Privacy Glass Market Size, Trends and Insights By Technology (Polymer Dispersed Liquid Crystal (PDLC) Glass, Electrochromic Glass, Suspended Particle Device (SPD) Glass, Thermochromic Glass, Micro-Blind Technology, Other Technologies (Photochromic, Liquid Crystal on Silicon)), By Application (Architectural & Construction (Commercial, Residential, Institutional), Automotive (Sunroofs, Side Windows, Rear Windows, Panoramic Roofs), Healthcare (Patient Rooms, Operating Suites, Examination Rooms), Aerospace & Defense (Aircraft Windows, Military Vehicles), Consumer Electronics (Displays, Smart Mirrors, Wearables), Other Applications (Marine, Rail, Retail Displays)), By End-Use (Commercial (Offices, Hotels, Retail, Hospitality), Residential, Industrial & Institutional, Other End-Uses), By Distribution Channel (Direct Sales (OEM and Specification-Based), Distributors & Dealers (Glazing Contractors, Automotive Suppliers), Online Retail), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- View Inc.

- Gauzy Ltd.

- AGC Inc.

- Gentex Corporation

- Others

Reports Description

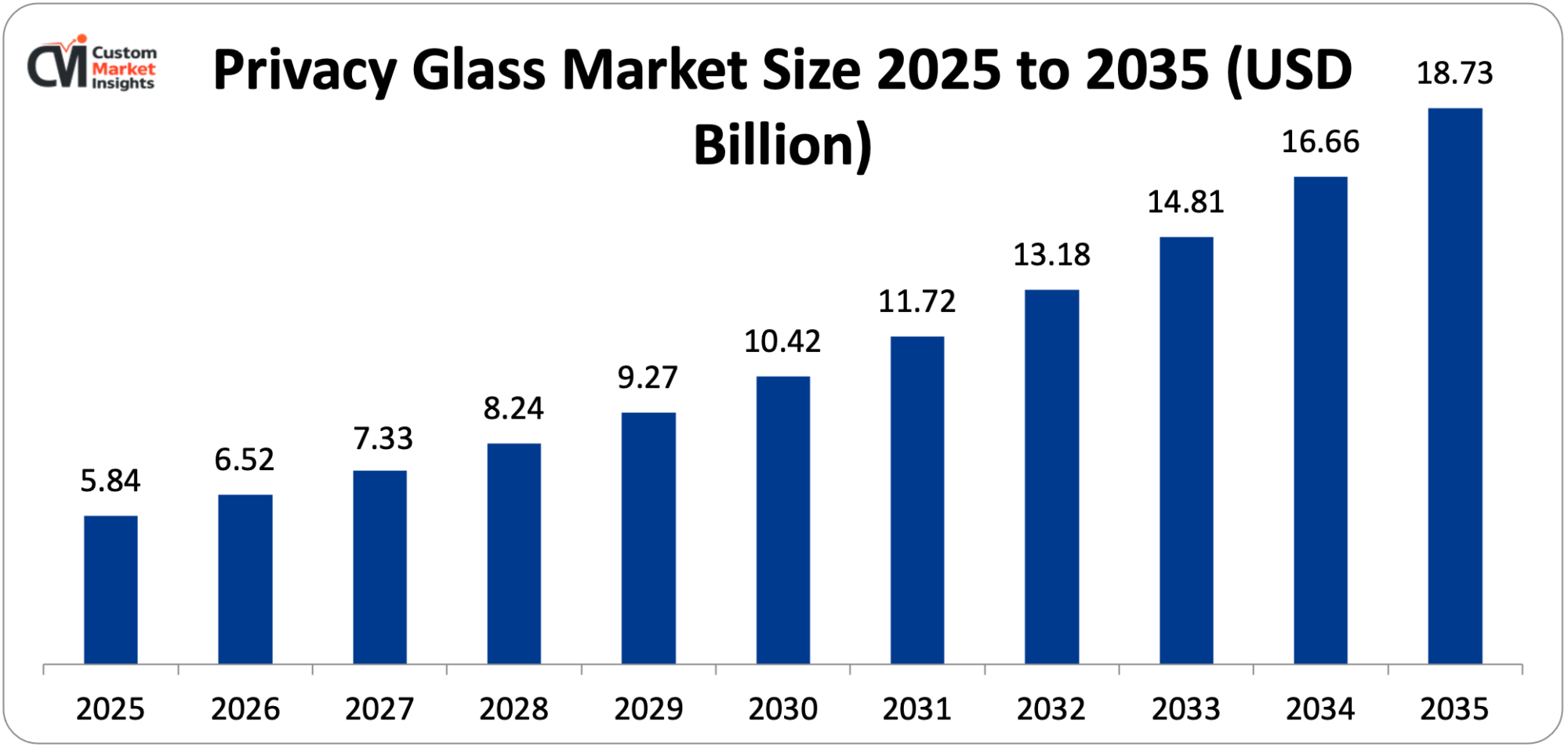

The privacy glass market size stands to be USD 5.84 billion in 2025 and is expected to grow to between USD 6.52 billion in 2026 and USD 18.73 billion in 2035 having a CAGR of 11.1% between 2026 and 2035.

The rapid adoption of smart building technologies that combine electronically switchable glazing to provide simultaneous privacy control and energy savings, the swift adoption of switchable privacy glass in vehicles to create sunroofs, side windows, and rear windshields as part of the premium vehicle and electric vehicle market, the increasing use of privacy glass in healthcare settings in which patient dignity and infection control hold priority, the ever-decreasing manufacturing costs of smart glass enhancing the competitive ability of the technology against the passive privacy options all drive strong and sustained growth of the market during the forecast period.

Market Highlight

- The privacy glass market in 2025 was headed by North America which had a market share of 37%.

- Asia Pacific: It is predictable that Asia Pacific will grow at the highest CAGR of 14.2 in a period between 2026 and 2035.

- Through technology, the PDLC glass segment was able to gain about 36% of the market share in 2025.

- By technology, the electrochromic glass segment is expanding at the highest CAGR of 13.8% between 2026 and 2035.

- Application-wise the architectural and construction segment will have the largest market share of 44% in 2025 with the automotive segment having the highest growth in CAGR of 14.9% in the estimated time frame of 2026 to 2035.

- By end-use, the commercial segment was taking 48% of the market share in 2025.

- By channel of distribution, the direct sales segment would have 62% of the market share in the year 2025.

- Privacy glass had a leading 18.3% market share of the total smart glass market in 2024, with privacy glass being the most commercialized and largest volume application area in the wider smart glazing technology range.

Significant Growth Factors

The Privacy Glass Market Trends present significant growth opportunities due to several factors:

- Smart Building Revolution and Energy Efficiency Mandates Driving Architectural Adoption:

The fact that switchable glazing technologies can easily switch between transparent and opaque modes on command is the major structural force behind the architectural adoption of privacy glass, as this technology offers building operators a combination of the previously unachievable simultaneous benefits of dynamic privacy control, solar heat gain control, glare control, and optimization of daylighting which, together, lowers flooring-based building energy use and improves occupant comfort and spatial flexibility.

The International Energy Agency (IEA) estimates that approximately 40% of global energy is consumed by buildings, and 33% of the global greenhouse gas emissions are attributed to buildings and window glazing according to the international energy agency is an active contributor of 25–30% of building heating and cooling energy loads, resulting in dynamic glazing that actively regulates solar heat gain and heat loss via glass surfaces to become an attractive constituent in building decarbonization strategies.

The green building market size is projected to reach USD 573 billion in 2024 and USD 1.36 trillion by 2032 with a CAGR of 11.4%, according to CMI, with privacy glass increasingly being defined as a standard feature on green building projects to meet the LEED, BREEAM, WELL, and similar sustainability certification standards. A series of experiments by Lawrence Berkeley National Laboratory showed electrochromic smart windows could save building cooling energy use by 20-30% as well as peak demand by up to 26% of traditional low-e glazing in commercial buildings, statistics that are having a dramatic effect on the development of building energy codes in the United States, the European Union, and key Asian markets.

The Net Zero Emissions by 2050 Roadmap of the IEA identifies building envelope performance, including that of glazing, as the key element of which improvement is needed in order to meet the global climate targets, and national building energy codes including the Energy Performance of Buildings Directive (EPBD) recast of 2024 in the EU and building energy efficiency standards of the U.S. Department of Energy are increasingly tightening the requirements of solar heat gain coefficient and thermal transmittance in ways that favour dynamic glazing over the less efficient solution of a static glass glazing. The Oxford Economics expects that the privacy glass will become a luxury architectural product in new commercial office towers, commercial mixed-use projects, airport terminals, healthcare facilities, and educational buildings by 2030, with privacy glass being specified as a building feature that will provide energy performance, occupant well-being, and spatial flexibility benefits in addition to its core privacy functionality.

- Growing Privacy, Wellness, and Human-Centric Design Consciousness in Architecture and Interior Design:

In addition to energy efficiency, the escalating value of privacy, psychological comfort, biophilic relationships to the outdoors, and human-centered workspace design principles by building owners, corporate tenants, and residential developers is generating an overwhelming demand that privacy glass will offer inhabitants on-demand visual privacy access without compromising daylight access and view connection or spatial openness. The old mechanisms of addressing the issue of visual privacy in glass-walled buildings, window films, blinds, curtains and fixed opaque partitions, place a long-lasting or short-term constraint on the access to natural light and view connectivity, which is becoming known to be damaging to the occupant wellbeing, productivity as well as satisfaction by corporate clients investing in high-end workplace facilities to draw and keep talent.

In a 2024 CBRE Global Workplace Survey of 12,000 office workers around the world, the most popular factor in workplace satisfaction was natural light, with 78% stating it as very important, and second, privacy to concentrate on work, with 71% stating it as very important, which is where a design solution such as privacy glass uniquely comes in, as it offers both features concurrently on demand. The global wellness real estate sector (including residential and commercial projects focused on occupant health and well-being) has been estimated to be USD 436 billion in 2024 and projected to expand to USD 913 billion by 2031 at a CAGR of 11.2, with biophilic design principles such as the highest possible glazing area and the dynamic control of privacy by use of switchable glass being a characteristic design strategy of the wellness real estate category.

What are the Major Advances Changing the Privacy Glass Market Today?

- Next-Generation Electrochromic Thin-Film Technology Enabling Cost-Competitive Commercial Scale:

The most technically advanced and commercially significant innovation in the privacy glass industry is the maturation of the electrochromic thin-film deposition technology, which enables all-solid-state, electrically switchable glazing, which gradually and accurately switches between transparent, tinted, and privacy modes, based on the electrochemical intercalation of ions in tungsten oxide and other transition metal oxide thin films. The electrochromic glazing is moving out of a high-end niche technology into a low-end target market through manufacturing process improvements, which are steadily driving down the cost. Electrochromic glass is based on the principle that a lithium or hydrogen ion can reversibly intercalate between tungsten trioxide electrochromic layers in response to a low direct current voltage of 1 5 volts across the stack of multiple layers of electrochromic substrate between these extremes with midpoints continuously adjustable between them.

The key commercial benefit of the technology over the PDLC privacy glass, which is switched between clear and milky-opaque, is that it can offer graduated tinting, which can be used to regulate the level of solar heat gain and glare but still maintain building energy control capabilities that are beyond the binary privacy switching. The most commercial prototypes of electrochromic glazing include Sage Electrochromics (Saint-Gobain), View Inc., and Halio Inc. View Smart Windows created by View Inc., have been installed in more than 75 million square feet of commercial spaces in North American cities such as the Apple in Austin, the Boston Properties office high-rises, and various international airports.

Continuous optimization of the sputtering process, higher coating line throughput and economies of scale due to a higher volume of production have led to cost reductions in the manufacturing of electrochromic glazing by an estimated 40-50% over the 2015-2024 period based on techno-economic analyses in the industry with further cost reductions of 25-35% expected in 2030 as volume grows and next generation coating materials such as NiO based counter electrode formulations with enhanced cycle stability lead to further cost reduction. The warranty Electrochromic glass market around the world is estimated to reach USD 1.28 billion by 2024 and is expected to grow to USD 4.87 billion by 2032 with a CAGR of 18.3, which in itself is the fastest-growing segment of privacy glass in the wider market.

- PDLC Film Technology Democratization and DIY Retrofit Market Development:

The switchening of polymer dispersed liquid crystal (PDLC) film technology, which is a rapid and easy to adopt technology to commoditized market, a small alternating current voltage of 4865 volts applied to liquid crystal droplets suspended in a polymer matrix, converting the milky-opaque scattering state into a transparent screening state is expanding the privacy glass market beyond new construction applications to the enormous retrofit and renovation market, as the applicability of PDLC switchable film can be applied as a retro.

The PDLC switchable film offered by various major manufacturers such as Gauzy Ltd., Chiefway Technology, DMDisplay, and Intelligent Glass retails at USD 80-USD 200 per square meter, comes in rolls that can be cut to size and applied to an existing piece of glass with adhesive mounting (where it is available), and provides switchable film such as PDDLC in a commercial grade of USD 80-USD 200 per square meter, which is a significant cost savings when compared to USD 500-USD 12 This affordability in cost is building a large DIY and professional installer retrofit market that includes residential bathroom and bedroom window projects, home office privacy reassurance, commercial conference room partitions retrofit, and hospitality venue privacy control – market segments which can not be effectively addressed by factory-fabricated privacy glass because of custom size and installation constraints. It is estimated to be worth USD 580 million in 2024 with a 19.4% CAGR increase to 2030, much higher than the factory-laminated glass segment as film accessibility and smart home integration functionality continues to increase, with the global PDLC film retrofit market expected to rise.

Films of PDLC with embedded wireless control – compatible with Amazon Alexa, Google Home, Apple HomeKit, and proprietary smart home platforms – are allowing consumer-level installations of smart home privacy glasses without the need to hire an electrical professional and opening up the range of consumers that are addressable to an unprecedented scale. Israel-based Gauzy of America, which floated in 2024 on the NYSE, has become a world leader in the technology of PDLC and SPD film technology.

Category Wise Insights

By Technology

Why Does PDLC Glass Lead the Market?

PDLC glass is the biggest segment in the technology with a share of about 36% in the market in 2025. This domination is due to PDLC having a combination of the lowest cost of manufacturability of any active privacy glass technology, the most extensive selection of commercial suppliers to offer competitive prices, the fastest switching rate – changing between opaque and clear in less than 100 milliseconds versus 1-3 minutes in electrochromic glass – that gives it the greatest choice of applications in the instant activation of privacy needed by the customer in applications such as hospital patient rooms, conference rooms, and retail fitting rooms, and its long-tested 20-plus years commercial history of reliability and performance that offers design spec The PDLC glass is made by placing a PDLC polymer film between two conductive coated glass layers in an alternating sequence of ITO (indium tin oxide), sandwicing the two layers, and then laminating under pressure and heat, a process that is well understood, extensively practiced by independent glass laminating fabricators around the globe and is accessible to custom size and shape production that can respond to the unique sizing needs of architecture and automotive applications.

The global PDLC glass industry is estimated to be USD 2.1 billion in 2024, and will grow to USD 6.8 billion by 2032 with a CAGR of 15.8 with architectural applications contributing about 58% of the PDLC glass revenue. The main drawback of the PDLC technology – its binary switching property that only offers clear or milky-opaque access levels without intermediate tinting – limits its use in situations where graduated solar control is needed to create a market segmentation between PDLC (privacy-oriented applications) and electrochromic glass (privacy and energy management applications) that will likely be maintained during the foreseeable period even though some of the PDLC product lines have developed partial tinting with advanced polymer matrix structures.

By Application

Why Does Architectural & Construction Dominate the Market?

The largest application segment is architectural and construction applications, which will provide about 44% of the total market share in 2025. Such a prominent stance indicates the size of the architectural market construction business has been USD 13.5 trillion in 2024 and will grow to USD 19.2 trillion by 2030, the growing specification of privacy glass in high-end commercial, hospitality, healthcare, and residential buildings as a design feature and credential of sustainability and the growing trend of glass-intensive open-plan architectural designs to provide simultaneous demand on transparency and demand-on-demand privacy that can only be optimally fulfilled with switchable glazing.

Commercial office buildings demonstrate the most volume of architectural use, due to the post-pandemic workplace redesign wave where the companies are investing in premium, extremely amenitized office spaces to bring employees back to in-person work, including privacy glass on conference rooms, executive offices, and collaboration spaces having a conspicuous role in high-profile workplace renovation projects. Hotel guest room bathroom privacy glass, spa and wellness facility privacy partitions, and restaurant private dining room glass wall applications are rapidly increasing as luxury brand hotels such as Marriott, Hilton and Four Seasons are adopting privacy glass as a brand feature of premium room category. The residential application sector is specifically a vibrant one where the price of the PDLC switchable glass into residential bathroom windows and glass walls on bedroom walls is fast approaching USD 150 1 USD 300 per square meter – a price point that is becoming more and more affordable to the high-end residential building market – and where smart home integration is making it possible to voice and smartphone controlled, which is finding favor with technology-obsessed homeowners.

By End-Use

Why Does Commercial Lead the Market?

The largest segment in terms of market share is commercial end-use with about 48% of the market share in 2025 due to the premium culture of specifying glass in the real estate of corporations, the large concentration of glass-intensive modern commercial building stock in need of privacy management solutions, the financial ability of contemporary real estate developers and corporate occupiers to invest in the advanced glazing technologies and the strong total cost of ownership value of privacy glass in commercial environments where the removal of the maintenance costs of curtain and blinds, cleaning services and frequent replacement offers some real measure of long-term cost savings In 2024, the world property market measured USD 34.4 trillion as a huge asset base, the privacy glass is an incremental confinement specification, which increases the quality of assets, energy performance certification rating, and occupancy and retention rates of occupants that fuel rental income and property value. Hotels and hospitality are one of the most valuable commercial application markets and privacy glass is being used with open-plan bathrooms in the luxury hotel rooms to enhance the aesthetic image and spaciousness of the rooms whilst maintaining on-demand privacy which is a premium feature that is being charged at 15-25% of the room rate at luxury hospitality properties where the feature is heavily advertised as a unique feature of the rooms.

By Distribution Channel

Why Does Direct Sales Dominate?

It is estimated that direct sales will achieve about 62% of the market share in the year 2025, and that privacy glass market is project-specification focused where the majority of the strongest architectural and automotive supply relations are formed directly between manufacturers of privacy glasses and architects, building developers, automotive OEMs, and large glazing contractors but not via the distributor intermediaries. Commercial architectural privacy glass is generally of a custom specification (such as custom glass sizes, film designs, frame details, control system design integration with building automation systems, and warranty information) which cannot be effectively mediated by distributor channel relationships.

OEM-direct supply business models in the automotive industry, such as that of a manufacturer of privacy glass selling directly to tier-1 automotive glazing suppliers, such as AGC, Pilkington/NSG, Guardian Glass, and Carlex, who are then selling directly to vehicle assembly plants, are similarly bypassing old distribution channels due to the volume, precision of the technical specifications and reliability imperatives of automotive OEM supply. Online retail – online retailing will be the most rapidly growing distribution channel with an estimated CAGR of 22.4% between 2026 and 2035 as the commoditization of PDLC film technology opens the possibility of retail-accessible product formats, and will involve distribution of switchable film products through online retail platforms such as Amazon, Alibaba and specialty smart glass e-commerce retailers without the need to involve distributor or contractor intermediaries.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 6.52 billion |

| Projected Market Size in 2035 | USD 18.73 billion |

| Market Size in 2025 | USD 5.84 billion |

| CAGR Growth Rate | 11.1% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Technology, Application, End-Use, Distribution Channel and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the North America Market Size?

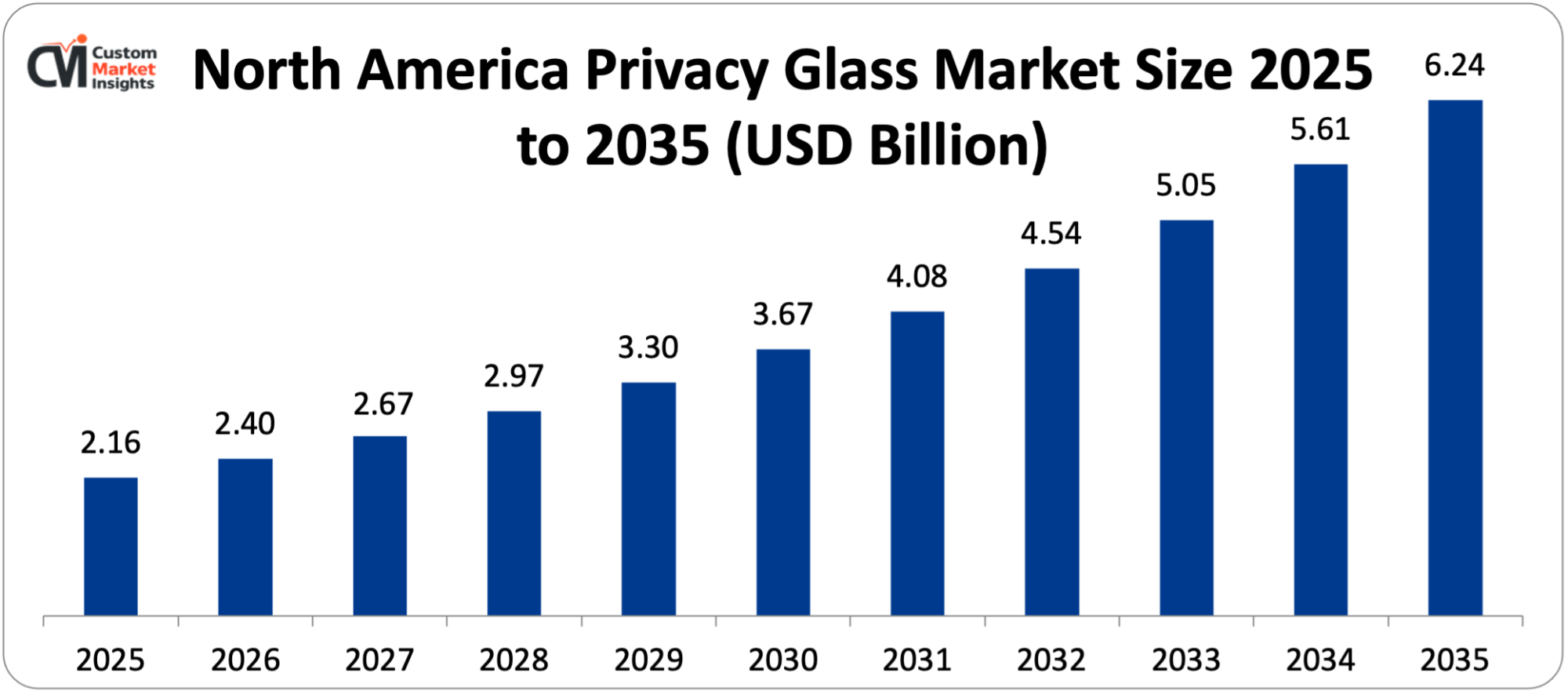

The North America privacy glass market size is estimated at USD 2.16 billion in 2025 and is projected to reach approximately USD 6.24 billion by 2035, with a CAGR of 11.2% from 2026 to 2035.

Why Did North America Dominate the Market in 2025?

In 2025 North America controls about 37% of the world market share, now showing that the region is the home market of the major world electrochromic glass producers View Inc. and Sage Electrochromics of Saint-Gobain, with its headquarters and manufacturing based in the United States, the highest commercialized and technologically advanced privacy glass market, with the greatest breadth of product technologies, uses and installation experience, a large commercial construction market with culture of premium specification, and the most advanced premium and electric vehicle markets in the world creating the greatest demand for automotive privacy glass. Investment in the development of electrochromic glazing technology by the U.S. Department of Energy through national laboratory research programs at Lawrence Berkeley National Laboratory and NREL has played a role in improving the commercial viability of the electrochromic privacy glass, with grant programs funded by the DOE SunShot and Building Technologies Office helping View Inc. and Sage Electrochromics reach the commercial scale level. The U.S. commercial office construction pipeline, with some 180 million square feet of new office space currently under construction in 2024, per CBRE, provides a significant near-term available market to architectural privacy glass, and targets of green building certification are propelling smart glazing specification rates to over 15% of new high-end construction of commercial office buildings in major urban areas.

U.S. Market Trends

The U.S. market is informed by the rising customization of View Smart Windows and SageGlass in LEED Platinum and WELL certified commercial buildings, the rising use of automotive privacy glass in Tesla, BMW, and Mercedes-Benz EV systems built in U.S. factories, and the hastening residential retrofit market informed by the availability of PDLC film via home improvement stores and otherwise.

The commercial building energy efficiency tax deduction under Section 179D of the U.S. Inflation Reduction Act that offers USD 0.505.00 per square foot tax deduction of energy efficiency improvements such as high-performance glazing is yielding real financial benefits to owners and developers of commercial buildings to specify smart glazing solutions that qualify them under maximum tax deduction rates, and privacy glass energy management capabilities allow them to qualify for higher incentive amounts than conventional high-performance static glazing.

Why is Europe a Strategically Important Market?

The European privacy glass market is projected to hit USD 1.52 billion in the year 2025 and is likely to hit USD 4.21 billion within the year 2035 with a CAGR of 10.7. Europe is a market of outstanding strategic value due to the most rigorous building energy performance regulatory framework in the world- the EU Energy Performance of Buildings Directive (EPBD) recast of 2024 requiring mandatory minimum energy performance standards for all buildings by 2030 that would effectively force high-performance dynamic glazing into the designs of glass-intensive commercial buildings, and the concentration of the global luxury automotive industry in Germany including BMW, Mercedes-Benz, Audi, and Porsche, which are already among the most vigorous adopters of automotive privacy and smart glazing.

The nearly zero-energy building (nZEB) mandate of the EU, which requires all new buildings in EU member states to comply with the standards of nZEB, is a direct stimulus to the specification of architectural smart glazing, and the reason why building designers are now considering providing building solutions that are both nZEB-compliant and dynamic, without sacrificing the glass-intensive look of modern European commercial construction. ChromoGenics AB, based in Uppsala, Sweden is a major European developer of electrochromic glasses, with a proprietary ConverLight dynamic glazing product in the European commercial construction market, one of the indigenous European innovations in the smart glazing market as well as the European activities of the U.S. and Japanese global leaders.

Why is Asia Pacific the Fastest-Growing Market?

The fastest-growing regional market will be Asia Pacific, which is expected to have a CAGR of 14.2% between 2026 and 2035, due to the explosive growth of premium and electric vehicle production in China which in 2023 produced 9.6 million electric vehicles, which is 58% of global electric vehicle production, and the domestic brands of which are currently incorporating smart glazing as a distinctive feature of their model portfolios, the overwhelming growth of premium commercial real estate development in Beijing, Shanghai, Shenzhen, Singapore The glass manufacturing industry of China, which is the largest in the world (in volume of production) with a yearly output of over 800 million weight boxes, offers China a formidable domestic manufacturing platform to scale the production of PDLC and SPD glass to serve the domestic market and export markets that are offering increased opportunities to international markets at lower costs, with Chinese manufacturers of PDLC glass such as Zhuhai Kaivo Optoelectronic and Nanjing Topwell Technology being key global suppliers of these two glass products.

Why is the Middle East & Africa Region an Important Emerging Market?

The LAMEA region is one of the hottest emerging growth markets for privacy glass, as the Gulf Cooperation Council has a combination of phenomenal solar intensity with Dubai and Riyadh having solar irradiance of 5.0-6.0 kWh/m²/day versus most European cities having 3.0-4.0 kWh/m²/day, which would make smart glazing a solar heat gain control a highly attractive energy efficiency proposal in a climate where building cooling represents 60-70% of total building energy consumption. With a projected 2025–2035 development horizon, the NEOM megaproject, a USD 500 billion smart city construction in Saudi Arabia that brings in the principles of sustainability-first design and smart building envelope technologies, including privacy and electrochromic glass, is expected to become one of the largest single buyers of advanced glazing technologies in the world. Specifications of energy-efficient smart glazing in commercial and residential construction are being demanded by the UAE in its Dubai Clean Energy Strategy 2050 that requires buildings to be net-zero carbon by 2050, and the Abu Dhabi-based Estidama Pearl Building Rating System, which is akin to LEED in its green building certification platform. The developed technological industry in Israel (such as Gauzy Ltd., currently traded on the NYSE and with its headquarters in Tel Aviv) makes the country a hub of privacy glass technology innovation with domestic application demand as well as export opportunities in technological advancement.

Top Players in the Market and Their Offerings

- Saint-Gobain SA (Sage Electrochromics)

- View Inc.

- Gauzy Ltd.

- AGC Inc.

- Nippon Sheet Glass Co. Ltd. (Pilkington)

- Gentex Corporation

- Research Frontiers Inc.

- Corning Incorporated

- ChromoGenics AB

- Halio Inc. (Kinestral Technologies)

- Polytronix Inc.

- Others

Key Developments

The industry has experienced major changes with players in the market trying to increase the capacity of production, improve on the performance of technology, experience on production costs, and get increased demand in the automotive, architectural and health care application sections around the world.

- In January 2022: View Inc. declared a strategic collaboration with Skanska – one of the biggest construction and development companies in the world, to make View Smart Windows the standard of smart glazing specified by Skanska in commercial office and life science building development across North America and Europe.

- In November 2025: Gauzy Ltd. declared that its SPD-Smart panoramic roof system designed for the Chinese domestic market was commercially available: the partner was a large Chinese electric car manufacturer whose name was withheld until the formal announcement of the model launch.

Such strategic actions have enabled businesses to consolidate positions in the market, develop additional production capability to handle the increasing demand in various segments of usage, form strategic partnerships with the construction industry and automobile OEM clients that provide revenue visibility over long terms, and take advantage of the broad growth potential created by the convergence of building energy efficiency regulation, electric vehicle adoption, healthcare design evolution, and consumer smart home technology engagement driving the adoption of privacy glasses across all major end-use markets worldwide.

The Privacy Glass Market is segmented as follows:

By Technology

- Polymer Dispersed Liquid Crystal (PDLC) Glass

- Electrochromic Glass

- Suspended Particle Device (SPD) Glass

- Thermochromic Glass

- Micro-Blind Technology

- Other Technologies (Photochromic, Liquid Crystal on Silicon)

By Application

- Architectural & Construction (Commercial, Residential, Institutional)

- Automotive (Sunroofs, Side Windows, Rear Windows, Panoramic Roofs)

- Healthcare (Patient Rooms, Operating Suites, Examination Rooms)

- Aerospace & Defense (Aircraft Windows, Military Vehicles)

- Consumer Electronics (Displays, Smart Mirrors, Wearables)

- Other Applications (Marine, Rail, Retail Displays)

By End-Use

- Commercial (Offices, Hotels, Retail, Hospitality)

- Residential

- Industrial & Institutional

- Other End-Uses

By Distribution Channel

- Direct Sales (OEM and Specification-Based)

- Distributors & Dealers (Glazing Contractors, Automotive Suppliers)

- Online Retail

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Privacy Glass by Segments

- 2.1.2. Privacy Glass by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Privacy Glass Market Attractiveness Analysis, By Technology

- 2.2.3. Privacy Glass Market Attractiveness Analysis, By Application

- 2.2.4. Privacy Glass Market Attractiveness Analysis, By End-Use

- 2.2.5. Privacy Glass Market Attractiveness Analysis, By Distribution Channel

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Smart Building Revolution and Energy Efficiency Mandates Driving Architectural Adoption

- 3.1.2. Growing Privacy

- 3.1.3. Wellness

- 3.1.4. and Human-Centric Design Consciousness in Architecture and Interior Design

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Privacy Glass Market – By Technology

- 4.1. Technology Market Overview, By Technology Segment

- 4.1.1. Privacy Glass Market Revenue Share, By Technology, 2025 & 2035

- 4.1.2. Polymer Dispersed Liquid Crystal (PDLC) Glass

- 4.1.3. Privacy Glass Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Electrochromic Glass

- 4.1.7. Privacy Glass Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Suspended Particle Device (SPD) Glass

- 4.1.11. Privacy Glass Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Thermochromic Glass

- 4.1.15. Privacy Glass Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Micro-Blind Technology

- 4.1.19. Privacy Glass Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Other Technologies (Photochromic, Liquid Crystal on Silicon)

- 4.1.23. Privacy Glass Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Technology Market Overview, By Technology Segment

- Chapter 5. Privacy Glass Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Privacy Glass Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Architectural & Construction (Commercial, Residential, Institutional)

- 5.1.3. Privacy Glass Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Automotive (Sunroofs, Side Windows, Rear Windows, Panoramic Roofs)

- 5.1.7. Privacy Glass Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Healthcare (Patient Rooms, Operating Suites, Examination Rooms)

- 5.1.11. Privacy Glass Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Aerospace & Defense (Aircraft Windows, Military Vehicles)

- 5.1.15. Privacy Glass Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Consumer Electronics (Displays, Smart Mirrors, Wearables)

- 5.1.19. Privacy Glass Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Other Applications (Marine, Rail, Retail Displays)

- 5.1.23. Privacy Glass Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Privacy Glass Market – By End-Use

- 6.1. End-Use Market Overview, By End-Use Segment

- 6.1.1. Privacy Glass Market Revenue Share, By End-Use, 2025 & 2035

- 6.1.2. Commercial (Offices, Hotels, Retail, Hospitality)

- 6.1.3. Privacy Glass Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Residential

- 6.1.7. Privacy Glass Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Industrial & Institutional

- 6.1.11. Privacy Glass Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Other End-Uses

- 6.1.15. Privacy Glass Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End-Use Market Overview, By End-Use Segment

- Chapter 7. Privacy Glass Market – By Distribution Channel

- 7.1. Distribution Channel Market Overview, By Distribution Channel Segment

- 7.1.1. Privacy Glass Market Revenue Share, By Distribution Channel, 2025 & 2035

- 7.1.2. Direct Sales (OEM and Specification-Based)

- 7.1.3. Privacy Glass Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Distributors & Dealers (Glazing Contractors, Automotive Suppliers)

- 7.1.7. Privacy Glass Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Online Retail

- 7.1.11. Privacy Glass Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Distribution Channel Market Overview, By Distribution Channel Segment

- Chapter 8. Privacy Glass Market – Regional Analysis

- 8.1. Privacy Glass Market Overview, By Region Segment

- 8.1.1. Global Privacy Glass Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Privacy Glass Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Privacy Glass Market Revenue, By Technology, 2026 – 2035

- 8.1.4. Global Privacy Glass Market Revenue, By Application, 2026 – 2035

- 8.1.5. Global Privacy Glass Market Revenue, By End-Use, 2026 – 2035

- 8.1.6. Global Privacy Glass Market Revenue, By Distribution Channel, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Privacy Glass Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Privacy Glass Market Revenue, By Technology, 2026 – 2035

- 8.2.3. North America Privacy Glass Market Revenue, By Application, 2026 – 2035

- 8.2.4. North America Privacy Glass Market Revenue, By End-Use, 2026 – 2035

- 8.2.5. North America Privacy Glass Market Revenue, By Distribution Channel, 2026 – 2035

- 8.2.6. U.S. Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Privacy Glass Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Privacy Glass Market Revenue, By Technology, 2026 – 2035

- 8.3.3. Europe Privacy Glass Market Revenue, By Application, 2026 – 2035

- 8.3.4. Europe Privacy Glass Market Revenue, By End-Use, 2026 – 2035

- 8.3.5. Europe Privacy Glass Market Revenue, By Distribution Channel, 2026 – 2035

- 8.3.6. Germany Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Privacy Glass Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Privacy Glass Market Revenue, By Technology, 2026 – 2035

- 8.4.3. Asia Pacific Privacy Glass Market Revenue, By Application, 2026 – 2035

- 8.4.4. Asia Pacific Privacy Glass Market Revenue, By End-Use, 2026 – 2035

- 8.4.5. Asia Pacific Privacy Glass Market Revenue, By Distribution Channel, 2026 – 2035

- 8.4.6. China Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Privacy Glass Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Privacy Glass Market Revenue, By Technology, 2026 – 2035

- 8.5.3. The Middle-East and Africa Privacy Glass Market Revenue, By Application, 2026 – 2035

- 8.5.4. The Middle-East and Africa Privacy Glass Market Revenue, By End-Use, 2026 – 2035

- 8.5.5. The Middle-East and Africa Privacy Glass Market Revenue, By Distribution Channel, 2026 – 2035

- 8.5.6. Saudi Arabia Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Privacy Glass Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Privacy Glass Market Revenue, By Technology, 2026 – 2035

- 8.6.3. Latin America Privacy Glass Market Revenue, By Application, 2026 – 2035

- 8.6.4. Latin America Privacy Glass Market Revenue, By End-Use, 2026 – 2035

- 8.6.5. Latin America Privacy Glass Market Revenue, By Distribution Channel, 2026 – 2035

- 8.6.6. Brazil Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Privacy Glass Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Privacy Glass Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Privacy Glass Market: Company Market Share, 2025

- 9.2. Global Privacy Glass Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Saint-Gobain SA (Sage Electrochromics)

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. View Inc.

- 10.3. Gauzy Ltd.

- 10.4. AGC Inc.

- 10.5. Nippon Sheet Glass Co. Ltd. (Pilkington)

- 10.6. Gentex Corporation

- 10.7. Research Frontiers Inc.

- 10.8. Corning Incorporated

- 10.9. ChromoGenics AB

- 10.10. Halio Inc. (Kinestral Technologies)

- 10.11. Polytronix Inc.

- 10.12. Others.

- 10.1. Saint-Gobain SA (Sage Electrochromics)

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 37

List Of Tables

Tables No 1 to 51

Prominent Player

- Saint-Gobain SA (Sage Electrochromics)

- View Inc.

- Gauzy Ltd.

- AGC Inc.

- Nippon Sheet Glass Co. Ltd. (Pilkington)

- Gentex Corporation

- Research Frontiers Inc.

- Corning Incorporated

- ChromoGenics AB

- Halio Inc. (Kinestral Technologies)

- Polytronix Inc.

- Others

FAQs

The key players in the market are Saint-Gobain SA (Sage Electrochromics), View Inc., Gauzy Ltd., AGC Inc., Nippon Sheet Glass Co. Ltd. (Pilkington), Gentex Corporation, Research Frontiers Inc., Corning Incorporated, ChromoGenics AB, Halio Inc. (Kinestral Technologies), Polytronix Inc., Others.

Government regulations form one of the most impactful demand drivers in the privacy glass market that could exist on building energy codes, automotive glazing standards, healthcare facility design regulations and sustainability certification models that form a combination of both mandatory and incentive-based adoption channels. Regulatory pressure is putting pressure on dynamic glazing in glass-intensive building designs as the only glazing technology able to optimize the glazing area at the same time as the solar heat gain control required to meet nZEB requirements is creating regulatory pressure. Section 179D of the U.S. Inflation Reduction Act commercial building energy efficiency tax deductions, which have a maximum deduction of USD 5.00 per square foot of qualifying high-performance building system, provides attractive financial incentives to the adoption of smart glazing that is successfully reducing the time frame of commercial decision-making on privacy glass specifications. The automotive glazing regulations such as UNECE Regulation 43 in Europe and FMVSS 205 in the United States define minimum light transmittance requirements for driver and front passenger side windows that restrict privacy glass tinting in safety significant positions in the automotive industry and steer automotive smart glass usage towards sunroofs, rear windows, and panoramic roof systems where privacy tinting does not affect driver visibility. Design standards in healthcare facilities such as the U.S. FGI guidelines on the Design and Construction of Health Care Facilities and similar guidelines in EU member countries are increasingly recommending single-patient room amenities with sufficient privacy provisions – mandates that switchable glass can fulfill better than curtain-based technologies – which establish institutional design standards that tend to recommend increasingly privatizing the specification of glass in new healthcare constructions.

The pricing of privacy glass ranges an unprecedented spectrum between commodity switchable film of PDLC at USD 802.00 per square meter as an example of residential and small commercial retrofit uses and the factory-laminated unit interlacing of PDLC glass at USD 3007.00 per square meter as an example of commercial architectural use, to the high-end SPD glass at USD 5009.00 per square meter as an example of automotive and specialty use. These price differences represent real performance and functional differences – the energy management capability of electrochromic glass, the precision of graduated tinting, and the service life of 20+ years justify its premium versus the binary switching of PDLC and the 10-15 year film life of the latter – and make different market segments that are served by different technology platforms instead of direct rivalry. The most significant short-term price trend is the electrochromic glass price-downward curve that is expected to have installed prices of USD 500-USD 700 per square meter in 2030, when the technology will realize the energy savings of commercial buildings to be comparable in cost to the investment, and the price-saving valuation of privacy functionality will not be necessary to justify the investment. The increasing supply of PDLC film as an addressable mass-consumer retail product via online channels at USD 80.15 per square meter is establishing an addressable market that was previously absent in the 2026–2030 horizon of the global privacy glass market, the DIY residential retrofit market being potentially the largest growth rate opportunity in the privacy glass ecosystem.

According to current analysis, the market is expected to grow to an approximate USD 18.73 billion by 2035 as a result of the full commercial maturation of electrochromic glazing as a cost effective building energy management tool just reaching the installation cost parity with high-performance static glazing systems in large commercial building applications, mass-market use of smart glass in automotive applications, including smart privacy displays, augmented reality device privacy screens, and smart mirror applications, creating an enormous new institutional market, at a CAGR of 11.1% between 2026 and 2035.

It is projected that North America will have the highest revenue share over the initial forecast period, with the markets holding about 37% of the entire world market share in 2025 given the concentration of the major manufacturers of electrochromic glass in the United States, the highest density of commercial real estate investment in the major metropolitan markets in the United States, which is fueling the high levels of specification to premium glazing, the most commercialized automotive privacy glass market led by the mass-market deployment of smart roofs by Tesla and integration of premium models by BMW and Mercedes-Benz. Asia Pacific is estimated to reach the size of the North American market by the year 2032 due to its better CAGR pattern.

The region of Asia Pacific is expected to be the fastest growing with a CAGR of 14.2% in the forecast period, as China manufactures 9.6 million of the electric vehicles in 2023 amounting to 58% of the worldwide EV production and integrates smart glazing at increasing rates across its domestic EV model lines, premium commercial real estate booms in Shanghai, Singapore, and Mumbai, adopting international green building standards that demand the use of smart glazing, AGC and Nippon Sheet Glass of Japan perfect domestic automotive smart glass technology with increasing OEM adoption across Toyota and Honda vehicle programs, India’s rapidly expanding premium construction and automotive sectors are approaching the price thresholds at which privacy glass becomes commercially viable at mass market scale, and Chinese domestic PDLC glass manufacturers are developing competitive export capabilities that are expanding privacy glass market access across Southeast Asian and Belt and Road initiative construction markets.

It is projected that the Global Privacy Glass Market will achieve significant growth due to the global green building market set to reach USD 1.36 trillion by 2032 with 11.4% CAGR and increasing popularity of electrochromic smart windows as a specified cutting-edge sustainability feature in building energy codes, the global electric vehicle market predicted to reach 40 million units annually by 2030 with an engine incentive to create automotive smart glazing demand at an unprecedented scale, the cost reduction of PDLC film to USD 80- USD 20–30% building cooling energy reduction from electrochromic smart windows driving building energy code alignment with dynamic glazing performance, the global electric vehicle market projected to reach 40 million units annually by 2030 creating automotive smart glazing demand at unprecedented scale, Oak Ridge National Laboratory research demonstrating 11–15% EV driving range improvement from smart glass panoramic roofs providing EV-specific value beyond conventional automotive smart glass benefits, the global healthcare privacy glass segment growing at 13.6% CAGR driven by hospital construction expansion and infection control imperatives replacing textile curtains, PDLC film cost reductions to USD 80–USD 200 per square meter unlocking the enormous residential and retrofit market previously inaccessible to smart glass technologies, and the U.S. Inflation Reduction Act’s commercial building energy efficiency deductions creating direct financial incentives for electrochromic glazing specification in North American commercial construction.