Canada Property & Casualty Insurance Market Size, Trends and Insights By Insurance Type (Auto Insurance, Personal Auto, Commercial Auto, Property Insurance, Homeowners, Commercial Property, Tenants/Renters, Liability Insurance, Other Insurance Types, Boiler and Machinery, Marine and Aircraft, Surety and Fidelity), By Distribution Channel (Direct, Agents, Brokers, Banks), By End User (Individual, Commercial), and By Region - Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Canada |

| Largest Market: | Canada |

Major Players

- Intact Financial Corporation

- Aviva Canada Inc.

- Desjardins Group

- Co-operators Group Limited

- Others

Reports Description

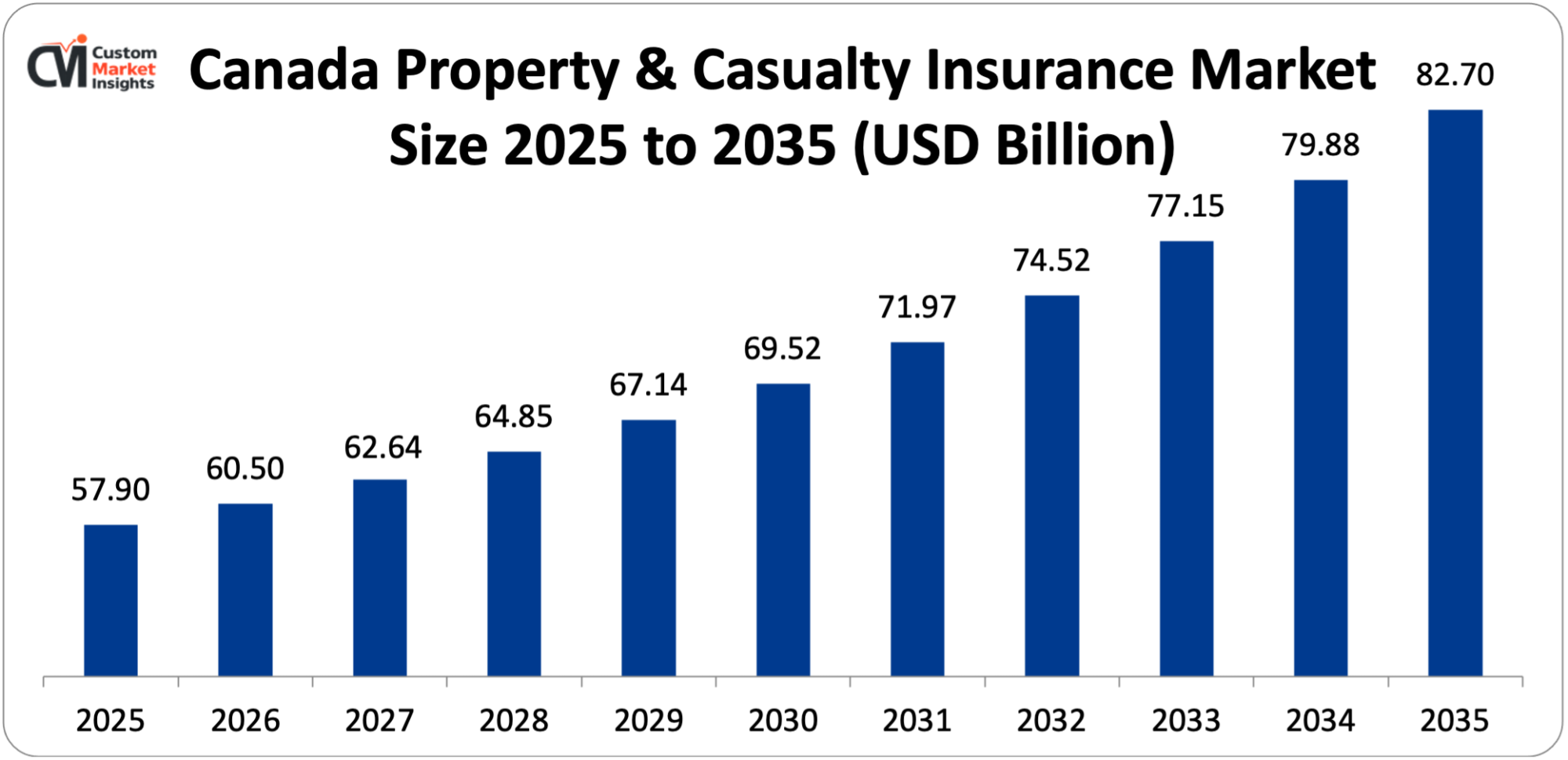

The size of the Canada property and casualty insurance market is estimated at USD 60.50 billion in 2026 and is estimated to grow up to a value of USD 82.7 billion by 2035 with a CAGR of 3.42% in the period between 2026 and 2035.

The increasing rate of growth of climate related disastrous losses, the rise in vehicle registration and population, the rise in the value of property located in urban areas, technological innovations such as telematics and online distribution, regulatory changes favoring innovation, increasing awareness of insurance advantages, and government efforts such as national flood insurance program are stimulating market growth.

Market Highlight

- In Canada, the share of property and casualty insurance in the world market in 2025 is estimated at 2.9%, and there are 631 business companies in this industry and more than 192 individual insurers involved in the auto insurance sector.

- By type of insurance, auto insurance had about 50% of the market share in 2025, which was compelled by the success of mandatory coverage requirements in all provinces and territories.

- Province wise, Ontario has the largest market share of 36.06% in 2025, and Alberta has the highest CAGR in the period 2026-2035 of 6.39% of the market.

- By distribution channel, agents/brokers had 58% of market share in 2025, but direct channels are increasing at 5.12% CAGR due to the adoption of digital.

- In 2024, the severe weather-related insured losses in Canada constituted USD 8.5 billion (USD 5.9 billion), the highest in its history, and almost three times more than in 2023. This is because insured losses that were caused by catastrophic weather and wildfires reached USD 37 billion between 2016 and 2025, compared to USD 14 billion between 2006-2015.

Significant Growth Factors

The Canada Property & Casualty Insurance Market Trends present significant growth opportunities due to several factors:

- Escalating Climate-Related Catastrophic Losses Driving Market Transformation:

The fact that the number and the size and intensity of climate-related disasters have dramatically increased is both the core challenge and opportunity that the P&C insurance market in Canada is facing with 2024 setting a record as the most costly year of severe weather-related insured losses in Canadian history, USD 8.5 billion, more than 2023, and more than twelve times the USD 701 million per annum average of the 2001-2010 years, creating an unprecedented volume of claims that demand a significant capital base and advanced risk modelling Catastrophe Indices and Quantification Inc. (CatIQ) predicts that the insured losses of USD 8.5 billion in 2024 will exceed the historical record of USD 6 billion in 2016 in the aftermath of the Fort McMurray wildfires, with significant contributors being the gigantic hailstorm in Calgary resulting in an estimated USD 3 billion in damages in a little over an hour, extensive wildfires in and around Jasper, and extreme floods and storms in cities such as Toronto and Montreal, proving the geographic heterogeneity.

The Canadian history of the most devastating season of the summer of 2024 in terms of insured losses due to wildfires, floods, and hailstorms. Over USD 7 billion in insured losses were already experienced and more than 250,000 claims were made by four disastrous weather events in July and August alone, which is half the number of claims insurers typically get in a year. This had operational pressure, capital pressure and pricing pressures throughout the industry. Canada had USD 37 billion as the annual insured losses on catastrophic weather and wildfires between 2016 and 2025, which is almost three times the USD 14 billion between 2006 and 2015. Against the same period the number of claims also nearly doubled with an accelerating trend which has changed the way risk is assessed, pricing methods, capital requirements and insurability, particularly in high risk areas. The temperature has increased at a rate of 1.7 degrees Celsius since 1948, twice that of the world, and in extreme northern Canada it is warming three times faster according to the Canadian Climate Institute information. This fast warming presents an unprecedented risk environment that necessitates fundamental re-evaluation of underwriting, product structure, and climate adjustment.

The ten largest severe-weather insured losses are all concentrated over the past three decades, with 9 of them happening since 2011 with over USD 1 billion of losses. Extreme weather is no longer a phenomenon but a new reality, and business models and risk-management frameworks and engagement with stakeholders, such as with governments on infrastructures to be climate-resilient, have to be permanently adjusted. The biggest threat that affects the climate in Canada is flooding which exposes millions of people to danger annually. The new category of products that did not exist before was the Overland flood insurance that was launched following the devastating floods of 2013 in Alberta and Ontario. The insurers are currently promoting the idea of a national flood insurance program in order to make sure that high-risk properties are covered and equitable access and affordable coverage are afforded to the high-risk populations.

- Digital Transformation and Usage-Based Insurance Revolution:

A disruptive trend includes technological innovation telematics, open-banking integration, artificial intelligence, digital distribution platform, and usage-based insurance as it enhances accuracy in risk assessment, customer experience, operational cost, and personalized pricing. It will reward safe behavior and make the market more accessible to consumers who are technologically inclined and prefer self-service and instant satisfaction. The Canadian open-banking system, suggested in the Canadian 2025 Budget, will start sharing secure data with accredited providers in January 2026. This model allows hyper-personalized usage-based coverage based on telematics and verified financial measures. Behavior-based programs that are administered through carrier apps also afford drivers meaningful savings.

Usage-based insurance is in a good position to combine telematics with existing financial measures to develop sophisticated risk-assessment data. The enrollment incentives are tied to the driving behavior, distractibility index, time-of-day index, and the renewal savings. But the number of people enrolling is still significantly lower than the number of people who have expressed interest, and carriers need to provide more value propositions and simpler participation processes that alleviate privacy fears and perceived complexity. Quebec has a privacy regime, including the explicit consent regulations and the purpose limitation regulation, which influence the communications and disclosures of a program. They increase customer trust by telling clients what they will do with their data, what they will keep confidential, and what benefits they will get practically such as premium discounts and enhanced safety due to behavioral feedback.

Quick expansion of digital distribution channels by incorporating insurance in financial services as well as in retail relationships enables products to get integrated at the point of need. First-mover software will reduce days of paperwork to minutes, all-day chatbots will support twenty-four-hour customer service, mobile-first interfaces will enable consumers with quick access to self-service, etc. These attributes remove the conventional aspects of tension in insurance purchasing and service. Artificial intelligence technologies include autonomous claims processing with image recognition, fraud detection that is capable of identifying suspicious patterns, predictive analytics that can estimate loss rates and set prices, and product recommendations, which make insurers technology-advanced, can be used to create more efficient processes, reduce expenses, increase customer satisfaction, and provide a competitive edge by using advanced digital capabilities and data-driven insights.

What are the Major Advances Changing the Canada P&C Insurance Market Today?

- Climate Adaptation Strategies and Resilient Building Initiatives:

The climate adaptation efforts led by the industry such as FireSmart community programs, investments in flood-defense infrastructure, advocacy of building codes modernization, and transparency of risk-based pricing are the most vital responses to the ever-increasing climate disasters, and Insurance Bureau of Canada established three-point plan to the policymakers that will make Canada the world leader in resilience through the holistic policy solutions that cover communities, ensure insurability and prevent affordability crisis affecting millions of Canadians.

The resilience framework of IBC recommends:

(1) property owners should be incentivized to make their homes more resilient to severe weather by giving them financial support, technical support, and simplified permitting.

(2) Canada should become the world leader in natural catastrophe mapping and early detection by creating, updating, and sharing detailed climate-risk maps on a local and national scale and investing in early warning processes and technologies that more effectively warn of severe convective storms.

(3) ensuring that public infrastructure is resilient by making government investments to strengthen community resilience and the property capacity is now selective as it offers good prices on well-secured risks and hikes deductibles in catastrophe areas to enhance targeted growth and retain risk-adjusted returns, with insurers increasingly demanding that homeowners take resilience steps such as backwater valves, sump pumps, and flood-resistant materials as conditions of coverage or premium rebates as an incentive to homeowners to adopt risk-reducing measures to prevent loss exposure.

FireSmart programs spreading into wildfire prone communities teach vegetation management, ignition resistant materials, and defensible space development, municipalities offer programs at the community level such as fuel reduction, fire breaks and emergency preparedness planning that decrease the risk of wildfire and enhance the insurability of high-hazard properties where otherwise carriers would limit coverage or charge prohibitive rates that threaten home values and community sustainability. Modernization programs in building codes promote high-quality standards that cover climate resilience, such as flood-resistant construction in potentially vulnerable zones, wind-resistant construction in potentially hurricane-prone zones, and ignition-resistant construction in potentially wildfire-prone zones with updated building codes offering a minimum level of protection against the potential risk of catastrophic losses without causing excessive expenditure over time through cost-effective designs. Planning reforms that would prohibit development on flood plains, wildfire interfaces, and other high-hazard land use areas are essential prevention strategies, and zoning restrictions and development moratoria in very hazardous zones are promoted by the insurers.

- National Flood Insurance Program Development:

The longstanding collaboration of the federal government with the property and casualty insurance sector to develop a low-cost national flood insurance program to households at high risk of floods is the breakthrough initiative to bridge the protection gaps, assure coverage availability to high-risk populations in the standard marketplace, and establish a risk-sharing program to ensure the viability of the private market.

The National flood insurance program is to offer affordable overland flood insurance on high risk properties that cannot be covered by private markets using the public-private partnership model whereby the government would assume the catastrophic tail risk with private insurers still serving the normal risk properties as a way of creating a comprehensive solution to covering every property by insuring it. Some program design factors are eligibility requirements that define high-risk properties that are to be eligible to receive subsidized coverage, a premium framework that balances both goals of affordability and actuarial soundness to prevent adverse selection, coverage limits and deductibles that fairly distribute risk between insurance companies and customers, and consistency with the existing private market to provide a seamless customer experience and not disrupt the market and cause unintended outcomes to negate the underlying coverage options.

Commitments under federal funding, such as Budget 2025, are to support the development of programs, implementation infrastructures, and long-term subsidy needs to keep the communities financially sustainable, and the government acknowledges the fact that flooding is a national crisis that needs federal intervention because of the magnitude of the risk, the inadequacy of purely market-driven responses, and the economic need to provide vulnerable communities with a chance to avoid catastrophic financial losses that would undermine housing stability and the ability to sustain a community. Issues of implementation include the establishment of risk mapping and assessment procedures, IT systems that can support the administration of the program, establishing distribution infrastructure to reach target populations, and intergovernmental contacts between federal, provincial, and municipal governments and private insurers to ensure successful program implementation, consumer education, and a central management system that responds to the changing flood risk as climate change effects intensify requiring adaptive management and frequent program changes to ensure remaining relevant and efficient.

- Consolidation and M&A Activity Reshaping Competitive Landscape:

Consolidation of the industry through M&A activity such as Intact Financial Corporation buying RSA Insurance Group in 2021, smaller regional insurers selling to larger national players, and private equity investment of insurance brokerages are major trend that creates scale advantages, operational efficiencies, and better competitive positioning and enhances technology capabilities, but there is highly competitive marketplace with no single player dominating more than 10% of the market share and a variety of players including national carriers, regional specialists, and direct writers.

The mergers and acquisitions save larger insurers through economies of scale, which distribute the cost of investment management, underwriting and support of the back-office operations across a larger client base, enhanced efficiency by integration of systems and standardization of processes, increased bargaining power in negotiations with reinsurance and service providers, geographic diversification which lowers concentration risk, and expanded product offerings that provide cross-selling opportunities and comprehensive solutions which may attract one-stop insurance solutions customers. Intact Financial Corporation has the largest market share of the Canadian P&C market after acquisition strategies that have given the company national presence, a book of business diversification, and more capabilities, but the market share of the company in the market stands at less than 15%, which means that the market is highly fragmented with numerous viable competitors that have strong regional placement, specialized niches, and differentiated value propositions that allow them to survive competitive pressures despite mergers and acquisitions.

Brokerage consolidations reflect a parallel trend including national consolidators, regional consolidators, and local independents competing over the distribution share and M&A activity based on succession plans where aging broker principals are seeking an exit strategy and the need for scale to make investments in technology and specialized expertise, and which have defensive properties and strong client relationships when facing economic uncertainty. With consolidation, the general market continues to be highly competitive with 631 businesses working within the property, casualty and direct insurance sector, according to the IBIS world data, about 192 privately based insurers offering auto insurance, and continuous new entrants with digital-first automobile carriers, MGA, and insurtechs that threaten the existing ones with innovative products, better customer experience, and efficient operating models that capitalize on technology benefits.

- Telematics and Usage-Based Insurance Maturation:

Telematics-based insurance (UBI) schemes that have moved beyond the first-mover phase into the mainstream acceptance phase, with large carriers offering smartphone-based apps based programs monitoring driving habits, vehicle usage patterns and contextual information such as the time of day and location, provide a discount on premiums in case of safe driving and create valuable information to use in risk selection, refinement of pricing models and loss prevention efforts through feedback mechanisms that can encourage safer behavior.

The UBI programs are under-enrolled compared to the potential despite consumer interest surveys indicating their willingness to join the programs with barriers being privacy concerns around location tracking and data sharing, perceived complexity of enrollment and continued participation, doubt about whether they genuinely deliver savings according to the promotion claims, and technical issues such as smartphone compatibility, battery life, and connectivity issues are also creating incongruence resulting in low enrollment rates below the threshold required to achieve full actuarial credibility and scale economies. Responding with improved value propositions such as initial enrollment discounts which ensure savings of at least one amount as customers drive regardless of the driving score, game functionality making participation thrilling and satisfying, easy to use apps that remove friction and enhance customer experience, and simple scoring systems that create trust and prove that rates are being set fairly, address the issues of black-box algorithms and arbitrary rate changes.

Laws such as privacy laws, insurance rating laws, and consumer protection laws influence the design and presentation of UBI programs, with Quebec laws demanding explicit consent and limited purpose restricting privacy to significant privacy demands, while the rest of the Canadian provinces emphasize a more laissez-faire stance, and new regulations continue to evolve the balance between the encouragement of innovation and consumer protection while ensuring the proper regulation of data, the transparency of algorithms, and procedural fairness in the processing of automated decision-making systems to the financial interests of consumers. Other current uses of telematics data outside rating include claims management with the use of crash reconstruction, fraud detection to identify those accidents that are staged, loss prevention through driver coaching and real-time alerts, and fleet management services provided to commercial insureds to enhance their safety and loss reduction, which offer additional value towards the continued investment of telematics infrastructure and program development.

Category Wise Insights

By Insurance Type

Why Auto Insurance Leads the Market?

The biggest segment in 2025 will be auto insurance with about half of the total market share. This type of dominance is representative of compulsory coverage in all of the Canadian provinces and territories that establish universal demand, high levels of vehicle ownership with increasing motor vehicle registrations that promote premium growth, a legal framework that ensures coverage and consumer protection, and high levels of claims frequency due to accidents, theft and weather damages that generate sustained premium revenue supporting market size.

The dominance of auto insurance through the legal requirements that all drivers have minimum liability coverage that protects the third parties against bodily injuries and property losses, with the provinces establishing minimum levels of coverage that are usually between USD 200,000 and USD 1 million is a floor to the market and most drivers buy higher coverage including collision, comprehensive coverage and other liability cover above minimums, due to lender requirements on financed vehicles and consumer preference for overall financial security. The Industry data indicates that there are about 192 foreign P/C insurance firms in the business of auto insurance in Canada and government-operated insurers in British Columbia (ICBC), Saskatchewan (SGI), and Manitoba (MPI) that feature a mandatory component creating a mixed public-private market structure with Quebec having Société de l’assurance automobile du Québec (SAAQ), which covers bodily injury and property damage insurance by private firms representing a unique hybrid model. The rising number of vehicles, resulting from population growth, urbanization that leads to higher levels of vehicle dependency, and economic development that supports vehicle ownership creates an increasing insured base, albeit partially neutralized by the ridesharing that leads to a smaller necessity of personal vehicles in urban areas and the development of autonomous vehicles that are likely to lower the number of accidents in the future and modal changes of the population to public transport, cycling, and micro-mobility solutions in place of excessive congestion, expensive parking, and the environmental issues associated with vehicles.

Property insurance has been steadily growing due to the increase in home prices especially in larger urban centers such as Toronto, Vancouver, and Montreal where property values are up and insured claims are correspondingly high, the rising frequency of severe weather damage that needs coverage for floods, wind, and hail, and the rising home ownership rates among millennials entering peak years in their household formation, which have created opportunities for new customer acquisitions.

By Province

Why Ontario Dominates the Market?

Ontario is the most significant provincial bloc representing about 36.06 market share in 2025. The basis of this dominance is the concentration of high value residential and commercial property in the Greater Toronto Area (GTA) into large insured values, concentration in auto exposure in GTA with the highest concentration of vehicle registrations in the country, the concentration in population with Ontario as a representative of about 38% of the Canadian population, and the economic activity that supports commercial insurance demand in the manufacturing, services, and technology industries.

Ontario dominates the market with the largest city in Canada Toronto and other leading urban centres such as Ottawa, Mississauga, Hamilton and London providing a concentrated insured exposure and even greater share of insured property value as a result of high commercial P&C demand due to premium real estate prices, high density commercial activity and a highly developed economy providing a large concentration of insured exposure. The highest rainfall on record in July 2024 resulted in massive losses due to floods in GTA illustrating the necessity to have more granular flood underwriting and higher deductibles in vulnerable neighborhoods, with the Toronto floods being the single most catastrophic event of 2024 in terms of insured losses, illustrating vulnerabilities of urban floods even in areas that are not traditionally considered to be at high risk of floods. The carrier who is pricing property as incurring continually increased construction and rebuilding costs in large urban centers with labor shortages, material inflation, and regulatory compliance costs that cause replacement costs that are significantly higher than historical values, and where inflation in the cost of construction in urban centers far outstrips general CPI, periodic adjustment of coverage will make sure that adequate protection is ensured and proper premiums are charged relative to the exposure.

Alberta has the highest growth of 6.39% CAGR between 2026 and 2035 due to expansion in the economy through the energy industry, diversification through technology and services, population growth due to interprovincial migration attracted by work opportunities and a lower cost of living than Ontario and BC and insurance market liberalization due to the lifting of the rate cap providing pricing flexibility to facilitate market entry and capacity growth.

By Distribution Channel

Why Agents/Brokers Dominate Distribution?

The biggest distribution channel is the agents and brokers who will take up around 58% of market share in 2025. This market leadership indicates consumer preference of professional guidance in the intricate coverage arrangements, federal necessities that reward broker compensation on a commission basis, distribution infrastructures in place that comprise thousands of brokerage companies throughout Canada, and trust bonds between brokers and customers that facilitate retention and cross-selling possibilities.

Brokerage distribution prevails by offering personalized service such as needs assessment, carrier recommendation, multi-carrier quote evaluation, policy placement and continuing service such as endorsements and claim assistance as well as renewals, which entail creating a total value proposition that goes beyond facilitation of transactions and development of long-term client relationships that result in high retention rates. Although the market has been consolidated with national firms and regional consolidators acquiring local independents, it has also been observed that overall market is not monopolized and as reported by Smythe LLP, the opinion of the owner of brokerages revealed that there have been many varied intentions of succession, constraints, and new trends that are experienced by the business despite many different business models which are observed in single-owner operations through multi-location businesses.

Direct channels boast the highest growth rates of 5.12% CAGR due to digital penetration of consumers researching online and making purchases over carrier websites and apps, the cost efficiency of doing away with compensations to the intermediary, the convenience of doing business, and being technologically advanced with younger populations opting to use the internet and apps to get the best offers and avoid traditional forms of brokerage interactions.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 60.50 billion |

| Projected Market Size in 2035 | USD 82.7 billion |

| Market Size in 2025 | USD 57.90 billion |

| CAGR Growth Rate | 3.42% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Insurance Type, Distribution Channel, End User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Economic Impact Analysis

How Significant is the Industry’s Economic Contribution?

The Canada P&C insurance market is a significant financial services sector component, with USD 57.9 billion worth of insurance protecting catastrophic loss of millions of Canadian households and businesses otherwise crippling families, sending businesses to the bank, and destabilizing communities without proper risk transfer mechanisms. Industry profit of 8.0% of revenue in 2025 was supported by an increase in interest rates and increase in asset of investment as the underwriting burden in the industry is caused by high catastrophe losses but carriers have sufficient capital bases and they can absorb major catastrophes without endangering their solvency position or necessitating emergency capital increases shown by their high claims years. The industry has ripple effects in terms of employment across the economy where actuaries, loss adjusters, legal professionals, construction contractors working on repairs, auto body shops, medical professionals treating injury claimants, and technology vendors offering systems and services to the industry have a total impact on economy that is multiplied in jobs. Canadian economy Canadian economy Investment portfolios of P&C insurers worth hundreds of billions of dollars fund Canadian economy both in debt and equity capital to governments, corporations, and real estate projects, with conservative investment strategies of fixed income and high-quality equities that give consistent returns to support claim-paying capabilities and contribute to the liquidity of the capital market and infrastructure funding.

What is the Market’s Social Protection and Economic Stability Role?

P&C insurance offers critical social protection functionality that makes economic action that would otherwise be unattainable or prohibitively costly possible, with auto liability insurance that covers individuals against catastrophic financial loss through the impacts of accidents, property insurance that allows individuals to finance mortgages by covering Lender insurance, and business insurance that assists businesspersons and trade to continue by covering property damage, liability claims, and business interruption. Each dollar of risk mitigation will result in a future loss reduction of USD 5 to USD 10 as per the IBC data, which proves to be a strong return on the expenditures put into preventing disasters, including flood defenses, forestry fire measures, and building enhancements that should be pursued by the property owners, municipalities, and provincial governments in the future due to good cost-benefit ratios. The economic loss due to climate change that would cost the Canadian economy USD 25 billion by 2025 as estimated in a 2022 Climate Institute report, equivalent to half a year of projected growth, and averaging USD 700 per capita in climate-related costs, has proven to be an externality with economic impacts across Canada and therefore demands a concerted effort to address.

Top Players in the Market

- Intact Financial Corporation

- Aviva Canada Inc.

- Desjardins Group

- Co-operators Group Limited

- TD Insurance Group

- Wawanesa Mutual Insurance Company

- SGI CANADA Insurance Services Ltd.

- RSA Canada

- Economical Insurance

- Pembridge Insurance Company

- Others

Key Developments

The market has undergone significant developments as industry participants seek to adapt capabilities and respond to challenges.

- In January 2025: Canada had the most expensive year on record for severe weather-related insured losses, amounting to USD 8.5 billion, just short of 2023, with hail damage in Calgary amounting to USD 3 billion, wildfires in Jasper amounting to USD 880 million, and floods in Toronto amounting to USD 940 million, showing that the impact of the climate crisis is growing and needs fundamental market adjustments.

- In July 2021: Intact Financial Corporation successfully equipped RSA Insurance Group to form one of the top 20 global P&C insurers, which shows a consolidation trend and scale-building strategies to support competitive positioning, efficiency, and scale-building capacity to serve the Canadian market with diversified product offerings and a broader distribution system.

- In April 2024: Canadian government collaborated with property and casualty insurers to create a low-cost national flood insurance scheme to cover high-risk households in case of floods, which is the first public-paying public-industry initiative to fill in insurance coverage gaps and guarantee coverage access to vulnerable populations facing flood risks due to climate change.

These strategic activities have ensured the firms consolidate market positions, address climate issues, increase technological capabilities, and leverage opportunities in the emerging market.

The Canada Property & Casualty Insurance Market is segmented as follows:

By Insurance Type

- Auto Insurance

- Personal Auto

- Commercial Auto

- Property Insurance

- Homeowners

- Commercial Property

- Tenants/Renters

- Liability Insurance

- Other Insurance Types

- Boiler and Machinery

- Marine and Aircraft

- Surety and Fidelity

By Distribution Channel

- Direct

- Agents

- Brokers

- Banks

By End User

- Individual

- Commercial

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Canada Property & Casualty Insurance by Segments

- 2.1.2. Canada Property & Casualty Insurance by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Canada Property & Casualty Insurance Market Attractiveness Analysis, By Insurance Type

- 2.2.3. Canada Property & Casualty Insurance Market Attractiveness Analysis, By Distribution Channel

- 2.2.4. Canada Property & Casualty Insurance Market Attractiveness Analysis, By End User

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Escalating Climate-Related Catastrophic Losses Driving Market Transformation

- 3.1.2. Digital Transformation and Usage-Based Insurance Revolution

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Canada Property & Casualty Insurance Market – By Insurance Type

- 4.1. Insurance Type Market Overview, By Insurance Type Segment

- 4.1.1. Canada Property & Casualty Insurance Market Revenue Share, By Insurance Type, 2025 & 2035

- 4.1.2. Auto Insurance

- 4.1.2.1. Personal Auto

- 4.1.2.2. Commercial Auto

- 4.1.3. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Property Insurance

- 4.1.6.1. Homeowners

- 4.1.6.2. Commercial Property

- 4.1.6.3. Tenants/Renters

- 4.1.6.4. Liability Insurance

- 4.1.7. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Other Insurance Types

- 4.1.10.1. Boiler and Machinery

- 4.1.10.2. Marine and Aircraft

- 4.1.10.3. Surety and Fidelity

- 4.1.11. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Insurance Type Market Overview, By Insurance Type Segment

- Chapter 5. Canada Property & Casualty Insurance Market – By Distribution Channel

- 5.1. Distribution Channel Market Overview, By Distribution Channel Segment

- 5.1.1. Canada Property & Casualty Insurance Market Revenue Share, By Distribution Channel, 2025 & 2035

- 5.1.2. Direct

- 5.1.3. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Agents

- 5.1.7. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Brokers

- 5.1.11. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Banks

- 5.1.15. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Distribution Channel Market Overview, By Distribution Channel Segment

- Chapter 6. Canada Property & Casualty Insurance Market – By End User

- 6.1. End User Market Overview, By End User Segment

- 6.1.1. Canada Property & Casualty Insurance Market Revenue Share, By End User, 2025 & 2035

- 6.1.2. Individual

- 6.1.3. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Commercial

- 6.1.7. Canada Property & Casualty Insurance Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End User Market Overview, By End User Segment

- Chapter 7. Canada Property & Casualty Insurance Market – Regional Analysis

- 7.1. Canada Property & Casualty Insurance Market Overview, By Region Segment

- 7.1.1. Global Canada Property & Casualty Insurance Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Canada Property & Casualty Insurance Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Canada Property & Casualty Insurance Market Revenue, By Insurance Type, 2026 – 2035

- 7.1.4. Global Canada Property & Casualty Insurance Market Revenue, By Distribution Channel, 2026 – 2035

- 7.1.5. Global Canada Property & Casualty Insurance Market Revenue, By End User, 2026 – 2035

- 7.1. Canada Property & Casualty Insurance Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Canada Property & Casualty Insurance Market: Company Market Share, 2025

- 8.2. Global Canada Property & Casualty Insurance Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. Intact Financial Corporation

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Aviva Canada Inc.

- 9.3. Desjardins Group

- 9.4. Co-operators Group Limited

- 9.5. TD Insurance Group

- 9.6. Wawanesa Mutual Insurance Company

- 9.7. SGI CANADA Insurance Services Ltd.

- 9.8. RSA Canada

- 9.9. Economical Insurance

- 9.10. Pembridge Insurance Company

- 9.11. Others.

- 9.1. Intact Financial Corporation

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Custom Market Insights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

List Of Figure

Figures No 1 to 29

List Of Tables

Tables No 1 to 2

Prominent Player

- Intact Financial Corporation

- Aviva Canada Inc.

- Desjardins Group

- Co-operators Group Limited

- TD Insurance Group

- Wawanesa Mutual Insurance Company

- SGI CANADA Insurance Services Ltd.

- RSA Canada

- Economical Insurance

- Pembridge Insurance Company

- Others

FAQs

The key players in the market are Intact Financial Corporation, Aviva Canada Inc., Desjardins Group, Co-operators Group Limited, TD Insurance Group, Wawanesa Mutual Insurance Company, SGI CANADA Insurance Services Ltd., RSA Canada, Economical Insurance, Pembridge Insurance Company, Others.

Regulations play a major role in the market by conditioning rate approvals within different provinces that impact the flexibility of prices and profitability; requiring mandatory coverage that makes sure that everyone is insured whilst maintaining industry sustainability and ensuring that all are adequately covered; mandating consumer protection in governing terms and claims settlements of policies; requiring capital that ensures that the market is financially sound; creating provincial variations that create a fragmented market with varied competitive patterns; and implementing ongoing reforms, such as Ontario auto insurance changes that will be implemented in 2026 and the national flood program development that is seen as a government reaction to market challenges balancing consumer affordability, industry sustainability, and adequate protection objectives.

Climate change essentially alters the market by increasing catastrophic losses from USD 37 billion in 2016-2025 versus USD 14 billion in 2006-2015 as almost a three-fold increase, and necessitating significant increases in premiums to sustain actuarial sustainability, creating insurability issues in high-risk regions where coverage is no longer affordable or available, fostering industry advocacy of climate adapting investments, obliging complex risk modelling and catastrophe solutions, and encouraging product innovations such as overland flood coverage and resilient building incentives addressing the evolving risk landscape while maintaining market viability.

According to the present analysis, the Canada property and casualty insurance market is expected to grow to around USD 82.7 billion by 2035, with moderate growth due to climate related loss increases necessitating price increases, population and economic growth increasing the insurable base, property value booms in city centres, technological advancements leading to efficiency, regulation facilitating the market, and industry consolidation which creates scale effects, with a CAGR of 3.42 in the 2026-2035 period reflecting the challenges and opportunities that lead to an evolving market.

Auto insurance is projected to remain dominant, with about 50% market share based on universal coverage requirements in all provinces and territories, universal demand, high vehicle ownership with increasing registrations, a regulatory environment to ensure universal availability, high claims frequency, and about 192 private insurance companies besides government owned entities in BC, Saskatchewan, Manitoba and Quebec, which create a competitive marketplace with differentiated product offerings and different distribution channels to suit a variety of consumer tastes and risk profiles.

The fastest growth is observed in Alberta with a projected CAGR of 6.39% between 2026 and 2035 due to the expansion of the economy attributed to increased energy production and a diversification in technology and services. The population is growing due to interprovincial migration that brings about employment opportunities and a low cost of living, liberalization of the insurance market, and removal of the rate cap, letting the insurance market drive residential and commercial development, increasing the property insured base, and creating premium growth opportunities for the insurers serving this growing market.

Canada Property and Casualty Insurance Market is expected to have a moderate growth due to increasing catastrophic losses related to climate with 2024 record USD 8.5 billion surpassing 2020 record USD 6.0 billion and increasing vehicle registrations and rising population increase that brings new insured base, technological innovation, such as telematics and digital distribution is more efficient, regulatory changes to infrastructure, such as national flood insurance program that ensures sustainability in the market and growth of insurance awareness in the consumer population with its eye opener recent catastrophic losses.