Fresh Seafood Packaging Market Size, Trends and Insights By Material Type (Plastic (Polyethylene, Polypropylene, PET, PVC, EPS), Paper & Paperboard, Modified Atmosphere Packaging (MAP) Films & Laminates, Biodegradable & Sustainable Materials (Molded Fiber, PHA, PLA, Seaweed-Based), Aluminum & Metallic Films, Other Materials), By Packaging Type (Trays & Clamshells, Bags & Pouches (Vacuum Bags, Zip-Lock, Stand-Up Pouches), Wraps & Films (Stretch Wrap, Shrink Film, Overwrap), Boxes & Cartons (Wax-Coated, Corrugated, Insulated), Nets & Mesh Bags (Primarily Shellfish), Other Packaging Types), By Application (Fish (Salmon, Tuna, Cod, Tilapia, and Other Finfish), Crustaceans (Shrimp, Crab, Lobster, Crayfish), Mollusks & Shellfish (Oysters, Clams, Mussels, Scallops), Cephalopods (Squid, Octopus, Cuttlefish), Other Seafood), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Fish Retailers & Fish Markets, Online Retail & Direct-to-Consumer, Food Service (Restaurants, Hotels, Catering), Other Channels), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- Sealed Air Corporation

- Amcor plc

- Berry Global Group Inc.

- Huhtamaki Oyj

- Others

Reports Description

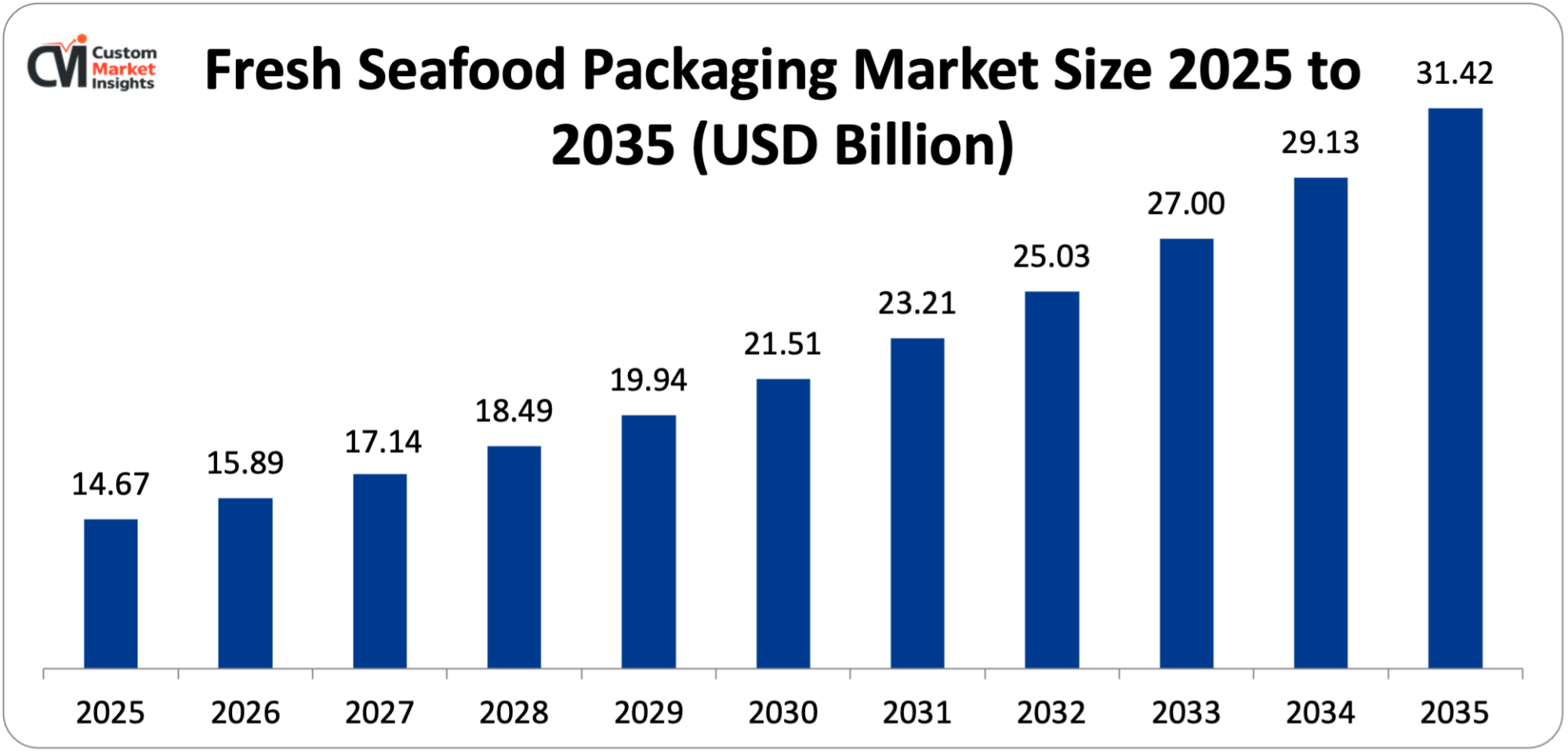

The fresh seafood packaging market is estimated at USD 14.67 billion in the year 2025 and is expected to grow at the rate of 7.9% between 2026 and 2035 to USD 15.89 billion to USD 31.42 billion respectively. The increasing demand for fresh and minimally processed seafood products in the world due to the increasing health consciousness, the accelerating demand of the extended shelf-life packaging solution systems, which reduce the amount of waste in the seafood supply chain; the rapid growth of aquaculture production to supplement the wild-catch fisheries, the strong and consistent demand of the market with high food safety standards requiring improved packaging hygiene and traceability specifications and the joint pressure exerted by retailers and consumers on packaging materials that are sustainable are all forces driving the vigorous and continuous growth of the market during the forecast period.

Market Highlight

- Asia Pacific was a top contender of fresh seafood packaging with a market share of 43% in 2025.

- North America will grow at 7.2% CAGR between 2026 and 2035.

- By material category, the plastic segment will take a market share of around 41% in 2025.

- By type of material, the biodegradable and sustainable materials segment is expected to experience the fastest CAGR of 12.8% between the years 2026 and 2035.

- By type of packaging, the trays and clamshells segment generated the largest market share of 36% in 2025, and the bags and pouches segment had the greatest CAGR of 9.4% over the estimated horizon of 2026-35.

- Application showed that the fish segment had the largest market share of 52% in the year 2025, and the crustacean’s segment is projected to have the highest CAGR of 8.7% in the years 2026 to 2035.

- By distribution channel, the segment of the supermarkets and hypermarkets had a market share of 48% in 2025.

Significant Growth Factors

The Fresh Seafood Packaging Market Trends present significant growth opportunities due to several factors:

- Rising Global Seafood Consumption and Health-Driven Dietary Shifts:

The structural driver of the emerging demand of new seafood packaging is the accelerated global transition to protein-rich, heart-healthy, and nutritionally fortified diets – the central and growing role of seafood in which seafood consumption demands packaging infrastructure to ensure safe handling, preservation, transportation, retail display, and delivery to the consumer. In 2023, the Food and Agriculture Organization of the United Nations (FAO) reported an all-time high of 162 million metric tons of fish consumed globally, and per capita fish consumption had risen from 9.9 kg per year in the 1960s to about 20.7 kg per year in 2023, a more than doubling of that consumption, which reflects the fundamental shift of seafood in food consumption, of a regional food product into a worldwide mainstream category of protein.

A suggestion of two to more servings of seafood per week by the American Heart Association, citing omega-3 fatty acid content and cardiovascular health benefits, plus similar dietary advice by health authorities in the EU, Japan, Australia, and China is generating significant growth in the frequency of fresh seafood purchases among the health-conscious consumer groups, willing to pay premium prices, on the promise of freshness and well-packaged products. The global market of healthy food was estimated to be USD 1.07 trillion in 2024 and is estimated to grow at an 8.1% CAGR to USD 1.71 trillion by 2030 with fresh seafood being one of the fastest growing protein products in the greater health food trend. Fresh and chilled seafood, which is the most packaging-intensive in terms of temperature control, modified atmosphere protection, and retail presentation appeal, is taking market share in the overall seafood consumption at the expense of canned and frozen products, as consumers are moving towards seafood of minimal packaging and restaurant quality to prepare at home. The aquaculture sector, which today supplies about 57% of the world’s seafood by volume, an increase over about 26% in 2000, is growing rapidly to satisfy this increasing demand, according to the Global Aquaculture Alliance, and, by 2030, aquaculture production will be 109 million metric tons, creating massive incremental demand on farm-to-retail packaging solutions in the fish, shrimp, shellfish, and emerging aquaculture species categories.

- Food Safety Imperatives and Shelf-Life Extension Technology Driving Packaging Innovation:

The well-documented food safety problems that plague the seafood industry, as the most frequently recalled food category in the United States, according to the FDA, and involved in a significant percentage of foodborne illness outbreaks worldwide, are generating strong regulatory and business will to invest in packaging technologies to increase safe shelf life, the preservation of cold chain integrity, tamper evidence, and rapid traceability in case of food contamination events. The world seafood sector has its share of estimated annual losses of about USD 35 billion due to spoilage and wastage according to the World Resources Institute, and improper packaging has been found to be the major contributor to the premature worsening of quality throughout the supply chain.

The most common premium packaging technology in the retail sector to fresh fish and shellfish is modified atmosphere packaging (MAP), where the normally present air around the product in a package is replaced by an accurately calculated combination of gases such as carbon dioxide, nitrogen and oxygen that prevent bacterial growth and oxidation and extends the shelf life of the product previously available as 3-5 days in standard over wrap packages to 10-18 days without negatively affecting any sensory quality indicators, such as color, texture, aroma and moisture, that are also important factors in consumer purchasing decisions. With packaging industry review, the retail prices of MAP-packed fresh seafood are 15-25% higher than those of traditional packaged counterparts in European and North American markets, as a result of consumers, who showed their readiness to pay more in order to guarantee freshness and convenience of reduced waste.

Several regulations on food packaging labels such as the Food Information to Consumers Regulation of the EU and the Food Safety Modernization Act (FSMA) of the U.S. FDA (Seafood Hazard Analysis and Critical Control Points, or HACCP) regulations also require stricter labeling on seafood packaging such as catch date, species verification, geographic origin, and allergen information, which has encouraged investment in advanced printing, labeling and digital traceability integration into seafood packaging systems. An additional layer of packaging labeling and documenting requirements on sustainable wild-catch seafood offered by the USDA National Organic Program extension of aquaculture and the Marine Stewardship Council (MSC) chain-of-custody certification raises the packaging labeling and documentation requirements that advanced packaging solutions must handle.

What are the Major Advances Changing the Fresh Seafood Packaging Market Today?

- Sustainable and Bio-Based Packaging Material Innovation:

The seafood packaging market is experiencing a radical material shift due to the combination of regulatory action on single-use plastics, sustainability commitment of retailers, and the demand of consumers on environmentally responsible packaging materials that satisfy the high-performance demands of fresh seafood preservation. The conventional seafood packing has been based upon the use of expanded polystyrene (EPS) foam tray which offers excellent thermal insulation, shock absorption and moisture protection, but is prohibited or severely limited in more than 100 jurisdictions worldwide including the EU, Canada and several U.S. states, presenting a dire need to find materials with functional substitutes.

The most commercially developed EPS alternative in fresh seafood retail packaging is molded fiber and formed pulp trays, which are made of recycled paper, sugarcane bagasse, bamboo fiber or wheat straw and made water-resistant, grease-resistant, and microwavable in most cases provide competitive cost and thermal and protective capabilities that are equivalent to EPS. Huhtamaki, Pactiv Evergreen, and UFP Technologies are companies that manufacture EPS competitive cost, thermal and protective capabilities, and competitive cost water-resistant, grease-resistant, and mic One of the most new emerging categories of sustainable material particularly in seafood packaging is seaweed-based packaging films, with companies such as Notpla, Loliware, and Evoware developing edible and home-compostable packaging films made of agar, carrageenan and alginate made out of abundant marine biomass – creating a thematically resonant relationship between the product and the material of the seafood packaging.

In 2024 the global sustainable seafood packaging market segment is estimated to have reached USD 2.8 billion and is set to increase at a 13.4% CAGR through 2032, much faster than the overall growth rate of seafood packaging market as regulatory and commercial sustainability requirements drive material change. Polyhydroxyalkanoates (PHA) – fully biodegradable and marine-biodegradable biopolymers made by microbial fermentation – are in development as commercially viable packaging films and coatings in the seafood industry (with Danimer Scientific, TotalEnergies Corbion, and CJ Biomaterials currently operating commercial PHA production plants and prioritizing seafood packaging as a new application) due to its connection to the marine environment and the PR appeal of packaging that promises no harm in the ocean environment because of its biodegradation.

- Cold Chain Integration and Temperature-Controlled Packaging Systems:

The development of temperature controlled packaging solutions such as phase change material (PCM) inserts, vacuum insulated panels (VIP), and aerogel based insulation embedded within the seafood packaging structure is allowing the fresh seafood distribution radius to be expanded and the commercial viability of direct-to-consumer online delivery of seafood to be made possible which is one of the most significant demand growth vectors of the premium packaging solutions. In 2024, the cold chain logistics market is worth USD 291 billion and is expected to grow at 10.5 CAGR to USD 647 billion by 2032 with seafood being the highest-valued and most temperature-sensitive perishable food to operate under the cold chain. Phase change materials, or those materials that absorb or release large amounts of latent heat as they change between solid and liquid phases at well determined temperatures, are being incorporated into seafood shipping boxes, retail display tray liners, and consumer delivery insulated bags to maintain selected temperature ranges of 0-18.4°C of fresh fish and frozen seafood over extended shipping periods without the need to maintain mechanical refrigeration.

PCM packaging concepts by such companies as Viking Cold Solutions, Cold Chain Technologies, and Gel Pak allow shipping fresh seafood at ambient temperature within 24-96 hours to maintain seafood quality temperatures, and this dramatically increases the size of the market addressable by high quality fresh seafood direct-to-consumer e-commerce. The online fresh seafood delivery market has seen an unprecedented growth in the COVID-19 pandemic and has retained and grown its consumer base, with global online seafood sales in USD 8.3 billion and expected to reach USD 21.7 billion in 2024 and 2030, respectively, with each online order needing a fully insulated shipping package solution, which is significantly more expensive than retail tray packaging. Next-generation ultra-slim packaging of seafood Vacuum insulated panels is making it possible, with a mechanism of thermal insulation performance 810 times better than conventional expanded polystyrene at the same thickness, which is enabling next-generation ultra-slim vacuum-insulated packaging that reduces the size of the package and minimizes the shipping cost without compromising thermal performance, including in high-end salmon, tuna, and live shellfish direct-to-consumer packaging designs where package aesthetics are significant to brand position.

- Digital Traceability and QR-Enabled Consumer Transparency Packaging:

Fresh seafood is packaged in digital traceability technologies, such as QR codes, NFC (Near-Field Communication) tags, RFID labels, and blockchain-linked data carriers to provide supply chain visibility never before seen, to satisfy regulatory requirements for seafood origin authentication and to meet an increasing consumer demand to confirm the sustainability-related credentials, catch or harvest methodology, and geographic provenance of the seafood they buy. Seafood fraud is an issue where less desirable species are labelled as premium species and estimates put it at about 20-40% of seafood sold at retail in the United States and Europe, according to the 2024 seafood fraud investigation by Oceana, which is both a failure in consumer protection and a market competition fairness issue for the legitimate producers of sustainable seafood that would be addressed by transparent packaging traceability.

QR code-based “boat-to-plate” traceability innovation (where every package of seafood has a scannable code that links to an online record of the fishing vessel, date and location of the fish, DNA verification of the species, processing plant, cold chain history, and sustainability certification) is being implemented by major seafood brands such as Bumble Bee Seafoods, Thai Union, and Mowi Salmon, with consumer scan rates of seafood QR codes increasing from about 4% in 2021 to 18% in 2024 as The most extensive regulatory requirement on digital seafood traceability in the world, the Fisheries Control Regulation of the European Commission, which will require the full digital identification of the lot and traceability of all seafood sold in the EU beginning in 2024, which mandates full digital representation of the chain of custody of all seafood sold in the EU, is the core driver of investment in the QR and integration of digital data carriers in seafood packaging in the EU market. In a 2024 survey of the global consumer market conducted by the IBM Institute for Business Value, 71% of consumers said they would pay an upcharge of up to 10% on food products whose provenance information was verified and could be accessed through packaging, with seafood having the highest premium willingness of any food category representing consumer anxieties about the authenticity and sustainability of species.

Category Wise Insights

By Material Type

Why Does Plastic Lead the Fresh Seafood Packaging Market?

Plastic materials will constitute the highest type of materials with a market share of about 41% in the year 2025. Such dominance indicates the unmatched functional performance of plastics as a fresh seafood packaging material: it has an excellent moisture barrier performance to prevent product dehydration and ensure that the weight of seafood remains intact; it has a transparent optical clarity in allowing a consumer to view the freshness and color of seafood products without opening the package; it is heat-sealable to provide hermetic closures critical to MAP and vacuum packaging; it can be formed into complex tray and clamshell shapes to fit a wide variety of seafood species and cut configurations; and it is cost-effective at the large volumes of production.

The most commonly used plastic materials in seafood overwrap and lidding film usage include polyethylene (PE), polypropylene (PP) materials are used to provide the structural rigidity needed in the display trays, and polyethylene terephthalate (PET) provides the best gas barrier and optical clarity needed in the premium MAP presentation. The Plastic Packaging Task Force estimates that seafood industry uses 2.8 million metric tons of plastic packaging each year, with the fresh seafood sector representing a disproportionately high percentage of the intensity of plastic packaging relative to product volume due to the many layers of packaging which are often necessary such as primary product tray, lidding film, secondary retail-ready box, and tertiary transport packaging. Although plastic still dominates the segment functionally, the regulatory constraints on single-use plastic package adoption across the EU, the UK, and Canada, and even more broadly, on the recyclability of packaging under the Packaging and Packaging Waste Regulation (PPWR) are posing substantial headwinds on the segment, with the EU Single-Use Plastics Directive provisions on expanded polystyrene food packages already implemented, and an even greater wave of recyclability demands on the industry under the Packaging and Packaging Waste Regulation (PPWR).

By Packaging Type

Why Do Trays & Clamshells Lead the Market?

The trays and the clam shells have the biggest%age of the total market share, 36% in 2025 of the packaging type since the latter are the most popular retail presentation of fresh fish fillets, portions, and ready-made seafood products in supermarket and specialty retail stores worldwide. This type of retail tray, in which a shaped tray of EPS, PP, or a shaped fiber is filled with fresh seafood, covered with stretch or shrink films, and placed in refrigerated open-deck retail cases has been the preferred seafood retail presentation format of choice over the decades, slowly extended to become the MAP-lidded tray formats, which provide both better shelf life and protection of the product and permit the display of fresh seafood in the retail shelves.

The global premium fresh seafood MAP tray market is represented by all three brands of Cryovac brand MAP tray systems of Sealed Air Corporation, modified atmosphere tray lidding films by Berry Global and FlexPrep tray systems by Amcor, all of which are utilized in large seafood processing and retailing businesses in North America, Europe, and Asia Pacific. The hinged, rigid, one-piece container with tamper-evident closure and 360-degree product visibility, called the clamshell design, is gaining market share in packaging crustaceans and shellfish packaging markets where presentation ease, and integrity of portions represent among the most influential purchase decision requirements. Retail analysis of the retail industry Retail price premiums between tray formats based on MAP-lidded compared to conventional stretch-wrapped formats of identical retail products in seafood are 12-18% at retail, and the long shelf life of 12-18 days provides the retailer with an estimated 23% reduction in retail shrink (waste of the unsold product due to expiry) that has a direct economic benefit to the retailer that offsets the higher packaging cost.

By Distribution Channel

Why Do Supermarkets & Hypermarkets Dominate?

In 2025, the region is estimated to control about 43% of the world market share, and Asia Pacific is simultaneously as the largest seafood producing and at the same time the largest seafood-consuming region on earth, with the FAO estimating that the Asia Pacific produces about 70% of world fish production and at the same time consumes about 70% of the total world fish consumption in volume. China alone generates an estimated 65 million metric tons of seafood every year – some 40% of the global generation – in terms of aquaculture, marine fish, and inland capture, creating a mammoth domestic packaging demand base at all levels of the supply chain at farm gate to processing, cold chain distribution, and retail.

A highly developed culture of fresh seafood retail and foodservice (with the highest per capita consumption rate of fresh fish in the world, estimated at about 50 kg per person per year, and a culture of high-value fresh seafood retail packaging based on aesthetic presentation and strict freshness requirements) makes Japan one of the most technologically advanced and highest-value fresh seafood packaging markets in the world. The fast growth in premium seafood retailing in South Korea, the exporting industries of Vietnam and Indonesia that require a large volume of packaging in order to have high-quality packaging that can meet the requirements of their export market, and the modernization of fresh seafood retailing in India through the organized retail sector in Tier 1 and Tier 2 cities are all contributing factors to the high position of Asia Pacific in the regional market.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 15.89 billion |

| Projected Market Size in 2035 | USD 31.42 billion |

| Market Size in 2025 | USD 14.67 billion |

| CAGR Growth Rate | 7.9% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Material Type, Packaging Type, Application, Distribution Channel and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

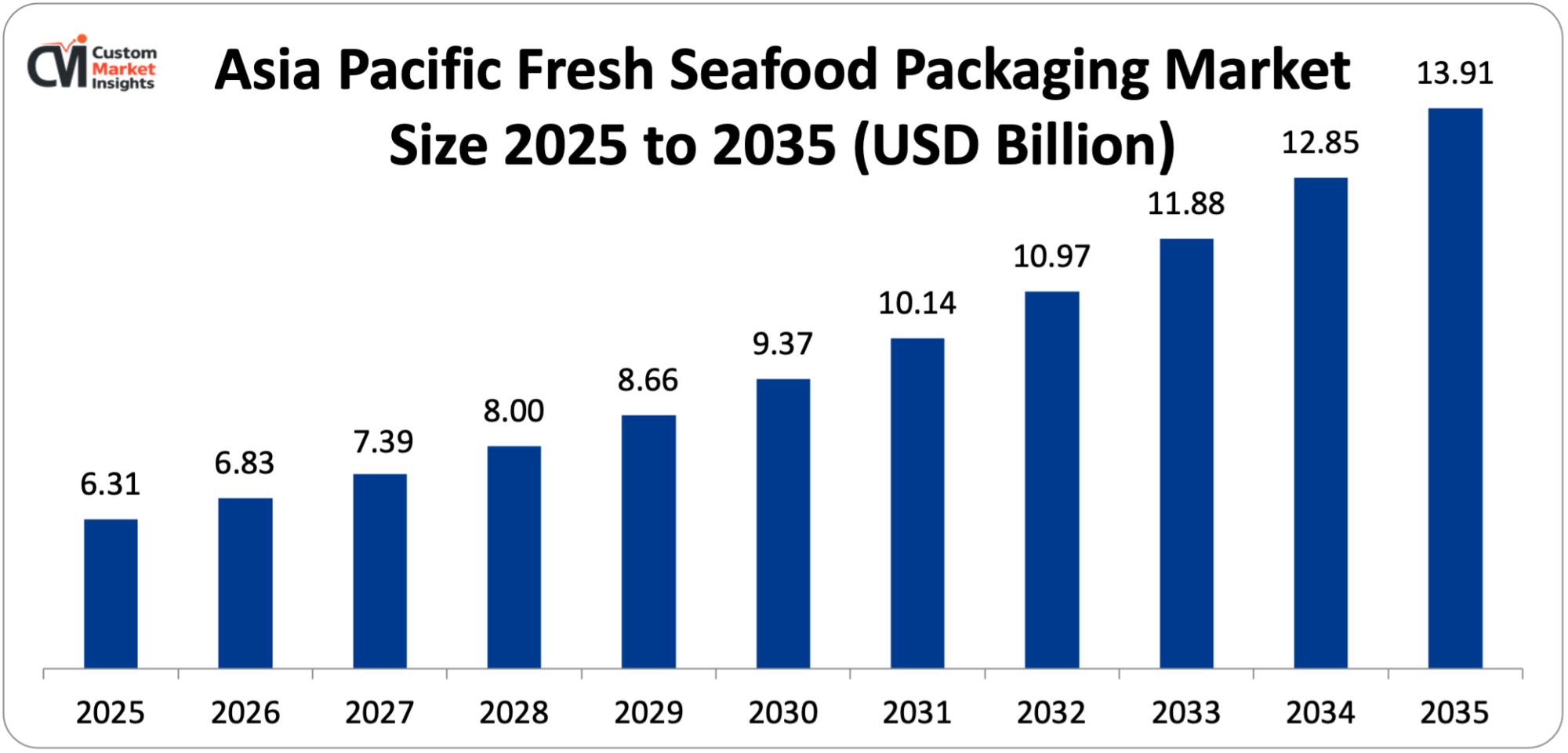

The Asia Pacific fresh seafood packaging market size is estimated at USD 6.31 billion in 2025 and is projected to reach approximately USD 13.91 billion by 2035, with an 8.2% CAGR from 2026 to 2035.

Why Did Asia Pacific Dominate the Market in 2025?

In 2025, the region is estimated to control about 43% of the world market share, and Asia Pacific is simultaneously the largest seafood producing and the largest seafood consuming region on earth with the FAO estimating that the Asia Pacific produces about 70% of world fish production and at the same time consumes about 70% of the total world fish consumption in volume. China alone generates an estimated 65 million metric tons of seafood every year – some 40% of the global generation – in terms of aquaculture, marine fish, and inland capture, creating a mammoth domestic packaging demand base at all levels of the supply chain from farm gate to processing, cold chain distribution, and retail.

A highly developed culture of fresh seafood retail and foodservice (with the highest per capita consumption rate of fresh fish in the world, estimated at about 50 kg per person per year and a culture of high-value fresh-seafood retail packaging based on aesthetic presentation and strict freshness requirements) makes Japan one of the most technologically advanced and highest-value fresh seafood packaging markets in the world. The fast growth in premium seafood retailing in South Korea, the exporting industries of Vietnam and Indonesia that require a large volume of packaging in order to have high-quality packaging that can meet the requirements of their export market, and the modernization of fresh seafood retailing in India through organized retail sector in Tier 1 and Tier 2 cities are all contributing factors to the high position of Asia Pacific in the regional market.

China Market Trends

The Chinese market has the largest fresh seafood packaging market in Asia Pacific, driven by the fact that China leads in the production of aquaculture products across the globe with a production of about 70% of the world’s farmed shrimp, carp, tilapia, and shellfish and a consumer base of 1.4 billion and a fast growing modern retail penetration in fresh seafood products. The fresh seafood retail market in China is also dealing with a structural change, an artificial shift in wet markets that once dominated (an estimated) 80% of fresh seafood retail transactions in the state but is now facing the threat of being forced to be subsidized by COVID-19-related hygiene regulations and urbanization through supermarkets as well as online shopping, which demand standardized and hygienically packaged fresh seafood products with convenient labeling and a specific shelf life. The Hema (Freshippo) supermarket form of Alibaba, a combination of online ordering, in-store live seafood tanks, and 30 minutes home delivery within a 3 km radius, is the most innovative format of fresh seafood shop in the world, and the requirements of Hema packaging to fit its 350 plus stores create a valuable stream of premium packaging demand. The domestic packaging companies of China such as Sealed Air China, Bemis China and local packaging manufactures are in a fast developing mode of providing modern day innovative MAP, vacuum skin packaging and sustainable tray designs to meet the modernizing fresh seafood retailing market.

Why is North America Experiencing Steady and Sustained Growth?

The U.S. is the largest importer of seafood by value globally and Alaska has a large wild-catch fishery that supplies about 60% of domestic U.S. seafood that will support the steady growth of the industry with an approximate CAGR of 7.2% through 2026-2035; the growing online fresh seafood delivery sector that provides consumers with direct access to fresh and frozen products will demand premium insulated packaging, and the growing use of MAP and vacuum skin packaging technologies by the U.S. retail chains is pursuing to cut seafood In 2024, the U.S. market for seafood consumption surpassed USD 102 billion in the retail and foodservice market, and the highest-growth and highest-margin segment of all seafood sales was fresh and chilled seafood.

U.S. Market Trends

The convergence of robust demand expansion by health-conscious consumers and premium seafood positioning; the increasing sustainability commitments by large retail chains setting plastic-free or recyclable-only seafood packaging objectives and the accelerating expansion of premium DTC fresh seafood brands developing competitive edges by differentiated insulated home delivery packaging, which conveys quality and sustainability credentials, shape the U.S. fresh seafood packaging market. The FSMA Seafood HACCP guidelines of the FDA and the National Oceanic and atmospheric Administration (NOAA) Seafood Inspection Program provide a platform of compulsory packaging documentation and labeling rules that prejudices advanced packaging solutions with added traceability capacities.

Why is Europe Emphasizing Sustainability and Regulatory Compliance?

The market size of the European fresh seafood packaging is approximated to be USD 3.24 billion in 2025 and estimated to be USD 6.47 billion in 2035 at a CAGR of 7.1. Europe is the most challenging to pack fresh seafood and EU regulations have already imposed regulations that the world has to adopt such as the Packaging and Packaging Waste Regulation (PPWR), requiring all plastic packaging to be recyclable by 2030 on the EU market, The Single-Use Plastics Directive already prohibiting the use of EPS food containers on the market in all EU countries and the Fisheries Control Regulation, requiring that all seafood sold on the EU market have full digital traceability.

The most influential source of fresh seafood packaging innovation in the world is Norway, the largest salmon exporter with about 1.2 million metric tons of farmed Atlantic salmon being exported every year, whose needs in terms of packaging options to preserve the quality of their products during 4-7 day air freight shipments to many markets around the globe are a continuous driver behind the development of innovative MAP, vacuum skin packaging (VSP), and insulated transport packaging systems. The four largest European national markets are Germany, France, the United Kingdom, and Spain, and they are characterized by well-developed fresh seafood retail culture and high packaging requirements. The development of its own sustainable packaging standards to be adopted in the UK post-Brexit (based on the EU but not identical) generates further compliance challenges for seafood exporters and importers operating in the two markets at the same time.

Why is the Middle East & Africa Region Experiencing Growth?

The LAMEA region exhibits market development trends due to the rapidly modernizing fresh seafood retailing industry of the Gulf Cooperation Council, over which the premium hypermarket chains of Carrefour UAE, LuLu Hypermarket and Spinneys are heavily investing in fresh seafood counter infrastructure and packaged seafood product ranges, Saudi Arabia and the UAE having large populations of expatriates in the cultures that consume seafood, novel fresh seafood demand being created by the geographic location of the Middle East as a transit hub of fresh seafood flowing out of the Indian Ocean producing regions to the European and North American markets generating significant transit and repackaging demand, South Africa’s significant domestic fishing industry, including the Cape Town-based hake and pilchard sectors generating export packaging demand, and Brazil’s substantial shrimp and tilapia aquaculture industries positioning Latin America as a growing source of packaged fresh seafood exports requiring international standard packaging solutions.

Top Players in the Market and Their Offerings

- Sealed Air Corporation

- Amcor plc

- Berry Global Group Inc.

- Huhtamaki Oyj

- Pactiv Evergreen Inc.

- Smurfit Kappa Group plc

- UFP Technologies Inc.

- Coveris Holdings S.A.

- Winpak Ltd.

- Plastipak Holdings Inc.

- Detmold Group

- Others

Key Developments

The market has seen considerable evolutions due to the demand by the industry players to grow the sustainable packaging capacity, the implementation of the active and intelligent packaging technology usage, and the solution of the increasing demands of the regulatory and commercial pressure on plastic reduction at various levels of the global supply chain of fresh seafood.

- In September 2025: Sealed Air Corporation reported the commercial introduction of its Cryovac Darfresh On Tray 2.0 vacuum skin packaging system, which has a new paper-based top web choice that substitutes the traditional plastic lidding film with a paper-laminate construction that offers the same gas protection but allows the package to be recycled in normal paper recycling streams after separation by the consumer.

- In November 2025: Amcor plc declared a strategic investment of USD 85 million in its Ghent, Belgium, flexible seafood packaging plant and grew capacity production of high-barrier MAP and vacuum pouch films by approximately 35% to satisfy quickening demand among European seafood processors seeking new plastic-recyclable flexible packaging items that are in line with the EU Packaging and Packaging Waste Regulation.

These strategic operations have enabled firms to consolidate market bases, develop sustainable packaging innovation pipelines, increase manufacturing capacity as demand grows on material transitions involving regulations, and exploit the huge commercial potential presented by the convergence of rising seafood consumption and increasing sustainable packaging adoption across all retail and foodservice sectors of the global restaurant and food sectors.

The Fresh Seafood Packaging Market is segmented as follows:

By Material Type

- Plastic (Polyethylene, Polypropylene, PET, PVC, EPS)

- Paper & Paperboard

- Modified Atmosphere Packaging (MAP) Films & Laminates

- Biodegradable & Sustainable Materials (Molded Fiber, PHA, PLA, Seaweed-Based)

- Aluminum & Metallic Films

- Other Materials

By Packaging Type

- Trays & Clamshells

- Bags & Pouches (Vacuum Bags, Zip-Lock, Stand-Up Pouches)

- Wraps & Films (Stretch Wrap, Shrink Film, Overwrap)

- Boxes & Cartons (Wax-Coated, Corrugated, Insulated)

- Nets & Mesh Bags (Primarily Shellfish)

- Other Packaging Types

By Application

- Fish (Salmon, Tuna, Cod, Tilapia, and Other Finfish)

- Crustaceans (Shrimp, Crab, Lobster, Crayfish)

- Mollusks & Shellfish (Oysters, Clams, Mussels, Scallops)

- Cephalopods (Squid, Octopus, Cuttlefish)

- Other Seafood

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Fish Retailers & Fish Markets

- Online Retail & Direct-to-Consumer

- Food Service (Restaurants, Hotels, Catering)

- Other Channels

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Fresh Seafood Packaging by Segments

- 2.1.2. Fresh Seafood Packaging by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Fresh Seafood Packaging Market Attractiveness Analysis, By Material Type

- 2.2.3. Fresh Seafood Packaging Market Attractiveness Analysis, By Packaging Type

- 2.2.4. Fresh Seafood Packaging Market Attractiveness Analysis, By Application

- 2.2.5. Fresh Seafood Packaging Market Attractiveness Analysis, By Distribution Channel

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Rising Global Seafood Consumption and Health-Driven Dietary Shifts

- 3.1.2. Food Safety Imperatives and Shelf-Life Extension Technology Driving Packaging Innovation

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Fresh Seafood Packaging Market – By Material Type

- 4.1. Material Type Market Overview, By Material Type Segment

- 4.1.1. Fresh Seafood Packaging Market Revenue Share, By Material Type, 2025 & 2035

- 4.1.2. Plastic (Polyethylene, Polypropylene, PET, PVC, EPS)

- 4.1.3. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Paper & Paperboard

- 4.1.7. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Modified Atmosphere Packaging (MAP) Films & Laminates

- 4.1.11. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Biodegradable & Sustainable Materials (Molded Fiber, PHA, PLA, Seaweed-Based)

- 4.1.15. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Aluminum & Metallic Films

- 4.1.19. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Other Materials

- 4.1.23. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Material Type Market Overview, By Material Type Segment

- Chapter 5. Fresh Seafood Packaging Market – By Packaging Type

- 5.1. Packaging Type Market Overview, By Packaging Type Segment

- 5.1.1. Fresh Seafood Packaging Market Revenue Share, By Packaging Type, 2025 & 2035

- 5.1.2. Trays & Clamshells

- 5.1.3. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Bags & Pouches (Vacuum Bags, Zip-Lock, Stand-Up Pouches)

- 5.1.7. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Wraps & Films (Stretch Wrap, Shrink Film, Overwrap)

- 5.1.11. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Boxes & Cartons (Wax-Coated, Corrugated, Insulated)

- 5.1.15. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Nets & Mesh Bags (Primarily Shellfish)

- 5.1.19. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Other Packaging Types

- 5.1.23. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Packaging Type Market Overview, By Packaging Type Segment

- Chapter 6. Fresh Seafood Packaging Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Fresh Seafood Packaging Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Fish (Salmon, Tuna, Cod, Tilapia, and Other Finfish)

- 6.1.3. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Crustaceans (Shrimp, Crab, Lobster, Crayfish)

- 6.1.7. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Mollusks & Shellfish (Oysters, Clams, Mussels, Scallops)

- 6.1.11. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Cephalopods (Squid, Octopus, Cuttlefish)

- 6.1.15. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Other Seafood

- 6.1.19. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Fresh Seafood Packaging Market – By Distribution Channel

- 7.1. Distribution Channel Market Overview, By Distribution Channel Segment

- 7.1.1. Fresh Seafood Packaging Market Revenue Share, By Distribution Channel, 2025 & 2035

- 7.1.2. Supermarkets & Hypermarkets

- 7.1.3. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Specialty Fish Retailers & Fish Markets

- 7.1.7. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Online Retail & Direct-to-Consumer

- 7.1.11. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Food Service (Restaurants, Hotels, Catering)

- 7.1.15. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Other Channels

- 7.1.19. Fresh Seafood Packaging Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Distribution Channel Market Overview, By Distribution Channel Segment

- Chapter 8. Fresh Seafood Packaging Market – Regional Analysis

- 8.1. Fresh Seafood Packaging Market Overview, By Region Segment

- 8.1.1. Global Fresh Seafood Packaging Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Fresh Seafood Packaging Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Fresh Seafood Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.1.4. Global Fresh Seafood Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 8.1.5. Global Fresh Seafood Packaging Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Fresh Seafood Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Fresh Seafood Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Fresh Seafood Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.2.3. North America Fresh Seafood Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 8.2.4. North America Fresh Seafood Packaging Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Fresh Seafood Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 8.2.6. U.S. Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Fresh Seafood Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Fresh Seafood Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.3.3. Europe Fresh Seafood Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 8.3.4. Europe Fresh Seafood Packaging Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Fresh Seafood Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 8.3.6. Germany Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Fresh Seafood Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Fresh Seafood Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.4.3. Asia Pacific Fresh Seafood Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 8.4.4. Asia Pacific Fresh Seafood Packaging Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Fresh Seafood Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 8.4.6. China Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Fresh Seafood Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Fresh Seafood Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Fresh Seafood Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 8.5.4. The Middle-East and Africa Fresh Seafood Packaging Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Fresh Seafood Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 8.5.6. Saudi Arabia Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Fresh Seafood Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Fresh Seafood Packaging Market Revenue, By Material Type, 2026 – 2035

- 8.6.3. Latin America Fresh Seafood Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 8.6.4. Latin America Fresh Seafood Packaging Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Fresh Seafood Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 8.6.6. Brazil Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Fresh Seafood Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Fresh Seafood Packaging Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Fresh Seafood Packaging Market: Company Market Share, 2025

- 9.2. Global Fresh Seafood Packaging Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Sealed Air Corporation

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Amcor plc

- 10.3. Berry Global Group Inc.

- 10.4. Huhtamaki Oyj

- 10.5. Pactiv Evergreen Inc.

- 10.6. Smurfit Kappa Group plc

- 10.7. UFP Technologies Inc.

- 10.8. Coveris Holdings S.A.

- 10.9. Winpak Ltd.

- 10.10. Plastipak Holdings Inc.

- 10.11. Detmold Group

- 10.12. Others.

- 10.1. Sealed Air Corporation

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 40

List Of Tables

Tables No 1 to 51

Prominent Player

- Sealed Air Corporation

- Amcor plc

- Berry Global Group Inc.

- Huhtamaki Oyj

- Pactiv Evergreen Inc.

- Smurfit Kappa Group plc

- UFP Technologies Inc.

- Coveris Holdings S.A.

- Winpak Ltd.

- Plastipak Holdings Inc.

- Detmold Group

- Others

FAQs

The key players in the market are Sealed Air Corporation, Amcor plc, Berry Global Group Inc., Huhtamaki Oyj, Pactiv Evergreen Inc., Smurfit Kappa Group plc, UFP Technologies Inc., Coveris Holdings S.A., Winpak Ltd., Plastipak Holdings Inc., Detmold Group, Others.

Government regulations impose extensive and tightening effect on all aspects of the fresh seafood packaging market, including standards of food contact materials safety and sustainable packaging standards, or traceability and labeling requirements specific to seafood. The most far-reaching regulatory trend that will impact the fresh seafood packaging industry in Europe, however, is the EU Packaging and Packaging Waste Regulation, which introduces a mandatory recyclability, recycled content, and packaging minimization rules that all packaging sold in the European market must meet by 2030, forcing systematic eradication of non-recyclable EPS, PVC and multi-material laminates, which have long defined the category. The FSMA Seafood HACCP regulations of the U.S. FDA are mandatory in packaging documentation, temperature management and labeling of allergens that incline towards packaging solutions with in-built quality management features. Fishery products and seafood packaging standards established in the Code of Practice of FAO, which includes internationally recognized standards of packaging and cold chain management of seafood, have an impact on regulatory systems of fish production countries that are developing. EU and U.S. seafood import regulation country-of-origin labeling, species authentication, and sustainable harvest certification documentation imposes packaging labelling demands which have to be ensured within packaging design limitations which necessitates high-resolution printing, labelising, and QR code linked digital documentation systems.

Prices of Fresh seafood packaging widely range according to the type of material, the type of a package, and the level of sophistication of the technology used in the packaging process, which could be USD 0.05-USD 0.15 per unit when it comes to basic PE wrap overwrap on foam trays, USD 0.25-USD 0.65 per unit when it comes to MAP lidded tray packaging systems using high-barrier multilayer films, USD 0.80-USD 2.50 per unit when it comes to high-end These higher packaging differentials are established based on equally differentiated packaging performance in terms of shelf life, reduction of product waste, and also quality of consumer experience that can be measured into retail margin gains. The savings on shrink rates in the seafood category on retailers who do implement MAP-lidded tray packaging of the fresh salmon, such as those, would typically realize 22-28% decreases in the rate of shrink in the seafood category, the equivalent to USD 15,000-USD 45,000 per store location decreases in the waste savings as compared to incremental packaging cost increases of USD 0.25-USD 0.40 per unit packaging that would clearly pay back with a strong ROI at the typical sales of the The increasing premiumization of fresh seafood in the world retail marketplace – with premium organic, sustainably certified, and species-authenticated seafood retailing at premiums of 30 -80% over conventional equivalents.

According to current market analysis, the market is expected to grow to about USD 31.42 billion in 2035, pushed by the ongoing growth of seafood consumption globally to an estimated 185 million metric tons per year by 2035 as the global expansion of aquaculture and sustainable management of all fisheries continues, the full adoption of passive and active packaging materials into the seafood industry, and the creation of active and intelligent packaging systems such as freshness sensors, time-temperature indicators, and antimicrobial systems that command higher prices than passive packaging options, the maturation of direct-to-consumer online seafood delivery as a mainstream shopping behavior requiring premium insulated packaging solutions, digital traceability integration becoming standard across global seafood supply chains enabling QR-based consumer transparency that drives premium brand positioning, and sustainable aquaculture expansion in new geographic markets including land-based recirculating aquaculture systems in Europe and North America creating new premium seafood categories requiring distinctive packaging solutions, at a CAGR of 7.9% from 2026 to 2035.

Asia Pacific should continue to have the largest revenue share throughout the forecast period as both the largest global producer and consumer of seafood at the same time. China is expected to produce 65 million metric tons of seafood every year and create packaging demand with every supply chain phase. the huge and fast-growing consumer populations of China, India, Southeast Asia, and South Korea, with their progressive modernization of seafood retailing infrastructure, are creating sustained demand upgrades from unpackaged traditional market products to packaged supermarket and online retail product, in effect the progressive modernization of seafood retailing infrastructure is creating sustained demand upgrades from unpackaged traditional market products to packaged supermarket and online retail formats, and government food safety and export quality programs across the region are driving continuous packaging specification improvement.

Asia Pacific will have the largest market share and the best growth trend at 8.2% CAGR over the forecast period because of the dominance of China, the largest global aquaculture producer with packaging demand at an unprecedented scale, the modernization of fresh seafood retail systems in India, Vietnam, Indonesia, and Thailand continues to move towards the packaged modern retail format, Japan has a high culture of using premium packaging, and the global per-capita consumption of fresh fish is the highest, the expansion of the Southeast Asian seafood processing export industries means that it needs international-standard packaging in order EU and North American market access, and government food safety modernization programs across the region mandating improved packaging hygiene and traceability standards that upgrade packaging specifications across supply chains.

It is estimated that in the next three years the Global Fresh Seafood Packaging Market will be substantially growing with the global fish consumption at a record 162 million metric tons in 2023, and the per capita consumption doubling with 9.9 kg rising to 20.7 kg since 1960s creating sustained packaging demand, the seafood industry estimated to suffer annual losses of USD 35 billion in spoilage and wastages creating compelling economic incentive to invest in advanced shelf-life extending packaging, MAP packaging increasing seafood shelf life 3-5 days to 10–18 days generating 23% retail shrink reduction that directly improves retailer economics, global aquaculture production projected to reach 109 million metric tons by 2030 generating substantial incremental farm-to-retail packaging demand, EU Packaging and Packaging Waste Regulation mandating recyclable or compostable seafood packaging by 2030 driving industry-wide material transition investment, the online fresh seafood delivery market projected to grow at 17.4% CAGR through 2030 requiring premium insulated shipping packaging, and digital traceability mandates under EU Fisheries Control Regulation driving QR and NFC integration investment across the European seafood packaging supply chain.