Clinical Informatics Market Size, Trends and Insights By Type (Electronic Health Records, Clinical Trial Management System, Clinical Data Management System, Randomization and Trial Supply Management, Electronic Trial Master File, Electronic Patient Reported Outcomes), By Component (Software, Services), By Deployment Type (Cloud-based, On-premise), By End-user (Hospitals, Ambulatory Surgical Centers, Others (Clinics, Research Institutes, and Pharmacies)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 13.36%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- Koninklijke Philips V.

- Cerner Corporation

- Veradigm LLC

- Epic Systems Corporation

- Others

Reports Description

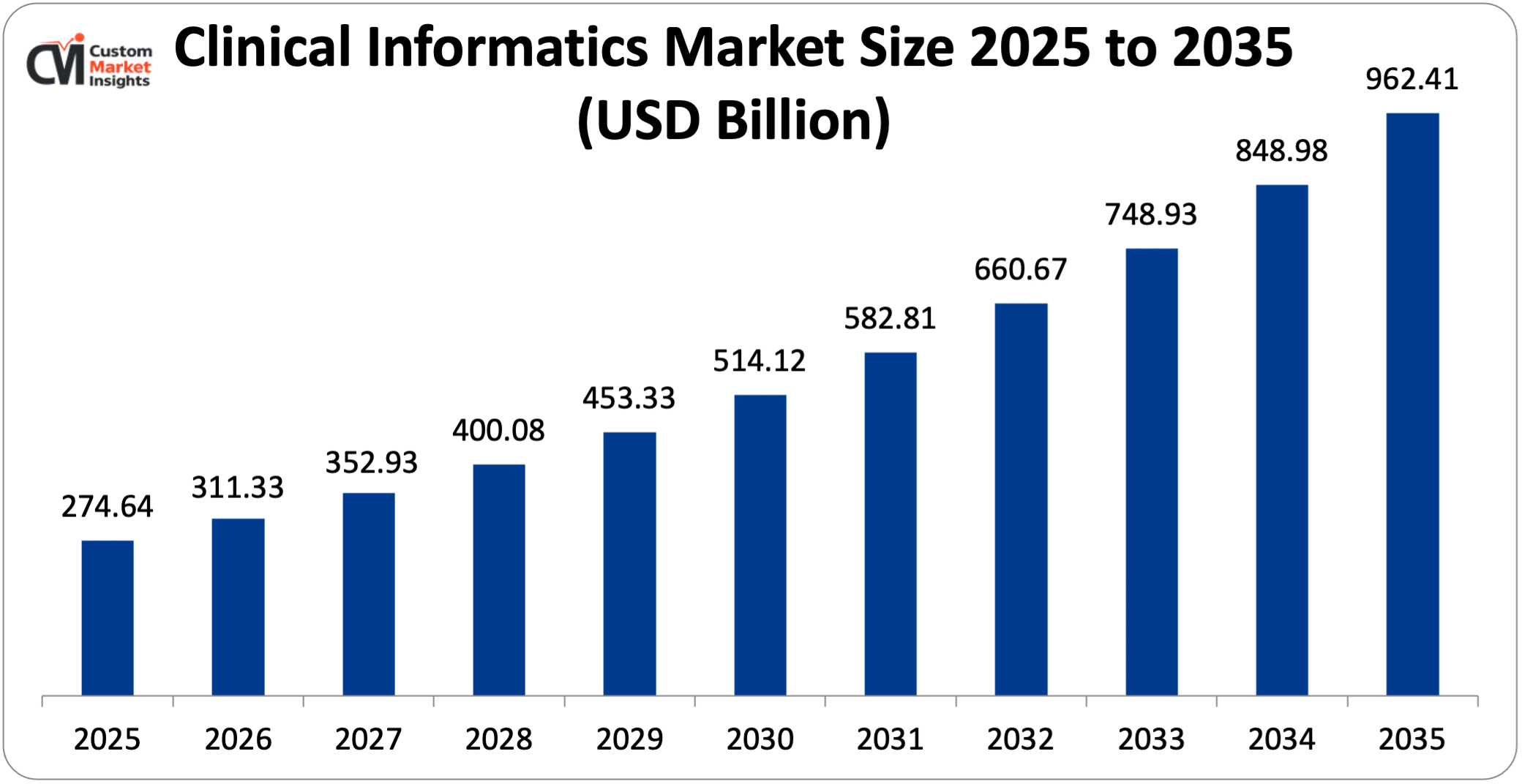

As per the clinical informatics market analysis conducted by the CMI team, the clinical informatics market is expected to record a CAGR of 13.36% from 2026 to 2035. In 2026, the market size was USD 311.33 Billion. By 2035, the valuation is anticipated to reach USD 962.41 Billion. The market is expanding due to the transition to cloud-native, AI-integrated platforms. As such, the healthcare organizations are increasingly adopting advanced data analytics and electronic health records (EHRs).

Market Highlights

- North America dominated the clinical informatics market in 2025 with 55.34% of the overall share.

- The Asia Pacific is expected to witness the fastest CAGR of 14.5% in the clinical informatics market during the forecast period.

- By type, the electronic health records (EHR) held around 39.37% of the market share by 2025.

- By type, the electronic patient reported outcomes (ePROs) segment is expected to witness the fastest CAGR of 12.34% between 2026 and 2035.

- Through the component, the services segment dominated in 2025 with 78.23% of the overall market share.

- By component, the software segment is expected to witness the fastest CAGR of 1297% between 2026 and 2035.

- Through deployment mode, the on-premise segment dominated in 2025 with 53.23% of the overall market share.

- By deployment mode, the cloud-based segment is expected to witness the fastest CAGR of 11.97% between 2026 and 2035.

- By end-user, the hospitals segment dominated in 2025 with 45.64% of the overall market share.

- By end-user, ambulatory surgical centers are expected to witness the fastest CAGR of 12.34% between 2026 and 2035.

Significant Growth Factors

- Call for Standardized Ecosystems

Over the last decade, there have been significant efforts made by academic researchers, health authorities, the private sector, and health systems to improve the structure and capabilities of clinical data systems. These efforts have already translated into rapid technological growth in medical software applications for the improvement of clinical practices apart from patient care and the performance of healthcare establishments and systems. The algorithms in software applications help physicians to better their decision-making and improve the quality of healthcare services delivered to patients. Consequently, the market for ‘clinical informatics,’ a term commonly associated with software applications of digital health that help integrate the field of clinical data science into clinical care systems, is continually growing due to the changing demands of patients and, therefore, that of healthcare.

- Upsurge in Real-World Evidence Integration

Decentralization of clinical trials and the advent of real-world evidence integration are pushing drug makers to adopt innovative technologies. The increasing demand for informatics tools for providing better data insights from remote monitoring, wearables, and patient registries is driving the market growth. These technologies streamline the drug development process, cut costs, and shorten drug development lifecycles, thereby causing a spur in the market for eClinical solutions and predictive analytics. Advent of advanced technologies, big data, and the increasing need for patient data from healthcare practitioners for reducing errors and enhancing patient experience are propelling the eClinical solutions and predictive analytics industry value. Global supervisory bodies, including the U.S. FDA and EMA are mandating digital-first data submission standards for clinical trials, which, in turn, is supplementing the market demand for eClinical solutions along with predictive analytics.

Adoption of eClinical solutions and predictive analytics by the pharmaceutical, biopharmaceutical, and medical device industries is expected to further spur market growth. Pharmaceutical and biopharmaceutical firms are developing their own platforms or collaborating with third-party providers to leverage technologies including machine learning and artificial intelligence to scrutinize data and make prompt and precise decisions in case of clinical trials. On these grounds, oracle life sciences cloud applications comprise comprehensive solutions that analyze data quickly and offer insights in real-time.

What are the Major Advancements Changing the Clinical Informatics Market Today?

- Switch to Ambient Clinical Intelligence and Generative AI

The digital assistants in use today are expected to evolve into agentic AI that are the workflow owners within a medical office. Ai will listen to all patient consultations, turn the conversation into a structured medical note with proper coding, and save around 70% of the time needed on manual count. The busy physician can now focus on providing high-quality patient care, not chasing around missing info to meet the high standards of clinical note documentation. As AI matures, it will evolve from a tool in which the human comes first to AI being the chief decision maker of complex systems, requiring humans only for exceptional cases. In medical environments, AI will triage patients who need to be seen and will schedule follow-ups. Moreover, unless there is a red flag regarding the diagnostic readings, it will send the patient home with the doctor’s orders. Instead of tools, AI will become a core component of the operating system of the hospital. Skilled professionals will be needed in both front lines and back offices.

- Edge Intelligence and Standardized Interoperability

The U.S. department of health and human services has launched a series of initiatives to facilitate the transition to strategic interoperability in healthcare. One pivotal statutory step in this direction was the 21st century cures act. For the first time, enabling seamless clinical data movement as necessary to put persons at the center of care and incorporate it with advanced technologies became mandatory.

The new era of multi-dimensional healthcare and resultant challenges and acute need for ubiquitous, seamless, interactive, and clinical-grade data delivery across the healthcare ecosystem are slated to the convergence of hl7 FHIR standard and edge computing. The aspirations of strategic interoperability pervade through the ideals of hl7 FHIR standard and edge computing. Hl7 FHIR emerged as a holistic health information interoperability solution from the confluence of multiple technology categories, including multimodal AI, communication protocols, data formats, and presentation standards. The paradigm of hl7 FHIR standard was latently focused on the competencies to deploy advanced technologies to automate the arduous task of tapping into existing clinical data, analyzing and interpreting it, and delivering the outputs to inform next steps in the healthcare continuum. It melded multiple user needs with the benevolence of advanced computational techniques.

To intelligently deliver actionable data and insights from mobile medical technologies called “edge computing,” it is indispensable to interpret incoming data, apply AI algorithms, and orchestrate the delivery of predicted metrics to mobile devices. Timely and intelligent processing of incoming data is of importance for the mobile healthcare ecosystem. Real-time processing improves patient outcomes, the accuracy of edge analytics, the performance of wearables, medical devices, and the respective advanced applications. It is imperative to ensure the lowest latency in edge analytics to enable converging multi-dimensional inputs, real-time data processing, risk stratification, performance analytics, and critical alerts. IoT edge architecture is optimized for ultra-thin-footprint systems with embedded AI engines capable of acquiring data, analyzing it, re-routing sizable data, and executing medications or alerts in real time.

- Impact of AI on Clinical Informatics Market

Artificial intelligence is poised to radically transform the practice of medicine and the delivery of healthcare. The healthcare industry generates large amounts of data from internally and externally sourced information across disparate healthcare systems. Predictive analytics enable healthcare organizations to derive actionable insights from their data. Applications of AI like ambient clinical documentation alleviate blame from human specialists by automating the documentation of patient encounters. By taking the burden of administrative tasks from human specialists, ambient clinical documentation helps address the current clinician burnout crisis.

Conventionally, drug discovery has taken years to produce market-ready pharmaceuticals, but AI has the ability to process and analyze trillions of data points on therapies, potential adverse events, drug interactions, and patient outcomes at superhuman speeds, thereby shortening development timelines from years to months. AI can also drive the practice of precision medicine, which takes into account the traits of the individual patient by tailoring treatments to their genomic profiles. The results of precision medicine could lead to better patient outcomes and lower costs of care by avoiding drugs that may result in adverse outcomes for certain patients.

Category Wise insights

By Type

- Why are electronic health records dominating the clinical informatics market?

Electronic health records (EHRs) represent the foundational data layer in the clinical informatics stack, which is a broad area spanning decision support applications, coding systems, reporting systems, and communication layers like hl7 and FHIR. EHRs have been mandated by the Hitech Act in the U.S. and the digital healthcare act in Germany. EHRs are the de facto standard for clinical care and have become a dominant player across diverse segments.

EHRs improve patient safety by automating alerts for drug interactions and ensuring a centralized collection of a patient’s real-time history. EHRs eliminate redundant testing and assist in the management of population health management initiatives. EHRs are the primary source of data for patient-oriented regulatory initiatives and the historical collection of datasets to support quality improvement. The majority of the market derives from larger networks such as system integrators dominated by Epic, Cerner, and Meditech combined with their ecosystem of add-on products and services. Software as a service (SaaS) and data as a service (DaaS) vendors have begun to dominate the space for ambulatory practices but remain locked out from across-the-continuum of care workflows and have limited access to specialty care EHRs or federated EHRs.

By Component

- How are services leading the clinical informatics market?

The services segment leads the global clinical informatics market, and the trend is projected to continue in the forthcoming period. This growth is expected as the demand for system integration and interoperability consulting increases in order to connect legacy data with AI-based platforms in hospitals. The reliance on specialized service vendors is also increasing for it services, user training, regulatory compliance, and consistency with standards such as HIPAA and GDPR. The software segment holds the second-largest share in the clinical informatics market, providing foundational systems for the services segment. The extensive application of software increases reliability, longevity, and clinical efficiency. However, the services segment will register as the fastest-growing area of the market owing to the outsourcing of informatics functions to reduce operational costs. The services segment consists of integration services for electronic health records, supply chain management systems, computerized physician order entry, information exchange, interoperability, diagnostic imaging, and many other software-based applications with enhanced suitability to hospital needs. The service segment capabilities assist hospitals in selecting and collaborating with specialized service vendors for key it services and user training in the case of clinical informatics to establish long-term relationships.

By Deployment Mode

- Why does the on-premise segment dominate the clinical informatics market?

The on-premise segment is expected to continue to dominate the clinical informatics market. Stringent data security and sovereignty requirements are among the major advantages that will fuel the on-premise segment’s sales during the forecast period. The most preferred model of deployment for hospitals and research centers is on-premises. They ensure compliance with regulations such as HIPAA and GDPR. Furthermore, the on-premises deployment model is looked upon as ideal by facilities with established it departments. The model allows for deep customization of legacy systems, which is necessary for enhancing clinical and operational processes. On-premise clinical informatics systems also provide low-latency access for organizations that must process datasets with high transaction volumes. The on-premise model is independent of internet connectivity. This characteristic is critical for ensuring admissions and discharges are performed in real-time via systems that are integral for functions such as diagnostic imaging and emergency care workflows.

By End-user

- Why are hospitals leading the clinical informatics market?

Hospitals hold the maximum share of the clinical informatics market as they house systems to handle all the patients and make sure they get the care they need. Hospitals are trying to lower their costs and help doctors who’re really tired and stressed out. So they are using computers to do things like keep track of records and billing. They are also using systems that help doctors make decisions. The world is moving toward a system where hospitals get paid based on how they take care of patients. There are also laws that say hospitals have to have computer systems. For example, in the United States there are rules called “Meaningful Use” that hospitals have to follow. In China they have a system that grades how well hospitals use computers. These translate into the fact that hospitals need to have clinical informatics systems with certainty. Hospitals need these systems to stay in business and to take care of patients.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 311.33 Billion |

| Projected Market Size in 2035 | USD 962.41 Billion |

| Market Size in 2025 | USD 274.64 Billion |

| CAGR Growth Rate | 13.36% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Component, Deployment Type, End-user and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How big is North America’s clinical informatics market size?

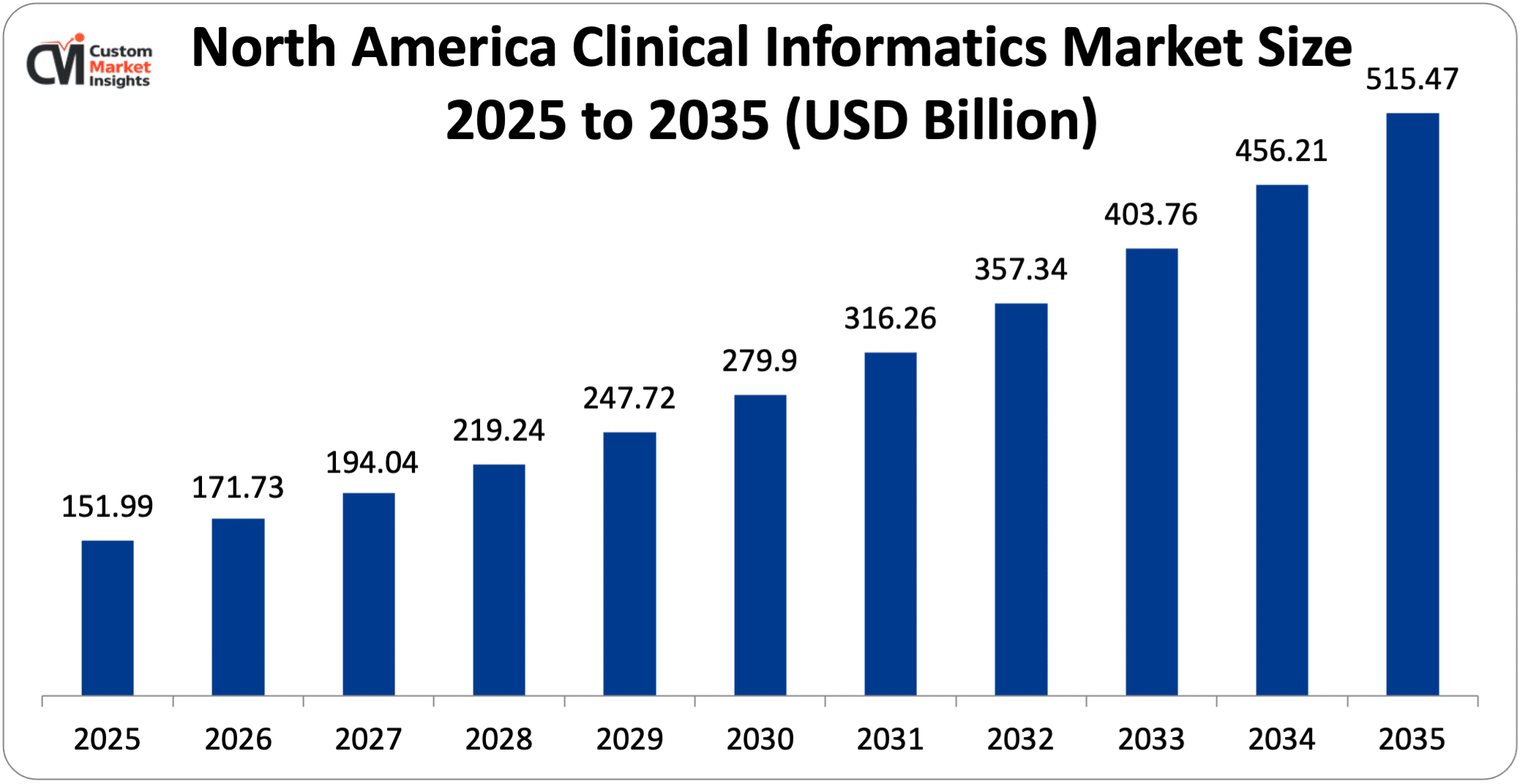

North America’s clinical informatics market was worth USD 151.99 Billion in 2025 and is expected to reach USD 515.47 Billion by 2035 at a CAGR of 12.99% between 2025 and 2035.

Why did North America Dominate the Clinical Informatics Market in 2025?

North America dominated the clinical informatics market in 2025. The presence of a mature healthcare it infrastructure and regulatory mandates on the interoperability of medical devices, such as the U.S. food and drug administration (FDA) and the 21st century cures act, are some of the key driving factors for the clinical informatics market. Players such as epic systems, oracle health, and UnitedHealth group (Optum) are spending heavily on R&D investments in AI-driven clinical decision support, which can help in providing a better diagnosis and treatment plan for a patient. Need for value-based care models, which are primarily driven by advanced analytics and allow healthcare stakeholders to realize better quality care delivery while optimizing operational efficiency to improve patient outcomes and reduce the cost of care, is also expected to provide a huge boost to the clinical informatics market.

What is the Size of the U.S. Clinical Informatics Market?

The market size of U.S. clinical informatics was USD 116.21 Billion in 2025 and is expected to reach USD 355.66 Billion in 2035, witnessing a CAGR of 11.83% between 2026 and 2035.

U.S. Clinical Informatics Market Trends

The U.S. clinical informatics market is set to expand on an exponential note between 2026 and 2035. The flourishing medical informatics industry is also one of the main drivers behind the evolving U.S. clinical informatics market. As a specialized informatics field, clinical informatics is primarily concerned with integration of healthcare data with clinical processes. Healthcare systems are undergoing a transition to generate volumes of data instead of solely relying on EHR systems in the subsequent phase of the clinical informatics market. The 21st century cures act and the shift to cloud-native platforms are propelling this transformation. FHIR-based interoperability is enabling a fundamentally different way of exchanging health data, thereby allowing organizations to access and share health data in orders of magnitude greater volume.

Why is the Asia Pacific experiencing the fastest growth in the clinical informatics market?

In this fast-paced and ever-evolving time in the clinical informatics industry, the Asia Pacific is expected to be the fastest-growing market. The market’s growth during the projected period of 2023-2035 is attributed to the growing interest in digital health. The healthcare informatics market is projected to be impacted positively by the growing use of digital technologies in the healthcare industry as well as by the increasing sensitivity to the use of health analytics among people and the growing number of digital natives. Clinical informatics has been effectively used in multiple clinical applications, including genomics, proteomics, and medication safety, and is gaining traction among healthcare service providers. The efforts of the governments to strengthen the regional healthcare sector and move it toward digital health are also anticipated to impact the market’s expansion positively. Another area of research that is anticipated to expand quickly in the region is artificial intelligence (AI)-driven clinical trials.

China Clinical Informatics Market Trends

China is expected to witness a significant growth in the clinical informatics market during the forecast period. The national mandate from the authority aimed at a “healthy china by 2030” will continue to impact future healthcare plans of the country. As people become more health-conscious, the demand for better technologies in the healthcare domain will increase, and thus this will drive the growth of the china clinical informatics market in the years to come. Research and development expenditure in the china clinical informatics market is anticipated to gain traction as the policies coming from the nation are inclined toward the same.

Policies made for the health sector through the 15th five-year plan (2026–2030) are focused on upgrading technologies in the years to come. Under the digital goals of the first phase of the “smart hospital” upgrades program, clinical trial management systems (CTMS) are anticipated to be created, thus bringing a spurt in the clinical informatics market in china. In order to gain a competitive edge over others, the key players of the china clinical informatics market are entering into joint ventures and collaborations, developing sophisticated products to retain their original customers, and engaging in mergers and acquisitions activities, thus pushing the growth of the clinical informatics market in china.

Improvements in telemedicine, particularly in urban area delivery and miniaturization of sensors and devices, are creating advanced imaging systems to enable patients to take critical information within the context of their existing health. In addition to these factors, investment in a digital-first healthcare ecosystem will further propel the growth of the clinical informatics market in china. The growing number of elderly people across the globe, particularly in china with over 400 million citizens over 60, are thus anticipated to bolster the market expansion in the years to come.

Where does Europe stand with respect to the clinical informatics market?

The European health data space initiative is the major factor propelling market growth. For instance, in October 2023, the European Commission announced its strategy to develop the European Health Data Space, which will allow better sharing of sensitive health data across borders. In recent years, the UK became the fastest-growing clinical informatics market across the globe. This is due to the government policies mandating interoperability among patient care systems, which also results in better ease of sharing patient data through interoperable systems. For instance, in England, the NHS requires providers of patient care to offer clinical solutions that use open standards and are enabled for national interoperability with the other systems through the use of FHIR (fast healthcare interoperability resources).

In addition, clinical informatics products and services that are interoperable make the data sharing easier, which, in turn, enhances the precision of the diagnosis, thus resulting in better treatment outcomes. Thus, there is a tremendous shift towards the use of interoperable systems, thereby contributing to the market growth. Innovative approaches like AI-driven diagnostics, improved patient monitoring through mobile apps, and personalized medicine for chronic diseases, are gaining popularity all across the europe. The governments are also implementing schemes to encourage the manufacturing and use of clinical informatics solutions by allowing reimbursements.

Germany Clinical Informatics Market Trends

Germany’s clinical informatics market is on the verge of modernization driven by a €50 billion initiative. The initiative ought to establish a transformation fund running from 2026 to 2035 to meet the requests of the association of German hospital directors for more investment into the modernization of the healthcare systems.

Market participants are adjusting their development strategies in line with this transformation initiative, particularly in terms of improving the software systems provided to hospitals. The vendors are expected to collaborate with their competitors to develop joint software solutions that can meet the modernization needs due to the full phase rollout of the eHealth act, hospital reform act, and others in the years to come.

Following the merger of some large hospital facilities, the demand for new healthcare information software will also surge in the medium and long run. By introducing new and enhanced software systems, hospitals and healthcare institutions are expected to meet their growing needs for a larger number of patients. On top of that, the intertwining of software and healthcare services with artificial intelligence (AI)-driven clinical decision support, cloud-based eClinical solutions, and others are expected to modernize the clinical informatics market. According to the federal ministry of health, Germany will fall short of 90,000 doctors by 2035. This will create a huge demand for clinical informatics.

Where is the Middle East & Africa regarding the clinical informatics market?

The rising adoption of advanced technologies in tandem with conducive government support is likely to foster the future of the clinical informatics industry in the Middle East and Africa. On the other hand, sustaining a robust growth trajectory will depend on solving the challenges such as discrepancies in developmental stage between high-income gulf nations and the rest, uneven digital infrastructure, regulatory fragmentation, workforce skill gaps, etc., especially in the Sub-Saharan African nations.

The sustained government support in the Middle Eastern and African countries to facilitate the integration of clinical informatics solutions is incrementally pushing the regional clinical informatics market. Saudi Arabia’s vision 2030 aims to upgrade its healthcare industry, and the country’s objective to utilize only AI-driven smart hospitals to diagnose and treat patients is expected to add traction to the regional industry. Similarly, the momentum surrounding the UAE’s national unified medical record is expected to be the key contributor to the rise in the region’s industry.

Further key countries, namely Oman, Qatar, and Kuwait, and the growing technology adoption in these gulf nations are anticipated to bolster the regional industry growth. The growing industry in the region is bolstered by the digital penetration across various industries, boosting the adoption of clinical informatics systems. For instance, South Africa, which leads in the clinical informatics market by contributing over half of the overall revenue, is progressively implementing cloud-based electronic data capture.

Brazil Clinical Informatics Market Trends

Brazil’s clinical informatics market is witnessing steadiness due to the government’s national digital health strategy being in place. This plan, also known as esd28, wants to bring all patient information in one place called the national health data network or RNDS.

The goal is to make it easier for healthcare groups, both public and private, to share information. Some big trends in this market through 2035 include moving to cloud-based health record systems. Another ongoing trend is that of using artificial intelligence to analyze data and help manage chronic diseases. This is crucial as brazil’s elderly population is growing. Private hospital chains are also handsomely investing in digital tools that help doctors make decisions faster.

Top players in the Clinical Informatics Market and their Offerings

- Koninklijke Philips V.

- Cerner Corporation

- Veradigm LLC

- Epic Systems Corporation

- McKesson Corporation

- Medical Information Technology Inc.

- Siemens Healthineers

- Cognizant

- GE HealthCare

- Oracle Corporation

- IQVIA Inc.

- UnitedHealth Group

- Others

Key Developments

Clinical informatics market has experienced considerable changes in the last few years as the market players are trying to diversify their technological aspects and develop product portfolios using strategic approaches.

- In January 2025, AMDIA and HIMDSS announced that they had entered into a partnership with the objective of empowering health system executives and physicians for sharing insights and collaborating regarding innovations that would shape the global health ecosystem’s future. As such, both players are looking forward to improving care delivery and enhancing patient outcomes through the integration of advanced technology and data-driven decision-making.

These strategic measures have enabled the companies to reinforce their competitive positions, increase the product line, boost their technological competencies, and also seize growth opportunities in the fast-growing clinical informatics market.

The Clinical Informatics Market is segmented as follows:

By Type

- Electronic Health Records

- Clinical Trial Management System

- Clinical Data Management System

- Randomization and Trial Supply Management

- Electronic Trial Master File

- Electronic Patient Reported Outcomes

By Component

- Software

- Services

By Deployment Type

- Cloud-based

- On-premise

By End-user

- Hospitals

- Ambulatory Surgical Centers

- Others (Clinics, Research Institutes, and Pharmacies)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Clinical Informatics by Segments

- 2.1.2. Clinical Informatics by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Clinical Informatics Market Attractiveness Analysis, By Type

- 2.2.3. Clinical Informatics Market Attractiveness Analysis, By Component

- 2.2.4. Clinical Informatics Market Attractiveness Analysis, By Deployment Type

- 2.2.5. Clinical Informatics Market Attractiveness Analysis, By End-user

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Call for Standardized Ecosystems

- 3.1.2. Upsurge in Real-World Evidence Integration

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Clinical Informatics Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Clinical Informatics Market Revenue Share, By Type , 2025 & 2035

- 4.1.2. Electronic Health Records

- 4.1.3. Clinical Informatics Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Clinical Trial Management System

- 4.1.7. Clinical Informatics Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Clinical Data Management System

- 4.1.11. Clinical Informatics Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Randomization and Trial Supply Management

- 4.1.15. Clinical Informatics Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Electronic Trial Master File

- 4.1.19. Clinical Informatics Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Electronic Patient Reported Outcomes

- 4.1.23. Clinical Informatics Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Clinical Informatics Market – By Component

- 5.1. Component Market Overview, By Component Segment

- 5.1.1. Clinical Informatics Market Revenue Share, By Component , 2025 & 2035

- 5.1.2. Software

- 5.1.3. Clinical Informatics Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Services

- 5.1.7. Clinical Informatics Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Component Market Overview, By Component Segment

- Chapter 6. Clinical Informatics Market – By Deployment Type

- 6.1. Deployment Type Market Overview, By Deployment Type Segment

- 6.1.1. Clinical Informatics Market Revenue Share, By Deployment Type , 2025 & 2035

- 6.1.2. Cloud-based

- 6.1.3. Clinical Informatics Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. On-premise

- 6.1.7. Clinical Informatics Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Deployment Type Market Overview, By Deployment Type Segment

- Chapter 7. Clinical Informatics Market – By End-user

- 7.1. End-user Market Overview, By End-user Segment

- 7.1.1. Clinical Informatics Market Revenue Share, By End-user , 2025 & 2035

- 7.1.2. Hospitals

- 7.1.3. Clinical Informatics Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Ambulatory Surgical Centers

- 7.1.7. Clinical Informatics Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Others (Clinics, Research Institutes, and Pharmacies)

- 7.1.11. Clinical Informatics Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-user Market Overview, By End-user Segment

- Chapter 8. Clinical Informatics Market – Regional Analysis

- 8.1. Clinical Informatics Market Overview, By Region Segment

- 8.1.1. Global Clinical Informatics Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Clinical Informatics Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Clinical Informatics Market Revenue, By Type , 2026 – 2035

- 8.1.4. Global Clinical Informatics Market Revenue, By Component , 2026 – 2035

- 8.1.5. Global Clinical Informatics Market Revenue, By Deployment Type , 2026 – 2035

- 8.1.6. Global Clinical Informatics Market Revenue, By End-user , 2026 – 2035

- 8.2. North America

- 8.2.1. North America Clinical Informatics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Clinical Informatics Market Revenue, By Type , 2026 – 2035

- 8.2.3. North America Clinical Informatics Market Revenue, By Component , 2026 – 2035

- 8.2.4. North America Clinical Informatics Market Revenue, By Deployment Type , 2026 – 2035

- 8.2.5. North America Clinical Informatics Market Revenue, By End-user , 2026 – 2035

- 8.2.6. U.S. Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Clinical Informatics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Clinical Informatics Market Revenue, By Type , 2026 – 2035

- 8.3.3. Europe Clinical Informatics Market Revenue, By Component , 2026 – 2035

- 8.3.4. Europe Clinical Informatics Market Revenue, By Deployment Type , 2026 – 2035

- 8.3.5. Europe Clinical Informatics Market Revenue, By End-user , 2026 – 2035

- 8.3.6. Germany Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Clinical Informatics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Clinical Informatics Market Revenue, By Type , 2026 – 2035

- 8.4.3. Asia Pacific Clinical Informatics Market Revenue, By Component , 2026 – 2035

- 8.4.4. Asia Pacific Clinical Informatics Market Revenue, By Deployment Type , 2026 – 2035

- 8.4.5. Asia Pacific Clinical Informatics Market Revenue, By End-user , 2026 – 2035

- 8.4.6. China Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Clinical Informatics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Clinical Informatics Market Revenue, By Type , 2026 – 2035

- 8.5.3. The Middle-East and Africa Clinical Informatics Market Revenue, By Component , 2026 – 2035

- 8.5.4. The Middle-East and Africa Clinical Informatics Market Revenue, By Deployment Type , 2026 – 2035

- 8.5.5. The Middle-East and Africa Clinical Informatics Market Revenue, By End-user , 2026 – 2035

- 8.5.6. Saudi Arabia Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Clinical Informatics Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Clinical Informatics Market Revenue, By Type , 2026 – 2035

- 8.6.3. Latin America Clinical Informatics Market Revenue, By Component , 2026 – 2035

- 8.6.4. Latin America Clinical Informatics Market Revenue, By Deployment Type , 2026 – 2035

- 8.6.5. Latin America Clinical Informatics Market Revenue, By End-user , 2026 – 2035

- 8.6.6. Brazil Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Clinical Informatics Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Clinical Informatics Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Clinical Informatics Market: Company Market Share, 2025

- 9.2. Global Clinical Informatics Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Koninklijke Philips N.V.

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Cerner Corporation

- 10.3. Veradigm LLC

- 10.4. Epic Systems Corporation

- 10.5. McKesson Corporation

- 10.6. Medical Information Technology Inc.

- 10.7. Siemens Healthineers

- 10.8. Cognizant

- 10.9. GE HealthCare

- 10.10. Oracle Corporation

- 10.11. IQVIA Inc.

- 10.12. UnitedHealth Group

- 10.13. Others.

- 10.1. Koninklijke Philips N.V.

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 31

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Koninklijke Philips V.

- Cerner Corporation

- Veradigm LLC

- Epic Systems Corporation

- McKesson Corporation

- Medical Information Technology Inc.

- Siemens Healthineers

- Cognizant

- GE HealthCare

- Oracle Corporation

- IQVIA Inc.

- UnitedHealth Group

- Others

FAQs

The key players in the market are Koninklijke Philips N.V., Cerner Corporation, Veradigm LLC, Epic Systems Corporation, McKesson Corporation, Medical Information Technology Inc., Siemens Healthineers, Cognizant, GE HealthCare, Oracle Corporation, IQVIA Inc., UnitedHealth Group, Others.

Various government regulations influence the clinical informatics market. For instance, in 2016, the U.S. Department of Health and Human Services implemented the 21st Century Cures Act, which prohibits information blocking between certified electronic health record (EHR) systems and the other data management systems. Government organizations are also offering financial incentives such as incentive payments under the meaningful use program to encourage hospitals to implement certified electronic health record (EHR) systems and ensure that patient data is easily accessible.

Government regulations such as the health insurance portability and accountability act (HIPAA) in the U.S. and the general data protection regulation (GDPR) in europe need healthcare providers to maintain patient privacy. However, many digital health solutions use patient data for research purposes. If patients do not provide permission for their data to be available for use in GitHub and other public repositories, technology developers will not be able to develop their applications.

As a result of government regulations regarding data security and privacy, the demand for alternative automated blockchain healthcare technology is rising to maintain the flow of patient data. In the future, blockchain technology will enable patients to access and control their health data while allowing developers to use the data in clinical trials of new applications. Government regulations are an important factor to consider for emerging economies in the clinical informatics market. For instance, various government organizations are developing legal frameworks to offer funding for hospital digitization while meeting regulatory obligations.

Clinical informatics systems come with a high initial cost, and that has posed barriers for small-to-mid-sized healthcare providers from actually implementing them. However, with the shift to cloud-based and SaaS models, the hefty upfront capex is no longer a deterrent. By using cloud-based solutions, healthcare providers – regardless of their size – can start small and invest in technologies in manageable lumps. Their initial investments would be less, and the short and manageable OPEX means that healthcare providers wouldn’t have to exhaust their entire operational budgets on technology alone. The doctors have easy access to patient information, which, in turn, ensures the timely diagnosis of a patient’s medical condition. Cloud computing technologies also offer streamlined workflows. In addition to ensuring the timely availability of patient data to the treating physician, cloud computing systems provide a customized and collective view of patient information.

The market for clinical informatics is expected to witness a significant growth of about USD 962.41 Billion in the year 2035 with a CAGR of 13.36% between the years 2026 and 2035 due to the switch to value-based care, government mandates for digital record keeping, and mounting need for AI-driven data analytics for managing complex patient information and improving clinical outcomes.

The clinical informatics market is dominated by North America owing to the region being home to mature healthcare infrastructure; widespread adoption of EHR and AI tools for health data management and quality improvements; regulatory mandates such as 21st century cures act facilitating health technology deployment; and massive investments by the major players, including oracle health and epic systems. The region has a sizable healthcare expenditure contributing to market growth. Moreover, market players are focusing on a wide range of clinical informatics solutions for value-based care models, thus making clinical informatics the most viable market in the region. For instance, sprint bioscience ab has developed a new metabolic therapy called Sprint Bioscience AB.

The Asia Pacific is projected to witness the fastest growth over the forecast period. Growing government-led digital health initiatives include china’s “healthy china 2030” and India’s Ayushman Bharat Digital Mission, which help in expanding the scope of digital health. In addition, the modernization of hospital infrastructures for better management of data and keeping health records for meeting the demand for integrated, connected, and smooth platforms significantly contributes to the growth of the market.

The growing middle class, changing lifestyles, and the need for the adoption of early diagnosis due to the surge in the aging population and the prevalence of chronic diseases and medical tourism are some other growth factors. To ensure efficient long-distance communication and collaboration, the demand for data interoperability is increasing significantly in the region. Moreover, Asia Pacific has become a global hub for cost-effective and productive clinical trials, which has encouraged the adoption of digital health solutions. Moreover, the high adoption of cloud-based informatics and mobile health solutions is expected to propel the growth of the digital health market in the Asia Pacific region. In addition, the growing private healthcare network is expected to spur the growth of the market in the coming years.

Several factors like government mandates for digital record-keeping, global shifts toward value-based care, demand for interoperability, integration of artificial intelligence (AI), cloud-based platforms, etc. Are driving the growth of clinical informatics among other factors. Ai has played a crucial role in mitigating the burden of healthcare professionals in the clinical informatics environment by employing intelligent software solutions in the market. For instance, computer technologies have aided in speeding up the process of drug development and have introduced new ways to personalize patient treatment.

Further, the adoption of cloud-based platforms has also surged rapidly in the clinical informatics market owing to their cost-effectiveness and flexibility. They empower the health information exchange among multiple healthcare systems and access various health cryptographics even on-site to ensure that patients can contact the service provider anywhere, anytime. Moreover, the cloud-based software tools and applications enable healthcare organizations to seamlessly share electronic medical records and offer various digital health solutions to expand their existing workflows. Some of the recent measures include affordable care act, the meaningful use program, and ACOs, which are aimed at the conversion of the healthcare system from a fee-for-service model to a value-based care model.