Polymers Used in Electric Vehicles Market Size, Trends and Insights By Polymer Type (Engineering Plastics, Polyamide (PA6, PA66, PA12), Polycarbonate (PC), Polyphthalamide (PPA), Polyphenylene Sulfide (PPS), Polyetheretherketone (PEEK), Polybutylene Terephthalate (PBT), Elastomers & Rubber, EPDM, Fluorosilicone Rubber, Thermoplastic Elastomers (TPE/TPV), Silicone Rubber, Polyurethanes, Rigid Foam, Flexible Foam, Thermoplastic Polyurethane (TPU), Fluoropolymers, PTFE, PVDF, ETFE, FEP & PFA, Epoxy Resins & Composites, Carbon Fiber Reinforced Epoxy, Glass Fiber Reinforced Epoxy, Other Polymer Types), By Application (Battery & Energy Storage Systems, Cell Separators & Pouch Films, Module Frames & Cell Holders, Battery Enclosures & Pack Structures, Thermal Interface Materials, Battery Sealing & Gasketing, Exterior Components, Body Panels & Closures, Bumpers & Fascias, Aerodynamic Underbody Panels, Interior Components, Instrument Panels & Dashboard, Door Panels & Trim, Seating Systems, Powertrain & Drivetrain, Thermal Management Systems, Electrical & Electronic Systems, High-Voltage Wiring & Cable Insulation, Connector Housings, Power Electronics Enclosures, Other Applications), By Vehicle Type (Battery Electric Vehicles (BEV), Plug-in Hybrid Electric Vehicles (PHEV), Hybrid Electric Vehicles (HEV), Fuel Cell Electric Vehicles (FCEV)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 15.1%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- BASF SE

- Covestro AG

- Solvay S.A.

- DuPont de Nemours Inc.

- Others

Reports Description

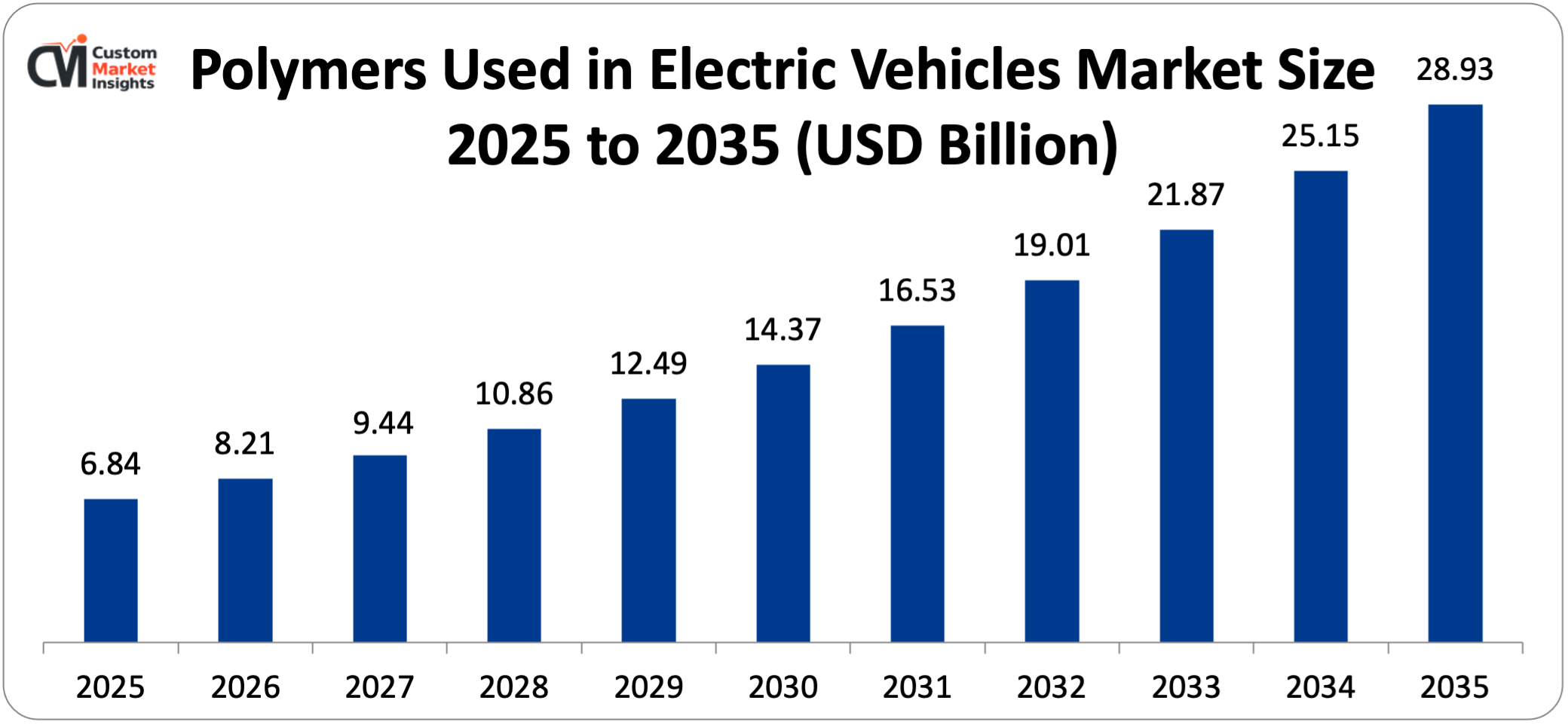

The global market for polymers used in electric vehicles is expected to grow at a rate of 15.1% per year from 2026 to 2035, going from USD 6.84 billion in 2025 to USD 8.21 billion in 2026 and then to about USD 28.93 billion by 2035. As emissions regulations get stricter, government purchase incentives grow, battery costs drop, and consumer acceptance grows, the global shift from internal combustion engine vehicles to electric powertrains is fundamentally changing the demand for polymers throughout the automotive value chain.

This is because electric vehicles need a lot more high-performance specialty polymers per vehicle than conventional vehicles do because of the unique thermal, electrical, mechanical, and lightweighting needs of EV-specific architectures. The market is growing because of a lot of things, including a rise in battery enclosure and thermal management applications, a rise in demand for lightweight structural polymers that can extend range, a rise in demand for high-voltage electrical insulation materials, and a rapid rise in global EV production capacity.

Market Highlight

- In 2025, Asia Pacific had the largest share of the polymers used in the electric vehicles market, with 52%. This was because China was the world’s largest market for making and using electric vehicles.

- Between 2026 and 2035, Europe is expected to grow at a CAGR of 14.2%. This is because German, French, and Italian automakers are making more commitments to electrification, and stricter CO₂ fleet emissions standards are being put in place.

- By polymer type, engineering plastics made up about 36% of the market in 2025. This shows how widely they are used in structural, thermal, and electrical applications throughout the EV architecture.

- The fastest-growing segment is the fluoropolymers segment with its CAGR of 18.3% between 2026 and 2035. This is due to the increasing demand for high-voltage cable insulation, battery sealing, and components that would be able to withstand electrolytes in the next-generation EV battery systems.

- The greatest percentage of the market in 2025 was in battery and energy storage systems, which accounted for 31%. This made EV-specific battery applications the primary driver of demand that differentiates the polymer requirements of electric cars as opposed to traditional cars.

- Battery electric vehicles (BEVs) made up 58% of all market revenue in 2025. This is because BEVs have more polymer per vehicle and a larger share of polymer value that is specific to EV applications.

Significant Growth Factors

The Polymers Used in Electric Vehicles Market Trends present significant growth opportunities due to several factors:

- Accelerating Global Electric Vehicle Production and Adoption Creating Structural Polymer Demand Growth:

The foundational driver of the polymers used in the electric vehicle market is the rapid and accelerating global transition of automotive production from internal combustion engine platforms to battery electric and hybrid electric architectures, a transition that is simultaneously expanding total polymer content per vehicle and shifting demand toward more sophisticated, higher-value specialty polymer grades specifically engineered for EV performance requirements. In 2024, global electric vehicle sales reached 17.1 million units, a 25% increase from 13.7 million units in 2023. EVs made up about 18.8% of all new vehicle sales around the world. This number is expected to rise to 40% by 2030 and 60% by 2035 under baseline regulatory scenarios. China is still the world’s biggest EV market, with about 11 million EVs made and sold in 2024. This is due to an all-encompassing policy ecosystem that consists of purchase subsidies, EV-friendly license plate policies in large cities, investment in public charging infrastructure, and forceful New Energy Vehicle (NEV) quotas on automakers that operate in the Chinese market.

The European EV sales of approximately 3.2 million units in 2024 are being stimulated by the promise of the EU to cease selling new ICE passenger cars after 2035 and the establishment of CO₂ fleet average goals of 95 grams per kilometer for passenger cars. Automakers that don’t meet electrification milestones will have to pay fines. In 2024, the United States will sell about 1.6 million electric vehicles (EVs). This is because of federal tax credits of up to $7,500 for each qualifying EV purchase, state-level zero-emission vehicle mandates in California and 16 other states, and a wave of domestic EV manufacturing investment, including Tesla’s Gigafactory Texas, Rivian’s Normal, Illinois plant, GM’s Ultium battery joint ventures, and Ford’s BlueOval facilities. Each battery electric vehicle has an estimated 120 to 180 kilograms of polymer in its battery structure, thermal, electrical, and interior applications. This is much more than the 80 to 100 kilograms found in similar conventional vehicles. This gives battery electric vehicles a structural unit-level polymer content advantage that boosts revenue growth as EV unit volumes grow. With an expected global production of 40–45 million electric vehicles by 2030, the total demand for polymers from electric vehicle-specific applications is likely to be one of the biggest single demand growth areas in the global specialty polymers market.

- Unique EV Battery Architecture Creating High-Value Polymer Applications Without Precedent in Conventional Automotive:

The lithium-ion battery pack — the defining technological component of battery electric vehicles, representing 30–40% of total vehicle cost and 60–70% of vehicle-specific engineering differentiation — creates an entirely new category of high-performance polymer applications that have no equivalent in conventional ICE powertrains and that require materials engineered to simultaneously satisfy thermal management, electrical insulation, electrolyte chemical resistance, mechanical structural, and fire safety performance requirements often within a single component Polymer applications at the battery cell level include separator membranes between the anode and cathode, which are usually made of polyethylene or polypropylene with a ceramic coating; cell pouch films for prismatic and pouch cell formats, which are made of aluminum-laminate structures with polyamide and polypropylene layers; and binder systems in electrode slurries, which use PVDF (polyvinylidene fluoride) and new aqueous binder alternatives. Polymer applications at the module level include cell holders and frames of glass-fiber-reinforced polyamide or PPS which support the structural structure with spacing between the cells; thermal interface materials such as polyurethane and thermally conductive silicone-based compounds which enable the flow of heat between the cells and the cooling plates; busbars overmolded in high-voltage-rated polyamide or PBT which furnish.

The applications in pack levels such as battery enclosures are currently engineered with glass-fiber-reinforced epoxy composite or aluminum-polymer hybrid constructions rather than all-metal constructions to reduce their weight. Others include battery management system circuit board encapsulants, thermal management fluid circuit components produced of chemically resistant polymers, and sealing systems that employ fluorosilicone and EPDM gaskets and O-rings to ensure that no water enters. The overall cost of the polymers of a typical 75 kWh mid-size BEV battery pack is estimated to range between USD 850 and USD 1,200, based on the cell format, pack architecture, and thermal management approach. This is worth more than the value of a few ICE vehicle body panels, revealing how valuable EV battery polymer uses are per vehicle.

What are the Major Advances Changing the Polymers Used in Electric Vehicles Market Today?

- High-Voltage Electrical Insulation Polymers Enabling 800-Volt Architecture Adoption:

The automotive industry’s shift from traditional 400-volt EV electrical architecture to 800-volt high-voltage systems, which began with Porsche’s Taycan in 2019 and quickly spread to Hyundai’s E-GMP platform, Kia EV6, Lucid Air, and more mainstream EV platforms, is driving up demand for polymer insulation materials that can reliably handle higher continuous operating voltages, greater partial discharge resistance, and the more demanding thermal conditions that come with higher-power charging and discharge cycles. For 800-volt systems, where partial discharge inception voltage, thermal aging stability, and long-term dielectric strength retention are more important, regular polyamide 6 and 6.6 wire and cable insulation isn’t good enough. It needs to be replaced with better options. Fluoropolymers, such as PTFE, FEP, ETFE, and PFA, are becoming the best insulation material for 800-volt high-voltage wiring harnesses, busbars, and charging port parts because they have great dielectric properties, can withstand temperatures up to 200°C, resist battery electrolytes, and are naturally flame retardant.

The fastest-growing segment of the fluoropolymers subsector is between 2026 and 2035, with a rate of 18.3 per year. This growth is primarily due to the need to use EV high-voltage electrical systems. Also gaining popularity in the high-voltage connector housings, busbar overmolding, and power electronics enclosures are high-performance thermoplastics such as PPS (polyphenylene sulfide), PEEK (polyether ether ketone), and LCP (liquid crystal polymer). These materials are costly due to their engineering performance and are simple to work with compared to fluoropolymer substitutes who require more specialized processing. The use of 800-volt architectures is growing quickly. Such architectures enable high-speed charging up to 270-350 kW, reducing the amount of time to less than 20 minutes to replenish the battery to 80 percent. Over 800-volt (or higher) architecture is projected to be used in over 35 different EV models by 2027, compared to fewer than 10 in 2023. This will result in a fast-moving installed base which will continue to keep high demands on high-voltage-rated polymer insulation materials both in OEM production and aftermarket service.

- Thermal Management Polymer Innovation Addressing Battery Safety and Longevity Requirements:

Thermal management is generally the most critical engineering task in battery electric vehicle design, and the performance, life and safety of lithium-ion batteries are heavily dependent on cell temperatures falling within limited operating ranges—15-35°C is considered optimal performance and life, and temperatures above 45°C lead to accelerated degradation, and above A modern BEV thermal management system is among the most polymer-intensive and technically challenging components of the car. It incorporates liquid cooling plates and channels, thermal interface between cells and cooling elements, insulation of battery pack, hose and fittings of coolant circuits and new immersion cooling systems where cells are dipped directly into dielectric cooling fluids.

Thermal conductive polymer compounds like PA6, PA66, PBT, PPS, and PEI filled with boron nitride, aluminum nitride or graphene based thermally conductive fillers at loadings of 30-60 wt. are reaching through-plane thermal conductivities of 3-10 W/mK. This implies that in non-structural thermal management applications, polymer thermal interface materials can be used to substitute metal components, which is beneficial in reducing weight and simplifying the process of manufacturing. From 2026 to 2030, the global market for thermally conductive plastics used in cars is expected to grow at a rate of more than 20% per year. The necessity of thermal management of EV batteries is the leading force behind this development. Immersion cooling is another recent technology, which consists of immersing battery cells in dielectric fluorocarbon or ester-based fluids within enclosures made of fluoropolymer. It provides better thermal uniformity than surface-contact liquid cooling and is getting a lot of investment from battery makers and EV OEMs as a way to allow faster charging without temperature changes. Immersion cooling system designs include polymer enclosures and sealing material.

- Structural Lightweighting Through Advanced Polymer Composites Directly Extending EV Range:

Vehicle mass reduction is of extraordinary importance in battery electric vehicles because energy consumption scales approximately linearly with vehicle weight — a 10% mass reduction delivers approximately 6–8% range improvement at constant battery capacity, or alternatively enables an equivalent battery cost reduction while maintaining target range — creating a compelling engineering and economic case for substituting polymer composites for metallic structural components across EV body, chassis, and closures. Carbon fiber reinforced polymer (CFRP) composites have tensile strength that is almost as strong as steel but only weigh about 20% as much. This makes them great for primary structural applications like body-in-white components, battery enclosures, structural floor panels, and roof panels where stiffness-to-weight ratios are important design factors. Compared to traditional ICE vehicles, the economics of CFRP are better for EVs. This is because the heavy battery pack (usually 400–700 kg for a mainstream BEV) makes it necessary to reduce the vehicle’s structural mass, which makes CFRP more expensive than steel or aluminum. This is especially true for premium-segment EVs, where OEMs can afford to pay more for materials in order to stand out in terms of performance and efficiency.

Glass fiber reinforced thermoplastic composites, such as long-fiber reinforced PA6, PPA (polyphthalamide), and PPS with fiber contents of 30–50 wt%, are the best lightweighting solution for mainstream BEV structural applications. They are much cheaper than CFRP and reduce mass by 20–35% compared to steel equivalents. The use of CFRP roof panels and structural elements in BMW’s i-series EVs, the structural CFRP battery enclosure in the Ferrari SF90 Stradale PHEV, and the glass-fiber-reinforced thermoplastic battery module frames used in many mainstream BEV platforms show the range of composite lightweighting solutions that are already in use. Adoption is expected to grow a lot in the mainstream EV market by 2035 as the cost of composite materials goes down and automated manufacturing processes like resin transfer molding and thermoplastic composite overmolding reach throughput rates that are compatible with high-volume automotive production.

Category Wise Insights

By Polymer Type

Why Engineering Plastics Lead the Polymers Used in Electric Vehicles Market?

Engineering plastics are the biggest group of polymers, making up about 36% of the total market revenue in 2025. This dominance is due to the fact that engineering thermoplastics can be used in a wide range of ways in the EV architecture, including battery module structural components, high-voltage connector housings, underhood thermal system components, power electronics enclosures, and exterior structural body panels. Different grades and formulations of polyamide, polycarbonate, PPS, PEEK, and other engineering thermoplastics are used in each application domain to meet different performance needs. Polyamide, which includes PA6, PA66, PA12, PPA, and PA4T grades, is the most common engineering plastic used in EVs.

It is used in battery module frames and cell holders, coolant circuit housings and manifolds, high-voltage connector systems, motor housings, and structural interior components. In 2024, global automotive polyamide consumption in EVs is expected to be 185,000 metric tonnes, and it is expected to grow at a rate of 14.8% per year through 2030. Polycarbonate and PC/ABS blends are used in clear and semi-clear EV parts like charging port covers, interior lighting parts, display bezels, and glazing elements. PPS and PEEK, on the other hand, are used in the most thermally and chemically demanding battery and underhood parts that need to stay stable at service temperatures above 180°C. The engineering plastics segment has the most established supply chain of any polymer category in EV applications. This is because global specialty compounds producers like BASF, Lanxess, Covestro, DuPont, and Celanese all have product development programs and OEM qualification relationships for EVs in all major automotive manufacturing regions.

By Application

Why Battery & Energy Storage Systems Dominate Polymer Applications in Electric Vehicles?

Battery and energy storage systems are the biggest part of the market, making up about 31% of all sales in 2025. This dominance is a direct result of the battery pack’s central role as the defining engineering system of battery electric vehicles. It is the part that sets EV design apart from ICE platforms and creates the most extensive and technically demanding set of polymer application requirements that are unique to electrified powertrains. Battery polymer applications must meet a lot of different performance requirements at the same time, unlike any other application in the car.

These include electrical insulation, thermal management, electrochemical resistance, mechanical structure, and fire safety. This means that premium polymer grades are needed, which cost a lot more per kilogram than other structural or aesthetic applications. A complete battery pack for a mainstream 75 kWh mid-size BEV is estimated to contain 25 to 35 kilograms of polymer. The polymer value per vehicle is between USD 850 and 1,200, which is about 40% of the total EV polymer value premium over an equivalent ICE vehicle, even though it only makes up 18 to 22% of the total vehicle polymer mass.

Battery polymer demand is expected to grow at the fastest rate of any EV application, at 17.6% per year from 2026 to 2035. This is because more EVs are being made and the size of the battery packs per vehicle is getting bigger as OEMs respond to consumer range anxiety by making batteries with more energy capacity. Solid-state battery development will need new polymer electrolyte and separator material platforms in order to reach commercial production by major manufacturers like Toyota, Samsung SDI, QuantumScape, and Solid Power from 2027 to 2030. This could lead to the creation of new premium polymer application categories within the battery system as solid-state cell architectures reach commercial scale.

By Vehicle Type

Why Battery Electric Vehicles Dominate the Market?

In 2025, battery electric vehicles (BEVs) will make up about 58% of total market revenue. This is because BEVs have the highest per-vehicle polymer value of all electrified vehicle types. This is because they have larger battery packs, don’t have any ICE powertrain parts (instead, they have electric motors, inverters, and high-voltage battery systems), and have more extensive high-voltage electrical architecture than hybrid vehicles. The BEV segment’s share of revenue is expected to rise to about 67% by 2035.

This is because the number of BEV units sold is growing faster than the number of PHEV and HEV units sold, thanks to government-mandated ICE phase-out timelines, better BEV economics that lower the cost premium compared to similar ICE vehicles, and more charging stations that ease range anxiety. PHEVs make up about 22% of the market’s revenue. Their polymer demand is based on their combined ICE and battery electric powertrain architecture, which includes both the usual ICE polymer applications and a smaller but still significant set of EV-specific battery and electrical polymer applications.

Fuel cell electric vehicles, which make up about 5% of the market right now but are growing, are creating a need for specialized fluoropolymer membrane electrode assemblies, with Nafion perfluorosulfonic acid membrane being the most common proton exchange membrane material. They also need bipolar plate materials, fuel cell stack sealing components, and high-pressure hydrogen storage vessel liners made from thermoplastic or thermoset polymers.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 8.21 billion |

| Projected Market Size in 2035 | USD 28.93 billion |

| Market Size in 2025 | USD 6.84 billion |

| CAGR Growth Rate | 15.1% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Polymer Type, Application, Vehicle Type and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

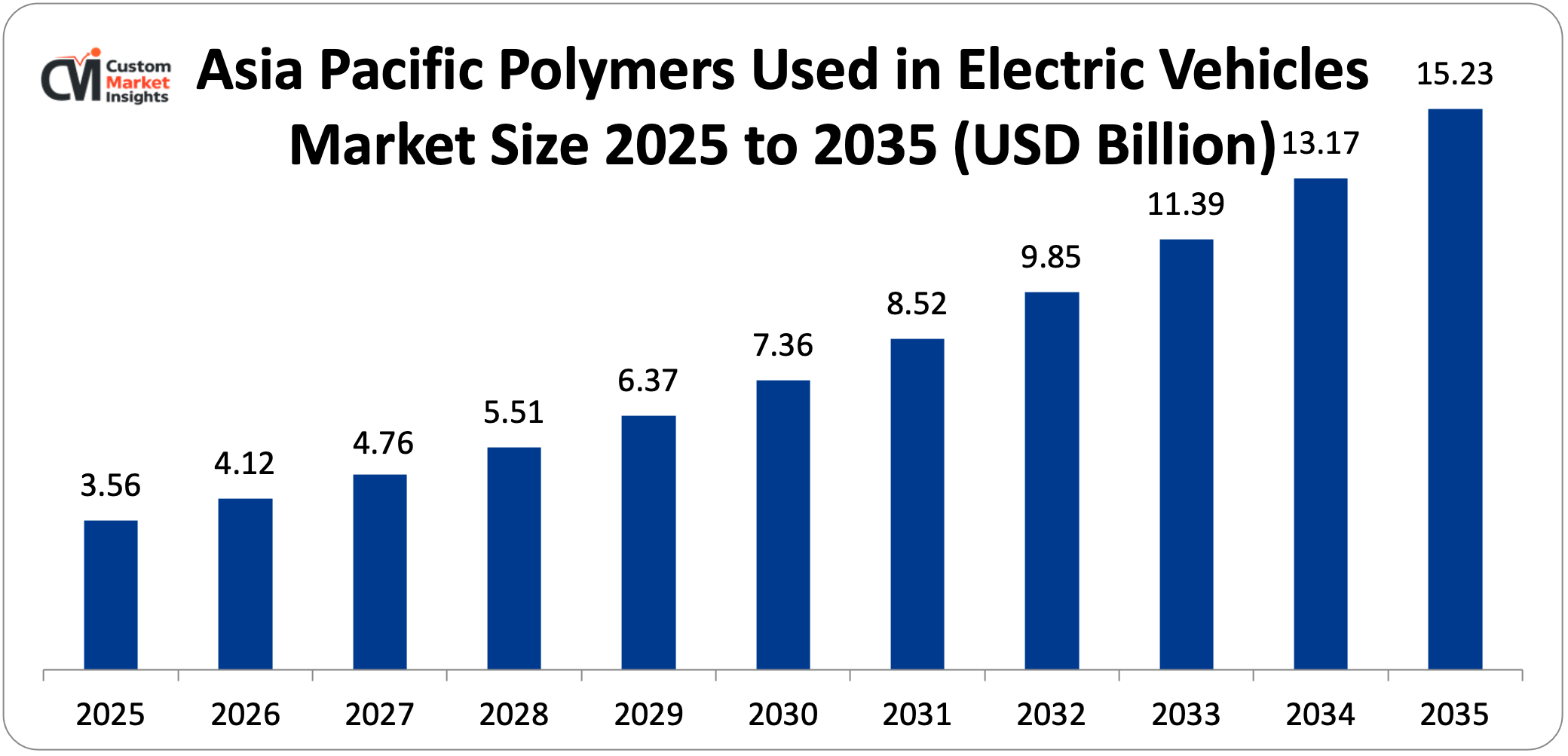

The Asia Pacific polymers used in electric vehicles market size are estimated at USD 3.56 billion in 2025 and are projected to reach approximately USD 15.23 billion by 2035, growing at a CAGR of 15.7% from 2026 to 2035.

Why did Asia Pacific Dominate the Market in 2025?

In 2025, Asia Pacific will account for about 52% of global market revenue. This is because it is the world’s main hub for electric vehicle production. In 2024, China alone will account for about 64% of global EV production, with domestic manufacturers like BYD, SAIC, Geely-Volvo, NIO, Li Auto, Xpeng, and Chery, as well as Tesla’s Shanghai Gigafactory and international joint ventures. Hyundai-Kia’s E-GMP and IONIQ platforms and LG Energy Solution, Samsung SDI, and SK On’s large-scale EV battery manufacturing operations are all important contributions from South Korea.

These companies make battery cells for both Korean OEMs and international customers like GM, Ford, and Volkswagen. Toyota, Honda, and Nissan of Japan are speeding up the development and production of BEV platforms after years of focusing on hybrids. Toyota’s promise to make 1.5 million BEVs a year by 2026 and 3.5 million by 2030 is a major new source of demand for EV-specific polymer materials.

China’s domestic polymer producers are improving their ability to develop compounds for electric vehicles (EVs). Companies like Kingfa Science & Technology, SINOPEC, and China National Chemical Corporation (ChemChina) are working on engineering thermoplastic compounds, fluoropolymer materials, and battery binder PVDF that are specifically designed for China’s huge domestic EV battery and vehicle manufacturing base. However, Western and Japanese specialty polymer suppliers with more experience in EV applications still dominate the premium EV market.

Why is Europe the Second-Largest and Most Regulatory-Driven Market?

In 2025, Europe will account for about 24% of global market revenue, or about USD 1.64 billion. This is because the EU has strict CO₂ fleet average regulations that require European OEMs to quickly increase EV production, regardless of short-term changes in consumer demand. Germany is the largest market in Europe and is home to the headquarters and main production facilities of Volkswagen Group (which includes Volkswagen, Audi, Porsche, SEAT, and ŠKODA), BMW Group, Mercedes-Benz, and Bosch. These companies are some of the biggest consumers of EV polymers in the world.

Germany is also home to the European headquarters and compound manufacturing facilities of major specialty polymer producers like BASF, Lanxess, Covestro, and Evonik. These companies have dedicated EV application development programs close to their OEM customers. European EV production is growing a lot thanks to new and bigger factories. For example, Volkswagen’s Zwickau and Emden plants, BMW’s Munich and Leipzig plants, Stellantis’ Mirafiori plant, and several new battery gigafactories run by Northvolt, ACC, and other international battery makers are all making more polymer demand in the region.

Why is North America Poised for Accelerating Growth?

By 2025, North America will account for about 17% of global market revenue. From 2026 to 2035, it is expected to grow at a CAGR of 13.5%. This growth will be fueled by the IRA-catalyzed wave of domestic EV manufacturing investment, the expansion of state-level ZEV mandates, and the creation of domestically oriented EV battery material supply chains that create new regional polymer demand centers. The North American market is likely to become more and more defined by premium EV segments, such as the Tesla Model 3 and Y, the Rivian R1T and R1S, the Cadillac LYRIQ, and the BMW iX. These segments have higher per-vehicle material value and a willingness to specify premium specialty polymer grades, which leads to higher revenue per unit of polymer volume.

Why is the Middle East & Africa Region an Emerging Opportunity?

In 2025, the LAMEA region will make up about 7% of the world’s market revenue. From 2026 to 2035, it will grow at a CAGR of 14.6%, thanks to Saudi Arabia and the UAE’s ambitious plans to increase EV adoption and manufacturing as part of their efforts to diversify their economies. The CEER electric vehicle brand is working to build a domestic EV manufacturing industry in Saudi Arabia, with plans to produce 100,000 vehicles a year by 2026. Meanwhile, the UAE is seeing more EV imports and charging infrastructure expansion, which is creating a domestic EV polymer aftermarket. Brazil is the main growth market in Latin America for LAMEA. This is because Chinese OEMs are working with Brazilian companies to make electric vehicles, and BYD is investing in a factory in Bahia state, which will increase the demand for polymers from Brazilian vehicle production.

Top Players in the Market and Their Offerings

- BASF SE

- Covestro AG

- Solvay S.A.

- DuPont de Nemours Inc.

- Celanese Corporation

- Lanxess AG

- Arkema S.A.

- Evonik Industries AG

- Toray Industries Inc.

- Sabic (Saudi Basic Industries Corporation)

- Others

Key Developments

The market has undergone significant developments as industry participants seek to expand capabilities and enhance product portfolios.

- In March 2025: BASF SE announced the commercial launch of its Ultramid Advanced N polyamide range. This range was specifically designed for 800-volt EV high-voltage connector and busbar overmolding applications. It has better partial discharge resistance, better hydrolysis stability during vehicle lifetime thermal cycling, and halogen-free flame retardancy rated at UL94 V-0 at 0.4mm wall thickness. This directly addresses the growing insulation performance requirements of next-generation 800-volt EV electrical architectures across mainstream and premium passenger vehicle platforms.

- In January 2025: Solvay S.A. announced that it would be increasing the capacity of its Solef PVDF production at its La Rochelle, France, facility. This is because there is a growing demand for battery-grade PVDF binder from EV battery cell manufacturers in Europe, North America, and Asia Pacific. The new capacity will meet the GMP-equivalent battery material quality standards required by leading EV battery cell producers, which will help IRA meet its domestic content compliance requirements for North American market vehicles.

These strategic actions have helped businesses improve their positions in the market, grow their product lines for electric vehicles (EVs), create new materials that meet the changing needs of EV architecture, and take advantage of the structural demand growth that is happening as the world moves from internal combustion engine vehicles to battery electric platforms in all major automotive markets.

The Polymers Used in Electric Vehicles Market is segmented as follows:

By Polymer Type

- Engineering Plastics

- Polyamide (PA6, PA66, PA12)

- Polycarbonate (PC)

- Polyphthalamide (PPA)

- Polyphenylene Sulfide (PPS)

- Polyetheretherketone (PEEK)

- Polybutylene Terephthalate (PBT)

- Elastomers & Rubber

- EPDM

- Fluorosilicone Rubber

- Thermoplastic Elastomers (TPE/TPV)

- Silicone Rubber

- Polyurethanes

- Rigid Foam

- Flexible Foam

- Thermoplastic Polyurethane (TPU)

- Fluoropolymers

- PTFE

- PVDF

- ETFE

- FEP & PFA

- Epoxy Resins & Composites

- Carbon Fiber Reinforced Epoxy

- Glass Fiber Reinforced Epoxy

- Other Polymer Types

By Application

- Battery & Energy Storage Systems

- Cell Separators & Pouch Films

- Module Frames & Cell Holders

- Battery Enclosures & Pack Structures

- Thermal Interface Materials

- Battery Sealing & Gasketing

- Exterior Components

- Body Panels & Closures

- Bumpers & Fascias

- Aerodynamic Underbody Panels

- Interior Components

- Instrument Panels & Dashboard

- Door Panels & Trim

- Seating Systems

- Powertrain & Drivetrain

- Thermal Management Systems

- Electrical & Electronic Systems

- High-Voltage Wiring & Cable Insulation

- Connector Housings

- Power Electronics Enclosures

- Other Applications

By Vehicle Type

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Fuel Cell Electric Vehicles (FCEV)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Polymers Used in Electric Vehicles by Segments

- 2.1.2. Polymers Used in Electric Vehicles by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Polymers Used in Electric Vehicles Market Attractiveness Analysis, By Polymer Type

- 2.2.3. Polymers Used in Electric Vehicles Market Attractiveness Analysis, By Application

- 2.2.4. Polymers Used in Electric Vehicles Market Attractiveness Analysis, By Vehicle Type

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Accelerating Global Electric Vehicle Production and Adoption Creating Structural Polymer Demand Growth

- 3.1.2. Unique EV Battery Architecture Creating High-Value Polymer Applications Without Precedent in Conventional Automotive

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Polymers Used in Electric Vehicles Market – By Polymer Type

- 4.1. Polymer Type Market Overview, By Polymer Type Segment

- 4.1.1. Polymers Used in Electric Vehicles Market Revenue Share, By Polymer Type, 2025 & 2035

- 4.1.2. Engineering Plastics

- 4.1.2.1. Polyamide (PA6, PA66, PA12)

- 4.1.2.2. Polycarbonate (PC)

- 4.1.2.3. Polyphthalamide (PPA)

- 4.1.2.4. Polyphenylene Sulfide (PPS)

- 4.1.2.5. Polyetheretherketone (PEEK)

- 4.1.2.6. Polybutylene Terephthalate (PBT)

- 4.1.3. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Elastomers & Rubber

- 4.1.6.1. EPDM

- 4.1.6.2. Fluorosilicone Rubber

- 4.1.6.3. Thermoplastic Elastomers (TPE/TPV)

- 4.1.6.4. Silicone Rubber

- 4.1.7. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Polyurethanes

- 4.1.10.1. Rigid Foam

- 4.1.10.2. Flexible Foam

- 4.1.10.3. Thermoplastic Polyurethane (TPU)

- 4.1.11. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Fluoropolymers

- 4.1.14.1. PTFE

- 4.1.14.2. PVDF

- 4.1.14.3. ETFE

- 4.1.14.4. FEP & PFA

- 4.1.15. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Epoxy Resins & Composites

- 4.1.18.1. Carbon Fiber Reinforced Epoxy

- 4.1.18.2. Glass Fiber Reinforced Epoxy

- 4.1.19. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Other Polymer Types

- 4.1.23. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Polymer Type Market Overview, By Polymer Type Segment

- Chapter 5. Polymers Used in Electric Vehicles Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Polymers Used in Electric Vehicles Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Battery & Energy Storage Systems

- 5.1.2.1. Cell Separators & Pouch Films

- 5.1.2.2. Module Frames & Cell Holders

- 5.1.2.3. Battery Enclosures & Pack Structures

- 5.1.2.4. Thermal Interface Materials

- 5.1.2.5. Battery Sealing & Gasketing

- 5.1.3. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Exterior Components

- 5.1.6.1. Body Panels & Closures

- 5.1.6.2. Bumpers & Fascias

- 5.1.6.3. Aerodynamic Underbody Panels

- 5.1.7. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Interior Components

- 5.1.10.1. Instrument Panels & Dashboard

- 5.1.10.2. Door Panels & Trim

- 5.1.10.3. Seating Systems

- 5.1.11. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Powertrain & Drivetrain

- 5.1.15. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Thermal Management Systems

- 5.1.19. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Electrical & Electronic Systems

- 5.1.22.1. High-Voltage Wiring & Cable Insulation

- 5.1.22.2. Connector Housings

- 5.1.22.3. Power Electronics Enclosures

- 5.1.23. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1.26. Other Applications

- 5.1.27. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 5.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.29. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Polymers Used in Electric Vehicles Market – By Vehicle Type

- 6.1. Vehicle Type Market Overview, By Vehicle Type Segment

- 6.1.1. Polymers Used in Electric Vehicles Market Revenue Share, By Vehicle Type, 2025 & 2035

- 6.1.2. Battery Electric Vehicles (BEV)

- 6.1.3. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Plug-in Hybrid Electric Vehicles (PHEV)

- 6.1.7. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Hybrid Electric Vehicles (HEV)

- 6.1.11. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Fuel Cell Electric Vehicles (FCEV)

- 6.1.15. Polymers Used in Electric Vehicles Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Vehicle Type Market Overview, By Vehicle Type Segment

- Chapter 7. Polymers Used in Electric Vehicles Market – Regional Analysis

- 7.1. Polymers Used in Electric Vehicles Market Overview, By Region Segment

- 7.1.1. Global Polymers Used in Electric Vehicles Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Polymers Used in Electric Vehicles Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Polymers Used in Electric Vehicles Market Revenue, By Polymer Type, 2026 – 2035

- 7.1.4. Global Polymers Used in Electric Vehicles Market Revenue, By Application, 2026 – 2035

- 7.1.5. Global Polymers Used in Electric Vehicles Market Revenue, By Vehicle Type, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Polymers Used in Electric Vehicles Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Polymers Used in Electric Vehicles Market Revenue, By Polymer Type, 2026 – 2035

- 7.2.3. North America Polymers Used in Electric Vehicles Market Revenue, By Application, 2026 – 2035

- 7.2.4. North America Polymers Used in Electric Vehicles Market Revenue, By Vehicle Type, 2026 – 2035

- 7.2.5. U.S. Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Polymers Used in Electric Vehicles Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Polymers Used in Electric Vehicles Market Revenue, By Polymer Type, 2026 – 2035

- 7.3.3. Europe Polymers Used in Electric Vehicles Market Revenue, By Application, 2026 – 2035

- 7.3.4. Europe Polymers Used in Electric Vehicles Market Revenue, By Vehicle Type, 2026 – 2035

- 7.3.5. Germany Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Polymers Used in Electric Vehicles Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Polymers Used in Electric Vehicles Market Revenue, By Polymer Type, 2026 – 2035

- 7.4.3. Asia Pacific Polymers Used in Electric Vehicles Market Revenue, By Application, 2026 – 2035

- 7.4.4. Asia Pacific Polymers Used in Electric Vehicles Market Revenue, By Vehicle Type, 2026 – 2035

- 7.4.5. China Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Polymers Used in Electric Vehicles Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Polymers Used in Electric Vehicles Market Revenue, By Polymer Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Polymers Used in Electric Vehicles Market Revenue, By Application, 2026 – 2035

- 7.5.4. The Middle-East and Africa Polymers Used in Electric Vehicles Market Revenue, By Vehicle Type, 2026 – 2035

- 7.5.5. Saudi Arabia Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Polymers Used in Electric Vehicles Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Polymers Used in Electric Vehicles Market Revenue, By Polymer Type, 2026 – 2035

- 7.6.3. Latin America Polymers Used in Electric Vehicles Market Revenue, By Application, 2026–2035

- 7.6.4. Latin America Polymers Used in Electric Vehicles Market Revenue, By Vehicle Type, 2026 – 2035

- 7.6.5. Brazil Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Polymers Used in Electric Vehicles Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Polymers Used in Electric Vehicles Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Polymers Used in Electric Vehicles Market: Company Market Share, 2025

- 8.2. Global Polymers Used in Electric Vehicles Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. BASF SE

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Covestro AG

- 9.3. Solvay S.A.

- 9.4. DuPont de Nemours Inc.

- 9.5. Celanese Corporation

- 9.6. Lanxess AG

- 9.7. Arkema S.A.

- 9.8. Evonik Industries AG

- 9.9. Toray Industries Inc.

- 9.10. Sabic (Saudi Basic Industries Corporation)

- 9.11. Others.

- 9.1. BASF SE

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Healthcare Foresights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

- Chapter 12. List Of Figures

- 12.1. Figures No 1 to 66

- Chapter 13. List Of Tables

- 13.1. Tables No 1 to 46

Prominent Player

- BASF SE

- Covestro AG

- Solvay S.A.

- DuPont de Nemours Inc.

- Celanese Corporation

- Lanxess AG

- Arkema S.A.

- Evonik Industries AG

- Toray Industries Inc.

- Sabic (Saudi Basic Industries Corporation)

- Others

FAQs

The key players in the market are BASF SE, Covestro AG, Solvay S.A., DuPont de Nemours Inc., Celanese Corporation, Lanxess AG, Arkema S.A., Evonik Industries AG, Toray Industries Inc., Sabic (Saudi Basic Industries Corporation), Others.

Government regulations are the foundational force driving EV adoption — and consequently polymer demand — through multiple complementary mechanisms: the EU’s 2035 ICE vehicle sales ban creating a firm regulatory deadline that makes OEM electrification strategies non-discretionary; CO₂ fleet average targets in Europe, China, and the United States imposing financial penalties on automakers failing to achieve EV sales mix targets; purchase subsidies and tax credits in China, the United States, Germany, France, Norway, and dozens of other markets reducing the consumer price premium of EVs relative to ICE equivalents and accelerating adoption timelines; domestic content requirements in the IRA and potential EU equivalents driving regionalization of EV battery and material supply chains creating new polymer demand in previously underserved manufacturing geographies; battery safety regulations including China’s GB 38031, UNECE Regulation 100, and developing equivalent standards in the United States and Japan mandating specific fire safety performance standards that drive adoption of flame-retardant polymer compounds and thermal runaway containment materials; and EV charging infrastructure investment programs — including the U.S. The National Electric Vehicle Infrastructure (NEVI) program and similar programs in the EU are making it easier for people to charge their electric vehicles in public, which directly lowers range anxiety and speeds up the adoption of BEVs among groups of people who were previously hesitant.

The price range for polymers used in electric vehicles is very wide. For example, battery module structural parts made of glass-fiber-reinforced polyamide cost USD 3–5 per kilogram, while engineering PEEK and PAI compounds for the most demanding thermal and electrical applications cost USD 80–200 per kilogram. Battery-grade PVDF costs USD 15–35 per kilogram because of its chemical complexity and the fact that demand for EVs is rising. The average polymer revenue per kilogram in EV applications is about 2.3 times that of similar ICE vehicle polymer applications. This is because EV applications use more premium engineering and specialty grades. Battery-grade PVDF prices went up to USD 50–80 per kilogram during the battery material shortage from 2021 to 2022. They have since come down with new capacity additions, but they are still much higher than they were before the shortage. They are expected to stay in the USD 20–35 per kilogram range until the mid-2020s, when production from Solvay, Arkema, Kureha, and Chinese producers reaches full capacity. Long-term supply agreements with annual or multi-year price adjustment mechanisms are becoming more common for EV battery polymer supply. This gives specialty polymer producers who are investing in dedicated EV-grade production capacity a clear picture of their future revenue.

Current analysis suggests that the market will reach about USD 28.93 billion by 2035. This is because global EV production is expected to grow to 40–50 million units per year, the size of battery packs per vehicle is expected to grow, the transition to 800-volt architectures is expected to expand the fluoropolymer application base, and the commercialization of solid-state batteries is expected to create new polymer electrolyte and structural material demand categories. Additionally, EV production is expected to move into North America, Europe, Southeast Asia, and India, creating new regional polymer demand centers. The market is expected to grow at a CAGR of 15.1% from 2026 to 2035.

Asia Pacific is expected to keep the largest share of revenue throughout the forecast period, rising from 52% in 2025 to about 55% by 2035. This is because China, South Korea, and Japan are still the main places where EVs and lithium-ion battery cells are made. As investment in domestic EV manufacturing grows, North America and Europe will gain market share. However, Asia Pacific will continue to lead in EV production volumes, battery cell manufacturing scale, and the gradual improvement of regional high-performance polymer supply chains. This will keep the region at the top of the market through 2035 and beyond.

Asia Pacific is expected to grow the fastest, at a rate of 15.7% per year, from 2026 to 2035. This is because China is expected to make 18–20 million electric vehicles (EVs) by 2027, CATL and BYD’s combined battery manufacturing capacity expansion will create the world’s largest incremental PVDF and engineering plastic demand, South Korea’s E-GMP platform expansion will affect Hyundai-Kia’s global production, Japan’s major BEV production scale-up will come from Toyota, Honda, and Nissan, and Southeast Asian EV manufacturing hubs will be set up in Thailand, Indonesia, and Vietnam, attracting Chinese and international OEM investment in regional production.

The Global Polymers Used in Electric Vehicles Market is predicted to experience substantial growth driven by global EV sales reaching 17.1 million units in 2024 and projected to represent over 60% of new vehicle sales by 2035; BEVs containing 120–180 kilograms of polymer content per vehicle versus 80–100 kilograms in comparable ICE vehicles creating structural per-unit polymer demand premium; PVDF binder demand from EV battery manufacturing projected to grow from 95,000 metric tonnes in 2024 to over 380,000 metric tonnes by 2030; 800-volt EV architecture adoption expanding across 35+ vehicle models by 2027 driving fluoropolymer insulation demand at the fastest CAGR of 18.3%; thermally conductive polymer compound demand growing at over 20% CAGR for battery thermal management applications; and the IRA and EU domestic content requirements driving North American and European EV battery material supply chain investment, generating new regional polymer demand centers independent of Asian supply chains.