Low Voltage DC Circuit Breaker Market Size, Trends and Insights By Type (Molded Case Circuit Breakers (MCCB), Miniature Circuit Breakers (MCB), Air Circuit Breakers (ACB), Insulated Case Circuit Breakers (ICCB), Other Types (Solid-State Circuit Breakers, Hybrid)), By Voltage Rating (Up to 250V, 251V–500V, 501V–750V, Above 750V (up to 1,500V)), By Application (Solar PV Systems, Battery Energy Storage Systems (BESS), Electric Vehicles & Charging Infrastructure, Data Centers & Telecom, Industrial Automation & Machinery, Marine & Shipboard Power, Other Applications (Railways, Microgrids)), By End-Use (Residential, Commercial, Industrial, Utility), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 9.5%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- ABB Ltd.

- Schneider Electric SE

- Eaton Corporation plc

- Siemens AG

- Others

Reports Description

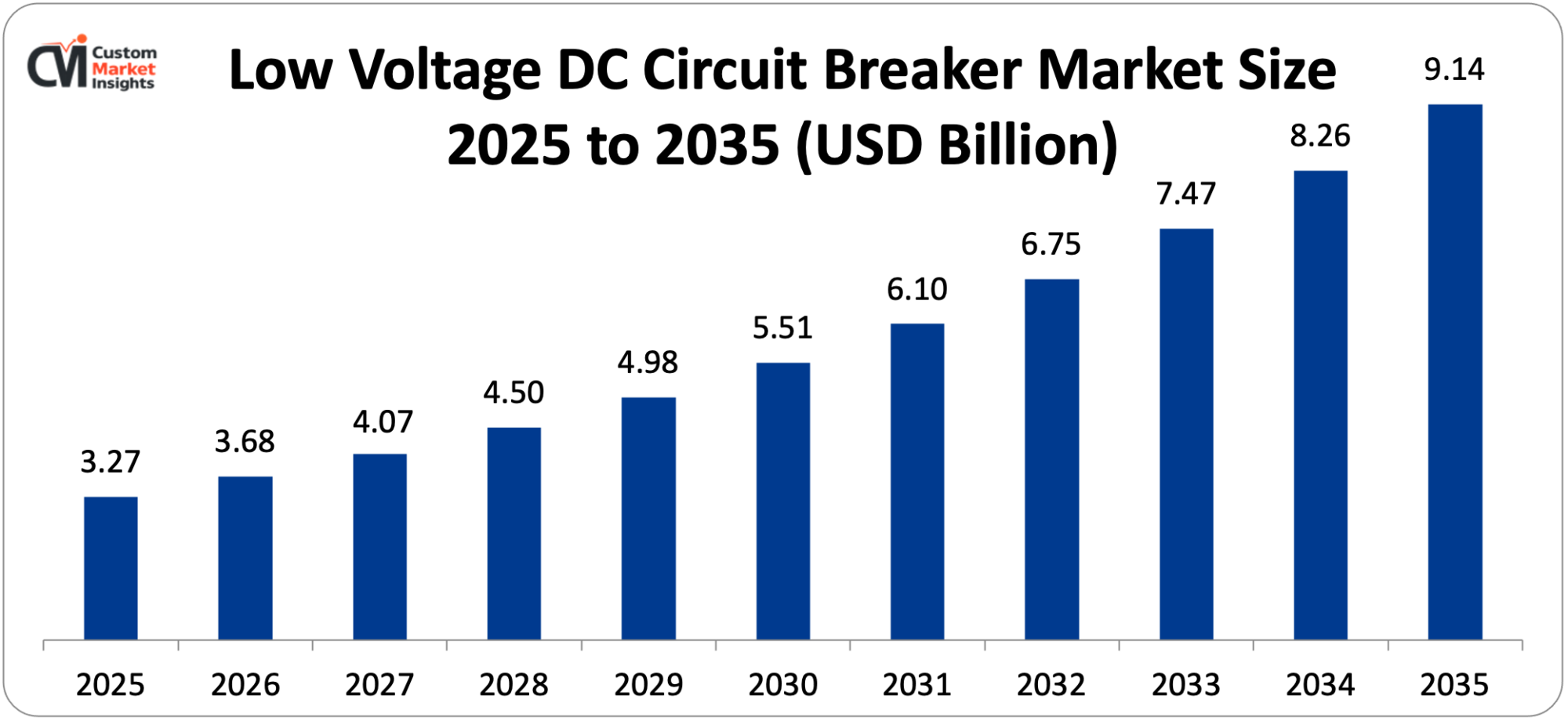

The world low voltage DC circuit breaker market is estimated at USD 3.27 billion in 2025 and it is expected to grow its market to USD 3.68 billion by 2026 and about USD 9.14 billion in 2035 with a CAGR of 9.5% between 2026 and 2035. The rising pace of deployment of solar photovoltaic generation systems that necessitate dedicated DC protection equipment, the rapid growth of battery energy storage systems in utility transmission, commercial, and residential sectors that demand special DC circuit protection, the unprecedented growth of electric vehicle charge systems that have generated multiple new market segments that need DC circuit protection, the incremental adoption of DC microgrids in data centers and operating plants that is offering energy savings opportunities over traditional AC distribution, and ongoing growth of DC circuit breaker technology that provides dependable arc interruption on higher voltages and fault currents are all contributors to vigorous and sustained market growth throughout the forecast period.

Market Highlight

- Asia Pacific The Asia pacific market leader with a low voltage DC circuit breaker market share of 41% in 2025.

- North America is likely to grow at a CAGR of 9.8% between 2026 and 2035.

- By design, the cases’ circuit breakers are molded and segmented at 38% of the market share.

- Projected is the miniature circuit breakers segment by type, with the highest CAGR of 11.2% between 2026 and 2035.

- Under voltage rating, the largest market share of 34 was recorded on the 251 V-500 V segment in 2025 and the segment extending over 750 V is projected to give the highest CAGR of 14.3 in the period between 2026 and 2035.

- The solar PV systems segment has contributed the largest market share of 36% in 2025, and the battery energy storage systems segment will have the highest CAGR of 15.8% between 2026 and 2035.

- By 2025, the commercial segment will take 31% of the market share, and the utility segment will be the fastest CAGR at 13.4% between 2026 and 2035.

Significant Growth Factors

The Low Voltage DC Circuit Breaker Market Trends present significant growth opportunities due to several factors:

- Solar PV Deployment Acceleration Creating Foundational DC Protection Demand: The underlying and largest building block contributor to low voltage DC circuit breaker demand is the unprecedented pace of global solar PV adoption, triggered by the plummeting solar module prices, ambitious renewable energy policies in major economies, uptake of corporate power purchase agreements, and the economical feasibility of residential rooftop solar generation, each of which would necessitate dedicated DC circuit breaker protection equipment on the generation side of the inverter operating at DC voltages between 48V in small residential systems and 1,500V in utility scale systems. According to the International Energy Agency in their report, Renewables 2023, solar PV capacity additions have reached record levels in 2023 with approximately 415 GW of solar capacity worldwide being added with solar being the largest source of new capacity additions of electricity-generating capacity in the fourth year in a row, and this translates directly into the need for DC protection equipment to be installed at every facility. Every megawatt of installed solar PV power will need DC circuit protection equipment that includes string combiners with DC fuses or miniature DC circuit breakers at the string level, DC molded case circuit breakers or DC air circuit breakers at the array combiner box level, and DC main circuit breakers between the DC collection system and the inverter – with the overall cost of the DC circuit protection equipment per MW of solar PV installation between USD 3,000 and USD 15,000 based on the system voltage, the complexity of the system configuration, and the product specifications The shift towards a 1500 V DC system architecture in large commercial and utility scale solar systems (and, in place of 1000 V architecture) is also resulting in a demand for DC circuit breakers with higher voltages to interrupt arc faults, which is much harder to do at 1500 V than at 1000 V since the arc voltage needed to limit arc current is greater to achieve current limiting. The IEA estimates that solar PV capacity will keep increasing significantly by 2030 in all energy transition scenarios, and solar will be the largest source of new electricity generation investment in the world, which will provide a long-term growth pattern in demand for DC protection equipment, the basis of the long-term business prospect of the low voltage DC circuit breaker market.

- Battery Energy Storage System Expansion Driving Premium DC Protection Demand: Following a technological ramp-up due to the rapidly increasing use of battery energy storage systems, (both utility-scale grid storage systems, commercial and industrial behind-the-meter storage systems, and home battery storage systems) are driving one of the most technically demanding and highest-value growth segments of low voltage DC circuit breakers: Battery storage systems are defining demands on fault current characteristics that are fundamentally different than those of solar PV sources, including the ability to maintain fault current indefinitely, unlike solar PV systems that decay over The DC protection concerns of battery energy storage systems are unique and highly technically challenging: lithium-ion battery banks can achieve a very high instant fault current of 5-20 times the rated current over sustained periods, the DC voltage is continuously varying with battery state of charge over a range of 20-30% of nominal voltage, current flows in each direction during both charge and discharge, and thermal runaway propagation of lithium-ion battery systems has made interrupting fault current in both directions at extremely high instantaneous fault current especially critical in preventing catastrophic battery fire events. The battery energy storage market has been growing exceptionally worldwide, with the IEA reporting approximately 42 GW of utility-scale battery storage additions in 2023 (for example, double the additions of 2022), due to grid-scale storage additions by utilities dealing with the growing renewable energy presence, by commercial and industrial clients interested in resilience and demand charge control, and by policy support in the form of the U.S. Investment Tax Credit extension to standalone battery storage under the Inflation Reduction Act. A battery energy storage capacity of one megawatt-hour would need DC circuit protection equipment at the cell module level, battery rack level, battery cabinet level, and battery bank DC bus level a multi-level protection architecture would need 4-8 DC protection devices per battery rack and hundreds of devices in a utility-scale BESS installation.

What are the Major Advances Changing the Low Voltage DC Circuit Breaker Market Today?

- DC Arc Fault Circuit Interrupter Technology Development: Following a technological ramp due to the rapidly increasing use of battery energy storage systems, (both utility-scale grid storage systems, commercial and industrial behind-the-meter storage systems, and home battery storage systems) are driving one of the most technically demanding and highest-value growth segments of low voltage. DC circuit breakers: Battery storage systems are defining demands on fault current characteristics that are fundamentally different than those of solar PV sources, including the ability to maintain fault current indefinitely, unlike solar PV systems that decay over The DC protection concerns of battery energy storage systems are unique and highly technically challenging: lithium-ion battery banks can achieve a very high instant fault current of 5-20 times the rated current over sustained periods, the DC voltage is continuously varying with battery state of charge over a range of 20-30% of nominal voltage, current flows in each direction during both charge and discharge, and thermal runaway propagation of lithium-ion battery systems has made interrupting fault current in both directions at extremely high instantaneous fault current especially critical in preventing catastrophic battery fire events. The battery energy storage market has been growing exceptionally worldwide, with the IEA reporting approximately 42 GW of utility-scale battery storage additions in 2023 (for example, double the additions of 2022), due to grid-scale storage additions by utilities dealing with the growing renewable energy presence, by commercial and industrial clients interested in resilience and demand charge control, and by policy support in the form of the U.S. Investment Tax Credit extension to standalone battery storage under the Inflation Reduction Act. A battery energy storage capacity of one megawatt-hour would need DC circuit protection equipment at the cell module level, battery rack level, battery cabinet level, and battery bank DC bus level a multi-level protection architecture would need 4-8 DC protection devices per battery rack and hundreds of devices in a utility-scale BESS installation.

Category Wise Insights

By Type

Why Do Molded Case Circuit Breakers Lead the Market?

Molded case circuit breakers represent the largest type segment at approximately 38% of total market share in 2025, reflecting their dominant position across the highest-value DC circuit protection applications including solar PV array main protection, battery energy storage DC bus protection, DC fast charging station internal protection, and industrial DC motor drive protection — applications where the higher current ratings, higher interrupting capacity, and adjustable trip settings of MCCB designs are required and justify the higher unit cost relative to MCB alternatives. DC-rated MCCBs — which must meet substantially more demanding arc interruption requirements than equivalent AC MCCBs of the same current rating given DC’s absence of natural current zero crossings — are engineered with enhanced arc extinguishing chamber designs, stronger contact operating mechanisms, and permanent magnetic arc blowout systems that increase manufacturing cost but provide the reliable DC arc interruption at voltages of 250–1,500V that solar PV, battery storage, and industrial DC applications require. Leading DC MCCB product lines, including ABB’s Tmax XT DC series, Schneider Electric’s ComPact NSX DC, Eaton’s NZM DC series, and Siemens’ 3VA Molded Case Circuit Breaker for DC applications represent mature, well-validated products with established track records in solar and industrial applications that command customer confidence and justify premium pricing of 40–80% above equivalent AC MCCB products of similar current rating. The solar PV application’s progressive adoption of 1,500V DC architecture — which has become the industry standard for utility-scale and large commercial installations given the balance-of-system cost savings from higher DC voltage operation — is driving demand specifically for 1,500V-rated DC MCCBs at the string combiner and inverter input circuit breaker positions, with 1,500V DC MCCB designs commanding the highest unit pricing within the MCCB segment.

By Voltage Rating

Why Does the 251V–500V Segment Lead the Market?

The 251 V-500 V and above voltage rating segment is the largest segment with about 34% of the market share in 2025 and includes the DC voltage range most commonly used in commercial and light industrial solar PV systems, residential and commercial battery energy storage systems, telecom power infrastructure, and DC motor drives. This voltage range falls within the working voltage range of most commercial scale solar PV string inverter systems—300-500V at maximum power point is a typical string voltage in rooftop commercial systems – and the nominal voltage of most commonly deployed lithium-ion battery energy storage chemistry systems of residential and light commercial storage. It is also the most common range of voltage (251 V to 500 V) at which telecom and data center DC power distribution operates—the ETSI 300 V and 380 V DC distribution standard used by many telecom operators and hyperscale data centers such as Google, Microsoft, and Meta to implement their DC power distribution systems represents the largest single deployment of the voltage range that is known.

By Application

Why Does Solar PV Systems Lead the Market?

The Sun PV systems form the most important application segment with some 36% of the overall market share in 2025 demonstrating solar as the greatest installed and increasing DC electrical generation technology worldwide, with the need of specific DC circuit protection throughout the entire collection, conditioning, and interconnection system. The solar PV implementation includes DC circuit breaker specifications at different system levels (5–20A and 500–1500V), individual string protection, array combiner box protection by 100–1000A, and the main DC disconnect between the solar array and inverter by the highest system current levels (4–12 DC circuit breakers per inverter string group DC circuit breaker requirements at different system levels depending on system design. Solar DC protection equipment industry The set requirements of the IEC 62548 (Design requirements for PV arrays) and the NEC Article 690 in the United States of America (mandatory protection levels, rating criteria, and certification requirements) are advantageous to the solar DC protection equipment market, as they allow predictable and well-defined circuit protection requirements to standardize the procurement specifications of DC circuit breakers across the global solar installation market and provide manufacturers with clear standards by which to establish the development of products.

By End-Use

Why Does the Commercial Segment Lead the Market?

The commercial end-use segment is the largest segment with more than 31% of market share in 2025, with a large-scale commercial solar PV market comprising rooftop solar on commercial and industrial buildings, solar carports, and ground-mounted commercial solar facilities, along with the growing commercial and industrial battery storage market and the DC fast charging infrastructure serving commercial transportation fleets and the commercial data center DC power distribution market, each representing the highest-value commercial DC electrical infrastructure investment. Commercial solar and storage installations usually demand more highly specified DC circuit breakers having larger current ratings, higher interrupting capacity, and communication interfaces than residential applications – fetching a higher price that makes commercial segments’ revenue exceed their proportion of the installation base. The unit of fastest growth to 2035 is the utility end-use sector, which is due to solar PV systems being used at utility scale, reaching multi-hundred MW and GW; the growth in grid-scale battery storage installations using hundreds of MWh of a project; and the DC collection systems of large renewable energy parks being connected to the transmission system, which require high-current and high-voltage DC circuit protection at the utility grade.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 3.68 billion |

| Projected Market Size in 2035 | USD 9.14 billion |

| Market Size in 2025 | USD 3.27 billion |

| CAGR Growth Rate | 9.5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Voltage Rating, Application, End-Use and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

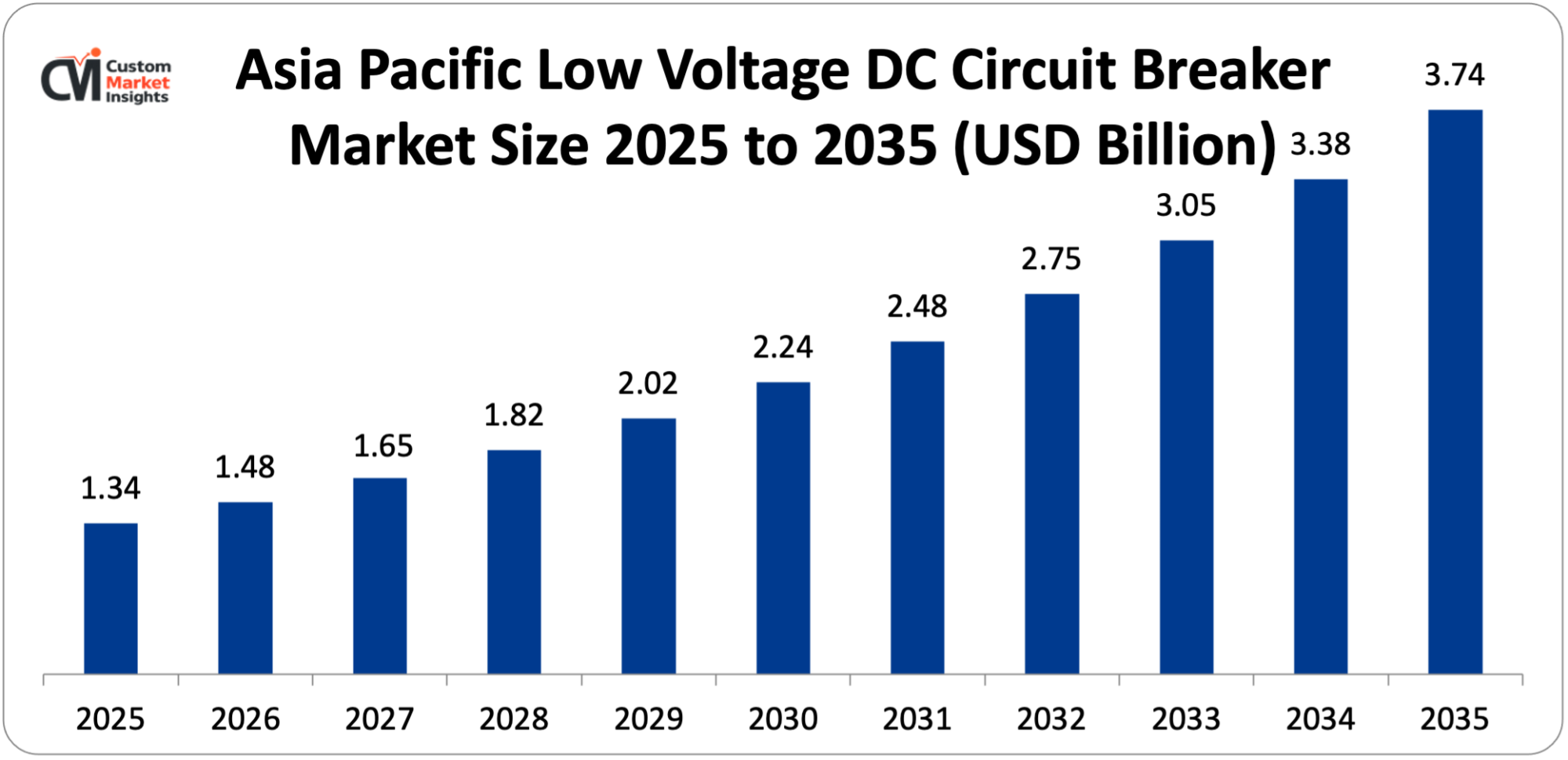

The Asia Pacific low voltage DC circuit breaker market size is estimated at USD 1.34 billion in 2025 and is projected to reach approximately USD 3.74 billion by 2035, with a CAGR of 10.8% from 2026 to 2035.

Why Did Asia Pacific Dominate the Market in 2025?

Asia Pacific controls a market share of about 41% globally in 2025, with the region constituting the largest geographical solar PV installation market in the world; the biggest and fastest growing battery energy storage deployment, the largest global EV market, where charging infrastructure investments are made to serve both domestic and export markets, and where major DC circuit breaker manufacturers such as Chint Group, Delixi Electric, LS Electric, Mitsubishi Electric, and Fuji Electric all base manufacturing plants in Asia to manufacture their products. The scale of solar PV deployment in China, its economic support based on the most extensive solar manufacturing supply chain in the world, where more than 80% of the global solar module manufacturing is produced, generates demand for DC protection equipment at an unprecedented scale; and every year of solar installations has solar implementation requirements of hundreds of millions of individual DC circuit breakers in the string and at the combiner and inverter levels. The national battery storage targets of China, which are instigated by a series of Five-Year Plans and grid modernization plans, are motivating the utility-scale and commercial storage applications that produce high-current, high-voltage DC MCCB purchases in great volume by Chinese and foreign manufacturers. The bustling solar program of India, aiming to have 500 GW of renewable energy capacity by 2030, is creating the booming demand of DC circuit breakers in India, with both local producers and global suppliers of circuit breakers competing to meet the high volumes of annual purchasing that are produced by the Indian solar rooftop program and solar park development.

Why is North America Experiencing Rapid Growth?

North America is also in rapid growth with a projected CAGR of 9.8% overall between 2026 and 2035 due to the transformative renewable energy investment incentives offered under the Inflation Reduction Act – the production tax credit extension and investment tax credit provisions are making the U.S. undergo a multi-year solar and battery storage investment boom, the NEVI program’s USD 5 billion EV charging network investment is creating DC fast charging station DC protection demand, the U.S. utility-scale battery storage market is increasing rapidly under standalone ITC provisions, and the progressive modernization of U.S. data center infrastructure toward DC power distribution architectures that improve energy efficiency relative to conventional AC distribution systems.

Why is Europe a Strategically Important Market?

The European low voltage DC circuit breaker market is projected to have a market size of about USD 718 million in 2025 with an estimated market size of about USD 1.69 billion in the year 2035 with a CAGR of 8.9. Europe is a market of unique strategic value fueled by the REPowerEU EU plan to reach 600 GW of solar capacity by the next 2030 – creating a large-scale need for massive DC protection equipment in residential, commercial and utility-scale solar systems – Germany is the largest solar market in Europe with aggressive capacity growth, the Alternative Fuels Infrastructure Regulation requires DC fast charging coverage infrastructure and grid-wide; and battery storage targets in the EU support the deployment of BESS at grid scale requiring high-performance DC circuit breaker protection equipment. The Energiewende energy transition program in Germany, the largest ever national renewable energy transformation program in the world expressed in units of national GDP, is producing continuous volumes of solar and storage installations that make Germany a large market in Europe as an individual DC circuit breaker.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region is showing an increasing market development due to the large-scale solar deployment programs of Saudi Arabia and the UAE under vision 2030 and the UAE Net Zero 2050 strategy – with solar PV projects such as the Al Dhafra Solar PV project in Abu Dhabi representing 2 GW of DC generation and extensive use of DC protection equipment; the emerging EV charger network in the Middle East due to government electrification programs, the growing rooftop solar market in Brazil, which has expanded considerably with the declining solar costs providing good economics to both residential and commercial installations, and South Africa’s emergency power generation programs incorporating solar PV and battery storage to address the country’s electricity supply challenges.

Top Players in the Market and Their Offerings

- ABB Ltd.

- Schneider Electric SE

- Eaton Corporation plc

- Siemens AG

- Legrand SA

- Mitsubishi Electric Corporation

- Fuji Electric Co. Ltd.

- Chint Group Corporation

- Delixi Electric Co. Ltd.

- Hager Group

- LS Electric Co. Ltd.

- Others

Key Developments

The market has undergone significant developments as industry participants seek to advance 1,500V DC circuit breaker capabilities, expand smart protection product portfolios, and respond to the extraordinary investment wave in solar, storage, and EV charging infrastructure globally.

- In October 2024: ABB also publicized the sales release of a new Tmax XT5-DC 1,500 V molded case circuit breaker series – extending its established Tmax XT platform to 1,500 V DC operation at current ratings between 16 A and 630 A—specifically to the utility-scale and large commercial 1,500 V DC architecture market segment where 1,500 V DC has become the industry standard of cost optimization of a balance-of-system.

- In December 2024: Schneider Electric announced integrating its line of Acti9 Active smart DC circuit breakers into the EcoStruxure Energy Management platform – providing real-time monitoring of solar performance at the string level, bi-directional energy flow monitoring of solar-plus-storage systems, and automated demand response with cloud-linked circuit breaker remote switching capabilities – Schneider Electric will be targeting commercial building owners operating solar and battery storage systems who want non-discrete energy intelligence beyond the standalone monitoring platforms that the inverter manufacturers have offered them heretofore.

The Low Voltage DC Circuit Breaker Market is segmented as follows:

By Type

- Molded Case Circuit Breakers (MCCB)

- Miniature Circuit Breakers (MCB)

- Air Circuit Breakers (ACB)

- Insulated Case Circuit Breakers (ICCB)

- Other Types (Solid-State Circuit Breakers, Hybrid)

By Voltage Rating

- Up to 250V

- 251V–500V

- 501V–750V

- Above 750V (up to 1,500V)

By Application

- Solar PV Systems

- Battery Energy Storage Systems (BESS)

- Electric Vehicles & Charging Infrastructure

- Data Centers & Telecom

- Industrial Automation & Machinery

- Marine & Shipboard Power

- Other Applications (Railways, Microgrids)

By End-Use

- Residential

- Commercial

- Industrial

- Utility

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Low Voltage DC Circuit Breaker by Segments

- 2.1.2. Low Voltage DC Circuit Breaker by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Low Voltage DC Circuit Breaker Market Attractiveness Analysis, By Type

- 2.2.3. Low Voltage DC Circuit Breaker Market Attractiveness Analysis, By Voltage Rating

- 2.2.4. Low Voltage DC Circuit Breaker Market Attractiveness Analysis, By Application

- 2.2.5. Low Voltage DC Circuit Breaker Market Attractiveness Analysis, By End-Use

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Solar PV Deployment Acceleration Creating Foundational DC Protection Demand

- 3.1.2. Battery Energy Storage System Expansion Driving Premium DC Protection Demand

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Low Voltage DC Circuit Breaker Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Low Voltage DC Circuit Breaker Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Molded Case Circuit Breakers (MCCB)

- 4.1.3. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Miniature Circuit Breakers (MCB)

- 4.1.7. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Air Circuit Breakers (ACB)

- 4.1.11. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Insulated Case Circuit Breakers (ICCB)

- 4.1.15. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Other Types (Solid-State Circuit Breakers, Hybrid)

- 4.1.19. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Low Voltage DC Circuit Breaker Market – By Voltage Rating

- 5.1. Voltage Rating Market Overview, By Voltage Rating Segment

- 5.1.1. Low Voltage DC Circuit Breaker Market Revenue Share, By Voltage Rating, 2025 & 2035

- 5.1.2. Up to 250V

- 5.1.3. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. 251V–500V

- 5.1.7. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. 501V–750V

- 5.1.11. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Above 750V (up to 1,500V)

- 5.1.15. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Voltage Rating Market Overview, By Voltage Rating Segment

- Chapter 6. Low Voltage DC Circuit Breaker Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Low Voltage DC Circuit Breaker Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Solar PV Systems

- 6.1.3. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Battery Energy Storage Systems (BESS)

- 6.1.7. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Electric Vehicles & Charging Infrastructure

- 6.1.11. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Data Centers & Telecom

- 6.1.15. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Industrial Automation & Machinery

- 6.1.19. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Marine & Shipboard Power

- 6.1.23. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1.26. Other Applications (Railways, Microgrids)

- 6.1.27. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 6.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.29. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Low Voltage DC Circuit Breaker Market – By End-Use

- 7.1. End-Use Market Overview, By End-Use Segment

- 7.1.1. Low Voltage DC Circuit Breaker Market Revenue Share, By End-Use, 2025 & 2035

- 7.1.2. Residential

- 7.1.3. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Commercial

- 7.1.7. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Industrial

- 7.1.11. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Utility

- 7.1.15. Low Voltage DC Circuit Breaker Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-Use Market Overview, By End-Use Segment

- Chapter 8. Low Voltage DC Circuit Breaker Market – Regional Analysis

- 8.1. Low Voltage DC Circuit Breaker Market Overview, By Region Segment

- 8.1.1. Global Low Voltage DC Circuit Breaker Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Low Voltage DC Circuit Breaker Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Low Voltage DC Circuit Breaker Market Revenue, By Type, 2026 – 2035

- 8.1.4. Global Low Voltage DC Circuit Breaker Market Revenue, By Voltage Rating, 2026 – 2035

- 8.1.5. Global Low Voltage DC Circuit Breaker Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Low Voltage DC Circuit Breaker Market Revenue, By End-Use, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Low Voltage DC Circuit Breaker Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Low Voltage DC Circuit Breaker Market Revenue, By Type, 2026 – 2035

- 8.2.3. North America Low Voltage DC Circuit Breaker Market Revenue, By Voltage Rating, 2026 – 2035

- 8.2.4. North America Low Voltage DC Circuit Breaker Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Low Voltage DC Circuit Breaker Market Revenue, By End-Use, 2026 – 2035

- 8.2.6. U.S. Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Low Voltage DC Circuit Breaker Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Low Voltage DC Circuit Breaker Market Revenue, By Type, 2026 – 2035

- 8.3.3. Europe Low Voltage DC Circuit Breaker Market Revenue, By Voltage Rating, 2026 – 2035

- 8.3.4. Europe Low Voltage DC Circuit Breaker Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Low Voltage DC Circuit Breaker Market Revenue, By End-Use, 2026 – 2035

- 8.3.6. Germany Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Low Voltage DC Circuit Breaker Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Low Voltage DC Circuit Breaker Market Revenue, By Type, 2026 – 2035

- 8.4.3. Asia Pacific Low Voltage DC Circuit Breaker Market Revenue, By Voltage Rating, 2026 – 2035

- 8.4.4. Asia Pacific Low Voltage DC Circuit Breaker Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Low Voltage DC Circuit Breaker Market Revenue, By End-Use, 2026 – 2035

- 8.4.6. China Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Low Voltage DC Circuit Breaker Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Low Voltage DC Circuit Breaker Market Revenue, By Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Low Voltage DC Circuit Breaker Market Revenue, By Voltage Rating, 2026 – 2035

- 8.5.4. The Middle-East and Africa Low Voltage DC Circuit Breaker Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Low Voltage DC Circuit Breaker Market Revenue, By End-Use, 2026 – 2035

- 8.5.6. Saudi Arabia Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Low Voltage DC Circuit Breaker Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Low Voltage DC Circuit Breaker Market Revenue, By Type, 2026 – 2035

- 8.6.3. Latin America Low Voltage DC Circuit Breaker Market Revenue, By Voltage Rating, 2026 – 2035

- 8.6.4. Latin America Low Voltage DC Circuit Breaker Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Low Voltage DC Circuit Breaker Market Revenue, By End-Use, 2026 – 2035

- 8.6.6. Brazil Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Low Voltage DC Circuit Breaker Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Low Voltage DC Circuit Breaker Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Low Voltage DC Circuit Breaker Market: Company Market Share, 2025

- 9.2. Global Low Voltage DC Circuit Breaker Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. ABB Ltd.

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Schneider Electric SE

- 10.3. Eaton Corporation plc

- 10.4. Siemens AG

- 10.5. Legrand SA

- 10.6. Mitsubishi Electric Corporation

- 10.7. Fuji Electric Co. Ltd.

- 10.8. Chint Group Corporation

- 10.9. Delixi Electric Co. Ltd.

- 10.10. Hager Group

- 10.11. LS Electric Co. Ltd.

- 10.12. Others.

- 10.1. ABB Ltd.

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 38

List Of Tables

Tables No 1 to 51

Prominent Player

- ABB Ltd.

- Schneider Electric SE

- Eaton Corporation plc

- Siemens AG

- Legrand SA

- Mitsubishi Electric Corporation

- Fuji Electric Co. Ltd.

- Chint Group Corporation

- Delixi Electric Co. Ltd.

- Hager Group

- LS Electric Co. Ltd.

- Others

FAQs

The key players in the market are ABB Ltd., Schneider Electric SE, Eaton Corporation plc, Siemens AG, Legrand SA, Mitsubishi Electric Corporation, Fuji Electric Co. Ltd., Chint Group Corporation, Delixi Electric Co. Ltd., Hager Group, LS Electric Co. Ltd., Others.

The government regulations have a decisive impact on the low voltage DC circuit breaker market by the electrical safety codes that require circuit protection requirements, renewable energy incentive programs that will drive the volumes of installations, EV infrastructure investment programs that create DC charging demand, and product certification standards that define the performance specifications that DC circuit breakers must meet to comply with the regulations in each market. Article 690 of the U.S. National Electrical Code, which covers solar photovoltaic systems, and Article 706 that cover energy storage systems, establish required DC circuit breaker protection, the maximum circuit protection device versus equipment current protection, arc fault circuit interrupter requirements, and rapid shutdown provisions that together form the DC circuit breaker requirements of all solar and storage systems in the United States. The IEC 60947-2 standard of low voltage circuit breakers, which is adopted as the reference standard used to certify DC circuit breakers in most international markets, defines the performance requirements of DC circuit breakers such as rated current, interrupting capacity, operating voltage, and endurance which DC circuit breakers are required to fulfill during type testing to obtain certification to enter the market under the IEC-framework. The Low Voltage Directive and the related CE marking requirements of the EU and the UL 489 and UL 489B listing requirements of the molded case and photovoltaic circuit breakers respectively, are the product certification systems that the DC circuit breaker manufacturers must be mindful of to enter the markets and the certification fee and schedule costs is a substantial impediment to market entry of a new manufacturer and a competitive moat around an established certified product portfolio. The GB/T standards of low voltage circuit breakers are administered by the Standardization Administration of China and outline similar national performance and certification requirements that both domestic and international manufacturers of DC circuit breakers must meet to have access to domestic and international markets in China, respectively. The continued work of the International Electrotechnical Commission on standards directly concerning battery energy storage system protection, e.g. in the new standard IEC 62619 on lithium-ion batteries and in the newly developing IEC TC69 on EV infrastructure, is gradually creating the technical requirements that DC circuit breakers in the storage and EV charging market must satisfy and the regulatory component that both drives investment in the technology over time and justifies the high price of new products and services that meet it.

The prices of low voltage DC circuit breakers are in a broad range in terms of types, voltage ratings, current ratings, and performance characteristics that are prevalent in the market. Residential grade DC MCBs to protect solar strings are the highest volume product type, costing USD 15–80 per unit based on current rating (6A–63A) and voltage capability (500V or 1000V), with Chinese manufacturers such as Chint and Delixi offering products at the low end of this category, whereas manufacturers in Europe are able to charge small premiums on their established certification and brand name. Solar array Modular Commercial and industrial DC MCCBs – at current ratings of 100A to 630A – cost USD 200 to USD 3000 apiece based on current rating, interrupting current, and voltage rating. Utility-scale solar and large commercial applications: 1,500 V DC MCCBs cost USD 800-USD 5,000 each, due to the technical complexity of 1,500 V DC arc interruption and the small number of manufacturers able to make certified 1,500 V DC products. DC air circuit breakers in the largest current applications, such as utility scale BESS main protection and large solar inverter protection, are priced at USD 3,000-USD 25,000 apiece. The DC circuit breakers used in solid state (commercially offered in small quantities since 2005) have high premiums of 5-15 times comparable electromechanical products, limiting their use to applications where the speed of interruption is worth the money. The even greater price premium of DC circuit breakers over similar AC breakers, typically 40120% in the case of MCCB and 3060% in the case of MCB, is a reflection of the additional engineering complexity of DC arc interruption (which the company has), and is a cost factor that still has to be systematically lowered with volume production and increased manufacturing efficiency.

According to the current analysis, the market is estimated to reach about USD 9.14 billion in 2035 due to the scaling of deployment of solar PV systems to meet the net zero targets of the IEA that will sustain a decade-long cycle of DC string and array protection procurement, battery energy storage deployment is accelerating across utility, commercial, and residential applications as the lithium-ion battery prices decrease and the economics of grid-scale storage is improving under carbon-pricing conditions, DC fast charging infrastructure is scaling to serve the projected global fleet of hundreds of millions of vehicles requiring a charging network expansion, solid-state DC circuit breaker technology commercializing and capturing premium market segments in data center and battery storage applications as SiC power device costs decline, the progressive adoption of DC microgrid architectures in data centers, commercial buildings, and industrial facilities creating new DC distribution protection requirements beyond the solar and storage applications dominating current demand, and Asia Pacific’s continued deployment acceleration adding China, India, and Southeast Asian market growth that collectively sustain above-GDP market expansion throughout the forecast period, at a CAGR of 9.5% from 2026 to 2035.

Asia Pacific will continue to take the largest share of revenue during the forecast period, with an estimated market share of about 41% of the overall market share in 2025, due to China as the world leader in solar PV deployment, dominance in the battery storage market making up a major market share in the region, and the largest market share in the EV and charging infrastructure market in the world with a leading concentration of major DC circuit breaker manufacturers in Asia Pacific, which provides competitive cost advantages in the region, consolidating market leadership position.

It is estimated that Asia Pacific will continue to have the largest market share and grow at a strong rate of 10.8% CAGR through the forecast period due to the fact that China is adding over 200 GW of solar every year, which requires DC protection equipment, India has a 500 GW renewable energy goal and is quickly adding solar and battery storage deployments; and cost-effective manufacturing of DC circuit breakers has become concentrated in the hands of Chint, Deluxi, LS Electric, Mitsubishi Electric, and Fuji Electric, which can provide competitive pricing that supports adoption across both premium and value market segments.

The IEA has estimated an addition of approximately 415 GW of global solar PV capacity additions in 2023, the largest annual addition of any electricity generation technology in the history of the world, is projected to result in a substantial growth of the Global Low Voltage DC Circuit Breaker Market as the individual protection equipment required at every battery-store installation, each charging station, and every installation in the battery storage and EV charging market. the IEA reports a doubling of utility-scale battery storage capacity additions to approximately 42 GW in 2023 creating a demand for premium bidirectional DC circuit protection equipment meeting lithium-ion battery fault current characteristics. the U.S. The Inflation Reduction Act’s investment tax credit extension to standalone battery storage is driving a multi-year U.S. BESS procurement boom requiring high-current DC MCCB investment, the USD 5 billion NEVI program is driving DC fast charging infrastructure deployment across the U.S. national highway system requiring DC circuit protection at each charging station, the EU’s REPowerEU plan targeting 600 GW of solar by 2030 is creating a decade-long European DC protection equipment procurement wave; NEC Article 690 DC AFCI requirements are driving residential and commercial solar DC arc fault protection device adoption; and solid-state DC circuit breaker technology is advancing toward commercial deployment with microsecond interruption times, enabling superior protection for sensitive power electronics in battery storage and EV charging applications.