Alumina-based Ceramics Market Size, Trends and Insights By Purity Grade (Standard Grade (90–95% Al₂O₃), High Purity Grade (96–99% Al₂O₃), Ultra-High Purity Grade (>99% Al₂O₃)), By Product Form (Tubes & Rods, Plates & Substrates, Crucibles & Saggers, Custom Shapes & Components, Balls & Grinding Media, Other Product Forms (Rings, Nozzles, Bushings)), By Application (Electronics & Semiconductors, Medical & Dental, Automotive (Conventional and Electric Vehicles), Aerospace & Defense, Industrial Machinery & Mining, Chemical Processing, Other Applications (Energy, Optics)), By End-Use Industry (Electronics, Healthcare, Automotive, Aerospace & Defense, Industrial & Mining, Energy, Other Industries), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- Kyocera Corporation

- CoorsTek Inc.

- Morgan Advanced Materials plc

- Saint-Gobain Advanced Ceramics

- Others

Reports Description

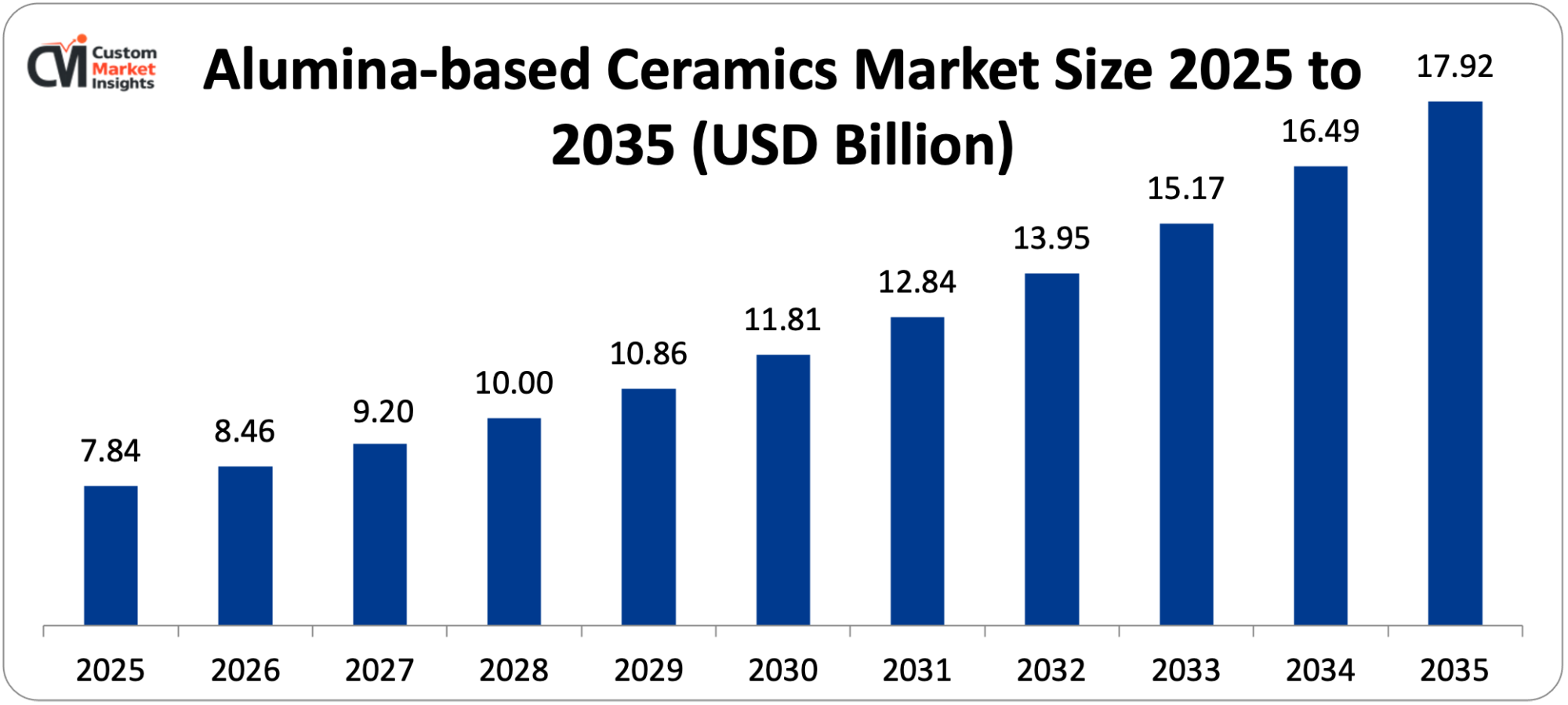

The market size of the global alumina based ceramics is estimated at USD 7.84 billion in 2025 and is projected to grow between USD 8.46 billion and USD 17.92 billion respectively in the years 2026 and 2035 respectively at the CAGR of 7.8%.

The increasing need for high-performance ceramic products in semiconductor fabrics and other sophisticated electronics, the increasing use of alumina ceramics in medical implants and dental restoration due to benefits of biocompatibility and wear resistance, the increased use of wear-resistant alumina products in industrial machinery and mining equipment, the increased use of alumina substrates and alumina insulators in electric vehicle powertrains and battery management, and the ongoing development of increasingly sophisticated sintering and forming technologies all contribute to strong and continuing market growth during the forecast period.

Market Highlight

- Asia Pacific dominated the market with alumina-based ceramics with a market share of 48% in 2025.

- North America: The CAGR is likely to reach 7.1% between 2026 and 2035.

- By the purity grade, the high purity grade (96-99% Al₂O₃) segment won about 43% of the market share in 2025.

- By grade, the best of the ultra-high purity grade (>99% Al₂O₃) segment is increasing at the highest CAGR rate of 10.6% between 2026 and 2035.

- Based on product form, the custom shapes & components segment had the largest market share of 34% in 2025, and the fastest CAGR of 11.2% over the forecasted 2026-2035.

- By segment, the electronics and semiconductors segment will have the largest market share of 38% in 2025 and the medical and dental segment will have the highest liquidity of 9.8% between 2026 and 2035.

- By end-use industry, the electronics segment had 41% of the market share in 2025.

Significant Growth Factors

The Alumina-based Ceramics Market Trends present significant growth opportunities due to several factors:

- Semiconductor Industry Expansion and Advanced Electronics Driving Ultra-High Purity Alumina Demand:

The unstoppable worldwide growth of semiconductor fabrication capacity, whether by increasing demand of logic chips, memory, power semiconductors and compound semiconductors for artificial intelligence, 5G communications, electric vehicles, and consumer electronics, is the strongest and fastest-growing structural feature that drives the demand of ultra-high purity alumina ceramics, since manufacturing equipment of semiconductors depends significantly on alumina ceramic materials to provide a combination of high levels of chemical resistance to corrosive gases in the environment, electrical insulation capabilities, dimensional stability at higher temperatures, and surfaces that are free of particle generation, which are necessary in cleanroom fab environments.

Semiconductor processing equipment Construction of alumina ceramic parts in semiconductor equipment implantation, etching chamber, chemical vapor deposition, and wafer handling equipment Use of such components must satisfy extremely strict specifications of purity (>99.8% Al₂O₃ to limit metallic impurities), surface roughness (Ra values below 0.4 mm to limit particle generation), dimensional control (±0.01 mm to fit into chamber) that can only be met by the most advanced powder synthesis, forming, and sintering techniques by specialized manufacturers Over the past few years, the market size of global semiconductor equipment has experienced a significant increase as a result of new fabrication facilities, often referred to as fabs, being invested in by major chipmakers such as TSMC, Samsung, Intel and SK Hynix, and the Semiconductor Industry Association reported that global semiconductor capital expenditure had increased to around USD 190 billion in 2023. Fabrication nodes extending down to sub-5nm processes used by TSMC and Samsung to produce state-of-the-art logic chips impose increased demands on alumina ceramic component functionality in terms of alumina alloy performance and have also necessitated a greater purity and more precisely engineered alumina ceramic grade.

The CHIPS and Science Act in the United States -binding USD 52 billion of incentives in domestic semiconductor manufacturing -and similar semiconductor sovereignty measures in Europe, Japan, South Korea and India are stimulating the development of new domestic semiconductor fabrication plants that will demand extended supply chains of ultra-high purity alumina ceramics in these locations, creating deep sustained long-term demand growth in ultra-high purity alumina ceramics in these areas. and surfaces that are free of particle generation, which are necessary in cleanroom fab environments. Semiconductor processing equipment Construction of alumina ceramic parts in semiconductor equipment implantation, etching chamber, chemical vapor deposition, and wafer handling equipment Use of such components must satisfy extremely strict specifications of purity (>99.8% Al₂O₃ to limit metallic impurities), surface roughness (Ra values below 0.4 mm to limit particle generation), dimensional control (±0.01 mm to fit into chamber) that can only be met by the most advanced powder synthesis, forming, and sintering techniques by specialized manufacturers Over the past few years, the market size of global semiconductor equipment has experienced a significant increase as a result of new fabrication facilities, often referred to as fabs, being invested in by major chipmakers such as TSMC, Samsung, Intel and SK Hynix, and the Semiconductor Industry Association reported that global semiconductor capital expenditure had increased to around USD 190 billion in 2023. Fabrication nodes extending down to sub-5nm processes used by TSMC and Samsung to produce state-of-the-art logic chips impose increased demands on alumina ceramic component functionality in terms of alumina alloy performance and have also necessitated a greater purity and more precisely engineered alumina ceramic grade.

The CHIPS and Science Act in the United States -binding USD 52 billion of incentives in domestic semiconductor manufacturing -and similar semiconductor sovereignty measures in Europe, Japan, South Korea and India are stimulating the development of new domestic semiconductor fabrication plants that will demand extended supply chains of ultra-high purity alumina ceramics in these locations, creating deep sustained long-term demand growth in ultra-high purity alumina ceramics in these areas.

- Electric Vehicle Revolution and Energy Transition Applications Creating New Demand Vectors:

The worldwide shift to electric vehicles and renewable energy infrastructure is developing significant new demand vectors over which the combination of electrical insulation, thermal control, and mechanical longevity properties of alumina-based ceramics has an enabling performance benefit not available to substitutes. Direct bonded copper (DBC) alumina substrates have also found important roles in electric vehicle powertrains and in dense power electronics modules, such as insulated gate bipolar transistor (IGBT) and silicon carbide (SiC) power module packaging, in which direct bonded copper (DBC) alumina substrates can offer the electrical isolation, thermal conductivity, and compatibility of coefficient of thermal expansion with silicon and silicon carbide semiconductor die to allow reliable operation of power modules over the thermal cycling stresses of automotive service.

The International Energy Agency estimated the electric vehicle market to be about 14 million vehicles sold globally in 2023, and it is expected that by 2030 the market will expand significantly, with EV sales likely to take off as national policy mandates and better economics on the purchase of an EV fuel many more buyers to adopt the technology, each EV powertrain including several alumina ceramic DBC substrates in the inverter, on-board charger, and DC-DC converter power modules. The use of alumina ceramics in the management of lithium-ion batteries as electrically isolating, thermally conductive substrates with battery management integrated circuits and as ceramic separators in advanced battery cell architectures is increasing with the EV battery market, which several analysts forecast will be one of the largest manufacturing sectors in the world in 2030. Solid oxide fuel cells (SOFCs) – an emerging technology of power generation technology applicable to research in stationary and transport systems – utilizes alumina ceramics in both structural and sealing applications to the system in the fuel cell stack, and alumina with high-temperature stability and compatibility with the SOFC operating environment of 700 -1000 o C makes it an essential structural material in the technology.

What are the Major Advances Changing the Alumina-based Ceramics Market Today?

- Advanced Sintering Technologies Enabling New Geometries and Improved Performance:

The energy and commercialization of high-technology powder processing and sintering methods, such as spark plasma sintering (SPS), microwave sintering, hot isostatic pressing (HIP), and additive manufacturing of alumina green bodies and then controlled sintering, are adding to the geometric complexity, dimensional accuracy, and microstructural quality that can be obtained in commercial production of alumina ceramics allowing manufacturers to satisfy application needs that have hitherto been out of reach using conventional die pressing and pressureless sintering. In the case of the Spark plasma sintering, with high pulsed DC currents through a graphite die containing the alumina powder compact, near-theoretical density alumina ceramics with sub-micron grain structures to provide ideal mechanical strength (greater than 600 MPa vs. 300-400 MPa with normal furnace sintering), ideal hardness, and enhanced translucency (dental and optical applications) are obtained.

The pioneering commercial production of SPS technology on a commercial scale by the Dr. Sinter systems of Fuji Electronic Industrial and later by leading producers of alumina ceramic components, including Kyocera, CoorsTek and Morgan Advanced Materials, is allowing high-performance alumina components to be manufactured using material properties that were previously accessible only through hot-isostatic pressing at much lower equipment cost and at much reduced processing time. Additive manufacturing of alumina ceramics Additive manufacturing of alumina ceramics Additive manufacturing 3D printing and additive manufacturing of alumina green body Additive manufacturing of alumina ceramic prototypes Additive manufacturing of alumina ceramic components Additive manufacturing of alumina prototypes Additive manufacturing of alumina components Additive manufacturing of alumina Additive manufacturing of alumina Additive manufacturing of alumina Additive manufacturing of alumina Additive manufacturing of alumina Additive manufacturing of alumina Additive manufacturing of alumina Additive The capability to fabricate internal channels, undercuts, and intricate geometry components of alumina in a die pressable material is creating new areas of use – such as alumina ceramic heat exchangers with internal cooling channels for semiconductor processing equipment, ceramic nozzle arrays with complex internal flow geometries in fluid handling, and patient-specific alumina dental and orthopedic components produced directly in response to a digital design file.

- Medical and Dental Alumina Ceramics Advancing Through Material and Processing Innovation:

The medical and dental uses of alumina ceramics that include alumina total hip arthroplasty femur heads, alumina total hip arthroplasty acetabular liners, alumina dental crowns and braces, alumina orthopedic bearing surfaces, and emerging alumina-based implantable sensor substrates are enjoying ever-increasing growth due to the aging population demographics expanding the orthopedic implant market and the material processing improvements allowing the manufacture of alumina ceramic medical parts with a level of reliability and lower fracture risk. Alumina ceramic femur heads with total hip replacement, which produce dramatically lower wear rates than metal-on-polyethylene bearing combinations, produce low wear debris which leads to the osteolysis based implant loosening that limits implant longevity in younger active patients. — have more than 40 years of clinical history of replacement joints with substantial long-term clinical evidence of superior wear performance.

Third- and fourth-generation alumina ceramic hip bearings, made with high-purity fine-grain alumina, with Weibull moduli significantly higher than first-generation materials, proof-tested for each component, and having burst-resistant design geometries, have reported fracture rates less than 0.01% in published registry studies and have allowed clinical specification by orthopedic surgeons in active younger patients where the longevity of the implant is the most important factor. Published market research estimates the market size of the global orthopedic implants industry to be around USD 57 billion in 2023 and ceramic bearing surfaces are making up an increasing proportion of total hip replacement surgeries as orthopedic surgeons and patients favor ceramic bearing surfaces on younger patients and on those where metal sensitivity has been observed. Alumina ceramic as a core material in all-ceramic dental crowns offers a platform of unprecedented strength and whiteness which, despite offering superior aesthetic results than metal-ceramic crowns, still allows long-term intraoral service through biocompatibility.

- Alumina Ceramics in Defense and Aerospace Armor and Structural Applications:

Alumina ceramics are rapidly becoming the cost-effective alternative to the expensive components: lightweight, high-performance ballistic protection systems and structural components are finding wider use in the defense and aerospace sectors in personal armor, vehicle armor, and aircraft structural protection applications. In body armor plates, vehicle armor kits, and helicopter airframe protection, the military and law enforcement worldwide use alumina ceramic strike face tiles, which operate by breaking incoming projectiles due to their extreme hardness (Vickers hardness of 1,400–1,600 HV as compared with about 500 HV in hardened steel armor plate) and absorb and dissipate the kinetic energy through the ceramic fracture process. The international defense expenditure context, as the NATO countries are upgrading to invest in defense spending to reach 2% of the GDP threshold after the Russian invasion of Ukraine, and the Asian countries are upgrading their defense spending to address the regional security issue, is fueling a continued procurement of personal and platform protection systems that use alumina ceramic armor components.

The lower price of alumina compared to other types of armor ceramics such as silicon carbide and boron carbide such as USD 5 to USD 20 per kilogram versus USD 40 to USD 80 per kilogram for SiC and USD 100 to USD 300 per kilogram for B₄, makes alumina the ceramic of choice in those cases where cost efficiency is more important than weight reduction, such as vehicle armor and facility protection involving stationary applications where weight is not a critical factor like in personal armor or aircraft work.

The combination of high-temperature stability, oxidation resistance, and specific stiffness of alumina ceramic also makes it applicable in aerospace structural applications such as thermal protection components and radome structures that are clear to radar frequencies. High purity grade alumina ceramics constitute the largest purity grade segment at about 43% of the total market share in 2025, as they can be found in the broadest possible set of demanding technical applications -such as semiconductor equipment components, electrical insulators in high-voltage applications, fine mechanical components with high dimensional tolerances needed, and chemical processing equipment needing resistance to concentrated acids and alkalis -where the high level of mechanical, electrical, and chemical performance of 96 to 99% alumina is seen to be paramount over Flexural strengths of up to 350 -500 MPa, volume resistivity of more than 10¹⁴ ohms/cm at room temperature, dielectric constant of 9.5-10 at 1 MHz, and maximum service temperatures of 1,600°C in oxidising atmospheres (high purity) alumina ceramics combine these properties so that no other material currently exists with these properties at an equivalent cost.

The 96% alumina grade which is the most commercially produced high purity grade, balances performance and economics by having a matrix step of mullite and glass binding the alumina grains that enables net-shape forming and sintering at temperatures of 1,550–1,650°C that can be achieved in the common high-temperature kiln without the specialized equipment needed in ultra-high purity sintering.

Category Wise Insights

By Purity Grade

Why Does High Purity Grade (96–99% Al₂O₃) Lead the Market?

Customized shapes and components denote the largest portion of the product form segment with an estimated large portion of 34% of the total market share of alumina ceramics in 2025 because the applications with the most value and the most rapid growth need application-specific geometries, which cannot be addressed by mass-produced product forms. The custom components segment has the greatest revenue per unit weight in the alumina ceramics market, engineered custom components with semiconductor OEM customers priced at USD 100 to USD 5,000 plus/unit depending on geometry complexity, purity grade, surface finish requirements, and volume commitment requirements. The design engineering support features such as finite element analysis of the stress distribution in ceramic components, failure mode analysis, and design optimization under ceramic material constraints distinguish competitively leading manufacturers of custom components in the market such as Kyocera, CoorsTek, and Precision Ceramics as competitors in the custom components market segments that require ceramic manufacturing expertise as a part of the supply relationship and not merely as a supplier of materials.

By Product Form

Why Do Custom Shapes & Components Lead the Market?

Custom shapes and components are the largest market share product form segment at about 34% of the total market share in 2025, owing to the fact that the highest value and fastest growing applications of alumina ceramics products, which include semiconductor equipment components, medical implants, automotive power electronics substrates, and aerospace structural components, all demand application-specific geometries unavailable on standard product forms. The custom components segment features the largest unit weight revenue per unit in the alumina ceramics market and engineered custom components to semiconductor OEM clients which carry pricing of USD 100 5,000+ per unit based on the complexity of the geometry, purity grade, and surface finish, as well as individual annual volume commitments. To compete competitively in the custom components market, the leading manufacturers such as Kyocera, CoorsTek, and Precision Ceramics also differentiate their products in design engineering support features, such as finite element analysis of the stress distribution on ceramic components, failure mode analysis, and design optimization to ceramic material constraints, which allow them to sell their components to OEM customers, who need ceramic component manufacturing expertise as part of the supply relationship and not merely as a material supplier.

By Application

Why Do Electronics & Semiconductors Lead the Market?

Electronics and semiconductor uses represent the most important application at approximately 38% of market share in 2025, attributable to the inability to replace alumina in a wide variety of important functions in the manufacture of electronic component parts and semiconductor fabrication equipment. The product of alumina dielectric characteristics (low dielectric loss allowing high frequency signal integrity), electrical insulation (volume resistivity at operating temperature of 10 or more 1014 ohms, fully compatible with copper metallization in DBC substrates), thermal conductivity (20 W/mK to high purity grade only, which is still significantly higher than most polymeric insulators), and dimensional stability (coefficient of thermal expansion at about 78 ppm/°C is virtually identical to that of silicon and can be used with copper metallization) combines to serve The semiconductor equipment market, which is the most demanding and highest-value application within electronics in relation to alumina ceramics. It is served by few manufacturers with the process capability of meeting the purity, accuracy, and reliability specifications demanded by OEMs such as Applied Materials, Lam Research, Tokyo Electron, and ASML.

By End-Use Industry

Why Does Electronics Lead the Market?

In 2025, the electronics end-use sector contributes the highest market share of about 41%, a result of convergence between semiconductor fabrication capacity growth, 5G telecommunication infrastructure development, electric vehicle power electronics development, and consumer electronics component manufacture, which creates the most absolute volume of alumina ceramic demand.

The cyclical nature of technology development of products within the electronics industry means the more aggressive manufacturing machines and component specifications needed by the next generation of products in its turn need more advanced alumina ceramic solutions, and the self-enhancing dynamic of increasing the demand causes both the development of the alumina ceramic markets and demands to be structurally related to the cycle of investments and innovations in the global electronics industry. The end-use sector of the energy industry is expected to be the quickest developing sector during the forecast period with SOFC applications, the application of alumina ceramic in nuclear reactor instruments and sealants, and an increase of high-voltage insulators due to the worldwide electricity grid modernization plans.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 8.46 billion |

| Projected Market Size in 2035 | USD 17.92 billion |

| Market Size in 2025 | USD 7.84 billion |

| CAGR Growth Rate | 7.8% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Purity Grade, Product Form, Application, End-Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

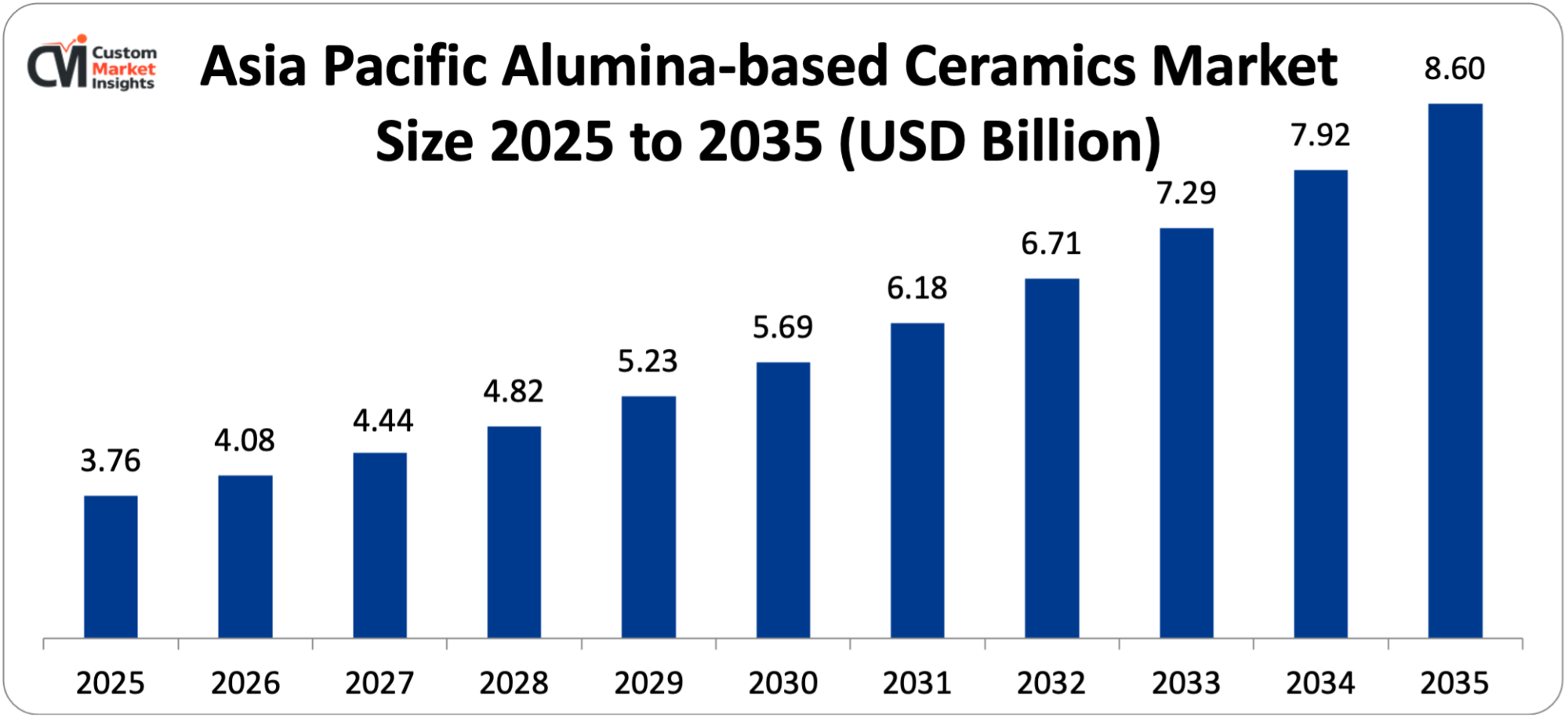

The Asia Pacific alumina-based ceramics market size is estimated at USD 3.76 billion in 2025 and is projected to reach approximately USD 8.60 billion by 2035, with an 8.6% CAGR from 2026 to 2035.

Why Did Asia Pacific Dominate the Market in 2025?

The region is expected to be the core of electronic manufacturing, semiconductor fabrication, and alumina ceramic production with a market share of about 48% in 2025 with Japan, China, South Korea, and Taiwan all having the majority of the entire semiconductor chip manufacturing capacity of the whole world, consumer electronics manufacturing capacity, and advanced ceramic component manufacturing capacity. Japan is the most technically advanced alumina ceramics market in the Asia Pacific area and is arguably the most technically advanced market in the world with Kyocera Corporation based in Kyoto being the largest and most technologically advanced manufacturer of semiconductor equipment parts, electronic packages, medical components, and industrial ceramics in all purity grades and product forms to global OEM customers. China is the largest single-country volume market in the world in terms of both a vast domestic industrial scale alumina ceramics consumption market – a giant mining, minerals processing and manufacturing sector of the country consuming standard and high purity wear-resistant components at a scale previously unknown outside of Chinese markets – and an emerging high-technology alumina ceramics sector for alumina-based wear-resistance components serving the expanding Chinese semiconductor equipment sector and EV powertrain manufacturing. The market of alumina ceramics in South Korea is stimulated by semiconductor fabrication facilities of Samsung and SK Hynix, which are among the most advanced in the world in memory chip manufacturing, and by the EV conversion of the automotive industry of South Korea, which leads to the demand for ultra-high purity of alumina chamber components from Hyundai, Kia, and their tier-1 supplier base.

Why is North America Experiencing Steady and Important Growth?

The United States semiconductor manufacturing renaissance of the CHIPS and Science Act USD 52 billion in manufacturing stimulus has begun, with the United States accounting for the full growth of North America, with an expected CAGR of 7.1% through 2026 to 2035, due to the construction of TSMC, Samsung, Intel, and Micron semiconductor and power generation fabs in Arizona, Texas, Ohio, and Idaho creating the need to supply domestic alumina ceramic components, the sustained demand of the world’s advanced in technology defence sector, the medical CoorsTek CoorsTek is the largest manufacturer of alumina ceramics in North America and the world leader in technical ceramics; its semiconductor, defense, medical and industrial markets are served by its manufacturing plants in the USA, Europe and Asia.

Why is Europe a Strategically Important Market?

The market for European alumina-based ceramics is projected to reach about USD 1.41 billion in the year 2025 and about USD 2.87 billion in the year 2035 at a CAGR of 7.4%. Europe is a strategically important market, with Germany as the centre of world-leading industrial ceramics manufacturing based companies – such as Rauschert GmbH, CeramTec GmbH, and Schunk Advanced Ceramics being the core of European technical ceramics manufacturing expertise — In France, there is Saint-Gobain, which has a highly developed ceramics segment, and in the United Kingdom, there is Morgan Advanced Materials plc, which is one of the most diversified advanced ceramics producers in the world with alumina products used in industrial, defense, medical, and electronic applications.

The automotive sector in Germany, which is in the process of an unprecedented transformation to electric vehicles with Volkswagen, BMW, Mercedes-Benz, and their tier-1 suppliers electrifying their product lineups, is creating increasing demand on DBC alumina substrates and power electronics ceramic components as vehicle lines with EV powertrains replace combustion-powered ones. The substantial defense expenditure increase in Europe after the Russian invasion of Ukraine, with Germany in particular, which has resolved to spend over 2% of GDP on defense, is resulting in the procurement of personal and vehicle protection systems that use alumina ceramic armor material at rates many times higher than in recent years before the invasion.

Why is the Middle East & Africa Region an Emerging Opportunity?

The LAMEA region is showing increased market development as a result of industrial diversification plans of Saudi Arabia and UAE that create demand of wear-resistant alumina ceramic components in the downstream petrochemical and mining sectors, the ambitious renewable energy and modernization programs of power and energy grids in the Middle East that are creatively demanding alumina ceramic electrical insulator products, the large mining sector of Brazil which is a steady market of wear components of alumina ceramic, and the gradual formation of high-technology manufacturing industries in the Gulf Cooperation Council economies that will increasingly

Top Players in the Market and Their Offerings

- Kyocera Corporation

- CoorsTek Inc.

- Morgan Advanced Materials plc

- Saint-Gobain Advanced Ceramics

- CeramTec GmbH

- 3M Advanced Materials (Ceradyne)

- Materion Corporation

- Rauschert GmbH

- Ortech Advanced Ceramics

- Precision Ceramics Ltd.

- Coorstek

- Others

Key Developments

The market has experienced considerable evolution as the industry players are striving to enhance manufacturing capacity of ultra-high purity, increase the supply capacity of semiconductor equipment components, and address the increased demand in the EV, defense, and medical application markets.

- In November 2024: Kyocera Corporation declared a JPY 15 billion capital investment into expanded ultra-high purity alumina ceramic production capacity in its Kagoshima, Japan, manufacturing complex, specifically into the semiconductor equipment component market where demand on leading-edge fab construction programs in the United States, Japan, and Europe has surpassed current production capacity.

- In February 2025: CoorsTek Inc. declared the qualification of its new alumina-silicon carbide composite substrate item, an AlSiC-9, with thermal conduction of 170 W/m³K, or more than 170 times higher than typical 96% alumina DBC substrates of 20 W/m³K, alongside the electrical separation and CTE compatibility, including dependable power module packaging in automotive grade power electronics.

The Alumina-based Ceramics Market is segmented as follows:

By Purity Grade

- Standard Grade (90–95% Al₂O₃)

- High Purity Grade (96–99% Al₂O₃)

- Ultra-High Purity Grade (>99% Al₂O₃)

By Product Form

- Tubes & Rods

- Plates & Substrates

- Crucibles & Saggers

- Custom Shapes & Components

- Balls & Grinding Media

- Other Product Forms (Rings, Nozzles, Bushings)

By Application

- Electronics & Semiconductors

- Medical & Dental

- Automotive (Conventional and Electric Vehicles)

- Aerospace & Defense

- Industrial Machinery & Mining

- Chemical Processing

- Other Applications (Energy, Optics)

By End-Use Industry

- Electronics

- Healthcare

- Automotive

- Aerospace & Defense

- Industrial & Mining

- Energy

- Other Industries

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Alumina-based Ceramics by Segments

- 2.1.2. Alumina-based Ceramics by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Alumina-based Ceramics Market Attractiveness Analysis, By Purity Grade

- 2.2.3. Alumina-based Ceramics Market Attractiveness Analysis, By Product Form

- 2.2.4. Alumina-based Ceramics Market Attractiveness Analysis, By Application

- 2.2.5. Alumina-based Ceramics Market Attractiveness Analysis, By End-Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Semiconductor Industry Expansion and Advanced Electronics Driving Ultra-High Purity Alumina Demand

- 3.1.2. Electric Vehicle Revolution and Energy Transition Applications Creating New Demand Vectors

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Alumina-based Ceramics Market – By Purity Grade

- 4.1. Purity Grade Market Overview, By Purity Grade Segment

- 4.1.1. Alumina-based Ceramics Market Revenue Share, By Purity Grade, 2025 & 2035

- 4.1.2. Standard Grade (90–95% Al₂O₃)

- 4.1.3. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. High Purity Grade (96–99% Al₂O₃)

- 4.1.7. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Ultra-High Purity Grade (>99% Al₂O₃)

- 4.1.11. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Purity Grade Market Overview, By Purity Grade Segment

- Chapter 5. Alumina-based Ceramics Market – By Product Form

- 5.1. Product Form Market Overview, By Product Form Segment

- 5.1.1. Alumina-based Ceramics Market Revenue Share, By Product Form, 2025 & 2035

- 5.1.2. Tubes & Rods

- 5.1.3. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Plates & Substrates

- 5.1.7. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Crucibles & Saggers

- 5.1.11. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Custom Shapes & Components

- 5.1.15. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Balls & Grinding Media

- 5.1.19. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Other Product Forms (Rings, Nozzles, Bushings)

- 5.1.23. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Product Form Market Overview, By Product Form Segment

- Chapter 6. Alumina-based Ceramics Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Alumina-based Ceramics Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Electronics & Semiconductors

- 6.1.3. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Medical & Dental

- 6.1.7. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Automotive (Conventional and Electric Vehicles)

- 6.1.11. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Aerospace & Defense

- 6.1.15. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Industrial Machinery & Mining

- 6.1.19. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Chemical Processing

- 6.1.23. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1.26. Other Applications (Energy, Optics)

- 6.1.27. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 6.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.29. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Alumina-based Ceramics Market – By End-Use Industry

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 7.1.1. Alumina-based Ceramics Market Revenue Share, By End-Use Industry, 2025 & 2035

- 7.1.2. Electronics

- 7.1.3. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Healthcare

- 7.1.7. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Automotive

- 7.1.11. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Aerospace & Defense

- 7.1.15. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Industrial & Mining

- 7.1.19. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Energy

- 7.1.23. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1.26. Other Industries

- 7.1.27. Alumina-based Ceramics Share Forecast, By Region (USD Billion)

- 7.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.29. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 8. Alumina-based Ceramics Market – Regional Analysis

- 8.1. Alumina-based Ceramics Market Overview, By Region Segment

- 8.1.1. Global Alumina-based Ceramics Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Alumina-based Ceramics Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Alumina-based Ceramics Market Revenue, By Purity Grade, 2026 – 2035

- 8.1.4. Global Alumina-based Ceramics Market Revenue, By Product Form, 2026 – 2035

- 8.1.5. Global Alumina-based Ceramics Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Alumina-based Ceramics Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Alumina-based Ceramics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Alumina-based Ceramics Market Revenue, By Purity Grade, 2026 – 2035

- 8.2.3. North America Alumina-based Ceramics Market Revenue, By Product Form, 2026 – 2035

- 8.2.4. North America Alumina-based Ceramics Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Alumina-based Ceramics Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2.6. U.S. Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Alumina-based Ceramics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Alumina-based Ceramics Market Revenue, By Purity Grade, 2026 – 2035

- 8.3.3. Europe Alumina-based Ceramics Market Revenue, By Product Form, 2026 – 2035

- 8.3.4. Europe Alumina-based Ceramics Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Alumina-based Ceramics Market Revenue, By End-Use Industry, 2026 – 2035

- 8.3.6. Germany Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Alumina-based Ceramics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Alumina-based Ceramics Market Revenue, By Purity Grade, 2026 – 2035

- 8.4.3. Asia Pacific Alumina-based Ceramics Market Revenue, By Product Form, 2026 – 2035

- 8.4.4. Asia Pacific Alumina-based Ceramics Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Alumina-based Ceramics Market Revenue, By End-Use Industry, 2026 – 2035

- 8.4.6. China Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Alumina-based Ceramics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Alumina-based Ceramics Market Revenue, By Purity Grade, 2026 – 2035

- 8.5.3. The Middle-East and Africa Alumina-based Ceramics Market Revenue, By Product Form, 2026 – 2035

- 8.5.4. The Middle-East and Africa Alumina-based Ceramics Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Alumina-based Ceramics Market Revenue, By End-Use Industry, 2026 – 2035

- 8.5.6. Saudi Arabia Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Alumina-based Ceramics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Alumina-based Ceramics Market Revenue, By Purity Grade, 2026 – 2035

- 8.6.3. Latin America Alumina-based Ceramics Market Revenue, By Product Form, 2026 – 2035

- 8.6.4. Latin America Alumina-based Ceramics Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Alumina-based Ceramics Market Revenue, By End-Use Industry, 2026 – 2035

- 8.6.6. Brazil Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Alumina-based Ceramics Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Alumina-based Ceramics Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Alumina-based Ceramics Market: Company Market Share, 2025

- 9.2. Global Alumina-based Ceramics Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Kyocera Corporation

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. CoorsTek Inc.

- 10.3. Morgan Advanced Materials plc

- 10.4. Saint-Gobain Advanced Ceramics

- 10.5. CeramTec GmbH

- 10.6. 3M Advanced Materials (Ceradyne)

- 10.7. Materion Corporation

- 10.8. Rauschert GmbH

- 10.9. Ortech Advanced Ceramics

- 10.10. Precision Ceramics Ltd.

- 10.11. Coorstek

- 10.12. Others.

- 10.1. Kyocera Corporation

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 41

List Of Tables

Tables No 1 to 51

Prominent Player

- Kyocera Corporation

- CoorsTek Inc.

- Morgan Advanced Materials plc

- Saint-Gobain Advanced Ceramics

- CeramTec GmbH

- 3M Advanced Materials (Ceradyne)

- Materion Corporation

- Rauschert GmbH

- Ortech Advanced Ceramics

- Precision Ceramics Ltd.

- Coorstek

- Others

FAQs

The key players in the market are Kyocera Corporation, CoorsTek Inc., Morgan Advanced Materials plc, Saint-Gobain Advanced Ceramics, CeramTec GmbH, 3M Advanced Materials (Ceradyne), Materion Corporation, Rauschert GmbH, Ortech Advanced Ceramics, Precision Ceramics Ltd., Coorstek, Others.

Regulations by the government influence the market of alumina-based ceramics in a variety of ways, including the regulatory approval systems of medical devices that utilize medical alumina components, ballistic systems as a source of medical alumina components, environmental regulations that control the production of alumina ceramics, and industrial policy programs that guide the development of semiconductor and other EVs, creating a demand on derived alumina ceramics. The medical device regulatory system of the FDA, which necessitates 510(k) clearance or PMA approval of alumina ceramic medical components such as orthopedic implants and dental devices, has imposed high-quality and clinical performance standards that have acted as a strong entry barrier to new medical ceramics suppliers and justified high pricing of existing, FDA-cleared alumina ceramic medical components. The Medical Device Regulation (MDR 2017/745) of the EU presents similar or stricter conditions for alumina ceramic medical components sold in the European markets, where the conditions of clinical evidence under MDR are more demanding in comparison to the former Medical Device Directive, pending a continuous investment burden on medical alumina ceramic manufacturers. The ballistic performance, quality, and documentation requirements of alumina ceramic body armor components that alumina ceramic armor components need to achieve to be accepted by the military procurement are established by U.S. military specifications such as MIL-dTL-32332 for ceramic body armor and equivalent requirements in NATO member countries that establish the standards of the testable quality of ceramic body armor components in military procurement. The industrial environmental standards such as the EU Industrial Emissions Directive and the similar U.S. EPA regulations on kilns and high-temperature ceramic manufacturing plants provide emissions restrictions upon alumina ceramic manufacturing plants which generate compliance cost burdens and concurrently promote investment in more energy efficient sintering technologies which both enhance the process economic and environmental performance.

The pricing of alumina ceramics has a very wide spread that is dependent on the variety of purity levels, product types and application requirements in the market. Types of alumina wear components Standard grade 90 to 95% wear parts, such as grinding media balls, pipe elbows, and pump liners, cost USD 3 to USD 15 per kilogram and compare on the overall cost of ownership with hardened steel and rubber wear components where the superior wear life of alumina makes the difference between the unit cost and the overall cost of ownership. Industrial and electronic custom alumina High purity components 96 -99% alumina are available at USD 20 to USD 200 per kilogram based on the complexity of geometry and specification stringency. Semiconductor equipment components of ultra-high purity sell at USD 500 to USD 5,000-plus per unit, varying by size and complexity and reflecting not only the materials cost of 99.5%+ purity alumina but also the investment needed to process a material to semiconductor grade in surface finish and dimensional accuracy, purity, etc. In the competitive orthopedic implant market medical alumina ceramic components, especially femur heads and acetabular liners in total hip replacement, cost between USD 200 and USD 600 per component based on both the quality of the material and the regulatory compliance costs of the FDA and the CE Mark regulatory compliance requirements required in the manufacture of medical ceramic components. These and related segments are strategically important to leading manufacturers of alumina ceramics, as the high prices they can command in semiconductor, medical, and defense markets drive further migration of manufacturer investment to higher-value application markets, though they have lower absolute volumes than the industrial wear applications.

According to present analysis, the market is expected to be USD 17.92 billion by 2035 due to the capacity expansion of semiconductor fabrication under the CHIPS Act; global semiconductor sovereignty plans; a 10-year-long ultra-high purity of alumina demand growth cycle, EV powertrain electrification to tens of millions of vehicles per year, creating DBC substrate demands in volumes never before in the industry, ageing population demographics and a better clinical evidence base of ceramic joint replacement in younger active patients, defense sector alumina wear ceramics growing with global mining and minerals processing output expansion, and additive manufacturing enabling new alumina ceramic applications in complex geometry components across medical, aerospace, and semiconductor equipment sectors, at a CAGR of 7.8% from 2026 to 2035.

Asia Pacific is projected to have the largest share of revenue even during the forecast period, with about 48% of the global market share, due to the combined location of the region being the world leader in electronics and semiconductor manufacturing geographies, with TSMC, Samsung, SK Hynix, and most of the global consumer electronics supply chain, the world leader in the alumina ceramics manufacturing industry that has anchored Kyocera, China being the world’s extreme industrial and growing high technology alumina ceramics consumption base, and the concentration of both alumina ceramics.

Asia Pacific is expected to both retain the largest market share and the highest growth rate at 8.6% CAGR over the forecast period, as it will continue to experience growth due to further expansion of semiconductor fabrication capacity in Taiwan, South Korea, Japan, and China, creating demand for ultra-high purity alumina components, and China, also with its own growing domestic semiconductor equipment manufacturing industry, will also create demand for high-performance alumina components in the various product categories that the region will continue to dominate in the global consumer electronics manufacturing industry.

The Global Alumina-based Ceramics Market is projected to grow significantly due to the increased global semiconductor capital expenditure of about USD 190 billion in 2023 sustaining demand of ultra-high purity alumina chamber components in semiconductor processing equipment, the global EV market of about 14 million units sold in 2023 and will substantially increase to 2030 driving DBC alumina substrate demand in IGBT and SiC power modules packaging, breaking through the barriers to complex geometries offered by additive manufacturing hither driving domestic alumina ceramic supply chain development, alumina ceramic hip bearing fracture rates below 0.01% in published registry studies resolving clinical concerns and enabling confident specification in younger active joint replacement patients, growing defense spending across NATO member nations following the Ukraine conflict driving alumina armor component procurement, and additive manufacturing of alumina ceramics enabling complex geometries previously unachievable through conventional forming that are opening new high-value application spaces.