Plastic Luxury Packaging Market Size, Trends and Insights By Material Type (Acrylic (PMMA), Polycarbonate (PC), PET & RPET, ABS (Acrylonitrile Butadiene Styrene), Polypropylene (PP), Bio-Based & Recycled Polymers (Bio-PET, PCR-PMMA, PLA), Other Materials (SAN, TPE, Nylon)), By Packaging Type (Bottles & Jars, Boxes & Cases (Compacts, Palettes, Gift Cases), Tubes & Cartridges, Caps & Closures (Pumps, Sprayers, Disc Tops), Bags & Pouches (Rigid-Structured and Flexible Luxury), Other Packaging Types (Applicators, Display Components)), By Application (Cosmetics & Personal Care (Skincare, Makeup, Haircare), Fragrance & Perfumery, Spirits & Premium Beverages, Jewelry & Watches, Fashion & Apparel Accessories, Other Applications (Gourmet Food, Nutraceuticals)), By End-User (Absolute Luxury (Ultra-Premium, Haute Couture Brands), Aspirational Luxury (Accessible Premium Brands), Mass Prestige (Masstige, Affordable Luxury)), By Distribution Channel (Specialty Luxury Retailers (Mono-Brand Boutiques), Department Stores & Multi-Brand Luxury Retail, Online Luxury Retail (Brand.com and Luxury E-tailers), Duty-Free & Travel Retail, Other Channels (Direct-to-Consumer, Subscription Boxes)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 8.1%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Europe |

Major Players

- Albéa Group

- HCP Packaging

- Quadpack Industries S.A.

- RPC Group (Berry Global)

- Others

Reports Description

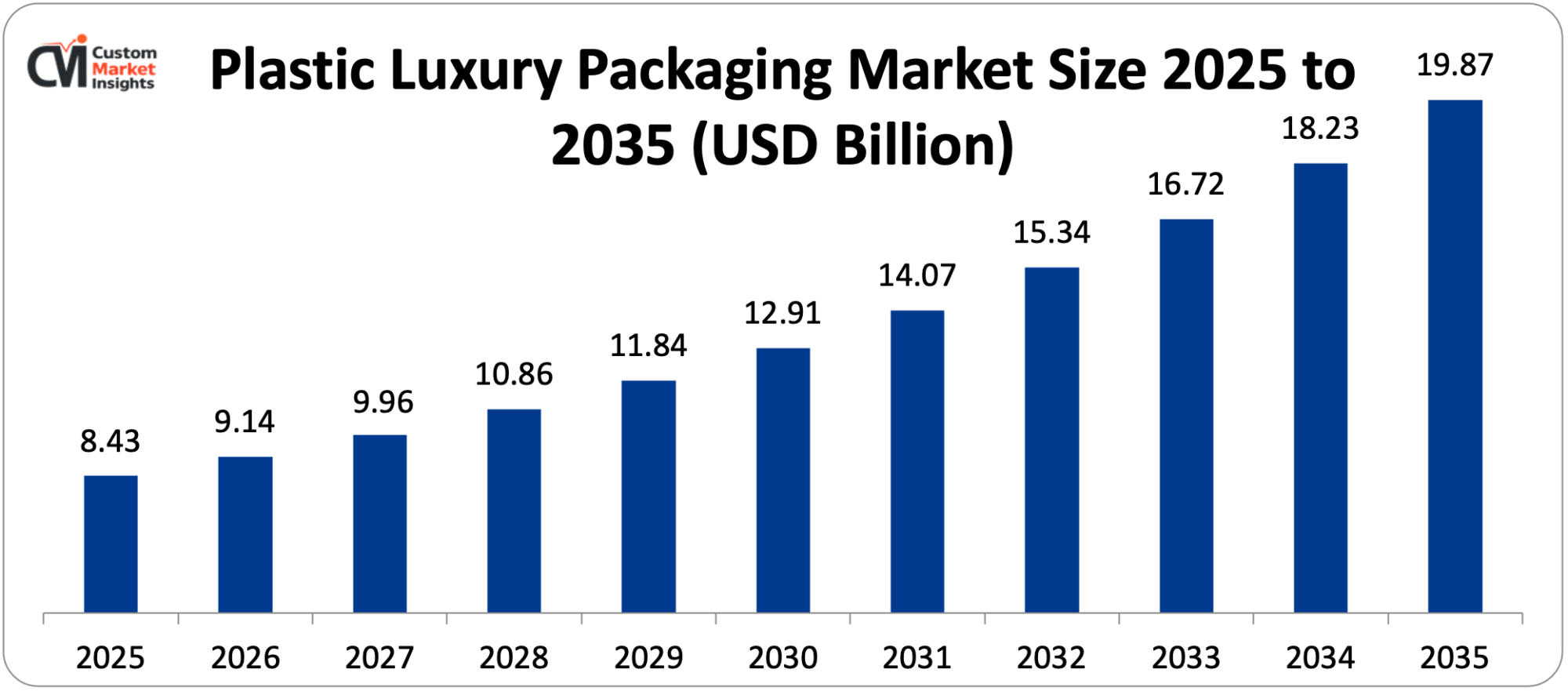

The 2025 market size of the plastic luxury packaging industry is estimated at USD 9.14 billion and is projected to grow at a CAGR of 8.1% between the years 2026 and 2035 to USD 19.87 billion.

The growing globalized luxury goods business fuelled by the surging ultra-high-net worth and aspirational high-end middle-class consumer groups in the emerging economies, the expanding use of advanced polymer engineering models that can employ plastic wraps to mimic the visual authority of glass and metal at higher design capability and product economic parameters, the growing sophistication of surface finishing technologies such as metallization, soft-touch finishes, and high-precision decorating that elevate the status of plastic luxury packaging to new levels of high-end premiums, the emerging industry pressures to produce sustainable luxury packaging using recycled formats across global markets collectively drive robust and sustained market growth throughout the forecast period.

Market Highlight

- In 2025, Europe’s plastic luxury packaging has a 34% market share.

- Asia Pacific: Asia Pacific will experience the highest CAGR of 11.3% between the years 2026 and 2035.

- By type of material, the acrylic segment had taken around 29% of the market share in 2025.

- By type of material, the polycarbonate segment has the highest CAGR of 10.4% between 2026 and 2035.

- By the type of packaging, the bottles and jars segment had the largest market share of 38% in 2025 with the caps and closures segment projected to grow at the highest CAGR rate of 9.6% in the forecast of 2026 to 2035.

- Application Cosmetic and personal care segment has the largest market share of 46 in 2025, and the fastest CAGR of the fragrance and perfumery segment is 10.2% from 2026 to 2035.

- By end-user, the aspirational luxury segment will win 43% of the market share in 2025.

Significant Growth Factors

The Plastic Luxury Packaging Market Trends present significant growth opportunities due to several factors:

- Global Luxury Market Expansion and Emerging Economy Aspirational Consumer Growth: The further development of the structure of the worldwide luxury goods business is the background of plastic luxury packaging demand. The increasing ultra-high-net-worth communities, fast-growing aspirational middle classes in China, India, Southeast Asia and the Middle East, and the luxury of consumption in all forms previously held by mass-market goods are all facilitating growth. The luxury goods market globally had been estimated to be EUR 363 billion in 2024 (Bain & Company) and is estimated to be EUR 500-540 billion in 2030, although the 2024 correction was caused by post-COVID normalization of demand, which is a factor of structuring expansion, not volatility. In 2024, the global UHNWI population (> 30M) increased by 4.2% to 395,000 and the HNWI population (> 1M) grew to 22.8 million, which is the largest luxury consumer base ever. The largest long-term demand vector is the growing aspirational middle class: China has already surpassed 1.2 billion people in the middle class, India is increasing its middle class by 25 million households each year and Southeast Asia is expected to increase its consumers by 140 million by 2030. The packaging factor is decisive in the performance of luxury: a 2024 survey conducted by Euromonitor revealed that 73% of Chinese, 68% of UAE, and 61% of U.S. consumers, to establish the quality of the purchase, paid great attention to its packaging. Since all luxury products need to be packaged with a message that conveys brand equity and provides a premium unboxing experience, the growth in luxury markets is directly proportional to the demand for structural plastic luxury packaging.

- Premiumization of Beauty and Personal Care Driving Sophisticated Packaging Demand: The most significant application-specific driver of plastic luxury packaging demand is the global trend of premiumization of beauty and personal care: consumer trade-up between mass and prestige is driving sophisticated packaging demand requirements. It is estimated that prestige beauty will grow to USD 280 billion in 2024 and 180 billion in 2030 with prestige skincare estimated to grow to USD 68 billion in 2024, and projected to increase at a 7.8% CAGR to 2030. The clinical skincare revolution – with products priced at USD 501,000 and above – necessitates packaging that communicates laboratory accuracy and ingredient credibility using innovative acrylic, polycarbonate, and high-quality PET. The use of acrylic as the primary material in high-end skincare jars, bottles, and palettes has resulted in the material being the most popular due to optical clarity comparable to glass, ability to apply superior finishes, reduced risk of breakage, and allowance for the creation of designs in three dimensions. The market of global acrylic cosmetic packaging is estimated to have a consumption of over 180,000 metric tons per annum, the prestige skincare is estimated to have an annual market demand of 320,000+ metric tons of luxury plastic packaging demand. K-beauty and J-beauty have globalized, making plastic a high-quality packaging material that changes the perception of consumers. The investment in innovation is being made by major players in the industry e.g. L’Oréal (EUR 41.2B revenue in 2024) has invested EUR 1.1B in packaging innovation and sustainability so far to support its prestige line.

What are the Major Advances Changing the Plastic Luxury Packaging Market Today?

- Advanced Polymer Engineering and High-Performance Resin Development: The ongoing development of specialty polymer engineering is broadening the visual and functional capabilities of plastic luxury packaging so that performance profiles that are challenging and sometimes superior to glass and metal are now available, with greater design flexibility and economy. Advances have been made to bio-acrylic resins of increased optical clarity (haze under 0.5%), increased scratch performance, and reduced birefringence; to high-flow, high-clarity polycarbonate resins allowing thick-walled (0.5–0.8 mm) highly dimensionally precise luxury components (tolerance of 0.05mm), and to cosmetic-grade PLA with increased optical clarity and heat resistance (HDT over 80 o C) to sustainable high-end formats. The specialty acrylic grades cost between EUR 4 and 8/kg compared to EUR 1.5-2.5/kg of commodity PMMA, which is due to performance customization to the luxury specifications. TPE and silicone-plastic composites also allow the incorporation of soft-touch and multi-sensory designs, which adds to the high-end feel.

- Surface Decoration and Finishing Technology Revolution: Surface decoration and finishing technologies, such as vacuum metallization, PVD coating, in-mold decoration, digital 3D inkjet printing, laser engraving, hot stamping, embossing, soft-touch coating, and multi-layer lacquering have allowed surface decoration and finishing to reach a parity with handmade glass and metal. Mirror-bright metallic finish is made possible through vacuum metallization at 40-60% of the cost of metal elements. World market The cosmetic packaging metallization market has reached USD 1.8 billion in 2024 and is expected to increase by 9.3% CAGR. PVDs offer hardness up to 9H, iridescent, and gold finishes, in addition to rose gold, which is much more durable than any other traditional finishes. Inkjet printing We have introduced a digital 3D printing technique making it possible to create custom and limited-run products at scale with high quality and soft-touch finishes providing unique velvet-touch results that enhance the premium brand positioning.

- Sustainable Luxury Plastic Packaging Innovation and Circular Design: Luxury packing industry is harmonizing the concerns of high-end style and sustainability with the rapid on-the-fly green innovation. In a 2024 survey by Deloitte, two out of every three luxury consumers aged below 35 are ready to pay a maximum of 12% higher on products sustainably packaged. Large luxury groups have made the target of 100% recyclable, refillable, reusable, or eco-designed packaging by 2025–2026. Its innovation involves the incorporation of 30-100% post-consumer recycled (PCR) plastics without compromising optical quality, the development of refillable systems with durable outer shells, replacing inner cartridges with new ones, and the development of chemical routes to PMMA producing virgin-equivalent monomer quality. They all have the beneficial effect of lessening the effects on the environment, improving the brand loyalty, and establishing repeat-buying patterns.

- Digital Integration and Smart Luxury Packaging Technologies: Digital integration is taking luxury packaging to an engagement, authentication, and data platform. As the problem of luxury counterfeiting at the global level is USD 4.5 trillion, implanted NFC chips, QR codes, blockchain-based authentication, and augmented reality activations are becoming competitive advantages. NFC packaging facilitates immediate product authentication, accessing stories, loyalty, and registration, and the collection of consumer analytics. The information provided by the provenance systems supported by blockchains will create more transparency, and the AR-enhanced packaging will turn tangible items into an interactive brand experience, making plastic luxury packaging the driver of both tangible and digital value.

Category Wise Insights

By Material Type

Why Does Acrylic Lead the Plastic Luxury Packaging Market?

The segment of acrylic (PMMA — polymethyl methacrylate) is the largest type of material in 2025, having around 29% share in the market. The fact that it is made of unmatched optical clarity, aesthetic versatility, and finishing compatibility is why it is the default premium polymer in skincare jars, cosmetic bottles, fragrance caps, and makeup palettes. Acrylic uninterrupted light transmission is 92 93 including the clarity of borosilicate glass, being half the weight, providing jewel-like brightness, and allowing the product to be seen at the point of sale and on opening the packaging. In 2024, the global market of luxury cosmetic packaging made of acrylic was estimated to be worth USD 2.4 billion. The packaging of prestige skincare has been defined over twenty years by iconic design styles like the Crème de la Mer jar produced by La Mer using optical-grade acrylic. The machinability of acrylic enables CNC prototyping, optical polishing, embedded decoration, and multi-material assemblage, providing diverse latitude of creativity over glass or metal. Although vulnerable to formulations that rely on solvents, this restriction is relatively easy to address by using liners and coatings and does not restrict secondary packaging or cap usage. Under luxury brand objectives, the ability of PMMA to be recycled through mechanical and developing chemical depolymerization routes is reinforcing its sustainability arguments.

The fastest-growing segment is polycarbonate (PC), which is estimated at 10.4% CAGR (202635). It has been developed to have excellent impact resistance (250x greater than glass), high optical clarity, and high heat deflection temperature at 120-135°C; thus, it can operate in hot climate conditions (Middle East and South Asia). PC luxury packaging refers to one of the segments that were estimated to be USD 890 million in 2024 and expected to be USD 2.34 billion in 2035. The highest growth will be in perfume caps, cosmetic compacts, and high-end haircare bottles, where PC is performing at a premium of 3050% to acrylic. Specialty grades of polycarbonate with UV-stabilization and food-contact-approved PC materials are also making polycarbonate the technical polymer of choice in terms of high-performance luxury applications.

By Packaging Type

Why Do Bottles & Jars Dominate the Market?

Containers Bottles and jars are the biggest sector of packaging type in 2025, as characterizing their fundamental position in prestige skincare, luxury haircare, fragrance, and spirits, with the container itself as the primary brand asset. Ultra-pricier skincare jars like the Crème de la Mer by La Mer, the Skin Caviar Luxe Cream by La Prairie, and the The Rich Cream by Augustinus Bader will qualify as the most expensive single packaging unit in luxury plastics, and ultra-luxury acrylic jar assemblies will also sell for USD 84 and USD 45 each without ornamentation. Although fragrance main bottles are normally made of glass, caps, overcaps, magnetic closures and structures are major components that use premium plastics, and the global luxury fragrance cap market is estimated at approximately USD 680 million each year. Within the spirits sector, travel retail and experience consumption use of acrylic and polycarbonate bottles in niche adoption are becoming a premium sub-market.

The packaging category that grows at the quickest rate is caps and closures at 9.6% CAGR (20262035). The distinction of closure systems is that they are the most frequent tactile between consumer and product, and as such, they are important to perceived quality. The luxury pump dispensing market, which includes airless pumps, lotion pumps, fragrance atomizers, and serum dispensers, is estimated to be USD 1.2 billion in 2024 and is estimated to grow by 10.8% CAGR until 2030. Premium airless bottles that shield the oxygen-sensitive formulations and offer controlled dispensing cost USD 3.50-USD 12.00 per unit, frequently amounting to 20-35% of the total skincare packaging cost, which makes them one of the highest-margin product segments in plastic luxury packaging.

By Application

Why Does Cosmetics & Personal Care Dominate the Market?

The cosmetics and personal care category has the highest application in the market share of about 46% in 2025, indicating prestige beauty as the most packaging-intensive luxury category. The beauty market in the world is expected to have USD 180 billion as of 2024 and USD 280 billion in 2030 (7.6% CAGR). The annual production of approximately 28 billion prestige beauty packaging units is estimated, with 65% of these units including plastic in their contents. High-performance active ingredients have led to the clinical skincare revolution, which has produced ultra-premium products, which are sold at USD 80-USD 800 per unit and require packaging that expresses scientific authority and exclusivity. The color cosmetics market is the largest unit-volume category in the world, where the global color cosmetics market is USD 92 billion in 2024 because of such a variety of formats that need plastic parts. K-beauty has also helped to standardize the advanced multi-component plastic packaging structures in the world, speeding up the innovation in compacts, cushions, and layered jar designs.

By End-User

Why Does Aspirational Luxury Lead the Market?

The aspirational luxury category will have about 43% market share in 2025, with the brands serving more affordable premium prices (USD 30 2 USD 200) and a high level of packaging sophistication. These brands have the capability of mixing high-quality specifications with large volumes of production (1–20 million units per SKU), and investing in proprietary toolings, sophisticated decoration, and material development is commercially feasible. By contrast, ultra-luxury brands tend to run at a smaller volume, which restricts the effectiveness of tooling amortization. Mass prestige (masstige) segment is the most dynamic end-user category with a projected CAGR of 11.8 (2026–2035) with brands used to increase the sophistication of the packaging but at a price point that remains mass-market disciplined.

By Distribution Channel

Why Do Specialty Luxury Retailers Dominate?

In 2025, mono-brand boutiques, curated multi-brand retailers, and department store beauty halls in the specialty luxury retailer segment have a market share of about 38%. Consumers in such settings touch the products, and they are also very sensitive to the packaging aesthetics, the tactile quality, and the sense impressions that have a direct impact on converting the purchases and average transaction value.

The quickest growing channel is online luxury retail, which is expected to have a CAGR of 14.3% (2026–2030) with the growth of luxury e-commerce growing to USD 178 billion in 2030, compared to USD 74 billion in 2024. E-commerce increases the significance of unboxing experience packaging, which results in social sharing and repeat purchases.

Duty-free and travel retail are strategically important because they are characterized by the concentration of aspirational luxury customers in discretionary, gift-giving purchase situations in which the quality of packaging plays a major role in perceived value.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 9.14 billion |

| Projected Market Size in 2035 | USD 19.87 billion |

| Market Size in 2025 | USD 8.43 billion |

| CAGR Growth Rate | 8.1% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Material Type, Packaging Type, Application, End-User, Distribution Channel and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Europe Market Size?

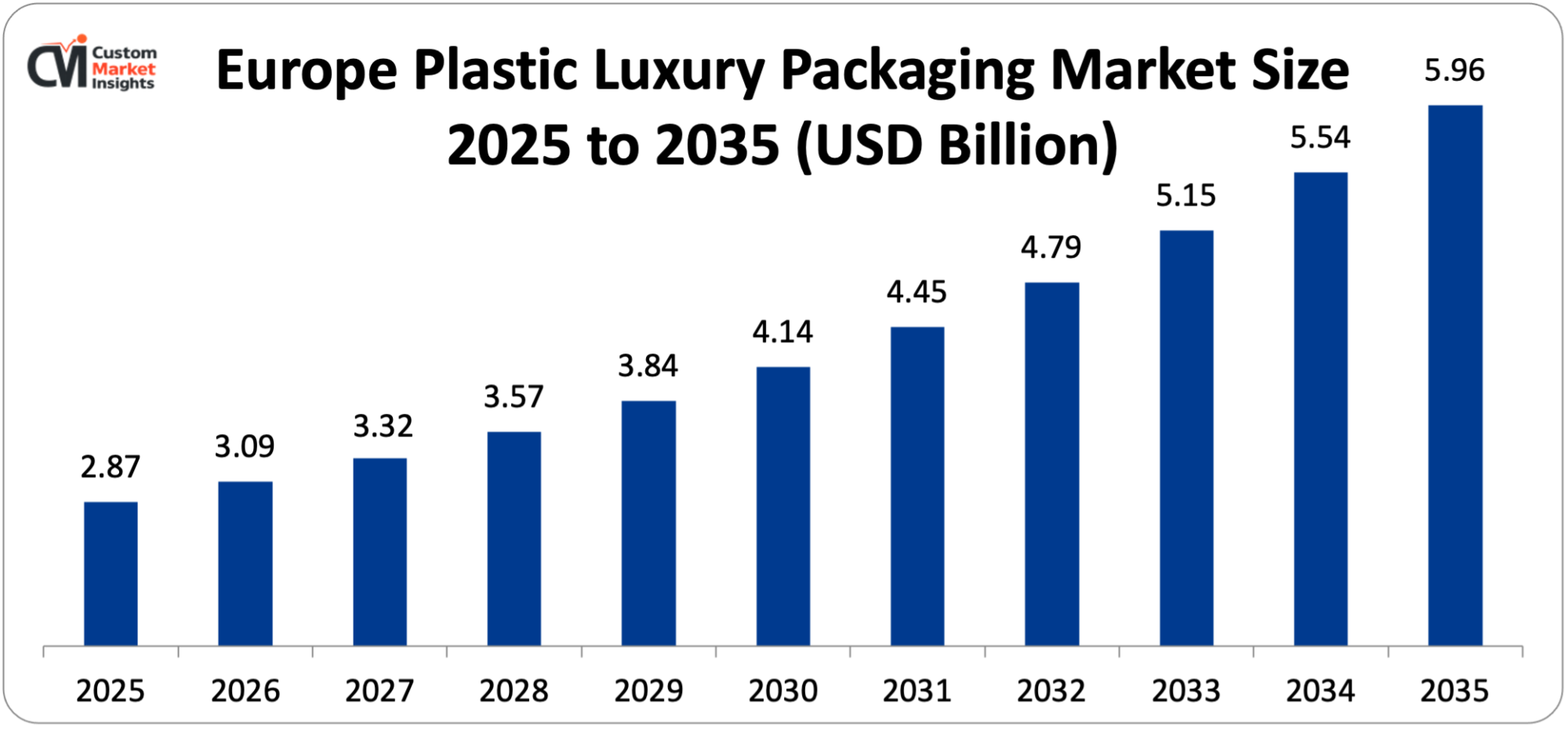

The European plastic luxury packaging market size is estimated at USD 2.87 billion in 2025 and is projected to reach approximately USD 5.96 billion by 2035, with a CAGR of 7.6% from 2026 to 2035.

Why Did Europe Dominate the Market in 2025?

Europe also controls about 34% of the worldwide marketplace in 2025, which demonstrates its status as the global luxury brand ownership and luxury packaging production heart of excellence – with France, Italy, Germany and the UK altogether homes to the most esteemed luxury conglomerates in the world, such as LVMH, Kering, Chanel, Hermès, L’Oréal Luxe, Estée Lauder Companies’ European creative hub, Coty, and Interparfums, with the most advanced ecosystem of luxury packaging design studios, injection molding and surface decoration experts and luxury packaging The largest luxury packaging design center in the world is based in the Ile-de-France region of France, which includes Paris and other departments, and it is estimated that there are over 300 specialist luxury packaging suppliers there, such as Albéa Group, Pochet Group, Cosmetic Component, Technipaq, and an array of artisan specialty fabricators producing the entire range of high-end packaging constituents for the most luxurious brands in the world.

The packaging manufacturing powerhouse of Italy, with its industrial centers in Lombardy, Veneto, and Emilia-Romagna, offers the second-most valuable luxury packaging manufacturing, and the Italian suppliers such as Bormioli Luigi, Gibo International, and Lumson SpA are known all over the world as producers of ceramic, glass, and high-end plastic luxury packaging parts serving the Italian fashion luxury houses of Gucci, Prada, Dolce & Gabbana, and Bulgari. The Packaging and Packaging Waste Regulation (PPWR) of the EU, which requires a minimum recycled content in plastic packaging and must have all packaging recyclable by 2030 is both creating compliance investment demands and sustainability innovation opportunities that are changing the design of European luxury plastic packaging, with major European luxury brands investing in the integration of PCR resin, refillable packaging systems, and chemical recycling infrastructure at a rate that is making European luxury packaging sustainability a global standard.

Why is North America a Major Market?

The North American plastic luxury packaging industry is approximated at around USD 2.19 billion in 2025 and is expected to grow to around USD 4.67 billion in 2035 with a CAGR of 7.9. North America is a strategic market of critical importance due to the presence of the United States as the largest single-country market of luxury goods consumption in the world, with Americans spending about USD 82 billion on luxury goods in 2024, according to Bain & Company; the headquarters location of major luxury and prestige brands, such as Estée Lauder Companies, Coty, Revlon, Bath and Body Works and Victoria’s Secret, creating a domestic packaging sourcing demand; and with the most developed market of luxury beauty e-commerce in the world, creating premium unboxing packaging investment by DTC luxury and prestige. One of the most innovative and fastest-growing plastic luxury packaging demand segments in the world, creating premium positioning at affordable price points by utilizing advanced plastic packaging aesthetics, is the American mass prestige beauty market, the brands of which include e.l.f., NYX, Rare Beauty, and Fenty Beauty.

U.S. Market Trends

The U.S. market is informed by the blowout of luxuriant and masstige beauty brands based on advanced plastic packaging as their chief brand assurance investment, the dominance of Sephora and Ulta Beauty as a retail environment with packaging visual effects at the point of sale being the primary driver of purchase for beauty customers shopping hundreds of competing brands, the proliferation of luxury beauty box services such as Birchbox and IPSY that expose consumers to high-quality packaging formats and induce a trade-up effect, and the FDA cosmetic packaging regulation under the Modernization of Cosmetics Regulation Act of 2022 imposing product listing and safety substantiation requirements that are driving luxury brands to invest in traceable, documentation-compliant packaging supply chains.

Why is Asia Pacific the Fastest-Growing Market?

Asia Pacific has the opportunity to grow to be the fastest-growing regional market, with an estimated CAGR of 11.3% between 2026 and 2035 due to the presence of China as the second largest luxury goods market in the world, estimated to have a luxury goods market of approximately EUR 59 billion in 2024 according to Bain and Company despite the 2024 luxury market softening, and its large and fast-growing middle-class consumer segment of 400 million+ consumers and increasing luxury expectations; South Korea, with Chinese in-country luxury beauty producers such as Florasis (Hua Xizi), Into You, and Perfect Diary, is aggressively developing its luxurious packaging of plastic material with Chinese-based references to cloisonné and compact designs, jade coloring of packaging material with traditional referral motives, and limited edition seasonal collections packaging that are creating both local as well as international consumer interest and has established Chinese luxury packaging design as a global creative powerhouse.

Why is the Middle East & Africa Region an Important Emerging Market?

LAMEA is a growing opportunity with high potential due to the unprecedented intensity of luxury consumption by the Gulf Cooperation Council, as the region has one of the highest rates of luxury consumption per capita in the world, with UAE luxury spending on fragrance production and consumption being particularly remarkable at an average of USD 1,450 per person per year and the culture of the region requiring uniquely premium packaging of their products, which conveys their sense of luxury and social standing. The Vision 2030 economic change agenda that focuses on luxury retail infrastructure, tourism investment, and domestic entertainment that are cumulatively driving consumption of luxury items in the Kingdom is growing the Kingdom’s luxury market at an estimated 12% CAGR to provide plastic luxury packaging demand that is growing at a brisk pace.

The luxury status of Dubai as a luxury duty-free shopping destination (Dubai International Airport is estimated to produce more than USD 2.1 billion of annual luxury retail activities) generates a high-value market interest in high-end packaging, which will be distinctive in a travel retail setting. The emerging luxury consumer market in Nigeria, Kenya, South Africa, and Morocco in Africa is the next stage of luxury market growth, and premium beauty products with luxurious packaging of plastic are getting into the markets through systematic retailing growth.

Top Players in the Market and Their Offerings

- Albéa Group

- HCP Packaging

- ABA-PGS (Techniques Plastiques Group)

- Quadpack Industries S.A.

- RPC Group (Berry Global)

- Aptar Group Inc.

- Silgan Holdings Inc.

- Graham Packaging Company

- Cosmopak Corporation

- Libo Cosmetics Company Ltd.

- Yoshino Kogyosho Co. Ltd.

- Others

Key Developments

The market has experienced tremendous changes with industry players trying to promote sustainable luxury packaging functions, incorporate digital authentication protocols, increase production capacity in the Asian Pacific, and react to the sustainability promises of luxury brands that have led to material innovation investments in the global luxury plastic supply chain of luxury packaging.

- In October 2024: Albéa Group, the largest beauty packaging company in the world, declared the commercial introduction of the PCR Luxe acrylic packaging line, which uses 30, 50 and 100% recycles of post-consumer PMMA material in its high-end skincare jar, bottle, and compact range.

- In January 2025: Aptar Group released the Iconic Refill System, a universal refillable luxury pump dispenser system where the outer pump housing is a high-gloss acrylic material designed to last 10+ years in consumer use, and the inner cartridge is interchangeable -launched in skincare, foundation, and serum programs, designed to fit many brands of its customers.

Such strategic actions have enabled companies to consolidate market positions, develop sustainable luxury packaging material capabilities in line with brand sustainability commitments, make investments in refillable packaging architectures in line with the requirements of the circular economy, and increase manufacturing presence in strategically significant markets and capitalize on the significant growth potential presented by expanding luxury markets globally, prestige beauty premiumization, and the rising importance of packaging as a core and strategically important luxury brand equity investment across all principal application categories and geographies.

The Plastic Luxury Packaging Market is segmented as follows:

By Material Type

- Acrylic (PMMA)

- Polycarbonate (PC)

- PET & RPET

- ABS (Acrylonitrile Butadiene Styrene)

- Polypropylene (PP)

- Bio-Based & Recycled Polymers (Bio-PET, PCR-PMMA, PLA)

- Other Materials (SAN, TPE, Nylon)

By Packaging Type

- Bottles & Jars

- Boxes & Cases (Compacts, Palettes, Gift Cases)

- Tubes & Cartridges

- Caps & Closures (Pumps, Sprayers, Disc Tops)

- Bags & Pouches (Rigid-Structured and Flexible Luxury)

- Other Packaging Types (Applicators, Display Components)

By Application

- Cosmetics & Personal Care (Skincare, Makeup, Haircare)

- Fragrance & Perfumery

- Spirits & Premium Beverages

- Jewelry & Watches

- Fashion & Apparel Accessories

- Other Applications (Gourmet Food, Nutraceuticals)

By End-User

- Absolute Luxury (Ultra-Premium, Haute Couture Brands)

- Aspirational Luxury (Accessible Premium Brands)

- Mass Prestige (Masstige, Affordable Luxury)

By Distribution Channel

- Specialty Luxury Retailers (Mono-Brand Boutiques)

- Department Stores & Multi-Brand Luxury Retail

- Online Luxury Retail (Brand.com and Luxury E-tailers)

- Duty-Free & Travel Retail

- Other Channels (Direct-to-Consumer, Subscription Boxes)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Plastic Luxury Packaging by Segments

- 2.1.2. Plastic Luxury Packaging by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Plastic Luxury Packaging Market Attractiveness Analysis, By Material Type

- 2.2.3. Plastic Luxury Packaging Market Attractiveness Analysis, By Packaging Type

- 2.2.4. Plastic Luxury Packaging Market Attractiveness Analysis, By Application

- 2.2.5. Plastic Luxury Packaging Market Attractiveness Analysis, By End-User

- 2.2.6. Plastic Luxury Packaging Market Attractiveness Analysis, By Distribution Channel

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Global Luxury Market Expansion and Emerging Economy Aspirational Consumer Growth

- 3.1.2. Premiumization of Beauty and Personal Care Driving Sophisticated Packaging Demand

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Plastic Luxury Packaging Market – By Material Type

- 4.1. Material Type Market Overview, By Material Type Segment

- 4.1.1. Plastic Luxury Packaging Market Revenue Share, By Material Type, 2025 & 2035

- 4.1.2. Acrylic (PMMA)

- 4.1.3. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Polycarbonate (PC)

- 4.1.7. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. PET & RPET

- 4.1.11. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. ABS (Acrylonitrile Butadiene Styrene)

- 4.1.15. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Polypropylene (PP)

- 4.1.19. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Bio-Based & Recycled Polymers (Bio-PET, PCR-PMMA, PLA)

- 4.1.23. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1.26. Other Materials (SAN, TPE, Nylon)

- 4.1.27. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 4.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.29. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Material Type Market Overview, By Material Type Segment

- Chapter 5. Plastic Luxury Packaging Market – By Packaging Type

- 5.1. Packaging Type Market Overview, By Packaging Type Segment

- 5.1.1. Plastic Luxury Packaging Market Revenue Share, By Packaging Type, 2025 & 2035

- 5.1.2. Bottles & Jars

- 5.1.3. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Boxes & Cases (Compacts, Palettes, Gift Cases)

- 5.1.7. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Tubes & Cartridges

- 5.1.11. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Caps & Closures (Pumps, Sprayers, Disc Tops)

- 5.1.15. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Bags & Pouches (Rigid-Structured and Flexible Luxury)

- 5.1.19. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Other Packaging Types (Applicators, Display Components)

- 5.1.23. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Packaging Type Market Overview, By Packaging Type Segment

- Chapter 6. Plastic Luxury Packaging Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Plastic Luxury Packaging Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Cosmetics & Personal Care (Skincare, Makeup, Haircare)

- 6.1.3. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Fragrance & Perfumery

- 6.1.7. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Spirits & Premium Beverages

- 6.1.11. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Jewelry & Watches

- 6.1.15. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Fashion & Apparel Accessories

- 6.1.19. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Other Applications (Gourmet Food, Nutraceuticals)

- 6.1.23. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Plastic Luxury Packaging Market – By End-User

- 7.1. End-User Market Overview, By End-User Segment

- 7.1.1. Plastic Luxury Packaging Market Revenue Share, By End-User, 2025 & 2035

- 7.1.2. Absolute Luxury (Ultra-Premium, Haute Couture Brands)

- 7.1.3. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Aspirational Luxury (Accessible Premium Brands)

- 7.1.7. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Mass Prestige (Masstige, Affordable Luxury)

- 7.1.11. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-User Market Overview, By End-User Segment

- Chapter 8. Plastic Luxury Packaging Market – By Distribution Channel

- 8.1. Distribution Channel Market Overview, By Distribution Channel Segment

- 8.1.1. Plastic Luxury Packaging Market Revenue Share, By Distribution Channel, 2025 & 2035

- 8.1.2. Specialty Luxury Retailers (Mono-Brand Boutiques)

- 8.1.3. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 8.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.5. Key Market Trends, Growth Factors, & Opportunities

- 8.1.6. Department Stores & Multi-Brand Luxury Retail

- 8.1.7. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 8.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.9. Key Market Trends, Growth Factors, & Opportunities

- 8.1.10. Online Luxury Retail (Brand.com and Luxury E-tailers)

- 8.1.11. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 8.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.13. Key Market Trends, Growth Factors, & Opportunities

- 8.1.14. Duty-Free & Travel Retail

- 8.1.15. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 8.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.17. Key Market Trends, Growth Factors, & Opportunities

- 8.1.18. Other Channels (Direct-to-Consumer, Subscription Boxes)

- 8.1.19. Plastic Luxury Packaging Share Forecast, By Region (USD Billion)

- 8.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.21. Key Market Trends, Growth Factors, & Opportunities

- 8.1. Distribution Channel Market Overview, By Distribution Channel Segment

- Chapter 9. Plastic Luxury Packaging Market – Regional Analysis

- 9.1. Plastic Luxury Packaging Market Overview, By Region Segment

- 9.1.1. Global Plastic Luxury Packaging Market Revenue Share, By Region, 2025 & 2035

- 9.1.2. Global Plastic Luxury Packaging Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 9.1.3. Global Plastic Luxury Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.1.4. Global Plastic Luxury Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 9.1.5. Global Plastic Luxury Packaging Market Revenue, By Application, 2026 – 2035

- 9.1.6. Global Plastic Luxury Packaging Market Revenue, By End-User, 2026 – 2035

- 9.1.7. Global Plastic Luxury Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 9.2. North America

- 9.2.1. North America Plastic Luxury Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.2.2. North America Plastic Luxury Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.2.3. North America Plastic Luxury Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 9.2.4. North America Plastic Luxury Packaging Market Revenue, By Application, 2026 – 2035

- 9.2.5. North America Plastic Luxury Packaging Market Revenue, By End-User, 2026 – 2035

- 9.2.6. North America Plastic Luxury Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 9.2.7. U.S. Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.8. Canada Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.9. Mexico Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.10. Rest of North America Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3. Europe

- 9.3.1. Europe Plastic Luxury Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.3.2. Europe Plastic Luxury Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.3.3. Europe Plastic Luxury Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 9.3.4. Europe Plastic Luxury Packaging Market Revenue, By Application, 2026 – 2035

- 9.3.5. Europe Plastic Luxury Packaging Market Revenue, By End-User, 2026 – 2035

- 9.3.6. Europe Plastic Luxury Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 9.3.7. Germany Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.8. France Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.9. U.K. Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.10. Russia Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.11. Italy Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.12. Spain Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.13. Netherlands Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.14. Rest of Europe Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4. Asia Pacific

- 9.4.1. Asia Pacific Plastic Luxury Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.4.2. Asia Pacific Plastic Luxury Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.4.3. Asia Pacific Plastic Luxury Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 9.4.4. Asia Pacific Plastic Luxury Packaging Market Revenue, By Application, 2026 – 2035

- 9.4.5. Asia Pacific Plastic Luxury Packaging Market Revenue, By End-User, 2026 – 2035

- 9.4.6. Asia Pacific Plastic Luxury Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 9.4.7. China Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.8. Japan Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.9. India Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.10. New Zealand Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.11. Australia Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.12. South Korea Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.13. Taiwan Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.14. Rest of Asia Pacific Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5. The Middle-East and Africa

- 9.5.1. The Middle-East and Africa Plastic Luxury Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.5.2. The Middle-East and Africa Plastic Luxury Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.5.3. The Middle-East and Africa Plastic Luxury Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 9.5.4. The Middle-East and Africa Plastic Luxury Packaging Market Revenue, By Application, 2026 – 2035

- 9.5.5. The Middle-East and Africa Plastic Luxury Packaging Market Revenue, By End-User, 2026 – 2035

- 9.5.6. The Middle-East and Africa Plastic Luxury Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 9.5.7. Saudi Arabia Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.8. UAE Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.9. Egypt Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.10. Kuwait Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.11. South Africa Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.12. Rest of the Middle East & Africa Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.6. Latin America

- 9.6.1. Latin America Plastic Luxury Packaging Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.6.2. Latin America Plastic Luxury Packaging Market Revenue, By Material Type, 2026 – 2035

- 9.6.3. Latin America Plastic Luxury Packaging Market Revenue, By Packaging Type, 2026 – 2035

- 9.6.4. Latin America Plastic Luxury Packaging Market Revenue, By Application, 2026 – 2035

- 9.6.5. Latin America Plastic Luxury Packaging Market Revenue, By End-User, 2026 – 2035

- 9.6.6. Latin America Plastic Luxury Packaging Market Revenue, By Distribution Channel, 2026 – 2035

- 9.6.7. Brazil Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.6.8. Argentina Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.6.9. Rest of Latin America Plastic Luxury Packaging Market Revenue, 2026 – 2035 (USD Billion)

- 9.1. Plastic Luxury Packaging Market Overview, By Region Segment

- Chapter 10. Competitive Landscape

- 10.1. Company Market Share Analysis – 2025

- 10.1.1. Global Plastic Luxury Packaging Market: Company Market Share, 2025

- 10.2. Global Plastic Luxury Packaging Market Company Market Share, 2024

- 10.1. Company Market Share Analysis – 2025

- Chapter 11. Company Profiles

- 11.1. Albéa Group

- 11.1.1. Company Overview

- 11.1.2. Key Executives

- 11.1.3. Product Portfolio

- 11.1.4. Financial Overview

- 11.1.5. Operating Business Segments

- 11.1.6. Business Performance

- 11.1.7. Recent Developments

- 11.2. HCP Packaging

- 11.3. ABA-PGS (Techniques Plastiques Group)

- 11.4. Quadpack Industries S.A.

- 11.5. RPC Group (Berry Global)

- 11.6. Aptar Group Inc.

- 11.7. Silgan Holdings Inc.

- 11.8. Graham Packaging Company

- 11.9. Cosmopak Corporation

- 11.10. Libo Cosmetics Company Ltd.

- 11.11. Yoshino Kogyosho Co. Ltd.

- 11.12. Others.

- 11.1. Albéa Group

- Chapter 12. Research Methodology

- 12.1. Research Methodology

- 12.2. Secondary Research

- 12.3. Primary Research

- 12.3.1. Analyst Tools and Models

- 12.4. Research Limitations

- 12.5. Assumptions

- 12.6. Insights From Primary Respondents

- 12.7. Why Custom Market Insights

- Chapter 13. Standard Report Commercials & Add-Ons

- 13.1. Customization Options

- 13.2. Subscription Module For Market Research Reports

- 13.3. Client Testimonials

List Of Figures

Figures No 1 to 47

List Of Tables

Tables No 1 to 56

Prominent Player

- Albéa Group

- HCP Packaging

- ABA-PGS (Techniques Plastiques Group)

- Quadpack Industries S.A.

- RPC Group (Berry Global)

- Aptar Group Inc.

- Silgan Holdings Inc.

- Graham Packaging Company

- Cosmopak Corporation

- Libo Cosmetics Company Ltd.

- Yoshino Kogyosho Co. Ltd.

- Others

FAQs

The key players in the market are Albéa Group, HCP Packaging, ABA-PGS (Techniques Plastiques Group), Quadpack Industries S.A., RPC Group (Berry Global), Aptar Group Inc., Silgan Holdings Inc., Graham Packaging Company, Cosmopak Corporation, Libo Cosmetics Company Ltd., Yoshino Kogyosho Co. Ltd., Others.

The range of plastic luxury packaging price is wide in line with the unbelievable variety of quality levels, design sophistication, decoration sophistication, and material specifications in the category: standard acrylic jars of cosmetic grade are USD 0.80 to USD 2.50 per unit; luxury acrylic jars with multiple steps of decoration are USD 3.00 to USD 12.00 per unit; and high-end acrylic or polycarbonate boxes custom-made are USD 15.00 to USD 80.00 Luxury pump and closure parts will be sold at USD 1.50 to USD 15.00 per unit of standard airless pump systems and USD 8.00 to USD 45.00 per unit of high end luxury metal-effect decoration, magnetic closure, and tactile surface treatment finish pump assemblies. The refillable packaging premium – in which primary refillable outer components are priced 40-120% more than comparable single-use outer components to reflect their improved life cycle and improvement in material and engineering complexity – are causing a structural pricing growth in the luxury packaging market since brand promises of refillability are triggering specification upgrades. The increased addition of smart packaging elements, NFC chips, AR triggers, and authentication functionalities costs USD 0.15-USD 2.50 per unit of packaging component depending on the level of technological sophistication, thus forming a new high-end segment of luxury packaging pricing that brands are recouping through brand protection and brand engagement returns on investment.

According to the current analysis, the market is expected to reach about USD 19.87 billion in 2035 due to the global expansion of the luxury market to the range of EUR 500–540 in the luxury market and the resulting proportional growth in luxury packaging systems in all of its forms of consumption, at a CAGR of 8.1% between 2026 and 2035.

Europe is anticipated to continue to control the largest share of revenue during the forecast period with a share of about 34% of the global market share in 2025, owing to its unrivaled concentration of global headquarters of the world’s most prestigious luxury brands creating demand in domestic packaging sourcing and worldwide leadership in the global supply chain, the most advanced luxury packaging designing and manufacturing ecosystem in the world with the base in France and Italy, EUR 145+ billion of the world’s most luxury goods revenues concentrated in LVMH, L’Oréal, Kering and related brands forming the largest and associated brands generating the world’s largest and most premium luxury packaging procurement base, Europe’s leadership in sustainable luxury packaging innovation driven by the EU’s PPWR and brand sustainability commitments establishing European luxury packaging as the global sustainability benchmark, and the concentration of the world’s most technically demanding luxury packaging specifications in European luxury brand development programs that drive continuous premium packaging innovation investment.

Asia Pacific will be the quickest CAGR in growth at 11.3% over the forecast period due to recovery and expansion of the EUR 59 billion luxury goods market in China; growing luxury purchasing frequency, expansion of luxury packaging innovation in the world-leading K-beauty industry across South Korea and China due to the Pearl River Delta luxury goods manufacturing cluster delivering world-class acrylic and polycarbonate luxury packaging at 2540 cost of manufacturing benefits over European competitors attracting international brand sourcing investment, the luxury consumer segment in India growing three times by 2030 creating a new major luxury market requiring appropriate premium packaging supply chain development, and Japan and South Korea’s sophisticated travel retail ecosystems generating high-value concentrated luxury packaging demand at the world’s highest-luxury-spending airport and cruise retail environments.

The Global Plastic Luxury Packaging Market is expected to be dramatically growing, with the global luxury market valued at EUR 363 billion in 2024 and forecasted to increase to EUR 500-EUR 540 billion in 2030 as a driver of packaging as a brand advocate and brand loyalty via purchase creation, the recyclability of acrylic packaging is 92-93%, which is close to glass and achieves 40-60% relative economies of scale over metallic and glass in making premium polymer packaging commercially superior across most luxury applications, 68% of luxury consumers under 35 are are willing to pay up to 12% premiums for sustainable luxury packaging in 2024 (Deloitte research validating sustainable luxury packaging business case); refillable luxury packaging systems are generating secondary purchase occasions and deepening consumer brand engagement while reducing packaging material waste by up to 73% per refill, and the global luxury e-commerce market is projected to grow from USD 74 billion in 2024 to USD 178 billion by 2030 driving unboxing experience packaging investment as a brand advocacy and repeat purchase driver.