Hydrogen Fuel Cell Vehicle Market Size, Trends and Insights By Vehicle Type (Passenger Cars (Sedan, SUV), Light Commercial Vehicles (Vans, Pickup Trucks), Heavy-Duty Trucks (Class 7–8, Semi-Trailers), Buses (Transit Buses, Intercity Coaches, School Buses), Other Vehicle Types (Forklifts, Trains, Marine Vessels)), By Technology (Proton Exchange Membrane Fuel Cells (PEMFC), Solid Oxide Fuel Cells (SOFC), Alkaline Fuel Cells (AFC), Other Technologies (Phosphoric Acid, Molten Carbonate)), By Application (Public Transportation (City Buses, Intercity Routes), Private Transportation (Personal Passenger Cars, Light Commercial), Commercial Freight & Logistics (Long-Haul Trucking, Last-Mile Delivery), Material Handling (Forklifts, Port Equipment), Other Applications (Rail, Maritime, Airport Ground Support)), By End-User (Individual Consumers, Fleet Operators (Logistics, Delivery, Rental), Public Transit Authorities, Government & Defense, Other End-Users (Mining, Industrial)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 18.7%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Europe |

| Largest Market: | Asia Pacific |

Major Players

- Toyota Motor Corporation

- Hyundai Motor Company

- Honda Motor Co. Ltd.

- Daimler Truck AG

- Others

Reports Description

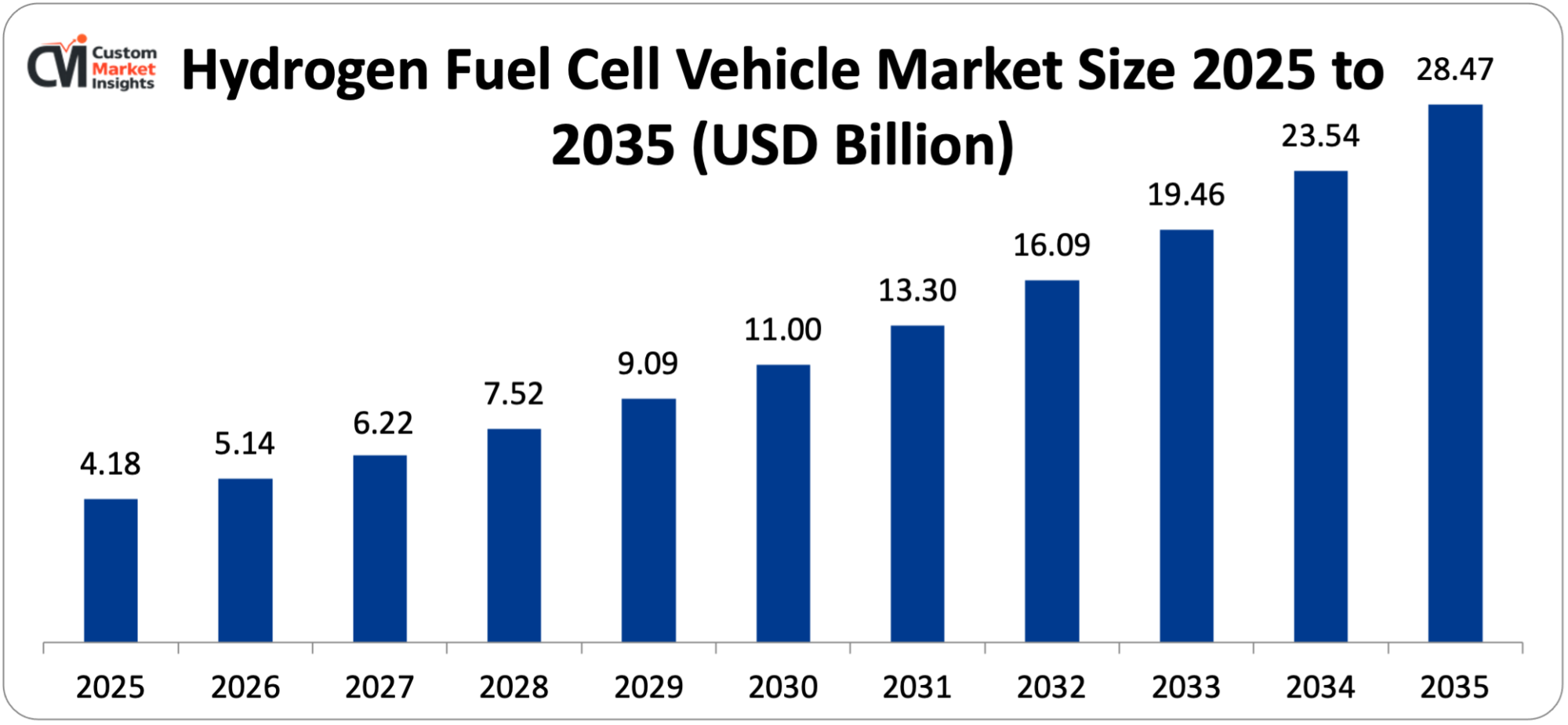

The Hydrogen Fuel Cell vehicle market is calculated at USD 4.18 Billion in 2025 and further forecasted to rise from USD 5.14 Billion in 2026 to about USD 28.47 Billion in 2035, for a projected CAGR of 18.7% (2026-2035).

The accelerating global policy commitment to hydrogen as a clean energy carrier across major economies including the European Union, Japan, South Korea, China and the United States creating regulatory frameworks, infrastructure investment programs and purchase incentives collectively contributing to hydrogen fuel cell vehicle adoption, the growing recognition of unique advantages of hydrogen fuel cell technology compared to clean battery electric vehicles in heavy duty long haul transportation applications where fast refueling, high energy density and high driving range address operational requirements that can’t currently be met at competitive weight/cost by battery technology, the rapid expansion of green hydrogen production capacity driven by renewable energy cost reductions making green hydrogen progressively more cost-competitive with fossil fuel alternatives, the accelerating development of hydrogen refueling infrastructure networks in leading hydrogen mobility markets providing the consumer and fleet operator confidence required for vehicle adoption at scale, and the continuous advancement of fuel cell stack durability, power density, and cost reduction through manufacturing scale and technology maturation collectively drive robust and sustained market growth throughout the forecast period.

Market Highlight

- Asia Pacific Dominates the Market for Hydrogen Fuel Cell Vehicles with a Market Share of 58% in 2025.

- Europe is projected to grow at a CAGR of 21.4% during 2026-2035.

- By vehicle type, the heavy-duty trucks & buses segment captured approximately 44% of the market share in 2025.

- By vehicle type, the heavy-duty trucks & buses segment is also growing at the fastest CAGR of 22.6% from 2026 to 2035.

- By technology, the proton exchange membrane fuel cell segment accounted for the largest market share of 86% in 2025, and the solid oxide fuel cell segment is projected to be the fastest growing segment (with a CAGR of 14.8%) during the forecast period 2026-2035.

- By application, the commercial freight & logistics segment accounted for the largest market share of 41% in 2025, while the public transportation segment is projected to show the fastest CAGR of 20.8% between 2026 and 2035.

- By end-user, fleet operators represented the largest market share of 48% in 2025 and the public transit authorities had the fastest CAGR (21.2%) of 2026-2035.

Significant Growth Factors

The Hydrogen Fuel Cell Vehicle Market Trends present significant growth opportunities due to several factors:

- Heavy-Duty Transportation Decarbonization Imperative Establishing Hydrogen as Essential Technology:

The international necessity of decarbonizing heavy-duty road transportation – that includes long-haul trucking, regional distribution, intercity bus operations and refuse collection that make up a disproportionate share of the road transport greenhouse gas emissions even though they constitute a minority of the vehicles – is driving the hydrogen fuel cell technology towards the status of a key complement to battery electric vehicles in the zero-emission commercial vehicle transition as defined by the fundamental operational requirements of the heavy-duty applications that hydrogen uniquely meets where battery technology has inherent physical limitations. Heavy duty long haul trucks – operating at gross vehicle weights in the range of 40-44 tonnes on routes of 400-1,000 km per day – require energy storage solutions that do not necessarily add excessive vehicle tare weight that would impact legal payload capacity, have refueling times of less than 15 minutes to minimize downtime of the driver and disruption to fleet scheduling, and have a range that is sufficient to cover an entire working day without refueling stops along the way at locations that may not necessarily have infrastructure to facilitate charging.

The European Union’s CO₂ emission standards for heavy duty vehicles – that require a 45% CO₂ emission reduction by 2030 and emission reductions of 90% by 2040 on a 2019 basis for new truck registrations – create binding targets for emission reduction in heavy duty parameters that European truck manufacturers cannot reach through incremental improvements in internal combustion engine efficiency; creating a mandatory regulatory transition to zero emissions powertrains where hydrogen fuel cell technology is commercially deployed alongside battery electric alternative propulsion to fulfil the full range of heavy duty use-cases.

The International Energy Agency’s analysis of heavy-duty vehicle decarbonization pathways consistently identifies hydrogen fuel cell technology as an essential contribution to achieving deep emissions reductions in the long-haul freight sector – especially for those routes and operations where there are weight or range limitations due to the use of battery energy storage – providing authoritative technical validation of hydrogen’s role in transportation decarbonization that supports government infrastructure investment as well as fleet operators procurement decisions. Published operational information from early commercial hydrogen truck deployments – including Hyundai XCIENT Fuel Cell trucks in operation in Switzerland, Nikola Tre FCEV trucks in North America, and Toyota hydrogen powered Class 8 trucks at the Port of Los Angeles – are demonstrating the real-world hydrogen truck performance on measures of fuel consumption, refueling time, reliability, and operating cost data that are providing the commercial proof points that fleet operators need before deciding to commit to large-scale hydrogen vehicle procurement.

The shipping and ports sector – where zero emission cargo handling equipment, drayage trucks and short sea shipping vessels have similar fast refueling and high energy density requirements to long haul trucking – are emerging as an important adjacent application market for hydrogen fuel cell technology with major port authorities including the Port of Rotterdam, Port of Hamburg and Port of Los Angeles investing in hydrogen infrastructure and hydrogen powered equipment procurement programs.

- National Hydrogen Strategies and Infrastructure Investment Programs Creating Market Foundations:

The remarkable wave of national hydrogen strategy publications and hydrogen economy investment programs around the world – with more than 40 countries already having published national hydrogen strategies by 2024 with combined government investment commitments of hundreds of billions of dollars in hydrogen production, infrastructure, and end-use application development – is laying the policy environment, infrastructure foundation and commercial confidence necessary for hydrogen fuel cell vehicle market development at scale.

Japan’s hydrogen strategy – updated in 2023 with aims for 3 million fuel cell vehicles as well as 1,200 hydrogen refueling stations by 2030 – is the world’s most mature and comprehensive national hydrogen mobility strategy, with decades of government investments in the development of hydrogen technology, the commercialization of fuel cell vehicles (Toyota and Honda which have produced hydrogen fuel cell cars), and infrastructure (developed by energy companies, including Iwatani) consuming existing hydrogen to achieve a functional, if still limited, hydrogen mobility ecosystem. South Korea’s hydrogen economy roadmap – aiming for 6.2 million hydrogen vehicles consisting of 5.9 million passenger vehicles and 300 thousand commercial vehicles, 1200 refueling stations, and domestic green hydrogen production capacity – is supported by government investment pledges and commercial leadership of Hyundai Motor Company, which has made hydrogen mobility a key strategic priority embodied in the Nexo passenger car and XCiENT commercial truck programs.

The European Clean Hydrogen Alliance – coordinating investment across hydrogen production, infrastructure and end-use sectors including hydrogen mobility under the EU Hydrogen Strategy which targets 6 million tonnes of domestic green hydrogen production and 6 million tonnes of imported green hydrogen by 2030 – seems to be mobilizing the private and public investment required for the expansion of the European hydrogen refueling network that hydrogen vehicle deployment depends upon. The U.S. National Clean Hydrogen Strategy and Roadmap — which was published in 2023 and is supported by USD 9.5 billion in hydrogen infrastructure and technology investment in the Bipartisan Infrastructure Law – USD 7 billion for Regional Clean Hydrogen Hubs – is providing the federal investment framework to support hydrogen refueling infrastructure development, hydrogen fuel cell vehicle technology demonstration, and cost reduction of green hydrogen production in the United States.

What are the Major Advances Changing the Hydrogen Fuel Cell Vehicle Market Today?

- Fuel Cell Stack Cost Reduction and Power Density Improvement Through Manufacturing Scale:

The ongoing reduction of the cost to manufacture the proton exchange membrane fuel cell stack – due to ever increasing Sc & Covid driven production volumes, improved manufacturing process automation, reduced cost by reducing the platinum catalyst loading by developing nanostructured electrodes, optimizing bipolar plate material and manufacturing costs, and improved membrane electrode assembly process yields – is shrinking the fuel cell vehicle powertrain towards cost competitiveness with both battery electric and internal combustion engine alternatives, which is crucial for commercial viability for mass market acceptance beyond the early adoption phase by government-sponsored early adopter initiatives. Toyota’s fuel cell system development trajectory – going from the first generation Mirai’s fuel cell stack to the second generation Mirai’s improved fuel cell stack achieving 174 kW peak power at 50% higher power density and approximately 20% less manufacturing cost from optimized cell design and increased cell voltage – is indicative of the cost and performance improvement trajectory possible through systematic engineering refinement and an increase in production scale.

The platinum group metal loading reduction by leading fuel cell developers — with current commercial automotive fuel cell stacks loading to about 0.125-0.25 grams of platinum per kilowatt of rated power as compared to 0.8 g/kW in early 2000s fuel cell stacks — represents a 70-85% reduction in the primary precious metals input cost that historically dominated fuel cell stack material cost, with ongoing research targeting sub-0.1 g/kW platinum loading from platinum alloy catalysts and platinum group metal-free catalyst development that would further reduce fuel cell stack cost to reach the USD The reductions in cost in the Department of Energy’s fuel cell cost modeling programs – which track the manufacturing cost at different annual production commitments – suggest that at 500,000 fuel cell system units per year, automotive PEMFC stack cost can be about USD 45/kW, which is at a point where fuel cell vehicle total cost of ownership is at a point where it is competitive with battery electric alternatives for heavy-duty use without continued subsidy support. Ballard Power Systems, Plug Power, and Cummins’ Hydrogenics division are investing in the capacity expansion of their manufacturing operations to produce heavy-duty fuel cell stacks – with Ballard’s Burnaby and Yunfu production facilities and the manufacturing expansion by Plug Power, which is manufacturing synthetic gas, in Rochester and the fuel cell manufacturing scale-up by Cummins, the companies are increasing the global fuel cells stack manufacturing capability at growth rates that support the heavy commercial vehicle deployment programs announced by some of the major manufacturers (Hyundai, Toyota, Daimler Truck, Volvo) and emerging hydrogen truck manufacturers.

- Green Hydrogen Production Cost Reduction Enabling Fuel Cost Competitiveness:

The rapid and sustained reduction in green hydrogen production cost – driven by the extraordinary cost decline of renewable electricity – which is the dominant input cost in electrolytic hydrogen production, along with the production cost reduction of electrolyzers – by scale-up and technology improvement – is creating a hydrogen fuel cost trajectory that is essential for hydrogen fuel cell vehicle total cost of ownership competitiveness – with delivered hydrogen fuel cost the primary determinant of operating cost competitiveness relative to diesel in commercial fleet applications. Green hydrogen production via water electrolysis powered by renewable electricity – the zero-carbon hydrogen production pathway needed for true lifecycle greenhouse gas emissions reduction from hydrogen fuel cell vehicles – has suffered historically from cost-uncompetitive green hydrogen production at USD 4 – USD 8/kg at renewable electricity costs of USD 40 – USD 80/MWh (an unfavorable cost comparison for fleet fuel budget management).

The dramatic reduction in utility-scale solar and wind electricity costs – with solar PPA prices dipping well below USD 20/MWh in the best resource locations including the Middle East, Chile and Australia – is opening up green hydrogen production at costs that are approaching USD 2 to USD 3/kg at point of production in the lowest cost production locations, with delivered costs at hydrogen refuelling stations in major markets projected to reach USD 4 to USD 6/kg in 2030 under favourable policy and infrastructure investment scenarios.

The IEA’s projections in their Global Hydrogen Review portend a path to green hydrogen production costs below USD 2/kg by 2030 in areas with excellent renewable resources – including the Middle East, Australia, Chile and Morocco – fueled by ongoing cost reduction in renewables and electrolyzer stack technology cost reduction from today’s USD 500 – USD 1,000 /kW to USD 100 – USD 200 /kW by 2030 through manufacturing scale-up. The European Hydrogen Bank – which was set up to offer competitive grant funding for the first wave of commercial-scale green hydrogen projects under the European Hydrogen Auctions program – awarded its first grants in 2024, to projects committing to supply green hydrogen at prices of EUR 0.48-EUR 0.99/kg of hydrogen produced, giving a subsidized delivered cost giving evidence of the trajectory towards cost-competitive green hydrogen as electrolyzer and renewable costs fall with volume.

- Heavy-Duty Hydrogen Truck Commercial Deployment Acceleration:

The acceleration of commercial hydrogen truck deployment by major commercial vehicle manufacturers around the world, including Hyundai, Toyota/Hino, Daimler Truck’s Mercedes-Benz GenH2 and Freightliner program, Volvo Trucks’ collaboration with Daimler in Cellcentric, IVECO and Nikola’s joint program, and emerging pure play hydrogen truck developers, is moving hydrogen commercial vehicles from proof-of-principle demonstration to volume production to generate the real-world operational data, fleet operator experience, and manufacturing cost reduction requirements for broader market adoption beyond early commercial programs. Hyundai’s XCIENT Fuel Cell truck – the world’s first commercially produced hydrogen fuel cell Class 8 heavy truck, with cumulative deployments of over 100 units in Switzerland and increasing fleet operations in South Korea, the United States, and Germany – is the most commercially mature hydrogen heavy truck program in the world, so it contains real-world operating data on hydrogen usage, maintenance needs, reliability, and driver acceptance under a variety of real-world commercial trucking operating conditions.

Toyota’s Class 8 hydrogen fuel cell truck demonstration at the Port of Los Angeles – with over 10,000 zero emission trips captured as part of the ZANZEFF project – provided the operational proof-of-concept for hydrogen drayage truck performance in terms of intensive port operations with refueling practicality, range adequacy, and payload capacity preservation to address fleet operator concerns over hydrogen truck operational similarity for high intensity port drayage applications. Daimler Truck’s GenH2 Truck — target of 1,000+ km range from just one fill of hydrogen (liquid hydrogen storage, not compressed gas storage) that allows for the equivalent of the energy density needed for real long-haul operation — the OneGenH2 Truck entered customer pilot programs in 2023 with volume production in the second half of the decade target and is one of the most technically ambitious commercial hydrogen truck programs and demonstrates that the major global truck OEMs are making serious engineering and manufacturing investments in hydrogen powertrain technology. The European hydrogen truck market is being catalyzed by the H2Accelerate initiative – a collaboration of Daimler Truck, Volvo, Shell and hydrogen infrastructure partners that is signing up to coordinated truck deployment and refueling infrastructure development, and the European Hydrogen Backbone initiative, which is developing the pipeline infrastructure for hydrogen distribution that will serve as the basis for hydrogen refueling station economics along European freight corridors.

Category Wise Insights

By Vehicle Type

Why Do Heavy-Duty Trucks & Buses Lead the Market?

Heavy-duty trucks and buses are the largest type of vehicle with an average of 44% market share in 2025 by revenue – reflecting the commercial vehicle segment’s higher per-unit vehicle value generating higher market revenue relative to passenger car unit volumes and the established commercial momentum of hydrogen bus programs across China, Europe, South Korea and Japan in combination with the growing hydrogen heavy truck deployments by Hyundai, Toyota and emerging commercial programs by major OEMs. The commercial vehicle hydrogen application commanding the majority of market revenue is due to the basic match between the operational characteristics of hydrogen fuel cell technology – fast refueling, high energy density, long range, and preserved payload capacity – and the demanding operational requirements of commercial freight and public transit that render hydrogen the zero emission control technology of choice for these applications in contrast to battery electric alternatives. Heavy-duty trucks at GVWR Higher Than 15 Tonnes is the fastest growing vehicle classification under the segment at a CAGR of 22.6% from 2026 to 2035 due to the EU heavy-duty vehicle CO₂ standards that require 90% emission reduction by 2040 creating a mandatory technology transition timeline and commercial deployment programs of Hyundai XCIENT, Daimler GenH₂, Volvo FM/FH fuel cell, and Nikola Tre FCEV establishing the commercial viability of the technology and analysis of the total cost of ownership of hydrogen versus battery electric showing for routes above 400 km daily that constitute a significant portion of long-haul freight operations.

By Technology

Why Do Proton Exchange Membrane Fuel Cells Lead the Market?

PEMFC has the highest market share of around 86% in the year 2025, accounting for its status as the only commercialized fuel cell technology suitable for automotive use – applications that demand rapid cold starting capability that is critical for vehicle applications, high power density to create compact packaging, operating temperatures of 60-80 degC with the potential of standard automotive thermal management requirements and dynamic load following capability to match vehicle power demand transients, compared to solid oxide fuel cells with operating temperatures of 600-1000 degC and prolonged warm-up times with the potential of incompatibility with Toyota’s PEMFC system developed over decades of fuel cell technology investments and utilized in the Mirai, FCHV-adv and commercial truck PEMFC system programs and Hyundai’s HTWO fuel cell system implemented in the NEXO and XCIENT are the most commercially proven PEMFC automotive system implementations with both companies testing the PEMFC system for millions of cumulative fuel cell vehicle hours of fuel cell operating experience proving PEMFC system durability and performance in actual fuel cell operating conditions. The commercial dominance of the PEMFC technology is supported by an established global supply chain for the delivery of PEMFC components – including Nafion membrane from Chemours, carbon fiber bipolar plates from SGL Carbon, and platinum catalyst from Johnson Matthey and Umicore – that offers competitive component supply to support the scale-up of PEMFC vehicle production by multiple manufacturers at the same time.

By Application

Why Does Commercial Freight & Logistics Lead the Market?

Commercial freight as well as logistics – making up the largest application at ~41% of overall market share in 2025 – reflects the commercial rationale to bring fleet operators towards hydrogen fuel cell technology for long-haul and regional freight operation – where combination of regulatory compliance obligation under tightening CO₂ standards and operational capability of hydrogen fast refueling benefits hydrogen heavy trucks performing high-utilization commercial vehicle applications and the proven performance of hydrogen heavy trucks in early commercial programs make hydrogen the favourable zero-emission solution to this application. Commercial freight operators managing long haul fleet operations experience the most severe operational case for hydrogen versus battery electric – the weight penalty from multi-tonne battery packs that costs them a lower legal payload; the charging times that spend too much time off the road, requiring additional vehicles or driver scheduling complexity; and the range limitations that require route modification and reduce operational efficiency – so the attributes that make hydrogen comparable in weight to diesel and fast refueling with long range translate directly into operational and commercial superiority for long haul applications that fleet operators can quantify and value in fleet total cost of ownership analyses.

By End-User

Why Do Fleet Operators Lead the Market?

Fleet operators tend to be the largest end user segment at about 48% of market share in 2025 and are reflective of the fact that the majority of current hydrogen vehicle deployment is in commercial fleet applications with centralized refueling infrastructure at depots addressing the station availability issue that is a constraint for individual consumer adoption where the operational and regulatory drivers of commercial vehicle decarbonization create compelling (beyond consumer environmental preference) drivers to adopt hydrogen vehicles, and the total cost of ownership analysis (vehicle acquisition, fuel cost, maintenance, and downtime cost) screens for commercial fleet purchase decisions. Fleet operators in the logistics sector, municipal services and public transit can consider shared investment in centralized hydrogen refueling infrastructure at their operating depots, eliminating the public refueling network dependence that restricts individual consumer adoption of hydrogen vehicles, and negotiating hydrogen supply contracts at scale which can achieve delivered fuel costs below the public station retail prices. Public transit authorities are the fastest growing end user segment at a CAGR of 21.2% from 2026 to 2035, driven by the occurrence of zero emission public transit mandates by governments, the proven performance of hydrogen buses in commercial operations in China, Germany, South Korea, and the UK, and the depot refueling model of transit bus operations, which simplifies hundreds of millions of dollars of investment in hydrogen infrastructure as part of existing bus depot infrastructure.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 5.14 Billion |

| Projected Market Size in 2035 | USD 28.47 Billion |

| Market Size in 2025 | USD 4.18 Billion |

| CAGR Growth Rate | 18.7% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Vehicle Type, Technology, Application, End-User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

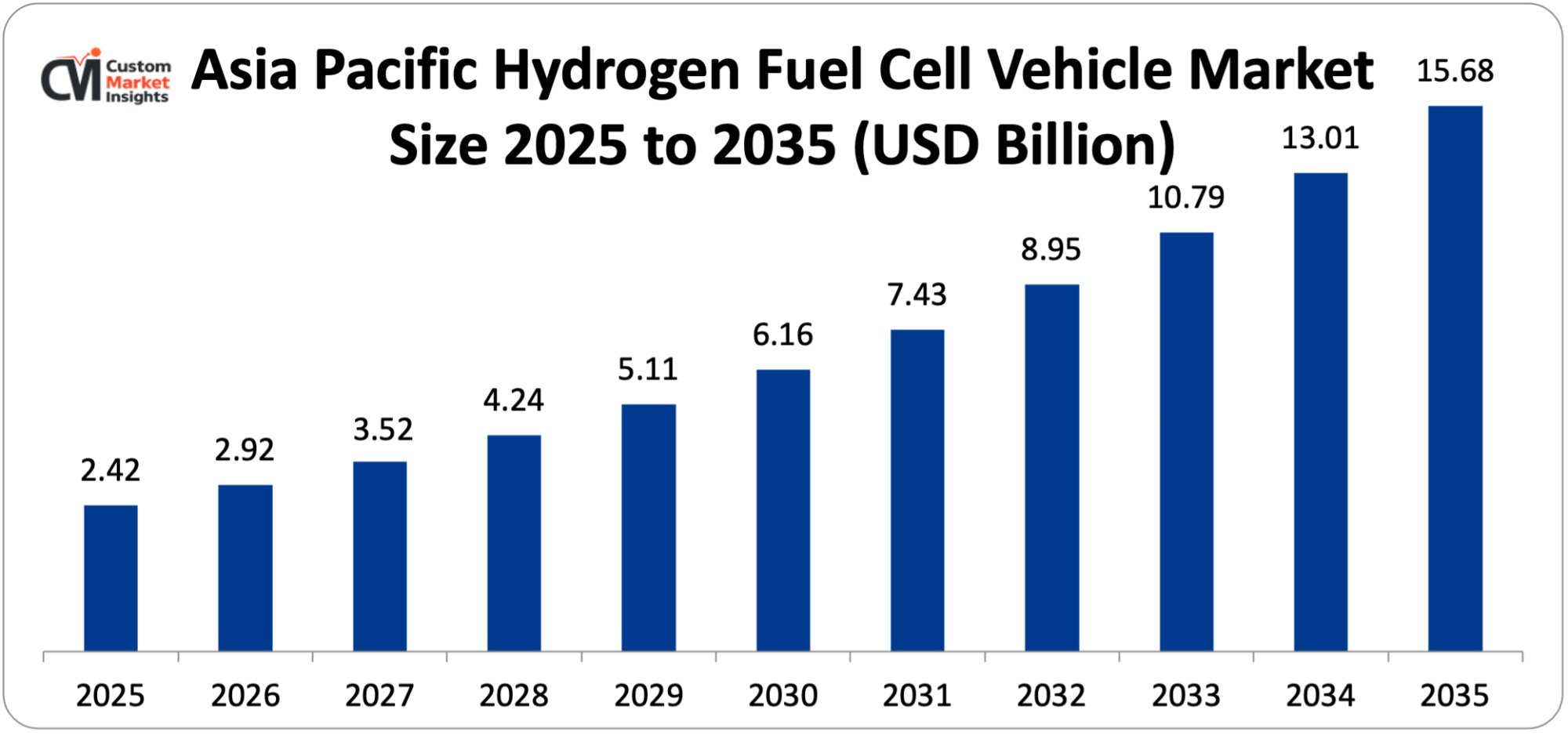

The Asia Pacific hydrogen fuel cell vehicle market size is estimated at USD 2.42 billion in 2025 and is projected to reach approximately USD 15.68 billion by 2035, with a CAGR of 20.6% from 2026 to 2035.

Why Did Asia Pacific Dominate the Market in 2025?

Asia Pacific commands approximately 58% of global market share in 2025 reflecting the region’s role in the global center of hydrogen fuel cell vehicle technology development and deployment – with Japan’s Toyota and Honda currently representing the only passenger car FCEV producers at commercial scale globally, South Korea’s Hyundai Motor Company operating the world’s most comprehensive commercial hydrogen vehicle program that spans passenger cars through to heavy trucks and China representing the world’s largest hydrogen fuel cell bus deployment market driven by the government’s hydrogen demonstration city cluster subsidy program. Japan’s cumulative hydrogen fuel cell vehicle fleet – including the Toyota Mirai, the Honda Clarity Fuel Cell and the fuel cell bus programs that function in Tokyo and other major cities – is the oldest and most operationally experienced hydrogen mobility ecosystem in the world – offering the range of technical learning, cost reducing trajectory and infrastructure development model that is informing hydrogen vehicle programs around the world.

South Korea’s hydrogen vehicle ecosystem – anchored by Hyundai’s NEXO passenger SUV, XCIENT commercial truck and the Korean government’s Hydrogen Economy Roadmap — have propelled South Korea to be the second most commercially advanced hydrogen vehicle market globally with increasing domestic hydrogen refueling infrastructure and progressive hydrogen vehicle expansion across public transit, logistics and private passenger car sectors. China’s hydrogen fuel cell commercial vehicle market – this driven by central and provincial government subsidies under the demonstration city cluster program and strategic importance given to hydrogen under China’s 14th and 15th Five-Year Plans, as well as the scale of production by Chinese hydrogen bus manufacturers such as Yutong, SAIC and King Long – has developed China as the world’s largest hydrogen commercial vehicle deployment market in terms of unit volume, although mostly serving the bus segment with heavy trucks deployment still in the demonstration phases.

Why is Europe the Fastest-Growing Major Market?

Europe is showing the highest growth among established large markets with an expected CAGR of 21.4% over the period from 2026 to 2035, driven by 90% emission reduction by the European Union (EU) mandatory heavy duty vehicle carbon dioxide (CO2) emission standards requiring heavy duty vehicles to be decarbonized by 2040 triggering a decade-long commercial vehicle de-carbonization transformation, the European Clean Hydrogen Alliance organizing investment activities along the value chain in hydrogen production, infrastructure, and mobility, the H2Accelerate initiative aligning truck OEM deployment with the Germany represents Europe’s largest hydrogen vehicle market – thanks to the country’s industrial foundation of heavy-duty vehicle manufacturers such as Daimler Truck, MAN and their fuel cell vehicle development initiatives, the German National Hydrogen Strategy investment in EUR9 billion in domestic and EUR2 billion in international hydrogen investment, as well as the fact that Germany has one of the largest and most dense autobahn freight road networks providing attractive market for hydrogen refueling infrastructure along major heavy freight corridors. The Netherlands, France and the United Kingdom are great examples, representing important European hydrogen vehicle markets with active government hydrogen mobility programs, growing hydrogen refueling infrastructure networks and commercial hydrogen bus and truck deployment programs at transit authorities/logistics operators.

Why is North America an Important and Growing Market?

The North American Hydrogen Fuel Cell Vehicles market is estimated to be worth USD 498 million in 2025 and is expected to reach USD 3.18 billion by 2035, with a compound annual growth rate of 20.4%. North America’s market development is driven by the following: U.S. Bipartisan Infrastructure Law’s USD 9.5 billion hydrogen investment, including USD 7 billion Regional Clean Hydrogen Hubs creating the green hydrogen production and distribution infrastructure prerequisite for competitive hydrogen fuel costs, California’s Low Carbon Fuel Standard and heavy-duty vehicle emission regulations driving hydrogen truck adoption at California ports and logistics hubs, the CARB Advanced Clean Trucks regulation requiring increasing%ages of zero-emission trucks among OEM sales in California with adoption by multiple additional states, and DOE’s Hydrogen Shot initiative targeting USD 1/kg green hydrogen production cost by 203 California’s hydrogen refueling infrastructure – with the largest network of public hydrogen stations in the United States concentrated in the Los Angeles, San Francisco Bay Area and San Diego metropolitan areas – provides the consumer FCEV market foundation for the sales of the Toyota Mirai and Hyundai NEXO in the California market, making California the largest FCEV passenger car market in the United States of America and the commercial proving ground for hydrogen vehicle operations under North American conditions.

Why is the Middle East & Africa an Emerging Strategic Market?

The LAMEA region exhibits high strategic importance fueled by the Middle East’s distinct position as a potential global green hydrogen export center – with Saudi Arabia’s NEOM project aiming to develop 600 tonnes per day of green hydrogen production for export, the UAE’s hydrogen strategy aiming to develop 25% of global clean hydrogen trade by 2030 and Oman’s hydrogen economy strategy aiming to develop green hydrogen export capacity to build an ecosystem for green hydrogen production and exports, and with a focus on hydrogen fuel cost reduction in importing regions, will in turn spur domestic hydrogen vehicles in demonstration programs. Saudi Arabia’s Vision 2030 transportation electrification goals include hydrogen fuel cell bus programs for the public transit systems of Riyadh and other large Saudi cities, with NEOM’s planned hydrogen-powered mobility systems being the world’s most ambitious integrated hydrogen mobility urban deployment concept. Australia’s large green hydrogen export potential – supported by plentiful solar and wind renewable energy resources and government investment in the Australian Hydrogen Council – is engaging hydrogen export supply chains to Japan, South Korea and Germany that will establish delivered green hydrogen cost benchmarks that have direct relevance to fuel cost economics for hydrogen vehicle fleets in importing markets.

Top Players in the Market and Their Offerings

- Toyota Motor Corporation

- Hyundai Motor Company

- Honda Motor Co. Ltd.

- Daimler Truck AG

- Volvo Group (Cellcentric JV with Daimler Truck)

- Nikola Corporation

- Ballard Power Systems Inc.

- Plug Power Inc.

- Nel ASA

- ITM Power plc

- Cummins Inc. (Hydrogenics)

- Others

Key Developments

The market has undergone significant developments as industry participants seek to advance commercial hydrogen truck deployment, expand hydrogen refueling infrastructure, and respond to the accelerating regulatory and commercial momentum for zero-emission heavy-duty transportation globally.

- In April 2025: Hyundai Motor Company announced the commercial launch of its next-generation XCIENT Fuel Cell 2.0 heavy truck – with the following features: New 200 kW dual fuel cell stack system, extending 40% higher power output than the first generation XCIENT, Liquid hydrogen storage enabling over 800 km driving range per hydrogen fill, Redesigned fuel cell system architecture adding 40% fewer balance of plant components for greater reliability, reduced maintenance requirements.

- In February 2025: Toyota Motor Corporation and Isuzu Motors recently announced a joint venture – HyTruck Japan – for the commercial manufacture and sale of hydrogen fuel cell heavy trucks for the Japanese domestic market, leveraging Toyota’s PEMFC system technology and its fuel cell vehicle manufacturing know-how with Isuzu’s market-leading Japanese commercial trucking position and its extensive network of dealers serving the Japanese fleet operator industry.

The Hydrogen Fuel Cell Vehicle Market is segmented as follows:

By Vehicle Type

- Passenger Cars (Sedan, SUV)

- Light Commercial Vehicles (Vans, Pickup Trucks)

- Heavy-Duty Trucks (Class 7–8, Semi-Trailers)

- Buses (Transit Buses, Intercity Coaches, School Buses)

- Other Vehicle Types (Forklifts, Trains, Marine Vessels)

By Technology

- Proton Exchange Membrane Fuel Cells (PEMFC)

- Solid Oxide Fuel Cells (SOFC)

- Alkaline Fuel Cells (AFC)

- Other Technologies (Phosphoric Acid, Molten Carbonate)

By Application

- Public Transportation (City Buses, Intercity Routes)

- Private Transportation (Personal Passenger Cars, Light Commercial)

- Commercial Freight & Logistics (Long-Haul Trucking, Last-Mile Delivery)

- Material Handling (Forklifts, Port Equipment)

- Other Applications (Rail, Maritime, Airport Ground Support)

By End-User

- Individual Consumers

- Fleet Operators (Logistics, Delivery, Rental)

- Public Transit Authorities

- Government & Defense

- Other End-Users (Mining, Industrial)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Hydrogen Fuel Cell Vehicle by Segments

- 2.1.2. Hydrogen Fuel Cell Vehicle by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Hydrogen Fuel Cell Vehicle Market Attractiveness Analysis, By Vehicle Type

- 2.2.3. Hydrogen Fuel Cell Vehicle Market Attractiveness Analysis, By Technology

- 2.2.4. Hydrogen Fuel Cell Vehicle Market Attractiveness Analysis, By Application

- 2.2.5. Hydrogen Fuel Cell Vehicle Market Attractiveness Analysis, By End-User

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Heavy-Duty Transportation Decarbonization Imperative: Establishing Hydrogen as Essential Technology

- 3.1.2. National Hydrogen Strategies and Infrastructure Investment Programs Creating Market Foundations

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Hydrogen Fuel Cell Vehicle Market – By Vehicle Type

- 4.1. Vehicle Type Market Overview, By Vehicle Type Segment

- 4.1.1. Hydrogen Fuel Cell Vehicle Market Revenue Share, By Vehicle Type, 2025 & 2035

- 4.1.2. Passenger Cars (Sedan, SUV)

- 4.1.3. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Light Commercial Vehicles (Vans, Pickup Trucks)

- 4.1.7. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Heavy-Duty Trucks (Class 7–8, Semi-Trailers)

- 4.1.11. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Buses (Transit Buses, Intercity Coaches, School Buses)

- 4.1.15. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Other Vehicle Types (Forklifts, Trains, Marine Vessels)

- 4.1.19. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Vehicle Type Market Overview, By Vehicle Type Segment

- Chapter 5. Hydrogen Fuel Cell Vehicle Market – By Technology

- 5.1. Technology Market Overview, By Technology Segment

- 5.1.1. Hydrogen Fuel Cell Vehicle Market Revenue Share, By Technology, 2025 & 2035

- 5.1.2. Proton Exchange Membrane Fuel Cells (PEMFC)

- 5.1.3. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Solid Oxide Fuel Cells (SOFC)

- 5.1.7. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Alkaline Fuel Cells (AFC)

- 5.1.11. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Other Technologies (Phosphoric Acid, Molten Carbonate)

- 5.1.15. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Technology Market Overview, By Technology Segment

- Chapter 6. Hydrogen Fuel Cell Vehicle Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Hydrogen Fuel Cell Vehicle Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Public Transportation (City Buses, Intercity Routes)

- 6.1.3. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Private Transportation (Personal Passenger Cars, Light Commercial)

- 6.1.7. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Commercial Freight & Logistics (Long-Haul Trucking, Last-Mile Delivery)

- 6.1.11. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Material Handling (Forklifts, Port Equipment)

- 6.1.15. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Other Applications (Rail, Maritime, Airport Ground Support)

- 6.1.19. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Hydrogen Fuel Cell Vehicle Market – By End-User

- 7.1. End-User Market Overview, By End-User Segment

- 7.1.1. Hydrogen Fuel Cell Vehicle Market Revenue Share, By End-User, 2025 & 2035

- 7.1.2. Individual Consumers

- 7.1.3. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Fleet Operators (Logistics, Delivery, Rental)

- 7.1.7. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Public Transit Authorities

- 7.1.11. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Government & Defense

- 7.1.15. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Other End-Users (Mining, Industrial)

- 7.1.19. Hydrogen Fuel Cell Vehicle Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-User Market Overview, By End-User Segment

- Chapter 8. Hydrogen Fuel Cell Vehicle Market – Regional Analysis

- 8.1. Hydrogen Fuel Cell Vehicle Market Overview, By Region Segment

- 8.1.1. Global Hydrogen Fuel Cell Vehicle Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Hydrogen Fuel Cell Vehicle Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Hydrogen Fuel Cell Vehicle Market Revenue, By Vehicle Type, 2026 – 2035

- 8.1.4. Global Hydrogen Fuel Cell Vehicle Market Revenue, By Technology, 2026 – 2035

- 8.1.5. Global Hydrogen Fuel Cell Vehicle Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Hydrogen Fuel Cell Vehicle Market Revenue, By End-User, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Hydrogen Fuel Cell Vehicle Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Hydrogen Fuel Cell Vehicle Market Revenue, By Vehicle Type, 2026 – 2035

- 8.2.3. North America Hydrogen Fuel Cell Vehicle Market Revenue, By Technology, 2026 – 2035

- 8.2.4. North America Hydrogen Fuel Cell Vehicle Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Hydrogen Fuel Cell Vehicle Market Revenue, By End-User, 2026 – 2035

- 8.2.6. U.S. Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Hydrogen Fuel Cell Vehicle Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Hydrogen Fuel Cell Vehicle Market Revenue, By Vehicle Type, 2026 – 2035

- 8.3.3. Europe Hydrogen Fuel Cell Vehicle Market Revenue, By Technology, 2026 – 2035

- 8.3.4. Europe Hydrogen Fuel Cell Vehicle Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Hydrogen Fuel Cell Vehicle Market Revenue, By End-User, 2026 – 2035

- 8.3.6. Germany Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Hydrogen Fuel Cell Vehicle Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Hydrogen Fuel Cell Vehicle Market Revenue, By Vehicle Type, 2026 – 2035

- 8.4.3. Asia Pacific Hydrogen Fuel Cell Vehicle Market Revenue, By Technology, 2026 – 2035

- 8.4.4. Asia Pacific Hydrogen Fuel Cell Vehicle Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Hydrogen Fuel Cell Vehicle Market Revenue, By End-User, 2026 – 2035

- 8.4.6. China Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Hydrogen Fuel Cell Vehicle Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Hydrogen Fuel Cell Vehicle Market Revenue, By Vehicle Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Hydrogen Fuel Cell Vehicle Market Revenue, By Technology, 2026 – 2035

- 8.5.4. The Middle-East and Africa Hydrogen Fuel Cell Vehicle Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Hydrogen Fuel Cell Vehicle Market Revenue, By End-User, 2026 – 2035

- 8.5.6. Saudi Arabia Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Hydrogen Fuel Cell Vehicle Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Hydrogen Fuel Cell Vehicle Market Revenue, By Vehicle Type, 2026- 2035

- 8.6.3. Latin America Hydrogen Fuel Cell Vehicle Market Revenue, By Technology, 2026 – 2035

- 8.6.4. Latin America Hydrogen Fuel Cell Vehicle Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Hydrogen Fuel Cell Vehicle Market Revenue, By End-User, 2026 – 2035

- 8.6.6. Brazil Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Hydrogen Fuel Cell Vehicle Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Hydrogen Fuel Cell Vehicle Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Hydrogen Fuel Cell Vehicle Market: Company Market Share, 2025

- 9.2. Global Hydrogen Fuel Cell Vehicle Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Toyota Motor Corporation

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Hyundai Motor Company

- 10.3. Honda Motor Co. Ltd.

- 10.4. Daimler Truck AG

- 10.5. Volvo Group (Cellcentric JV with Daimler Truck)

- 10.6. Nikola Corporation

- 10.7. Ballard Power Systems Inc.

- 10.8. Plug Power Inc.

- 10.9. Nel ASA

- 10.10. ITM Power plc

- 10.11. Cummins Inc. (Hydrogenics)

- 10.12. Others.

- 10.1. Toyota Motor Corporation

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 37

List Of Tables

Tables No 1 to 51

Prominent Player

- Toyota Motor Corporation

- Hyundai Motor Company

- Honda Motor Co. Ltd.

- Daimler Truck AG

- Volvo Group (Cellcentric JV with Daimler Truck)

- Nikola Corporation

- Ballard Power Systems Inc.

- Plug Power Inc.

- Nel ASA

- ITM Power plc

- Cummins Inc. (Hydrogenics)

- Others

FAQs

The key players in the market are Toyota Motor Corporation, Hyundai Motor Company, Honda Motor Co. Ltd., Daimler Truck AG, Volvo Group (Cellcentric JV with Daimler Truck), Nikola Corporation, Ballard Power Systems Inc., Plug Power Inc., Nel ASA, ITM Power plc, Cummins Inc. (Hydrogenics), Others.

Government regulations are the most consequential driver for the development of the hydrogen fuel cell vehicle market, which operates through vehicle emission standards creating a mandatory technology transition timeline, infrastructure investment programs creating the prerequisite for the refueling network required for the adoption of the vehicles, purchase incentive programs reducing the effective cost for the vehicle purchase, and green hydrogen production support reducing fuel cost towards commercial competitiveness. The EU’s CO₂ emission standards for heavy-duty vehicles – of 45% CO₂ emission reduction in 2030 and 90% in 2040 – are the single most commercially significant regulation affecting the hydrogen truck market; this law mandates legally binding emission reduction levels of new truck registrations that OEMs cannot meet without the powertrains, configuring a mandatory commercial vehicle technology transition that includes hydrogen as a required transition – and is very much happening in the long-haul area where battery electric shortfalls are most notable. The U.S. EPA’s Phase 3 Greenhouse Gas Standards for Heavy-Duty Vehicles – to take effect in 2024 and require progressive reduction of CO₂ emissions between model years 2027 through 2032 – put up equivalent regulatory pressure in the U.S. for commercial vehicle decarbonization to support investment in hydrogen truck development by U.S.-market truck manufacturers and create demand signals for hydrogen infrastructure development along the U.S. freight highways. California’s Advanced Clean Trucks regulation – which mandates growing percentages of zero-emission trucks among new OEM sales in California, with other states adopting California’s standards under Clean Air Act Section 177, creates the largest single-state regulatory hydrogen truck demand driver in North America, with the scale of California’s freight market and regulatory precedent-setting role in driving CARB regulation having an outsized influence on North America commercial vehicle technology strategy. Japan’s subsidy program for fuel cell vehicle purchases – offering purchase subsidies of JPY 1.5-3.3 million per passenger FCEV and offering larger subsidies for commercial hydrogen vehicles—directly lowers the effective acquisition cost premium that represents the main adoption barrier for both individual consumers and small fleet operators, with subsidy continuation being a key policy variable for developing hydrogen passenger cars in Japan on a near-term basis. The decarbonization goals of the International Maritime Organization for shipping.

Hydrogen fuel cell vehicle pricing is projected to command high premiums over equivalent diesel- and battery-electric options. (ta = 12 years) due to the debuted practices of the commercial production of fuel cell motorcycles and the pricing of PEMFC pipeline reactors, including platinum catalysts, membrane electrode assemblies, and bipolar plates at current production economies per. The Toyota Mirai passenger car – retailing for approximately USD 50,000 – USD 67,000 before federal and state incentives in the United States – commands a premium of approximately USD 15,000 – USD 25,000 over similar battery electric and hybrid vehicles, with government purchase incentives of USD 8,000 – USD 15,000 in the United States and equivalent incentives in Japan and South Korea bringing effective purchase price premiums down to prices which are acceptable to early adopter consumers in markets where there is a sufficient refueling The Hyundai XCIENT Fuel Cell heavy truck – available for purchase at about USD 300,000 – USD 400,000 per unit in European markets—is a premium of around 100 – 150% over equivalent diesel Class 8 trucks (offset in part by reduced effective fleet operator acquisition cost via reduced fuel cost per kilometer over the life of the truck on routes where hydrogen fuel prices closely approach diesel energy equivalency as well as by Government purchase benefits in South Korea, Germany and Switzerland). The pathway to achieving commercial cost competitiveness in hydrogen fuel cell vehicles – which requires the simultaneous addressing of manufacturing cost reduction to USD 45-100/kW, cost reduction for green hydrogen fuel (between USD 4-6/kg as delivered), and increased hydrogen refueling infrastructure density reducing the risk premium to hydrogen fueling infrastructure operators – is expected to be reached incrementally through the forecast period – with heavy-duty commercial vehicles achieving total cost of ownership parity with diesel in countries with favorable policies, including Germany, South Korea, and California, by around 2028-2030 balancing supporting policy environments.

Based on an analysis to date, the market is estimated to reach around USD 28.47 billion by 2035, as the heavy duty commercial vehicles segment scales from early commercial deployment to mainstream adoption as the EU CO2 regulations mandate mandatory procurement transitions, cost of green hydrogen production declining to USD 2 – USD 3/kg delivered in refueling stations at production volumes of 0.25 – 0.50 kg production per hour, fuel cell stack costs between USD 45 – USD 100/kW at production volumes of 100,000 – 500,000 units annually through manufacturing scale-up by Toyota, Hyundai, Ballard, and Cummins, European hydrogen refueling infrastructure scaling along TEN-T freight corridors under H2Accelerate and EU Innovation Fund co-investment providing the infrastructure coverage required for fleet operator route planning confidence, Asia Pacific’s continued leadership through expanding Chinese commercial vehicle deployment, growing Japanese infrastructure network, and Hyundai’s XCIENT 2.0 European commercial scale-up, and North America’s hydrogen ecosystem development accelerating through Regional Clean Hydrogen Hub infrastructure investment and California’s regulatory leadership in zero-emission truck requirements, at a CAGR of 18.7% from 2026 to 2035.

Asia Pacific is projected to have the highest revenue share during the forecast period, commanding about 58% of global market share in 2025, due to the leadership of Toyota and Honda in PEMFC technology globally which produces the most commercially mature passenger car FCEV products, the comprehensive hydrogen vehicle program carried out by Hyundai that spans the entire spectrum from passenger cars to Class 8 trucks, the world’s widest in terms of number of commercial hydrogen vehicle types, the world-leading hydrogen fuel cell commercial vehicle deployment in China driven by subsidies from Chinese government demonstration city clusters coupled with Chinese-scale production of hydrogen buses by Chinese hydrogen bus manufacturers, Japan’s decades of cumulative hydrogen mobility ecosystem development providing the world’s most operationally mature hydrogen vehicle infrastructure and fleet experience, and South Korea’s government hydrogen economy roadmap providing sustained policy commitment and investment supporting Hyundai’s commercial hydrogen vehicle programs across multiple vehicle segments simultaneously.

Europe is expected to record the highest CAGR of 21.4% towards the established major markets during the forecast period due to the mandatory heavy-duty CO₂ regulation in the EU that mandates the commercial vehicle decarbonization timeline to be unavoidable, the H₂Accelerate initiative that is mandating the simultaneous deployment of trucks and refueling infrastructure, which will at least mitigate the challenge of infrastructure adoption in circularity, the Daimler Truck and Volvo Cellcentric joint venture that is working together to promote shared development of PEMFC systems in a way that is likely to reach production-cost parity, the European Hydrogen Bank reducing green hydrogen production costs through competitive auction mechanisms, and Germany’s EUR 9 billion national hydrogen strategy investment creating the largest single national hydrogen economy investment program in Europe that is funding refueling infrastructure, green hydrogen production, and hydrogen vehicle procurement programs simultaneously.

The Global Hydrogen Fuel Cell Vehicle Market is projected to witness significant growth due to the mandatory heavy-duty vehicle CO2 emission standards of the EU that require 90% emission reduction by 2040 for new truck registrations creating a binding commercial vehicle technology transition timeline including hydrogen as a fundamental pathway, the USD 9.5 billion USD hydrogen investment in the US Bipartisan Infrastructure Law including USD 7 billion for Regional Clean Hydrogen Hydrogen Hub creation creating green hydrogen production and distribution infrastructure, the EU Energy Watch Group and International Energy Agency (IEA) Hydrogen Pathway scenario supporting the reach of 2040 USD creating green hydrogen production and distribution infrastructure, the IEA projecting a pathway to green hydrogen production costs below USD 2/kg by 2030 in favorable resource regions as renewable electricity and electrolyzer costs decline, Japan’s hydrogen strategy targeting 3 million fuel cell vehicles and 1,200 hydrogen refueling stations by 2030 backed by government investment and Toyota and Honda commercial programs, South Korea’s hydrogen economy roadmap targeting 6.2 million hydrogen vehicles with Hyundai’s XCIENT deployment demonstrating commercial viability across Swiss, Korean, and German operations, Hyundai’s XCIENT 2.0 announcement of 500-unit purchase commitments from European logistics operators marking the transition from demonstration to commercial deployment scale, the H2Haul consortium’s EUR 1.4 billion EU Innovation Fund grant funding coordinated truck and infrastructure deployment along European TEN-T freight corridors, and the European Hydrogen Bank’s first green hydrogen auction results demonstrating EUR 0.48–EUR 0.99/kg produced green hydrogen cost trajectory validating long-term fuel cost competitiveness.