Plastic Free Smart Food Packaging Market Size, Trends and Insights By Material Type (Paper & Paperboard, Coated Paperboard, Uncoated Kraft Paper, Barrier-Coated Paper Systems, Molded Fiber, Aluminum Foil & Metallized Films, Aluminum Foil Laminates, Bio-Based Metallized Films, Aluminum Composite Laminates, Glass, Primary Food Contact Glass Containers, Smart Glass Packaging with Sensor Integration, Biopolymer-Based Materials, PLA-Based Films & Laminates, PHA-Based Films, Cellulose-Based Films (NatureFlex), Chitosan Films, Starch-Based Composite Films, Plant-Based Composites, Sugarcane Bagasse Composites, Bamboo Fiber Composites, Hemp & Flax Fiber Composites, Agricultural Waste Composites, Other Material Types), By Technology (Active Packaging, Oxygen Scavengers, Antimicrobial Active Systems, Moisture Regulators & Desiccants, Ethylene Absorbers, Carbon Dioxide Emitters, Intelligent Packaging, Time-Temperature Indicators (TTI), Freshness Sensors & Indicators, NFC & RFID-Enabled Packaging, QR Code & Blockchain-Connected Packaging, Gas Sensors & Biosensors, Modified Atmosphere Packaging, Controlled Atmosphere Packaging, Equilibrium Modified Atmosphere, Edible Packaging, Seaweed-Based Edible Films, Protein-Based Edible Coatings, Starch-Based Edible Films, Water-Soluble Packaging, Other Technologies), By Application (Fresh Produce & Fruits, Meat, Poultry & Seafood, Dairy Products, Bakery & Confectionery, Beverages, Ready Meals & Convenience Foods, Other Applications), By End Use (Food Manufacturers, Foodservice & HoReCa, Retail & Grocery, Other End Uses), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 13.8%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Europe |

Major Players

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- Sealed Air Corporation

- Others

Reports Description

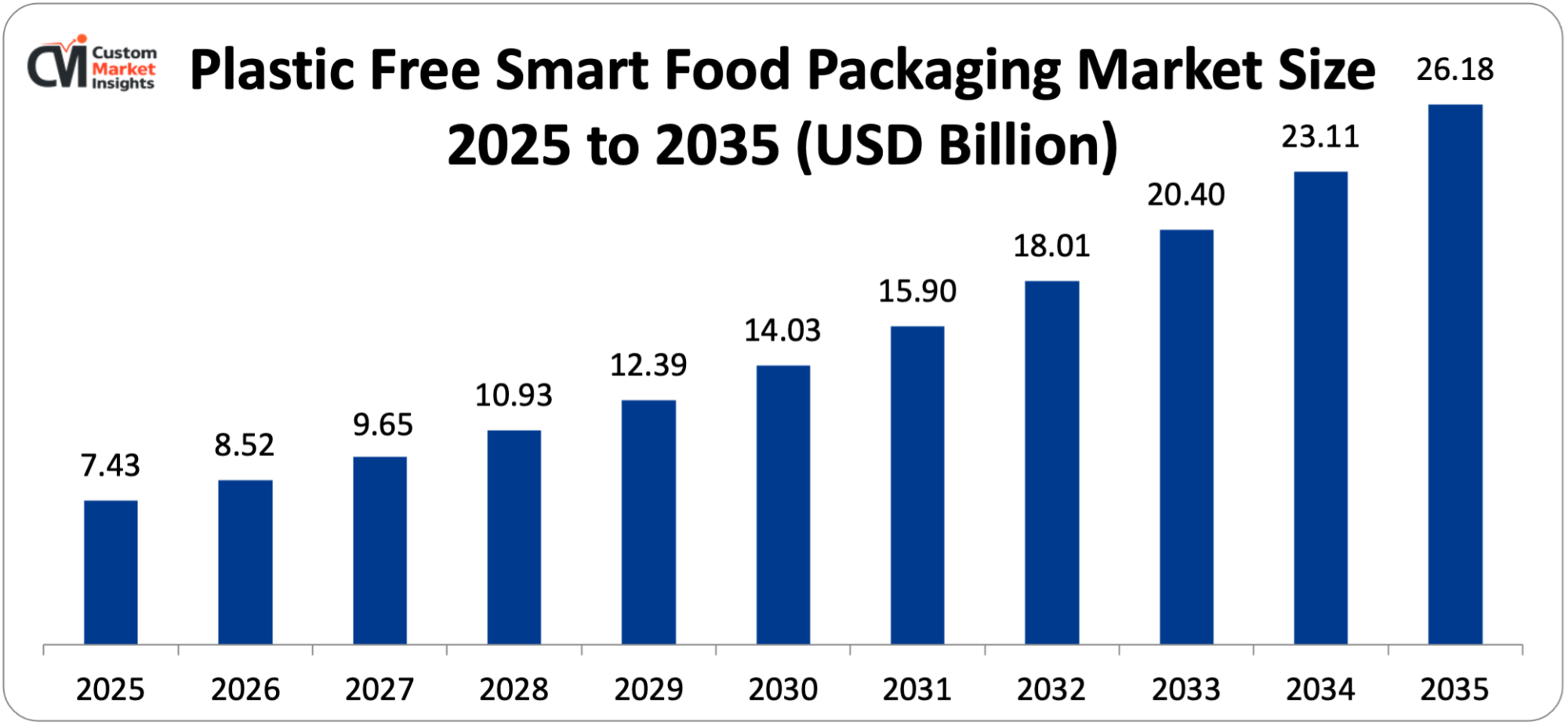

The global plastic free smart food packaging market is estimated at USD 7.43 billion in 2025 and is expected to grow from USD 8.52 billion in 2026 to USD 26.18 billion by 2035 at a 13.8% CAGR from 2026 to 2035.

Market Highlight

- In 2025, Europe was the dominant region in the plastic free smart food packaging market with a 36% share and the world’s most complex plastic packaging regulations, which require plastic elimination in all packaging segments, combined with the greatest number of smart packaging technology developers and sustainable material innovators.

- The Asia Pacific region will witness the highest CAGR of 16.4% from 2026 to 2035 with the implementation of a national single-use plastics action plan in China, increasing organized retail footprint across the region and the unprecedented surge of fresh food e-commerce in the region calling for smart packaging that can enable traceability and freshness management while also being plastic-free.

- Paper and paperboard accounted for about 34% of market share in 2025, representing the most commercially proven and established plastic-free packaging material, with a long supply chain, and the lowest cost for packagers among the various packaging material types and food application categories.

- From a material type perspective, the biopolymer-based materials segment is expected to register the highest CAGR (17.2%) between 2026 and 2035, due to the rapidly evolving platforms of PLA, PHA, and cellulose materials that are poised to meet the barrier, mechanical, and processability criteria for use in active and intelligent packaging.

- From a technology perspective, active packaging claimed the largest share of 38% in 2025, corresponding to the commercial maturity of oxygen scavengers, antimicrobial agents, moisture control agents and ethylene absorbers for shelf life extension in perishable food categories embedded in plastic-free packaging substrates.

- By technology, the intelligent packaging segment will grow at the highest CAGR of 18.6% during the forecast period (2026–2035) owing to the convergence of low-cost printed sensor technology, NFC and RFID connectivity, and consumer smartphone adoption that will allow smart packaging digital engagement at scale across retail food applications.

Impact of Middle East War on Plastic Free Smart Food Packaging Market

The ongoing wars in the Middle East have resulted in an enhanced awareness concerning sustainable and safe food supply chains, thus aiding in the growth of the market for plastic free smart packaging solutions. Increased crude oil prices have contributed to a hike in the price of traditional plastic-based food packaging options, thereby boosting the appeal of environmentally friendly food packaging options.

Significant Growth Factors

The Plastic Free Smart Food Packaging Market Trends present significant growth opportunities due to several factors:

- Converging Regulatory Mandates Simultaneously Eliminating Plastic Packaging and Mandating Food Traceability Creating Unified Market Demand: The most structural and commercially driving growth factor for the plastic free smart food packaging market is the unprecedented up-scaling of two different, but complementary, regulatory drivers: The global process of banning single-use plastic food packaging and the progressive introduction of digital food traceability requirements along the food supply chain – which are even more compatible than they may sound, as they will eventually push food manufacturers and retailers in big markets towards smart food packaging solutions, no longer a premium differentiator but increasingly demanded by regulations. The European Union’s Packaging and Packaging Waste Regulation (PPWR), on its way to legislative adoption with an ambition of having all packaging be reusable, recyclable or compostable by 2030, and also requires digital product passports for all packaging in the EU containing machine-readable data on material content, recyclability or instructions for the end-of-life process – creating a regulatory confluence that the plastic free smart food packaging market is uniquely capable of meeting. The EU Farm to Fork Strategy, one of the four pillars of the European Green Deal, explicitly calls for a 15% reduction of food packaging waste by 2030, as well as promoting food safety by enhancing traceability – both of which are met by plastic free smart packaging as a material and technology platform. The Food Safety Modernization Act (FSMA) in the USA, which will come into effect from January 2026 and require full compliance by January 2026, introduces the Food Traceability Final Rule requiring strengthened traceability record keeping for a specific set of high-risk foods such as fresh cut fruits and vegetables, shell eggs, nut butters, and ready to eat deli salad foods; this means that smart packaging systems will face a new challenge of capturing and communicating critical tracking events along the food supply chain. At a time when China’s massive food manufacturing and retail sector is tackling the twin challenges of plastic elimination and compliance with the food traceability standards set by the State Administration for Market Regulation under the Food Safety Law, China’s national single-use plastics action plan is creating the world’s biggest market development opportunity for plastic free smart food packaging. These regulatory pressures, combined with voluntary brand commitments towards brand sustainability and consumer demand, are driving a growing compound commercial pull towards plastic free smart food packaging as one of the most strategically important and commercially attractive market segments within the emerging global food packaging arena throughout the forecast period.

- Food Waste Reduction Imperative Driving Functional Packaging Innovation Beyond Simple Plastic Substitution: UN reports indicate that the global food waste problem is severe, with approximately 1.3 billion tonnes of food or 1/3 of all food produced for human consumption lost or wasted annually, at a cost of approximately USD 1 trillion annually to the global food economy, and robust commercial and regulatory incentives are emerging to innovate packaging to make food last longer, provide real-time information on its freshness to consumers and retailers, and enable timely decisions in the supply chain to minimize losses. Food packaging can directly contribute to preventing food waste, as well as cause food waste: Good food packaging with the appropriate barrier, modified atmosphere and freshness management functionality can increase the commercially marketable life of fresh foods by 2-7 days, meat and poultry by 3-10 days, and dairy products by 5-15 days compared to otherwise equivalent foods in poor packaging, signifying significant waste savings — a consumer value proposition and a supply chain economic benefit that is worth the premium price of good packaging. At the same time, an estimated 30-40% of fresh produce is wasted at the retail and consumer level because it is too early to consume, as the result of conservative fixed expiry dates that take no account of the actual product condition, which is what a real-time freshness indicator and intelligent packaging solution can solve directly by providing condition-based information rather than time-based information about product quality. In the plastic free smart food packaging market, the smart packaging technology components most directly related to food waste reduction goals are the time-temperature indicator (TTI) that can visualize the cold chain history, the freshness sensor that can detect gas biomarkers of product spoilage, and the antimicrobial active packaging systems that inhibit microbial growth to extend shelf life, offering a commercially viable case for the adoption of smart packaging that stands apart and complements the sustainability attributes of the plastic-free material platforms. The estimated USD 38 billion annual economic value of smart packaging technologies that could be used to cut food waste by even 5% by the entire food supply chain participants is a strong economic argument to invest in smart packaging across the food supply chain and a rational basis to invest – at least for food manufacturers and retailers – into smart packaging, even if consumers don’t always pay a higher price for smart packaging.

What are the Major Advances Changing the Plastic Free Smart Food Packaging Market Today?

- Printed and Flexible Electronics Integration Into Paper and Biopolymer Substrates Enabling Cost-Effective Smart Packaging at Commercial Scale: The most technically relevant innovation that allowed the plastic-free smart food packaging market to grow is the successful integration of printed and flexible electronic sensor components, such as printed electrochemical sensors, colorimetric freshness indicators, NFC and RFID antenna systems, and printed time-temperature indicators, onto paper, paperboard and biopolymer packaging substrates using roll-to-roll printing processes compatible with conventional packaging manufacturing infrastructure, allowing for smart functionality to be added to plastic-free packaging at incremental cost and at an approach to the economics of conventional plastic smart packaging while eliminating the use of the petroleum-derived substrate. Companies such as Thin Film Electronics (Thinfilm), PragmatIC Semiconductor, and smart paper packaging division Stora Enso are printing functional inks – carbon nanotube conductive inks, silver nanowire antenna systems, or enzymatic/chemical indicator inks – onto the cellulose-based packaging substrates from the lab, towards roll-to-roll manufacturing and per-unit costs of USD 0.03–0.08, making it economically viable to integrate basic smart NFC paperboard with high quality consumer food brands. The challenge for integration of printed electronics onto non-plastic packaging materials has historically been the ability to encapsulate conductive ink formulations in water-resistant binder systems, as well as to apply ultra-thin conformal protective coatings that prevent ambient moisture from degrading printed electronic components without increasing the cost of the substrate or reducing substrate compostability. Printable and compostable biopolymer freshness indicator systems that utilize colour changes in the enzymatic reaction or gas sensitive dye complexes due to volatile amine, hydrogen sulphide or carbon dioxide concentration changes to indicate meat, fish or produce spoilage have been successfully formulated, with examples from COX Technologies (FreshTag) and Novatek International (ripeness indicator) now commercially used for consumer visible freshness assessment at the point of purchase. Printed NFC tags on paper-based wine labels that allow the consumer to tap their smartphone to unlock wine vintage, pairing recommendations, authenticity checks and even sustainability certification data have shown consumer engagement benefits of connected plastic-free smart packaging and has fast-tracked brand owner investment in NFC-enabled paper and biopolymer food packaging in wine, dairy and specialty food categories.

- Active Packaging Functionalities Achieving Performance Parity on Plastic-Free Substrates for Perishable Food Applications: Active packaging technologies, such as oxygen scavengers, antimicrobial agents, and moisture and ethylene regulators have been successfully transferred from conventional plastic packaging materials to paper and paperboard and biopolymer-based packaging. Companies such as Sealed Air’s Cryovac division, Multisorb Technologies and Mitsubishi Gas Chemical’s Ageless system have been successful in embedding oxygen scavenging systems into paperboard cartons, biopolymer film pouches or cellulose-based laminates to keep the oxygen level below 0.1% in sealed food packages, thereby slowing oxidative food spoilage of processed meats, cheese, coffee and snack foods. The technical hurdle of integrating an oxygen scavenger into a permeable paper-based substrate has been addressed by multi-layer construction, such as a high barrier biopolymer-coated substrate with oxygen scavenger sachets or an incorporated oxygen scavenger layer, to deliver both the oxygen barrier and active scavenging properties required for challenging perishable food applications, while still being 100% plastic-free. Antimicrobial active packaging — products in which the bioactive ingredient is a natural antimicrobial agent such as rosemary extract, cinnamon oil, thymol, nisin or lysozyme, which are incorporated or coated on the packaging surface to inhibit the growth of surface microorganisms on packaged food products — is increasingly being used in the commercial market on paper, cellulose film and biopolymer packaging systems, with the clean label and natural origin properties of the botanical active ingredients fitting comfortably with the clean label and natural origin packaging system proposition. The commercialization of chitosan, obtained from the waste of crustaceans, as a biopolymer film-forming material and as an inherently antimicrobial packaging coating is picking up commercial momentum, as chitosan-based packaging films offer a combination of plastic-free, compostable and antimicrobial functionality in a single material that meets the sustainability and food safety performance requirements for fresh produce and seafood packaging applications.

- Edible and Water-Soluble Packaging Technologies Achieving Commercial Deployment in Food Service and E-Commerce Applications: The most extreme expression of the plastic-free packaging concept is “edible packaging” where the entire package or part of the packaging is made from food-grade materials that can be eaten with the food product and which is advancing from concept demonstration to specific commercial packaging applications where the packaging economics are most favourable: food service, single-serve, and e-commerce food delivery. Notpla’s seaweed-based Ooho capsule, which has been used at major events such as the London Marathon, and partnering with JustEat Takeaway for the sauce sachets, is one of the first edible seaweed packaging products that has been deployed in food service applications to date, showing the potential of seaweed edible packaging to withstand food contact and to offer sufficient barrier properties for liquid food packaging while also being accepted by consumers in food service environments. Companies such as TerVia and Monosol are commercializing whey protein based edible films as portion scale, edible packages for premium food service and specialty food retail applications as oxygen or lipid oxidation barriers applied to cheese, ready to eat deli products and individual confectionery items. Water soluble polyvinyl alcohol (PVA) packaging is a non-natural package film that is marine biodegradable in many definitions of plastic-free packaging and has already been commercialized in dishwasher pod format for cleaning products and is being developed for use in food-service single serve applications for seasoning sachets, spice sachets, and sauce sachets, where the convenience of dissolving the entire package into a hot food preparation means that there is no need to dispose of the sachet. The edible packaging segment is small, accounting for around 4% of the total plastic free smart food packaging market revenue, but is growing at an estimated 22.4% CAGR from 2026 to 2035 as food service operators and food manufacturers discover specific application niches for which the economic and functional viability of edible packaging is commercially relevant, while material costs are expected to fall with scale and familiarity with edible packaging concepts will increase through exposure in the food service channel.

Category Wise Insights

By Material Type

Why Does Paper and Paperboard Lead the Plastic Free Smart Food Packaging Market?

In 2025, paper and paperboard are the top material type market segment, with revenue of around 34% of the market. This leadership is partly due to the fact that paper and paperboard uniquely combine commercial maturity, the breadth of its global packaging supply chain, regulatory acceptance across virtually all food contact applications, consumer familiarity and trust, and existing smart packaging technology compatibility, making it the packaging substrate of choice for brand owners who are embarking on packaging sustainability transitions and for smart packaging developers who want the widest possible deployment platform. As one of the biggest and longest-established categories in the packaging industry, the global paper-based food packaging market is growing to become a significant alternative to plastic packaging, replacing plastic packaging in hundreds of millions of SKUs per day worldwide in paperboard cartons, corrugated fiber cases, kraft paper bags, and molded fiber trays. Established paper packaging substrate is evolving to a smart packaging platform with incremental packaging manufacturing cost due to the integration of smart packaging functionalities such as water-resistant QR code printing, lamination of an RFID antenna onto kraft liner board, integration of oxygen scavenger sachets onto paperboard packaging, and barrier coating systems, which allow paper to replace plastic flexible packaging in dry food applications. The most significant recent advances in coatings for paper-based plastic-free packaging that can be used to replace plastic flexible packaging materials include the development of aqueous barrier coatings for paper surfaces, such as polyvinyl alcohol (PVA), poly(lactic acid) dispersion, and nanocellulose composite coatings, which can achieve moisture vapor transmission rates (MVR) and oxygen transmission rates (OTR) comparable to those of polyethylene or polypropylene plastic packaging films, as these materials can be applied to the surfaces of composite paper structures. Barrier paper and paperboard product development spending has been significant across a range of companies – including Mondi, Smurfit Kappa, DS Smith and Stora Enso – all of whom have commercialized plastic substitution paper packaging platforms using barrier coating technologies that allow food manufacturers to make the switch from plastic to paper packaging without sacrificing shelf life.

By Technology

Why Does Active Packaging Lead the Technology Segment?

The active packaging technology segment is the largest, with around 38% of the market’s revenue in 2025. Active packaging solutions that include oxygen scavenging, moisture control, and antimicrobial technologies are now commercially available and have been proven to be commercially successful as active conventional plastics for more than 20 years, providing a technology readiness base that is being increasingly transferred to plastic free substrates allowing for market entry based on using established supply chains, regulatory approval, and customer awareness, not fresh market development. The increased use of iron-based oxygen scavengers in oxygen sachets, active oxygen scavenging layers in plastic-free packaging for PLA-biopolymer laminates, and UV-activated coatings onto paperboard cartons in processed meat, cheese and coffee packaging, where the passive barrier performance of plastic-free packaging was not adequate to match the extended shelf life achievable with conventional plastic vacuum packaging, are examples of the highest-value active packaging sub-segments where oxygen scavengers have been incorporated into plastic-free packaging for the first time. Clean-label natural antimicrobial system development, including packaging systems containing essential oils (EO) from rosemary, thyme and oregano as active ingredients on paper and biopolymer materials, is expected to boost growth in the antimicrobial active packaging sub-segment, which is expected to grow at the rate of around 15.3% CAGR within the active packaging technology segment. EAS, or ethylene absorption systems, in which ethylene absorbers such as potassium permanganate or mineral zeolites are incorporated into fresh produce packaging for the purpose of reducing ethylene levels to help extend the shelf life of produce by 3–7 days, are being used in an increasing number of commercial paper and biopolymer packaging bags and trays, including those from It’s Fresh! and BioXTEND, who are both applying ethylene management solutions across plastic-free substrate platforms.

By Application

Why Does Fresh Produce and Fruits Lead the Application Segment?

In 2025, fresh produce and fruits are the biggest application segment, accounting for around 27% of the total market revenue. It is an extraordinary convergence of urgency around food waste, regulatory push to remove plastic packaging and commercial value in the functionality of smart packaging that makes the fresh produce category one of the most ideal candidates for plastic free smart food packaging. Given that fresh produce waste is the highest of all food waste categories ranging from 45 to 55% globally across the fresh produce supply chain, there is the greatest economic urgency to invest in active and intelligent packaging for this food category. In some countries, the regulatory framework for fresh produce plastic packaging has been developed the most: plastic packaging suitable for produce is prohibited in Italy, France, Portugal, and many other markets, while EU PPWR requirements have added other requirements for compostable plastic packaging, which at the same time discourages plastic packaging and introduces requirements for plastic-free materials that can be certified as compliant with the European standards. When it comes to consumer value, packaged goods with smart packaging feature the biggest impact on fresh produce, where packaging that monitors the time-temperature chain, absorbs ethylene and detects ripeness via a freshness sensor provides immediate feedback on product quality, which directly minimizes household food waste — the consumer benefit most closely tied to the motivations for adopting plastic-free packaging for the sake of sustainability. Meat, poultry and seafood at about 21% market revenue is the highest value per pack application category, where the premium price of protein products is more than compensating for the investment in highly developed plastic-free smart packaging that incorporates high barrier biopolymer substrates, modified atmosphere packaging, oxygen scavenging active systems and freshness indicator intelligent packaging for premium retail positioning.

By End Use

Why Do Food Manufacturers Lead the End Use Segment?

In 2025, food manufacturers are estimated to occupy around 46% of the total market revenue, with their involvement in the food supply chain ranging from being the biggest volume buyer of primary food packaging to the party making packaging specification decisions that dictate which material and technology platforms are used throughout the food supply chain. Notably, a number of major food companies, such as Nestlé, Unilever, Danone, Kraft-Heinz, and General Mills, have made clear declarations to phase out plastic packaging altogether or to make significant reductions by 2025-2030, with these commitments now appearing in procurement specifications that specify plastic-free alternatives, generating the largest volume of commercial demand for plastic free smart food packaging in every market segment. Retailers’ sustainability gateway requirements continue to drive plastic free smart packaging adoption: Key food retailers such as Tesco, Carrefour, Walmart and Kroger have introduced packaging sustainability scorecards that rate and, in some cases exclude brands from supermarket shelves that don’t demonstrate their packaging sustainability compliance, which puts great commercial pressure on food manufacturers to develop plastic free smart packages. Foodservice and HoReCa account for around 28% of market revenues and are structurally important end use, as there are EU, UK, Canadian, and many other regulations or guidelines that limit the use of single-use plastic foodservice packaging, and the transition to plastic-free packaging is a requirement. Smart packaging technology integration is a growing trend in this end use segment, where plastic-free material compliance is combined with the delivery of information on provenance and allergens via QR codes.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 8.52 billion |

| Projected Market Size in 2035 | USD 26.18 billion |

| Market Size in 2025 | USD 7.43 billion |

| CAGR Growth Rate | 13.8% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Material Type, Technology, Application, End Use and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Europe Market Size?

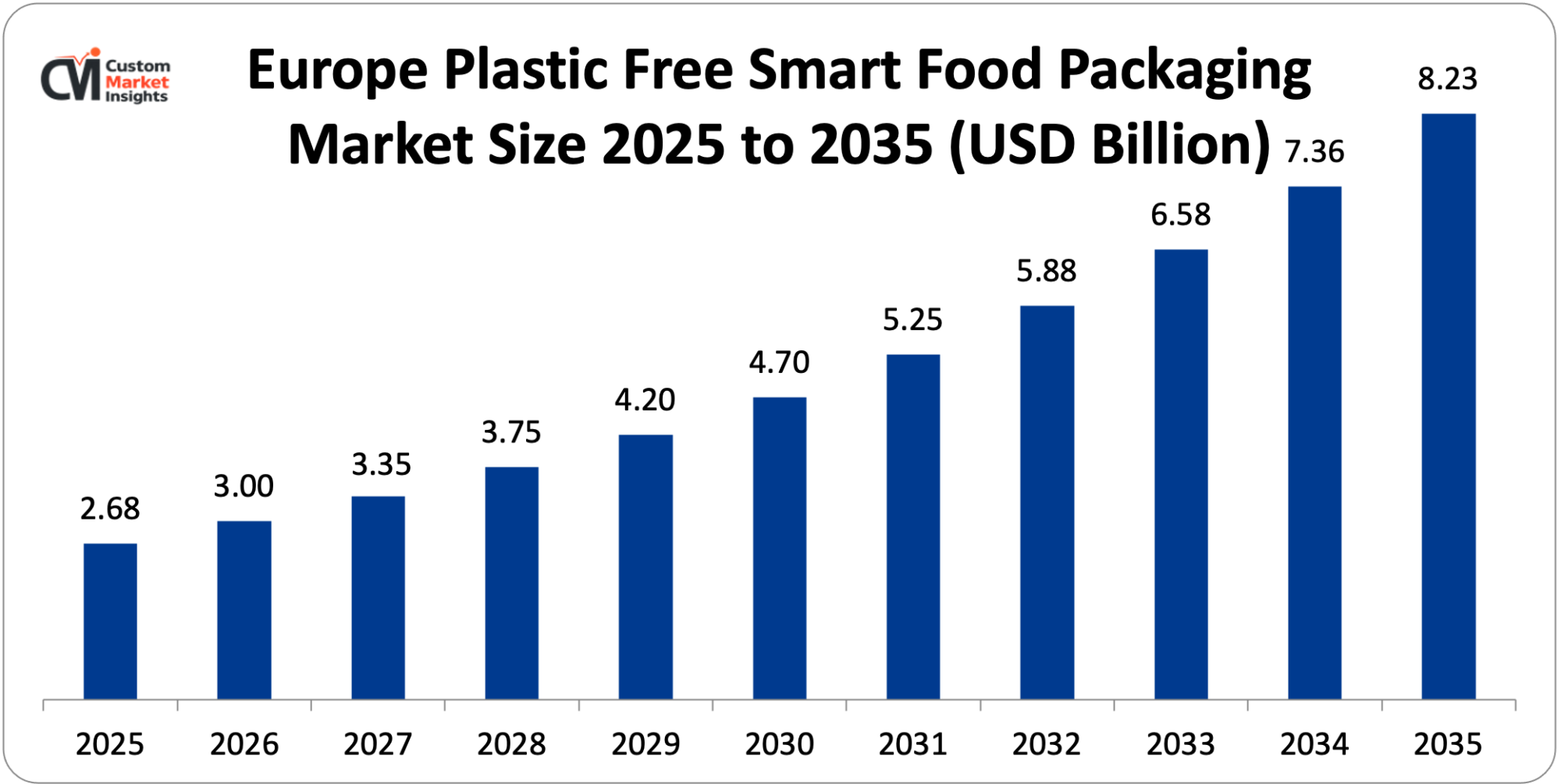

The Europe plastic free smart food packaging market size is estimated at USD 2.68 billion in 2025 and is projected to reach approximately USD 8.23 billion by 2035, growing at a CAGR of 11.9% from 2026 to 2035.

Why did Europe Dominate the Market in 2025?

Facing a global market, Europe holds about 36% of the market revenue in 2025, driven by the world’s most extensive and continuously developing regulatory framework for sustainable food packaging, highest consumer awareness and acceptance of plastic-free food packaging alternatives, greatest concentration of smart packaging technology developers and innovation companies, and a retail sector that has most aggressively adopted supplier sustainability requirements to drive food manufacturers’ packaging transitions.

The EU policy environment, with the parallel pressures of the PPWR, Single-Use Plastics Directive, Farm to Fork Strategy, and digital product passport, is unique in that the EU has a set of regulatory instruments laying down the requirements for plastic-free and smart packaging simultaneously and thereby creating the most promising commercial environment for the plastic-free smart packaging market anywhere in the world. Germany is the biggest European market, with a large food manufacturing base including brands of Nestlé, Unilever Germany and many other domestic brands, the world’s most sophisticated separate waste collection system which includes the industrial composting infrastructure necessary to validate end-of-life claims for compostable plastic packaging, and a technically sophisticated retail sector led by Rewe, Edeka, Lidl and Aldi with some of the most advanced packaging sustainability requirements anywhere in the world.

The plastic packaging tax for plastic packaging with less than 30% recycled content at GBP 200 per tonne and the ban on single-use plastics are creating direct financial incentives for a plastic-free packaging transition, thus pushing up the time horizon for commercial decisions of food manufacturers in the UK market. Swedish, Danish and Norwegian markets are among the most advanced markets, especially for smart food packaging, in the plastic free substrate context, with several groundbreaking commercial deployments of NFC in plastic free packaging and blockchain connected fresh food traceability systems for grocery retailers in these countries now proving the ability and commercial viability of integrated smart food packaging systems in the plastic free substrate context.

Why is Asia Pacific the Fastest-Growing Regional Market?

In 2025, the Asia Pacific region accounts for about 24% of global market revenue valued at approximately USD 1.78 billion, and is projected to have the highest CAGR of 16.4% from 2026 to 2035 owing to an extraordinary combination of all regulatory drivers, e-commerce growth and food safety modernization investment in China, Japan, South Korea, India and Australia, which collectively will drive the fastest growing market for plastic free smart food packaging across the world.

China’s national single-use plastics action plan, which includes phased bans on certain plastic food packaging formats and the requirement to keep track of food traceability for a growing number of food categories, is the single largest national regulatory incentive for plastic free smart packaging solutions globally, and China’s huge food manufacturing and retail sector generates the biggest volume market for smart packaging solutions.

Japan’s advanced packaging technology, as well as progressive legislation of plastic packaging restriction to start from April 2022, which is expected to push businesses to take action to reduce the use of single-use plastics, is pushing Japanese food manufacturers toward smart plastic-free packaging solutions, while Japan’s technically advanced food retail sector is providing commercial validation for advanced packaging technologies that will in turn roll out across other markets in the region.

The Act on the Promotion of Saving and Recycling of Resources in South Korea, which curtails excessive packaging and calls for recyclability and/or compostability in all packaging categories, is steadily driving market pull for smart packaging without plastic for food companies such as CJ CheilJedang, Lotte Food, and Nongshim. The Indian government’s recent roll-out of the ban on single-use plastics, the remarkable rise in organized food retail and food delivery services such as Zomato and Swiggy, and India’s ambitious plans for food traceability under the Food Safety and Standards Authority of India (FSSAI) are key factors fueling the Indian plastic free smart food packaging market, which is projected to expand at the fastest rate in the Asia Pacific region at a CAGR of 19.2% between 2026 and 2035.

Why is North America Showing Strong and Accelerating Growth?

North America is expected to remain the leader in global market revenue in 2025 with a 12.4% CAGR from 2026 to 2035, owing to the imposition of FSMA traceability regulations, plastic packaging restrictions by the states, and retailers’ sustainability initiatives, coupled with the phenomenal growth of e-commerce food delivery, which requires plastic-free smart packaging solutions for fresh food distribution. The region’s innovative packaging startups, such as packaging technology companies using seaweed (Notpla), pea protein (Xampla), or edible coatings (Apeel Sciences), have seen significant venture capital investment and are expected to provide a steady stream of new packaging technologies that can be commercially deployed during the forecast period.

Why is the Middle East & Africa Region an Emerging Opportunity?

With a CAGR of 14.1% between 2026 and 2035, the LAMEA region is expected to experience a moderate growth rate in 2025, accounting for around 9% of global market revenue, which is attributable to varied demand vectors across the region’s individual markets. GCC states (namely the UAE and Saudi Arabia) have started enacting single-use plastics policies that are in line with the global frameworks, and the UAE is introducing a ban on certain food packaging items that are considered single-use plastic from 2024 which is driving compliance demand.

Saudi Arabia’s food safety and traceability programs, Vision 2030 and 2032, are encouraging smart packaging in the country’s fast-modernizing food retail market, which is dominated by Panda Retail and Carrefour KSA. The extended producer responsibility regulations for packaging in South Africa, which came into effect from May 2023, are providing market incentives for food manufacturers in South Africa to switch to a plastic-free packaging approach. Brazil is the leading Latin American market for plastic free smart food packaging: the food traceability requirements by ANVISA and the single-use plastics ban by municipalities in São Paulo and Rio de Janeiro are contributing to increased uptake.

Top Players in the Market and Their Offerings

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- Sealed Air Corporation

- Huhtamaki Oyj

- Sonoco Products Company

- DS Smith plc

- Notpla Ltd.

- Novamont S.p.A.

- Stora Enso Oyj

- Others

Key Developments

The market has experienced a number of changes, with various companies striving to expand their products and capabilities.

- In March 2025: Mondi Group announced the commercial launch of its FunctionalBarrier Paper PRO platform which includes an ultra-thin water-based PLA dispersion barrier coating that delivers grease resistance, moisture vapor barrier (MVB) and oxygen barrier properties, allowing the direct replacement of polyethylene-coated paper and multi-layer plastic laminates in dry food, confectionery and chilled dairy packaging applications as well as the integration capability to apply water-resistant NFC antenna lamination to a 100% plastic-free, curbside-recyclable, how2recycle and FEFCO European certified substrate, which makes it the most comprehensive commercially deployed convergence of plastic-free material performance and smart packaging connectivity functionality in paper-based food packaging.

- In February 2025: Stora Enso Oyj entered into a strategic collaboration with PragmatIC, a developer of flexible integrated circuit technology (FlexIC) for NFC smart packaging, to create NFC-enabled paperboard packaging for fresh food applications, where the integration of NFC at volume is currently cost-prohibitive for conventional silicon ICs due to high NFC chip integration prices.

These strategic activities have led companies to be better positioned in the market, have enabled them to build new smart packaging platforms with plastic-free materials that meet the convergence of market and regulatory needs for sustainable packaging compliance and supply chain intelligence, have shortened the cost reduction curve for the implementation of smart packaging technology on sustainable packaging materials and have made great strides toward capturing the unprecedented structural growth momentum of being required to have plastic-free packaging in an international environment while the digital food traceability industry is expanding at the same time across all key food markets around the world.

The Plastic Free Smart Food Packaging Market is segmented as follows:

By Material Type

- Paper & Paperboard

- Coated Paperboard

- Uncoated Kraft Paper

- Barrier-Coated Paper Systems

- Molded Fiber

- Aluminum Foil & Metallized Films

- Aluminum Foil Laminates

- Bio-Based Metallized Films

- Aluminum Composite Laminates

- Glass

- Primary Food Contact Glass Containers

- Smart Glass Packaging with Sensor Integration

- Biopolymer-Based Materials

- PLA-Based Films & Laminates

- PHA-Based Films

- Cellulose-Based Films (NatureFlex)

- Chitosan Films

- Starch-Based Composite Films

- Plant-Based Composites

- Sugarcane Bagasse Composites

- Bamboo Fiber Composites

- Hemp & Flax Fiber Composites

- Agricultural Waste Composites

- Other Material Types

By Technology

- Active Packaging

- Oxygen Scavengers

- Antimicrobial Active Systems

- Moisture Regulators & Desiccants

- Ethylene Absorbers

- Carbon Dioxide Emitters

- Intelligent Packaging

- Time-Temperature Indicators (TTI)

- Freshness Sensors & Indicators

- NFC & RFID-Enabled Packaging

- QR Code & Blockchain-Connected Packaging

- Gas Sensors & Biosensors

- Modified Atmosphere Packaging

- Controlled Atmosphere Packaging

- Equilibrium Modified Atmosphere

- Edible Packaging

- Seaweed-Based Edible Films

- Protein-Based Edible Coatings

- Starch-Based Edible Films

- Water-Soluble Packaging

- Other Technologies

By Application

- Fresh Produce & Fruits

- Meat, Poultry & Seafood

- Dairy Products

- Bakery & Confectionery

- Beverages

- Ready Meals & Convenience Foods

- Other Applications

By End Use

- Food Manufacturers

- Foodservice & HoReCa

- Retail & Grocery

- Other End Uses

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Plastic Free Smart Food Packaging by Segments

- 2.1.2. Plastic Free Smart Food Packaging by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Plastic Free Smart Food Packaging Market Attractiveness Analysis, By Material Type

- 2.2.3. Plastic Free Smart Food Packaging Market Attractiveness Analysis, By Technology

- 2.2.4. Plastic Free Smart Food Packaging Market Attractiveness Analysis, By Application

- 2.2.5. Plastic Free Smart Food Packaging Market Attractiveness Analysis, By End Use

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Converging Regulatory Mandates Simultaneously Eliminating Plastic Packaging and Mandating Food Traceability Creating Unified Market Demand

- 3.1.2. Food Waste Reduction Imperative Driving Functional Packaging Innovation Beyond Simple Plastic Substitution

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Plastic Free Smart Food Packaging Market – By Material Type

- 4.1. Material Type Market Overview, By Material Type Segment

- 4.1.1. Plastic Free Smart Food Packaging Market Revenue Share, By Material Type, 2025 & 2035

- 4.1.2. Paper & Paperboard

- 4.1.2.1. Coated Paperboard

- 4.1.2.2. Uncoated Kraft Paper

- 4.1.2.3. Barrier-Coated Paper Systems

- 4.1.2.4. Molded Fiber

- 4.1.3. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Aluminum Foil & Metallized Films

- 4.1.6.1. Aluminum Foil Laminates

- 4.1.6.2. Bio-Based Metallized Films

- 4.1.6.3. Aluminum Composite Laminates

- 4.1.7. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Glass

- 4.1.10.1. Primary Food Contact Glass Containers

- 4.1.10.2. Smart Glass Packaging with Sensor Integration

- 4.1.11. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Biopolymer-Based Materials

- 4.1.14.1. PLA-Based Films & Laminates

- 4.1.14.2. PHA-Based Films

- 4.1.14.3. Cellulose-Based Films (NatureFlex)

- 4.1.14.4. Chitosan Films

- 4.1.14.5. Starch-Based Composite Films

- 4.1.15. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Plant-Based Composites

- 4.1.18.1. Sugarcane Bagasse Composites

- 4.1.18.2. Bamboo Fiber Composites

- 4.1.18.3. Agricultural Waste Composites

- 4.1.18.4. Hemp & Flax Fiber Composites

- 4.1.19. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Other Material Types

- 4.1.23. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Material Type Market Overview, By Material Type Segment

- Chapter 5. Plastic Free Smart Food Packaging Market – By Technology

- 5.1. Technology Market Overview, By Technology Segment

- 5.1.1. Plastic Free Smart Food Packaging Market Revenue Share, By Technology, 2025 & 2035

- 5.1.2. Active Packaging

- 5.1.2.1. Oxygen Scavengers

- 5.1.2.2. Antimicrobial Active Systems

- 5.1.2.3. Moisture Regulators & Desiccants

- 5.1.2.4. Ethylene Absorbers

- 5.1.2.5. Carbon Dioxide Emitters

- 5.1.3. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Intelligent Packaging

- 5.1.6.1. Time-Temperature Indicators (TTI)

- 5.1.6.2. Freshness Sensors & Indicators

- 5.1.6.3. NFC & RFID-Enabled Packaging

- 5.1.6.4. QR Code & Blockchain-Connected Packaging

- 5.1.6.5. Gas Sensors & Biosensors

- 5.1.7. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Modified Atmosphere Packaging

- 5.1.10.1. Controlled Atmosphere Packaging

- 5.1.10.2. Equilibrium Modified Atmosphere

- 5.1.11. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Edible Packaging

- 5.1.14.1. Seaweed-Based Edible Films

- 5.1.14.2. Protein-Based Edible Coatings

- 5.1.14.3. Starch-Based Edible Films

- 5.1.14.4. Water-Soluble Packaging

- 5.1.15. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Other Technologies

- 5.1.19. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Technology Market Overview, By Technology Segment

- Chapter 6. Plastic Free Smart Food Packaging Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Plastic Free Smart Food Packaging Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Fresh Produce & Fruits

- 6.1.3. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Meat, Poultry & Seafood

- 6.1.7. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Dairy Products

- 6.1.11. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Bakery & Confectionery

- 6.1.15. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Beverages

- 6.1.19. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Ready Meals & Convenience Foods

- 6.1.23. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1.26. Other Applications

- 6.1.27. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 6.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.29. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Plastic Free Smart Food Packaging Market – By End Use

- 7.1. End Use Market Overview, By End Use Segment

- 7.1.1. Plastic Free Smart Food Packaging Market Revenue Share, By End Use, 2025 & 2035

- 7.1.2. Food Manufacturers

- 7.1.3. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Foodservice & HoReCa

- 7.1.7. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Retail & Grocery

- 7.1.11. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Other End Uses

- 7.1.15. Plastic Free Smart Food Packaging Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End Use Market Overview, By End Use Segment

- Chapter 8. Plastic Free Smart Food Packaging Market – Regional Analysis

- 8.1. Plastic Free Smart Food Packaging Market Overview, By Region Segment

- 8.1.1. Global Plastic Free Smart Food Packaging Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Plastic Free Smart Food Packaging Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Plastic Free Smart Food Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.1.4. Global Plastic Free Smart Food Packaging Market Revenue, By Technology, 2026 – 2035

- 8.1.5. Global Plastic Free Smart Food Packaging Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Plastic Free Smart Food Packaging Market Revenue, By End Use, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Plastic Free Smart Food Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Plastic Free Smart Food Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.2.3. North America Plastic Free Smart Food Packaging Market Revenue, By Technology, 2026 – 2035

- 8.2.4. North America Plastic Free Smart Food Packaging Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Plastic Free Smart Food Packaging Market Revenue, By End Use, 2026 – 2035

- 8.2.6. U.S. Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Plastic Free Smart Food Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Plastic Free Smart Food Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.3.3. Europe Plastic Free Smart Food Packaging Market Revenue, By Technology, 2026 – 2035

- 8.3.4. Europe Plastic Free Smart Food Packaging Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Plastic Free Smart Food Packaging Market Revenue, By End Use, 2026 – 2035

- 8.3.6. Germany Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Plastic Free Smart Food Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Plastic Free Smart Food Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.4.3. Asia Pacific Plastic Free Smart Food Packaging Market Revenue, By Technology, 2026 – 2035

- 8.4.4. Asia Pacific Plastic Free Smart Food Packaging Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Plastic Free Smart Food Packaging Market Revenue, By End Use, 2026 – 2035

- 8.4.6. China Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Plastic Free Smart Food Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Plastic Free Smart Food Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Plastic Free Smart Food Packaging Market Revenue, By Technology, 2026 – 2035

- 8.5.4. The Middle-East and Africa Plastic Free Smart Food Packaging Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Plastic Free Smart Food Packaging Market Revenue, By End Use, 2026 – 2035

- 8.5.6. Saudi Arabia Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Plastic Free Smart Food Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Plastic Free Smart Food Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.6.3. Latin America Plastic Free Smart Food Packaging Market Revenue, By Technology, 2026 – 2035

- 8.6.4. Latin America Plastic Free Smart Food Packaging Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Plastic Free Smart Food Packaging Market Revenue, By End Use, 2026 – 2035

- 8.6.6. Brazil Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Plastic Free Smart Food Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Plastic Free Smart Food Packaging Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Plastic Free Smart Food Packaging Market: Company Market Share, 2025

- 9.2. Global Plastic Free Smart Food Packaging Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Amcor plc

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Mondi Group

- 10.3. Smurfit Kappa Group

- 10.4. Sealed Air Corporation

- 10.5. Huhtamaki Oyj

- 10.6. Sonoco Products Company

- 10.7. DS Smith plc

- 10.8. Notpla Ltd.

- 10.9. Novamont S.p.A.

- 10.10. Stora Enso Oyj

- 10.11. Others.

- 10.1. Amcor plc

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 74

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- Sealed Air Corporation

- Huhtamaki Oyj

- Sonoco Products Company

- DS Smith plc

- Notpla Ltd.

- Novamont S.p.A.

- Stora Enso Oyj

- Others

FAQs

The key players in the market are Amcor plc, Mondi Group, Smurfit Kappa Group, Sealed Air Corporation, Huhtamaki Oyj, Sonoco Products Company, DS Smith plc, Notpla Ltd., Novamont S.p.A., Stora Enso Oyj, Others.

Government regulation is the main catalyst for market development for plastic free smart food packaging, working through a series of parallel regulatory processes that collectively are making the combination of plastic-free materials and smart functionality more obligatory than beneficial. The demand foundation for plastic-free packaging materials is laid by plastic packaging elimination regulations; the EU PPWR, SUPD, national single-use plastic bans, and state-level packaging laws directly target a number of packaging categories and markets for the transition to plastic-free substrates. The demand foundation for smart packaging connectivity adoption is formed and provided by the food traceability requirements such as the FSMA Food Traceability Final Rule, EU Farm to Fork traceability requirements, China’s food safety traceability framework, and FSSAI India traceability mandates. Extended producer responsibility (EPR) systems in France, Germany, the UK and increasingly in the Asia Pacific involve economic responsibility and financial obligations for packaging producers and brand owners that are linked to packaging sustainability performance, with the most advantageous EPR fee structures relating to certified compostable and recyclable plastic-free packaging and further incentivizing material transition. Regulatory push on product quality and safety rules regarding fresh food shelf life labelling, such as EU Regulation 1169/2011 and proposed changes to the freshness communication rules for dynamic date labelling, facilitated by smart packaging technology, could see intelligent packaging freshness monitoring solutions being viewed more as a regulatory compliance enabler than a premium differentiator, giving the plastic free smart packaging market a chance to place its technology platform in a better light.

The price premium of plastic free smart food packaging is significantly different from conventional plastic packaging baselines in both the plastic free material and the smart technology integration aspect, depending on the actual application, material platform and the level of technology sophistication. When used for dry food applications, barrier packaged products can be sold for 15–35% more than an equivalent plastic flexible packaging product at the current production scale, but this premium is expected to narrow to 5–15% by 2030, due to increased production scale of barrier paper and reduced costs of barrier coatings. The prices for biopolymer-based active packaging for fresh food applications are 45-80% higher than the prices of conventional MAP packages made using plastic packaging films, due to the cost of packaging films as well as the cost of integration of the active packaging components. NFC-enabled smart paper packaging offers per-unit premiums of USD 0.04–0.12 over equivalent non-connected packaging without plastic elements, making it economically viable for use in brand engagement, supply chain traceability, and anti-counterfeiting applications where the smart functionality can provide a measurable commercial value above the incremental packaging cost. Currently the most sophisticated plastic free smart packaging solutions, such as a PHA film pouch with an oxygen scavenging layer, NFC traceability connectivity and a freshness indicator, are commanding premiums of up to 200% above conventional plastic packaging solutions depending upon the product application, with premium food and specialty food applications justifying the packaging cost increment by the value the packaging generates for the consumer and supply chain through a long shelf life and providing the traceability and communication evidence of origin.

The global regulatory framework convergence, which at the same time is reducing plastic packaging while introducing new plastic-free regulatory requirements, will drive the market forward and will be complemented by the commercial ROI justification for smart packaging investment – even in the absence of sustainability considerations – as declining NFC and RFID integration costs will support the deployment of smart packaging solutions on mass-market food packaging, along with the geographic expansion of both plastic-free packaging regulatory requirements and food traceability mandates across Asia Pacific and LAMEA, creating new large-scale demand centers for packaged plastic free smart food packaging solutions at a CAGR of 13.8% from 2026 to 2035.

With such a high differential in revenue growth rates, Europe will have the biggest revenue share in the early years of the forecast period (roughly 32% of global market revenue in 2030) but will be overtaken by Asia Pacific revenue growth, with Asia Pacific forecast to exceed European revenue growth in 2033. Europe’s continued dominance is due to the most complete and effective regulatory framework that requires plastic removal while enforcing requirements for traceability; the highest consumer awareness and acceptance of plastic-free smart packaging; and the largest number of smart packaging technology innovators and producers of sustainable materials, with their commercial infrastructures supporting premium pricing and first-mover positioning in the most technically advanced market applications.

Asia Pacific will be seeing the highest CAGR of 16.4% between 2026 and 2035 due to the introduction of the world’s largest national single-use plastics action plan by China, the growing FSSAI traceability requirements driving the packaging recycling market in India, Japan’s progressive plastic restriction legislation, packaging recycling requirements in South Korea creating plastic-free transition mandates, and the region’s exceptional growth of the fresh food e-commerce platform, which will boost demands for packaging that performs freshness management and is plastic-free. The world’s fastest growth of consumer food sales, the most dynamic regulatory development for plastic-free packaging, and the fastest growth of fresh food e-commerce infrastructure all combine to create a uniquely powerful demand environment for plastic-free smart food packaging in Asia Pacific.

The United States Food Traceability Final Rule, which takes effect beginning in January 2026, will drive a significant increase in the regulatory demand for plastic-free smart packaging, particularly within the U.S. food supply chain; the EU PPWR, which will require all plastic packaging to be reusable, recyclable or compostable by 2030, will further create a unified global regulatory push for plastic-free smart packaging; and China’s national single-use plastics action plan, comprising the world’s largest single national market, will provide a significant regulatory catalyst to drive the plastic-free packaging transition. Global food waste is estimated at 1.3 billion tonnes per year accounting for a USD 1 trillion loss in the value of food, compelling a commercial case for active and intelligent packaging technology to extend the shelf life of food products; NFC antenna integration costs on paper substrates are declining towards USD 0.03-0.08 per unit, making smart paper packaging economically viable across mass market food categories; biopolymer-based technology is achieving performance parity with plastic packaging and making it economically viable to integrate active and intelligent packaging technology in food packaging; European grocery retail pilot deployments are demonstrating food waste reduction up to 12-22%; and India’s plastic free smart food packaging market is growing at approximately 19.2% CAGR representing one of the fastest individual national market growth rates globally.