EPDM Rubber Market Size, Trends and Insights By Fabrication Method (Compression Molding, Injection Molding, Extrusion, Calendaring, Blowing), By Product Type (Solid EPDM Rubber, EPDM Rubber Compounds, EPDM Rubber Sheets, EPDM Rubber Profiles, EPDM Rubber Molded Products), By Application (Automotive, Construction, Electrical and Electronics, Industrial, Medical), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 4.62%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- Kraton Corporation

- Lanxess AG

- Dow Inc.

- ExxonMobil Chemical

- Others

Reports Description

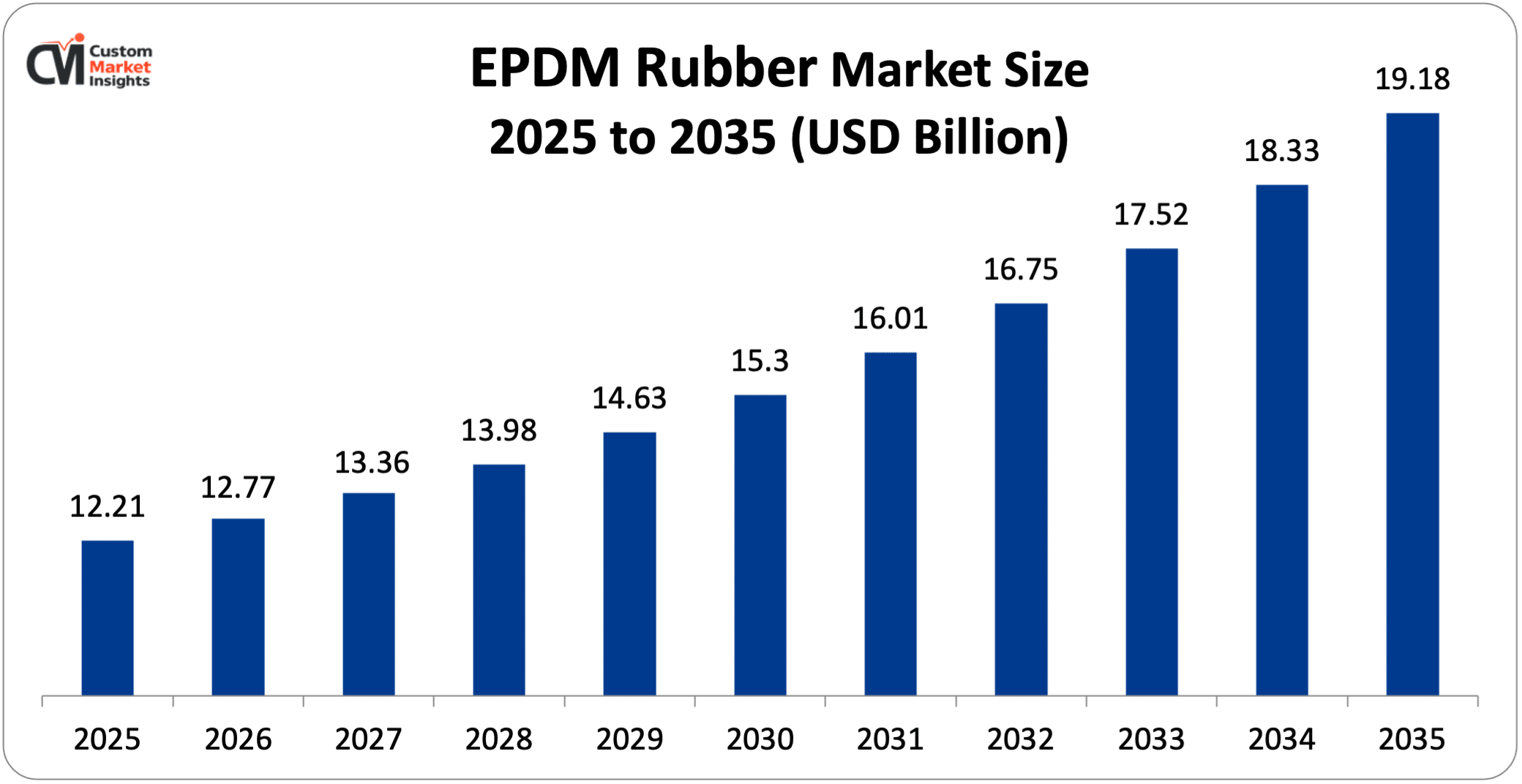

As per the EPDM rubber market analysis conducted by the CMI team, the EPDM rubber market is expected to record a CAGR of 4.62% from 2026 to 2035. In 2026, the market size was USD 12.77 Billion. By 2035, the valuation is anticipated to reach USD 19.18 Billion.

The market is expanding due to the transition of the automotive sector to EVs coupled with increased demand for long-lasting single-ply roofing membranes in green construction. North America is at the forefront of bio-based innovations, whereas the Asia Pacific is expected to witness the fastest CAGR during the forecast period.

Market Highlights

- North America dominated the EPDM rubber market in 2025 with 55.65% of the overall share.

- The Asia Pacific is expected to witness the fastest CAGR of 4.85% in the EPDM rubber market during the forecast period.

- By fabrication method, compression molding held around 54.37% of the market share by 2025.

- By fabrication method, injection molding is expected to witness the fastest CAGR of 4.34% between 2026 and 2035.

- Through product type, solid EPDM rubber dominated in 2025 with 60.23% of the overall market share.

- By product type, EPDM rubber compounds are expected to witness the fastest CAGR of 4.97% between 2026 and 2035.

- Through application, the automotive segment dominated in 2025 with 54.37% of the overall market share.

- By application, the construction segment is expected to witness the fastest CAGR of 4.07% between 2026 and 2035.

Significant Growth Factors

- Exponential Demand for Electric Vehicles (EVs)

Increased production of electric vehicles (EVs) translates to usage of specialized EPDM formulations for noise-vibration-harshness (NVH) systems and advanced thermal management. EPDM is known for superlative heat resistance and inherent electrical insulation. These properties make it indispensable for cooling hoses, battery enclosures, and high-voltage cable connectors. With automotive OEMs shifting away from ICEs (internal combustion engines), demand for metallocene-catalyzed, high-purity EPDM is increasing on a visible note. This, in turn, ascertains the long-term safety and reliability of EV battery architectures.

- Growing Inclination Toward Climate-Resilient and Sustainable Construction

With mounting pressure from decarbonization mandates, the construction industry is visibly adopting the EPDM single-ply roofing membranes owing to their five-decade lifecycle with extreme weatherability. The trend is expedited by bio-based EPDM’s development, which does leverage renewable feedstock in order to adhere to green building and LEED certifications. These factors are combined with investments in government infrastructure at a large scale, especially in the developing economies.

What are the Major Advancements Changing the EPDM Rubber Market Today?

- Commercialization of Sustainable and Bio-based EPDM

Kraton (a provider of bio-based products that replace petroleum-derived feedstock with sustainable, renewable sources like sugarcane-based ethanol) is commercializing Keltan Eco (its “green” EPDM technology that reduces the product’s carbon footprint without sacrificing the weather and heat resistance for which Keltan is known). Automotive OEMs, in their quest to simultaneously lower carbon footprints and expand “green” product offerings and sustainability initiatives, are seeking more than just rubber and plastic products that have been third-party-approved for green building certifications. Kraton has certainly made strides to offer such products. The producer’s Keltan Eco “green” EPDM technology replaces petroleum-derived feedstock with sustainable renewable sources such as sugarcane-based ethanol to lower the carbon footprint of a given product without sacrificing the quality and performance.

Producers of end-product consumer goods also require that their future car and truck tires (and all other rubber and plastic commodities in their respective automobiles) be made with materials that are low in carbon content and therefore renewable. This has resulted in a substantial market shift in terms of how much of a commodity-driven sector of the automotive market evolves into high-value, circular economy solutions.

- Integration of Metallocene Catalyst Systems

EPDM rubber’s performance and consistency are being elevated by the integration of metallocene catalyst systems. Metallocene, unlike conventional Ziegler-Natta catalysts, allows for accurate control over ethylene distribution and molecular structure, thereby resulting in the formation of EPDM with superlative physical properties and quicker curing rates. This advancement does facilitate the manufacture of low-gel, high-purity grades that are necessary for reliable gaskets and seals needed in EV battery systems and higher-voltage electrical insulation. Such high-performance polymers allow for production of lighter, thinner, and more durable components, thereby extending support to lightweighting and efficiency.

- Impact of AI on EPDM Rubber Market

AI is set to have an impact on several aspects, including the production and formulation of EPDM rubber, in addition to its maintenance and the quality of the final product. Ai is being used for performing formulation optimization by design. AI-driven formulation optimization technology is capable of rapidly providing manufacturers with sustainable, bio-based EPDM variants. Machine learning can be applied to optimizing ethylene-propylene ratios in addition to the other copolymer ratios in order to provide a viable option to manufacturers when formulating their EPDMs under extreme environmental stress. The use of AI however is likely to be more pronounced in the automotive and aerospace sectors. Deploying a machine learning system can considerably reduce the R&D cycles of automotive and aerospace seals with the predictive capabilities of the AI.

AI is also anticipated to play an important role in the predictive maintenance of production plants. AI-powered predictive maintenance solutions can play a vital role in reducing any downtime. Machine learning can be applied to the solutions that will help manufacturers optimally plan their operations while optimizing energy consumption during vulcanization. This, however, may see limited adoption owing to the vulnerability of machine learning models to volatile feedstock costs. The application of AI for manufacturing could also provide manufacturers with the ability to optimize their recycling and reuse strategies.

Category Wise insights

By Fabrication Method

-

Why is compression molding dominating the EPDM rubber market?

This process is customized for ensuring superior performance in the final part, such as heavy-duty engine mounts or automotive gaskets. The process results in the formation of parts that can provide significantly increased load-bearing capabilities, with precise dimensions, functional surface parameters, and tolerances. Compression molding is basically used for producing large, thick, or geometrically complex components that need high structural integrity. Common applications include large-scale gaskets and seals. The overall advantages of this process, such as minimal material waste and nearly uniform cross-linking in part thickness, do largely contribute to strengthening the final part and providing superlative mechanical properties.

By Product Type

- How is solid EPDM rubber leading the EPDM rubber market?

Solid EPDM rubber is leading the EPDM rubber market owing to its superlative mechanical strength coupled with higher density, which does make it one of the preferred choices for heavy-duty industrial applications wherein durability is paramount. Solid EPDM also offers the highest resistance to physical wear and compression set, thereby upholding its dominance in segments like window seals, automotive weatherstripping, and radiator hoses. Also, its ability to get precisely extruded into complicated profiles while retaining structural integrity lets it capture most of the aerospace and construction revenue.

By Application

- Why does the automotive sector dominate the EPDM rubber market?

The automotive sector dominated the EPDM rubber market, as EPDM rubber is known for its exceptional ozone resistance and thermal stability, which do make it one of the industry standards for various sealing systems, inclusive of glass run channels, weatherstripping, and radiator hoses. Its ability to maintain structural integrity and flexibility under extreme temperatures does ensure a longer life span for components of vehicles. Also, transformation to EVs has amplified its dominance, as EPDM has exceptional vibration-dampening and electric insulation properties.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 12.77 Billion |

| Projected Market Size in 2035 | USD 19.18 Billion |

| Market Size in 2025 | USD 12.21 Billion |

| CAGR Growth Rate | 4.62% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Fabrication Method, Product Type, Application and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How big is North America’s EPDM rubber market size?

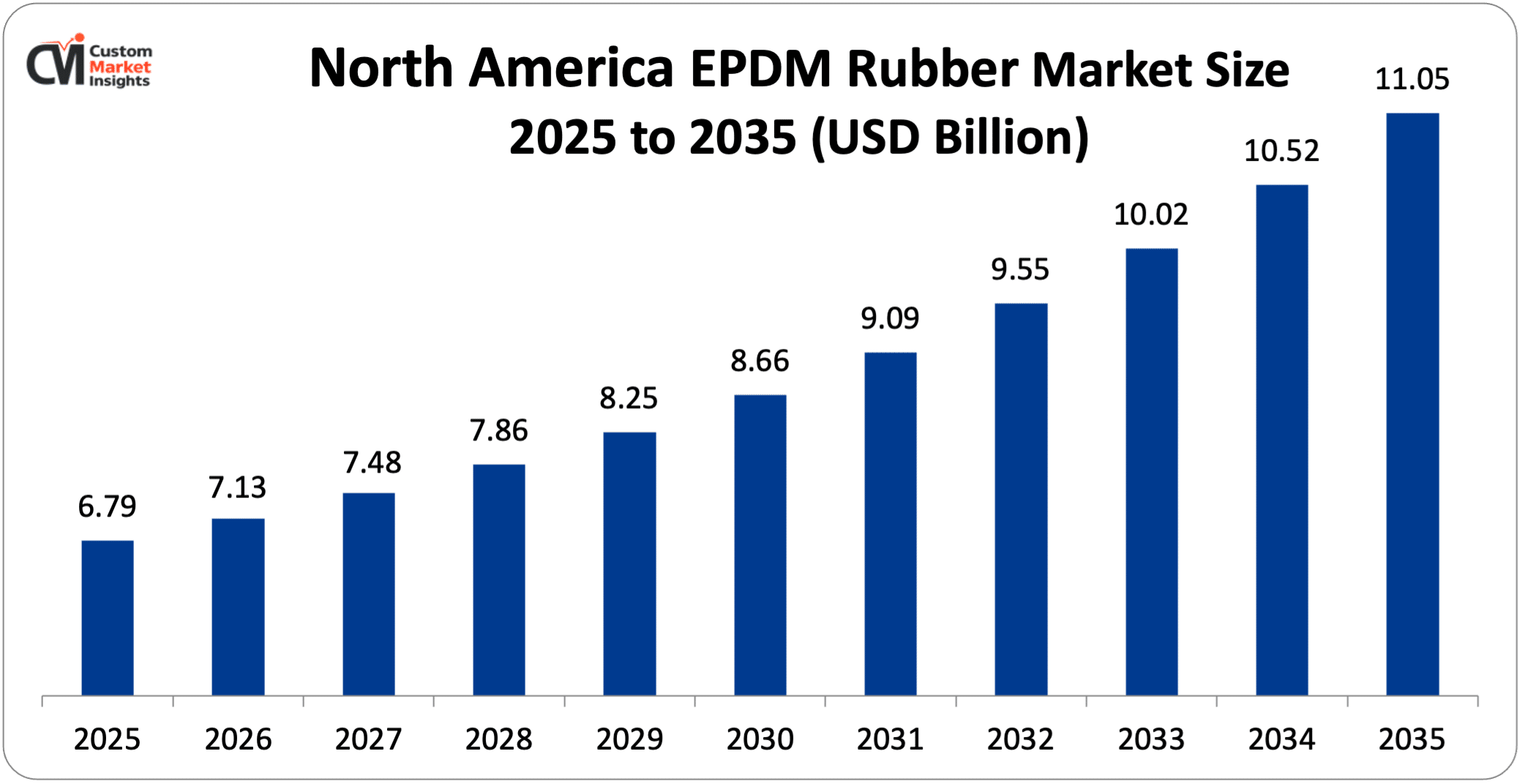

North America’s EPDM rubber market was worth USD 6.79 Billion in 2025 and is expected to reach USD 11.05 Billion by 2035 at a CAGR of 4.99% between 2025 and 2035.

Why did North America Dominate the EPDM Rubber Market in 2025?

North America dominated the EPDM rubber industry in 2025 owing to the presence of an established automotive manufacturing base and the expansion of the construction sector in the region. A major end-user of EPDM rubber is the automotive industry that uses several components such as tires, interior and exterior trims, seals, and gaskets. EPDM rubber provides exceptional weather resistance, flexibility, and durability, thereby improving automotive applications and performance features. Moreover, the construction sector, a major EPDM rubber end-user, will drive the demand for highly energy-efficient single-ply roofing membranes on account of rising infrastructure in the region. Market players including ExxonMobil and Dow are investing heavily in North America to produce high-performance, solution-polymerized EPDM grades that are used in manufacturing tires for electric vehicles (EVs).

What is the Size of the U.S. EPDM Rubber Market?

The market size of the U.S. EPDM rubber was USD 5.19 Billion in 2025 and is expected to reach USD 8.12 Billion in 2035, witnessing a CAGR of 4.63% between 2026 and 2035.

U.S. EPDM Rubber Market Trends

The growth of the U.S. EPDM rubber market from 2026 to 2035 is likely to be driven by the electrification of the automotive sector coupled with strong demand for climate-resilient infrastructure. The production of electric vehicles (EVs) calls for specialized EPDM grades for advanced battery cooling systems and noise-vibration-harshness (NVH) dampening. Climate-resilient EPDM is critical to the construction of higher reflecting EPDM roofing membranes for buildings, thereby adhering to tightening federal energy-efficiency standards and Leed certifications.

Why is the Asia Pacific experiencing the fastest growth in the EPDM rubber market?

The Asia Pacific region is projected to witness the fastest CAGR in the ethylene propylene diene monomer (EPDM) rubber market at the highest compound annual growth rate (CAGR) across the forecast period. This region is now an advanced manufacturing collaborator and global hub for electric vehicle (EV) manufacturing, while massive infrastructure spending in the Asia Pacific region is further anticipated to drive the demand for EPDM rubber products.

The governments of china and india is changing urbanization policies and implementing lucrative FDI schemes that would drive the demand for EPDM rubber products in the region. The demand for roofing membranes and weather-resistant seals for high-rise construction in china and india is likely to boost the demand for EPDM rubber products in the upcoming period. In addition, urbanization is the core policy focus of china and india, driving construction activities across the two nations. According to the “automotive mission plan 2026” policy, India’s PLI scheme is further incentivizing the local and domestic production of EPDM rubber components in the region.

China EPDM Rubber Market Trends

China’s EPDM rubber market is witnessing growth due to the emergence of numerous intricacies in the EPDM rubber industry. China is anticipated to produce the largest amount of EPDM rubber by 2026, while it is forecasted that from 2026 to 2035 the nation will experience a notable growth rate. In contrast to conventional goals of high-volume production, the industry is bound to concentrate on the production of high-value specialty grades. Given the importance of sustainability in the national economy and environmental protection, the “dual carbon” objectives are bound to imply a key industry advancement from 2026 until 2035. Additionally, the expansion of china’s new energy vehicle (NEV) sector will lead to a rise in production as the world’s largest EPDM consumer. In order to reduce reliance on high-end imports, which are often more affordable, china is increasing its domestic production capacity, especially that of specialty grades. China has the ability to enhance its position as the major EPDM manufacturer in the global EPDM market, especially in the specialty grades segment, due to the implementation of new solution-polymerization technologies.

Where does Europe stand with respect to the EPDM rubber market?

Europe is a mature, high-value market regarding the production and adoption of innovative recycled and bio-based EPDM variants. The launch of the European green deal that aims to make europe the first climate-neutral continent by 2050 has already led governments across several sectors to adopt targets and strategies aligned with circular economy principles. The European union’s reach (registration, evaluation, authorisation and restriction of chemicals) legislation, established in 2007 calls for manufacturers to develop considerably more sustainable EPDM solutions, which would be characterized by lower carbon footprints.

Furthermore, Europe’s automotive and construction sectors are characterized by a comparatively higher density of demand for premium-grade EPDM products, where Europe’s EPDM players (e.g., Arlanxeo and Versalis) have successfully created value through the introduction of specialized, high-purity grades designed for the manufacture of end-use products that comply with stringent low-VOC emission standards.

Germany EPDM Rubber Market Trends

Germany’s EPDM rubber market is poised to grow on a strong note between 2026 and 2035 with increased demand for sustainability as a result of the nation’s decarbonization goals, electric vehicle (EV) production, and numerous high-tech automotive and construction applications. As consumer interest in long-lasting, sustainable alternatives rises, the specialized EPDM grades enable advanced thermal management and noise-vibration-harshness (NVH) systems for automotive applications. EPDM grades prove an ideal fit for the construction sector, thereby making way for long-lifecycle roofing membranes and window seals. Sustainability mandates, which are offered by the European Union’s circular economy, have also spurred the advent of bio-based and recyclable variants.

Where is the Middle East & Africa regarding the EPDM rubber market?

The Middle East & Africa (MEA) EPDM rubber market grows due to the region being recognized as a high-growth industrial manufacturing hub, with the broader regional market projected to expand at a decent CAGR between 2026 and 2035. Growth is concentrated in the GCC countries, particularly in Saudi Arabia, where the expansion of the automotive and construction sectors under vision 2030 is driving localized demand for weather-resistant roofing and membranes and seals. While the region benefits from low-cost feedstock availability bolstered by the major production facilities like the Petro Rabigh joint venture, the market remains bifurcated between the foundational infrastructure needs of Sub-Saharan Africa and high-tech, energy-efficient construction projects in the gulf. Furthermore, rising investments in renewable energy installations across south Africa and Morocco have generated demand for EPDM-based electrical insulation and high-durability seals for wind power and solar applications.

Brazil EPDM Rubber Market Trends

Brazil’s EPDM rubber market is expected to expand on the back of a revitalized automotive sector coupled with the expansion of the civil construction industry under government initiatives like the new growth acceleration program (PAC). A basic trend is the adoption of bio-based EPDM, wherein it is leveraging brazil’s extensive ethanol production as a sustainable feedstock to align with global decarbonization targets. Moreover, as the economy upscales its renewable energy infrastructure, the demand is rising for EPDM-based electrical insulation and high-durability seals for solar and wind installations. To quell the impact of fluctuations in currency on imported raw materials, there is a distinct switch to localized manufacturing and the development of high-performance grades specifically formulated for the region’s tropical weathering conditions.

Top players in the EPDM Rubber Market and their Offerings

- Kraton Corporation

- Lanxess AG

- Dow Inc.

- ExxonMobil Chemical

- Kumho Polychem Co. Ltd.

- JSR Corporation

- Mitsui Chemicals Inc.

- Trelleborg AB

- SABIC

- Others

Key Developments

The EPDM rubber market has experienced considerable changes in the last few years as the market players are trying to diversify their technological aspects and develop product portfolios using strategic approaches.

- In July 2024, Dow announced that it had launched a novel line of bio-based EPDM called NORDEL REN Ethylene Propylene Diene Terpolymers (EPDM) to provide sustainability to the infrastructure and automotive sectors.

These strategic measures have enabled the companies to reinforce their competitive positions, increase the product line, boost their technological competencies, and also seize growth opportunities in the fast-growing EPDM rubber market.

The EPDM Rubber Market is segmented as follows:

By Fabrication Method

- Compression Molding

- Injection Molding

- Extrusion

- Calendaring

- Blowing

By Product Type

- Solid EPDM Rubber

- EPDM Rubber Compounds

- EPDM Rubber Sheets

- EPDM Rubber Profiles

- EPDM Rubber Molded Products

By Application

- Automotive

- Construction

- Electrical and Electronics

- Industrial

- Medical

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. EPDM Rubber by Segments

- 2.1.2. EPDM Rubber by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. EPDM Rubber Market Attractiveness Analysis, By Fabrication Method

- 2.2.3. EPDM Rubber Market Attractiveness Analysis, By Product Type

- 2.2.4. EPDM Rubber Market Attractiveness Analysis, By Application

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Exponential Demand for Electric Vehicles (EVs)

- 3.1.2. Growing Inclination Toward Climate-Resilient and Sustainable Construction

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. EPDM Rubber Market – By Fabrication Method

- 4.1. Fabrication Method Market Overview, By Fabrication Method Segment

- 4.1.1. EPDM Rubber Market Revenue Share, By Fabrication Method , 2025 & 2035

- 4.1.2. Compression Molding

- 4.1.3. EPDM Rubber Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Injection Molding

- 4.1.7. EPDM Rubber Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Extrusion

- 4.1.11. EPDM Rubber Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Calendaring

- 4.1.15. EPDM Rubber Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Blowing

- 4.1.19. EPDM Rubber Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Fabrication Method Market Overview, By Fabrication Method Segment

- Chapter 5. EPDM Rubber Market – By Product Type

- 5.1. Product Type Market Overview, By Product Type Segment

- 5.1.1. EPDM Rubber Market Revenue Share, By Product Type , 2025 & 2035

- 5.1.2. Solid EPDM Rubber

- 5.1.3. EPDM Rubber Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. EPDM Rubber Compounds

- 5.1.7. EPDM Rubber Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. EPDM Rubber Sheets

- 5.1.11. EPDM Rubber Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. EPDM Rubber Profiles

- 5.1.15. EPDM Rubber Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. EPDM Rubber Molded Products

- 5.1.19. EPDM Rubber Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Product Type Market Overview, By Product Type Segment

- Chapter 6. EPDM Rubber Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. EPDM Rubber Market Revenue Share, By Application , 2025 & 2035

- 6.1.2. Automotive

- 6.1.3. EPDM Rubber Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Construction

- 6.1.7. EPDM Rubber Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Electrical and Electronics

- 6.1.11. EPDM Rubber Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Industrial

- 6.1.15. EPDM Rubber Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Medical

- 6.1.19. EPDM Rubber Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. EPDM Rubber Market – Regional Analysis

- 7.1. EPDM Rubber Market Overview, By Region Segment

- 7.1.1. Global EPDM Rubber Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global EPDM Rubber Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global EPDM Rubber Market Revenue, By Fabrication Method , 2026 – 2035

- 7.1.4. Global EPDM Rubber Market Revenue, By Product Type , 2026 – 2035

- 7.1.5. Global EPDM Rubber Market Revenue, By Application , 2026 – 2035

- 7.2. North America

- 7.2.1. North America EPDM Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America EPDM Rubber Market Revenue, By Fabrication Method , 2026 – 2035

- 7.2.3. North America EPDM Rubber Market Revenue, By Product Type , 2026 – 2035

- 7.2.4. North America EPDM Rubber Market Revenue, By Application , 2026 – 2035

- 7.2.5. U.S. EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe EPDM Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe EPDM Rubber Market Revenue, By Fabrication Method , 2026 – 2035

- 7.3.3. Europe EPDM Rubber Market Revenue, By Product Type , 2026 – 2035

- 7.3.4. Europe EPDM Rubber Market Revenue, By Application , 2026 – 2035

- 7.3.5. Germany EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific EPDM Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific EPDM Rubber Market Revenue, By Fabrication Method , 2026 – 2035

- 7.4.3. Asia Pacific EPDM Rubber Market Revenue, By Product Type , 2026 – 2035

- 7.4.4. Asia Pacific EPDM Rubber Market Revenue, By Application , 2026 – 2035

- 7.4.5. China EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa EPDM Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa EPDM Rubber Market Revenue, By Fabrication Method , 2026 – 2035

- 7.5.3. The Middle-East and Africa EPDM Rubber Market Revenue, By Product Type , 2026 – 2035

- 7.5.4. The Middle-East and Africa EPDM Rubber Market Revenue, By Application , 2026 – 2035

- 7.5.5. Saudi Arabia EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America EPDM Rubber Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America EPDM Rubber Market Revenue, By Fabrication Method , 2026 – 2035

- 7.6.3. Latin America EPDM Rubber Market Revenue, By Product Type , 2026 – 2035

- 7.6.4. Latin America EPDM Rubber Market Revenue, By Application , 2026 – 2035

- 7.6.5. Brazil EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America EPDM Rubber Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. EPDM Rubber Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global EPDM Rubber Market: Company Market Share, 2025

- 8.2. Global EPDM Rubber Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. Kraton Corporation

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Lanxess AG

- 9.3. Dow Inc.

- 9.4. ExxonMobil Chemical

- 9.5. Kumho Polychem Co. Ltd.

- 9.6. JSR Corporation

- 9.7. Mitsui Chemicals Inc.

- 9.8. Trelleborg AB

- 9.9. SABIC

- 9.10. Others.

- 9.1. Kraton Corporation

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Healthcare Foresights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

- Chapter 12. List Of Figures

- 12.1. Figures No 1 to 31

- Chapter 13. List Of Tables

- 13.1. Tables No 1 to 46

Prominent Player

- Kraton Corporation

- Lanxess AG

- Dow Inc.

- ExxonMobil Chemical

- Kumho Polychem Co. Ltd.

- JSR Corporation

- Mitsui Chemicals Inc.

- Trelleborg AB

- SABIC

- Others

FAQs

The key players in the market are Kraton Corporation, Lanxess AG, Dow Inc., ExxonMobil Chemical, Kumho Polychem Co. Ltd., JSR Corporation, Mitsui Chemicals Inc., Trelleborg AB, SABIC, Others.

Government regulations and public infrastructure policies that mandate stringent environmental and quality standards for production processes and end-use applications are driving manufacturers in the EPDM rubber market toward higher-performance and more sustainable materials. The EU’s reach regulations coupled with strict EPA emissions standards have catalyzed the development of recyclable and biodegradable EPDM variants that minimize carbon footprints and volatile organic compound (VOC) emissions. The U.S. infrastructure investment and jobs act and India’s production linked incentive (PLI) scheme are expediting the demand for weather-resistant sealing and roofing solutions, which are, in turn, creating a need for sustainable alternatives to petrochemical-based rubbers. Lead players are shifting their focus to sustainable, high-performance formulations driven by the goals of the Paris Agreement.

EPDM pricing is basically driven by cost dynamics inherent in propylene and ethylene feedstock (primary sources) and the global demand for rubber products. Large volumes of product (zillions of pounds) are required for serving premium EPDM grades, which contribute to the cost. As production expands for capturing price-sensitive sectors, substitutes (e.g., SBR and natural rubber) reduce the total available market for EPDM. Two regions—North America and Europe—currently prefer premium EPDM grades over substitute resins but will expand the total available market for bio-based EPDM as day-to-day and end-of-product-life disposal regulations dictate multiple ongoing sustainability needs. Ultimately, the conditions that facilitate bio-based EPDM demand in North America and Europe (regulatory sustainability requirements) are satisfied in Asia Pacific for regional adoption.

The market for EPDM rubber is expected to witness a significant growth of about USD 19.18 Billion in the year 2035 with a CAGR of 4.62% between the years 2026 and 2035 due to growing demand for weather-resistant materials from construction and automotive verticals, apart from modernization of government infrastructure and sustainable construction solutions.

North America is projected to capture the maximum share in the EPDM rubber market through 2035. This is attributed to the recovering automotive manufacturing sector, along with green building initiatives. Key applications of EPDM-based roofing membranes include high-performance roofing membranes used for single-ply membranes and flat roofs, which help in lowering the cooling cost. ExxonMobil and Dow, and likewise, are focusing on the delivery of high-grade, solution-polymerized EPDM that has superlative heat and weather resistance. Successful implementation of the U.S. infrastructure investment and jobs act is projected to boost the demand for EPDM-based seals and gaskets for public works. The growth of the electric vehicles (EVs) industry is also bound to play a crucial role in uplifting the overall market statistics in the upcoming period.

The Asia Pacific is expected to witness the fastest CAGR in the EPDM rubber market due to industrial expansion and infrastructure spending. The growing number of smart city projects and electric vehicle (EV) manufacturing in the region are expected to further propel industry growth. The major players operating in the region are setting up numerous production facilities to cater to the rising demand, given the competitive pricing in the region owing to lower manufacturing costs. Increased government investments in various sectors, including construction and automotive, are providing considerable revenue opportunities to product manufacturers for extending their applications. EPDM is widely used for manufacturing weather-resistant roofing and seals for buildings and components like wheels, discs, and impact bumpers for automobiles that are rapidly used to cater to the increasing demand from the global hub for electric vehicle (EV) manufacturing.

The factors majorly contributing to the EPDM rubber market are EPDM’s resistance to weathering, heat, and ozone; high-performance automotive seals; and single-ply roofing membranes. The global push for electric vehicles (EVs) has created a notable demand for vibration-dampening materials and electrical insulation, like battery enclosures and advanced cooling systems, with certain EPDM variants being preferred for use as sustainable construction materials, basically due to low costs for gaining government investments in infrastructure modernization. Also, the demand for EPDM rubber in emerging economies would further propel forward the global effort in switching from conventional to long-lasting elastomers in the automotive and construction markets.