Power Schottky Diode Market Size, Trends and Insights By Material Type (Silicon (Si), Silicon Carbide (SiC), Gallium Nitride (GaN), Other Material Types (Germanium, Gallium Arsenide)), By Package Type (Surface Mount (SOD, SMA, SMB, SMC, PowerDI, DPAK, D2PAK), Through-Hole (DO-41, DO-15, DO-201, Axial Lead), Chip Scale Package (WLCSP, Flip-Chip), Other Package Types (Press-Fit, Power Module Integrated)), By Application (Power Supplies & Converters (SMPS, Server PSU, Adapters), Motor Drives & Inverters, Solar & Renewable Energy (Bypass Diodes, String Inverters, Microinverters), Electric Vehicles & Charging Infrastructure, Consumer Electronics (Smartphones, Laptops, Wearables), Telecommunications & Data Centers, Other Applications (Railways, Medical Equipment)), By End-Use Industry (Automotive, Industrial, Consumer Electronics, Telecommunications & Data Centers, Energy & Power, Other Industries (Medical, Defense, Aerospace)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 8.7%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- Infineon Technologies AG

- ON Semiconductor (onsemi)

- STMicroelectronics N.V.

- Vishay Intertechnology Inc.

- Others

Reports Description

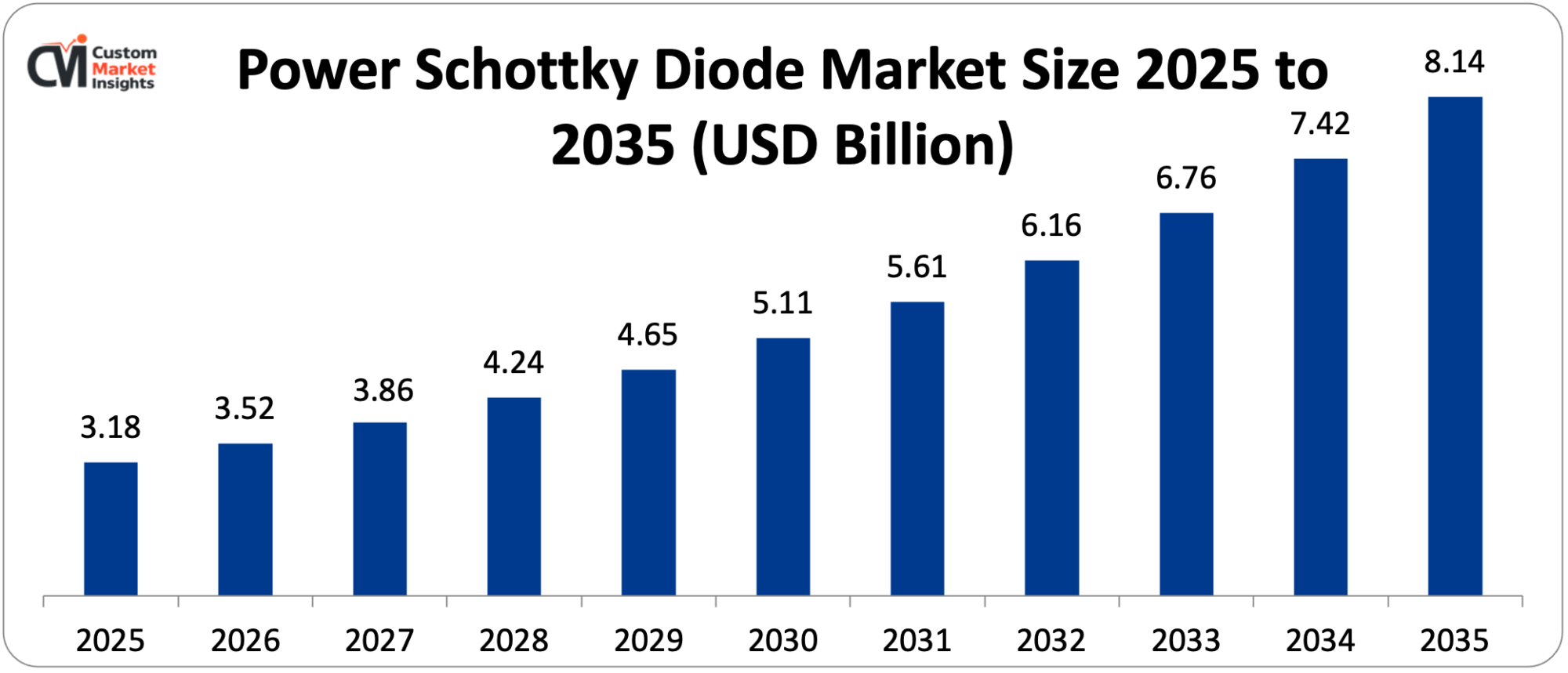

The size of the global market of Schottky diodes is estimated to grow to USD 3.52 billion in 2026 and is expected to grow to around USD 8.14 billion by 2035 with a CAGR of 8.7% between 2026 and 2035.

The increased electric vehicle adoption and electric vehicle demand of high-efficiency power conversion devices in traction inverters, on-board chargers, and DC-DC converters, the high power conversion demand of high-frequency rectification and power factor correction devices across solar photovoltaic and wind systems, the increasing use and growing demand of switching power supplies in data centers and telecommunications infrastructure with the low forward voltage drop and near-zero reverse recovery time of Schottky diodes, the strong and steady market growth through the forecast period are due to the high demand and low cost of silicon carbide Schottky diodes enabling higher operating temperatures and blocking voltages than silicon alternatives across demanding power electronics applications and the expanding consumer electronics market driving miniaturized surface mount Schottky diode demand collectively driving robust and sustained market growth throughout the forecast period.

Market Highlight

- In 2025, the Asia Pacific controlled a 44% market share of power Schottky diodes.

- North America will grow at a CAGR of 8.4% in the period of 2026-2035.

- By type of the material, the silicon segment was able to take about 62% of the market share as of 2025.

- By material type, the silicon carbide (SiC) segment has the highest CAGR of 18.6% between the years 2026 and 2035.

- By type of package, the surface mount segment had the largest market share of 54% in 2025 and the surface mount segment had a CAGR of 9.8% in the predicted years of 2026-2035.

- By segment, the power supplies and converters segment paid off the largest market share of 31% in 2025 with the solar and renewable energy segment anticipated to experience the quickest CAGR of 12.4% between the years 2026 and 2035.

- By end-use industry, the industrial segment had 28% of market share in 2025 with the automotive segment projected to have the highest CAGR of 16.2% between 2026 and 2035.

Significant Growth Factors

The Power Schottky Diode Market Trends present significant growth opportunities due to several factors:

- Electric Vehicle Power Electronics Revolution Driving Premium Schottky Diode Demand:

The unprecedented world-wide acceleration of electric vehicle adoption, due to the declining cost of lithium-ion batteries, the development of charging infrastructure, the enforced adoption of zero-emission vehicles by governments, and the increasing accessibility of the EV model across the car line, is driving one of the largest and fastest-growing sources of demand for power Schottky diodes, since every electric car has a number of power electronics subsystems that are subject to the high-efficiency rectification and freewheeling diode functions, where Schottky technology provides significant improvements in system efficiency. It is being reported by the International Energy Agency that global electric vehicle sales are currently reaching around 14 million units in 2023, with international EV sales expected to reach 40 million units annually by 2030 under stated policy conditions—a sales curve that directly translates into an increase in power Schottky diode purchases by automotive power electronics manufacturers worldwide.

A battery electric vehicle has Schottky diodes in a variety of subsystems: the on-board charger, which transforms AC grid power into DC to charge the batteries, needs Schottky rectifier diodes in its power factor correction stage and secondary rectification stage where forward voltage drop is directly proportional to charger energy loss in each charging cycle; the DC-DC converter, which transforms the high-voltage battery bus to the 12V or 48V auxiliary electrical system, needs high-efficiency Schottky rectification to ensure minimum conversion losses across the hundreds of amps.

The largest growth market in the premium SiC Schottky diode product line is the increased use of silicon carbide Schottky diodes in on-board chargers and DC-DC converters used in EVs, and in DC-DC converters used in the DC-AC conversion of large-scale DC power systems, replacing silicon Schottky diodes and allowing higher switching frequencies, higher operating temperatures, and higher power density at equivalent efficiency, with Tesla, BYD, Volkswagen Group, and Hyundai-Kia being leading manufacturers of EVs using silicon carbide power devices such The EV charging infrastructure market, including the Level 2 AC chargers, Level 3 DC fast chargers and the newer megawatt charging systems of commercial vehicles, needs power electronics that use the Schottky diode at the rectifier and power factor correction steps of each individual charging unit of the USD 5 billion EV charging network investment by the U.S. NEVI program.

- Renewable Energy Expansion and Power Conversion Efficiency Mandates Driving Market Growth:

The growing and fast worldwide adoption of solar photovoltaic and wind energy generation systems – establishing unexampled amounts of need of high-efficiency power conversion electronics, such as string inverters, central inverters, microinverters and power optimizers converting DC solar generation or AC wind generation to grid-appropriate AC power – is creating significant and increasing mathematical demand on power Schottky diodes in numerous different functional positions within renewable power conversion systems where their high performance attributes over conventional PN junction rectifiers are beneficial to energy yield.

The Schottky bypass diodes used in solar PV systems (such as installed across the individual solar cell strings in the PV module to eliminate reverse voltage damage to shaded cells) are currently some of the most volume-intensive applications of Schottky bypass diodes in the world, with a typical 6072 cell solar module using 3-6 Schottky bypass diodes that help protect the operation of the module when partially shaded. The fact that the IEA reports that about 415 GW of solar PV in the world were added in 2023, and every installed MW of solar PV capacity brings in about 2,000-4,000 Schottky bypass diodes, spreading them among the module array, implies that the demand on the manufacturers of solar modules alone is in the hundreds of millions of Schottky bypass diodes each year.

The use of Schottky diodes in the power factor correction and boost converter stages of string inverters and microinverters converts minibox-scale converters and introduces 0.520 percentage-point efficiency advantages over the comparable converter circuit with conventional fast recovery diodes that is due to the zero reverse recovery charge of Schottky devices at the switching frequencies of 16200 kHz, which removes switching-transmission efficiency losses due to the current spike and switching loss caused by high-frequency rectification at the switching frequency. The worldwide imperative of renewable energy efficiency improvement (by energy yield maximization at fixed installed infrastructure cost) causes even a fraction of a percent power conversion efficiency increment to be commercially important, and solar plant operators and inverter manufacturers seek code improvements to reduce parasitic losses and enhance energy recovery throughout the 25-30 year operational life of installed solar equipment.

What are the Major Advances Changing the Power Schottky Diode Market Today?

- Silicon Carbide Schottky Diode Technology Commercialization and Cost Reduction:

The approaching obsolescence of silicon Schottky diodes by silicon carbide Schottky diodes in an increasingly wider set of demanding high-performance power electronics uses is possible due to the combined efforts of the following:

- 1) the commercial maturation of silicon carbide Schottky diodes with the high-volume shipment growth stimulus needed to significantly increase the activators’ market share.

- 2) the simultaneous expansion of SiC wafer fabrication capacity, improvement of the epitaxial growth process, enhanced yield in the development of silicon carbide Schottky diodes, and The basic material performance of silicon carbide in power Schottky diode applications include a critical value of the electric field strength about 10 times greater than silicon – allowing SiC Schottky diodes to conduct voltages of 600 V to 1700 V with dramatically thinner drift layers than silicon, a bandgap of 3.26 eV versus 1.12 eV in silicon, allowing continuous operation of junction temperatures up to 175 o C and peak operation up to 200 o C under high power density operating conditions, and This removal of reverse recovery charge, the characteristic strength of Schottky diodes over PN junction diodes, is preserved in SiC Schottky diodes by a totally different mechanism than in silicon Schottky devices. although silicon Schottky diodes can accomplish low reverse recovery by exploiting the high-conduction majority carrier conduction of the metal-semiconductor junction that does not store minority carriers, SiC Schottky diodes with a junction barrier Schottky (JBS) structure can do so despite it having to operate at 600 V-1 The best-known commercial offerings of SiC Schottky diodes are the Thinline SiC Schottky diode series of Infineon Technologies, the SiC Schottky diode portfolio of ON Semiconductor, the SiC Schottky diodes of Wolfspeed (formerly Cree), and the SiC Schottky product line of STMicroelectronics, with these companies continually lowering the price of SiC Schottky diodes through the scale-up of manufacture at 150mm and 200mm wafer diameter, which lowers costs.

The downward path of SiC substrate and epitaxy cost-bringing development – of billions of dollars invested by Wolfspeed, STMicroelectronics, Infineon, onsemi, and newcomers such as Coherent (formerly II-VI) in SiC manufacturing.

- High-Frequency Power Conversion System Design Enabling Schottky Technology Advantages:

The gradual rise in switching frequencies used in power conversion systems, motivated by the desire of power electronics designers to achieve an ever-higher power density by using smaller magnetic parts, which switching frequency reduction makes possible, and facilitated by the enhanced switching performance of the current GaN and SiC power transistors, which allow switching losses to depend on switching frequency and whose near-zero reverse recovery eliminates this scaling component of switching losses, is steadily moving the competitive situation towards Schottky diodes and away from them. At lower switching frequencies of 16-100 kHz—as in a traditional silicon IGBT-based power converter – fast recovery diodes can be used to achieve mediocre efficiency in synchronous rectification with appropriate drive timing. Nevertheless, in applications where converters based on GaN and SiC transistors drive switching frequencies to 100 kHz–1 MHz (e.g., server power supplies, EV onboard chargers, wireless power transfer systems, etc.), reverse recovery losses of standard PN diodes become the leading contributors of converter losses that Schottky diodes can eliminate.

The efficiency standards of power supply, such as the 80 PLUS certification program of server and desktop power supplies with an efficiency rating of 80 to 96% (Titanium grade), the efficiency standards of the ErP directive of the European Commission and efficiency standards of the external power supply of the U.S. department of energy, provide regulatory and commercial incentives to power supply designers to use the most efficient rectification technology possible, which again is regularly Schottky diodes in front-end PFC boost converter and secondary rectification steps where Schottky technology offers the efficiency advantage to satisfy certification Improvement in data center power supply efficiency is facilitated by the hypersensitivity of hyperscale data center operators to the power usage effectiveness (PUE) of electricity as an operating expense dominates.

- Packaging Technology Innovation Enabling Miniaturization and Higher Power Density:

The ever-increasing power Schottky diode deployment technology such as the expansion of wafer-level chip-scale packages (WLCSP), dual-die packages that combine two Schottky diodes on one footprint, and low-inductance surface mount packages, is being put into operation in high-frequency circuits, and the development of high-performance thermal interface materials to allow more power to be dissipated in smaller packages is enabling the initiation of power Schottky diode applications in ever-smaller sizes and power-dense electronic system environments where the traditional package formats are no longer compatible with Surface mount Schottky diode packages such as SOD-123, SOD-323, DO-214AA (SMA), DO-214AB (SMB), DO-214AC (SMC), and PowerDI product families – have become the most popular package format in consumer electronics, telecommunications, and industrial use, with the miniaturization of packages being propelled by the incremental progressively greater density of modern PCB designs by apportioning smaller and smaller areas of the board to each discrete component such as rectifier diodes.

PowerPAK and DirectFET surface mount packages, with a flip-chip mounting of the Schottky diode on the lead frame of the package with no wire bond, providing a package thermal resistance of 0.5 – 2°C/W at rated current, compared to 5 – 15°C/W of standard through-hole packages, allow very high power dissipation in a small PCB footprint, which is very important in automotive and industrial Schottky diode uses where the ambient temperature and power density factor is pushing package thermal performance to its extremes. The two-die, dual common-cathode and dual common-anode Schottky diode package configurations, i.e. using two identical diodes in one package, sharing a cathode or anode connection respectively, are common in three-phase rectifier bridge, voltage clamping and flyback converter secondary rectification systems, where a single package boasts twice the number of diodes but they can be shared using fewer connections.

Category Wise Insights

By Material Type

Why Does Silicon Lead the Market?

Silicon is the most dominant material type segment with a market share of about 62% of all market share in 2025, as silicon has proven to dominate most commercial Schottky diode applications in terms of individual unit volume and revenue due to its decades of manufacturing maturity, the widespread availability of the global silicon semiconductor fabrication infrastructure affording to produce competitive volumes of silicon at low cost, and the wide range of blocking voltage of 20 V to 200 V where silicon Schottky technology offers a unique performance-price-quality balance with low forward Silicon Schottky diodes are commercially fabricated devices using existing metal evaporation and alloying technologies etched on p type or n type silicon epitaxial substrates in standard semiconductor fab manufacturing facilities and realize forward current drops of 0.2 -0.45V at rated current levels based on current rating, blocking voltage and metal contact system, which gives the rectification efficiency advantage defining the Schottky diode value proposition in consumer electronics power management, PC peripheral charging, low-voltage telecommunications equipment, and solar module bypass diode designs.

Substantial competitive supply in the silicon Schottky diode market is provided by large international semiconductor manufacturers as well as a large number of Asian commodity producers of silicon Schottky diodes, including many Chinese, Taiwanese and South Korean manufacturers who have set up silicon Schottky diode fabrication capacity in the high volume, low price, commodity markets of consumer electronics and standard power supply. The main technical drawback of silicon Schottky diodes is the exponentially growing reverse current as the blocking voltage rating becomes larger than 200 V, which becomes unacceptably large at higher voltages needed in industrial and automotive power electronics. This sets the demarcation beyond which silicon carbide Schottky technology offers necessary performance benefits to warrant its higher price.

By Package Type

Why Does Surface Mount Lead the Market?

Surface mount package, the largest segment of the package type market at about 54% of the market in 2025, is the result of overwhelming adoption of surface mount technology (SMT) in modern PCB assembly through consumer electronics, telecommunications, automotive electronics, and industrial control markets, where through-hole component assembly has been phased out of new designs in favor of surface mount components that can be assembled with automated pick-and-place assembly and solder reflow processes that incur low assembly cost and high production throughput compared to the through-hole insertion and wave soldering.

The SOD-123 and SOD-323 packages – one of the most widely used surface mount Schottky diode packages to date – have component footprints of 1.6mm x 0.8mm and 1.2mm x 0.8mm respectively, which allows component packing densities in the end product to be highly efficient in the limited resource of board area. Higher-powered Schottky diode applications such as automotive DC-DC converters, industrial motor drive freewheeling functions, and higher-current switching power supply rectification, where the thermal demand of the heater must be addressed substantially beyond the thermal performance capability offered by fully encapsulated surface mount packages, typically use the DPAK (TO-252) and D2PAK (TO-263) package forms, which have exposed metal pads on the underside of the package to provide efficient heat transfer to the PCB copper thermal planes. The chip scale package and the wafer-level packaging format are enjoying a particularly high growth rate in smartphone charging IC and wearable device applications, where the smallest possible component footprint is needed, with WLC-packaged Schottky diodes having component sizes of 0.4mm x 0.4mm the smallest commercially available power rectifier footprint.

By Application

Why Do Power Supplies & Converters Lead the Market?

Power supplies and converters are the most significant application area at about 31% of the overall market share in 2025 due to the universal need for Schottky diodes in switched-mode power supplies to power virtually every electronic device in the manufacturing of electronics worldwide, SMPS designs with Schottky diodes in the rectification of output, power factor correction boost converter diode operations, and snubber circuits, which collectively amount to huge annual Schottky diode purchases in the electronics manufacturer supply industry. One of the most technically challenging and commercially important Schottky diode application areas is the server power supply market, which is being driven by an unprecedented growth in data center capacity that is being driven by cloud computing, AI model training and the growing demand on digital services that is driving the overall efficiency above 96% on server power supplies that are being certified by 80 PLUS Titanium, which requires the lowest possible rectifier voltage drop to be achieved by premium Schottky diode selection. As a standard server application, 750W-3000W each server power supply unit — incorporates multiple Schottky diodes in the secondary rectification stage and PFC boost converter stage, with the global data center power supply market consuming hundreds of millions of Schottky diodes annually at price points reflecting both the commodity silicon Schottky devices used in standard efficiency tiers and premium devices used in platinum and titanium efficiency tier products.

By End-Use Industry

Why Does the Industrial Segment Lead the Market?

The industrial end-use segment is the largest segment with a market share of about 28% in 2025, due to the wide and varied range of Schottky diode applications in industrial motor drives, industrial switching power supplies, programmable logic controllers, robotics and automation equipment, instrumentation, and industrial communication infrastructure of the industrial electronics market – the largest and most diverse collection of Schottky diode applications.

The applications of industrial Schottky diodes cover the whole industry product line, extending to high-voltage SiC devices in 3-phase industrial motor drive rectifier bridges at 600 V-1200 V blocking levels to low-voltage silicon devices in 5 V and 12 V industrial control circuit power supplies. The fastest-growing automotive market at 16.2% CAGR between 2026 and 2035 is because the EV powertrain transition has created a demand for on-board chargers and DC-DC converters of automobile manufacturers at royalties of SiC Schottky diodes, the electrification of automotive auxiliary systems, such as electric power steering, air conditioning compressors and 48V mild hybrid systems is using Schottky diodes in power electronics and the increasing numbers of advanced driver assistance system (ADAS) controllers and radar systems are creating demand for high-reliability silicon Schottky diodes in automotive radar and sensor power management circuits.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 3.52 billion |

| Projected Market Size in 2035 | USD 8.14 billion |

| Market Size in 2025 | USD 3.18 billion |

| CAGR Growth Rate | 8.7% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Material Type, Package Type, Application, End-Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

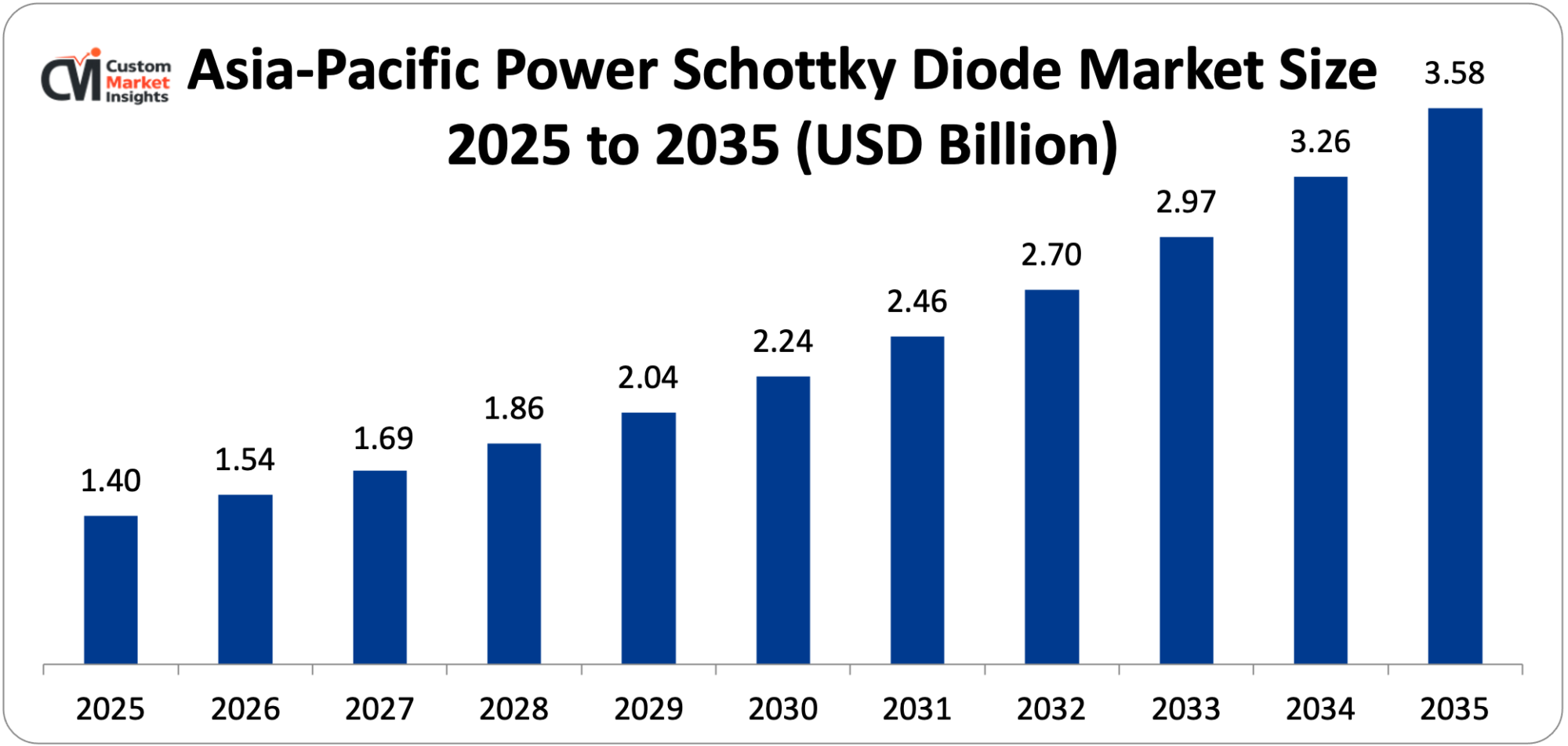

The Asia Pacific power Schottky diode market size is estimated at USD 1.40 billion in 2025 and is projected to reach approximately USD 3.58 billion by 2035, with a CAGR of 9.8% from 2026 to 2035.

Why Did Asia Pacific Dominate the Market in 2025?

The control of some 44% of market share in 2025 suggests that Asia Pacific is the dominant geography of the world’s electronics manufacturing, where most global consumer electronics, smartphones, laptops, and industrial electronics manufacturing are concentrated and where most of the world’s solar PV installation market creates the demand for electronics bypass diodes in solar modules, the primary focus of the global EV market, with the concentration of major Schottky diode manufacturers such as ROHM Semiconductor (Japan), Toshiba (Japan), and many Taiwanese and Chinese diode manufacturers.

The immense volumes of solar PV installations in China, which increased its new solar capacity to more than 200 GW by 2023 according to the National Energy Administration, are creating billions of units of solar module bypass diode demand each year between Chinese and foreign solar module manufacturers with manufacturing plants concentrated in the Yangtze River Delta and Pearl River Delta industrial belts. A significant market for silicon and SiC Schottky diodes in automotive power electronics applications is the automotive electronics sector of Japan, which serves Toyota, Honda, Nissan, and their vast system of tier-1 automotive suppliers; the Japanese automotive sector is increasingly electrifying schemes in which Japanese automotive electronics manufacturers are specifying SiC Schottky diodes in power electronics designs.

Why is North America Experiencing Rapid Growth?

North America is undergoing a rapid growth trend with a projected CAGR of 8.4% between 2026 and 2035, due to the renewable energy and EV incentives in the Inflation Reduction Act that create a vast solar, storage, and EV charging infrastructure investment, which creates Schottky diode demand, the surging expansion of U.S. data center capacity through artificial intelligence compute demand creating server power supply demand, and Wolfspeed investing heavily in manufacturing SiC in North Carolina to create U.S. domestic infrastructure to supply SiC to the automotive and industrial customers prioritizing supply chain resilience.

Why is Europe a Strategically Important Market?

The Schottky diode market is approximated to be USD 668 million in 2025 and an approximated USD 1.52 billion in 2035 with a CAGR of 8.6. Europe is a market of strategic core significance guided by the fact that Germany is the largest automotive electronics market in Europe – with the Volkswagen Group, BMW, and Mercedes-Benz and their long-established Tier-1 supplier base of Bosch, Continental, and Infineon Technologies consuming large volumes of SiC in EV power electronics designs, the EU market powered by the solar installation targets of EUREPowerEU; and the concentration of the major power Schottky diode companies such as Infineon Technologies and STMicroelectronics in Germany, Austria, and France. The largest manufacturer of SiC Schottky diodes globally and one of the primary silicon Schottky diode suppliers is Infineon Technologies, based in Munich and headquartered in Villach, Austria and Dresden, Germany, which is close to the European automotive OEM industry which gives commercial and engineering collaboration benefits to Infineon Technologies in the high-end automotive SiC Schottky diode market.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region is experiencing an increasing market development of solar energy investment programs by the Gulf Cooperation Council, with Saudi Arabia’s NEOM and renewable energy installed projects and the UAE on Mohammed bin Rashid Al Maktoum Solar Park having the largest solar installations in the Middle East and generating demand for silicon Schottky bypass diodes; Brazil has become one of the fastest-growing solar markets in the world; and the South African power generation project including the renewable energy procured under the REIPPPP program, is generating solar-powered inverter power electronics components demand.

Top Players in the Market and Their Offerings

- Infineon Technologies AG

- ON Semiconductor (onsemi)

- STMicroelectronics N.V.

- Vishay Intertechnology Inc.

- Wolfspeed Inc.

- ROHM Semiconductor

- Diodes Incorporated

- Nexperia B.V.

- Littelfuse Inc.

- Micro Commercial Components (MCC)

- Toshiba Electronic Devices & Storage Corporation

- Others

Key Developments

The market has undergone significant developments as industry participants seek to advance SiC Schottky diode manufacturing scale, expand automotive-qualified product portfolios, and respond to the extraordinary investment wave in EV, solar, and data center power electronics applications globally.

- In October 2024: Infineon Technologies declared commercial qualification and volume production of its fifth-generation CoolSiC Schottky diode platform – including a new junction barrier Schottky device architecture with cut forward voltage reduced by 15% at rated current versus the fourth-generation CoolSiC platform and at the same level of reverse leakage current at rated blocking voltage of 650 V and 1,200 V—to the EV on-board charger and industrial power supply markets, where each millivolt of forward voltage reduction would result in quantifiable efficiency enhancement of the system.

- In March 2025: STMicroelectronics has introduced a new family of 200 V silicon Schottky diodes in ultra-compact WLCSP packages with a footprint rate of 0.62mm x 0.62mm: a new family of 200 V silicon Schottky diodes with a package footprint of 0.62mm the smallest commercially available 200 V silicon diode package—specifically in next-generation ultrabook laptop charging applications.

The Power Schottky Diode Market is segmented as follows:

By Material Type

- Silicon (Si)

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Other Material Types (Germanium, Gallium Arsenide)

By Package Type

- Surface Mount (SOD, SMA, SMB, SMC, PowerDI, DPAK, D2PAK)

- Through-Hole (DO-41, DO-15, DO-201, Axial Lead)

- Chip Scale Package (WLCSP, Flip-Chip)

- Other Package Types (Press-Fit, Power Module Integrated)

By Application

- Power Supplies & Converters (SMPS, Server PSU, Adapters)

- Motor Drives & Inverters

- Solar & Renewable Energy (Bypass Diodes, String Inverters, Microinverters)

- Electric Vehicles & Charging Infrastructure

- Consumer Electronics (Smartphones, Laptops, Wearables)

- Telecommunications & Data Centers

- Other Applications (Railways, Medical Equipment)

By End-Use Industry

- Automotive

- Industrial

- Consumer Electronics

- Telecommunications & Data Centers

- Energy & Power

- Other Industries (Medical, Defense, Aerospace)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Power Schottky Diode by Segments

- 2.1.2. Power Schottky Diode by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Power Schottky Diode Market Attractiveness Analysis, By Material Type

- 2.2.3. Power Schottky Diode Market Attractiveness Analysis, By Package Type

- 2.2.4. Power Schottky Diode Market Attractiveness Analysis, By Application

- 2.2.5. Power Schottky Diode Market Attractiveness Analysis, By End-Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Electric Vehicle Power Electronics Revolution Driving Premium Schottky Diode Demand

- 3.1.2. Renewable Energy Expansion and Power Conversion Efficiency Mandates Driving Market Growth

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Power Schottky Diode Market – By Material Type

- 4.1. Material Type Market Overview, By Material Type Segment

- 4.1.1. Power Schottky Diode Market Revenue Share, By Material Type, 2025 & 2035

- 4.1.2. Silicon (Si)

- 4.1.3. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Silicon Carbide (SiC)

- 4.1.7. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Gallium Nitride (GaN)

- 4.1.11. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Other Material Types (Germanium, Gallium Arsenide)

- 4.1.15. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Material Type Market Overview, By Material Type Segment

- Chapter 5. Power Schottky Diode Market – By Package Type

- 5.1. Package Type Market Overview, By Package Type Segment

- 5.1.1. Power Schottky Diode Market Revenue Share, By Package Type, 2025 & 2035

- 5.1.2. Surface Mount (SOD, SMA, SMB, SMC, PowerDI, DPAK, D2PAK)

- 5.1.3. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Through-Hole (DO-41, DO-15, DO-201, Axial Lead)

- 5.1.7. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Chip Scale Package (WLCSP, Flip-Chip)

- 5.1.11. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Other Package Types (Press-Fit, Power Module Integrated)

- 5.1.15. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Package Type Market Overview, By Package Type Segment

- Chapter 6. Power Schottky Diode Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Power Schottky Diode Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Power Supplies & Converters (SMPS, Server PSU, Adapters)

- 6.1.3. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Motor Drives & Inverters

- 6.1.7. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Solar & Renewable Energy (Bypass Diodes, String Inverters, Microinverters)

- 6.1.11. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Electric Vehicles & Charging Infrastructure

- 6.1.15. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Consumer Electronics (Smartphones, Laptops, Wearables)

- 6.1.19. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Telecommunications & Data Centers

- 6.1.23. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1.26. Other Applications (Railways, Medical Equipment)

- 6.1.27. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 6.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.29. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Power Schottky Diode Market – By End-Use Industry

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 7.1.1. Power Schottky Diode Market Revenue Share, By End-Use Industry, 2025 & 2035

- 7.1.2. Automotive

- 7.1.3. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Industrial

- 7.1.7. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Consumer Electronics

- 7.1.11. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Telecommunications & Data Centers

- 7.1.15. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Energy & Power

- 7.1.19. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Other Industries (Medical, Defense, Aerospace)

- 7.1.23. Power Schottky Diode Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 8. Power Schottky Diode Market – Regional Analysis

- 8.1. Power Schottky Diode Market Overview, By Region Segment

- 8.1.1. Global Power Schottky Diode Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Power Schottky Diode Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Power Schottky Diode Market Revenue, By Material Type, 2026 – 2035

- 8.1.4. Global Power Schottky Diode Market Revenue, By Package Type, 2026 – 2035

- 8.1.5. Global Power Schottky Diode Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Power Schottky Diode Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Power Schottky Diode Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Power Schottky Diode Market Revenue, By Material Type, 2026 – 2035

- 8.2.3. North America Power Schottky Diode Market Revenue, By Package Type, 2026 – 2035

- 8.2.4. North America Power Schottky Diode Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Power Schottky Diode Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2.6. U.S. Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Power Schottky Diode Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Power Schottky Diode Market Revenue, By Material Type, 2026 – 2035

- 8.3.3. Europe Power Schottky Diode Market Revenue, By Package Type, 2026 – 2035

- 8.3.4. Europe Power Schottky Diode Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Power Schottky Diode Market Revenue, By End-Use Industry, 2026 – 2035

- 8.3.6. Germany Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Power Schottky Diode Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Power Schottky Diode Market Revenue, By Material Type, 2026 – 2035

- 8.4.3. Asia Pacific Power Schottky Diode Market Revenue, By Package Type, 2026 – 2035

- 8.4.4. Asia Pacific Power Schottky Diode Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Power Schottky Diode Market Revenue, By End-Use Industry, 2026 – 2035

- 8.4.6. China Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Power Schottky Diode Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Power Schottky Diode Market Revenue, By Material Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Power Schottky Diode Market Revenue, By Package Type, 2026 – 2035

- 8.5.4. The Middle-East and Africa Power Schottky Diode Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Power Schottky Diode Market Revenue, By End-Use Industry, 2026 – 2035

- 8.5.6. Saudi Arabia Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Power Schottky Diode Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Power Schottky Diode Market Revenue, By Material Type, 2026 – 2035

- 8.6.3. Latin America Power Schottky Diode Market Revenue, By Package Type, 2026 – 2035

- 8.6.4. Latin America Power Schottky Diode Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Power Schottky Diode Market Revenue, By End-Use Industry, 2026 – 2035

- 8.6.6. Brazil Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Power Schottky Diode Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Power Schottky Diode Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Power Schottky Diode Market: Company Market Share, 2025

- 9.2. Global Power Schottky Diode Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Infineon Technologies AG

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. ON Semiconductor (onsemi)

- 10.3. STMicroelectronics N.V.

- 10.4. Vishay Intertechnology Inc.

- 10.5. Wolfspeed Inc.

- 10.6. ROHM Semiconductor

- 10.7. Diodes Incorporated

- 10.8. Nexperia B.V.

- 10.9. Littelfuse Inc.

- 10.10. Micro Commercial Components (MCC)

- 10.11. Toshiba Electronic Devices & Storage Corporation

- 10.12. Others.

- 10.1. Infineon Technologies AG

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 39

List Of Tables

Tables No 1 to 51

Prominent Player

- Infineon Technologies AG

- ON Semiconductor (onsemi)

- STMicroelectronics N.V.

- Vishay Intertechnology Inc.

- Wolfspeed Inc.

- ROHM Semiconductor

- Diodes Incorporated

- Nexperia B.V.

- Littelfuse Inc.

- Micro Commercial Components (MCC)

- Toshiba Electronic Devices & Storage Corporation

- Others

FAQs

The key players in the market are Infineon Technologies AG, ON Semiconductor (onsemi), STMicroelectronics N.V., Vishay Intertechnology Inc., Wolfspeed Inc., ROHM Semiconductor, Diodes Incorporated, Nexperia B.V., Littelfuse Inc., Micro Commercial Components (MCC), Toshiba Electronic Devices & Storage Corporation, Others.

The government legislation has an effect on the power Schottky diode market on various levels, both in terms of energy efficiency standards, which create a commercial incentive to use Schottky diodes in power conversion, and in terms of EV and renewable energy policy requirements, which push volumes of installation that drive demand of Schottky diodes, as well as semiconductor exportation regulations and supply chain security regulations that affect the manufacture and trade of Schottky diodes. Energy efficiency standards on external power supplies, battery chargers, and uninterruptible power supplies set by the U.S. Department of Energy under the Energy Policy and Conservation Act set minimum efficiency levels that effectively require low-loss rectification technology in regulated product categories under which Schottky diodes enjoy an advantage over conventional PN junction diodes in energy efficiency levels that comply with and exceed regulatory requirements at lower system costs than other strategies. The Ecodesign Regulation of power supplies and external power supplies by the European Commission (for power supplies and external power supplies) of establishing minimum energy efficiency requirements and standby power limits on products sold to the market in the EU, has provided similar regulatory efficiency incentives that prefer the use of Schottky diodes in the power supply rectification step within the European consumer electronics, information technology device, and telecommunications product ranges. The USD 52 billion in domestic semiconductor manufacturing incentives that the CHIPS and Science Act provides, such as the CHIPS for America program that provides funding to advanced semiconductor fabrication and research, is favoring domestic investment in semiconductor power semiconductor manufacturing, including Wolfspeed and other U.S.-based manufacturers, as well as domestic supply of advanced semiconductor technology through the Entity List of the U.S. Commerce Department and the multilateral Wassenaar Arrangement on advanced semiconductor technology.

Power Schottky diodes are provided at a very large price range which is indicative of the variety of types of materials, voltage, current ratings, packaging, and automotive qualification. Consumer electronics Commodity silicon Schottky diodes Consumer electronics commodity silicon Schottky diodes such as SOD-123 packaged 30V/1A devices used in smartphone charging circuits and laptop power regulation cost USD 0.02 to USD 0.08 each in a large-volume purchase, making them one of the cheapest discrete semiconductor elements in the market and ubiquitous in virtually every battery-powered consumer electronic device. Industrial and telecom power supply Mid-range silicon Schottky diodes (DO-214 packed 200 V/3 A) A unit is used as a switching power supply secondary for rectification) cost USD 0.10 – USD 0.50 each depending on current rating, reverse voltage, and brand name. High-current silicon Schottky diodes in high-power rectification applications – such as TO-220 packaged 45 V/30 A device used to supply power distribution in servers costs USD 0.80 to USD 3.00 each, with automotive-qualified equivalents selling at 3060% premiums over industrial grade devices. SiC Schottky diodes – the high-end segment – are sold at USD 2.00 – USD 15.00 each with standard commercial grade items with current rating, blocking voltage, and package type, or at USD 5.00 – USD 25.00 each with automotive AEC-Q101-qualified SiC Schottky diodes an extra qualification test, paperwork, and traceability. The SiC Schottky diode price bonus over similar blocking voltage silicon fast recovery diodes—currently 5-10 times on a unit scale basis – is the main commercial adoption impediment in cost-sensitive industry applications, but is gradually declining as the scale of SiC wafer manufacturing increases and is more than compensated by system-level savings in heat sink, magnetics, and PCB area that higher switching frequency SiC-enabled designs are actually able to accomplish.

Under the current analysis, the market will reach about USD 8.14 billion by 2035, as the market for the EV market scales to 40 million units annually by 2030 creating unprecedented ordinary SiC Schottky diode demand in the automotive power electronics market; solar PV implementation at current levels continues into the forecast period; and the Asian Pacific continued EV, solar, and electronics manufacturing growth to maintain the dominating role of the region throughout the forecast period with a CAGR of 8.7% between 2026 and 2035.

Asia Pacific is projected to continue to take the largest revenue share during the forecast period, with an approximate control of 44% of global market share in 2025, depending on the characteristic of the region being the largest power manufacturing geography in the world in both consumer electronics, solar modules, EVs, and industrial products at the same time, the world-leading deployment of solar and EV technology by China; the world-leading EV deployment by South Korea, the concentration of major Schottky diode manufacturers in Japan, South Korea, China, and Taiwan provides both market supply and commercial headquarters benefits, and the manufacturing industries generate broad Schottky diode demand across the full product spectrum from commodity silicon devices to premium SiC power devices.

Asia Pacific is expected to retain the greatest market share and a robust growth momentum in the forecast period of 9.8% CAGR due to China having the largest EV market in the world, absorbing SiC Schottky diodes in its automotive power electronics designs at a phenomenal rate, China having over 200 GW of yearly solar PV additions, which require hundreds of millions of Schottky bypass diodes to drive its domestic module suppliers, Japan with its accelerating automotive electronics industry that is moving to EV power electronics designs, South Korea with its Samsung and LG electronics supply chains generating silicon Schottky diode demand across consumer electronics and EV components, and India’s rapidly growing solar market and emerging EV sector adding incremental Schottky diode demand across both silicon and SiC technology segments.

The IEA is projecting an annual growth in the Global Power Schottky Diode Market of many tens of% with the IEA reporting global electric vehicle sales of about 14 million vehicles in 2023 and projecting upward to 40 million vehicles in the year 2030 in stated policy cases – each EV with Schottky diodes in on-board charger, DC-DC converter and auxiliary power systems applications – the IEA reporting about 415 GW of global solar PV additions in 2023 with each MW of added capacity incorporating approximately 2,000–4,000 Schottky bypass diodes, 80 PLUS Titanium server power supply efficiency requirements above 96% creating regulatory-driven Schottky diode adoption in data center power supply designs, silicon carbide Schottky diodes achieving zero reverse recovery charge at 650V–1,200V blocking voltages enabling EV power electronics performance levels unachievable with silicon alternatives, the U.S. NEVI program’s USD 5 billion EV charging network investment generating DC fast charging station power electronics component demand, Wolfspeed’s SiC manufacturing capacity expansion targeting over 1 million SiC wafers annually providing supply availability enabling SiC Schottky adoption at automotive volume scale, and GaN Schottky diode development advancing toward commercial deployment enabling higher switching frequency power conversion in premium applications where silicon and SiC Schottky performance limits are being approached.