Saudi Arabia Entertainment and Events Market Size, Trends and Insights By Event Type (Music Concerts & Festivals, Sports Events, Football Matches, Formula 1 & Motorsports, Combat Sports, Esports Tournaments, Cultural & Heritage Events, Corporate Events & Conferences, Exhibitions & Trade Shows, Theatre & Performing Arts, Others), By Venue Type (Indoor Venues, Outdoor Venues, Stadiums & Arenas, Convention Centers, Cultural Centers & Theatres, Others), By Revenue Source (Ticket Sales, Sponsorships & Partnerships, Food & Beverage, Merchandise & Retail, Media Rights, Others), By Audience Type (Family Entertainment, Youth & Young Adults, Corporate & Business, Tourists & International Visitors, Others), and By Region - Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Saudi Arabia |

| Largest Market: | Saudi Arabia |

Major Players

- Qiddiya Investment Company

- NEOM Entertainment

- Red Sea Global

- Live Nation Middle East

- Others

Reports Description

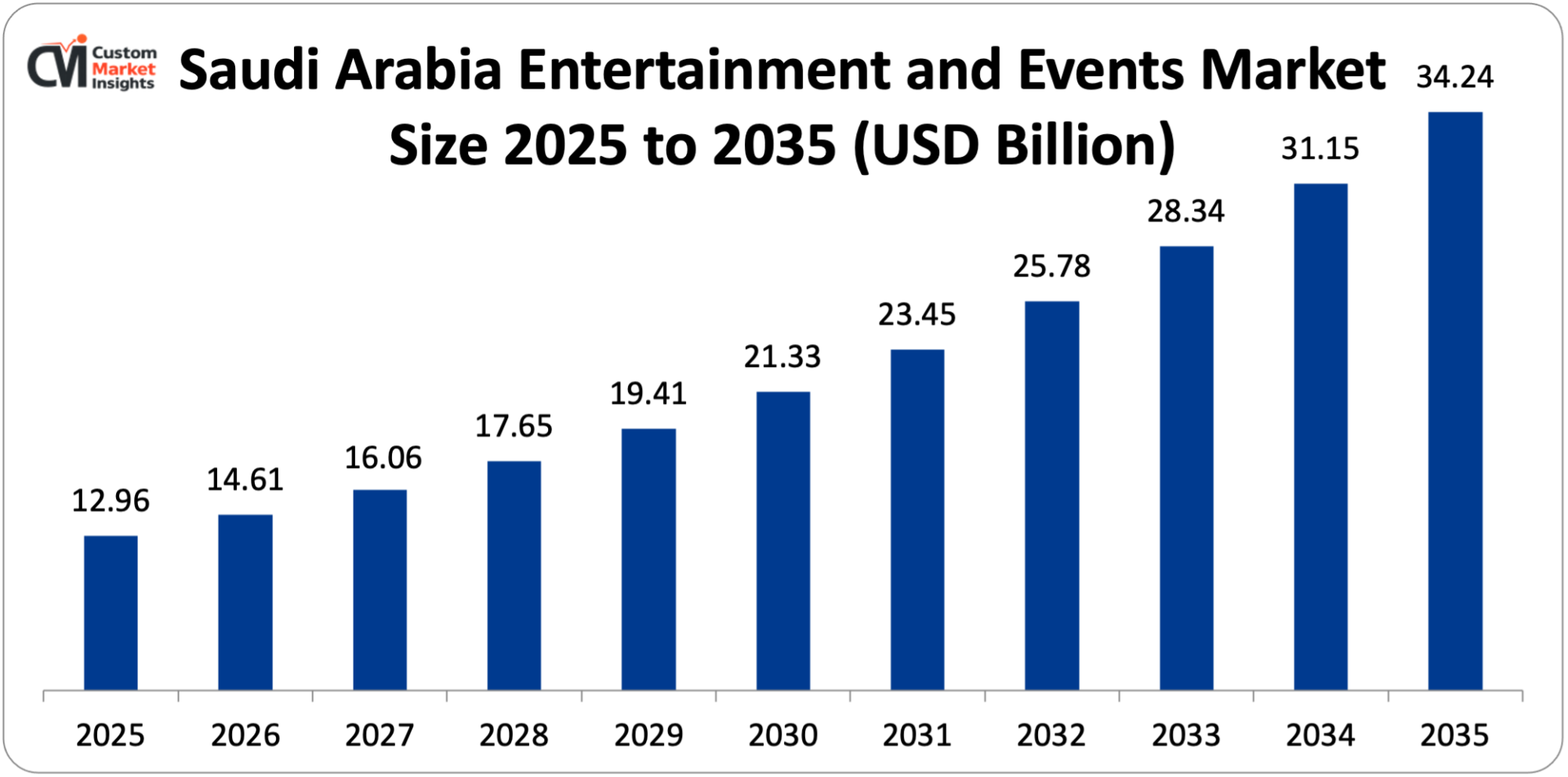

It is estimated that the market size of the entertainment and events market in Saudi Arabia will be USD 12.96 billion in 2025 and the market size will be increased to USD 14.61 billion in 2026 and about USD 34.24 billion in 2035 with an annual CAGR of 12.8% between the years 2026 and 2035.

The market is expanding due to the Vision 2030 strategic plans reshaping the entertainment industry, the massive investment of government in entertainment infrastructure and giga-projects, the escalating youth population with the growing disposable income, cultural reforms enabling concerts, cinema, and mixed-gender events, and the establishment of Saudi Arabia as a regional entertainment and tourism center.

Market Highlight

- Riyadh was the Saudi Arabia entertainment and events market leader that held a 42% market share in 2025.

- The Western Region (Jeddah) will be increasing by 14.6% during the years 2026-2035.

- By the type of event, the music concerts and festivals segment had acquired more than 28% of the market segment in 2025.

- Sport venue type of stadiums and arenas segment will achieve a maximum 15.2% CAGR 2026-2035.

- Revenue source-wise Ticket sales segment grabbed 38% of the market share in 2025.

- By types of audience, youth and young adults would enjoy a market share of 48% in 2025.

- In 2024 Saudi Arabia will host more than 8,500 entertainment events featuring 85 full-size international concerts, 240 sports tournaments, and 1,200+ local cultural festivals with an attendance of 68 million.

Significant Growth Factors

- Vision 2030 Transformation and Quality of Life Program:

The Vision 2030 blueprint of Saudi Arabia identifies entertainment and cultural activities as the core pillars of economic diversification and social change that will ensure unprecedented investment and regulatory reforms will establish the world’s fastest-growing entertainment market. Among the 13 Vision 2030 realization programs is the Quality of Life Program which has allocated SAR 240 billion (USD 64 billion) to entertainment infrastructure, cultural development and tourism projects up to 2030.

The General Entertainment Authority (GEA) is an institution formed in 2016 that organizes and licenses entertainment with annual budgets of over SAR 12 billion and hosts 8,500+ events in 2024 as compared to virtually no international concerts being held until 2018. With the opening of entertainment industries that were previously banned, this has opened up completely new markets with the cinema industry contributing SAR 1.8 billion in 2024 with 560 screens spread over 85 multiplexes run by AMC, VOX, and Muvi and serving 28 million moviegoers since the 2018 ban lift. In 2024, music concerts with international artists like Bruno Mars, BTS, Metallica, and Andrea Bocelli drew 2.4 million people to the events, and their ticket sales amounted to more than SAR 3.2 billion.

The goal of the government to expand the household expenditure on entertainment to 6% as opposed to 2.9 in 2016 translates to SAR 95 billion more spending by the households per year considering the projected growth in household incomes. Vision 2030 will establish Saudi Arabia as one of the top 10 world entertainment destinations with the targeted number of 100 million international visitors annually by 2030 with half of them engaging in cultural and entertainment tourism activities. In 2024 the Cultural Development Fund made SAR 2.4 billion in grants and investments in 340 cultural and entertainment projects, including the development of heritage sites, performing arts venues, and start ups in the creative industry. The liberalization of regulations to permit mixed-gender events, extend the hours of entertainment up to 3 AM, and make the application of the event licensing process easier made the approval process drop to 4-8 weeks, which made it easy to expand the market.

- Demographic Dividend and Rising Youth Population:

The youthful and digitally engaged Saudi Arabia with nearly 70% of the total population under the age of 35 and a median age of 31.8 years generates gigantic demand for various entertainment experiences that are in line with global trends as well as cultural considerations. By 2024 the population of the kingdom was 36.4 million, of which 63% are Saudi citizens and 37% expatriates, with a growth rate of 2.1 every year and an estimated 42 million by 2030. The young people aged 15-34 constitute 42% of the total population (15.3 million), and this group has significantly been involved in the entertainment industry, with 78% attending at least one paid entertainment event in 2024 compared to 23% in 2017.

The emerging levels of education with 68% of the young people achieving secondary school education and 34% attaining university education, are associated with the emergence of cultural inclination and a readiness to spend on experiential entertainment. The number of women who attended entertainment activities grew by a factor of 46 times between pre-2018, when it was insignificant and 2024 when it reached 46% of the overall attendees, which positively impacts the market that can be addressed and provides a family-friendly entertainment concept. By 2024, the participation rate of women in the labor force had reached 35.6% (compared to 17% in 2016), which raised the income levels of households and buying power among women to spend on entertainment. The per capita disposable income increased to SAR 89,400 in 2024 compared to SAR 71,200 in 2018 with the entertainment expenditure moving to SAR 5,340 per year against SAR 2,100 in 2018. Digital marketing, mobile ticketing, and social sharing facilitated by social media penetration of 99% among young people and smartphone adoption of 97% make viral event marketing possible, with Instagram, Snapchat, and TikTok platforms having 72% influence on the decision to attend an event by under-30 year-old audiences.

- Mega Entertainment Destinations and Giga-Projects:

The construction of entertainment megaprojects such as Qiddiya, NEOM, the Red Sea Project and Diriyah Gate will turn Saudi Arabia into integrated entertainment resorts that combine theme parks, cultural spaces, sports venues, and hospitality facilities. Located in the Riyadh area as the Capital of Entertainment, Sports and the Arts, Qiddiya is an SAR 150 billion investment construction of 366 km², consisting of Six Flags and a water park theme park to a water park, motorsports circuits to sports stadiums, and a performing arts district to sports stadiums, which will be constructed in phases between 2025-2030. By 2030, the project is expected to bring 17 million visitors annually which will create 55000 jobs and contribute 55000 to the GDP in the form of revenue.

Phase 1 facilities such as 45,000 seat stadium, multi-purpose arena and initial theme park space went live in 2024, used in hosting esports tournaments, Formula 1 exhibition races, and music festivals. Entertainment aspects of NEOM comprise integrated cultural venues in THE LINE, Trojena with a 365 days mountain resort, skiing and adventure sports; and Sindalah, a luxury island with a marina, beach clubs, and event amenities aiming to bring 2 million visitors to the venue every year by 2030. Boulevard Riyadh City is a SAR 6 billion seasonal entertainment park open October-March with 15 themed zones, 200 restaurants, and 30 entertainment attractions that bring 12 million visitors with SAR 4.8 billion in visitor spending. The 50 resort islands and six inland locations of the Red Sea Project include cultural experiences, underwater dining and experiential entertainment aimed at ultra-luxury groups with an average of SAR 22,000 per visit, while the number is estimated to be 1 million visitors yearly. As part of preserving the UNESCO World Heritage site At-Turaif, the Diriyah Gate development integrates cultural museums, performing arts, boutique hotels and restaurants to form authentic Saudi cultural entertainment destinations with 27 million visitors per year by 2030.

- International Partnerships and Major Event Hosting:

The international alliances with international entertainment brands, sports bodies and event organizers allow Saudi Arabia to be the prime destination as a host to mega events and also send the skills involved in building domestic entertainment industry capacities. In 2024, the kingdom hosted 240 large-scale sporting events such as the Saudi Arabian Grand Prix (Formula 1), which had an attendance of 320,000 over the weekend of the event, LIV Golf tournaments with a purse of USD 405 million and WWE events with a crowd of 65,000 and above. The acquisition of international football stars such as Cristiano Ronaldo, Neymar, Karim Benzema, and N’Golo Kanté by the Saudi Pro League boosted the profile of the league and the sales of broadcast rights rose to 140 countries and the number of fans who attended the matches rose by 156% to 1.8 million in the 2023-2024 season.

Partnering with WWE: Collaborating over the course of several years, the company should have premium live events, integration of the Riyadh Season festivities, and the possibility of a permanent WWE Performance Center to make Saudi Arabia the wrestling center of the Middle East. Resident show development agreements with Cirque du Soleil, the development of Qiddiya theme park with Six Flags, and the expansion of cinema with AMC Theatres will utilize expertise across the world and provide 45,000 Saudis with employment and training opportunities in the entertainment industry by 2030. The General Entertainment Authority collaborated with Live Nation, AEG, and local promoters to host 85 international concerts in 2024 with such artists as Beyoncé, Ed Sheeran, and Imagine Dragons, putting Saudi Arabia on international touring lists. Riyadh Season as a flagship entertainment programs was initiated in 2019 with 14 different zones, 8,000 events in 6 months with an investment of SAR 18 billion, and a projected 15 million visitors with an average spending of SAR 2,400. Investments in gaming and esports such as the Gamers8 festival with a USD 45 million prize pool, collaboration with ESL Gaming and BLAST Premier, and the creation of special esports arenas aim at USD 13.3 billion of the gaming market involvement by 2030.

What are the Major Advances Changing the Saudi Arabia Entertainment and Events Market Today?

- Digital Transformation and Smart Entertainment Platforms:

Digital infrastructure, mobile applications, and integrated platforms are up to the new generation of discovery of events, ticketing, payment, and enhancement of the experience and yield valuable data to optimize operations and marketing. The Nusk platform is a ticketing platform created by Sela (Saudi Entertainment Ventures) to centralize the majority of big entertainment events and pay 18.4 million transactions in 2024 with an average booking time of 90 seconds to 8 minutes through simplified interfaces and payment systems.

The use of Apple Pay, STC Pay, and Mada to make payments allows frictionless transactions, and online transactions are 89% of ticket sales compared to 34% of cash/credit in 2019. Dynamic pricing software maintains price changes in response to demand, time of the event, and customer types, boosting revenue per event by 18-26% and maximizing attendance using variable pricing that does not compromise access. Virtual reality tours around the venue help customers see where they will sit before making a purchase, which will decrease customer dissatisfaction with their purchases by 42% and increase the sale of premium seats by 23%. Recommendation engines that are powered by artificial intelligence analyzing user behavior, past attendance, and preferences recommend events that are highly relevant and attendance to cross-category events increases by 31% as customers learn about new forms of entertainment.

Facial recognition and biometric entry systems that have been implemented in 12 large venues save on entry processing time from 3-4 minutes per attendee to 30-45 seconds per attendee to enhance the crowd flow and security and provide contactless experiences. IoT sensors and mobile device-tracking real-time crowd management systems improve venue density, streamline the entry/exit flows, and avoid overcrowding, and implementations at Boulevard Riyadh City have led to a reduction in security incidents (68). The integration of digital content using augmented reality produces improved live experiences, and AR filters, interactive games, and social media integration add to the audience engagement and event virality, with each major event producing 3.2 million social media impressions.

- Localized Content and Cultural Entertainment Formats:

Creation of genuine Saudi cultural entertainment that combines heritage conservation with new presentation forms can be offered as unique offerings that distinguish the kingdom’s entertainment offer without any disrespect to the cultural values. Theatrical performances in Arabic that include Saudi tales, historical accounts and contemporary themes received 840,000 viewers in 2024 in productions at King Fahd Cultural Center, Ithra (King Abdulaziz Center of World Culture), and new-purpose theaters. In 2024, the Saudi Film Festival supported the local creative industry through Film Commission grants valued at SAR 280 million, showcasing 65 Saudi-produced films as compared to 8 films in 2019.

Cultural festivals that exalt the Saudi heritage such as the Janadriyah National Festival, the AI-Jenadriyah Heritage and Cultural Festival and regional heritage celebrations brought 8.4 million visitors in 2024, balancing the traditional crafts, cuisine, music, and tales with the modern presentation technologies. Modern Saudi music personalities such as Mohammed Abdo, Abdul Mazed Abdullah, and upcoming musicians are holding concerts at special music venues that are sold out, and Saudi music streaming is now rising 340% between 2020 and 2024. Saudi culture is integrated into family entertainment parks and theme parks and the Via Riyadh area of Riyadh Season is a replica of historic Najd architecture with 200 dining and retail shops bringing in SAR 1.2 billion in a 6-month season. Arabic comedy programs and stand-up of Saudi comedians have drawn 420,000 people in 2024, and there are special comedy clubs in Riyadh, Jeddah, and AI-Khobar. The combination of Islamic values, gender-oriented entertainment formats and family-friendly content will guarantee cultural equivalence but offer a variety of choices, as family entertainment events take up 68% of overall events, compared to 21% for the youth-only format.

- Sustainable Event Management and Green Entertainment:

Environmental sustainability programs that include renewable energy, waste minimization, water saving and carbon offset schemes make the Saudi entertainment industry the leader in terms of sustainable event management in the region. Big projects such as King Fahd International Stadium, King Abdullah Sports City, and the new Qiddiya facilities include solar panels to generate 30-45% of their operating electric power, and the solar systems at Boulevard Riyadh City generate 12 MW capacity to counter 8,400 tons of CO₂ per year. The outdoor event venues have water recycling systems in use that treat and use gray water as landscape irrigation in place of drinking water, conserving 40-55%, which is important in the water-deprived environment where per capita water use is at 82 m³ per year, one of the lowest in the world. Recycling waste and major-event segregation programs recorded a 48% diversion rate in 2024, with Riyadh Season running an extensive recycling program of 2,850 tons of recyclable waste including plastics and metals as well as organics.

Single use plastic was substituted by biodegradable and compostable material in food service, preventing 72 out of 100 major events each year and saving 1,240 tons annually of plastic. Verified emission reduction credits bought under the carbon offset programs offset the emissions caused by the events where Saudi Entertainment Ventures, which is planning to achieve carbon-neutral operations by 2030 will need to offset the estimated 280,000 tons of CO₂ equivalent of emissions every year. Event logistics and attendee transportation are also run by electric and hybrid vehicles, which makes the fleet reduce the level of emissions, and Boulevard Riyadh City used 45 electric shuttle buses that removed 580 tons of CO₂ in comparison with the diesel counterparts. Permanent entertainment buildings such as the LEED Gold standard of new Qiddiya buildings are green certified buildings that guarantee energy efficiency and sustainable materials and environmental performance over the lifecycles of the facilities.

- Immersive and Experiential Entertainment Technologies:

The newest technologies such as virtual reality, augmented reality, projection mapping and interactive installation offer immersion that distinguishes Saudi entertainment services and find customers who enjoy working with technological devices. In 2024, Noor Riyadh, the annual light art festival, showcased 190 installations by 130 artists throughout 20 sites with a total attendance of 3.2 million people, making Riyadh the Light art capital of the world and estimating the economic impact of the event on 850 million SAR by tourism and hospitality expenditures. Historical sites, such as Diriyah, AIUla, and Edge of the World, are being transformed into a storytelling experience with projection mapping spectacles, with the Forever is Now installation at AIUla drawing 95,000 visitors at SAR 250-450.

Entertainment destinations also have virtual reality zones that provide immersive gaming experiences, education, and adventure, with VR Park Riyadh having 35 attractions on 7,000 m² of space earning SAR 42 million a year in revenue with 280,000 visitors per year. Touch screens, motion sensors, and AR overlays used in interactive museums at such institutions as the National Museum, Ithra, and future museums in Diriyah Gate turn a flat display into an interactive experience and boost the average visit time, which grew to 142 minutes long instead of 68 minutes. Hologram shows from virtual performers, past personalities, and fantasy characters provide innovative forms of entertainment that cannot be achieved through conventional performances, and the hologram concerts and 5G network coverage have earned 40-65% premium ticket prices in 2024 (78% of urban locations with 5G coverage). Combining theatrical performance, projection, and multi-sensory experiences, immersive dining is appealing to more high-income people who are able to spend SAR 800-2,400 per person on unique culinary entertainment fusion experiences.

Category Wise Insights

By Event Type

Why Music Concerts & Festivals Lead the Market?

The largest market share of 28% in 2025 is dominated by music concerts and festivals because they offer unprecedented access to international artists never seen before, huge government investment in music festival infrastructure, and the preference of the youth demographic to enjoy music live. In 2024, the sector had a total of SAR 13.6 billion in 85 international concerts, 420 regional artist shows and 15 large scale music festivals with ticket sales amounting to SAR 680 million with 730,000 people over 4 days. Government subsidies in the form of international artist fees of SAR 7.5 million-95 million to the highest achievers make sure that the prices of tickets are kept at a competitive SAR 450-1 200 on average compared with comparable concerts in Dubai or Abu Dhabi. Specific music venues such as the 15,000 seat Mohammed Abdo arena in Riyadh and the 20,000 seat venue proposed at Qiddiya present state-of-the-art acoustics and production facilities. The format of music festivals incorporates various genres, food experiences, and cultural activities as destination events in 3 days, and Soundstorm 2024 includes 200+ artists on 8 stages that have drawn international attendees from 73 countries.

By Venue Type

Why Stadiums & Arenas Show Fastest Growth?

The highest CAGR of 15.2% in the period of 2026-2035 is exhibited by the stadiums and arenas because of the enormous investment in the infrastructure construction of world class facilities to host sports, concerts and mega events. Saudi Arabia has invested SAR 42 billion in building stadiums and arenas 2020-2024, which will consist of 12 large stadiums such as the 92,000-capacity King Salman Stadium in Riyadh currently under construction to be completed in 2027, the 45,000-capacity Qiddiya Stadium to be opened in 2024, and the refurbished King Fahd Stadium to host the AFC Asian Cup 2027. Multi-purpose arenas allow a wide array of programming to make optimum use, and in the case of Riyadh, the new 25,000-seat arena will feature 140 events in 2024 including concerts, WWE wrestling, basketball, and awards ceremonies that will contribute SAR 580 million towards venue revenue. Premium seating and hospitality suites cost SAR 5,000-45,000 per event, bringing in 35-42% of venue income at 12-18% capacity, and corporate packages of Saudi Pro League season cost SAR 380,000. The international design standards and the latest technologies such as retractable roofs, sophisticated lights, and immersive sound systems allow the conduct of high profile worldwide competitions as FIFA, AFC, and Formula 1 approved competitions are attracted.

By Revenue Source

Why Sponsorships Drive Significant Revenue?

Sponsorships and partnerships contribute to 32% of market revenue, and this indicates the strategic alignment of Saudi corporations with Vision 2030 and massive marketing budgets channeled towards entertainment properties. The total amount of sponsorship expenditure was SAR 15.6 billion in 2024, and Saudi Aramco, STC, Saudi Airlines, and AI Rajhi bank are some of the major sponsors. Major event title sponsorships cost between SAR 45-180 million/year, with Diriyah Season sponsoring Riyadh Season for SAR 120 million giving it the right to name and integrate its brand and the ability to have exclusive activations.

The regional brands use entertainment platforms that have access to a mass audience, and the average sponsorship ROI is 4.8:1 based on brand awareness, sales uplift, and consumer engagement metrics. Entertainment properties provide a wide range of sponsorship packages, such as SAR 500,000 presenting sponsors and SAR 75+ million title partners, and can be accessed by anyone, but as much as possible, maximize revenue. Activation rights permit sponsors to design branded experiences; sampling of products and opportunities for consumer engagement and activations create an average of SAR 2.8 million in extra value related to media exposure per big occasion.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 14.61 billion |

| Projected Market Size in 2035 | USD 34.24 billion |

| Market Size in 2025 | USD 12.96 billion |

| CAGR Growth Rate | 12.8% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Event Type, Venue Type, Revenue Source, Audience Type and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

City Wise Analysis

Riyadh Market Leadership

Riyadh is the market leader with a 42% share worth SAR 20.4 billion in 2025, due to its capital city status, government ministry concentration, highest population of 8.3 million people and status as the main entertainment centre of Vision 2030. It has a total of 3,200+ entertainment events every year such as Riyadh Season (15 million visitors), Boulevard Riyadh City (12 million visitors), and 45 major international concerts. Infrastructure projects are over SAR 85 billion plus the Qiddiya development, King Salman stadium, the new arena complex and the King Abdulaziz historical center expansion. The 2024 version of Riyadh Season was a 6-month event that created SAR 18 billion in the economy and comprised 14 zones that produced hospitality, dining, and retail other than ticket sales. In 2024, the employment in entertainment in the city was 42,000, which is expected to surpass 95,000 by 2030 to offer career opportunities in the fields of event management, hospitality, technical production, and creative services. Riyadh averages household expenditure on entertainment amounting to SAR 7,200/year (35% above the national average), indicating a higher income and increased access to events.

Jeddah and Western Region Growth

The second-largest city in Saudi Arabia, with 4.7 million people, Jeddah, has been found to have the highest growth rate in the region, with 14.6% CAGR due to Red Sea coastal position, cultural regional entrance, and tourism infrastructure to accommodate both local and foreign tourists. In 2024, the city received SAR 11.8 billion of waterfront events, cultural festivals, concerts located at King Abdullah Sports City, and heritage activations in historic AI-Balad district entertainment revenue. Jeddah Season introduced in 2019 recorded 8.5M visitors in the 2024 season, with beachfront entertainment areas, water sports, dining, and concerts bringing SAR 6.4 billion to the economy.

The location of the Red Sea Project provides Jeddah an opportunity to serve as a port of luxury tourism and entertainment, and cultural events, water-based entertainment and heritage experiences are being integrated. A new cultural destination, AIUla accrued SAR 850 million by drawing 340,000 attendees to the Winter at Tantora festival, permanent art installations, and experiences of the heritage sites, with projections of 2 million visitors per year by 2030. Jeddah’s entertainment infrastructure has refurbished King Abdullah Sports City, which hosts the Formula 1 Saudi Arabian Grand Prix with 320,000 visitors throughout the weekend racing event, which has a local economic impact of SAR 1.2 billion in the form of hospitality, dining, and tourism spending.

Eastern Province Market Dynamics

The Eastern Province, with Dammam and AI-Khobar with a total population of 2.8 million, enjoys closeness to Bahrain and a successful oil industry labour force as well as expatriate groups that provide a wide range of entertainment needs. In 2024, the region drove SAR 8.4 billion in entertainment businesses, and the key areas were family entertainment facilities, dining entertainment, and corporate events.

King Fahd international stadium in Dammam is used for playing Saudi Pro League, concerts, and cultural events with 2024 use projected to rise by 89% compared to 2019 due to diversified programming. The growth of the entertainment sector of Eastern Province is aimed at expatriate and cross-border viewers, where 30% of the event visitors are based in Bahrain and other GCC nations due to a growing number of products and services in Saudi Arabia and competitive prices. Corniche waterfront construction within Dammam and AI-Khobar includes entertainment precincts comprising dining, leisure and entertainment, and event facilities that receive 15.4 million visitors in a year.

Emerging Entertainment Cities

AIthough mostly pilgrimage areas that receive 20 million religious visitors every year, Mecca and Medina create complementary cultural and family entertainment to the residents and visitors in the off-pilgrimage seasons. The cities drove SAR 4.2 billion in aggregate entertainment earnings in 2024, most of which was in family entertainment businesses, cultural museums, and culinary experiences, all based on religious tourism facilities.

The northwestern areas of Tabuk and AIUla develop into heritage and nature based entertainment destinations, where cultural festivals, adventure tourism, and experiences of historical sites are all being invested in to serve both domestic and international cultural tourists. The mountain climate and natural sightseeing are used in the southern cities such as Abha and Khamis Mushait to provide seasonal entertainment to the 2.4 million domestic tourists who come year-round during summer when the heat in the central areas is too intense.

Top Players in the Market

- General Entertainment Authority (GEA)

- Saudi Entertainment Ventures (SEVEN)

- Qiddiya Investment Company

- NEOM Entertainment

- Red Sea Global

- Live Nation Middle East

- MDLBEAST

- VOX Cinemas Saudi Arabia

- AMC Cinemas Saudi Arabia

- Muvi Cinemas

- AI Hokair Group

- Time Entertainment

- Others

Key Developments

- In February 2025: Qiddiya Investment Company declared that Phase 1 infrastructure such as a 45,000 seater stadium, a Six Flags theme park preview center, and a motorsport circuit, with an estimated two million visitors in the first year, will be completed in Q2 2025.

- In February 2025: Saudi Entertainment Ventures (SEVEN) obtained SAR 8.5 billion in financing through the Public Investment Fund to build 21 entertainment centers in 14 cities to generate 35,000 jobs, aiming to receive 45 million visitors annually by 2028.

- In December 2025: General Entertainment Authority declared Riyadh Season 2025-2026 version including SAR 22 billion and will cover 18 zones and 10,000-plus occasions within 7 months, and will aim to attract 20 million and SAR 24 billion in economic effect and outcomes, respectively.

These strategic moves have enabled the entities to consolidate their market positions, expand entertainment products, improve the infrastructure capacity, and exploit growth opportunities in the fast-growing Saudi Arabian entertainment and events market.

The Saudi Arabia Entertainment and Events Market is segmented as follows:

By Event Type

- Music Concerts & Festivals

- Sports Events

- Football Matches

- Formula 1 & Motorsports

- Combat Sports

- Esports Tournaments

- Cultural & Heritage Events

- Corporate Events & Conferences

- Exhibitions & Trade Shows

- Theatre & Performing Arts

- Others

By Venue Type

- Indoor Venues

- Outdoor Venues

- Stadiums & Arenas

- Convention Centers

- Cultural Centers & Theatres

- Others

By Revenue Source

- Ticket Sales

- Sponsorships & Partnerships

- Food & Beverage

- Merchandise & Retail

- Media Rights

- Others

By Audience Type

- Family Entertainment

- Youth & Young Adults

- Corporate & Business

- Tourists & International Visitors

- Others

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Saudi Arabia Entertainment and Events by Segments

- 2.1.2. Saudi Arabia Entertainment and Events by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Saudi Arabia Entertainment and Events Market Attractiveness Analysis, By Event Type

- 2.2.3. Saudi Arabia Entertainment and Events Market Attractiveness Analysis, By Venue Type

- 2.2.4. Saudi Arabia Entertainment and Events Market Attractiveness Analysis, By Revenue Source

- 2.2.5. Saudi Arabia Entertainment and Events Market Attractiveness Analysis, By Audience Type

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Vision 2030 Transformation and Quality of Life Program

- 3.1.2. Demographic Dividend and Rising Youth Population

- 3.1.3. Mega Entertainment Destinations and Giga-Projects

- 3.1.4. International Partnerships and Major Event Hosting

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Saudi Arabia Entertainment and Events Market – By Event Type

- 4.1. Event Type Market Overview, By Event Type Segment

- 4.1.1. Saudi Arabia Entertainment and Events Market Revenue Share, By Event Type, 2025 & 2035

- 4.1.2. Music Concerts & Festivals

- 4.1.3. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Sports Events

- 4.1.6.1. Football Matches

- 4.1.6.2. Formula 1 & Motorsports

- 4.1.6.3. Combat Sports

- 4.1.6.4. Esports Tournaments

- 4.1.7. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Cultural & Heritage Events

- 4.1.11. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Corporate Events & Conferences

- 4.1.15. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Exhibitions & Trade Shows

- 4.1.19. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Theatre & Performing Arts

- 4.1.23. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1.26. Others

- 4.1.27. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 4.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.29. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Event Type Market Overview, By Event Type Segment

- Chapter 5. Saudi Arabia Entertainment and Events Market – By Venue Type

- 5.1. Venue Type Market Overview, By Venue Type Segment

- 5.1.1. Saudi Arabia Entertainment and Events Market Revenue Share, By Venue Type, 2025 & 2035

- 5.1.2. Indoor Venues

- 5.1.3. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Outdoor Venues

- 5.1.7. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Stadiums & Arenas

- 5.1.11. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Convention Centers

- 5.1.15. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Cultural Centers & Theatres

- 5.1.19. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Others

- 5.1.23. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Venue Type Market Overview, By Venue Type Segment

- Chapter 6. Saudi Arabia Entertainment and Events Market – By Revenue Source

- 6.1. Revenue Source Market Overview, By Revenue Source Segment

- 6.1.1. Saudi Arabia Entertainment and Events Market Revenue Share, By Revenue Source, 2025 & 2035

- 6.1.2. Ticket Sales

- 6.1.3. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Sponsorships & Partnerships

- 6.1.7. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Food & Beverage

- 6.1.11. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Merchandise & Retail

- 6.1.15. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Media Rights

- 6.1.19. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Others

- 6.1.23. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Revenue Source Market Overview, By Revenue Source Segment

- Chapter 7. Saudi Arabia Entertainment and Events Market – By Audience Type

- 7.1. Audience Type Market Overview, By Audience Type Segment

- 7.1.1. Saudi Arabia Entertainment and Events Market Revenue Share, By Audience Type, 2025 & 2035

- 7.1.2. Family Entertainment

- 7.1.3. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Youth & Young Adults

- 7.1.7. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Corporate & Business

- 7.1.11. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Tourists & International Visitors

- 7.1.15. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Others

- 7.1.19. Saudi Arabia Entertainment and Events Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Audience Type Market Overview, By Audience Type Segment

- Chapter 8. Saudi Arabia Entertainment and Events Market – Regional Analysis

- 8.1. Saudi Arabia Entertainment and Events Market Overview, By Region Segment

- 8.1.1. Global Saudi Arabia Entertainment and Events Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Saudi Arabia Entertainment and Events Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Saudi Arabia Entertainment and Events Market Revenue, By Event Type, 2026 – 2035

- 8.1.4. Global Saudi Arabia Entertainment and Events Market Revenue, By Venue Type, 2026 – 2035

- 8.1.5. Global Saudi Arabia Entertainment and Events Market Revenue, By Revenue Source, 2026 – 2035

- 8.1.6. Global Saudi Arabia Entertainment and Events Market Revenue, By Audience Type, 2026 – 2035

- 8.1. Saudi Arabia Entertainment and Events Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Saudi Arabia Entertainment and Events Market: Company Market Share, 2025

- 9.2. Global Saudi Arabia Entertainment and Events Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. General Entertainment Authority (GEA)

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Saudi Entertainment Ventures (SEVEN)

- 10.3. Qiddiya Investment Company

- 10.4. NEOM Entertainment

- 10.5. Red Sea Global

- 10.6. Live Nation Middle East

- 10.7. MDLBEAST

- 10.8. VOX Cinemas Saudi Arabia

- 10.9. AMC Cinemas Saudi Arabia

- 10.10. Muvi Cinemas

- 10.11. AI Hokair Group

- 10.12. Time Entertainment

- 10.13. Others.

- 10.1. General Entertainment Authority (GEA)

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 41

List Of Tables

Tables No 1 to 2

Prominent Player

- General Entertainment Authority (GEA)

- Saudi Entertainment Ventures (SEVEN)

- Qiddiya Investment Company

- NEOM Entertainment

- Red Sea Global

- Live Nation Middle East

- MDLBEAST

- VOX Cinemas Saudi Arabia

- AMC Cinemas Saudi Arabia

- Muvi Cinemas

- AI Hokair Group

- Time Entertainment

- Others

FAQs

The key players in the market are the General Entertainment Authority (GEA), Saudi Entertainment Ventures (SEVEN), Qiddiya Investment Company, NEOM Entertainment, Red Sea Global, Live Nation Middle East, MDLBEAST, VOX Cinemas Saudi Arabia, AMC Cinemas Saudi Arabia, Muvi Cinemas, Al Hokair Group, Time Entertainment, Others.

Regulations have a critical role in the form of General Entertainment Authority licensing conditions, creating a vision of safety, cultural suitability and operational standards for 8,500+ annual events, Vision 2030 policies that offer regulatory clarity and investment incentives to achieve SAR 180 billion in annual entertainment investments, cultural guidelines that help ensure that entertainment conforms to Saudi values whilst allowing previously restricted activities such as concerts and cinemas, and streamlined licensing that reduces approval duration from 6-9 months down to 4-8 weeks, facilitating rapid market growth whilst keeping a check on quality and compliance with cultural norms.

The market has been projected to take shape of about USD 34.24 billion by 2035 with a growth of 12.8% CAGR between 2026-2035 due to the ongoing implementation of the vision 2030, mega-project developments such as Qiddiya and NEOM entertainment elements, hosting of international events, the development of the tourism industry to 100 million visitors per year by 2030 with 50% participation of the entertainment industry, and the maturity of the domestic entertainment industry into a creating sustainable ecosystem beyond government-subsidized initiatives.

The capital city status and focus on concentrating entertainment initiatives in Riyadh have Riyadh maintaining its leadership with a 42% share worth SAR 20.4 billion in 2025, with the largest population of 8.3 million as a source of a substantial domestic audience, the Qiddiya entertainment destination with 17 million visitors by 2030, the Riyadh Season flagship event with 15 million visitors generating SAR 18 billion in economic impact, and SAR 85+ billion invested in stadiums, arenas, and entertainment districts creating a world-class venue ecosystem.

Western Region, with the focus on Jeddah, has the highest growth rate of 14.6% CAGR between 2026-2035, due to the Red Sea coast position, with its position allowing unique waterfront entertainment, nearness to the Red Sea Project, with the attraction of luxury tourists and cultural tourists, the Jeddah Season, which creates SAR 6.4 billion in economic activity, 8.5 million visitors, and its historical importance as a gateway to the cultural realm, where SAR 28 billion in infrastructure investment is made in entertainment facilities, supported by SAR 28 billion infrastructure investment in entertainment venues and cultural districts.

Saudi Arabia Entertainment and Events Market This market is growing due to initiatives relating to Vision 2030, which spend SAR 240 billion on entertainment infrastructure, demographic growth (70% of the population is under 35, 42% are under 15-34), cultural transformation (enabling concerts, cinemas, and mixed-gender events), mega-project investment (Qiddiya, SAR 150 billion), and positioning the kingdom as an entertainment destination (disposable income is projected to grow by increasing the spend on entertainment, with per capita entertainment spending increasing from SAR 2,100 in 2018 to SAR 5,340 in 2024).