Compostable Flexible Packaging Market Size, Trends and Insights By Material Type (PLA (Polylactic Acid)-Based, PHA (Polyhydroxyalkanoate)-Based, Starch-Based, Thermoplastic Starch (TPS), Starch/PLA Blends, Starch/PBAT Blends, Cellulose-Based, Regenerated Cellulose Films, Nanocellulose Composites, Other Materials), By Packaging Type (Pouches & Bags, Stand-Up Pouches, Flat-Bottom Pouches, Side-Gusset Bags, Films & Wraps, Liners, Other Packaging Types), By End Use (Food & Beverage, Personal Care & Cosmetics, Pharmaceuticals, Retail & E-Commerce, Other End Uses), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- NatureWorks LLC

- Novamont S.p.A.

- Danimer Scientific

- TIPA Corp.

- Others

Reports Description

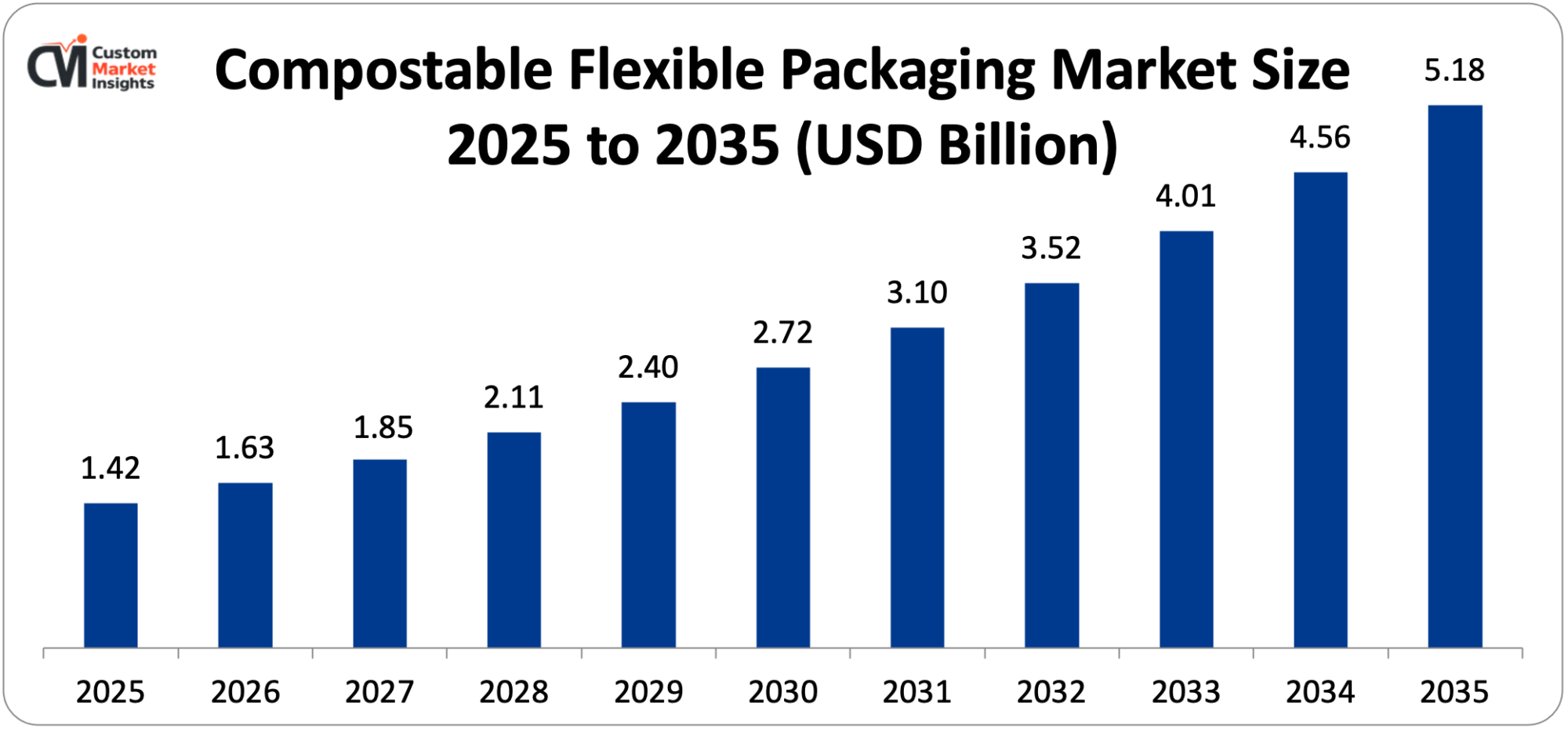

The market size of compostable flexible packaging is estimated to be USD 1.63 billion in 2026 and the prognosis is that it is going to grow by USD 5.18 billion between 2026 and 2035 with a CAGR of 12.3%.

The growing consumer and regulatory pressure to adopt a plastic-free supply chain, the increasing composting networks, increased investment in biopolymer development, and the increasing rate at which food and beverage brands switch to sustainable packaging solutions are all driving the market development.

Market Highlight

- Asia Pacific Aspect As one of the leading companies in the compostable flexible packaging market, it held a market share of 36% in 2025.

- Europe is the most developed regulatory market and is anticipated to capture 29% of the world revenue in 2025 with a CAGR of 11.6% between 2026 and 2035.

- By type of material, the PLA (polylactic acid)-based packaging has gained nearly 38% of market share in 2025.

- By type of material, the PHA-based segment is expanding at the quickest CAGR of 15.2% from 2026 to 2035.

- By end use, the food and beverage segment will contribute the highest market share of 54 in 2025, and the e-commerce and retail segment will have the highest projected CAGR of 16.8 in the next period between 2026 and 2035.

- By type of packaging, the pouches and bags achieved the highest share of 44% in 2025.

- Compostable flexible packaging has also taken a leading sustainable packaging market of about 8.3% of the global market compared to 5.6% in 2020, showing the rapid gains of the share.

Significant Growth Factors

The Compostable Flexible Packaging Market Trends present significant growth opportunities due to several factors:

- Intensifying Regulatory Pressure to Phase Out Conventional Plastics: The best and strongest catalyst driving faster adoption of compostable flexible packaging is the growing international regulatory system that aims at eliminating traditional single-use plastic packaging in practically all the key consumer markets. Governments across all continents are introducing bans, levies, prolonged producer responsibility (EPR) programs, and necessities of recycled content which are all finding the traditional plastic packaging more and more expensive and legally unsustainable. The Single-Use Plastics Directive, which has already banned a variety of single-use plastic products in the European Union, and the Packaging and Packaging Waste Regulation (PPWR), which was proposed in 2022 and is in the process of enactment into law, are expected to effectively ban all packaging by 2030 and only permit reusable or recyclable and compostable products, which in turn will pull certified compostable alternatives into the market. The Ellen MacArthur Foundation confirmed that over 130 million tonnes of plastic packaging are produced each year, of which less than 15% is collected and recycled into similar uses globally and only 2% of that is actually recycled into similar uses, and this creates the strong case of compostable alternatives that can bypass landfill by using industrial composting facilities. The United Nations Environment Programme (UNEP) is working to make a legally binding global plastics treaty, which, upon ratification would create additional regulatory pressures on nations, with 175 countries having already committed to complete the treaty talks, a move that observers believe could produce new tsunamis of voluntary and compulsory brand moves to compostable packaging over the period 2026-2035. On the national level, single-use plastics laws have been either introduced or extended in countries such as the United Kingdom, Canada, Australia, India, and dozens more since 2022 and disallowing specific types such as thin-film bags, sachets, and multi-layered pouches has compelled food brands and retailers to step up their roadmaps to compostable packaging. The financial pressure is also moving via EPR schemes, in France, Germany, the Netherlands and more and more in Asia, packaging manufacturers have to pay levies according to the recyclability or compostability profile of their packaging and this has produced a direct financial incentive to move to certified compostable flexible packages.

- Rising Consumer Environmental Consciousness and Brand Sustainability Commitments: Consumer behaviour towards packaging sustainability has experienced a structural and quantifiable change in the form of the environmental credentials becoming a determining factor in food, personal care and retail product purchases. A 2024 NielsenIQ global survey states that 73% of consumers state that they would certainly or likely shift their consumption behaviours to reduce environmental impact, and 66% of the people in the world say they would go out of their way to spend money on a product made by a brand committed to making a good environmental impact. This is directly being reflected in brand action: the large food and consumer goods companies such as Nestlé, Unilever, PepsiCo and Danone have established clear packaging sustainability goals that are binding them to ensure all packaging is reusable, recyclable or compostable by certain dates between 2025 and 2030. The reputational and business risk of being linked to plastic pollution, which is enhanced by the NGO campaigns, social media attention, and the growing visibility of environmental journalism, is influencing brand managers to move faster in switching packaging even before regulatory expiry. Food service and quick-service restaurants Chains worldwide have invested in compostable packaging as a direct food-contact product (wraps, liners, and bags), and the food service compostable packaging market segment alone is projected to expand at a CAGR of 14.1% through 2030. Changes are also being forced by retailers: in Europe, shelf listing requirements have compelled European grocery chains such as Carrefour, Tesco, and REWE, and natural retailers in the U.S. such as Whole Foods Market and Sprouts Farmers Market, to implement supplier packaging designs that use certified compostable or recyclable formats in preference over traditional plastic, in effect compelling category-wide changes. The combination of all these consumer and commercial pressures is a self-continuous cycle that would create a bigger addressable market in the use of compostable flexible packaging than would have been created because of regulatory compliance.

What are the Major Advances Changing the Compostable Flexible Packaging Market Today?

- Next-Generation Biopolymer Innovation and Material Performance Enhancement: The absolute obstacle to the adoption of compostable flexible packaging has traditionally been performance differences in comparison to traditional plastic films- in their moisture barrier characteristics, heat seal strength, mechanical durability, and their ability to extend shelf life. Next-generation biopolymer development and multi-layer compostable film engineering are the methods that advanced material science is currently using at high velocity to bridge these gaps. The existing leading compostable material in the market which is polylactic acid (PLA), with a current market share of 38%, is being developed with stereocomplex blending and nucleating agent modification to overcome one of its major limitations in hot-fill and retort packaging usage: the lack of heat resistance and the rate of crystallization. PHA (polyhydroxyalkanoate) polymers are becoming game changing materials promising marine biodegradability and better property profiles, the PHA market is expected to expand at 18.8% CAGR with the global PHA market reaching USD 97 million in 2024 to USD 383 million in 2032 as new production plants go online, companies such as Danimer Scientific, CJ BIO, and Kaneka continue to make more polymers. Flexible film films made using thermoplastic starch (TPS) with PLA or PBAT (polybutylene adipate terephthalate) are showing performance that is equivalent to standard LDPE and can be certified as home compostable which is a critical benefit compared to industrial compostable formats that rely on special infrastructure. Films made of cellulose such as transparent NatureFlex (Futamura) and barrier-enhanced cellulose are increasingly used in candy twist wraps, baked goods wrappings, and fresh produce pouches in which optical clarity is needed. Multi-layer compostable laminates of PLA/PBAT with inorganic barrier layers vacuum-deposited over them (SiOx, AlOx) are getting oxygen transmission rates of less than 1 cc/m²/day—nearing metallized conventional materials – making compostable packaging available to snack, coffee, and dry food packaging. Industry analysis As shown in the performance increases in materials, compostable flexible packaging has grown in the technically addressable application range by an estimated 35% between 2020 and 2025, and by another 25% by 2030.

- Scaling Industrial Composting Infrastructure and Certification Standardization: Scaling up of small and medium-sized composting infrastructure and the standardization of certified compostable material: Availability and accessibility of certified composting infrastructure are the determinants of yeomeness and commercial incentive of compostable flexible packaging. Industrial levels of composting capacity have been growing in size throughout the world: the Compost Manufacturing Alliance in the United States estimates that the number of certified composting facilities accepting compostable packaging will have grown to more than 540 by 2024, and much more is planned. The European Bioplastics association estimates that Europe handles around 130 million tonnes of organic waste every year, anaerobically digested and composted, and with infrastructure renovation, a new awareness is beginning to develop of certified compostable packaging used as a co-substrate. CEN standard EN 13432 sets industrial compostability standards in the EU, and EN 17437 compostability in the home compostability – standards that are the basis of the TUV Austria OK Compost certification system used in 50+ nations. ASTM D6400 is used in the U.S. as the composting standard basis of BPI (Biodegradable Products Institute) certification, used in most municipal compostable organics programs. The internationalization of the standards – talks are ongoing in ISO Technical Committee 61 to standardize compostability certification systems – is providing more clarity on the market and enhancing cross-border product development of multinational brands. There is also the emergence of digital tracking systems that install QR codes and smart labels on compostable packages, thus allowing consumers to find the nearest composting drop-off locations and brands access to product end-of-life information to prove their sustainability claims to retailers and regulators.

- E-Commerce Packaging Sustainability Revolution and Protective Compostable Solutions: The skyrocketing growth of e-commerce, in which global online retail sales had reached USD 6.3 trillion in 2024 and are expected to reach USD 8.0 trillion by 2027, is creating a large and rapidly growing demand channel of compostable flexible packaging solutions tailored to the performance attributes of direct-to-consumer shipping. The classic e-commerce packaging has been dependent on expanded polystyrene (EPS) void fill, polyethylene mailers, and bubble wrap – packages that are experiencing increasingly restrictive regulatory pressure as well as increasing consumer rejection. Compostable options such as kraft paper-lined compostable mailers, starch-based loose fill instead of EPS, compostable poly mailers based on PBAT/PLA blends, and mushroom based protective packaging by companies like Ecovative Design are spreading like wildfire. The compostable e-commerce packaging sub-segment is projected to grow at the quickest rate in the wider market at a CAGR of 16.8% between 2026 and 2035, which is no less impressive than the level of e-commerce growth and environmental frustration created by the disposal of non-recyclable plastics in the environment by consumers directly to their homes. Large e-commerce companies such as Amazon, which offers the Frustration-Free Packaging program, and Shopify, which makes sustainability pledges, are actively empowering and encouraging sellers to switch to their certified sustainable format packaging. The subscription box market, which is especially strong in compostable packaging as a brand distinguishing factor, is specifically aggressive in implementing compostable packaging as examples of the brand that demonstrate its commitment to environmentally responsible initiatives to the environmentally minded consumer groups in their real lives over the past several years.

- Digital Printing and Customization Enabling Brand Adoption: The situation of compostable packaging being barred commercially by large minimum order quantities and the setup costs of a flexographic or gravure printing system is being overcome with the advent of digital printing technology that can print on compostable substrates at shorter quantitative runs and with high customizability. The suppliers such as Siegwerk, Sun Chemical, and Flint Group, have also developed water-based and UV-curable inks that are certified as compostable film substrates, and these ink systems have been shown in testing to be compostable on certified substrates under the standards of EN 13432 and ASTM D6400. Brands can also create regionally tailored packaging with market-specific claims, seasonal designs, limited edition, and QR-code enabled digital content without compromising the sustainable positioning of the compostable substrate through digital printing onto compostable films. It can be projected that the global market of digital printing of flexible packaging will experience 8.4 CAGR until 2030, and compostable substrates are projected to be the fastest growing print media types in the said segment. To emerging and mid-size food brands, especially those serving natural, organic, and specialty foods, digital printing on compostable flexible packaging gives a route to high-end looking sustainable packaging at entry quantities, forming the long tail of the sustainability-motivated consumer brands.

Category Wise Insights

By Material Type

Why PLA-Based Materials Lead the Market?

Packaging made of PLA-based material will have the biggest market share, with a figure of about 38% in 2025. This leadership indicates how PLA is commercially the most mature and lowest cost compostable biopolymer with the NatureWorks Ingeo platform alone providing 750 converters of packaging worldwide with resin of PLA, backed by 400,000-plus metric tons per year production capacity of PLA throughout the world as of 2025. PLA is highly glossy, optically clear and moderately stiff, which is highly appropriate for food packaging products such as bakery overwraps, fresh produce windows, and cold-fill packaging. The production of the material using fermented plant-based feedstocks such as corn starch, sugarcane, and cassava gives a compelling source of renewable origin stories that can be strongly communicated in the brand sustainability message. The industry statistics have shown that PLA packaging has had a lifecycle greenhouse gas reduction of 5070% over petroleum based plastic, and this is a significant carbon footprint advantage that a brand is progressively quantifying and reporting on-pack.

The dominance of PLA in the market is also supported by the fact that its PLA-based films are easily certified: they are a PLA-based film and can acquire TUV Austria OK Compost Industrial and BPI certification that satisfies the requirements of most commercial composting programs worldwide. The fabric is also being more frequently digested in anaerobic digestion units and it has been proven that PLA can be broken down in AD settings given that it can be properly managed and that end of life pathways are further diversified. Relative moisture sensitivity and a low heat deflection temperature of about 55°C have in the past been used as barriers to PLA in terms of application in hot-fill or humid applications, but the latest generation of PDLA/PLLA stereocomplex blends with a high heat resistance of over 140°C are gradually eliminating such limitations.

The fastest-growing section of materials; PHA-based packaging, is projected to grow by a CAGR of 15.2% in the period between 2026 and 2035, owing to the distinct combination of marine biodegradability, home compostability, and property characteristics of PHA, which are closer to conventional plastics when compared to PLA. PHA polymers are currently manufactured by fermenting sugars, plant oils, and more recently methane and carbon dioxide by microbes, and the latter feeds allow a negative-carbon route of production. New production sites by firms such as Danimer Scientific, CJ BIO, Kaneka and Shenzhen Ecomann are expected to boost the global PHA market to USD 383 million by the year 2032 as compared to USD 97 million in 2024. With PHA production costs falling to the same level as PLA, a point a number of market analysts estimate to happen between 2028-32, volume adoption will happen significantly faster.

By End Use

Why Food & Beverage Dominates Compostable Flexible Packaging Applications?

The highest end-use segment is food and beverage applications that occupy about 54% of total market share in 2025. This preeminence is indicative of the regulatory compulsiveness that is specifically directed to food packaging plastic waste, the quantity and frequency of food packaging that produces significant volumes of addressable volumes, and the substantial compatibility between food brand sustainability stories and compostable packaging qualifications. The largest food application areas of compostable flexible packaging include fresh produce, bakery, snack food, dry goods, coffee, and tea, with each segment having a specific requirement in the form of barrier properties to modify closures. The Food and Agriculture Organization (FAO) estimates that one-third of all food produced in the world is lost or wasted; packaging failures are a major contributor in the fresh category, a dynamic that is making compostable packaging developers willing to invest a significant amount of money in trying to create barrier and shelf-life performance to prove that sustainable packaging does not mean compromised food preservation. Large food corporations such as Nestle, which has pledged to make all its packaging, including plastic, recyclable or reusable by 2025, are already experimenting with compostable packaging of confectionary, snacks, and coffee pods.

The food service industry of food and beverage is a very high-growth subcategory, where compostable bags, wraps and liners that substitute the use of conventional plastic in food service operations are adopted in municipalities that have adopted organics programs that require the use of compostable serviceware. Variations of requirements on food service packaging, requiring compostable formats certified or strongly encouraging them, have been implemented in Seattle, San Francisco, New York City, and Portland, in the United States, and in Amsterdam, London, and Copenhagen in Europe. The fastest growing market end-use segment is the retail and e-commerce with the CAGR of 16.8% between 2026 and 2035 where direct-to-consumer brands use compostable plastic mailers, tissue wraps, and poly bags as differentiation tools in the competitive and sustainability-focused direct-to-consumer marketplace.

By Packaging Type

Why Pouches & Bags Lead the Packaging Type Segment?

The biggest segment of the packaging type is pouches and bags, which will occupy about 44% of the market share in 2025. Stand-up, side-gusset, and flat-bottom pouches have achieved perfection as the most popular packaging styles in the food, coffee, pet food, and personal care segments based on impact on retail shelves, convenience to consumers, and efficiency compared to the rigid packaging styles. Commercial success of these formats translating to compostable forms has been a major target of flexible packaging converters and biopolymer resin manufacturers, and compostable stand-up pouch varieties are currently produced in industrial (PLA/PBAT laminates) and home (PHA/cellulose) compostable specifications. Compostable flexible films and wraps will have the second largest market, especially in fresh produce packaging, bakery over-wraps, and food service usage, where thin-gauge films with tight shrink or cling characteristics are essential.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 1.63 billion |

| Projected Market Size in 2035 | USD 5.18 billion |

| Market Size in 2025 | USD 1.42 billion |

| CAGR Growth Rate | 12.3% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Material Type, Packaging Type, End Use and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

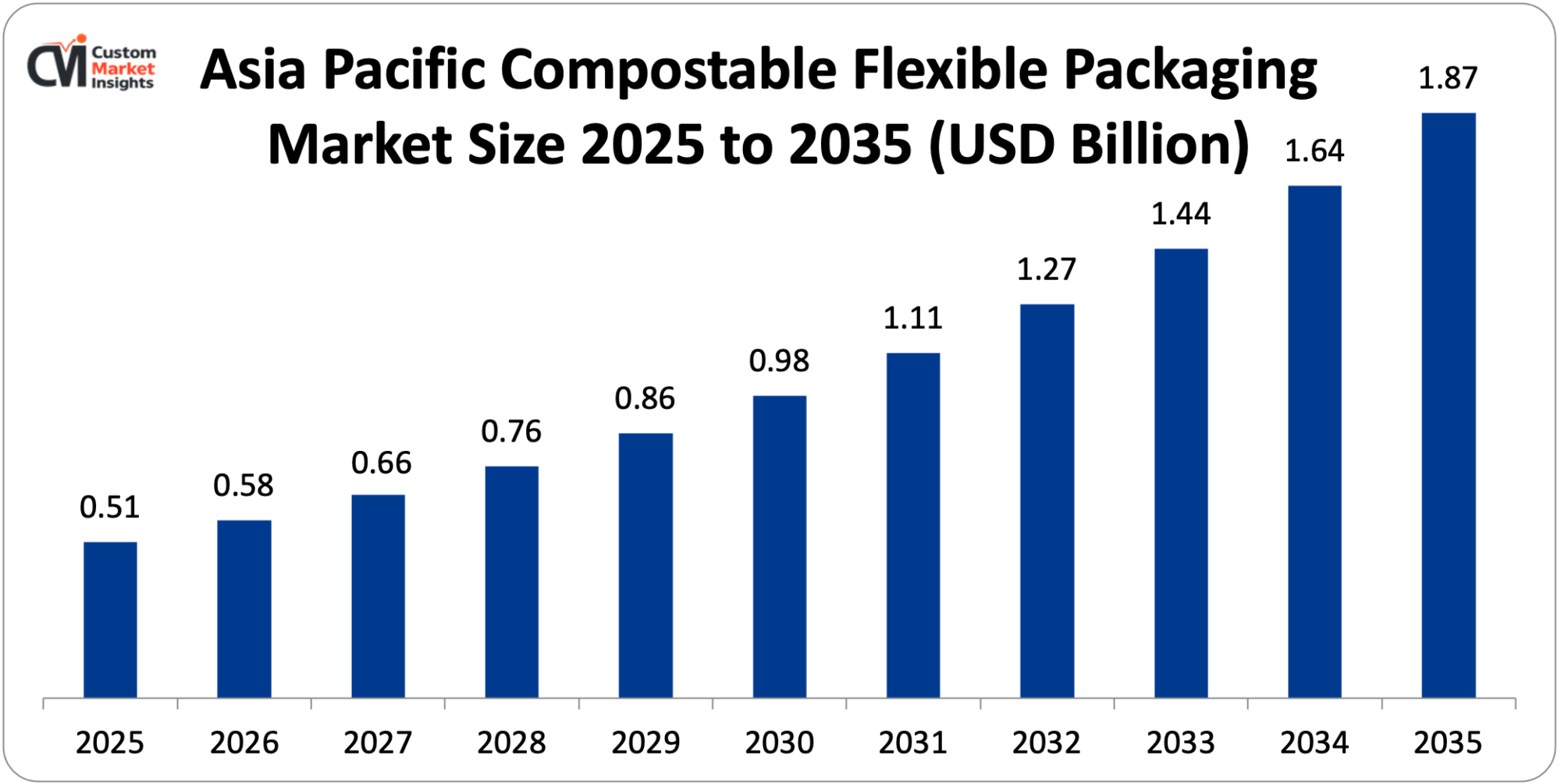

The Asia Pacific compostable flexible packaging market size is estimated at USD 512 million in 2025 and is projected to reach approximately USD 1.87 billion by 2035, with a CAGR of 13.8% from 2026 to 2035.

Why did Asia Pacific Dominate the Market in 2025?

Asia Pacific captures about 36% of the worldwide market share in 2025 due to the unison of huge packaging consumption volumes, swiftly increasing single-use plastics laws in the region, increasing production capacity of compostable packaging resources, and an increasing modern retail and food service industry that requires environmentally friendly packaging options. China, India, Japan, South Korea, and Australia represent the largest part of the regional demand, and each of them is fueled by various regulatory and commercial factors. The action plan on plastic pollution implemented by the National Development and Reform Commission in China, which prohibits single use plastic products and establishes a target of increased infrastructure to recycle and compost plastics, is generating market demand, with China having a large scale capacity of production of bioplastics packaging posing the country as both a consumer and producer of compostable flexible packaging. The adoption of compostable flexible packaging is also being driven by the Single Use Plastics ban implemented in India in phases since 2022 and the increasing presence in the Indian market of the organized food retail sector, with the market projected to grow by 14.6% CAGR between 2026 and 2035, one of the highest rates of growth of an individual country on the global front.

Why is Europe the Most Regulatory-Mature Market?

Europe is the most developed regulatory area of compostable packaging and is estimated to have around 29% market share in the world in 2025 worth USD 412 million. The EU Single-Use Plastics Directive, the Packaging and Packaging Waste Regulation, and the Farm to Fork strategy of the European Green Deal, which aims to package sustainable food systems in certified compostable packages, influence the European market, which has its individual EPR schemes in France, Germany, Spain, Italy, and other countries providing financial incentives to brands to use certified compostable packaging. The largest European packaging market, Germany, has a well-developed system of industrial composting and the DKT (Deutsches Kompostierzeichen) system of certification and Italy has the system of compostable produce bags in supermarkets that has been enforced since 2018 and created one of the highest rates of compostable flexible packaging utilization in the whole world. Many European flexible packaging converters, such as Mondi, Coveris and Constantia Flexibles are making significant investments in compostable materials, several of them also declaring compostable packaging product lines between 2023 and 2025.

What is the Size of the U.S. Market?

The U.S. compostable flexible packaging market size is calculated at USD 248 million in 2025 and is expected to reach approximately USD 816 million by 2035, growing at a CAGR of 12.7% between 2026 and 2035.

U.S. Market Trends

The patchwork of state and municipal regulation that drives the demand characterizes the U.S. market as opposed to a single federal framework, which makes the market complex and offers opportunities. SB 54 of California, which mandates 30% recycled content in single-use plastic packaging by 2028 with gradual increases in the requirement through 2032 has spurred a notable bundle of brand activity in all types of packaging. Certified compostable packaging is also now accepted in municipal organics programs in large metropolitan regions as a co-collection stream with food scraps, and the U.S. Composting Council reported an over 400% increase in composting facilities that accepted compostable packaging between 2019 and 2024. The natural and organic food market – an early adopter of compostable packaging with an estimated 22% of U.S. compostable flexible packaging revenue, although a smaller portion of total food sales – is compressed, with a concentration of sustainability-oriented brands in this market.

Why is the Middle East & Africa Region an Emerging Growth Market?

The LAMEA region is one of those opportunities that are emerging and developing, with single-use plastics laws being enacted in all countries of the Gulf Cooperation Council, modern retail infrastructure expanding in the UAE and Saudi Arabia where premium food brands are seeking sustainable packaging distinction, and composting infrastructure developing further in association with smart city initiatives in the Gulf countries. Africa, although, at present, with limited infrastructure in composting, portrays more of a long-term opportunity due to the urbanization process and the growth of organized food retail, with South Africa being the most promising market in the near future due to its rather developed retail industry and increased policy activity in plastic waste reduction.

Top Players in the Market and Their Offerings

- NatureWorks LLC

- Novamont S.p.A.

- Danimer Scientific

- TIPA Corp.

- Futamura Group

- Vegware

- Amcor plc

- Berry Global Group Inc.

- Mondi Group

- Sealed Air Corporation

- Others

Key Developments

The market has undergone significant developments as industry participants seek to expand capabilities and enhance product portfolios.

- In January 2025: TIPA Corp. declared the commercial introduction of its home compostable laminate portfolio in the high end food packaging including a transparent high barrier film construction in coffee packaging that was certified as TUV Austria OK Compost Home, further increasing the number of markets the high compostable systems could address with high barrier dry food packaging.

- In August 2021: NatureWorks stated they will expand capacity by 25% by April at its Blair, Nebraska PLA manufacturing plant and that they are building a new 75,000 metric ton/year integrated PLA plant in Thailand, and production will start in 2026, greatly increasing the availability of PLA to the global market, which will greatly supply the growing demand of the Asia Pacific region.

These strategic endeavours have enabled businesses to solidify market share, increase their product lines, increase material performance and certification expenses, and take advantage of the rapidly growing regulatory and commercial shift in the way people are moving to conventional plastic flexible packaging.

The Compostable Flexible Packaging Market is segmented as follows:

By Material Type

- PLA (Polylactic Acid)-Based

- PHA (Polyhydroxyalkanoate)-Based

- Starch-Based

- Thermoplastic Starch (TPS)

- Starch/PLA Blends

- Starch/PBAT Blends

- Cellulose-Based

- Regenerated Cellulose Films

- Nanocellulose Composites

- Other Materials

By Packaging Type

- Pouches & Bags

- Stand-Up Pouches

- Flat-Bottom Pouches

- Side-Gusset Bags

- Films & Wraps

- Liners

- Other Packaging Types

By End Use

- Food & Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Retail & E-Commerce

- Other End Uses

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Compostable Flexible Packaging by Segments

- 2.1.2. Compostable Flexible Packaging by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Compostable Flexible Packaging Market Attractiveness Analysis, By Material Type

- 2.2.3. Compostable Flexible Packaging Market Attractiveness Analysis, By Packaging Type

- 2.2.4. Compostable Flexible Packaging Market Attractiveness Analysis, By End Use

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Intensifying Regulatory Pressure to Phase Out Conventional Plastics

- 3.1.2. Rising Consumer Environmental Consciousness and Brand Sustainability Commitments

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Compostable Flexible Packaging Market – By Material Type

- 4.1. Material Type Market Overview, By Material Type Segment

- 4.1.1. Compostable Flexible Packaging Market Revenue Share, By Material Type, 2025 & 2035

- 4.1.2. PLA (Polylactic Acid)-Based

- 4.1.3. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. PHA (Polyhydroxyalkanoate)-Based

- 4.1.7. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Starch-Based

- 4.1.10.1. Thermoplastic Starch (TPS)

- 4.1.10.2. Starch/PLA Blends

- 4.1.10.3. Starch/PBAT Blends

- 4.1.11. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Cellulose-Based

- 4.1.14.1. Regenerated Cellulose Films

- 4.1.14.2. Nanocellulose Composites

- 4.1.15. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Other Materials

- 4.1.19. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Material Type Market Overview, By Material Type Segment

- Chapter 5. Compostable Flexible Packaging Market – By Packaging Type

- 5.1. Packaging Type Market Overview, By Packaging Type Segment

- 5.1.1. Compostable Flexible Packaging Market Revenue Share, By Packaging Type, 2025 & 2035

- 5.1.2. Pouches & Bags

- 5.1.2.1. Stand-Up Pouches

- 5.1.2.2. Flat-Bottom Pouches

- 5.1.2.3. Side-Gusset Bags

- 5.1.3. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Films & Wraps

- 5.1.7. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Liners

- 5.1.11. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Other Packaging Types

- 5.1.15. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Packaging Type Market Overview, By Packaging Type Segment

- Chapter 6. Compostable Flexible Packaging Market – By End Use

- 6.1. End Use Market Overview, By End Use Segment

- 6.1.1. Compostable Flexible Packaging Market Revenue Share, By End Use, 2025 & 2035

- 6.1.2. Food & Beverage

- 6.1.3. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Personal Care & Cosmetics

- 6.1.7. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Pharmaceuticals

- 6.1.11. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Retail & E-Commerce

- 6.1.15. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Other End Uses

- 6.1.19. Compostable Flexible Packaging Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End Use Market Overview, By End Use Segment

- Chapter 7. Compostable Flexible Packaging Market – Regional Analysis

- 7.1. Compostable Flexible Packaging Market Overview, By Region Segment

- 7.1.1. Global Compostable Flexible Packaging Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Compostable Flexible Packaging Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Compostable Flexible Packaging Market Revenue, By Material Type, 2026 – 2035

- 7.1.4. Global Compostable Flexible Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 7.1.5. Global Compostable Flexible Packaging Market Revenue, By End Use, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Compostable Flexible Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Compostable Flexible Packaging Market Revenue, By Material Type, 2026 – 2035

- 7.2.3. North America Compostable Flexible Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 7.2.4. North America Compostable Flexible Packaging Market Revenue, By End Use, 2026 – 2035

- 7.2.5. U.S. Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Compostable Flexible Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Compostable Flexible Packaging Market Revenue, By Material Type, 2026 – 2035

- 7.3.3. Europe Compostable Flexible Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 7.3.4. Europe Compostable Flexible Packaging Market Revenue, By End Use, 2026 – 2035

- 7.3.5. Germany Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Compostable Flexible Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Compostable Flexible Packaging Market Revenue, By Material Type, 2026 – 2035

- 7.4.3. Asia Pacific Compostable Flexible Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 7.4.4. Asia Pacific Compostable Flexible Packaging Market Revenue, By End Use, 2026 – 2035

- 7.4.5. China Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Compostable Flexible Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Compostable Flexible Packaging Market Revenue, By Material Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Compostable Flexible Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 7.5.4. The Middle-East and Africa Compostable Flexible Packaging Market Revenue, By End Use, 2026 – 2035

- 7.5.5. Saudi Arabia Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Compostable Flexible Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Compostable Flexible Packaging Market Revenue, By Material Type, 2026 – 2035

- 7.6.3. Latin America Compostable Flexible Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 7.6.4. Latin America Compostable Flexible Packaging Market Revenue, By End Use, 2026 – 2035

- 7.6.5. Brazil Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Compostable Flexible Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Compostable Flexible Packaging Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Compostable Flexible Packaging Market: Company Market Share, 2025

- 8.2. Global Compostable Flexible Packaging Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. NatureWorks LLC

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Novamont S.p.A.

- 9.3. Danimer Scientific

- 9.4. TIPA Corp.

- 9.5. Futamura Group

- 9.6. Vegware

- 9.7. Amcor plc

- 9.8. Berry Global Group Inc.

- 9.9. Mondi Group

- 9.10. Sealed Air Corporation

- 9.11. Others.

- 9.1. NatureWorks LLC

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Custom Market Insights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

List Of Figures

Figures No 1 to 38

List Of Tables

Tables No 1 to 46

Prominent Player

- NatureWorks LLC

- Novamont S.p.A.

- Danimer Scientific

- TIPA Corp.

- Futamura Group

- Vegware

- Amcor plc

- Berry Global Group Inc.

- Mondi Group

- Sealed Air Corporation

- Others

FAQs

The key players in the market are NatureWorks LLC, Novamont S.p.A., Danimer Scientific, TIPA Corp., Futamura Group, Vegware, Amcor plc, Berry Global Group Inc., Mondi Group, Sealed Air Corporation, Others.

The government regulations constitute the most influential market defining force and operate in a variety of distinct modes: bans on particular single-use plastic packaging formats directly removing the demand on traditional alternatives; EPR fee structures making compostable packaging economically competitive with conventional alternatives; government procurement policies specifying compostable packaging as a mandatory requirement in food service and event government-operated sectors; investment programmes in composting infrastructure creation that creates the end-of-life pathways required to substantiate compostability claims; and green labeling and certification frameworks that provide a definition of the regulation that provides a credible This combination of these regulatory levers and voluntary brand commitments and consumer pressure is producing a compounding adoption effect which will likely continue to drive market growth in the single digits.

Current cost: The relative cost of compostable flexible packaging is currently priced 40-120% higher than similar conventional plastic packaging, which is the greatest adoption barrier to cost-sensitive applications and markets. Plastic films made of PLA should cost between USD 2.50 and USD 4.50 per kilogram, compared to USD 1.20 to USD 1.80 per kilogram of similar LDPE or CPP films. Nevertheless, a variety of forces are gradually narrowing this premium: rising biopolymer production capacity through additional facilities of NatureWorks, CJ BIO and TotalEnergies Corbion is enhancing economies of scale; regulatory pressures such as EPR levies are raising the effective cost of traditional plastic packaging; carbon pricing in the EU ETS and other systems is also adding to the cost of petroleum-based resins; and more efficient converters in processing compostable substrates is lowering the cost of conversion premiums. The analysts forecast the premium upon PLA-based compostable films to narrow to 2040% over conventional offerings in 2030, and to a similarity in the high-volume commodity uses by 2035.

According to the current analysis, the market is expected to hit about USD 5.18 billion by 2035 owing to the regulatory requirements in the key markets, brand-led sustainability engagements, material performance advancements that broaden the technically addressable application range, infrastructure advancements that allow composting at a large scale, and the integration of new geographic markets such as India, Southeast Asia, and the Middle East in the compostable packaging adoption curve with a CAGR of 12.3 between 2026 and 2035.

Asia Pacific will be the most important in terms of revenue share, with the share increasing to 36% in 2025, and to an estimated 40% of the world market revenue in 2035 due to the dominant position of the region in world packaging consumption, rapid changes in regulations, and the increasing manufacturing capacity in biopolymer production and flexible packaging conversion.

The region of Asia Pacific is projected to expand at the quickest CAGR of 13.8% between 2026 and 2035, due to the enormous volume of packaging consumption in China, India, Japan, South Korea, and Australia; the rapid development of single-use plastics laws in the area; the rising domestic compostable packaging production capacity; and the rising contemporary retail and food service industries in need of convincing green-green packaging options.

It is expected that the Global Compostable Flexible Packaging Market will grow significantly due to the increasing regulatory bans on single-use plastics in 60 or more countries, consumer demands on sustainability with 73% of global consumers reporting readiness to modify consumption behavior towards environmental benefit, corporate pledges to use compostable packaging to meet 100% sustainable packaging by 2025-2030, the growth in industrial composting infrastructure with certified composting facilities growing more than 400% in the U.S. between 2019 and 2024, continued biopolymer innovation closing performance gaps with conventional plastics, and e-commerce expansion creating new demand vectors for compostable mailers and protective packaging.