Digital Twin in Marine Market Size, Trends and Insights By Component (Software (Digital Twin Platforms, Simulation Software, Analytics), Hardware (IoT Sensors, Edge Computing Devices, Connectivity Equipment), Services (Consulting, Integration, Managed Services, Training)), By Application (Fleet Management & Operations, Predictive Maintenance, Ship Design & Engineering, Port & Harbor Management, Cargo & Logistics Optimization, Training & Simulation, Other Applications (Environmental Compliance, Safety Management)), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By End-User (Commercial Shipping (Container, Tanker, Bulk Carrier, Cruise), Naval & Defense, Offshore Oil & Gas, Port Authorities & Terminal Operators, Shipbuilders & Yards, Other End-Users), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Europe |

Major Players

- Kongsberg Digital AS

- Wärtsilä Corporation

- ABB Ltd.

- Siemens AG

- Others

Reports Description

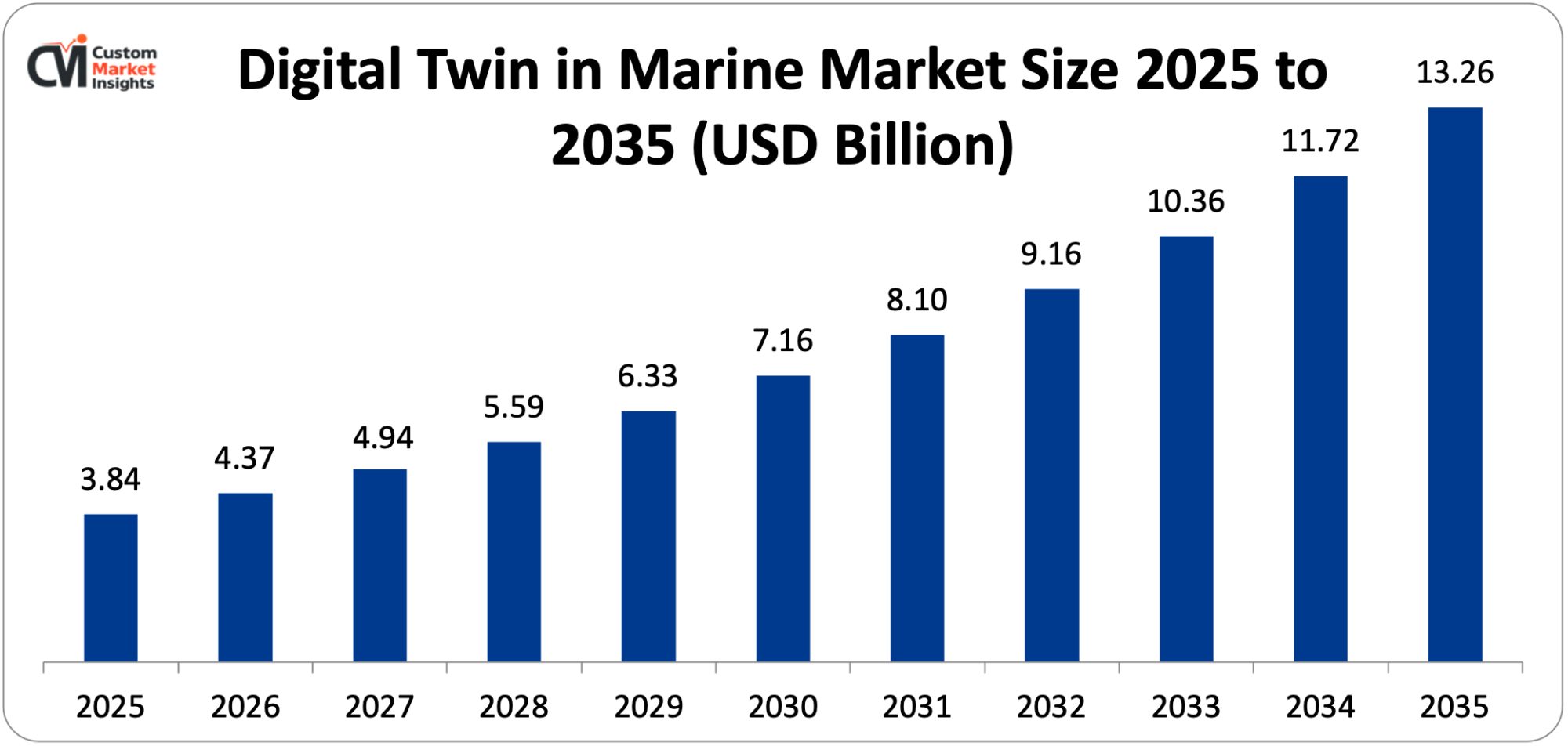

The overall size of the digital twin in the marine market around the globe will be assessed at USD 3.84 billion in 2025 and is projected to grow between USD 4.37 billion in 2026 and around USD 13.26 billion in 2035 at an 11.7% CAGR rate between 2026 and 2035.

The increasing use of Industry 4.0 technologies in maritime functions due to the need to decarbonize and meet the fuel consumption requirements and efficiency, the increasing use of IoT sensor networks on ships, which allow real-time monitoring of performance and synchronization of the digital twin, the growing regulatory demands by the International Maritime Organization that force the management of emissions to be data-driven and reported, the growing complexity of contemporary vessel systems that necessitate advanced simulation requirements to streamline marine operations, and the intensive maturing of AI and machine learning platforms that allow predictive analytics to be provided by big data on maritime operational datasets collectively drive robust and sustained market growth throughout the forecast period.

Market Highlight

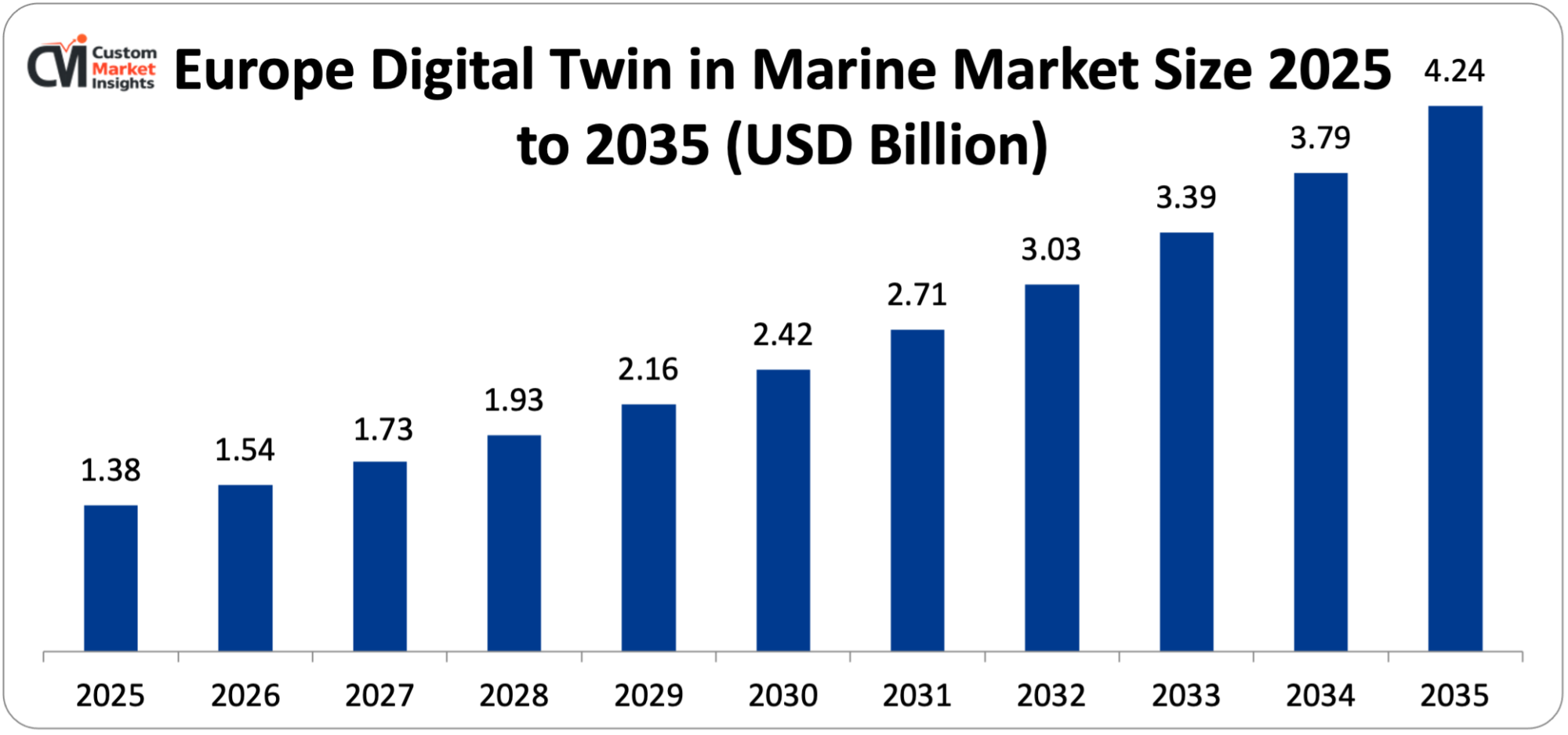

- Europe dominated in the Marine market with a 36% market share of the digital twin in 2025.

- Asia Pacific will be adding at the quickest CAGR of 14.8% amid 2026 and 2035.

- By component, the software segment took about 52% of the market share in the year 2025.

- By segment, the services segment is increasing in CAGR fastest at 13.4 between 2026 and 2035.

- Application-wise, the fleet management and operations segment will have the largest market share of 31% in 2025 and the predictive maintenance segment is likely to have the highest growth rate of 15.2% throughout the forecasted years of 2026 to 2035.

- By deployment mode, the cloud-based segment earned market share of 64% in 2025, and the cloud-based segment is likely to rise at the highest CAGR rate of 13.9% between 2026 and 2035.

- By end-user, the commercial shipping segment offered the largest market share of 48% in 2025, and the port authorities segment is expected to experience the highest CAGR between 2026 and 2035 at 16.1%.

Significant Growth Factors

The Digital Twin in Marine Market Trends present significant growth opportunities due to several factors:

- IMO Decarbonization Mandates and Fuel Efficiency Imperatives Driving Digital Twin Adoption:

The progressive expansion of greenhouse gas emission reduction targets to the global shipping fleet under the Carbon Intensity Indicator (CII) regulation is establishing the strongest regulatory force of digital twins in the marine industry since vessel operators are obligated to show specific annual changes in carbon intensity or risk operational limitations that directly affect the deployment of commercial vessels and their charter rate competitiveness. Global shipping industry is identified as contributing around 2.89% of global greenhouse gases in the IMO Fourth GHG Study and shipping about 90% of world trade by weight, so decarbonization of shipping is not only of commercial necessity owing to regulatory vulnerability but also of technical difficulty by virtue of the energy intensity of large ship propulsion over long ocean routes where real-time operational optimization is the most immediately available emissions reduction lever.

Digital twin platforms enable the physics-based capability of simulating the hydrodynamics and thermodynamics of vessel propulsion and auxiliary system energy consumption in a wide range of scenarios: vessel speeds, loading, weather, route conditions, and cargo delivery guarantees allow a vessel operator to make the optimisation decision of a voyage to minimise fuel consumption and carbon intensity without breaching cargo delivery obligations. The publication of case studies of early deployments of the digital twin to maritime has documented up to a 5-15% fuel reduction, which could be achieved through the use of a digital twin to optimize voyage and propulsion which can be considered annual savings of USD 500,000-USD 3 million in fuel costs at present bunker fuel prices on a large container ship or bulk carrier. An annual rating system (under the CII regulation) based on the performance of carbon intensity, whereby vessels are assigned letter grades A (best) to E (worst) and whereby vessels with a rating of D or E must prepare corrective action plans, establishes a conflict of competitive fleet management whereby an operationally optimized digitally twinned vessel directly translates to commercial differentiation through high CII ratings, which can be used to support charter rate premiums and vessel employment security.

The introduction of shipping into the Emissions Trading System (EU ETS) by the EU, which goes into effect in January 2024, which compels shipping companies to purchase and sell EU Allowances to cover CO₂ emissions on voyages visiting European ports, introduces a direct financial cost of CO₂ emissions to the European shipping industry of EUR 60-EUR 80 per tonne of CO₂, which is directly cost-recovered by ETS allowance cost savings.

- Growing IoT and Connectivity Infrastructure Enabling Real-Time Vessel Digital Twins:

The recent maturation of marine sensor technology in the IoT and the lowering of the cost of satellite broadband connectivity as well as edge computing infrastructure aboard vessels is enabling the fluid generation of real-time data on the vessel systems that is the technical precondition in the operational digital twins, that is, turning the marine digital twin into a design-time simulation device into an operational decision support platform that reflects the condition and performance of the vessel in real-time throughout the voyages. Large modern vessels, which may be either container ships, tankers, bulk carriers, or cruise ships, contain thousands of sensor measurement points in propulsion equipment, hull areas, cargo and navigation systems, and environmental control systems, and sensor data have traditionally been logged in siloed system specific databases that did not allow cross-system analysis of performance.

Marine IoT systems such as Kongsberg Vessel Insight, Wartsila Unified Connectivity and ABB ability systems combine sensor data streams across various vessel systems into unified data lakes, which supply the integrated operational database on which digital twin models are constantly being updated and verified. High-bandwidth vessel-to-shore data transmission at wireless access prices that render continuous real-time vessel data streaming to cloud-based digital twin platforms economically viable, with Starlink Maritime achieving 350 Mbps of data bandwidth access aboard vessels, is being made possible by the deployment of both VSAT and low Earth orbit (LEO) satellite broadband connectivity, such as the services being offered by Starlink Maritime, OneWeb, and Intelsat, and (when implemented) effectively converts the connectivity bottleneck that has traditionally necessitated data compression and select the e-Navigation strategy of the International Maritime Organization the adoption of a universal digital exchange of data among vessels, ports, and maritime administrations, is developing a regulatory ecosystem that increasingly necessitates a digital connectivity standard on board ships, which offers the basis on which a digital twin system of data acquisition can be constructed. Published market data indicate that the marine IoT connectivity market is expanding at a very fast rate, with vessel operators transitioning their old satellite-based systems to new high-bandwidth options and deploying extensive sensor networks, and that the overall marine IoT hardware and connectivity services market is offering a closely correlated demand stimulus to the marine digital twin software and services market.

What are the Major Advances Changing the Digital Twin in Marine Market Today?

- AI-Powered Predictive Maintenance Transforming Fleet Reliability Management:

Predictive maintenance is also being enabled by integrating artificial intelligence and machine learning algorithms with digital twin models of the vessel machinery systems, including main engines, auxiliary engines, gearboxes, propellers, pumps, compressors, and heat exchangers, so that developing equipment failures are detected many weeks ahead of the physical manifestations appearing, and planned interventions to effectively maintain the equipment can be performed during the regularly scheduled port calls, avoiding an expensive unplanned onboard breakdown with the associated repair costs, delayed cargo transit, and possible accidental incidents.

The use of all three parts of condition-based maintenance, namely continuous sensor monitoring, digital twin performance modeling, and AI anomaly detection, which compares the real performance of equipment with physics-based digital twin prognostication to detect deviations that can be linked to the development of faults, is replacing traditional marine maintenance methods, which include fixed-interval calendar-based maintenance and reactive repair after equipment failure. Engine computer twins – simulation of the thermodynamic cycle of marine diesel and dual-fuel engines based on the data on cylinder pressure, exhaust temperatures, fuel consumption rates, and turbocharger performance parameters can identify early warning signs of degradation of the fuel injection system, piston ring wear, turbocharger fouling, and bearing wear that start to appear as small deviations in the predicted performance baseline of the engine twin before leading to detectable loss of power or operational disturbance.

The Expert Insight predictive analytics platform, a platform offering engine digital twin modeling with machine learning anomaly detection on a fleet of thousands of monitored engines by Wartsilas, has published case study data indicating that predicted maintenance interventions found by the predictive analytics platform have prevented engine failures with hold-up avoided downtime costs of USD 50,000-USD 500,000 broken down per incident, which has provided a return on investment multiple of 5-20 times the annual platform subscription cost per fleet operator. Economics of AI predictive maintenance digital twins is especially strong in high value commercial vessels, such as those of large container vessels, VLCCs, and LNG carriers, where unscheduled off-hire costs the charter operator USD 30,000-USD 150,000/day in lost revenue and emergency maintenance costs, and a single prevented failure per year alone can provide enough of a financial rationale to invest in a comprehensive digital twin predictive maintenance program.

Classification society incorporation Digital twin-enabled maintenance interval extension is developing regulatory validation routes to digital twin-informed maintenance interval extension to allow vessel operators to postpone expensive dry-docking maintenance when the digital twin condition monitoring system is in place to determine that the system is still healthy and generates a separate direct monetary reward on digital twin investment.

- Ship Design Digital Twins Accelerating Naval Architecture Innovation:

The integration of digital twin technology into the design and development of a ship, through the concept design process to detailed engineering, hydrodynamic optimization, structural analysis, systems integration modeling, and construction monitoring, is fundamentally speeding up the innovation cycle in the field of naval architecture, lowering design iteration costs, and letting the complexity of current vessel architecture projects, including alternative fuel propulsion systems, sophisticated energy efficiency technology, and autonomous operation capability, be developed in a way that would not be practically manageable without and through robust digital simulation environments.

The design phase digital twin combines the computational fluid dynamics (CFD) hydrodynamic models that calculate hull resistance, propeller efficiency, and seakeeping performance over the entire range of operation speed and loading with structural finite element analysis models, propulsion system thermodynamic simulations, and systems engineering models of electrical power distribution, HVAC and cargo handling systems into a single virtual vessel prototype with interdisciplinary design optimization prior to the start of physical construction. Major vendors of naval architecture and marine engineering systems such as Deltamarin (Wartsila), users of the FORAN system, adherents of the AVEVA Marine platform and users of the Siemens Simcenter marine simulation toolkit are supplying digital twin design services that allow new vessel concept evaluation cycles in weeks, not months, and CFD-validated hull form optimization which has delivered documented fuel consumption savings of 3-8% over conventionally designed baseline hulls.

Engineering of the next generation of alternative fuel vessels, such as methanol dual-fuel container ships, ammonia-ready tankers, LNG-powered cruise ships, and hydrogen fuel cell ferries, should have a particularly intense load on digital twin-supported engineering due to the unprecedented safety, operational, and structural performance of these fuels, and the digital simulation is the only way the design team can test safety scenarios, optimize fuel system layouts, and certify compliance with regulations before building physical prototypes, which are expensive. High-profile shipbuilders such as Hyundai Heavy Industries, Daewoo Shipbuilding and Marine Engineering and Fincantieri are developing shipyard digital twins, which simulate the construction process itself, such as berth logistics, block assembly sequencing, material flow, workforce allocation, and outfitting progress, to optimize the construction scheduling and resource utilization, and simulating the construction process allows detecting a bottleneck and risks in the timetable before reflecting on the physical berth.

- Port and Harbor Digital Twins Enabling Smart Port Transformation:

The creation and implementation of port and harbor digital twins – the creation of comprehensive virtual representations of port infrastructure, vessel traffic, berth utilization, cargo handling equipment, gate operations, and intermodal connections – are allowing port officials and terminal operators to optimize the incredibly complex logistics system of a large commercial port without necessarily expanding physical infrastructure. The largest container ports in the world, such as Shanghai, Singapore, Shenzhen, and Rotterdam process tens of millions of twenty-foot equivalent units (TEUs) per year, and the efficiency of the port directly influences the competitiveness of the supply chains to which it is linked and the productivity of billions of dollars of capital investment into cranes, yard tractors, and storage facilities. One of the most sophisticated applications of a digital twin to operational port deployments in the world is the digital twin of the Port of Rotterdam, which is built on a digital twin at a city scale and is designed to simulate vessel traffic scenarios, optimize the allocation of berths, and model the reaction of the port to storm surges and other disruption events in real time using real-time vessel AIS transponder, quay crane sensor, weather station, water level gauge, and traffic monitoring system data.

The digital twin program by the Singapore Maritime and Port Authority (as part of a wider Smart Nation digital infrastructure program) has created a detailed 3D model of the port waters, vessel traffic management systems and port terminal operations of Singapore which is being utilised to streamline vessel scheduling, diminish the length of time of anchorage waiting, and simulate the implementation of autonomous vessel functions into Singapore’s congested port approach channels. Digital twin technology has been identified by the International Association of Ports and Harbors (IAPH) as a priority type of investment of port modernization globally, and an IAPH survey conducted in 2024 found that more than 60% of major ports in the world had either installed or were in the process of installing digital twins – one of the fastest rates of adoption, making port authority digital twin programs one of the most important short-term drivers of market growth in the marine digital twin market.

Category Wise Insights

By Component

Why Does Software Lead the Market?

Software is the highest share segment at about 52% of total market share in 2025, since the sheer intellectual property intensity of developing a digital twin platform is years of engineering development that fetches high subscription and licensing rates, compared to the physical hardware infrastructure. Kongsberg Digital: Kongsberg Digital develops Vessel Insight along with Kognifai ecosystem software platforms to provide the application layer through which the vessel operators, fleet managers, and port authorities can access operational insights, predictive alerts, and simulation capabilities that drive business value out of the underlying sensor data infrastructure. Wärtsilae: Wärtsilae develops Fleet Operations Solution software to offer the application layer through which the vessel operators, fleet managers, and port authorities can access operational insights, predictive alerts, and simulation capabilities generated by the underlying sensor data infrastructure.

AVEVA The dominance of the software segment is enhanced by the subscription based revenue model used by the major maritime digital twin platform providers, where the annual fees on software licenses generate recurring revenue that increases with the addition of capabilities and user base to the platform – which creates highly visible and compounding revenue streams that are appealing to both the providers of the platform and their investors. This transformation to platform-as-a-service modes of delivery (where maritime digital twin capabilities are sold in the form of cloud-based subscription services as opposed to on-premise software licenses) is driving higher software segment revenue per customer in that it integrates the cost of cloud infrastructure into platform pricing and enhances customer accessibility, as well as making deployment more complex.

By Application

Why Does Fleet Management & Operations Lead the Market?

The largest area of application is fleet management and operations at about 31% of total market share in 2025 because this reflects the immediate and measurable commercial benefit that digital twin-enabled fleet performance optimization represents to vessel operators in terms of fuel costs, which is the largest controllable operating cost of commercial shipping companies, generally 40–60% of daily operating costs of vessels at prevailing bunker fuel prices. Strategic technology investments in operational excellence Digital twin platforms at the fleet level (where vessel performance data is aggregated on the fleet scale, or tens or hundreds of vessels) can be deployed by large shipping companies such as Maersk, MSC, CMA CGM, and Evergreen as strategic technology platforms that directly support financial performance and achievement of decarbonization targets. The digital twin market of the fleet operations market executing fuel savings has a clear and measured payback, which is fuel savings of 5-10% of a large fleet will result in tens of millions of dollars of annual savings, which will indisputably justify the investment in digital twins platforms, which will generate a strong demand pull in the market that exist on the basis of which the assistance of regulatory pressure or a motivation to study sustainability is irrelevant.

By Deployment Mode

Why Does Cloud-Based Deployment Lead the Market?

In cloud-based deployment, the biggest deployment is the biggest deployment mode with around 64% market share in 2025, indicating a fundamental appropriateness of cloud infrastructures to the maritime digital twin use case: where the operational data of vessels at sea is continuously sent to analytics platform on shore, processed against fleet-scale machine learning models trained on aggregated multi-vessel data, and accessed by the fleet management teams and shore-based operations centres via web browser interfaces that do not necessarily require any software to be installed on-premise. Cloud deployment provides maritime digital twin platform providers with global shipping fleets of vessels operating in all oceans because the need to deploy a server on each vessel or to have various data centers located on shores is removed.

The scalability benefit of cloud infrastructure – allowing the digital twin platform providers to handle data of increasing vessel fleets without the corresponding capital investment in infrastructure – allows the economics of subscription pricing models that digitally twin access is economically viable to smaller fleet operators who would not be willing to make the capital investment of on-premise enterprise software. Maritime-specific cloud security models and the gradual development of maritime cybersecurity standards such as IMO MSC-FAL.1/Circ.3 guidelines and the BIMCO Guidelines on Cyber Security Onboard Ships is also addressing cybersecurity concerns, which have traditionally supported on-premise deployment of sensitive vessel operational data.

By End-User

Why Does Commercial Shipping Lead the Market?

The greatest end-user segment is commercial shipping, which is estimated at about 48% of total market share in 2025, as it reflects the juxtaposition of the largest addressable vessel fleet, that is, more than 100,000 commercial vessels over 100 gross tonnage are operating globally according to UNCTAD Review of Maritime Transport; the greatest fuel cost and decarbonization pressure of any maritime industry, and the greatest financial capacity of large shipping corporations and their financial investors to invest in enterprise digital twins. Container shipping Underpinned by the largest carriers active in the business, such as Maersk, MSC, CMA CGM, Hapag-Lloyd and Evergreen, the scale of their operations, the complexity of their technical systems, and the high competitive pressure to run a profitable business are the primary consumers of comprehensive digital twin fleet management systems.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 4.37 billion |

| Projected Market Size in 2035 | USD 13.26 billion |

| Market Size in 2025 | USD 3.84 billion |

| CAGR Growth Rate | 11.7% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Component, Application, Deployment Mode, End-User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Europe Market Size?

The European digital twin in marine market size is estimated at USD 1.38 billion in 2025 and is projected to reach approximately USD 4.24 billion by 2035, with a CAGR of 11.9% from 2026 to 2035.

Why Did Europe Dominate the Market in 2025?

The leading maritime technology companies of the world, including Koningsberger Digital, Wartsilas Marine, ABB marine, Rolls-Royce marine and AVEVA, are all concentrated in Norway, Finland, Switzerland, and the United Kingdom, the most advanced maritime decarbonization regulatory environment globally, and are major shipping companies and port operators, making Europe one of the main leaders of global maritime digitalization. The Norwegian maritime cluster, which includes Kongsberg Digital, DNV, and an extensive ecosystem of maritime technology firms based in the Vestfold and Telemark area, is the most innovative and productive geography in the development of maritime digital twins technology, though the Norwegian maritime technology companies pioneered the development of vessel performance monitoring, integrated bridge systems, and the development of dynamic positioning technologies that are the technical backbone of the current maritime digital twin systems.

The Fit for 55 legislative package and European Green Deal – demand a 55% cut in EU greenhouse gas emissions by 2030 since 1990, with the maritime transport sector covered by extension of the EU ETS — establishes the highest level of decarbonization regulatory framework of shipping across the world and encourages European fleet operators to invest heavily in digital optimization tools that will deliver the quantifiable carbon intensity reductions needed to comply with the regulations. The European gateway operations of Rotterdam, Antwerp-Bruges, Hamburg, and the Port of Singapore have been the most digitally advanced port operations in the world, and the digital twin investment in these ports has been the world leader in benchmarking port operations elsewhere in the world that are looking to emulate the changes in operational efficiency that has been displayed in these advanced facilities.

Why is Asia Pacific the Fastest-Growing Market?

The fastest-growing regional market is Asia Pacific where the expected CAGR is 14.8% over 2026-35 due to the fact that the region is the dominant global shipbuilding geography; South Korea, China and Japan alone build more than 90% of the world’s vessels by compensated gross tonnage, providing an enormous new market in vessel construction where digital twin capabilities are now seen as standard features by advanced ship owners, and competitive differentiators as offered by shipyards. The three largest Korean shipbuilders, Hyundai Heavy Industries, Samsung Heavy Industries, and Daewoo Shipbuilding and Marine Engineering, have invested heavily in digital twin and smart shipbuilding technologies, with Integrated Intelligent Ship (HiSIS) digital twin platform of HHI and SmartShip Hub of DSME being the most developed digital twins technologies available in the shipyard in the global market. The Chinese digital maritime is a push to invest in digital twins to manage commercial fleet at major Chinese shipping lines such as COSCO Shipping and China Merchants Energy Shipping, as well as to develop smart ports within the massive Chinese port network that also includes the largest container port in the world in Shanghai and a number of other top-ten container ports in the world. Digital transformation of Japan, via i-Shipping by the Ministry of Land, Infrastructure, Transport and Tourism.

What is the Size of the North America Market?

The digital twin market size of the North American marine sector is approximated to be USD 807 million in 2025 and it is estimated to reach USD 2.25 billion in 2035 with a 10.8% CAGR between 2026 and 2035. The U.S. digital twin investment programs include the U.S. Navy with its extensive digital twin investment programs to date, including the Naval Sea Systems Command (NAVSEA) accelerating the development of digital twin applications to ship maintenance, life cycle management, and ship performance monitoring into the surface fleet, submarine fleet, the U.S. Coast Guard vessel tracking and maritime domain awareness system, and the offshore oil and gas industry with massive investment in digital twins to support offshore platform and FPSO vessel management. The Ship-to-Shore Connector program of the U.S. Navy and the overall Digital Shipyard initiative, which is aimed at deploying the concept of digital twins in the large naval shipyards of Huntington Ingalls Industries and the Bath Iron Works of General Dynamics, is the most important nearest U.S. government investment in digital twins in the maritime sector.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region is experiencing an increasing market development due to the strategic ambition of the UAE to establish Abu Dhabi and Dubai as global marine centres with Abu Dhabi Ports Group and DP World investing in digital port infrastructure with digital twin platforms under construction in Khalifa Port and Jebel Ali Port, respectively. Saudi Arabia has a growing diet of maritime development programs with Vision 2030, expanding domestic shipping and port capacity, Qatar has an LNG shipping fleet digitization program with QatarEnergy leading the world in LNG production and export; and Brazil has an offshore oil sector digital twin investment driven by Petrobras’s extensive FPSO fleet requiring sophisticated digital performance management and predictive maintenance infrastructure.

Top Players in the Market and Their Offerings

- Kongsberg Digital AS

- Wärtsilä Corporation

- ABB Ltd.

- Siemens AG

- AVEVA Group plc (Schneider Electric)

- Dassault Systèmes SE

- Ansys Inc.

- DNV AS

- Bureau Veritas S.A.

- Rolls-Royce Holdings plc

- General Electric (Vernova)

- Others

Key Developments

The market has undergone significant developments as industry participants seek to advance digital twin platform capabilities, expand autonomous vessel development programs, and respond to growing regulatory pressure for digital emissions management.

- In October 2024: Kongsberg Digital showed the release of its new Vessel Insight 3.0 platform with a generative AI interface that allows a fleet manager to query vessel performance data using natural language prompts, and generate fuel optimization recommendations, maintenance scheduling recommendations, and carbon intensity improvement action plans without the need to have data science skills.

- In March 2025: Wartsili Corporation and DNV declared a collaborative endeavor to define an industry-wide standard of maritime digital twin data model the Maritime Digital Twin Framework (MDTF) identifying standardized information designs, interface protocols, and performance model frameworks of vessel and port digital twins that allow interoperability between digital twin offerings among different vendors and allow data exchange among vessel digital twins and port management systems.

The Digital Twin in Marine Market is segmented as follows:

By Component

- Software (Digital Twin Platforms, Simulation Software, Analytics)

- Hardware (IoT Sensors, Edge Computing Devices, Connectivity Equipment)

- Services (Consulting, Integration, Managed Services, Training)

By Application

- Fleet Management & Operations

- Predictive Maintenance

- Ship Design & Engineering

- Port & Harbor Management

- Cargo & Logistics Optimization

- Training & Simulation

- Other Applications (Environmental Compliance, Safety Management)

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

By End-User

- Commercial Shipping (Container, Tanker, Bulk Carrier, Cruise)

- Naval & Defense

- Offshore Oil & Gas

- Port Authorities & Terminal Operators

- Shipbuilders & Yards

- Other End-Users

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Digital Twin in Marine by Segments

- 2.1.2. Digital Twin in Marine by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Digital Twin in Marine Market Attractiveness Analysis, By Component

- 2.2.3. Digital Twin in Marine Market Attractiveness Analysis, By Application

- 2.2.4. Digital Twin in Marine Market Attractiveness Analysis, By Deployment Mode

- 2.2.5. Digital Twin in Marine Market Attractiveness Analysis, By End-User

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. IMO Decarbonization Mandates and Fuel Efficiency Imperatives Driving Digital Twin Adoption

- 3.1.2. Growing IoT and Connectivity Infrastructure Enabling Real-Time Vessel Digital Twins

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Digital Twin in Marine Market – By Component

- 4.1. Component Market Overview, By Component Segment

- 4.1.1. Digital Twin in Marine Market Revenue Share, By Component, 2025 & 2035

- 4.1.2. Software (Digital Twin Platforms, Simulation Software, Analytics)

- 4.1.3. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Hardware (IoT Sensors, Edge Computing Devices, Connectivity Equipment)

- 4.1.7. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Services (Consulting, Integration, Managed Services, Training)

- 4.1.11. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Component Market Overview, By Component Segment

- Chapter 5. Digital Twin in Marine Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Digital Twin in Marine Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Fleet Management & Operations

- 5.1.3. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Predictive Maintenance

- 5.1.7. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Ship Design & Engineering

- 5.1.11. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Port & Harbor Management

- 5.1.15. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Cargo & Logistics Optimization

- 5.1.19. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Training & Simulation

- 5.1.23. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1.26. Other Applications (Environmental Compliance, Safety Management)

- 5.1.27. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 5.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.29. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Digital Twin in Marine Market – By Deployment Mode

- 6.1. Deployment Mode Market Overview, By Deployment Mode Segment

- 6.1.1. Digital Twin in Marine Market Revenue Share, By Deployment Mode, 2025 & 2035

- 6.1.2. Cloud-Based

- 6.1.3. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. On-Premise

- 6.1.7. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Hybrid

- 6.1.11. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Deployment Mode Market Overview, By Deployment Mode Segment

- Chapter 7. Digital Twin in Marine Market – By End-User

- 7.1. End-User Market Overview, By End-User Segment

- 7.1.1. Digital Twin in Marine Market Revenue Share, By End-User, 2025 & 2035

- 7.1.2. Commercial Shipping (Container, Tanker, Bulk Carrier, Cruise)

- 7.1.3. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Naval & Defense

- 7.1.7. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Offshore Oil & Gas

- 7.1.11. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Port Authorities & Terminal Operators

- 7.1.15. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Shipbuilders & Yards

- 7.1.19. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Other End-Users

- 7.1.23. Digital Twin in Marine Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-User Market Overview, By End-User Segment

- Chapter 8. Digital Twin in Marine Market – Regional Analysis

- 8.1. Digital Twin in Marine Market Overview, By Region Segment

- 8.1.1. Global Digital Twin in Marine Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Digital Twin in Marine Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Digital Twin in Marine Market Revenue, By Component, 2026 – 2035

- 8.1.4. Global Digital Twin in Marine Market Revenue, By Application, 2026 – 2035

- 8.1.5. Global Digital Twin in Marine Market Revenue, By Deployment Mode, 2026 – 2035

- 8.1.6. Global Digital Twin in Marine Market Revenue, By End-User, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Digital Twin in Marine Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Digital Twin in Marine Market Revenue, By Component, 2026 – 2035

- 8.2.3. North America Digital Twin in Marine Market Revenue, By Application, 2026 – 2035

- 8.2.4. North America Digital Twin in Marine Market Revenue, By Deployment Mode, 2026 – 2035

- 8.2.5. North America Digital Twin in Marine Market Revenue, By End-User, 2026 – 2035

- 8.2.6. U.S. Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Digital Twin in Marine Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Digital Twin in Marine Market Revenue, By Component, 2026 – 2035

- 8.3.3. Europe Digital Twin in Marine Market Revenue, By Application, 2026 – 2035

- 8.3.4. Europe Digital Twin in Marine Market Revenue, By Deployment Mode, 2026 – 2035

- 8.3.5. Europe Digital Twin in Marine Market Revenue, By End-User, 2026 – 2035

- 8.3.6. Germany Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Digital Twin in Marine Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Digital Twin in Marine Market Revenue, By Component, 2026 – 2035

- 8.4.3. Asia Pacific Digital Twin in Marine Market Revenue, By Application, 2026 – 2035

- 8.4.4. Asia Pacific Digital Twin in Marine Market Revenue, By Deployment Mode, 2026 – 2035

- 8.4.5. Asia Pacific Digital Twin in Marine Market Revenue, By End-User, 2026 – 2035

- 8.4.6. China Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Digital Twin in Marine Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Digital Twin in Marine Market Revenue, By Component, 2026 – 2035

- 8.5.3. The Middle-East and Africa Digital Twin in Marine Market Revenue, By Application, 2026 – 2035

- 8.5.4. The Middle-East and Africa Digital Twin in Marine Market Revenue, By Deployment Mode, 2026 – 2035

- 8.5.5. The Middle-East and Africa Digital Twin in Marine Market Revenue, By End-User, 2026 – 2035

- 8.5.6. Saudi Arabia Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Digital Twin in Marine Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Digital Twin in Marine Market Revenue, By Component, 2026 – 2035

- 8.6.3. Latin America Digital Twin in Marine Market Revenue, By Application, 2026 – 2035

- 8.6.4. Latin America Digital Twin in Marine Market Revenue, By Deployment Mode, 2026 – 2035

- 8.6.5. Latin America Digital Twin in Marine Market Revenue, By End-User, 2026 – 2035

- 8.6.6. Brazil Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Digital Twin in Marine Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Digital Twin in Marine Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Digital Twin in Marine Market: Company Market Share, 2025

- 9.2. Global Digital Twin in Marine Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Kongsberg Digital AS

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Wärtsilä Corporation

- 10.3. ABB Ltd.

- 10.4. Siemens AG

- 10.5. AVEVA Group plc (Schneider Electric)

- 10.6. Dassault Systèmes SE

- 10.7. Ansys Inc.

- 10.8. DNV AS

- 10.9. Bureau Veritas S.A.

- 10.10. Rolls-Royce Holdings plc

- 10.11. General Electric (Vernova)

- 10.12. Others.

- 10.1. Kongsberg Digital AS

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 37

List Of Tables

Tables No 1 to 51

Prominent Player

- Kongsberg Digital AS

- Wärtsilä Corporation

- ABB Ltd.

- Siemens AG

- AVEVA Group plc (Schneider Electric)

- Dassault Systèmes SE

- Ansys Inc.

- DNV AS

- Bureau Veritas S.A.

- Rolls-Royce Holdings plc

- General Electric (Vernova)

- Others

FAQs

The key players in the market are Kongsberg Digital AS, Wärtsilä Corporation, ABB Ltd., Siemens AG, AVEVA Group plc (Schneider Electric), Dassault Systèmes SE, Ansys Inc., DNV AS, Bureau Veritas S.A., Rolls-Royce Holdings plc, General Electric (Vernova), Others.

The price of the maritime digital twin platform is very diverse as it depends on the size of deployment, scope of functionality, and client population in the market. Digital twin products at the entry-level tier of vessel performance monitoring — fuel efficiency data and simple predictive maintenance notifications on a single vessel — cost around USD 15,000- USD 50,000 per vessel annually, in which case ROI of individual vessels can be justified at comparatively low fuel savings rates. Enterprise digital twin platform licenses on fleets of 20-200+ vessels or larger (e.g. fleet-wide, fleet-level performance management, AI predictive maintenance, compliance management with CII, and optimization of the voyage) are available at USD 200,000-USD 2 million each year based on the size of the fleet and the scope of platform functionality, with enterprise-level contracts often served as multi-year contracts offering platform providers a revenue stream. Implementations of port digital twins are the most valuable category of individual contracts, and comprehensive port-wide port digital twin deployments in large container terminals cost USD 5-USD 30 million to implement and USD 500,000 – USD 3 million to support each year. Naval and defense digital twin programs Government procurement and not operating budget: Naval and European naval digital twin programs are the largest aggregate contract values in the market with U.S. Navy and European naval digital twin programs being structured as multi-year government contracts that may have USD 50 – USD 500 million in value covering platform development, fleet-wide deployment and long-term support. The type of subscription and SaaS delivery models that market leaders in commercial maritime digital twins are adopting are enhancing the availability of the market by transforming high upfront costs of capital to predictable annual operating costs, which are easier to do in the shipping companies technology budgets than the traditional models of enterprise software licenses.

According to current analysis, the market will reach about USD 13.26 billion by 2035, as the near-universal use of fleet management digital twin platforms in large commercial shipping companies becomes a cost-effective and financially necessary rather than optional task as CII regulatory pressure and EU ETS carbon costs compel digital fuel optimization to become a mainstream cost-saving activity rather than an experiment, and as a result of major commercial shipping firms, port digital twins and digital twins operational monitoring infrastructure causes port and terminal digital twins to become cost-saving activities of mainstream importance, and the IMO MASS regulatory framework solidifies, the scaling of port digital twin implementations from pioneering megaports to the global tier-two port network as demonstrated ROI drives adoption and platform costs reduce, AI-powered predictive maintenance digital twins achieving mainstream adoption across the commercial fleet as proven ROI case studies eliminate adoption hesitancy, new vessel construction specifications routinely requiring digital twin delivery as contractual deliverables that make shipyard digital twin investment a competitive necessity, and the maturation of cross-platform digital twin interoperability standards enabling ecosystem-level data sharing that multiplies the value of individual platform investments, at a CAGR of 11.7% from 2026 to 2035.

It is projected that Europe will continue to generate the largest share of revenue through the early forecast period, with around 36 percent of the global market share dominating in 2025 as per the density of the world’s leading maritime digital twin technology corporations, consisting of Kongsberg Digital, Wartsila, ABB Marine and DNV concentrating on the area, the most restrictive regulatory environment in the world to realize decarbonization through EU ETS and Fit for 55 and the greatest urgency of digital adoption among the European fleet operators, the most advanced commercial port digital twins in the It is estimated that Asia Pacific will be close to the European market size by 2031 based on the better CAGR growth curve supported by shipbuilding volume and fleet growth.

Asia Pacific will experience the highest CAGR of 14.8% in the forecast period, with South Korea, China, and Japan all contributing more than 90% of the world’s shipbuilding output, which makes the region the most prominent location of a fresh vessel digital twin capability incorporation. Hyundai Heavy Industries, Samsung Heavy Industries, and DSME, the significant investments of the various digital twin platforms by China, COSCO Shipping, and China Merchants Energy Shipping, and smart port programs in Singapore and Shanghai establish the area as a leader in incorporating digital twins into fleet management alongside established European benchmarks.

The Global Digital Twin in Marine Market is forecasted to grow substantially over the next five years due to the IMO 2023 revised GHG Strategy with its net-zero or near-net-zero shipping emissions target by 2050 and the introduction of the Carbon Intensity Indicator regulation effective January 2023 with a mandatory annual improvement in carbon intensity of 515 per cent of vessels offering annual savings of USD 500,000- USD 3 million delivering savings at the margin of annual savings of USD 500,00–USD 3 million per vessel justifying platform investment, the EU ETS extension to shipping from January 2024 adding direct carbon costs of EUR 60–EUR 80 per tonne CO₂ making digital fuel efficiency investment directly cost-recoverable, the International Association of Ports and Harbors reporting over 60% of major world ports had deployed or were planning digital twin implementations in 2024, Starlink Maritime achieving up to 350 Mbps vessel connectivity enabling real-time digital twin synchronization previously impossible under legacy VSAT bandwidth constraints, and classification society digital twin certification programs from DNV and Bureau Veritas enabling regulatory credit for digital twin-informed maintenance interval extension.