Vacuum Skin Packaging Market Size, Trends and Insights By Type (Flat Skin Packaging, Hanging Skin Packaging, Skin-on-Tray, Skin Pouches, Skin-on-Blister), By Material Type (PVC, PET, PE, PP, Multi-Layer Films, Bio-Based & Compostable Materials), By End-Use Industry (Food, Meat, SeafoodDairy, Ready-to-Eat Meals, Medical & Healthcare, Consumer Goods, Industrial Components, Retail & E-commerce), By Packaging Function (Protection, Shelf-Life Extension, Tamper-Evidence, Display Enhancement), By Process Technology (Thermoforming, Manual, Semi-Automatic, Fully Automatic), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- Sealed Air Corporation

- Amcor

- Winpak Ltd.

- Linpac Packaging

- Others

Reports Description

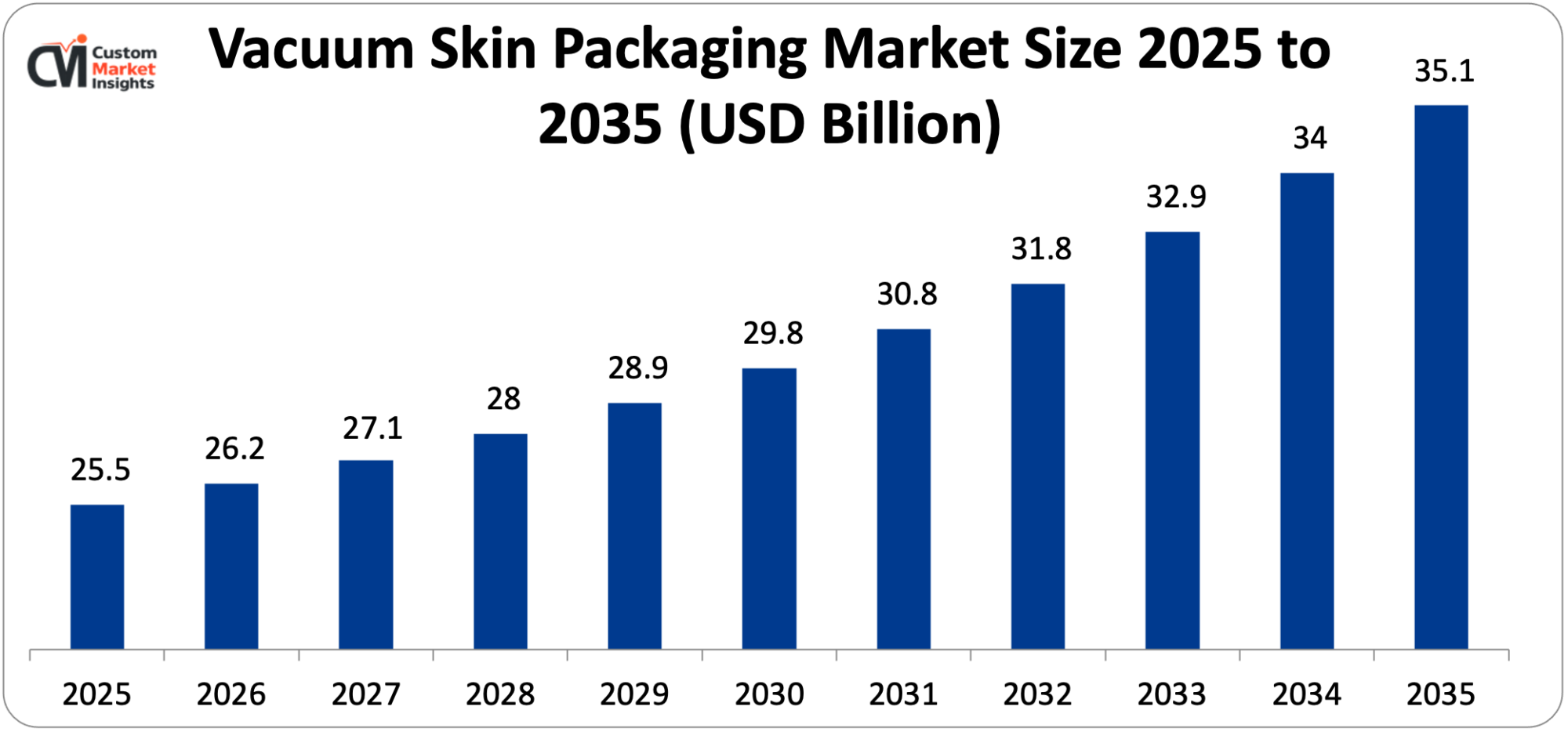

It is estimated that the market size of the global Vacuum Skin Packaging Market will be USD 26.2 billion in 2026 and that the market size will be USD 35.1 billion in 2035 with the forecast period and CAGR at 2026-2035 of 3.6%. Market is expanding because of the increasing demand for extended shelf life and improved product protection in the food industry especially for meat, seafood, dairy and ready to eat food. The demand is further being fuelled by the growing consumer preference towards high quality and attractive packaging solutions as well as the growth of structured retail and e-commerce industries. Further, the increasing use of vacuum skin packaging of medical equipment and consumer products as a secure and tamper-evident packaging, coupled with the development of high-barrier films, sustainable and recyclable packaging materials, and automated packaging lines, is adding a substantial amount to the general market expansion.

Market Highlight

- Asia Pacific- The Asian market dominates the Vacuum Skin Packaging Market with a market share of 41.5 % in 2025.

- Importantly, North America is expected to have a CAGR of 3.2% over the forecast period 2026-2035.

- Skin-on-Tray segment had the highest market share of 38.5% in 2025 because it is widely used in ready-to-eat food packaging, meat, and seafood packaging.

- The Skin Pouches segment will be projected to record the highest CAGR of 3.9% in the period 2026 to 2035 due to the rising need for flexible and sustainable packaging formats.

- PET will take 37.3% of the market share in 2025 because of its high transparency and high barrier properties, whereas bio-based and compostable films are expected to experience the most rapid increase over the forecast period.

- By end-use industry, the Food industry report will enjoy the highest market share of 52.5% in 2025, but the Medical and Healthcare segment will experience the greatest CAGR from 2026 to 2035 because of the increasing demand for sterile and tamper-evident packaging solutions.

- On the process technology front, the thermoplasts attained 47.8% of the market in 2025 owing to their effectiveness and scalability in large-scale packaging processes.

Significant Growth Factors

The high growth rate of Vacuum Skin Packaging (VSP) has been attributed to the growth of the demand for the product in the food sector and the showcasing of high quality products and sustainable packaging systems within the food, healthcare, and consumer goods industries.

- The Increasing Demand of Fresh and High-End Food Packaging: The increasing global market of Fresh meat, seafood, dairy, and ready-to-eat food is one of the driving forces of the market of Vacuum Skin Packaging. VSP technology enhances the product visibility through increasing the shelf life by minimizing the oxygen absorption and eradicating leakage. Asia Pacific, North America and Europe have witnessed a rapid expansion of organised retail chains, supermarkets, and online grocery stores, and this has increased the demand for high-clarity, tamper-evident, and hygienic types of packaging. The urbanization process, the dietary habit changes, and the growing preference of consumers towards using the visually appealing packaging forms are driving the food processing industry to resort to the skin-on-tray and skin pouch types. Besides, stringent food safety laws in the developed economies are compelling food manufacturers to invest in better barrier movies and automated packaging machinery as a means of ensuring compliance and reducing risks of food contamination.

- Creation of Sustainable and Recyclable Packaging Solutions: Sustainability is one of the key growth factors of the market in the VSP space because governments and companies devote more attention to the programs aimed at reducing carbon emissions and the circular economy. Mono-material recyclable films and bio-based solutions are also of high investment among major packaging organizations, in place of the conventional multi-layer plastics. In September 2023, Sealed Air announced that it had developed recyclable vacuum skin packaging films in its food packaging division, designed to reduce plastic use and have high barrier performance. Amcor introduced new recyclable flexible packaging in the protein and dairy applications to help achieve its sustainability roadmap in March 2024. Such developments are assumed to be used in order to ensure that the transition to environmentally friendly VSP formats can be made faster and will allow the market to grow eventually.

The Major Innovations That Are Transforming The Vacuum Skin Packaging Market of The Modern World.

- Automation and High-performance Packaging System: VSP production lines are being changed to automation and smart packaging systems in order to improve speed, consistency, and operational efficiency. The currently used thermoforming and skin packaging machines have a digital monitoring system, a predictive maintenance system and optimized sealing systems that require less energy. In April 2024, MULTIVAC included in its lineup of automated vacuum skin packaging machinery nicer digital control interfaces to improve throughput as well as reduce downtime. Similarly, in April 2025, ULMA Packaging introduced refined skin packaging equipment, which is to be used in high-output facilities in meat and seafood preparation facilities, and it is designed around energy efficiency and sustainability. The innovations are also enabling increased production levels of the processors without compromising the quality and the look of the product.

- Mergers and Capacity Expansion: Consolidation and strategic investments are altering the nature of competition in the industry of Vacuum Skin Packaging. Back in August 2023, Berry Global acquired directional packaging and high-barrier film in a strategic move that contributed to its protein and fresh food packaging. Coveris announced the expansion of its sustainable packaging production plant in Europe, including recyclable vacuum skin film products aimed at food retailers in February 2024. These expansions are making supply chains efficient and meeting the growing demand of the high performance VSP materials in the world.

- Advanced Barrier Film Innovations: Under the development of technical progress in high-barrier and ultra-barrier films, major advances are being made in the vacuum skin packaging concerning oxygen and moisture protection. In June 2024, Winpak introduced next-generation high-barrier films that are designed to be applied in the vacuum skin industry, in meat and cheese segments that require long shelf life. The manufacturers are also struggling to maintain a balance between performance and environmental responsibility with the help of an ongoing effort in the development of multi-layer co-extrusion technology and mono-material recyclable film.

Category Wise Insights

By Type

Why Skin-on-Tray is Leading the Market?

The biggest segment in 2025 is Skin-on-Tray packaging which will occupy a good portion of the market of Vacuum Skin Packaging (VSP). Such a hegemony is mainly motivated by the fact that it is widely used in fresh meat, seafood, poultry and ready to eat foodstuffs. Skin-on-tray packaging provides better product exposure, shelf life, seal leakage, and long shelf life, which makes it very desirable to retailers and food processors. The format closely encloses the product and tray with a film that has limited oxygen exposure to the product and minimizes spoilage and preserves the freshness and hygiene of the product.

The increasing growth of the organized retail chains and supermarket distribution networks has further promoted the development of skin-on-tray formats, especially in North America and Europe, where high quality food presentation constitutes a major distinctiveness. Also, the development of high-barrier films and recyclable tray materials has reinforced the stance of this segment. It can also be used in large-scale food processing activities because it is compatible with automated thermoforming and high-speed packaging lines and is cost-effective.

The Skin Pouches segment will see the most rapid CAGR in the period of 2026-35 as the demand for lightweight, flexible, and sustainable packaging solutions will go up. Skin pouches consume less material than rigid trays, provide easy storage and are also sustainable. The growth in this segment is further boosted by increasing demand for portion-controlled and takeaway food packaging.

By Material Type

The Preference of PET and Multi-Layer Films?

PET and multi-layer high-barrier films are among the most promising materials in 2025 as they are characterized by high quality of clarity, durability, and oxygen and moisture barrier. PET-based trays with high barrier top films have a long shelf life and thus are suitable in the packaging of proteins. Coreshell co-extrusion films promote mechanical high-strength and sealing properties, which guarantee the integrity of the product throughout transportation and storage.

Nevertheless, bio-based and compostable materials are expected to experience the most significant growth in the forecast period due to regulatory factors to reduce the amount of plastic waste and rising consumer demand for eco-friendly packaging. In the name of a circular economy, a large number of packaging producers are making mono-material solutions that can be recycled to reduce waste and achieve sustainability goals established by governments and retailers.

By End-Use Industry

Why Vacuum Skin Packaging is Screwaged by the Food Industry?

Food industry is the biggest end-use category in the year 2025, due to the growing global demand for fresh and processed food. Vacuum skin packaging is a major contributor to shelf life, food wastage, and product appearance, which is of utmost importance in the contemporary retailing setups. VSP technology is particularly used in applications of meat and seafood to preserve their freshness, avoid contamination, and meet food safety requirements.

Big food processing plants are increasingly adopting automated processing systems of VSPs as a way of enhancing efficiency and minimizing the dependency on labor. Segment dominance is also being caused by the increased demand for convenient, ready-to-eat food and portion-controlled packaging formats.

The Medical and Healthcare business segment is projected to achieve high growth up to 2035 due to the increased demand for the sterile, tamper-evident packaging solutions in the medical devices and instruments. Vacuum skin packaging offers protection of vacuum sealing and protection from contamination, so it may be applied in sensitive healthcare procedures.

By Packaging Function

The Reason to Focus on Shelf-Life Extension as the Major Growth Driving Force?

The key driver of the market of the Vacuum Skin Packaging is shelf-life extension. VSP prevents oxidation and microbial growth by eliminating air and creating a tight closure that prevents freshness from occurring over longer periods of time than traditional packaging methods. This role is especially useful in minimizing food waste along supply chains, as well as enhancing distribution efficiency by exporters.

Also, the display enhancement feature is also important in determining whether the consumer will buy the product or not. Clear and transparent, high-gloss films increase the visibility and presentation of the products, adding value to the brand in the competitive retail markets.

By Process Technology

The reasons why Thermoforming Systems are dominating the market?

The thermoforming technology has the potential to take over the market in 2025 because it is very efficient and scalable, and it can be used with the production lines that are automated. Thermoforming VSP machines are also capable of running at high speed, which means that the quality of sealing remains the same and the amount of wasted material is also minimal. Such systems find a wide application in large food processing plants that have to run continuous and high volume packaging systems.

The fully automatic systems are rapidly being adopted because manufacturers are focusing on how to enhance productivity, reduce the downtime period and incorporate digital monitoring tools. The automation also facilitates the minimization of labor costs and maintains standardization of packaging particularly in areas that have shortages of workforces. The former is still applicable to semi-automatic systems in small- and medium-sized processors and to the manual type of system in the low-volume or customized packaging.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 26.2 billion |

| Projected Market Size in 2035 | USD 35.1 billion |

| Market Size in 2025 | USD 25.5 billion |

| CAGR Growth Rate | 3.6% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Material Type, End-Use Industry, Packaging Function, Process Technology and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

What is the Size of the Asia Pacific Market?

The region is the biggest and most dynamic market in the entire world, backed by the good growth in food processing, modernisation of the retail industry and the growing demands of long shelf-life packaging solutions.

Why Did Asia Pacific Take Over the Market in 2025?

The market share of the Asia Pacific was estimated at 58% in the year 2025, which was mainly attributed to a high rate of urbanization, growth of organized retail, increase in disposable incomes, and good growth in the consumption of packaged foods. The growing population of middle-income people in the area has increased the consumption of fresh meat, seafood, dairy, and ready-to-eat foods in hygienically filled packages, all of which are major markets of vacuum skin packaging.

It is also the case because of development in food processing infrastructure and cold chain logistics that are growing rapidly in countries like China, India, and Japan. The giant supermarket chains and electronic grocery stores are also encouraging high-grade packaging options which improve product visibility and increase shelf life. Also, the increase in exports of seafood and meat products in Southeast Asia is increasing the demand for high-barrier VSP solutions.

The high expectations of the region are also due to government education on food safety and food waste reduction. The rising number of automated thermoforming and completely automated packaging line facilities in major food processing plants in the Asia Pacific is likely to continue its leading position in the forecast period.

China Market Trends

China enjoys the largest market in the Asia Pacific, as it has the largest food processing industry, a growing retail chain, and a robust export market of seafood and meat items. The shift toward the use of vacuum skin packaging is increasing as a result of the increasing popularity of premium packaged protein products among consumers and stringent food safety rules.

The increased investment of China in the production of high-level packaging equipment and the production of the high barrier film domestically also add more weight to the China market. Moreover, there are sustainability efforts that are promoting the use of recyclable PET trays and mono-material films, which are influencing the growth trends in the future

What is driving the Steady Growth in North America?

North America is expected to increase by a stable CAGR rate of 3.5% between 2026 and 2035 with an indication of a mature packaging industry that is still innovative. Favorable growth is encouraged by a high rate of consumption of packaged meat and ready to eat meals, good infrastructure of the cold chain, and a high presence of leading packaging manufacturers.

The area focuses on automation, operational efficiency and sustainable materials. The growing retailer interest in leak-proof, tamper-evident packaging formats, and attractive packaging formats are further permeating the growth of VSP technologies in supermarkets and warehouse retail chains.

How big is the U.S. Market?

The market of vacuum skin packaging in the United States is projected at USD 4.58 billion in 2025 and projected to increase at a CAGR of 3.5% within the period of 2026 to 2035.

U.S. Market Trends

The US market has a high level of fresh meat, poultry, and seafood packaging demand, as well as an increase in the use of medical device packaging. Retailers are focusing their attention on packaging formats that will prolong the shelf life of the product and cut down on food waste, which is sustainable. The investments in automation and the substitution of older packaging lines with the fully automatic thermoforming systems are further enhancing the growth of the market.

What is Europe So Preoccupied about Sustainability and Efficiency?

Europe constitutes a major portion of the world vacuum skin packaging market due to the strict environmental laws, food safety, and good recycling systems. Germany, France, and the United Kingdom are some of the countries that focus on recyclable and mono-material packaging solutions to meet the circular economy policies.

The area demonstrates the high usage of fully automated VSP systems with low energy consumption and the increase in the level of demand for compostable or bio-based materials. Consumers in Europe also like the premium packaging presentation which makes the high clarity of the skin films continue to be in demand.

Germany Market Trends

Germany is well placed in Europe because it has a highly developed food processing industry, stringent environmental policies and is the pioneer in the innovation of packaging machinery. To contribute to the long-term growth in the market, German manufacturers are oriented to high-efficiency thermoforming systems, sustainable material solutions, and low-emission production systems.

What is the Reason behind the Growth of the Middle East & Africa Region?

The Middle East & Africa area has been experiencing stable growth in the region because of the growth in urbanization, spread of modern retail forms, and growth in imports of packaged food products. The countries of the Gulf Cooperation Council, especially Saudi Arabia and the United Arab Emirates, are making a major investment in food processing infrastructure and cold storage facilities in order to boost food security.

Africa is an area where development is supported by slow expansion of the supermarket networks and rising food safety standards. The growing dependence of the region on packaged protein imports will be viewed as new opportunities for vacuum skin packaging solutions in the forecast period.

Top Players in the Market and Their Offerings

- Sealed Air Corporation

- Amcor

- Winpak Ltd.

- Linpac Packaging

- MULTIVAC

- DuPont

- Mondini

- Schur Flexibles

- Plastopil Hazorea

- Quinn Packaging

- Coveris Holdings

- Berry Global Inc.

- Others

Key Developments

There have been significant advancements in the Vacuum Skin Packaging (VSP) market, with the manufacturer developing automation, sustainability, and high-barrier packaging innovations in order to create better competitive advantages and product lines.

- In March 2025, Sealed Air Corporation launched an improved version of a recyclable vacuum skin packaging scheme to be used in fresh meat and seafood. The new system focuses on mono-material structures to enhance recyclability without compromising the high-barrier level of performance and long shelf life. In 2004, the company sold about 130 million products and has a workforce exceeding 100,000 employees around the world. The company has a workforce of over 100,000 employees in different parts of the world and sold approximately 130 million products between 2004 and 2008.

- In February 2025, MULTIVAC Group introduced a new generation of fully automatic vacuum skin packaging line with improved energy efficiency, digital control, and increased capacity in throughput capacity of large scale food processors. The system enables sustainable film choice and better flexibility in production. In 2003, the firm additionally introduced several innovations that have led to its leading position in this market. In 2003, the company also launched a number of innovations that have seen it dominate this market.

Through these strategic efforts, the companies have been able to enhance market positions, increase sustainable packaging, higher automation, and leverage the increasing demand in high end, shelf-life extending packaging applications in the food, medical, and retail industries.

The Vacuum Skin Packaging Market is segmented as follows:

By Type

- Flat Skin Packaging

- Hanging Skin Packaging

- Skin-on-Tray

- Skin Pouches

- Skin-on-Blister

By Material Type

- PVC

- PET

- PE

- PP

- Multi-Layer Films

- Bio-Based & Compostable Materials

By End-Use Industry

- Food

- Meat

- SeafoodDairy

- Ready-to-Eat Meals

- Medical & Healthcare

- Consumer Goods

- Industrial Components

- Retail & E-commerce

By Packaging Function

- Protection

- Shelf-Life Extension

- Tamper-Evidence

- Display Enhancement

By Process Technology

- Thermoforming

- Manual

- Semi-Automatic

- Fully Automatic

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Vacuum Skin Packaging by Segments

- 2.1.2. Vacuum Skin Packaging by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Vacuum Skin Packaging Market Attractiveness Analysis, By Type

- 2.2.3. Vacuum Skin Packaging Market Attractiveness Analysis, By Material Type

- 2.2.4. Vacuum Skin Packaging Market Attractiveness Analysis, By End-Use Industry

- 2.2.5. Vacuum Skin Packaging Market Attractiveness Analysis, By Packaging Function

- 2.2.6. Vacuum Skin Packaging Market Attractiveness Analysis, By Process Technology

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. The Increasing Demand of Fresh and High-End Food Packaging

- 3.1.2. Creation of Sustainable and Recyclable Packaging Solutions

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Vacuum Skin Packaging Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Vacuum Skin Packaging Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Flat Skin Packaging

- 4.1.3. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Hanging Skin Packaging

- 4.1.7. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Skin-on-Tray

- 4.1.11. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Skin Pouches

- 4.1.15. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Skin-on-Blister

- 4.1.19. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Vacuum Skin Packaging Market – By Material Type

- 5.1. Material Type Market Overview, By Material Type Segment

- 5.1.1. Vacuum Skin Packaging Market Revenue Share, By Material Type, 2025 & 2035

- 5.1.2. PVC

- 5.1.3. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. PET

- 5.1.7. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. PE

- 5.1.11. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. PP

- 5.1.15. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Multi-Layer Films

- 5.1.19. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Bio-Based & Compostable Materials

- 5.1.23. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Material Type Market Overview, By Material Type Segment

- Chapter 6. Vacuum Skin Packaging Market – By End-Use Industry

- 6.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 6.1.1. Vacuum Skin Packaging Market Revenue Share, By End-Use Industry, 2025 & 2035

- 6.1.2. Food

- 6.1.2.1. Meat

- 6.1.2.2. Seafood/Dairy

- 6.1.2.3. Ready-to-Eat Meals

- 6.1.3. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Medical & Healthcare

- 6.1.7. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Consumer Goods

- 6.1.11. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Industrial Components

- 6.1.15. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Retail & E-commerce

- 6.1.19. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 7. Vacuum Skin Packaging Market – By Packaging Function

- 7.1. Packaging Function Market Overview, By Packaging Function Segment

- 7.1.1. Vacuum Skin Packaging Market Revenue Share, By Packaging Function, 2025 & 2035

- 7.1.2. Protection

- 7.1.3. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Shelf-Life Extension

- 7.1.7. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Tamper-Evidence

- 7.1.11. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Display Enhancement

- 7.1.15. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Packaging Function Market Overview, By Packaging Function Segment

- Chapter 8. Vacuum Skin Packaging Market – By Process Technology

- 8.1. Process Technology Market Overview, By Process Technology Segment

- 8.1.1. Vacuum Skin Packaging Market Revenue Share, By Process Technology, 2025 & 2035

- 8.1.2. Thermoforming

- 8.1.3. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 8.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.5. Key Market Trends, Growth Factors, & Opportunities

- 8.1.6. Manual

- 8.1.7. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 8.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.9. Key Market Trends, Growth Factors, & Opportunities

- 8.1.10. Semi-Automatic

- 8.1.11. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 8.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.13. Key Market Trends, Growth Factors, & Opportunities

- 8.1.14. Fully Automatic

- 8.1.15. Vacuum Skin Packaging Share Forecast, By Region (USD Billion)

- 8.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.17. Key Market Trends, Growth Factors, & Opportunities

- 8.1. Process Technology Market Overview, By Process Technology Segment

- Chapter 9. Vacuum Skin Packaging Market – Regional Analysis

- 9.1. Vacuum Skin Packaging Market Overview, By Region Segment

- 9.1.1. Global Vacuum Skin Packaging Market Revenue Share, By Region, 2025 & 2035

- 9.1.2. Global Vacuum Skin Packaging Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 9.1.3. Global Vacuum Skin Packaging Market Revenue, By Type, 2026 – 2035

- 9.1.4. Global Vacuum Skin Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.1.5. Global Vacuum Skin Packaging Market Revenue, By End-Use Industry, 2026 – 2035

- 9.1.6. Global Vacuum Skin Packaging Market Revenue, By Packaging Function, 2026 – 2035

- 9.1.7. Global Vacuum Skin Packaging Market Revenue, By Process Technology, 2026 – 2035

- 9.2. North America

- 9.2.1. North America Vacuum Skin Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.2.2. North America Vacuum Skin Packaging Market Revenue, By Type, 2026 – 2035

- 9.2.3. North America Vacuum Skin Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.2.4. North America Vacuum Skin Packaging Market Revenue, By End-Use Industry, 2026 – 2035

- 9.2.5. North America Vacuum Skin Packaging Market Revenue, By Packaging Function, 2026 – 2035

- 9.2.6. North America Vacuum Skin Packaging Market Revenue, By Process Technology, 2026 – 2035

- 9.2.7. U.S. Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.8. Canada Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.9. Mexico Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.10. Rest of North America Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3. Europe

- 9.3.1. Europe Vacuum Skin Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.3.2. Europe Vacuum Skin Packaging Market Revenue, By Type, 2026 – 2035

- 9.3.3. Europe Vacuum Skin Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.3.4. Europe Vacuum Skin Packaging Market Revenue, By End-Use Industry, 2026 – 2035

- 9.3.5. Europe Vacuum Skin Packaging Market Revenue, By Packaging Function, 2026 – 2035

- 9.3.6. Europe Vacuum Skin Packaging Market Revenue, By Process Technology, 2026 – 2035

- 9.3.7. Germany Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.8. France Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.9. U.K. Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.10. Russia Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.11. Italy Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.12. Spain Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.13. Netherlands Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.14. Rest of Europe Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4. Asia Pacific

- 9.4.1. Asia Pacific Vacuum Skin Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.4.2. Asia Pacific Vacuum Skin Packaging Market Revenue, By Type, 2026 – 2035

- 9.4.3. Asia Pacific Vacuum Skin Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.4.4. Asia Pacific Vacuum Skin Packaging Market Revenue, By End-Use Industry, 2026 – 2035

- 9.4.5. Asia Pacific Vacuum Skin Packaging Market Revenue, By Packaging Function, 2026 – 2035

- 9.4.6. Asia Pacific Vacuum Skin Packaging Market Revenue, By Process Technology, 2026 – 2035

- 9.4.7. China Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.8. Japan Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.9. India Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.10. New Zealand Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.11. Australia Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.12. South Korea Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.13. Taiwan Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.14. Rest of Asia Pacific Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5. The Middle-East and Africa

- 9.5.1. The Middle-East and Africa Vacuum Skin Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.5.2. The Middle-East and Africa Vacuum Skin Packaging Market Revenue, By Type, 2026 – 2035

- 9.5.3. The Middle-East and Africa Vacuum Skin Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.5.4. The Middle-East and Africa Vacuum Skin Packaging Market Revenue, By End-Use Industry, 2026 – 2035

- 9.5.5. The Middle-East and Africa Vacuum Skin Packaging Market Revenue, By Packaging Function, 2026 – 2035

- 9.5.6. The Middle-East and Africa Vacuum Skin Packaging Market Revenue, By Process Technology, 2026 – 2035

- 9.5.7. Saudi Arabia Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.8. UAE Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.9. Egypt Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.10. Kuwait Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.11. South Africa Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.12. Rest of the Middle East & Africa Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.6. Latin America

- 9.6.1. Latin America Vacuum Skin Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.6.2. Latin America Vacuum Skin Packaging Market Revenue, By Type, 2026 – 2035

- 9.6.3. Latin America Vacuum Skin Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.6.4. Latin America Vacuum Skin Packaging Market Revenue, By End-Use Industry, 2026 – 2035

- 9.6.5. Latin America Vacuum Skin Packaging Market Revenue, By Packaging Function, 2026 – 2035

- 9.6.6. Latin America Vacuum Skin Packaging Market Revenue, By Process Technology, 2026 – 2035

- 9.6.7. Brazil Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.6.8. Argentina Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.6.9. Rest of Latin America Vacuum Skin Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.1. Vacuum Skin Packaging Market Overview, By Region Segment

- Chapter 10. Competitive Landscape

- 10.1. Company Market Share Analysis – 2025

- 10.1.1. Global Vacuum Skin Packaging Market: Company Market Share, 2025

- 10.2. Global Vacuum Skin Packaging Market Company Market Share, 2024

- 10.1. Company Market Share Analysis – 2025

- Chapter 11. Company Profiles

- 11.1. Sealed Air Corporation

- 11.1.1. Company Overview

- 11.1.2. Key Executives

- 11.1.3. Product Portfolio

- 11.1.4. Financial Overview

- 11.1.5. Operating Business Segments

- 11.1.6. Business Performance

- 11.1.7. Recent Developments

- 11.2. Amcor

- 11.3. Winpak Ltd.

- 11.4. Linpac Packaging

- 11.5. MULTIVAC

- 11.6. DuPont

- 11.7. G. Mondini

- 11.8. Schur Flexibles

- 11.9. Plastopil Hazorea

- 11.10. Quinn Packaging

- 11.11. Coveris Holdings

- 11.12. Berry Global Inc.

- 11.13. Others.

- 11.1. Sealed Air Corporation

- Chapter 12. Research Methodology

- 12.1. Research Methodology

- 12.2. Secondary Research

- 12.3. Primary Research

- 12.3.1. Analyst Tools and Models

- 12.4. Research Limitations

- 12.5. Assumptions

- 12.6. Insights From Primary Respondents

- 12.7. Why Custom Market Insights

- Chapter 13. Standard Report Commercials & Add-Ons

- 13.1. Customization Options

- 13.2. Subscription Module For Market Research Reports

- 13.3. Client Testimonials

List Of Figures

Figures No 1 to 47

List Of Tables

Tables No 1 to 56

Prominent Player

- Sealed Air Corporation

- Amcor

- Winpak Ltd.

- Linpac Packaging

- MULTIVAC

- DuPont

- Mondini

- Schur Flexibles

- Plastopil Hazorea

- Quinn Packaging

- Coveris Holdings

- Berry Global Inc.

- Others

FAQs

The key players in the market are Sealed Air Corporation, Amcor, Winpak Ltd., Linpac Packaging, MULTIVAC , DuPont, G. Mondini, Schur Flexibles, Plastopil Hazorea, Quinn Packaging, Coveris Holdings, Berry Global Inc., Others.

The government regulations have a great impact on the Vacuum Skin Packaging market by providing the food safety standards, labeling requirements, environmental policies, and waste minimization targets. Vacuum technologies are used because of the policies that promote the hygienicity of meat and seafood packaging. Some of the sustainability policies that promote the development of recyclable, bio-based, and mono-material packaging materials include policies on plastic waste reduction as well as the circular economy implementation in such regions as the European Union, among others. Also, there exist legislations that are pro-shelf-life-prolonging packaging technology, such as VSP that seek to minimize the food waste and enhance cold chains that contribute to the demand.

Depending on the level of automation and the capacity to produce, vacuum skin packaging systems have moderate or high initial capital investment requirements. Manual and semi-automatic systems are cheaper and are more commonly used by small- and medium-sized processors, whereas fully automatic thermoforming lines are a higher investment but offer higher throughput, labor savings, and cost-efficiency in the long run. The higher prices can be justified by high-barrier films and special trays, but the longer shelf life, fewer returns, less food waste, and better retail looks justify the higher prices. Leasing schemes and equipment financing schemes allow the manufacturers to implement advanced VSP systems without significant initial investments.

As per the latest analysis, it is estimated that by 2035, the market size of the Vacuum Skin Packaging will be about USD 35.1 billion with a CAGR of 3.6% in the period of 2026–2035. Increasing demand for high-end formats of packaging, automation of food production facilities, rising sustainability campaigns, creation of recyclable high-barrier films, and expansion of retail-ready packages that will improve product exposure and consumer attraction help support growth.

It is expected that the global Vacuum Skin Packaging will be dominated by the Asia Pacific, which will contribute the most proportion of revenues. The area enjoys the huge food processing industry, good retailing growth, and a high demand for packaged protein products. The country is still a major contributor, as China has a huge meat processing sector and more and more automated packaging machines. The further urbanization, retail supply chain modernization, and the existence of favorable food safety policies are likely to guarantee perpetual domination throughout the next decade.

Asia-Pacific should record the highest CAGR in the forecast period because it is a fast growing region in terms of urbanization, proliferation of food processing industries, growth of disposable incomes, and supermarket and online grocery store penetration. There is high demand for hygienically packaged fresh meat, seafood and ready meals in countries like China and India. Increased exports of protein products and expansion of cold chain facilities are other factors contributing to the use of new technologies in vacuum skin packaging in the region.

Global Vacuum Skin Packaging (VSP) market has been projected to record high growth due to the increase in demand of food products with a long shelf-life, growth in global meat and seafood consumption, the rise in organized retailing, and the increase in the importance of food safety and hygiene standards. The world packaged food market is still booming with the growing urbanization and shifting lifestyles that favor readymade food and convenience food. VSP can save a lot of oxygen and increase the shelf life of products, and food waste can be reduced to a minimum: an extremely important aspect in the context of the current demands of governments and retail chains to minimize losses in the supply chain. Also, the development of high-barrier films, automation of thermoforming systems, and the growing use of recyclable and mono-material packaging solutions are also further enhancing marketing growth. Healthcare sector is also playing a role in terms of the demand for medical devices and instruments in sterile and tamper-evident packaging.