Europe Privacy Management Software Market Size, Trends and Insights By Component (Software, Data Discovery & Mapping, Consent Management, DSAR Automation, Privacy Impact Assessment, Vendor Risk Management, Services, Professional Services, Managed Services), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Industry Vertical (BFSI (Banking, Financial Services, Insurance), Healthcare & Life Sciences, RetAIl & E-commerce, IT & Telecommunications, Government & Public Sector, Manufacturing, Media & EntertAInment, Others), By Functionality (Data Mapping & Discovery, Consent Management, Data Subject Access Requests (DSAR), Privacy Impact Assessment (PIA), Vendor & Third-Party Risk Management, Cookie & Tracker Management, Breach Response Management, Privacy TrAIning & Awareness), and By Region - Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Europe |

| Largest Market: | Europe |

Major Players

- OneTrust

- BigID

- TrustArc

- Securiti ai

- Others

Reports Description

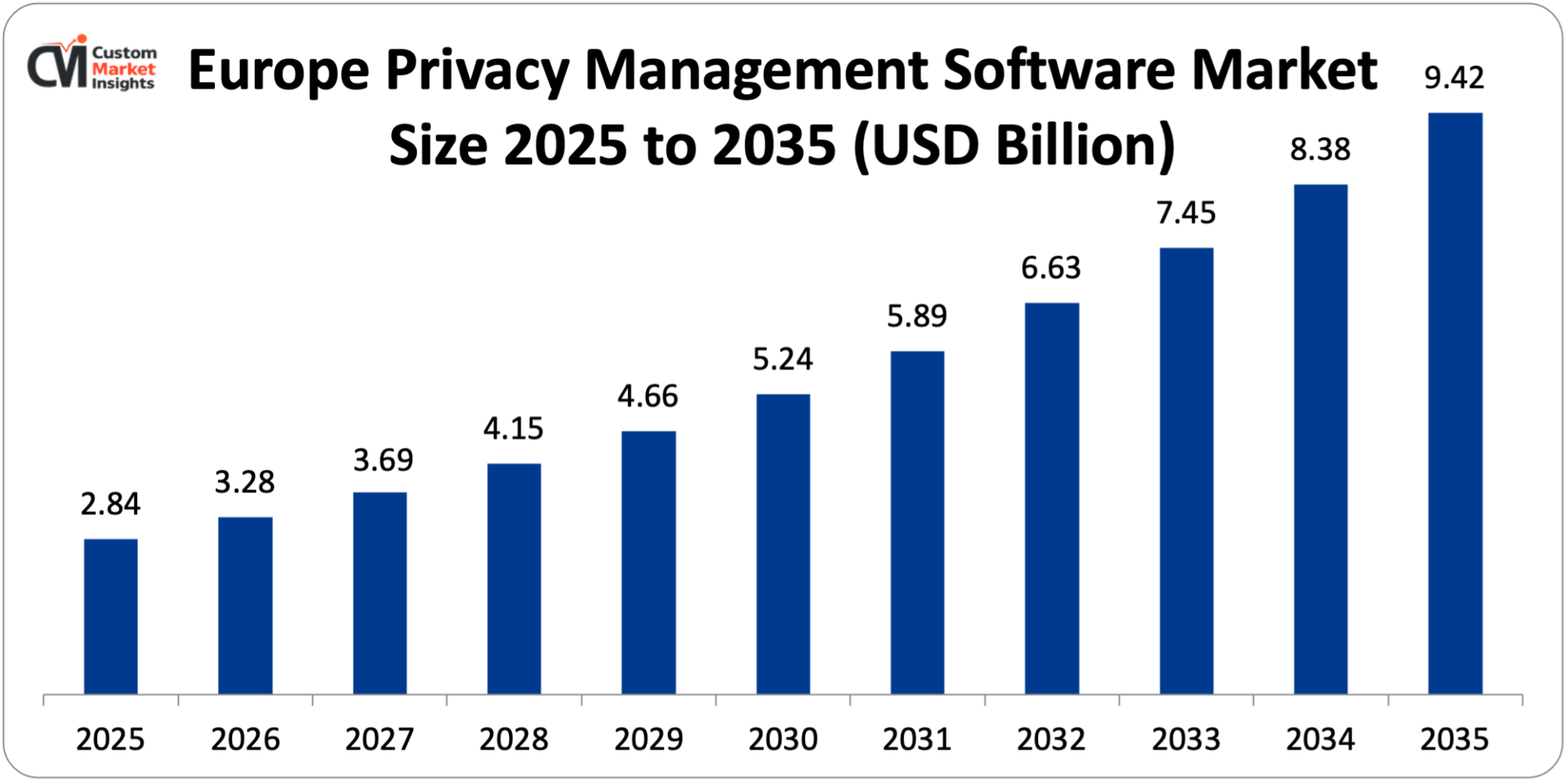

It is projected that the market size of the Europe privacy management software market will be USD 2.84 billion in the year 2025, and at an annual CAGR of 15.4% between 2026 and 2035, it is projected that the market size is going to increase to USD 3.28 billion in the year 2026 and to approximately USD 9.42 billion in the year 2035.

The market is expanding due to the highly restrictive enforcement of GDPR with penalties ever increasing with non-use, advancements in control of data privacy rules in EU member states and the UK, enhanced customer understanding and assertion of privacy rights, augmented quantity of individual data requiring handling across digital ecologies, and augmented cyber threats compelling elaborate information protection frameworks.

Market Highlight

- The Europe privacy management software market has a 28% market share in the United Kingdom, which is the market leader in the market in 2025.

- Germany will increase by 16.8% in the duration between 2026 and 2035.

- By component, the software segment had conquered 64% of the market share in 2025.

- By mode of deployment, the cloud-based segment will record the largest CAGR of 16.2% over 2026–2035.

- In terms of size, the large enterprises segment contributed 68% of market share in 2025.

- By the industry vertical, BFSI had 32% market share in 2025.

- It is also important to note that the USD 4.8 billion of GDPR fines levied by the EU data protection regulators in 2024 and the 142,000 data breach notifications that have been registered confirm that regulations have been implemented for the software adoption in the area.

Significant Growth Factors

- Stringent GDPR Enforcement and Escalating Compliance Costs:

The stringent application of the General Data Protection Regulation in terms of high financial fines and reputational losses provides an immediate need to use privacy management software that would allow organizing compliance with basic regulations in case of the complex regulatory environment. In 2024, European data protection regulators fined USD 4.8 billion (up from USD 2.9 billion in 2023) under the GDPR, and the average size of these fines is also growing (from USD 3.2 million to USD 5.8 million) due to the readiness by regulators to issue maximum fines of 4% of global annual turnover agAInst serious offenders. High profile enforcement actions in 2024 were a USD 1.2 billion fine on Meta Ireland due to cross-border data transfers, USD 405 million on Amazon Luxembourg due to behavioral advertisements, and USD 345 million on TikTok Ireland due to children’s privacy violations, indicating that no organization is too small to escape enforcement. Submission of notifications of data breaches to supervisory authorities increased by 18% in 2024 to 142,000, and organizations are experiencing pressure to operate under 72-hour notification rules and automated breach detection and reporting options exert operational pressure on organizations.

The cost of compliance goes beyond fines which include legal expenses amounting to USD 2.8 million on average per investigation, remediation costs amounting to USD 4.2-8.6 million on major violations and loss of customers as 67% of the European consumers report that they would cease doing business with companies that have had major privacy violations. The privacy management software achieves a lighter compliance burden (discovering the existence of personal data within the systems), provides consent management (340 million consumer preferences), offers automated Data Subject Access Request workflows (handling requests within the required 30-day limit), and provides audit trAIls (documenting compliance actions). Companies that have implemented a holistic privacy management solution state 60-75% of manual compliance processes are reduced, 85% of response time on DSAR is shortened from 22 days to 3.3 days, and 45% of the risk of a regulatory fine is due to systematic controls deterring violations.

- Evolving Regulatory Landscape Beyond GDPR:

Multiple sector-specific and national privacy laws extend beyond those of Europe, posing complicated compliance needs that demand adaptable privacy control systems that can satisfy several rules and regulations at the same time. The post-Brexit UK Data Protection Act 2018 provides an autonomous regime that diverges from the EU GDPR across a variety of areas, such as international transfers and the introduction of dual compliance requirements on organizations with operations in both the EU and UK with an estimated 18000 companies impacted.

The Federal Data Protection Act (BDSG) of Germany has further requirements than GDPR such as a data protection officer in the organization with 20 or more employees systematically processing personal data as opposed to the 250 employees requirement in the GDPR, which impacts 142,000 more German companies. The Data Protection Act of France adheres to the GDPR through some particular provisions of the employee data, health data, and biometric authentication that demand a higher level of security and impact analysis.

The ePrivacy Regulation, which is likely to become effective in 2025-2026, creates stringent regulations on electronic communications, cookies, and metadata processing, and the consent management systems are to be developed further than the existing GDPR cookie banners to include emAIl marketing, messaging applications, and communications with the IoT devices. Specific regulations of the industry, such as the NIS2 Directive on critical infrastructure that covers 160,000 entities, the Digital Operational Resilience Act (DORA) on financial services with 22,000 entities, and the EU AI Act establishing privacy requirements in high-risk artificial intelligence systems, are also creating the need to implement specific compliance modules. Such complexity in compliance provides market opportunity to unified privacy management systems that help mAIntAIn various regulations with configurable policy engines, jurisdiction-specific templates, and automatic regulatory change management updating systems as the needs change.

- Digital Transformation and Data Ecosystem Expansion:

The speeding up of digital business models, cloud adoption, and data ecosystems of interconnecting data increases the volume of personal data and the complexity of the data processing exponentially, requiring a solution to privacy management that is no longer based on spreadsheet tools. The mean is 2.4 petabytes of data per company in European organizations in 2024, and personal data represents an estimated percentage of 35-48 of the total data that must be controlled by GDPR controls. By 2024 cloud adoption had reached 78% of European businesses with multi-cloud architectures having an average of 3.8 cloud providers per organization that generates data distribution between AWS, Microsoft Azure, Google Cloud and local providers such as OVHcloud and Deutsche Telekom and privacy management needs visibility and control over fragmented infrastructure.

The average number of applications used by enterprises is 254, and 68% of them involve personal information, such as CRM systems, human resource platforms, marketing automation, and collaboration tools, and should be managed as a single privacy policy throughout the entire technology stack. 85% of European businesses are subject to cross-border data flows, and Standard Contractual Clauses are necessary in 148 million data transfers to third countries such as the United States, India and Southeast Asia, which causes an administrative burden in handling the impact assessment of transfers and documentation.

The Internet of Things creates 28.5 billion connected devices within Europe that gather personal information via smart homes, wearables, connected cars, and industrial sensors, which are managed by privacy management systems to expand their reach to the IoT device inventories, consent management at the device level, and data reduction automated policies. Technology stacks used in marketing of 12-35 tools per organization handle behavioral information, preferences, and customer paths that need consent co-ordination, preference centers, and cookie management that are integrated across digital experiences such as websites, mobile applications, and connected TVs.

- Consumer Privacy Awareness and Rights Exercise:

Greater consumer sensitivity to the issue of privacy rights and easy access to privacy rights enforcement mechanisms puts pressure on the operations of an organization that needs to have highly efficient workflows facilitated by privacy management automation. According to consumer surveys, in 2024, 82 out of 100 Europeans are aware of GDPR rights, and these awareness levels have risen to 56 out of 100 in 2019 and 64 out of 100 in 2024, with 64 out of 100 reporting that they have exercised at least one of the data protection rights of access, deletion, portability, or objection. In 2024, Data Subject Access Requests in Europe increased by 42% to 18.4 million requests, with an average cost of USD 1,200-2,400 to process the manual workflow compared to an automated platform (USD 180-340).

The mean large business gets 2800-4500 DSARs per year with the highest amount of 800-1200 in a month during awareness of privacy campAIgns or after data breaches, which need dedicated teams comprising 8-15 full-time workers compared to 2-3 with extensive privacy management programs. Consumer preference centers that allow granular consent management have 340 million unique user interactions monthly in Europe and users change preferences an average of 3.2 times annually and they demand real time synchronization across marketing databases, analytics platforms, and CRM systems.

The right to be forgotten generates 4.2 million of the deletion requests per year, and companies are forced to find personal data in production databases, backup systems, analytics warehouses, and third-party processors and delete it in 30-7 days, which has reduced the time of completion, which used to take 18-28 days, down to 4-7 days, through automated deletion processes. Privacy-conscious consumers are increasingly seeking to use browser privacy control modes, 42% of European internet users have started using ad blockers, and privacy-oriented options such as DuckDuckGo search which has 28 million European dAIly users are putting pressure on transparent privacy policies and a strong customer consent model that keeps customers trusting the company and marketing successfully.

What are the Major Advances Changing the Europe Privacy Management Software Market Today?

- AI-Powered Data Discovery and Classification:

Intelligence-Powered Data Discovery and Classification: Artificial intelligence and machine learning algorithms standardize the process of discovery, classification, and mapping of personal data to complex technology environments to solve a basic compliance challenge: What data is where. Data discovery software The software scans structured databases, unstructured file systems, cloud storage, SaaS applications, and data lakes identifying personal data with 92-96% accuracy using pattern recognition, natural language processing and contextual analysis. It is a classification engine that is used to automatically label data points as name, emAIl, phone number, IP address, financial information, health data, and sensitive data such as race, religion and biometric data, with confidence scores and human review processes of unclear cases.

Organizations that apply AI-based discovery save 3-6 weeks on data mapping that would require 6-12 months on manual data mapping and initial inventory and continuous automated updates to recognize new data sources and processing activities. Major vendors such as OneTrust, BigID, and Collibra handle petabytes of environments that identify 250 million plus personal data elements with 15,000 plus data sources like databases, files, emAIls, and APIs. Machine learning models trAIned on 500,000+ labeled data samples identify personal data as business data with a precision of 94, and eliminate false positives that would need manual handling by keyword-based methods by 85%. Configured lineage tracking Auto-lineage data tracks data movement between collection and processing, data storage, data sharing with third parties, and data deletion to create visual maps of 50,000+ processing activities needed to support Records of Processing Activities (ROPA) and Privacy Impact Assessment mandatory by GDPR Article 30 and Article 35.

- Automated Consent and Preference Management Platforms:

The most advanced versions of consent management platforms orchestrate customer preferences across all marketing and analytics touchpoints and mAIntAIn their real-time synchronization and respect granular consent choices. Cloud-based consent platforms are used to handle 340 million unique user interactions each month across European websites, mobile applications, emAIl and Internet of Things devices to obtAIn consent, legitimate interest and opt-out preferences at milliseconds latency to guarantee immediate impact across the systems they are connected to. High-tech cookie consent systems go beyond simple non-compliance, auto-detection of all cookies and trackers on websites, automatic classification into strictly necessary, functional, analytics or marketing, and dynamic blocking of non-essential cookies until specified consent is recorded, with 98% effectiveness in cookie identification, which saves 40 hours of manual configuration time down to 2 hours per site.

Preference centers allow controlling down to multiple consent purposes, an average of 12-18 in each organization such as emAIl marketing, SMS, push notifications, personalized advertising, analytics, social media integration, and sharing of third party data, with mobile-optimized forms yielding 78 completion versus 43 completion of non-optimized forms. APIs on Integration synchronize consent status to 30-50 downstream systems in 500 milliseconds down to emAIl service providers (Salesforce marketing cloud, adobe analytics), analytics platforms (Google analytics 4, adobe analytics), advertising networks, and CRM systems, with a guarantee of consistency in preference enforcement across the technology stack. Consent lifecycle Management automates re-consent processes when the material privacy policy is updated, consent will expire after 12-24 months according to industry best practice and the update of regulatory requirements with automated emAIl campAIgns that achieve 64% re-consent rates lowering customer attrition rates in the database. Audit trAIls record consent collection time, type (web form, emAIl, or API), individual consent granted/denied, IP address, and user agent that generates evidentiary records of regulatory investigations, and blockchAIn-based immutable consent registries are now being designed to be used with high-assurance applications.

- Privacy-Enhancing Technologies Integration:

Advanced privacy enhancing technologies, such as differential privacy, homomorphic encryption, secure multi-party computation, and federated learning, can be integrated to allow the usefulness of data with reduced privacy risks associated with technical protection. Implementations of different types of privacy use mathematical noise to add privacy guarantees to datasets and analytics queries on a specific individual level but mAIntAIn statistical accuracy on aggregate insights, with examples of organizations deploying it, including ING bank analysing patterns of customer transactions with a formal privacy guarantee agAInst re-identifying an individual. K-anonymity, l-diversity, and t-closeness engines are used to convert datasets involving personal data into anonymized equivalents that can be used in analytics, research, and sharing with third parties without GDPR limitations, and the re-identification risk assessment scores produced by the engines are automatically scored and generalized to reach desired privacy levels.

Generation Generative adversarial networks generate synthetic data sets statistically close to real-world personal data and are used to trAIn AI models and develop analytics, industrial collaborators can work on their models without privacy concerns, and as of 2024, European healthcare and financial service organizations have generated 2.8 billion synthetic records as synthetic data. Federated learning techniques allow collaborative machine learning across organizational borders, without centralizing personal information, and applications in fraud detection consortia learning on 850 Million transactions across 42 European banks, and healthcare studies learning 12 Million patient records across 180 hospitals to get clinical understanding.

Homomorphic encryption allows an encrypted dataset to be computed without being decrypted, providing cloud-based analytics and AI processing without decryption and end-to-end encryption, and has been implemented in financial services to evaluate risk scores based on 240 million encrypted transactions and compliance monitoring. Privacy management platforms are using these technologies to provide wizard-based configuration where privacy teams with minimal technical understanding can use these features to create sophisticated and complex controls, and there are defined templates that can be used for common scenarios, such as analytics anonymization, testing data generation, and secure collaboration.

Category Wise Insights

By Component

Why Software Dominates the Market?

Software components are predicted to dominate the market at 64% in 2025 as a result of the repeatability of subscription income, ongoing feature upgrade necessities and implementation of multiple modules. Mean cost of enterprise privacy management software deployment is USD 180,000-450,000/Year subscription expenses for 5,000-15,000 employees with modules costing separately USD 45,000-85,000 (data discovery), USD 38,000-72,000 (consent management), USD 28,000-54,000 (DSAR automation), and USD 22,000-46,000 (privacy SaaS platforms are predominantly in the cloud (76% deployment vs. on-premises) due to faster implementation (6-12 weeks deployment vs. 4-8 months deployment), automatic updates to stay regulatory-compliant and scalability to manage data volume (average deployment 2.4 petabytes, projected 8.6 petabytes in 2030). Implementation, customization, trAIning, and ongoing advisory of software implementations (36% of market); typical costs of implementation projects are USD 120,000-380,000 to implement privacy software packages, USD 120,000-380,000 to customize privacy software, USD 120,000-380,000 to trAIn privacy staff, and USD 120,000-380,000 to mAIntAIn privacy staff on advisory services.

By Deployment Mode

Why Cloud-Based Shows Fastest Growth?

Cloud-based deployment shows the highest CAGR of 16.2% between 2026-2035 due to lower total cost of ownership by 85% compared to on-premises including USD 180,000-450,000 annual subscription compared to USD 680,000-1.2 million perpetual license plus 18-22% annual mAIntenance, shorter deployment time by 6-12 weeks compared to on-premises deployment which needs 4-8 months, and the ability to provide SaaS designs Multi-tenant SaaS designs offer elastic scalability to deal with data discovery in petabyte-scale environments and consent management to process 5-15 million interactions monthly in the absence of infrastructure investment. Integrating marketplaces with ready-to-use connectors to 200 + enterprise apps such as Salesforce, SAP, Microsoft 365, AWS and Google cloud save up to 60-75% of integration costs compared to in-house development. The need for the European data residency further encourages the use of regional cloud providers such as OVHcloud, Deutsche Telekom and Orange business services that provides GDPR compliant infrastructure, with 68% of organizations that need EU data residency hosted on European cloud providers.

By Industry Vertical

Why BFSI Leads Market Share?

Financial Services, Banking and Insurance industry has a 32% market share that is determined by harsh regulation requirements such as GDPR, PSD2, AML5 and DORA with the 22,000 financial institutions; a high level of sensitive personal data with 8.4 million records per bank and extreme reputational risk following a breach of privacy with customer churn rates at 73%. All transactions in Europe of 2.8 billion dAIly between financial institutions with payment data, credit scores, account balances and behavioral analytics demand full privacy protection.

The average European bank is spending USD 2.4-4.8 million on privacy control software to support 5,000-12,000 databases and applications to find the data, consent control to support 4-12 million customers, and DSAR to process requests of 15,000-42,000 requests per year. The PSD2 obligation of open banking mandates consent management of 180 million European bank individuals who grant third parties access to their financial data, and API-based consent platforms handle 420 million authentication requests every month. Health and medical data Insurance firms that operate with health data, behavior, and clAIms history have the increased attention of GDPR, leveraging privacy impact assessment modules to scan 200-400 processing activities a year.

Report Scope

| Feature of the Report | DetAIls |

| Market Size in 2026 | USD 3.28 billion |

| Projected Market Size in 2035 | USD 9.42 billion |

| Market Size in 2025 | USD 2.84 billion |

| CAGR Growth Rate | 15.4% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Component, Deployment Mode, Organization Size, Industry Vertical, Functionality and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | Europe |

| Buying Options | Request tAIlored purchasing options to fulfil your requirements for research. |

Country Wise Analysis

United Kingdom Market Leadership

The United Kingdom has the largest market share of 28% with USD 795 million in 2025 due to the post-Brexit UK GDPR generating dual compliance obligations on 18,000 companies operating in the EU and the UK (compared to 68% in the EU), high enforcement rates through issuing USD 840 million in fines by the Information Commissioner Office in 2024, and high technology adoption rates with 84% of British enterprises using privacy management software compared to 68% in the EU. The financial services sector in London with 420 institutions is highly demanding, the annual spending of the UK BFSI privacy software is USD 285 million. The UK market has 145 privacy software sellers such as domestic (TrustArc, DataGrAIl) and international (establishing operations in the UK) vendors. The USD 22 million fine pAId by British Airways in 2020, the collective USD 142 million in fines given to British Airways and Marriott International and the continuing regulatory review make executives more aware of privacy management and allocate budget to it, with an average enterprise spending of USD 380,000 in the UK versus USD 280,000 in the EU.

Germany Market Growth

Germany estimates USD 680 million in 2025 are recorded highest growth of 16.8% CAGR due to the presence of a strict culture on data protection, BDSG which imposes requirements not only on GDPR, but also on the existence of strong manufacturing and automotive industries dealing with IoT and connected vehicle data. German companies have an average of 3.8 petabytes of data, 45% of which is personal data that needs to be discovered and categorized, and this accounts for the USD 245M/year spent on data mapping software.

The 28.5 million connected vehicles in the automotive sector that yield 2.4 exabytes worth of location, driving behavior, and diagnostic information every year need location-specific privacy management platforms that facilitate the deletion of vehicle data, consent capture by infotAInment systems, and cross-border transfers. The German focus on privacy-by-design makes Privacy Impact Assessment module adoption 76% of the organization compared to the 58% European average. Significant implementations surround the USD 12.8 million privacy management system deployed by Deutsche Bank in support of 90,000 employees in 58 countries and the internal implementation of employee data by SAP in support of 108,000 employees around the world.

France Market Dynamics

The USD 512 million worth in 2025 of France marrying the benefits of CNIL that actively issues USD 680 million in fines in 2024 and USD 90 million agAInst Google and USD 60 million agAInst Amazon; a robust retAIl and e-commerce industry that has to control 72 million online shoppers, and government projects in digital transformation that must meet privacy requirements. French organizations are awarded 2.8 million DSARs per year, the second highest in Europe after the UK, which spurs the adoption of the automation platform with 72% of enterprises adopting the DSAR modules. The 67 million patient records in the healthcare sector need a higher level of protection as per the French Data Protection Act, with the market size of USD 85 million in health data privacy software being fuelled by hospitals, clinics and pharmaceutical firms. The French firms also show a high interest in European software providers in 64% of the market areas as compared to US vendors in 36% market share since data sovereignty is a major concern and the government procurement preference is towards EU vendors.

Nordics and Benelux Markets

Higher rates of 82, 78, and 76, respectively, through digitally developed economies, good privacy culture, and active regulation strategy are found in Sweden, the Netherlands, and Denmark, respectively. The market of USD 385 million of the Netherlands enjoys the position of Amsterdam as the European hub of data centers with 200+ facilities demanding privacy compliance, the financial service industry with ING Bank and ABN AMRO implementing extensive platforms, and effective implementation by the Dutch DPA issuing USD 245 million in fines in 2024. Swedish market of USD 285 million via GDPR gold-plating by national legislation, telecommunications industry comprising Ericsson and Telia to handle subscriber data, and healthcare digitalization with 95% electronic health records. The 198 million USD market was highly adopted by Danish SMEs, 68% compared to 42% on average in Europe due to simplified requirements to comply with smaller companies and the avAIlability of the SaaS platforms.

Top Players in the Market and Their Offerings

- OneTrust

- BigID

- TrustArc

- Securiti AI

- Collibra

- Informatica

- SAP

- Microsoft (Priva)

- IBM

- WireWheel

- DataGrAIl

- Cookiebot (Cybot)

- Others

Key Developments

- In April 2025: The European Commission is proposing to amend the ePrivacy Regulation, according to which the requirements of the cookie consent become strict. Such developments are pushing consent-management upgrades, with vendors like Cookiebot and OneTrust launching new compliance modules.

- In March 2025: To grow its market in Europe, BigID issued a USD 180M Series E equity rAIse with a total of 3 European firms, such as Eurazeo and Insight Partners. It will open new offices in Frankfurt, Amsterdam, and Stockholm to help it achieve its projected 45 percent growth rate per year.

- In April 2025: When the CNIL of France and the ICO of the UK collaborated on guidance on the effect of AI privacy impact assessment, they stimulated the need of specific PIA modules. TrustArc and WireWheel are some of the vendors that responded with measures towards compliance with the EU AI Act.

These strategic initiatives have enabled the companies to consolidate market positions, increase the geographic presence, increase control capabilities in regulatory aspects, and exploit growth opportunities in the changing market of Europe privacy management software.

The Europe Privacy Management Software Market is segmented as follows:

By Component

- Software

- Data Discovery & Mapping

- Consent Management

- DSAR Automation

- Privacy Impact Assessment

- Vendor Risk Management

- Services

- Professional Services

- Managed Services

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By Organization Size

- Large Enterprises

- Small & Medium Enterprises

By Industry Vertical

- BFSI (Banking, Financial Services, Insurance)

- Healthcare & Life Sciences

- RetAIl & E-commerce

- IT & Telecommunications

- Government & Public Sector

- Manufacturing

- Media & EntertAInment

- Others

By Functionality

- Data Mapping & Discovery

- Consent Management

- Data Subject Access Requests (DSAR)

- Privacy Impact Assessment (PIA)

- Vendor & Third-Party Risk Management

- Cookie & Tracker Management

- Breach Response Management

- Privacy TrAIning & Awareness

Regional Coverage:

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- SpAIn

- Netherlands

- Rest of Europe

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Europe Privacy Management Software by Segments

- 2.1.2. Europe Privacy Management Software by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Europe Privacy Management Software Market Attractiveness Analysis, By Component

- 2.2.3. Europe Privacy Management Software Market Attractiveness Analysis, By Deployment Mode

- 2.2.4. Europe Privacy Management Software Market Attractiveness Analysis, By Organization Size

- 2.2.5. Europe Privacy Management Software Market Attractiveness Analysis, By Industry Vertical

- 2.2.6. Europe Privacy Management Software Market Attractiveness Analysis, By Functionality

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Stringent GDPR Enforcement and Escalating Compliance Costs

- 3.1.2. Evolving Regulatory Landscape Beyond GDPR

- 3.2. Market RestrAInts

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value ChAIn Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Europe Privacy Management Software Market – By Component

- 4.1. Component Market Overview, By Component Segment

- 4.1.1. Europe Privacy Management Software Market Revenue Share, By Component, 2025 & 2035

- 4.1.2. Software

- 4.1.2.1. Data Discovery & Mapping

- 4.1.2.2. Consent Management

- 4.1.2.3. DSAR Automation

- 4.1.2.4. Privacy Impact Assessment

- 4.1.2.5. Vendor Risk Management

- 4.1.3. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Services

- 4.1.6.1. Professional Services

- 4.1.6.2. Managed Services

- 4.1.7. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Component Market Overview, By Component Segment

- Chapter 5. Europe Privacy Management Software Market – By Deployment Mode

- 5.1. Deployment Mode Market Overview, By Deployment Mode Segment

- 5.1.1. Europe Privacy Management Software Market Revenue Share, By Deployment Mode, 2025 & 2035

- 5.1.2. Cloud-Based

- 5.1.3. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. On-Premises

- 5.1.7. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Hybrid

- 5.1.11. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Deployment Mode Market Overview, By Deployment Mode Segment

- Chapter 6. Europe Privacy Management Software Market – By Organization Size

- 6.1. Organization Size Market Overview, By Organization Size Segment

- 6.1.1. Europe Privacy Management Software Market Revenue Share, By Organization Size, 2025 & 2035

- 6.1.2. Large Enterprises

- 6.1.3. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Small & Medium Enterprises

- 6.1.7. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Organization Size Market Overview, By Organization Size Segment

- Chapter 7. Europe Privacy Management Software Market – By Industry Vertical

- 7.1. Industry Vertical Market Overview, By Industry Vertical Segment

- 7.1.1. Europe Privacy Management Software Market Revenue Share, By Industry Vertical, 2025 & 2035

- 7.1.2. BFSI (Banking, Financial Services, Insurance)

- 7.1.3. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Healthcare & Life Sciences

- 7.1.7. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. RetAIl & E-commerce

- 7.1.11. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. IT & Telecommunications

- 7.1.15. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Government & Public Sector

- 7.1.19. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Manufacturing

- 7.1.23. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1.26. Media & EntertAInment

- 7.1.27. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 7.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.29. Key Market Trends, Growth Factors, & Opportunities

- 7.1.30. Others

- 7.1.31. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 7.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.33. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Industry Vertical Market Overview, By Industry Vertical Segment

- Chapter 8. Europe Privacy Management Software Market – By Functionality

- 8.1. Functionality Market Overview, By Functionality Segment

- 8.1.1. Europe Privacy Management Software Market Revenue Share, By Functionality, 2025 & 2035

- 8.1.2. Data Mapping & Discovery

- 8.1.3. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 8.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.5. Key Market Trends, Growth Factors, & Opportunities

- 8.1.6. Consent Management

- 8.1.7. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 8.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.9. Key Market Trends, Growth Factors, & Opportunities

- 8.1.10. Data Subject Access Requests (DSAR)

- 8.1.11. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 8.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.13. Key Market Trends, Growth Factors, & Opportunities

- 8.1.14. Privacy Impact Assessment (PIA)

- 8.1.15. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 8.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.17. Key Market Trends, Growth Factors, & Opportunities

- 8.1.18. Vendor & Third-Party Risk Management

- 8.1.19. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 8.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.21. Key Market Trends, Growth Factors, & Opportunities

- 8.1.22. Cookie & Tracker Management

- 8.1.23. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 8.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.25. Key Market Trends, Growth Factors, & Opportunities

- 8.1.26. Breach Response Management

- 8.1.27. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 8.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.29. Key Market Trends, Growth Factors, & Opportunities

- 8.1.30. Privacy TrAIning & Awareness

- 8.1.31. Europe Privacy Management Software Share Forecast, By Region (USD Billion)

- 8.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.33. Key Market Trends, Growth Factors, & Opportunities

- 8.1. Functionality Market Overview, By Functionality Segment

- Chapter 9. Europe Privacy Management Software Market – Regional Analysis

- 9.1. Europe Privacy Management Software Market Overview, By Region Segment

- 9.1.1. Global Europe Privacy Management Software Market Revenue Share, By Region, 2025 & 2035

- 9.1.2. Global Europe Privacy Management Software Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 9.1.3. Global Europe Privacy Management Software Market Revenue, By Component, 2026 – 2035

- 9.1.4. Global Europe Privacy Management Software Market Revenue, By Deployment Mode, 2026 – 2035

- 9.1.5. Global Europe Privacy Management Software Market Revenue, By Organization Size, 2026 – 2035

- 9.1.6. Global Europe Privacy Management Software Market Revenue, By Industry Vertical, 2026 – 2035

- 9.1.7. Global Europe Privacy Management Software Market Revenue, By Functionality, 2026 – 2035

- 9.2. Europe

- 9.2.1. Europe Europe Privacy Management Software Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.2.2. Europe Europe Privacy Management Software Market Revenue, By Component, 2026 – 2035

- 9.2.3. Europe Europe Privacy Management Software Market Revenue, By Deployment Mode, 2026 – 2035

- 9.2.4. Europe Europe Privacy Management Software Market Revenue, By Organization Size, 2026 – 2035

- 9.2.5. Europe Europe Privacy Management Software Market Revenue, By Industry Vertical, 2026 – 2035

- 9.2.6. Europe Europe Privacy Management Software Market Revenue, By Functionality, 2026 – 2035

- 9.2.7. Germany Europe Privacy Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.8. France Europe Privacy Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.9. U.K. Europe Privacy Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.10. Russia Europe Privacy Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.11. Italy Europe Privacy Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.12. SpAIn Europe Privacy Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.13. Netherlands Europe Privacy Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.14. Rest of Europe Europe Privacy Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 9.1. Europe Privacy Management Software Market Overview, By Region Segment

- Chapter 10. Competitive Landscape

- 10.1. Company Market Share Analysis – 2025

- 10.1.1. Global Europe Privacy Management Software Market: Company Market Share, 2025

- 10.2. Global Europe Privacy Management Software Market Company Market Share, 2024

- 10.1. Company Market Share Analysis – 2025

- Chapter 11. Company Profiles

- 11.1. OneTrust

- 11.1.1. Company Overview

- 11.1.2. Key Executives

- 11.1.3. Product Portfolio

- 11.1.4. Financial Overview

- 11.1.5. Operating Business Segments

- 11.1.6. Business Performance

- 11.1.7. Recent Developments

- 11.2. BigID

- 11.3. TrustArc

- 11.4. Securiti AI

- 11.5. Collibra

- 11.6. Informatica

- 11.7. SAP

- 11.8. Microsoft (Priva)

- 11.9. IBM

- 11.10. WireWheel

- 11.11. DataGrAIl

- 11.12. Cookiebot (Cybot)

- 11.13. Others.

- 11.1. OneTrust

- Chapter 12. Research Methodology

- 12.1. Research Methodology

- 12.2. Secondary Research

- 12.3. Primary Research

- 12.3.1. Analyst Tools and Models

- 12.4. Research Limitations

- 12.5. Assumptions

- 12.6. Insights From Primary Respondents

- 12.7. Why Custom Market Insights

- Chapter 13. Standard Report Commercials & Add-Ons

- 13.1. Customization Options

- 13.2. Subscription Module For Market Research Reports

- 13.3. Client Testimonials

List Of Figure

Figures No 1 to 46

List Of Tables

Tables No 1 to 15

Prominent Player

- OneTrust

- BigID

- TrustArc

- Securiti AI

- Collibra

- Informatica

- SAP

- Microsoft (Priva)

- IBM

- WireWheel

- DataGrAIl

- Cookiebot (Cybot)

- Others

FAQs

The key players in the market are OneTrust, BigID, TrustArc, Securiti ai, Collibra, Informatica, SAP, Microsoft (Priva), IBM, WireWheel, DataGrail, Cookiebot (Cybot), Others.

Regulations essentially propel the market by GDPR with the establishment of a comprehensive privacy framework with a 4% global revenue fine on breaches, the ePrivacy Regulation requiring consent management on electronic communications, the NIS2 Directive with a cybersecurity and privacy mandate on 160,000 critical infrastructure entities, DORA with operational resilience for 22,000 financial institutions, and the EU AI Act with privacy impact assessment obligations on high-risk AI systems with enforcement penalty measures imposing a USD 1.2 billion Meta fine and a USD 405 million Amazon penalty, reflecting credibility.

The market is estimated to reach approximately USD 9.42 billion by 2035, growing at a 15.4% CAGR from 2026-2035, driven by expanding regulatory scope through ePrivacy, the AI Act, and sector-specific laws; data volume growth from 2.4 to 8.6 petabytes on average, requiring automated management, increasing consumer privacy awareness, with 82% GDPR rights awareness, and technology evolution integrating AI-powered discovery, automated workflows, and privacy-enhancing technologies.

The United Kingdom is the leader with a 28% share worth USD 795 million by 2025 due to the dual compliance between the UK GDPR and the EU GDPR due to 18,000 cross-border companies, enforcement by the Information Commissioner’s Office that issued USD 840 million in fines in 2024, Financial service sector of London with 420 institutions that need sophisticated privacy controls, and an uptake rate of 84% in the enterprise that is more than the EU average of 68%.

Germany has the highest growth rate of 16.8% CAGR between 2026-2035, led by BDSG governing stricter requirements than GDPR on 142,000 more companies, powerful manufacturing and automotive sectors operating 28.5 million connected vehicles that generate 2.4 exabytes of IoT data, BDSG culture of data protection that places premium on privacy-by-design, and strong enforcement of federal and state data protection controls to drive adoption of software to 76% of large companies.

The Europe Privacy Management Software Market is growing due to GDPR penalties of USD 4.8 billion in fines in 2024 generating compliance urgency, 142,000 notifications of data breaches annually mandating 72-hour reporting automation, 18.4 million annual DSARs necessitating efficient processing, shifting regulations of ePrivacy, NIS2, DORA, and the AI Act imposing complex compliance demands, and digital transformation of 2.4 petabytes per organization on average that needs automated data discovery and classification to replace manual practices.