Advanced Driver Assistance Systems (ADAS) Market Size, Trends and Insights By Component (Processor, Sensors, Software, Others), By Solution (Adaptive Cruise Control (ACC), Park Assistance, Blind Spot Detection System (BSD), Tire Pressure Monitoring System (TPMS), Lane Departure Warning System (LDWS), Adaptive Front Lights (AFL), Autonomous Emergency Braking (AEB), Others), By Vehicle (Passenger Cars, Commercial Vehicle), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 12.5%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- Aptiv PLC

- Robert Bosch GmbH

- DENSO Corporation

- Continental AG

- Others

Reports Description

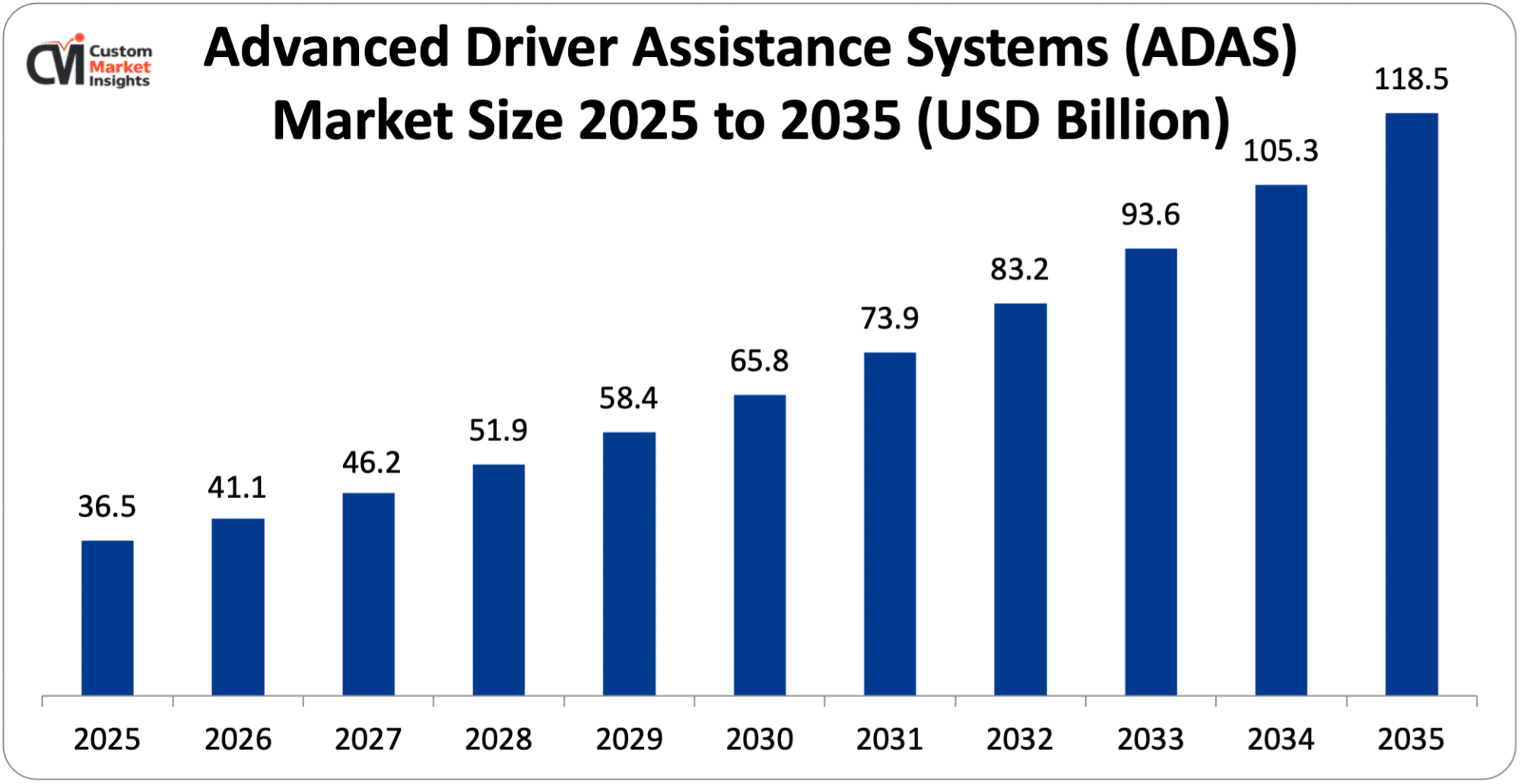

The market size of global Advanced Driver Assistance Systems (ADAS) will be estimated at USD 36.5 billion in 2025 and is expected to grow to between USD 41.1 billion in 2026 and about USD 118.5 billion by 2035, with a current CAGR (compound annual growth rate) of 12.5% during the period of 2026 to 2035. Advanced Driver Assistance Systems (ADAS) are defined as the collection of electronic systems installed in road vehicles that modify the driving task to enhance safety and vehicle control and to support driver decisions. Such can be achieved by processing and interpreting vehicle and environment information via sensors, cameras, radar, and software in order to alert the drivers of hazardous situations or even automatically react. Examples are automatic braking, blind spot detection, lane departure, automatic parking, and others. Since human error contributes to 90% of all accidents, the implementation of ADAS can significantly contribute to safer roads and is regarded as a precursor to future mostly autonomous mobility.

Market Highlight

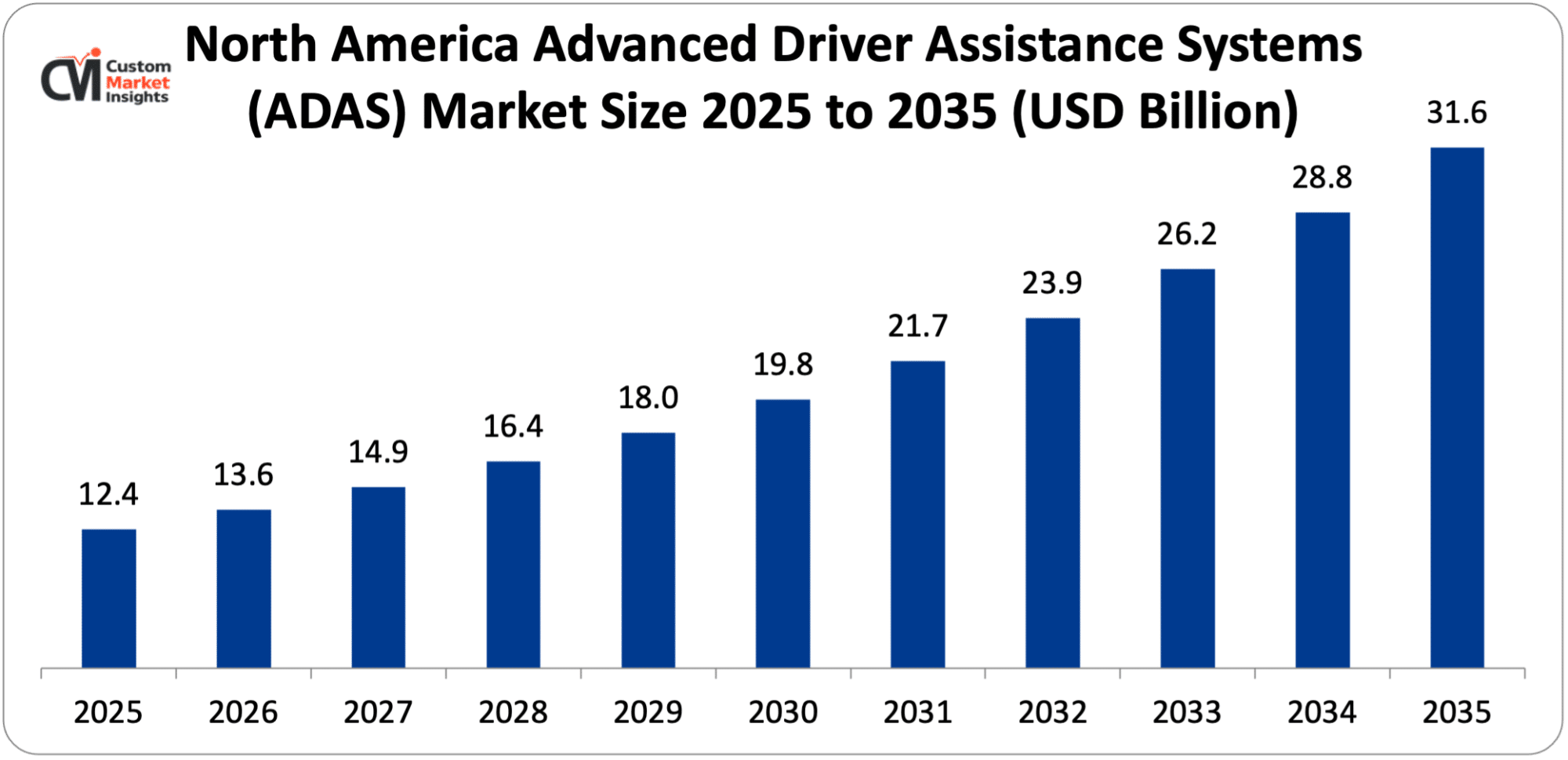

- In 2025, North America will dominate the global market with an estimated market share of 34%. This growth is driven by the region’s increasing adoption of advanced technology.

- The Asia Pacific is growing at a highest CAGR over the analysis period. Increasing demand for EV drives the industry growth.

- By component, the sensor segment accounted for the highest revenue share in 2025.

- By solution, the Adaptive Cruise Control (ACC) segment would have the highest share of the market in 2025 of 18.5%.

- By vehicle, the passenger car segment dominated the market in 2025.

Significant Growth Factors

The Advanced Driver Assistance Systems (ADAS) market trends present significant growth opportunities due to several factors:

- Increasing Focus on Vehicle Safety: The shift in focus from vehicle comfort to safety will drive the growth of the ADAS market. Governments and automakers, as well as the general public, have started placing more importance on the need to avoid traffic accidents and, hence, the need for ADAS. Since a majority of accidents take place due to human error, there is a rising demand for sensors and other technologies that can actively assist the vehicle driver and prevent accidents, such as automatic emergency braking systems, lane departure warning systems, blind-spot detection systems, and adaptive cruise control. More stringent industry safety regulations and the development of crash-test rating programs have seen a rise in the use of ADAS in premium as well as mass-market vehicles. As the buying behavior of consumers shifts toward more safety features, consumer awareness will make ADAS more of a requirement than a luxury, instigating higher growth.

- Growth in Electric Vehicles (EVs) & Premium Cars: The growth of electric vehicles and the luxury car segment is significantly contributing to the expansion of the ADAS market, as these segments are the first to adopt new technologies. Electric vehicle makers like Nissan and Chevrolet are now promoting features like ADAS an forward collision warning system, as part of their standard offerings; this is the future of intelligent, connected mobility. Premium and luxury segments of the car industry have been experimentally testing a whole bunch of new features, including automatic parking systems, lane departure warnings, adaptive cruise controls, and collision mitigation, and these are now increasingly finding their way into mid-range cars too. The growing consumption of electric vehicles across the world, driven by emissions and fluctuations in fuel prices, and the increasing adoption of high-end vehicles with all the latest safety features, compensating for falling battery prices and greater access to resources, are driving the growth in the ADAS market.

What are the Major Advances Changing the Advanced Driver Assistance Systems (ADAS) Market Today?

- Artificial Intelligence (AI) & Machine Learning Integration: The integration of artificial intelligence (AI) and machine learning (ML) can be considered one of the most prominent trends taking place in the ADAS market. This technology is bringing a whole new level of significance to ADAS by moving away from conventional rule-based systems; these AI-enabled systems are capable of studying both the environment around a vehicle and the vehicle’s existing surroundings, allowing them to accurately identify most objects or hazards, such as pedestrians, vehicles, or street signs. Using ML techniques, the ability of an ADAS to study a broader spectrum of driving scenarios from various road types can be markedly increased. This, in turn, can see ADAS gradually moving from basic warning systems to proactive technology like predicting the onset of a collision before it happens and helping the vehicle and the system drive more intelligently to avoid it.

- Evolution of LiDAR & Radar Technologies: The advancement in the field of LiDAR and Radar has significantly advanced the ADAS market, now evolving in a way that enhances the precision and dependability of vehicle perception systems. With the emergence of 3D High-Definition solid state LiDAR technology, the sensors that were earlier large mechanical devices that emitted and detected laser beams have morphed into small, affordable devices that are capable of producing high resolution, 3-dimensional maps of the world around the vehicle. The automotive radar sensors are also evolving, namely into 4D imaging radar, which can compute object distance, velocity, azimuth, and elevation with great precision even while traversing through rain, dust, or fog. With these developments in sensing technology, ADAS will be able to boast about better sensor fusion and will be able to bank upon a more holistic picture of the world around the vehicle at every instant of time. This will facilitate the proper functioning of various ADAS functions like automatic emergency braking, adaptive cruising, and even vehicle pilot-ship, and ultimately vehicle independence.

Category Wise Insights

By Component

Why Sensor Hold a Prominent Position in the Market?

The sensor segment accounted for the highest revenue share in 2025. Sensors are responsible for the active operating mode of ADAS. Sensors provide data about the vehicle’s environment, recognize objects, pedestrians, lanes, and surrounding vehicles, recognize approaching hazards, and give system information and driver assistance. The working of ADAS is based on sensors and their working correctness. LIDAR, RADAR, ultrasonic, camera, and other sensors collaborate and execute the required assistance and safety function.

The processor segment is growing at a highest CAGR during the forecast period. The growth is due to the rising demand for higher and more complex automotive systems. ADAS systems require high-powered processors to execute the complex algorithms necessary for object detection, motion tracking, and decision-making. Higher-powered processors may allow automotive systems to perform even more complex functions such as lane-keeping assistance and adaptive cruise control.

By Solution

Why Adaptive Cruise Control (ACC) Capture the Highest Market Share in the Advanced Driver Assistance Systems (ADAS) Market?

The Adaptive Cruise Control (ACC) segment would have the highest share of the market in 2025 of 18.5%. The combination of higher safety feature demands and advanced sensor and radar technology and government regulations that require commercial vehicles to have ACC systems is driving current market growth. The segment experiences growth because more people are using electric vehicles and hybrid vehicles.

The Blind Spot Detection System (BSD) segment is growing at a rapid rate over the projected period. BSD systems employ sensors which track vehicle movements within a driver’s blind spot while they provide visual and audible alerts to the driver. The system prevents accidents by alerting drivers when they attempt to change lanes without performing blind spot checks. The BSD segment experiences growth because of two factors which include rising safety feature requirements and technological progress. The system has gained higher affordability and greater dependability since its introduction.

By Vehicle

Does the Passenger Cars Capture Majority of Market Share in the Advanced Driver Assistance Systems (ADAS) Market?

The passenger car segment dominated the market in 2025. The market segment is experiencing growth because of the rising supply of luxury vehicles, motor vehicles, electric cars, hybrids, and others, from the developed countries of the world to the cities. Awareness among customers about safety, safety assistance technology, default security measures, and combinations thereof is increasing from consumers. Many Asia Pacific, North American, and European countries have already had a certain set of regulations established for the passenger car segment consisting of many types of ADAS. Vision Zero has planned to decrease the number of deaths to zero in the European Union by 2050. The authority has plans for a 50% counteractive speed reduction and casualty reduction by 2030.

The commercial vehicle segment is growing at a rapid rate over the projected period. Safety and security are some of the key features of commercial vehicles owing to the rising number of transportation and logistics players inclined toward adopting newer technologies. The boom in industries such as e-commerce, online retail, shipping and logistics, consumer products, and agriculture, among others, has accentuated this trend.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 41.1 billion |

| Projected Market Size in 2035 | USD 118.5 billion |

| Market Size in 2025 | USD 36.5 billion |

| CAGR Growth Rate | 12.5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Component, Solution, Vehicle and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is North America Advanced Driver Assistance Systems (ADAS) Market Size?

Its market size, in terms of North America Advanced Driver Assistance Systems (ADAS), is projected to be USD 12.41 billion in 2025 with a growth of about USD 31.6 billion in 2035 with a CAGR of 9.8% between 2026 and 2035.

Why did North America Dominate the Advanced Driver Assistance Systems (ADAS) Market in 2025?

In 2025, North America will dominate the global market with an estimated market share of 34%. This is due to the technological development in the automotive industry and the presence of few major players in this region. Additionally, the higher adoption of new technology and better economic situation in this region are fueling the growth of this market. Growing death rate and increasing sales of high-end vehicles in this region, such as in Canada and US is fueling the growth of this market.

US Advanced Driver Assistance Systems (ADAS) Market Trends

In North America region, US is expected to dominate the market over the projected period. This market is mainly driven by the availability of several global manufacturers for passenger cars and commercial vehicles in the country, growing awareness about the need for safety assistance, and the stringent rules about the safety standards in the country. The growth of the market is driven by the availability of advanced technologies and the presence of several IT & telecom industry companies in the U.S.

Why is Europe Experiencing a Significant Growth in the Advanced Driver Assistance Systems (ADAS) Market?

Europe holds a significant market share in 2025. The reasons responsible for the growth of this market include rules related to the performance of vehicles from a security perspective in the EU, a rise in demand for PCCs with sophisticated technology, increasing preferences for electric and hybrid vehicles, and the presence of more than one car manufacturing company in this region.

Germany Advanced Driver Assistance Systems (ADAS) Market Trends

Germany held the dominant position in the market in 2025. The strength of the manufacturing industry in this country, coupled with the growing tendency of manufacturers to add more advanced features and increased demands for passenger cars with the current capabilities, has fueled the increase.

Why is the Asia Pacific Growing at a Highest CAGR in the Advanced Driver Assistance Systems (ADAS) Market?

The Asia Pacific is expected to grow at a significant rate over the projected period. The region growing government initiatives for safety and increasing demand for advanced technology in passenger vehicle.

India Advanced Driver Assistance Systems (ADAS) Market Trends

India holds the prominent market share in the industry. Increasing disposable income of population and growing focus on safety propel the industry expansion.

Why is the Middle East & Africa Region is growing rapidly in the Advanced Driver Assistance Systems (ADAS)?

The MEA region is growing at a steady rate over the projected period. The growth in sales of passenger vehicles and increasing investment in advanced technology.

UAE Advanced Driver Assistance Systems (ADAS) Market Trends

UAE is growing at the highest CAGR during the forecast period. The increasing innovative product launch and investment in advanced infrastructure drives the market growth.

Top Players in the Advanced Driver Assistance Systems (ADAS) Market and Their Offerings

- Aptiv PLC

- Robert Bosch GmbH

- DENSO Corporation

- Continental AG

- ZF Friedrichshafen AG

- Magna International

- NXP Semiconductors

- Hyundai Mobis

- Aisin Corporation

- Mobileye (Intel)

- NVIDIA Corporation

- Valeo SA

- Infineon Technologies

- Renesas Electronics

- ]ON Semiconductor

- STMicroelectronics

- Hitachi Astemo

- Autoliv Inc.

- Others

Key Developments

Advanced Driver Assistance Systems (ADAS) market has experienced considerable changes in the last two years as the market players are trying to diversify their technological aspects and develop product portfolio using strategic approaches.

- In January 2025, Garmin presented its latest innovation, Unified Cabin 2025, during the Consumer Electronics Show, hosted in Las Vegas, U.S. Some of the additional features associated with the solution include Ultra-Wide Band (UWB) technology that provides Child Presence Detection (CPD), enhanced blind spot visions, improved computer vision and augmented reality capabilities, and more.

- In January 2025, InfineonTechnologies AG announced the establishment of a new business unit, which aims to combine existing sensor and radio frequency businesses into one organization to strengthen growth in the sensors market. The newly formed SURF (Sensor Units & Radio Frequency) business unit is part of the Power & Sensor Systems (PSS) division.

These strategic measures have enabled the companies to reinforce their competitive positions, increase the product line, boost their technological competencies and also seize growth opportunities in the fast-growing Advanced Driver Assistance Systems (ADAS) market.

The Advanced Driver Assistance Systems (ADAS) Market is segmented as follows:

By Component

- Processor

- Sensors

- Software

- Others

By Solution

- Adaptive Cruise Control (ACC)

- Park Assistance

- Blind Spot Detection System (BSD)

- Tire Pressure Monitoring System (TPMS)

- Lane Departure Warning System (LDWS)

- Adaptive Front Lights (AFL)

- Autonomous Emergency Braking (AEB)

- Others

By Vehicle

- Passenger Cars

- Commercial Vehicle

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Advanced Driver Assistance Systems (ADAS) by Segments

- 2.1.2. Advanced Driver Assistance Systems (ADAS) by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Advanced Driver Assistance Systems (ADAS) Market Attractiveness Analysis, By Component

- 2.2.3. Advanced Driver Assistance Systems (ADAS) Market Attractiveness Analysis, By Solution

- 2.2.4. Advanced Driver Assistance Systems (ADAS) Market Attractiveness Analysis, By Vehicle

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Increasing Focus on Vehicle Safety

- 3.1.2. Growth in Electric Vehicles (EVs) & Premium Cars

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Advanced Driver Assistance Systems (ADAS) Market – By Component

- 4.1. Component Market Overview, By Component Segment

- 4.1.1. Advanced Driver Assistance Systems (ADAS) Market Revenue Share, By Component, 2025 & 2035

- 4.1.2. Processor

- 4.1.3. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Sensors

- 4.1.7. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Software

- 4.1.11. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Others

- 4.1.15. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Component Market Overview, By Component Segment

- Chapter 5. Advanced Driver Assistance Systems (ADAS) Market – By Solution

- 5.1. Solution Market Overview, By Solution Segment

- 5.1.1. Advanced Driver Assistance Systems (ADAS) Market Revenue Share, By Solution, 2025 & 2035

- 5.1.2. Adaptive Cruise Control (ACC)

- 5.1.3. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Park Assistance

- 5.1.7. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Blind Spot Detection System (BSD)

- 5.1.11. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Tire Pressure Monitoring System (TPMS)

- 5.1.15. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Lane Departure Warning System (LDWS)

- 5.1.19. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Adaptive Front Lights (AFL)

- 5.1.23. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1.26. Autonomous Emergency Braking (AEB)

- 5.1.27. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 5.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.29. Key Market Trends, Growth Factors, & Opportunities

- 5.1.30. Others

- 5.1.31. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 5.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.33. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Solution Market Overview, By Solution Segment

- Chapter 6. Advanced Driver Assistance Systems (ADAS) Market – By Vehicle

- 6.1. Vehicle Market Overview, By Vehicle Segment

- 6.1.1. Advanced Driver Assistance Systems (ADAS) Market Revenue Share, By Vehicle, 2025 & 2035

- 6.1.2. Passenger Cars

- 6.1.3. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Commercial Vehicle

- 6.1.7. Advanced Driver Assistance Systems (ADAS) Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Vehicle Market Overview, By Vehicle Segment

- Chapter 7. Advanced Driver Assistance Systems (ADAS) Market – Regional Analysis

- 7.1. Advanced Driver Assistance Systems (ADAS) Market Overview, By Region Segment

- 7.1.1. Global Advanced Driver Assistance Systems (ADAS) Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Advanced Driver Assistance Systems (ADAS) Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Advanced Driver Assistance Systems (ADAS) Market Revenue, By Component, 2026 – 2035

- 7.1.4. Global Advanced Driver Assistance Systems (ADAS) Market Revenue, By Solution, 2026 – 2035

- 7.1.5. Global Advanced Driver Assistance Systems (ADAS) Market Revenue, By Vehicle, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Advanced Driver Assistance Systems (ADAS) Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Advanced Driver Assistance Systems (ADAS) Market Revenue, By Component, 2026 – 2035

- 7.2.3. North America Advanced Driver Assistance Systems (ADAS) Market Revenue, By Solution, 2026 – 2035

- 7.2.4. North America Advanced Driver Assistance Systems (ADAS) Market Revenue, By Vehicle, 2026 – 2035

- 7.2.5. U.S. Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Advanced Driver Assistance Systems (ADAS) Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Advanced Driver Assistance Systems (ADAS) Market Revenue, By Component, 2026 – 2035

- 7.3.3. Europe Advanced Driver Assistance Systems (ADAS) Market Revenue, By Solution, 2026 – 2035

- 7.3.4. Europe Advanced Driver Assistance Systems (ADAS) Market Revenue, By Vehicle, 2026 – 2035

- 7.3.5. Germany Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Advanced Driver Assistance Systems (ADAS) Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Advanced Driver Assistance Systems (ADAS) Market Revenue, By Component, 2026 – 2035

- 7.4.3. Asia Pacific Advanced Driver Assistance Systems (ADAS) Market Revenue, By Solution, 2026 – 2035

- 7.4.4. Asia Pacific Advanced Driver Assistance Systems (ADAS) Market Revenue, By Vehicle, 2026 – 2035

- 7.4.5. China Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Advanced Driver Assistance Systems (ADAS) Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Advanced Driver Assistance Systems (ADAS) Market Revenue, By Component, 2026 – 2035

- 7.5.3. The Middle-East and Africa Advanced Driver Assistance Systems (ADAS) Market Revenue, By Solution, 2026 – 2035

- 7.5.4. The Middle-East and Africa Advanced Driver Assistance Systems (ADAS) Market Revenue, By Vehicle, 2026 – 2035

- 7.5.5. Saudi Arabia Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Advanced Driver Assistance Systems (ADAS) Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Advanced Driver Assistance Systems (ADAS) Market Revenue, By Component, 2026 – 2035

- 7.6.3. Latin America Advanced Driver Assistance Systems (ADAS) Market Revenue, By Solution, 2026 – 2035

- 7.6.4. Latin America Advanced Driver Assistance Systems (ADAS) Market Revenue, By Vehicle, 2026 – 2035

- 7.6.5. Brazil Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Advanced Driver Assistance Systems (ADAS) Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Advanced Driver Assistance Systems (ADAS) Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Advanced Driver Assistance Systems (ADAS) Market: Company Market Share, 2025

- 8.2. Global Advanced Driver Assistance Systems (ADAS) Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. Aptiv PLC

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Robert Bosch GmbH

- 9.3. DENSO Corporation

- 9.4. Continental AG

- 9.5. ZF Friedrichshafen AG

- 9.6. Magna International

- 9.7. NXP Semiconductors

- 9.8. Hyundai Mobis

- 9.9. Aisin Corporation

- 9.10. Mobileye (Intel)

- 9.11. NVIDIA Corporation

- 9.12. Valeo SA

- 9.13. Infineon Technologies

- 9.14. Renesas Electronics

- 9.15. ]ON Semiconductor

- 9.16. STMicroelectronics

- 9.17. Hitachi Astemo

- 9.18. Autoliv Inc.

- 9.19. Others.

- 9.1. Aptiv PLC

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Custom Market Insights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

List Of Figures

Figures No 1 to 30

List Of Tables

Tables No 1 to 46

Prominent Players

- Aptiv PLC

- Robert Bosch GmbH

- DENSO Corporation

- Continental AG

- ZF Friedrichshafen AG

- Magna International

- NXP Semiconductors

- Hyundai Mobis

- Aisin Corporation

- Mobileye (Intel)

- NVIDIA Corporation

- Valeo SA

- Infineon Technologies

- Renesas Electronics

- ]ON Semiconductor

- STMicroelectronics

- Hitachi Astemo

- Autoliv Inc.

- Others

FAQs

The key players in the market are Aptiv PLC, Robert Bosch GmbH, DENSO Corporation, Continental AG, ZF Friedrichshafen AG, Magna International, NXP Semiconductors, Hyundai Mobis, Aisin Corporation, Mobileye (Intel), NVIDIA Corporation, Valeo SA, Infineon Technologies, Renesas Electronics, ]ON Semiconductor, STMicroelectronics, Hitachi Astemo, Autoliv Inc., Others.

Government regulations play a crucial role in shaping the development of the Advanced Driver Assistance Systems (ADAS) market by mandating the inclusion of key safety features such as automatic emergency braking, lane departure warning, and electronic stability control in vehicles, thereby accelerating widespread adoption, encouraging technological innovation, and pushing automakers to integrate advanced safety systems across both premium and mass-market segments.

The price point significantly impacts the growth and adoption of the Advanced Driver Assistance Systems (ADAS) market, as high system costs can limit penetration to premium and luxury vehicles, while declining prices of sensors, cameras, and processing units are enabling wider adoption in mid-range and entry-level vehicles, thereby accelerating overall market expansion.

According to the present analysis and forecast modeling, the market of Advanced Driver Assistance Systems (ADAS) will witness a significant growth of about USD 118.5 billion in the year 2035 with the growing innovative product launch, increasing collaboration, increasing demand for EVs with a CAGR of 12.5% between the years 2026 and 2035.

It is projected that North America will hold the largest market share in the Advanced Driver Assistance Systems (ADAS) market in the forecast period, with a share of about 34% of the global market share, which is owing to the electrification trends.

The Asia Pacific is expected to grow at a highest rate during the forecast period. The increasing investment in advanced technology drives the market growth.

Key drivers of the Advanced Driver Assistance Systems (ADAS) market include increasing focus on vehicle safety, stringent government regulations, rapid advancements in AI and sensor technologies, growing adoption of electric and premium vehicles, and rising consumer demand for enhanced driving comfort and automation.