptic Cartons, Standard Aseptic Brick Cartons, Aseptic Cartons with Closure Systems, Aluminum-Free Aseptic Cartons, Other Product Types, Wedge-Shaped Cartons, Shaped Premium Cartons), By Material (Paperboard, Solid Bleached Sulfate (SBS), Coated Unbleached Kraft (CUK), Recycled Paperboard (CRB), Folding Boxboard (FBB), Liquid Packaging Board, Virgin Fiber Liquid Packaging Board, Bio-Based Barrier Coated Board, Cartonboard, Chromoboard, Graphoboard, Other Materials), By Printing Technology (Offset Printing, Flexographic Printing, Digital Printing, Gravure Printing, Other Printing Technologies, Screen Printing, Inkjet Coding & Marking), By End Use Industry (Food & Beverage, Dry Food & Cereals, Liquid Food & Juices, Confectionery & Snacks, Frozen Food, Dairy Products, Fresh Milk & Cream, UHT Milk & Dairy Beverages, Yogurt & Fermented Dairy, Cheese & Butter, Healthcare & Pharmaceuticals, Prescription Medicines, OTC Healthcare Products, Medical Devices Packaging, Personal Care & Cosmetics, Skincare & Hair Care, Fragrances & Premium Cosmetics, Household Products, Detergents & Cleaning Products, Home Care Packaging, Other End Use Industries), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 5%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | LAMEA |

| Largest Market: | Asia Pacific |

Major Players

- WestRock Company

- Smurfit Kappa Group

- Mondi Group

- DS Smith plc

- Others

Reports Description

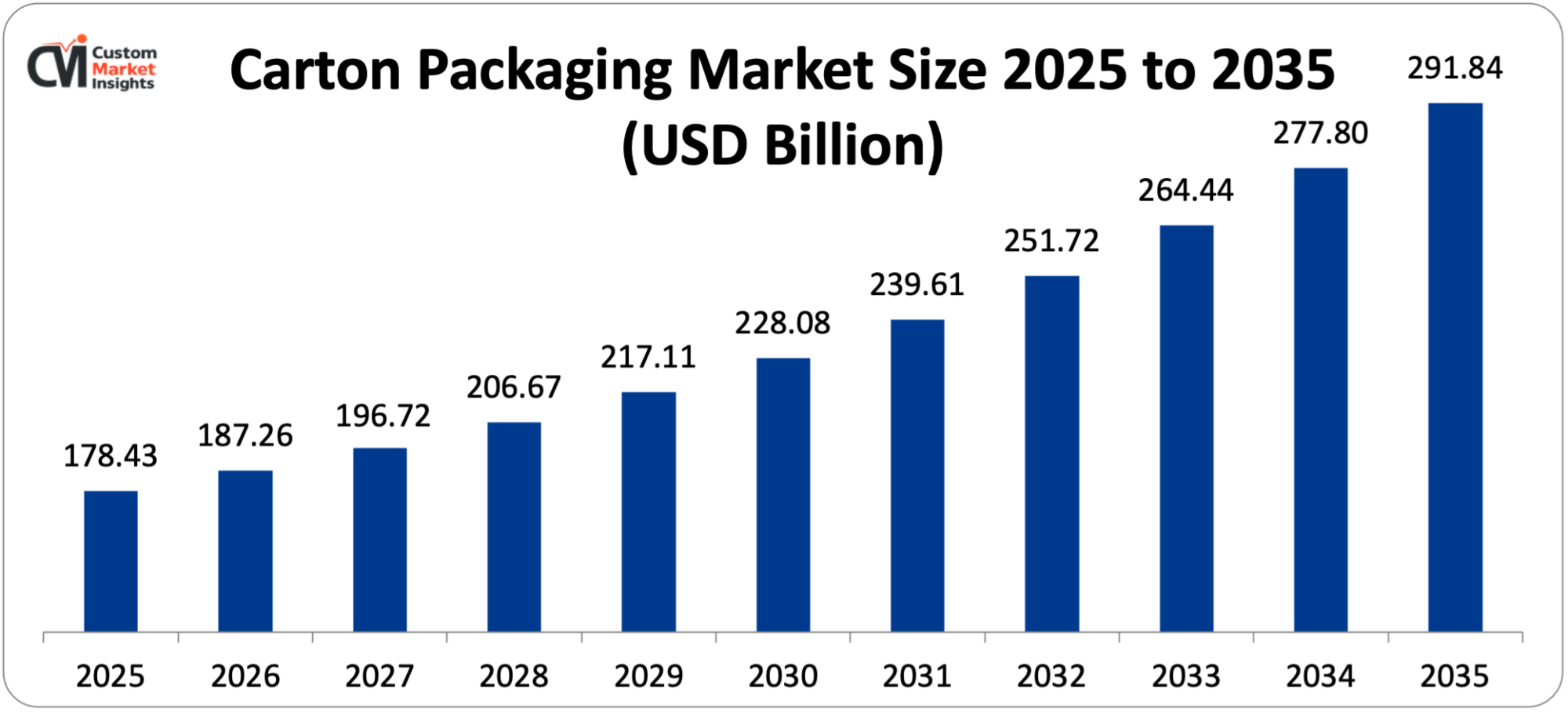

The carton packaging market is estimated to reach USD 178.43 billion by 2025 and is expected to grow from USD 187.26 billion in 2026 to USD 291.84 billion by 2035 at 5% CAGR from 2026 to 2035.

Market Highlight

- Asia Pacific dominated the carton packaging market with a 39% market share in 2025, supported by the fact that Asia Pacific is home to the world’s largest food and beverage manufacturing and consumption region, with China, India, Japan, and Southeast Asia witnessing a rapid growth in organized retail, which is demanding carton packaging solutions that can be used as shelf-ready packaging, and the extraordinary growth of liquid food and dairy consumption driving the carton packaging market in Asia Pacific.

- Europe is anticipated to continue to have the second largest market share at 26% in 2025, and is the home of the most advanced packaging regulatory framework requiring renewable and recyclable packaging, the highest per-capita carton packaging consumption in the world, and the center of global carton packaging technology innovation and manufacturing leadership.

- Folding cartons accounted for around 47% of market value in 2025, having taken the majority of the market share; as the most versatile, widely used, and cost-effective carton format, folding carton is consumed in food, pharmaceutical, personal care, and consumer goods applications all over the world.

- By product type, aseptic cartons are projected to grow at the highest CAGR of 6.8% between 2026 and 2035 with the need to offer market opportunities that are not possible by conventional refrigerated carton packaging, as the markets of Asia Pacific and LAMEA are experiencing tremendous growth in the consumption of liquid food and dairy goods, which places a significant strain on the cold chain infrastructure.

- Food and beverage accounted for the largest share of 52% in 2025, making it the leading carton packaging consumption category for dry food, liquid food, dairy, juice and convenience food applications as the predominant end use industry worldwide.

- The healthcare and pharmaceuticals segment will grow at a 6.3% CAGR during 2026-2035, owing to the proliferation of pharmaceutical products, increased OTC consumption of healthcare products and anti-counterfeiting serialization and smart carton technology in the pharmaceutical supply chain.

Impact of Middle East War on Carton Packaging Market

As a result of the Middle East war, the carton packaging industry faces rising logistics and freight expenses in addition to increasing expenses of paper and pulp manufacturing plants due to elevated energy costs. The disruption of shipments through primary shipping routes has slowed down international metal delivery supply chains. On the other hand, increased demand for packaged foods and necessities is driven by geopolitics and contributes positively to market demand.

Significant Growth Factors

The Carton Packaging Market Trends present significant growth opportunities due to several factors:

- Accelerating Plastic-to-Carton Substitution Driven by Regulatory Mandates and Consumer Sustainability Expectations Across Multiple Consumer Goods Categories: The fastest growing market and most commercially viable growth potential in carton packaging is the global shift from petroleum-based plastics to renewable, recyclable and fiber-based carton packaging, as the shift is supported by quickly increasing regulatory restrictions on certain plastic packaging formats, commitment from many consumer goods brands to reduce the amount of plastic packaging used in their product offerings, and the consumer preference for purchasing products packed in materials that are perceived as environmentally responsible. The European Union’s Packaging and Packaging Waste Regulation — which is set to be fully implemented by 2030 with its intention for all packaging to become reusable, recyclable or compostable — explicitly calls for the shift from plastic to other packaging formats in categories where carton packaging is the commercially most viable plastic-free alternative, such as dry food outer packaging, beverage multipacks, personal care outer cartons and healthcare product packaging. The EU Single-Use Plastics Directive has already banned certain single-use plastic formats, such as food containers and beverage cups where alternatives like carton and fiber are technically possible, thus creating immediate displacement demand for carton packaging manufacturers. SB 54 in California mandates a 30% recycled content target for single-use plastic packaging by 2028 with the%age increasing in stages until 2032; many state jurisdictions are enacting plastic packaging taxes; and these financial incentives are prompting brand owners to switch to carton packaging for specific product categories. The UK Plastic Packaging Tax (GBP 200 per tonne for packaging containing less than 30% recycled content) has helped drive U.K. brand owner decisions to switch to carton packaging – which can be made with sustainable ingredients and offers consumers the renewable material and recyclability they value, without triggering the tax. The opportunity to substitute plastic with carton is very large, – the global FOB value of the rigid plastic containers market alone is around USD 180 billion and even the partial penetration of this market by carton alternatives – as a result of regulatory requirements, brand sustainable commitments, and consumer preferences – will constitute an incremental carton packaging demand opportunity above the baseline growth of the market. Many of the world’s leading consumer goods companies such as Nestlé, Unilever, Procter & Gamble, and Danone have made clear pledges to phase out certain plastic packaging formats by 2025-2030 with carton packaging emerging as a key platform of change and a significant potential replacement across multiple product categories, with food manufacturers making procurement transitions from plastic to carton packaging in their global supply chains.

- Aseptic Carton Technology Enabling Ambient Liquid Food Distribution in Cold Chain-Limited Emerging Markets: The unmatched commercial advantages of aseptic carton packaging – filling liquid foods such as milk, juice, soups, creams and plant food beverages into sterile, multiple-layer cartons while operating in an aseptic environment and therefore achieving ambient shelf stability of 6-12 months without refrigeration – are gradually being realised in Asia Pacific, Latin America, the Middle East, and Africa, where cold chain infrastructure constraints, high cold chain costs and the economic viability of ambient shelf-stable liquid nutrition are creating structural demand for the new aseptic packaging format to enable market development that would not be possible with liquid food packaged in conventional refrigerated formats. The global UHT milk market is the largest of all, accounting for around 35% of all liquid milk production, and is growing at a fast pace, ranging from well over 95% of milk produced sold in UHT carton format in some European markets such as Spain, France and Portugal, to under 10% in others, such as the USA and Australia, where consumer preference has a strong preference for refrigerated pasteurized milk. The proportion of milk sold in UHT carton boxes is hugely variable by country, and in most emerging markets is the commercial alternative for most consumers in most areas of the country to fresh milk because the cold chain is unreliable. In 2024, the global UHT milk market was valued at around USD 196 billion and is expected to reach USD 284 billion by 2030, the major growing region being the Asia Pacific, especially China, India, and the Southeast Asian countries, where growing incomes allow for increased demand for dairy products and the cold chain can support aseptic packing over refrigerated packing.

What are the Major Advances Changing the Carton Packaging Market Today?

- Advanced Barrier Technology Innovation Enabling Plastic-Free and Reduced-Plastic Liquid Carton Constructions: The most significant technology development affecting liquid carton packaging was the systematic development and commercialization of bio-based and mineral-based barrier coating technologies that offer equivalent liquid barrier, heat seal, and processing performance to the thin PE extrusion coating (usually in the range of 15–30 grams per square meter) currently used on the exterior and interior surfaces of liquid carton board packages, but with minimal or no plastic in the barrier layer. Historically, the PE-paper laminate separation that must take place in liquid carton repulping is the major source of complexity and cost that has hindered the recovery of liquid carton fibre in most national recycling systems, and the polyethylene extrusion coating (15-25% of total carton weight) is the primary barrier to making a liquid carton conventional. The aqueous barrier coatings, which are based on polyvinyl alcohol (PVA), starch derivatives, biopolymer dispersions and nanocellulose composites, have been developed and are commercialised by companies such as Tetra Pak, Billerud, Iggesund Paperboard and Sappi, among others, to obtain the water vapor transmission rate, oil and grease resistance and heat seal properties necessary for the packaging of fresh and ambient liquid food cartons without polyethylene extrusion. Tetra Pak’s pioneering Plant-based Tetra Brik Aseptic carton is a first step that meets renewable material credentials but still possesses the same processing and recyclability characteristics, while the company’s future plans are for 100% fiber-based and aluminum-free liquid cartons, with advanced bio-based barrier systems, making them fully recoverable in mainstream paper recycling. The commercial introduction of water-based barrier coatings for gable top fresh dairy cartons is progressing quickly and several European dairy companies have begun offering PE-free liquid carton packaging, putting their brands at the forefront of sustainable liquid carton packaging innovation, such as Oatly, Arla Foods, and Alpro. The aluminum foil layer, which is a critical component in the conventional aseptic liquid carton construction is also where Tetra Pak’s LightCap carton and SIG’s combiCraft aluminum-free aseptic carton have shown that it is possible to achieve the same level of oxygen barrier as aluminum foil in liquid carton applications, but with a better recyclability in the paper recovery streams, by replacing aluminum foil with polymer layers.

- Digital Printing Technology Enabling Mass Customization, Short-Run Flexibility, and Retail Channel Differentiation on Carton Packaging: As fast speed digital inkjet and electrophotographic printing technologies have continued to develop and become commercially available, with the ability to print at production speed on carton board substrates, the commercial and creative flexibility that brand owners could specify in carton packaging is changing rapidly — with short-run production, personalized packaging, regionally variant execution, and new product development cycles that would have been economically prohibitive with the conventional flexographic and offset printing economics of large minimum orders and long make-ready times. Conventional folding carton printing, which is mostly flexographic and offset based, with pre-engraved or pre-made printing plates, has a high capital cost per fold test design, requires order quantities of 50,000–500,000 cartons, and limits the number of colour variants, design refresh cycles and the ability to create packaging that is suited to local markets. With minimum order quantities between 1,000 and 5,000 cartons, without any investment in plates, digital carton printing using UV inkjet systems from various manufacturers such as HP PageWide, Durst, or EFI Nozomi and at production speeds between 75 and 100 m/min on carton board substrates, it offers brand owners commercially viable short-run production for market testing, the launch of limited edition packaging, event-specific packaging, and region-specific customization programs. The global digital packaging printing market is expected to witness a growth rate of approximately 12.3% CAGR till 2030 with carton packaging being the largest single application due to the high value of carton packaging per unit, as compared to flexible packaging, as well as the high commercial value of digital packaging in the most demanding carton applications, which are driven by a proliferation of variants and serialization requirements. A major incentivizing force for digital carton printing is the ability to print a unique 2D matrix code and serial number on every carton, as required by pharmaceutical serialization standards, such as the EU Falsified Medicines Directive 2011/62/EU and the equivalent standard in the United States, Saudi Arabia, Turkey, and many other markets; the variable data printing capability of digital systems allows for 2D matrix code and serial number printing at the individual carton level, with no incremental cost per variable data element compared to the engineering complexity of incorporating variable data into conventional printing methods.

- Sustainable Fiber Sourcing and Circular Economy Cartonboard Production Strengthening the Environmental Credentials of Carton Packaging: As key carton packaging producers increasingly shift towards verified sustainable fiber sourcing, more recycled fiber usage, reduction in water and energy consumption in cartonboard production, and development of closed-loop fiber recovery infrastructure, carton packaging producers are making better progress towards carton packaging at the material level earning better environmental credentials — complementing claims of recyclability and renewable origin made at the consumer-facing packaging level — and substantiating comprehensive lifecycle carbon footprint advantages over plastic alternatives through audited supply chain data. The presence of Forest Stewardship Council (FSC) and Programme for the Endorsement of Forest Certification (PEFC) certified virgin wood fibre in cartonboard production, which confirms that virgin wood fibre comes from sustainably managed forests in which regeneration, biodiversity protection and community impact requirements are met, has become a de facto market access requirement for carton packaging sold into European and North American consumer goods supply chains and major carton converters report FSC or PEFC certified sourcing rates of more than 90% of virgin wood fibre. The recycled fiber content of carton packaging is steadily rising; applications such as liquid food or pharmaceuticals, which are subject to high food contact safety standards are still in the main using virgin bleached kraft fibre to meet the purity specification of preventing possible migration of contaminants from recycled fibre to the food; dry food outer carton packaging, retail shelf ready cartons and secondary packaging corrugated elements are progressively raising the recycling content targets to 80-100%, as the technology and safety standards of recycled fiber cleaning and bleaching further enhance the optical and structural properties of high-recycled content cartonboard.

Category Wise Insights

By Product Type

Why Do Folding Cartons Lead the Carton Packaging Market?

Folding cartons are the biggest product type share in 2025, with around 47% of market revenues. This dominance is the result of folding cartons’ unparalleled versatility in end use applications – being the dominant outer packaging format for dry breakfast cereals, frozen foods, confectionery, pharmaceutical medicines, personal care products, household detergents and consumer electronics in almost every consumer goods retail category – and the most mature and widely distributed converting infrastructure of any carton format. The most widely spread carton making capability in the world is folding carton production, where converting facilities are operated by regional or local carton converters as well as by the multinational carton integrated producing companies, applying well-known carton die-cutting, scoring, gluing and printing technologies that are available to these carton converters as well. In 2024, an estimated 22.5 million metric tonnes of cartonboard were used in the global folding carton market, of which packaging applications in the food and beverage sector accounted for about 42% of cartonboard consumption, the pharmaceutical sector about 16%, the personal care sector about 14%, and the household products and other consumer goods sector about 28% of cartonboard consumption. The food dry packaging sub-segment—which includes breakfast cereal cartons, cracker and cookie boxes, cake mix cartons, pasta packaging, and frozen food outer cartons—is the largest single application of folding carton products; for example, Kellogg’s, General Mills, Nestlé Cereals, and Post Holdings are all expected to use about 180,000 metric tons of breakfast cereal cartons alone annually. The structural strength, printing capabilities, shelf stability and consumer convenience benefits of folding carton packaging with reclosable features, clear windows and easy-open perforations.

By Material

Why Does Paperboard Lead the Material Segment?

Paperboard is the largest material segment with sales of around 58% of the total sales due to its dominant position in folding carton packaging applications in the food, pharmaceutical, personal care, and consumer goods sectors. High printing surface quality, high brightness, and superior food contact safety of paper materials make Solid Bleached Sulfate (SBS) paperboard the material of choice for premium food, pharmaceutical and cosmetic folding cartons where requirements for quality dictate material specification toward the highest grade cartonboard. Consumer goods folding carton applications demand the highest volume individual cartonboard grade, the Folding Boxboard (FBB), which is a multilayer cartonboard consisting of a bleached chemical pulp outer layer, a mechanical pulp middle layer and a bleached chemical pulp inner layer. Liquid Packaging Board, a specially designed multi-ply paperboard with improved dimensional stability and moisture resistance and superior ability to be coated with barriers, is the second largest material market at 27% of the market revenue and is used in the gable top, aseptic and brick carton liquid food packaging markets, which represent the highest value application of liquid cartons. The bio-based barrier coated board sub-segment in liquid packaging board is the fastest growing material innovation in liquid carton production at around 15.3% CAGR, as carton manufacturers are introducing and commercializing PE-free barrier-coated board that will allow liquid cartons to be recycled in mainstream paper recycling streams.

By Printing Technology

Why Does Offset Printing Lead the Carton Printing Technology Segment?

Offset printing is also the biggest printing technology segment that is expected to occupy around 38% of carton packaging printing revenue in 2025. The offset lithographic method uses an aluminum flat printing plate to transfer ink onto a rubber offset blanket and then onto the carton’s paperboard printing substrate to produce the highest quality printing of any commercial carton printing method, with fine dot control, smooth gradations and color consistency required for high-quality carton graphics that demand photographic image quality and Pantone color reproduction. However, the market is also primarily dominated by offset printing for pharmaceutical, premium food, luxury cosmetics and spirit carton applications where brand equity, consumer trust and regulatory compliance dictate the label quality requirements, which makes offset more expensive for the shorter run length and thus less competitive. Flexographic printing is the second largest technology at 29% of market revenue, covering applications such as gable top and aseptic carton printing, in which Tetra Pak, SIG Combibloc and Elopak are running proprietary high-speed flexographic printing systems incorporated into their liquid carton board converting and filling machine infrastructure. Pharmaceutical serialization requirements, the launch of premium food and beverage brands on a short-run basis, seasonal promotional campaigns and the increasing e-commerce direct-to-consumer packaging market where per-unit economics and design flexibility requirements increasingly sway digital printing processes over conventional plate-based processes are driving digital printing to become the fastest growing printing technology with a CAGR of 12.3% through 2035. The lower cost per meter (CPCM) of digital printing, especially with some of the world’s leading HP PageWide industrial digital printing systems becoming cost competitive with medium-run offset production around 50,000-80,000 square meters per print run (PPM), is extending the usage range of digital printing beyond traditionally digital print applications, such as short-run production and variable data, into medium-run carton production for mainstream consumer goods applications.

By End Use Industry

Why Does Food and Beverage Dominate the Carton Packaging End Use Landscape?

Food and beverage accounts for approximately 52% of total carton packaging market revenue in 2025, reflecting the fundamental role of carton packaging as the primary outer and primary packaging format across the enormous and continuously growing global food and beverage manufacturing sector. The food and beverage carton packaging market encompasses the extraordinary breadth of applications from ambient dry food folding cartons through refrigerated gable top liquid food cartons to ambient aseptic brick cartons — a range that collectively ensures carton packaging is present across virtually every food product category in every geographic market globally. The breakfast cereal category — with a global market value of approximately USD 65 billion — is one of the most carton-packaging-dependent food categories globally, with the standard paperboard folding carton being the universal primary packaging format for boxed cereal across all major producing markets. The frozen food carton market — growing at approximately 6.1% CAGR driven by the expanding globally traded frozen meal, frozen seafood, and frozen vegetable markets — is an important and growing folding carton consumption segment, with carton packaging providing the structural integrity for stack storage in frozen distribution, the printing surface for regulatory and nutritional labeling compliance, and the consumer convenience features that drive purchase decisions in competitive frozen food retail environments.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 187.26 billion |

| Projected Market Size in 2035 | USD 291.84 billion |

| Market Size in 2025 | USD 178.43 billion |

| CAGR Growth Rate | 5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Product Type, Material, Printing Technology, End Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

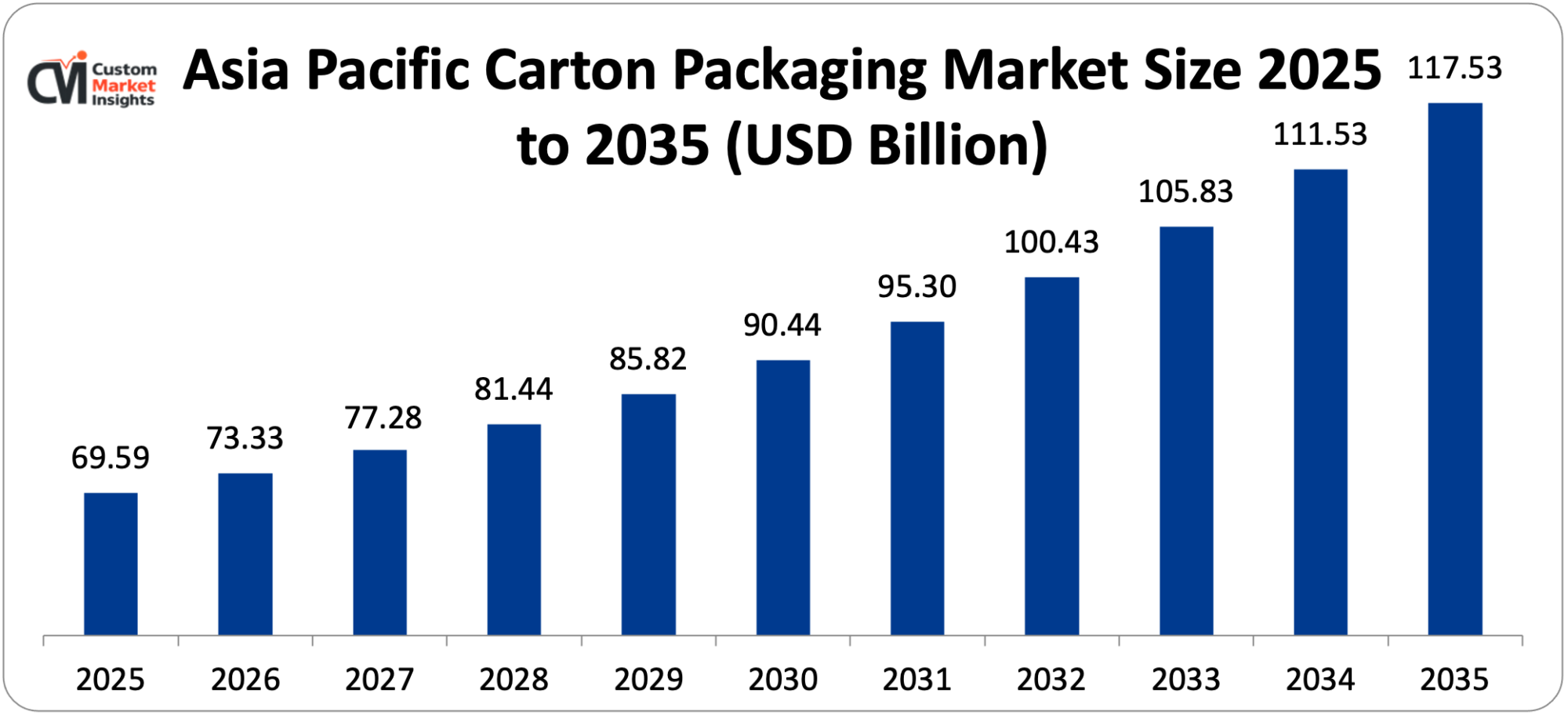

The Asia Pacific carton packaging market size is estimated at USD 69.59 billion in 2025 and is projected to reach approximately USD 117.53 billion by 2035, growing at a CAGR of 5.4% from 2026 to 2035.

Why did Asia Pacific Dominate the Market in 2025?

Asia Pacific is expected to account for around 39% of global carton packaging market revenue in 2025 owing to the region being the largest base for food and beverages, the fastest-growing organized retail sector that requires shelf-ready carton solutions, the largest market for liquid foods and UHT dairy products that is driving huge demand for aseptic carton packaging, and the most dynamic pharmaceutical and personal care manufacturing base consuming folding carton packaging.

The largest national carton packaging market by volume in the world is China, and carton consumption across all packaging formats is estimated at more than 3.8 million metric tons per annum, fuelled by the largest packaged food industry in the world, the world’s second largest pharmaceutical market consuming folding cartons in significant volume, a huge personal care manufacturing industry and the world’s largest UHT milk consumption market served mainly by aseptic brick carton packaging from Tetra Pak, SIG Combibloc and domestic carton manufacturers.

India is the most dynamically growing carton market in APAC, where the carton packaging market is expected to expand at around 8.1% CAGR, owing to the exceptional growth in organized grocery retail penetration (from around 12% of food retail in 2019, to an estimated 22% by 2025), carton consumption by the rapidly expanding pharmaceutical manufacturing market for medicine packaging, and carton consumption in the growing dairy processing market, which is moving from bulk and loose purchased milk towards packaged gable top and aseptic carton formats.

Within Asia Pacific, two markets stand out for their technical maturity – Japan and South Korea, and consumer requirements for superior print, value-added structural carton formats and added convenience features such as ease of opening via perforations or closures and ergonomic shapes drive continuous product innovation and premium pricing, which results in a significant share of revenue from these products, compared to volume.

Why is Europe the Second-Largest and Most Technically Advanced Market?

Europe accounts for around 26% of global market revenue of carton packaging in 2025, estimated at around USD 46.39 billion, and is characterized by the highest per-capita carton packaging consumption of approximately 42 kilograms per capita per year (across all carton packaging formats) resulting from the highly developed carton packaging culture in European food and beverage retail and the advanced stage of the consumer economy, which leads to high per-capita consumer goods consumption.

Not only is Sweden a leading consumption market for carton packaging, but it is also the birthplace of the modern aseptic liquid carton packaging, and together with the two other liquid carton technology leaders, with headquarters in Northern Europe, Tetra Pak (in Sweden, founded in 1951) and SIG Combibloc (in Switzerland), the region is globally significant in terms of technology leadership and concentration of R&D efforts in carton packaging for liquid foods. Germany has a significant market for carton packages, as well as a large pharmaceutical market that consumes the most pharmaceutical folding cartons in Europe, while food manufacturers such as Nestlé Germany, Dr. August Oetker and Müller Dairy use vast quantities of carton packaging for their packaged food and dairy product ranges.

The EU’s Green Deal Packaging Regulations (PPWR), the EU Taxonomy for sustainable activities and CSRD Corporate sustainability reporting requirements are establishing Europe’s most advanced sustainability compliance landscape for carton packaging, pushing European carton suppliers and brand owners to the cutting edge of sustainable fiber supply, barrier innovation for liquid cartons, and digital product passport implementation.

Why is North America Showing Moderate but Consistent Growth?

The global market will be dominated by the North American market with the presence of pharmaceutical carton growth due to generic drug packaging market growth, aseptic carton demand growth in the plastic-to-carton substitution momentum driven by state-level packaging regulations and the use of premium carton packaging formats for the premium food & beverage category as brand differentiation and a platform of sustainability communication.

Why is the Middle East and Africa Region an Emerging High-Growth Market?

The LAMEA region contributes about 9% of global market revenue in 2025, but will grow at the highest CAGR (6.8%) from 2026 to 2035, led by the structure of its market growth with the expansion of organized food retail across its key markets (the Gulf), rapid population growth creating growth in the packaged food demand, the exceptional growth of dairy product consumption in the Middle East and North Africa driving growth in aseptic carton demand, and the growth in the pharmaceutical manufacturing and distribution infrastructure across the Gulf states and South Africa where the consumption of folding carton packaging will increase.

Saudi Arabia and the UAE are at the top of the list of the most commercialized carton packaging markets in the Gulf, and both nations have seen increased demand for carton packaging in their food processing and pharmaceutical sectors, along with high consumption rates among the large expatriate populations and investment programs designed to boost domestic manufacturing under Vision 2030 and similar national development plans.

Sub-Saharan Africa is the greatest long-term growth market in the wider LAMEA market, and Nigeria, Kenya, Ethiopia and South Africa are witnessing accelerated urbanisation and growth in consumer incomes, leading to a shift from bulk/loose food purchases to the purchase of packaged foods, where carton is the main packaging material for dairy, juice and processed foods. The aseptic carton packaging format is especially relevant for the development of the Sub Saharan African market, as the distribution of foods in this type of packaging is the realistic commercial solution for rural/peri-urban environments to offer ambient stable UHT milk and juice in addition to refrigerated foods in the cities.

Top Players in the Market and Their Offerings

- Tetra Pak International S.A.

- SIG Combibloc Group AG

- Elopak AS

- Graphic Packaging International LLC

- WestRock Company

- Smurfit Kappa Group

- Mondi Group

- DS Smith plc

- Stora Enso Oyj

- International Paper Company

- Others

Key Developments

The market has undergone significant developments as industry participants seek to expand capabilities and enhance product portfolios.

- In March 2025: The Tetra Pak Bridge 1000 Edge with a fully bio-based and aluminum-free barrier system is the largest step Tetra Pak International has taken in its liquid carton material innovation since the launch of the original aseptic brick carton, commercializing the material for the first time and proving equivalent in its 6-month ambient shelf stability performance while also being fully recyclable in mainstream paper recycling streams without the need for aluminum separation, with a carbon footprint reduction of approximately 20% when compared to the traditional aluminum-based construction in the Tetra Brik Aseptic, as assessed in a cradle-to-gate lifecycle assessment, and certified under FSC Chain of Custody.

- In February 2025: The Coca-Cola Company, PepsiCo and AB InBev with their plastic substitution to carton (PSTC) initiatives, Graphic Packaging International announced it is expanding its KeelClip and ClipCombo paperboard multipack beverage carrier system to new carton formats for canned sparkling water, energy drink and craft beer applications in North America and Europe, where the majority of paperboard packages are currently used.

These strategic moves have helped companies strengthen market positions, increase sustainable carton packaging portfolios to meet the growing regulatory and brand sustainability demands from their customers in the food/beverage, pharmaceutical and consumer goods sectors, advance next-generation carton barrier innovations to truly qualify liquid carton packaging as a solution for the circular economy, and take advantage of the structural growth created by the substitution of plastic bottles with cartons, aseptic carton adoption in emerging markets and pharma packaging serialization investments.

The Carton Packaging Market is segmented as follows:

By Product Type

- Folding Cartons

- Reverse Tuck End (RTE) Cartons

- Straight Tuck End (STE) Cartons

- Auto Bottom Cartons

- Sleeve Cartons

- Shelf-Ready Cartons

- Gable Top Cartons

- Standard Gable Top Cartons

- Extended Shelf Life (ESL) Gable Top

- Reclosable Gable Top Cartons

- Brick Liquid Cartons

- Standard Brick Cartons

- Slim and Square Brick Variants

- Aseptic Cartons

- Standard Aseptic Brick Cartons

- Aseptic Cartons with Closure Systems

- Aluminum-Free Aseptic Cartons

- Other Product Types

- Wedge-Shaped Cartons

- Shaped Premium Cartons

By Material

- Paperboard

- Solid Bleached Sulfate (SBS)

- Coated Unbleached Kraft (CUK)

- Recycled Paperboard (CRB)

- Folding Boxboard (FBB)

- Liquid Packaging Board

- Virgin Fiber Liquid Packaging Board

- Bio-Based Barrier Coated Board

- Cartonboard

- Chromoboard

- Graphoboard

- Other Materials

By Printing Technology

- Offset Printing

- Flexographic Printing

- Digital Printing

- Gravure Printing

- Other Printing Technologies

- Screen Printing

- Inkjet Coding & Marking

By End Use Industry

- Food & Beverage

- Dry Food & Cereals

- Liquid Food & Juices

- Confectionery & Snacks

- Frozen Food

- Dairy Products

- Fresh Milk & Cream

- UHT Milk & Dairy Beverages

- Yogurt & Fermented Dairy

- Cheese & Butter

- Healthcare & Pharmaceuticals

- Prescription Medicines

- OTC Healthcare Products

- Medical Devices Packaging

- Personal Care & Cosmetics

- Skincare & Hair Care

- Fragrances & Premium Cosmetics

- Household Products

- Detergents & Cleaning Products

- Home Care Packaging

- Other End Use Industries

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Carton Packaging by Segments

- 2.1.2. Carton Packaging by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Carton Packaging Market Attractiveness Analysis, By Product Type

- 2.2.3. Carton Packaging Market Attractiveness Analysis, By Material

- 2.2.4. Carton Packaging Market Attractiveness Analysis, By Printing Technology

- 2.2.5. Carton Packaging Market Attractiveness Analysis, By End Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Accelerating Plastic-to-Carton Substitution Driven by Regulatory Mandates and Consumer Sustainability Expectations Across Multiple Consumer Goods Categories

- 3.1.2. Aseptic Carton Technology Enabling Ambient Liquid Food Distribution in Cold Chain-Limited Emerging Markets

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Carton Packaging Market – By Product Type

- 4.1. Product Type Market Overview, By Product Type Segment

- 4.1.1. Carton Packaging Market Revenue Share, By Product Type, 2025 & 2035

- 4.1.2. Folding Cartons

- 4.1.2.1. Reverse Tuck End (RTE) Cartons

- 4.1.2.2. Straight Tuck End (STE) Cartons

- 4.1.2.3. Auto Bottom Cartons

- 4.1.2.4. Sleeve Cartons

- 4.1.2.5. Shelf-Ready Cartons

- 4.1.3. Carton Packaging Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Gable Top Cartons

- 4.1.6.1. Standard Gable Top Cartons

- 4.1.6.2. Extended Shelf Life (ESL) Gable Top

- 4.1.6.3. Reclosable Gable Top Cartons

- 4.1.7. Carton Packaging Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Brick Liquid Cartons

- 4.1.10.1. Standard Brick Cartons

- 4.1.10.2. Slim and Square Brick Variants

- 4.1.11. Carton Packaging Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Aseptic Cartons

- 4.1.14.1. Standard Aseptic Brick Cartons

- 4.1.14.2. Aseptic Cartons with Closure Systems

- 4.1.14.3. Aluminum-Free Aseptic Cartons

- 4.1.15. Carton Packaging Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Other Product Types

- 4.1.18.1. Wedge-Shaped Cartons

- 4.1.18.2. Shaped Premium Cartons

- 4.1.19. Carton Packaging Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Product Type Market Overview, By Product Type Segment

- Chapter 5. Carton Packaging Market – By Material

- 5.1. Material Market Overview, By Material Segment

- 5.1.1. Carton Packaging Market Revenue Share, By Material, 2025 & 2035

- 5.1.2. Paperboard

- 5.1.2.1. Solid Bleached Sulfate (SBS)

- 5.1.2.2. Coated Unbleached Kraft (CUK)

- 5.1.2.3. Recycled Paperboard (CRB)

- 5.1.2.4. Folding Boxboard (FBB)

- 5.1.3. Carton Packaging Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Liquid Packaging Board

- 5.1.6.1. Virgin Fiber Liquid Packaging Board

- 5.1.6.2. Bio-Based Barrier Coated Board

- 5.1.7. Carton Packaging Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Cartonboard

- 5.1.10.1. Chromoboard

- 5.1.10.2. Graphoboard

- 5.1.11. Carton Packaging Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Other Materials

- 5.1.15. Carton Packaging Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Material Market Overview, By Material Segment

- Chapter 6. Carton Packaging Market – By Printing Technology

- 6.1. Printing Technology Market Overview, By Printing Technology Segment

- 6.1.1. Carton Packaging Market Revenue Share, By Printing Technology, 2025 & 2035

- 6.1.2. Offset Printing

- 6.1.3. Carton Packaging Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Flexographic Printing

- 6.1.7. Carton Packaging Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Digital Printing

- 6.1.11. Carton Packaging Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Gravure Printing

- 6.1.15. Carton Packaging Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Other Printing Technologies

- 6.1.18.1. Screen Printing

- 6.1.18.2. Inkjet Coding & Marking

- 6.1.19. Carton Packaging Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Printing Technology Market Overview, By Printing Technology Segment

- Chapter 7. Carton Packaging Market – By End Use Industry

- 7.1. End Use Industry Market Overview, By End Use Industry Segment

- 7.1.1. Carton Packaging Market Revenue Share, By End Use Industry, 2025 & 2035

- 7.1.2. Food & Beverage

- 7.1.2.1. Dry Food & Cereals

- 7.1.2.2. Liquid Food & Juices

- 7.1.2.3. Confectionery & Snacks

- 7.1.2.4. Frozen Food

- 7.1.3. Carton Packaging Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Dairy Products

- 7.1.6.1. Fresh Milk & Cream

- 7.1.6.2. UHT Milk & Dairy Beverages

- 7.1.6.3. Yogurt & Fermented Dairy

- 7.1.6.4. Cheese & Butter

- 7.1.7. Carton Packaging Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Healthcare & Pharmaceuticals

- 7.1.10.1. Prescription Medicines

- 7.1.10.2. OTC Healthcare Products

- 7.1.10.3. Medical Devices Packaging

- 7.1.11. Carton Packaging Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Personal Care & Cosmetics

- 7.1.14.1. Skincare & Hair Care

- 7.1.14.2. Fragrances & Premium Cosmetics

- 7.1.15. Carton Packaging Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Household Products

- 7.1.18.1. Detergents & Cleaning Products

- 7.1.18.2. Home Care Packaging

- 7.1.19. Carton Packaging Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Other End Use Industries

- 7.1.23. Carton Packaging Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End Use Industry Market Overview, By End Use Industry Segment

- Chapter 8. Carton Packaging Market – Regional Analysis

- 8.1. Carton Packaging Market Overview, By Region Segment

- 8.1.1. Global Carton Packaging Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Carton Packaging Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Carton Packaging Market Revenue, By Product Type, 2026 – 2035

- 8.1.4. Global Carton Packaging Market Revenue, By Material, 2026 – 2035

- 8.1.5. Global Carton Packaging Market Revenue, By Printing Technology, 2026 – 2035

- 8.1.6. Global Carton Packaging Market Revenue, By End Use Industry, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Carton Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Carton Packaging Market Revenue, By Product Type, 2026 – 2035

- 8.2.3. North America Carton Packaging Market Revenue, By Material, 2026 – 2035

- 8.2.4. North America Carton Packaging Market Revenue, By Printing Technology, 2026 – 2035

- 8.2.5. North America Carton Packaging Market Revenue, By End Use Industry, 2026 – 2035

- 8.2.6. U.S. Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Carton Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Carton Packaging Market Revenue, By Product Type, 2026 – 2035

- 8.3.3. Europe Carton Packaging Market Revenue, By Material, 2026 – 2035

- 8.3.4. Europe Carton Packaging Market Revenue, By Printing Technology, 2026 – 2035

- 8.3.5. Europe Carton Packaging Market Revenue, By End Use Industry, 2026 – 2035

- 8.3.6. Germany Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Carton Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Carton Packaging Market Revenue, By Product Type, 2026 – 2035

- 8.4.3. Asia Pacific Carton Packaging Market Revenue, By Material, 2026 – 2035

- 8.4.4. Asia Pacific Carton Packaging Market Revenue, By Printing Technology, 2026 – 2035

- 8.4.5. Asia Pacific Carton Packaging Market Revenue, By End Use Industry, 2026 – 2035

- 8.4.6. China Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Carton Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Carton Packaging Market Revenue, By Product Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Carton Packaging Market Revenue, By Material, 2026 – 2035

- 8.5.4. The Middle-East and Africa Carton Packaging Market Revenue, By Printing Technology, 2026 – 2035

- 8.5.5. The Middle-East and Africa Carton Packaging Market Revenue, By End Use Industry, 2026 – 2035

- 8.5.6. Saudi Arabia Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Carton Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Carton Packaging Market Revenue, By Product Type, 2026 – 2035

- 8.6.3. Latin America Carton Packaging Market Revenue, By Material, 2026 – 2035

- 8.6.4. Latin America Carton Packaging Market Revenue, By Printing Technology, 2026 – 2035

- 8.6.5. Latin America Carton Packaging Market Revenue, By End Use Industry, 2026 – 2035

- 8.6.6. Brazil Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Carton Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Carton Packaging Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Carton Packaging Market: Company Market Share, 2025

- 9.2. Global Carton Packaging Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Tetra Pak International S.A.

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. SIG Combibloc Group AG

- 10.3. Elopak AS

- 10.4. Graphic Packaging International LLC

- 10.5. WestRock Company

- 10.6. Smurfit Kappa Group

- 10.7. Mondi Group

- 10.8. DS Smith plc

- 10.9. Stora Enso Oyj

- 10.10. International Paper Company

- 10.11. Others.

- 10.1. Tetra Pak International S.A.

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 78

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Tetra Pak International S.A.

- SIG Combibloc Group AG

- Elopak AS

- Graphic Packaging International LLC

- WestRock Company

- Smurfit Kappa Group

- Mondi Group

- DS Smith plc

- Stora Enso Oyj

- International Paper Company

- Others

FAQs

The key players in the market are Tetra Pak International S.A., SIG Combibloc Group AG, Elopak AS, Graphic Packaging International LLC, WestRock Company, Smurfit Kappa Group, Mondi Group, DS Smith plc, Stora Enso Oyj, International Paper Company, Others.

The government regulations have the strongest influence on the market development of carton packaging through multiple regulatory mechanisms that are simultaneously applied in the various primary markets of carton packaging around the world. There are now more than 60 countries that have national single-use plastics bans as well as the EU PPWR, SUPD, UK Plastic Packaging Tax, and California SB54, all of which either mandate or provide financial incentives for the replacement of plastic packaging with carton packaging in an increasing number of food, beverage, and consumer goods packaging categories, with each regulation expanding the number of legal plastic-free packaging alternatives that carton packaging is well positioned to fill. Extended producer responsibility schemes in France, Germany, Belgium, and increasingly throughout the Asia Pacific region impose a levy on packaging that is based on the recyclability of materials and renewable content, providing carton packaging with direct financial benefits over non-recyclable plastic packaging, and indirectly promoting carton packaging adoption through the levy on competing plastic packaging formats. Pharmaceutical serialization requires unique pack-level identifiers on medicine outer cartons, which essentially forces a digital print infrastructure on pharmaceutical carton converting plants and also places a barrier on entry for new pharmaceutical packaging suppliers, unless they invest in a serialization capability. Food safety and food contact regulations (EU Framework Regulation 1935/2004, FDA 21 CFR regulations for food contact materials, and China’s GB 9685 standard) require documentation of compliance and migration testing, presenting carton producers and converters with continuous, ongoing regulatory management needs when packaging food for their customers.

The packaging prices of cartons can be significantly differentiated across product categories, material quality, and print quality, which results in different market segments with varying competitive dynamics. Packaging printed in 2-4 colors on standard SBs or FBB cartonboard, especially commodity folding cartons for dry food applications, is one of the most competitive carton formats that the world has, with the price of converting cartons to USD 0.02-0.08 per carton in high volume, which causes high competition among converters and restricts margin expansion in commodity packaging. Premium folding pharmaceutical cartons and luxury consumer goods folding cartons (MPP, specialty finishes, serialization variable data, and sophisticated structural engineering) carry prices of converting ranging between USD 0.30 and 5.00 per carton; the carton for pharmaceutical applications has a higher premium, which is partly attributable to the investment made in the regulatory aspects of the serialization system and partly due to the quality control requirements for the qualification of pharmaceutical packaging suppliers. The technology licensing and the economics of the filling machine are the drivers of the prices of the major aseptic system providers when it comes to aseptic carton pricing: Tetra Pak, SIG Combibloc, and Elopak provide carton sleeves at prices between USD 0.04 and 0.15 per pack depending on quantity, format, and closure system, while the combined costs of the carton material and filling system account for 8-15% of the retail price of packaged liquid food products, which historically has helped to maintain the pricing power of the aseptic carton system providers. At around 45–55% of converter production cost, raw material cost is the biggest single cost input in carton packaging production, and cartonboard cost is dependent on global pricing of pulp, energy cost at paper mills, and recycled fiber market conditions, all of which result in commodity cost volatility, which is managed by converters through index-linked pricing contracts with key customer accounts in the food and consumer goods sector.

The carton market is expected to reach approximately USD 291.84 billion by 2035 at a 5.0% CAGR, driven by ongoing food and beverage consumption growth around the world creating new carton demand across all formats, plastic-to-carton substitution mandates in the key regulatory markets providing incremental demand above baseline consumption growth, the barrier innovations of PE-free and aluminum-free that will enable fully recyclable liquid carton packaging and strengthen the carton’s competitive position against plastic across liquid food applications, digital printing adoption, which will enable new commercial carton packaging models such as personalization and short-run specialty applications, and aseptic carton growth in Asia Pacific and LAMEA, which will open the door for carton-based ambient liquid food distribution in cold chain-limited geographies.

The Asia Pacific region is projected to have the largest share of the market in the years ahead, rising from 39% in 2025 to about 42% by 2035 due to the growth of China’s huge food and beverage carton demand, entry of organized retailers in India, which is leading to a rapidly expanding carton market, and market development in Southeast Asia, creating new aseptic carton and folding carton demand centers. European carton producers will continue to lead the development of the global carton packaging market, both in terms of technology and sustainability, with a special focus on sustainable barrier innovation, digital printing, and smart carton packaging.

The LAMEA region will witness the highest CAGR of 6.8% from 2026 to 2035, as a result of the expansion of the food processing sector in the GCC countries under the Vision 2030 industrial development initiative, the development of organized retail and packaged food markets across Nigeria, Kenya, and Ethiopia, the exceptional growth of the pharmaceutical manufacturing industry in the Middle East and Africa region, which is consuming folding carton packaging, and the rapid growth of the Dairy manufacturing sector in the Middle Eastern region, which is consuming Aseptic carton packaging. In the Asia Pacific region, the individual market growth is at a higher level of around 8.1% CAGR, owing to the growth of the organized retail market and expansion in the pharmaceutical industry and modernization of the dairy processing industry from bulk to carton packaged formats.

The global processed food market (5.8% CAGR) will generate proportional carton packaging demand, the EU PPWR (which requires all packaging to be reusable, recyclable, or compostable by 2030) will drive plastic-to-carton substitution across multiple processed food packaging categories, the global UHT milk market (2030 USD 284 billion) will fuel aseptic carton packaging demand, especially in Asia Pacific and LAMEA cold chain-limited markets, and the national single-use plastics policy being pursued in China will create the world’s largest national market regulatory catalyst for the plastic-to-carton packaging transition, among others.