Group IV and V Lubricants Market Size, Trends and Insights By Product Type (Polyalphaolefins (PAO) — Group IV, Low Viscosity PAO (PAO 2, PAO 4, PAO 6), Medium Viscosity PAO (PAO 8, PAO 10), High Viscosity PAO (PAO 40, PAO 100, mPAO), Polyalkylene Glycols (PAG) — Group V, Water-Soluble PAG, Oil-Soluble PAG, Polyol Esters — Group V, Diesters — Group V, Phosphate Esters — Group V, Alkylated Naphthalenes — Group V, Silicone Fluids — Group V, Others), By Application (Engine Oils, Heat Transfer Fluids (HTF), Transmission Fluids, Metalworking Fluids, Hydraulic Fluids, Compressor & Refrigeration Oils, Gear Oils & Greases, Others), By End-Use Industry (Automotive & Transportation, Passenger Vehicles, Commercial Vehicles, Electric & Hybrid Vehicles, Industrial Machinery & Manufacturing, Aerospace & Defense, Marine, Power Generation (Wind, Thermal, Gas Turbine), Others), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 3.49%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Europe |

Major Players

- ExxonMobil Corporation

- Royal Dutch Shell plc

- BP plc (Castrol)

- Chevron Corporation

- Others

Reports Description

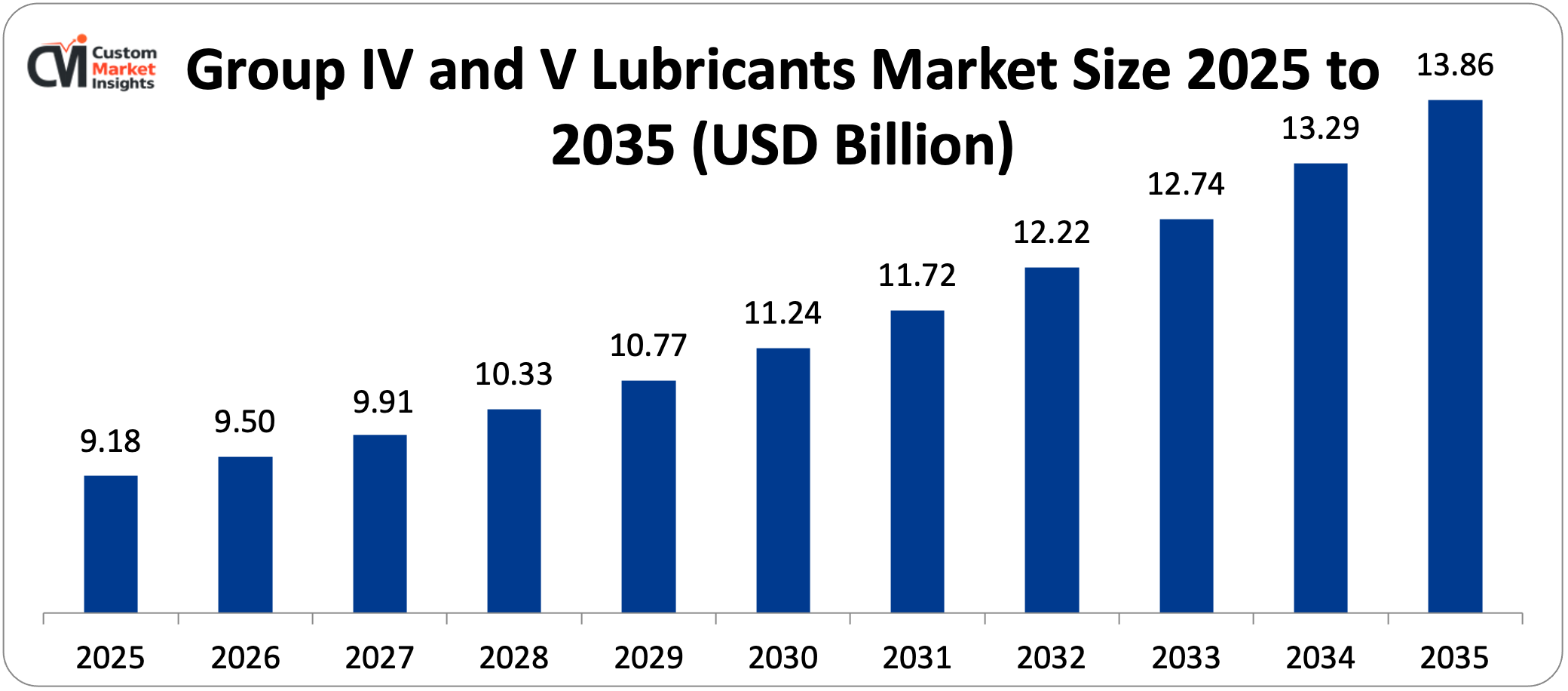

The global Group IV and V Lubricants market is estimated to have USD 9.18 billion in 2025 and USD 12.61 billion in 2033 with a CAGR of 3.49% in the forecast period. Taking the market projection out to 2035, this study estimates that the market would grow at an average of 4.3% between the years 2026 and 2035, to an approximate USD 13.86 billion as compared to USD 9.50 billion in 2026.

The escalating need to use high-performance synthetic lubricants in the automotive, industrial, aerospace and power generation markets, the increasing strictness of emission control and fuel efficiency regulations that force the use of advanced lubricant chemistries, the rapid electrification of vehicle fleets that results in niche thermal management fluid demands and the increased utilization of extended drain lubricants in industrial machines, among others all represent market growth drivers.

Market Highlight

- Europe will be the biggest market of Group IV and V lubricants based on its regulation support and the growing demand of high end usage, but Asia Pacific will be the most growing market as a result of growing domestic demand of the industrial and automobile industries.

- The share of revenue owned by North America was expected to be very high in 2025, the basis of which was sound aerospace, automotive, and industrial end-use demand and the existence of major lubricant producers.

- Polyalphaolefin (PAO) is the most popular base oil by product type, commanding a significant market share of synthetic lubricants of high grade with a good balance between performance and compatibility in a wide selection of formulations.

- In 2024, automotive lubricants correlated with a share of 65.3% domination in the polyalphaolefin segment because automotive engine and drivetrain applications were predominant in the consumption of the total Group IV lubricant.

- Low Viscosity PAO also dominated the market with a 48.6% share of product grade segments in 2024 due to high usage in synthetic engine oils, transmission fluids, and greases that require thermal stability and long drain intervals.

- The global EV lubricants market is projected to be USD 1.9 billion in 2025 and is estimated to reach USD 6.7 billion by 2032 with a CAGR of 19.7%, which is a high-growth adjacent market opportunity for the Group IV and V lubricant chemistries in battery thermal management and drive fluid applications.

Significant Growth Factors

The Group IV and V Lubricants Market Trends present significant growth opportunities due to several factors:

- Stringent Emission Regulations and Fuel Efficiency Standards Accelerating Synthetic Lubricant Adoption: The most significant systemic force behind Group IV and V lubricant demand is considered to be the progressive tightening of vehicle emission standards and machine fuel efficiency mandates in large markets. The market expansion is mainly due to the increased need for high-performance lubricants in the following industries cars, industrial, aerospace, marine and power generation. The increased use of electric and hybrid cars will result in a rise in the demand for Group IV and V lubricants because they have better properties such as low volatility, high viscosity index, and the best thermal and oxidation stability. The Euro 7 regulations by the European Union on emissions, the greenhouse gas regulations of light and heavy-duty vehicles by the U.S. EPA and the Chinese standards of the same are associated with engine designs that demand lubricants that can withstand higher working temperatures, longer drain periods and the ever-increasing specifications of low-viscosity levels. Group IV PAO engine oils have continuously out-performed Group III mineral-based synthetics in all-important performance parameters such as oxidation stability, volatility control and retention of viscosity – parameters that are directly related to emissions compliance and fuel economy. Group IV base oils are commonly employed in power turbines, air compressor, aircraft engines, and industrial drive systems, as they have a consistent molecular structure that combines with a low volatility enabling PAO to remain in service and be low in viscosity and results in less usage and low deposits as the equations vary across only between -60°C and above 150°C. Energy efficiency programs that are not only mandated by regulatory demands but also by corporate sustainability promises are hastening the adoption of traditional mineral oils by Group IV and V synthetic lubricants that have demonstrated quantifiable improvements in friction losses, operating temperatures and energy usage. Research continually indicates that PAO based industrial lubricants cut gear and bearing friction losses by 2-5% over mineral oil counterparts and offer substantial energy savings to manufacturing processes over large scale production operations.

- Electric Vehicle Proliferation Creating Specialized Group V Lubricant Demand: The global switch to battery electric and hybrid vehicles is changing the lubricant faculties case tally fast with varying oil volumes of conventional engine oils and creating completely new demand categories in the Group V specialty in thermal management, e-drive lubrication, and immersion cooling applications. Glycol-based oils, including Polyalkylene Glycol (PAG), and aqueous blends of glycol are dominant at that point with a leading market share of about 38% in the EV lubricants market in 2025 due to the exceptional thermal characteristics and broad use in battery thermal management systems. Polyalphaolefin (PAO) base stocks have the second-largest market share, which is the conventional synthetic hydrocarbon base of conventional transmission fluids and motor cooling where lubrication characteristics are needed along with thermal management. Polyol Esters (POE) are also preferred in high-temperature applications and state-of-the-art immersion cooling systems because their oxidation stability can be very high and service life is often long. The accelerated development of the global EV market, such as battery thermal management, electric motor and transmission, and advanced dielectric fluids mass-market, offers very promising demand platforms due to the significant development of the global EV market whose market share has hit more than 17 million EVs sold worldwide in 2024 and is projected to reach more than 40 million units of EVs per year by 2030. PAO lubricants are valued due to their high-quality performance properties as compared to mineral oils, where their high viscosity index, high oxidation resistance, and low pour point ensure that they are of great use in a large variety of equipment, including high-performance engines as well as challenging industrial machines. New innovations are aimed at improving those qualities even more, using biodegradable alternatives, and adding some specific additives to meet a particular customer demand. EV fluids, which are also required to lubricate the planetary gear systems at much higher speeds than traditional transmissions, must also be electrically compatible to avoid corrosion of copper motor windings and electronic components and have thermal performance to ensure optimal battery and motor temperatures, performance needs that cannot be achieved by mineral-based oils and create differentiated demand on precisely engineered Group V synthetic fluid formulations.

What are the Major Advances Changing the Group IV and V Lubricants Market Today?

- Bio-Based and Biodegradable Group V Ester Lubricants: The imperatives of environmental sustainability are changing the development of the Group V lubricants, with much technology in this direction toward bio-derived ester base oils whose performance appears to match that of petroleum-derived equivalents but which have a far less adverse impact on the environment. Oils based on esters can be up to 80% biodegradable, which is a high level of availability to satisfy the strict European environmental requirements, and thus are favored in renewable energy projects, electric vehicles, and high-performance applications where high performance and ecological safety are obligatory. The Group IV and V base oils are highly chemically stable and they do not form any harmful sludge and reduce the risk of pollution. Polyol esters of natural fatty acids such as trimethylolpropane oleate and pentaethyl esters of vegetable oils have excellent low temperature performance, a high viscosity index and excellent sealability with a biodegradation of 60-90 in traditional OECD tests. In the marine industry, which is heavily restricted by International Maritime Organization (IMO) policies against the use of non-biodegradable lubricants in ecologically sensitive zones, is one of the main commercial uses of biodegradable Group V esters in stern tube lubricants, controllable pitch propeller systems, and wire rope lubricants. Offshore wind energy industry, of which the global installed capacity is estimated to top 400 GW by 2033, presents the high demand of highly biodegradable ester-based gear oils for wind turbine gears working in the marine condition where direct leakage of lubricants poses a direct threat to the sensitive marine ecosystems. This accelerated development of ester-based bio-lubricants brings a competitive factor to the market share of PAO, in environmentally sensitive use, a recent lifecycle analysis of some plant-derived esters has demonstrated equal performance at the 15-20% lower carbon footprint.

- Digital Tribology, Predictive Maintenance, and Smart Lubrication Systems: The convergence of sensor technology, data analytics and industrial IoT systems with lubrication management changes the system of the Group IV and V lubricant specification, monitoring, and replacement in industrial systems. The increased use of automated and electrified machine working in industries is creating a demand for more lubricants that have a longer drain time and better resistant properties of equipment, and the trend is highlighted by the increased emphasis on energy-saving and emission regulation measures. Predictive lubrication management systems Predictive lubrication management systems (in which real-time measurements of oil conditions (viscosity, oxidation products, metal wear particles, and water contamination) are paired with machine learning algorithms that predict remaining useful lubricant life) are also allowing condition-based oil change schedules, replacing fixed maintenance intervals. Group IV and V synthetic lubricants also use these systems especially well, as their higher prices can be warranted much easier with the improved drain interval and proven machine protection advantages. Research in heavy manufacturing facilities has also established that condition-based maintenance with Group IV synthetic lubricants saves total lubrication cost by 25-40% over traditional mineral oil programs that run on constant drain intervals, as well as enhancing equipment availability and minimizing waste oil production. Group IV and V improvement in lubricants is going further with the development of smart lubricants with nanoscale additives (such as graphene, molybdenum disulfide, functionalized nanodiamonds, and more) with nano-enhanced PAO formulations showing a 20-35% reduction in friction coefficient in lubrication regimes at boundaries relative to unadditized ones.

- Aerospace and Defense Applications Driving Premium Group V Demand: Aerospace and Defense Applications Driving Group V Premium Group V lubricants are used in the aerospace industry to demonstrate the most valuable application area of the lubricants, with high-value products being the aviation turbine oils, aircraft engine oils and hydraulic fluids as they are used in high-quality demanding applications that demand a high level of performance. The group IV and V lubricants find application in aircraft engines and gas turbines and starters and gears of pumps and starters among others. They are very important in other functions such as lubrication, anti-corrosion protection, cooling, reduction of noise, and propeller systems. As it is anticipated, the demand for Group IV and V lubricants would rise as global activities of aircraft production are in a greater rise. It is estimated that 40,000 new-generation aircraft will be delivered annually to the world over the next 20 years in the delivery of visionary commercial aircraft and each of these new generation aircraft includes more challenging engine and hydraulic requirements, necessitating the use of Group V ester-based aviation lubricants to meet de facto MIL-PRF-23699 and other comparable civil specifications. Next-generation turbofan engines, such as the CFM LEAP and Pratt and Whitney PW1000G geared turbofan family, are Running at higher bypass and combustor temperatures than the previous generation, meaning that they put additional extreme thermal stress on the turbine oil system that further benefits thermally superior Group V ester formulations, as opposed to low-performance alternatives. The military aircraft and rotorcraft are other high value demand mediums and the defense procurement programs of North America, Europe and the Asia Pacific have specified high value Group V synthetic lubricants due to their high operational temperatures of extreme cold arctic cold start down to high temperatures in desert operations.

Category Wise Insights

By Product Type

Why Do Polyalphaolefins (PAO) Dominate the Group IV and V Lubricants Market?

Polyalphaolefin (PAO) dominates the base oil segment where it is used in high grade synthetic lubricants giving a good balance between performance and compatibility in different formulations. PAO has the advantage of being thermally stable and resistant to oxidation, which is why it is the material of choice in harsh environments, spanning automobiles to aerospace. The market leadership of PAO is a compelling attribute of a distinctive set of properties brought about by the choice of molecular structure precisely engineered: the lack of branched chain structures and impurities present in mineral-derived base oils provide excellent oxidative stability, a viscosity index of typically over 120 to 140 (compared to 90 to 110 for the corresponding Group II mineral oils), a low pour point By the year 2034, the global polyalphaolefin market is projected to have a value of approximately USD 3.3 billion as compared to USD 2.4 billion in 2024 which is projected to increase at a rate of 3.1% between the years 2025 and 2034, with automotive lubricants consuming 65.3% of PAO end-use in 2024.

By Application

Why Do Engine Oils Lead the Application Segment?

The biggest market segment of Group IV and V lubricants is the engine oils which comprise almost 42% of the total market revenue in 2025. The market share of the engine oils segment is likely to be the highest given that it is commonly used to lubricate the internal combustion engines and the automotive segment will have the highest market share given the growth in demand in the recent years especially in the developing countries. The 1.5 billion passenger and commercial vehicles in the global installed base need routine engine oil fill-up and change programs with the premium synthetic lubricant market segment such as the full synthetic engine oils based on Group IV PAO as a component capturing growing market share as buyers appreciate the performance, protection and extended drain interval benefits of synthetic formulations.

By End-Use Industry

Why Does the Automotive Sector Lead Group IV and V Lubricant Consumption?

The domination of the automotive end-use industry in total Group IV and V lubricant market revenue, which is estimated at 45% in 2025, is attributed to the sheer magnitude of world vehicle production and operation and the push in automotive lubricant system performance expectations and requirements. Group IV and V lubricants are pure polyalphaolefin and polyalkylene glycol polyol base oils, among other oils that are mainly used in the automotive engine in order to provide easy performance and smooth operations. There will be an upsurge in the manufacture of automobiles hence the market of Group IV and V lubricants will rise. The automotive lubricant market is structurally bifurcating worldwide: the volume of conventional ICE vehicle lubricants is slow-growing in the developing markets, and extending drain intervals are exerting pressure on conventional lubricants in developed markets- the booming EV and hybrid vehicle fleet is introducing quite novel demand segments to Group IV and V specialty lubricants with no natural mineral oil counterparts.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 9.50 billion |

| Projected Market Size in 2035 | USD 13.86 billion |

| Market Size in 2025 | USD 9.18 billion |

| CAGR Growth Rate | 3.49% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Product Type, Application, End-Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

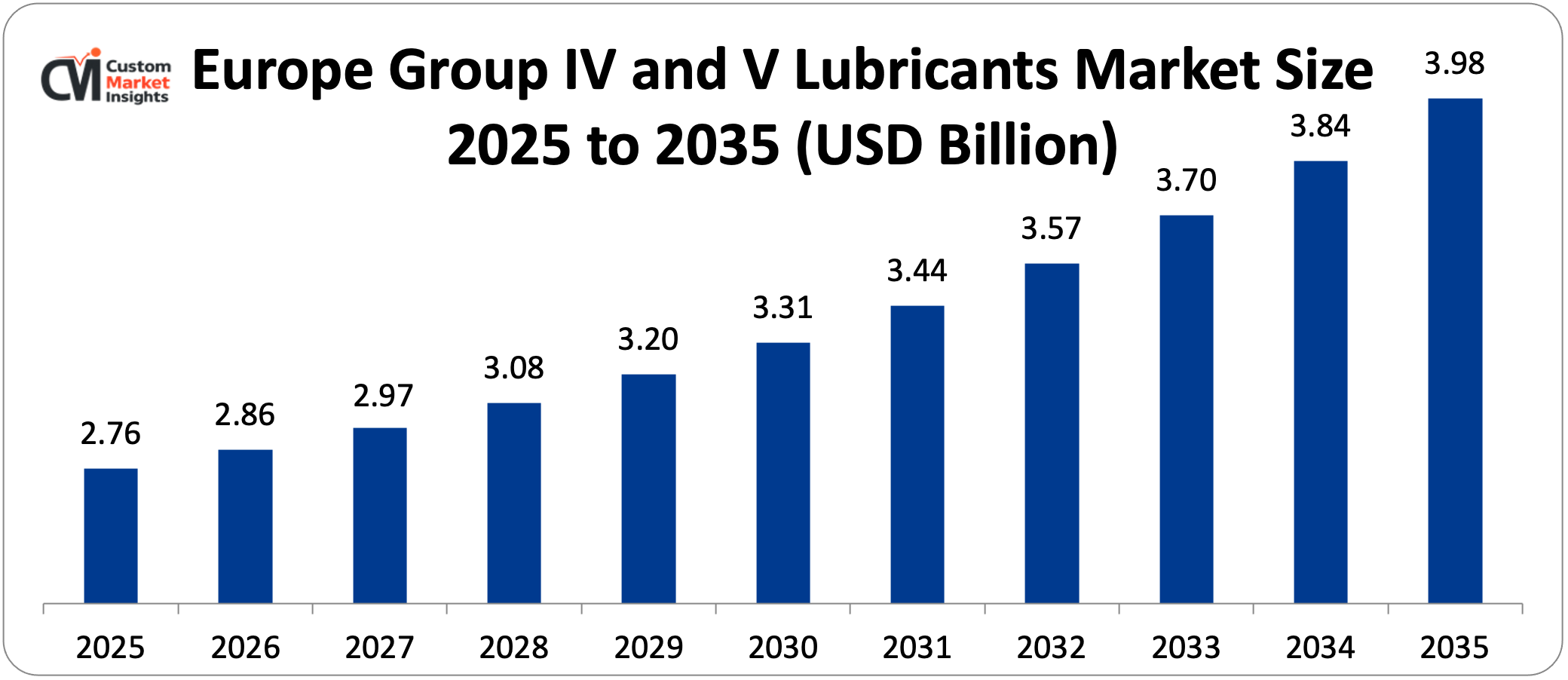

How Big is the Europe Group IV and V Lubricants Market?

The biggest Group IV and V lubricant market is Europe due to the regulatory support and the rising demand in the high-end use of lubricants. The market size of the European Group IV and V lubricants is estimated at USD 2.76 billion in 2025 and is expected to increase to USD 3.98 billion in 2035 at a CAGR of 3.7 between 2026 and 2035.

Why does Europe Lead the Group IV and V Lubricants Market in 2025?

The domination of the European market is a symptom of the well developed regulatory framework in the region that has required the use of high-performance synthetic lubricants, a highly developed automotive and industrial manufacturing platform with high lubrication demand, the high consumer awareness on the benefits of synthetic lubricants and the availability of leading lubricant manufacturers and additive firms. Groups IV and V are only considered synthetics in Europe, but Groups III, IV and V are called synthetic lubricants in North America, Europe being more demanding of what constitutes a synthetic that sustains high-end positioning of PAO-based and ester-based products.

European OEM specifications of automotive lubricants – especially the premium vehicles of Germany – are the most challenging requirements in the world with ultra-low viscosity grades (0W-20, 0W-16) and very long drain intervals effectively forcing the use of Group IV PAO based base oils in order to obtain consistent compliance. A large continuing demand is in Group IV and V synthetic gear oils used in wind turbine gearboxes due to the present strength of the European wind energy sector in the European market, which is the second largest wind power market in the world with more than 260 GW installed and needs a 5-year drain interval and low-temperature pumpability (only available with PAO and synthetic ester formulations) in offshore wind farm applications.

Why does North America Maintain a Strong Position in the Group IV and V Lubricants Market?

The solid market presence of North America is based on the wide automotive vehicle fleet owned by the United States, the leading aerospace and defense manufacturer that drives the need for high-end Group V aviation lubricants, a highly advanced industrial manufacturing industry, and the existence of ExxonMobil, the largest PAO producer in the world with the largest PAO production facility at Bayway, New Jersey. The Group IV V Lubricant Market has the highest market share in North America which is the most innovative in matters of products and the United States has some of its most significant players in the industry that are investing in research and development to improve drug formulations and increase therapeutic uses. The SpectraSyn and SpectraSyn Elite product lines are used globally as reference group PAO base oils by fine automotive, industrial, and specialty lubricant formulators of North America and the international market.

Why is Asia Pacific Experiencing the Fastest Growth?

The Asia Pacific market is projected as the fastest expanding market of group IV and V lubricants because domestic consumption has risen in both the industrial and the automotive markets. With its huge, rapidly growing automotive fleet switching to increasingly high-end synthetic lubricants, India with its accelerating industrialization and expanding motor vehicle output, Japan and South Korea with their developed automotive and electronics manufacturing industries offering demanding lubricant-usage situations, and the region with its rapidly developing renewable energy infrastructure providing wind turbine lubricants demand the Asia Pacific market is expected to experience a CAGR of 5.6% in 2 In the Group IV and V Lubricants Market in 2021, the biggest portion of the industry belonged to the Asia pacific with consumption rates up to 28%, the highest consumption recorded due to the growing demands by the automotive and aerospace industries. China, South Korea, Japan, and India alone manufacture tens of millions of vehicles every year, which also reflects a lot on Group IV and V lubricant demand within the region.

Why is LAMEA Showing Accelerating Adoption?

Demand for Group IV and V lubricants is growing progressively but at a slow rate in the LAMEA region due to the growth of infrastructure and industrialization in Middle East Gulf Cooperation Council countries, growth in manufacturing sectors in Brazil and South Africa, and the rapid use of high-performance lubricants in the rising automotive aftermarket. By 2034, the market is expected to be growing in its valuations as industrial growth and the demand for high-performance lubricants rise in the Middle Eastern and African markets due to the faster pace of infrastructure development and growth in the region. The economic diversification programs underway in Saudi Arabia and the UAE include the massive allocation of funds into downstream petrochemical and lubricant blending capacity, as both countries are in the process of becoming self-sufficient in domestically produced Group IV and V lubricant blending and distribution.

Top Players in the Group IV and V Lubricants Market and Their Offerings

- ExxonMobil Corporation

- Royal Dutch Shell plc

- BP plc (Castrol)

- Chevron Corporation

- TotalEnergies SE

- FUCHS Petrolub SE

- Idemitsu Kosan Co. Ltd.

- PETRONAS Lubricants International

- Valvoline Inc.

- ConocoPhillips

- Sinopec Group

- PetroChina Company Limited

- Millers Oils

- Houghton International

- Others

Key Developments

The Group IV and V lubricants market has undergone significant developments over the past couple of years as industry participants seek to expand capabilities and enhance product portfolios.

- By the beginning of 2025, a top synthetic lubricants manufacturer launched a commercially available full synthetic 0W-16 engine oil product designed especially for hybrid powertrains that require oils capable of meeting both combustion and electric engine cooling demands, with the product being based on advanced PAO and Group V ester blends designed for compliance with BMW Longlife-21 and Mercedes-Benz MB 229.71 OEM specifications.

- In January 2022, a major lubricant supplier acquired a lube blending plant, which is indicative of the company’s efforts to strengthen its Group IV and V blending operations in the synthetic lubricants segment, another illustration of the prevailing market consolidation tendency whereby market leaders are investing in production assets to address growing synthetic lubricants demand in automotive and industrial applications.

These strategic activities have allowed companies to strengthen market positions, expand product portfolios targeting EV and industrial applications, enhance production capabilities, and capitalize on growth opportunities within the evolving Group IV and V lubricants market.

The Group IV and V Lubricants Market is segmented as follows:

By Product Type

- Polyalphaolefins (PAO) — Group IV

- Low Viscosity PAO (PAO 2, PAO 4, PAO 6)

- Medium Viscosity PAO (PAO 8, PAO 10)

- High Viscosity PAO (PAO 40, PAO 100, mPAO)

- Polyalkylene Glycols (PAG) — Group V

- Water-Soluble PAG

- Oil-Soluble PAG

- Polyol Esters — Group V

- Diesters — Group V

- Phosphate Esters — Group V

- Alkylated Naphthalenes — Group V

- Silicone Fluids — Group V

- Others

By Application

- Engine Oils

- Heat Transfer Fluids (HTF)

- Transmission Fluids

- Metalworking Fluids

- Hydraulic Fluids

- Compressor & Refrigeration Oils

- Gear Oils & Greases

- Others

By End-Use Industry

- Automotive & Transportation

- Passenger Vehicles

- Commercial Vehicles

- Electric & Hybrid Vehicles

- Industrial Machinery & Manufacturing

- Aerospace & Defense

- Marine

- Power Generation (Wind, Thermal, Gas Turbine)

- Others

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Group IV and V Lubricants by Segments

- 2.1.2. Group IV and V Lubricants by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Group IV and V Lubricants Market Attractiveness Analysis, By Product Type

- 2.2.3. Group IV and V Lubricants Market Attractiveness Analysis, By Application

- 2.2.4. Group IV and V Lubricants Market Attractiveness Analysis, By End-Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Stringent Emission Regulations and Fuel Efficiency Standards Accelerating Synthetic Lubricant Adoption

- 3.1.2. Electric Vehicle Proliferation Creating Specialized Group V Lubricant Demand

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Group IV and V Lubricants Market – By Product Type

- 4.1. Product Type Market Overview, By Product Type Segment

- 4.1.1. Group IV and V Lubricants Market Revenue Share, By Product Type, 2025 & 2035

- 4.1.2. Polyalphaolefins (PAO) — Group IV

- 4.1.2.1. Low Viscosity PAO (PAO 2, PAO 4, PAO 6)

- 4.1.2.2. Medium Viscosity PAO (PAO 8, PAO 10)

- 4.1.2.3. High Viscosity PAO (PAO 40, PAO 100, mPAO)

- 4.1.3. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Polyalkylene Glycols (PAG) — Group V

- 4.1.6.1. Water-Soluble PAG

- 4.1.6.2. Oil-Soluble PAG

- 4.1.7. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Polyol Esters — Group V

- 4.1.11. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Diesters — Group V

- 4.1.15. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Phosphate Esters — Group V

- 4.1.19. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Alkylated Naphthalenes — Group V

- 4.1.23. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1.26. Silicone Fluids — Group V

- 4.1.27. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 4.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.29. Key Market Trends, Growth Factors, & Opportunities

- 4.1.30. Others

- 4.1.31. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 4.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.33. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Product Type Market Overview, By Product Type Segment

- Chapter 5. Group IV and V Lubricants Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Group IV and V Lubricants Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Engine Oils

- 5.1.3. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Heat Transfer Fluids (HTF)

- 5.1.7. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Transmission Fluids

- 5.1.11. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Metalworking Fluids

- 5.1.15. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Hydraulic Fluids

- 5.1.19. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Compressor & Refrigeration Oils

- 5.1.23. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1.26. Gear Oils & Greases

- 5.1.27. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 5.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.29. Key Market Trends, Growth Factors, & Opportunities

- 5.1.30. Others

- 5.1.31. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 5.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.33. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Group IV and V Lubricants Market – By End-Use Industry

- 6.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 6.1.1. Group IV and V Lubricants Market Revenue Share, By End-Use Industry, 2025 & 2035

- 6.1.2. Automotive & Transportation

- 6.1.2.1. Passenger Vehicles

- 6.1.2.2. Commercial Vehicles

- 6.1.2.3. Electric & Hybrid Vehicles

- 6.1.3. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Industrial Machinery & Manufacturing

- 6.1.7. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Aerospace & Defense

- 6.1.11. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Marine

- 6.1.15. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Power Generation (Wind, Thermal, Gas Turbine)

- 6.1.19. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Others

- 6.1.23. Group IV and V Lubricants Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 7. Group IV and V Lubricants Market – Regional Analysis

- 7.1. Group IV and V Lubricants Market Overview, By Region Segment

- 7.1.1. Global Group IV and V Lubricants Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Group IV and V Lubricants Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Group IV and V Lubricants Market Revenue, By Product Type, 2026 – 2035

- 7.1.4. Global Group IV and V Lubricants Market Revenue, By Application, 2026 – 2035

- 7.1.5. Global Group IV and V Lubricants Market Revenue, By End-Use Industry, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Group IV and V Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Group IV and V Lubricants Market Revenue, By Product Type, 2026 – 2035

- 7.2.3. North America Group IV and V Lubricants Market Revenue, By Application, 2026 – 2035

- 7.2.4. North America Group IV and V Lubricants Market Revenue, By End-Use Industry, 2026 – 2035

- 7.2.5. U.S. Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Group IV and V Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Group IV and V Lubricants Market Revenue, By Product Type, 2026 – 2035

- 7.3.3. Europe Group IV and V Lubricants Market Revenue, By Application, 2026 – 2035

- 7.3.4. Europe Group IV and V Lubricants Market Revenue, By End-Use Industry, 2026 – 2035

- 7.3.5. Germany Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Group IV and V Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Group IV and V Lubricants Market Revenue, By Product Type, 2026 – 2035

- 7.4.3. Asia Pacific Group IV and V Lubricants Market Revenue, By Application, 2026 – 2035

- 7.4.4. Asia Pacific Group IV and V Lubricants Market Revenue, By End-Use Industry, 2026 – 2035

- 7.4.5. China Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Group IV and V Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Group IV and V Lubricants Market Revenue, By Product Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Group IV and V Lubricants Market Revenue, By Application, 2026 – 2035

- 7.5.4. The Middle-East and Africa Group IV and V Lubricants Market Revenue, By End-Use Industry, 2026 – 2035

- 7.5.5. Saudi Arabia Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Group IV and V Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Group IV and V Lubricants Market Revenue, By Product Type, 2026 – 2035

- 7.6.3. Latin America Group IV and V Lubricants Market Revenue, By Application, 2026 – 2035

- 7.6.4. Latin America Group IV and V Lubricants Market Revenue, By End-Use Industry, 2026 – 2035

- 7.6.5. Brazil Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Group IV and V Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Group IV and V Lubricants Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Group IV and V Lubricants Market: Company Market Share, 2025

- 8.2. Global Group IV and V Lubricants Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. ExxonMobil Corporation

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Royal Dutch Shell plc

- 9.3. BP plc (Castrol)

- 9.4. Chevron Corporation

- 9.5. TotalEnergies SE

- 9.6. FUCHS Petrolub SE

- 9.7. Idemitsu Kosan Co. Ltd.

- 9.8. PETRONAS Lubricants International

- 9.9. Valvoline Inc.

- 9.10. ConocoPhillips

- 9.11. Sinopec Group

- 9.12. PetroChina Company Limited

- 9.13. Millers Oils

- 9.14. Houghton International

- 9.15. Others.

- 9.1. ExxonMobil Corporation

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Healthcare Foresights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

- Chapter 12. List Of Figures

- 12.1. Figures No 1 to 46

- Chapter 13. List Of Tables

- 13.1. Tables No 1 to 46

Prominent Player

- ExxonMobil Corporation

- Royal Dutch Shell plc

- BP plc (Castrol)

- Chevron Corporation

- TotalEnergies SE

- FUCHS Petrolub SE

- Idemitsu Kosan Co. Ltd.

- PETRONAS Lubricants International

- Valvoline Inc.

- ConocoPhillips

- Sinopec Group

- PetroChina Company Limited

- Millers Oils

- Houghton International

- Others

FAQs

The key players in the market are ExxonMobil Corporation, Royal Dutch Shell plc, BP plc (Castrol), Chevron Corporation, TotalEnergies SE, FUCHS Petrolub SE, Idemitsu Kosan Co. Ltd., PETRONAS Lubricants International, Valvoline Inc., ConocoPhillips, Sinopec Group, PetroChina Company Limited, Millers Oils, Houghton International, Others.

One of the strongest forces in the Group IV and V lubricants market in respect of various dimensions is the environmental regulations. The REACH regulation of Europe imposes a costly and lengthy process of safety assessment and registration of lubricant additives and base oils, creating higher costs of compliance and market entry barriers. The low-viscosity engine oils being prescribed by the emission standards of the U.S., European Union, China, and India are providing a verifiable fuel economy benefit, an aspect that would prefer formulations based on Group IV PAO rather than a mineral formulation. The use of Group V biodegradable ester lubricants is being facilitated by the use of marine environments such as marine environmental zones that have mandated use of biodegradable lubricants such as the biodegradable ester lubricants. Group IV and V base oils are highly stable in chemical properties and do not form harmful sludge and reduce the risk of pollution, with some lubricant base oils being over 80% biodegradable to a high level according to the strict European environmental regulations, and this puts the group IV and V-based oils in a good position since the intensity of certain environmental regulations continues to rise in world markets.

The market is exposed to volatile costs of raw materials used in alpha-olefins production as PAO feedstocks, high production costs, compliance costs, compared to Group II and Group III mineral oils, disruptions in the supply chains of specialty chemical feedstocks and competition by Group III base oils and bio-based substitutes in the cost-sensitive applications. Other limitations are that the structure of ICE vehicle lubricant volumes will decrease over the long term due to EV adoption replacing the traditional engine oil demand, high prices limiting demand in the cost-established developing market segments, the complexity of reformulating lubricant systems with OEM specifications continually changing to new lower viscosity grades and performance specifications that do not work with older approved lubricating formulations.

Group IV and V global lubricants market is expected to vary between USD 13.86 billion in 2035 rising up to USD 9.50 billion in 2026 with a CAGR of 4.3. The positive growth expectations will be supported by the gradual increase in regulatory enforcement of automotive emission and fuel economy standards, the swift increase in EV fleets that will create a new market in Group V specialty fluids, the expansion of renewable energy infrastructure that needs advanced synthetic lubricants and the standardization of industrial lubrication practices away from mineral lubricants to Group IV and V synthetic formulations.

Group IV and V lubricants find the greatest market in Europe due to the supportive regulatory environment and the rising trend of high-value end applications, and the region continues to hold its premium status due to the challenges facing the world automotive OEM lubricant quality requirements, high emission and environmental standards that favor synthetic lubricants, and sophisticated industrial making industries that demand high-quality lubricants. North America is also enjoying a healthy market position that is anchored by the leading aerospace market in the world and the massive and growing synthetic-driven automotive lubricant market as well as the presence of ExxonMobil as the largest global producer of PAO.

The regional CAGR of the Asia Pacific is expected to be the most rapid at 5.6% during the forecast period, as China is set to move towards National VI emission standards, which will force the use of low-viscosity synthetic lubricants in vehicles, the largest production of EVs in the world will demand the use of Group V specialty fluids, the region is rapidly investing in industrial automation, India is rapidly growing in automotive and industrial growth, and expanding adoption of premium synthetic lubricants in automotive aftermarket channels across Southeast Asia as consumer awareness and income levels rise.

7 . What are the key driving factors influencing the growth of the Group IV and V lubricants market?

The Group IV and V Lubricants Market Industry is recording a high demand for high-performance lubricants that have the capability of working in extreme conditions and provide a high level of protection. This is because there is a demand in many sectors such as automotive, industrial, and marine. The production of Group IV and V lubricants with technological advancements has enabled a higher stability of the viscosity index and a high thermal and oxidative stability as well as the lubricating property. The oils play a very vital role in maximizing the efficiency of the engines, the life of the equipment and lowering the costs of maintenance. Other forces are the stiffening of emission laws requiring low-viscosity synthetic lubricants, the rapid spread of EVs to form new Group V specialty fluids, the rising renewable energy infrastructure, which necessitates top quality synthetic gear and bearing lubricants, and the increasing awareness of synthetic lubricant performance and cost-of-ownership advantages by consumers.