India Religious Tourism Market Size, Trends and Insights By Religion Type (Hinduism, Islam, Sikhism, Buddhism, Christianity, Other Religions), By Sector Type (Organised, Unorganised), By Tourism Type (Pilgrimages, Religious & Heritage Tours, Day Trips & Local Getaways, Spiritual Retreats), By Booking Channel (Online Booking, Phone Booking, In-Person Booking), By End User (Domestic Pilgrims, International Tourists, Spiritual Seekers, Tour Operators), and By Region - Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | India |

| Largest Market: | India |

Major Players

- Thomas Cook (India) Limited

- MakeMyTrip (India) Private Limited

- Cleartrip Private Limited

- Easy Trip Planners Pvt. Ltd.

- Others

Reports Description

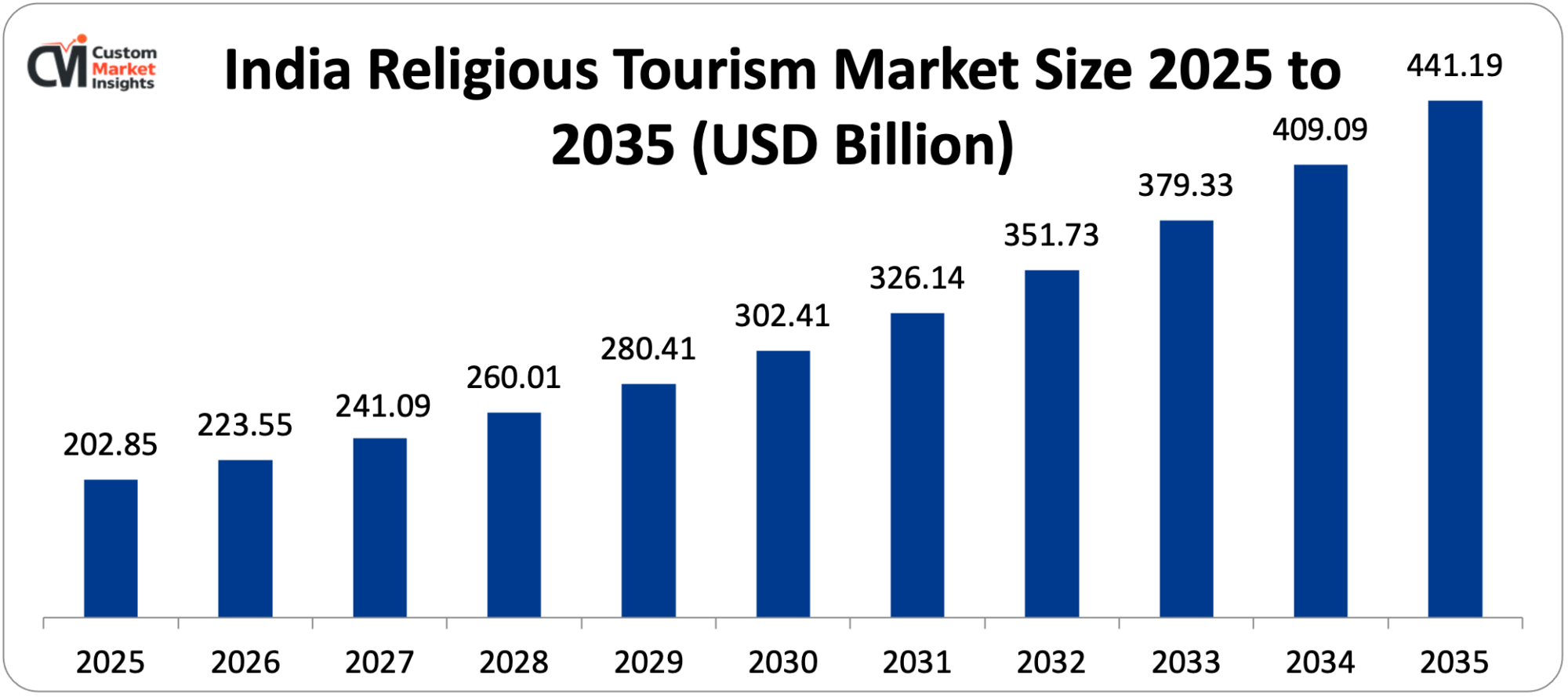

Calculations have estimated the India religious tourism market size: USD 202.85 billion in FY2025 and projected that it will grow at an annual CAGR of 8.08% between FY2026 and FY2035 to indicate that the market size will grow to USD 223.55 billion in FY2026 and USD 441.19 billion in FY2035.

The market is growing due to the deep-seated cultural and spiritual practices, government investments in infrastructure via the PRASHAD and Swadesh Darshan 2.0 schemes, increased disposable incomes that allow many people to spend money on pilgrimages, the growing organized tourism operators that are offering high quality packages, the availability of online platforms that have led to better bookings, and the growing interest of international tourists in the diverse religious cultures of India.

Market Highlight

- In 2025, religious tourism contributes 60% of domestic Indian tourism, and there are 1,433 million domestic religious travelers as compared to 677 million domestic religious travelers in 2021.

- In 2025, the market registered a revenue of USD 16,380 million that was double that of USD 8,600 million in 2021, which shows post-pandemic recovery momentum.

- By religion, Hinduism is the most dominant religion with 68% market share, propelled by 1.1 billion followers who constitute 94% of the population in the world who are Hindu.

- By sector type, organised sector was the largest participant with a market share of 54% in 2025, as the management of temples and corporate pilgrimage services became professional.

- 6 million devotees were registered in Kashi (Varanasi), and 79,154 temples are located in Tamil Nadu and 77,283 temples in Maharashtra.

- Sanctions Swadesh darshan 2.0 46 PRASHAD projects worth USD 200 million have been sanctioned by the government by January 2024 and 57 destinations have been included.

Significant Growth Factors

- Deep Cultural-Spiritual Roots and Diverse Religious Heritage:

This puts India in a special niche of having the birth and spiritual homeland of most of the major world religions, giving rise to a distinct religious tourism ecosystem unparalleled anywhere on the planet with Hinduism, Buddhism, Jainism, and Sikhism rooted in Indian soil and Islam and Christianity having long histories of presence establishing unparalleled diversity of religious sites, pilgrimage rituals, and spiritual experiences that draw domestic and international pilgrims. Statistics from 2024 recorded an estimated population of 1.1 billion, or 110 crores of people as Hindu in India which makes Hinduism a predominant religion, and India has around 94% of the total population of Hinduism making it a significant cultural and religious force in the world, with about 3.22 crore people practicing Christianity, and high numbers of Muslims, Sikhs, Buddhists, and Jains also contributing to the religious pluralism that defines and establishes the national identity.

Religious tourism is a significant part of the entire tourism business in India with 60% of the domestic tourists taking part in religious tourism and this shows that religious tourism is not a niche sector but rather a core area of overall tourism business and this phenomenal penetration aspect of religious practice and pilgrimage within the Indian cultural consciousness cuts across socio-economic lines as well as geographical borders. The growing religious tourism of areas such as Puri, Varanasi, Tirupati and Shirdi is an important element that greatly contributes to the growth of the market as well as the fact that cities such as Puri and Varanasi are offering more than the traditional spiritual experience and thus contribute to helping people revive through yoga retreats and Ayurvedic Spas and hence the integration of ancient practices and modern wellness tourism trends.

Tamil Nadu contains 79,154 temples and Maharashtra contains 77,283 temples, with its sacred geography being concentrated, providing pilgrimage loops between numerous temples to the same area with a local cluster of temples providing economic spillovers to the overall economy beyond direct tourist spending. India is also the land of many famous religious and spiritual destinations such as Golden Temple in Amritsar, Varanasi ghats on Ganges River, Vaishno Devi shrine in Jammu, Tirupati Balaji in Andhra Pradesh, Meenakshi Temple in Madurai and recently opened Ram Mandir in Ayodhya that hosts millions of visitors a year, and also the Buddhist pilgrims come in large numbers to the country especially Thailand, Japan, Sri Lanka and Myanmar with Buddha related sites such as Bodh Gaya where Kumbh Mela is the largest religious congregation in the world and has been conducted in India such that millions of worshipers occupying 49 days have attended it and demonstrated an incredible level of Indian religious celebrations with huge economic impact through accommodation and transport services, food services and religious offerings, and the organizational ability to handle thousands of visitors at once with sanitation, security and infrastructure to support millions of pilgrims.

- Government Infrastructure Investment and Development Initiatives:

Government strategic investments in religious tourism infrastructure through special schemes such as PRASHAD (Pilgrimage Rejuvenation and Spiritual Heritage Augmentation Drive) and Swadesh Darshan 2.0 are critical growth drivers and investment in Infrastructure is made to improve connectivity, accommodation structure, visitor amenities, heritage conservation, and digital infrastructure of major pilgrimage spots to change visitor experience and capacity to receive increasing numbers of tourists. As of January 2024, the Ministry of Tourism approved 46 PRASHAD-programme projects which had a total value of USD 200 million and the projects included the development of facilities in pilgrimage locations, heritage conservation, visitor information centers, parking facilities, illumination and landscaping, and digital connectivity to ensure that pilgrimage sites were able to match up with modern tourist expectations without losing the spiritual essence and heritage that attracted both domestic and foreign visitors.

In the Swadesh Darshan 2.0 scheme introduced with the objective of developing sustainable and responsible tourism 57 destinations have been noted, with major religious tourism destinations receiving investments that have enhanced infrastructure, local culture, and the enhanced tourism experience through holistic development which has addressed bottlenecks in transportation, shortage of accommodation, lack of sanitation facilities, and lack of visitor services, which were major constraints in the past that limited the capacity and comfort of pilgrimage sites. Kashi (Varanasi) saw the influx of tourists with 72.6 million visitors in 2025 after heavy development projects including the Kashi Vishwanath Corridor and ghat redevelopment projects, made accessibility and visitor experience of the temple easy. The ghats were restored, more navigation infrastructure was built, and increased lighting, cleanliness campaigns and cultural programming were implemented to make the place an international pilgrimage destination and retain its sacred nature to attract both devout pilgrims and heritage tourists.

The world’s highest statue at the site in Gujarat, the Statue of Unity, is 182 meters in honor of Sardar Vallabhbhai Patel, the Statue of Unity has become a major tourist attraction with 2.9 million visitors in annual statistics since its inauguration in 2018, and has proven the ability of monumental-religious-cultural landmarks to produce tourism economic impacts both through direct visitor expenditure and indirect impacts of fostering development of a given tourist ecosystem, such as hotels, transportation networks, and other ancillary services. Industry reports show that in 2022, the religious tourism market in India registered revenue of USD 16,380 million, a huge growth compared to USD 8,600 million in 2021, and is a sign of post-pandemic recovery as pilgrimage was again undertaken with pent-up demand, infrastructure development driving more and more pilgrimage journeys, and a rise in disposable incomes allowing more frequent and costlier pilgrimage journeys than previously seen in the industry due to the pandemic.

The Digital India project enhancing 3G connections and smartphone adoption empowers pilgrims who can access information, make advance bookings, spend using digital payment solutions, and share their experiences using social media, and online platforms can democratize access to pilgrimage planning resources that were previously monopolized by travel agents and can allow direct booking of accommodations, transportation, and tour guides reducing the cost of intermediaries and enhancing the level of transparency which benefits price-sensitive domestic pilgrims.

What are the Major Advances Changing the India Religious Tourism Market Today?

- Organized Sector Professionalization and Premium Service Development:

The shift of unorganized and fragmented service provision into the organized professionally managed tour operator and hospitality providers is a form of transformative market development, with organized sector taking 54% of the market share in 2025 through corporate entities, temple trusts, and specialized pilgrimage companies offering standardized and quality assured services at premiums to appeal to middle-class and affluent pilgrims willing to pay premiums for convenience, comfort, and reliability. The present pilgrimage tour operators offer full services such as transportation in the form of AC bus service or train services, good accommodation in the form of budget hotels or even luxury hotels, and sightseeing of their temples by including hopping queues in addition to the fact that they can arrange for them to eat vegetarian food and discourses by spiritual scholars and cultural programming that develops them to be holistic experiences instead of just visiting hotels and doing arrangements for travelling.

The rising availability of better-off pilgrims that seek high quality experiences facilitates the demand for premium products such as helicopters to inaccessible shrines such as Vaishno Devi, luxury train rides on the Buddhism circuit visiting various holy places, five star heritage hotels around major temples and exclusive access arrangements that would evade crowds during peak seasons and willing to pay extra to experience the products, which also creates a good market niche that hospitality industry investments calculating only on leisure tourism cannot afford. Temple trusts and religious institutions are becoming more professional with the appointment of trained administrators, the introduction of digital queue management systems, online donation systems, visitor information centers and branded accommodation facilities to provide consistent quality even as the temple operations continue to generate revenue beyond traditional donation-driven fundraising models. An example of professional religious institution management is the Tirumala Tirupati Devasthanams, which manages the Lord Venkateswara temple in Tirupati, with an annual budget of over USD 1 billion, extensive real estate, educational institutions, and well-organized darshan systems for 60,000-100,000 daily visitors during peak seasons through advanced crowd management, online booking modules, and a wide variety of accommodation facilities including free choultries up to the high end guesthouses.

- Digital Platforms and Online Booking Revolution:

The introduction of specific online religious tourism websites and booking systems and the integration of religious sites within regular online travel agents changes booking habits, with online bookings allowing pilgrims to research their destinations, compare prices, read reviews, and book entire packages and pay upfront costs without any lawyers or middlemen present in the marketplace being needed, fixing information asymmetry and the business model of these operators, whose closed systems exacerbated the situation to inflate costs and restrict options.

Tourism websites such as Yatra.com, MakeMyTrip, and religious tourism portals with pilgrimage sections have dedicated pilgrimage sections providing pilgrims with the ability to make informed decisions when booking complete journeys through single interfaces, provide packages to pilgrimage destinations, have temple calendars displaying dates and auspicious timings of festivals, have virtual darshan to worship at a distance, have donation options, and have guides to destinations giving pilgrims detailed information about their chosen destinations. They consolidate complex pilgrimage circuits that involve multiple destinations in multiple states. Online booking claimed 47% market share in 2025 as it became common among older pilgrims who are not so technologically savvy but are becoming increasingly more dependent on smartphone applications to fulfill religious services such as temple live darshans, accommodation booking, and access to spiritual content, and with easy-to-use interfaces in local languages and assisted booking services enabled older pilgrims and rural pilgrims were able to experience the convenience of online booking and competitive prices.

The COVID-19 pandemic shifted towards digital transformation with temples shutting down physical access but also providing virtual darshans via live streaming platforms, online offering boxes being replaced with online payment systems and e-prasad delivery services bringing the blessings to the homes of the devotees, and the digital transformations continuing beyond the pandemic as a complement to a physical pilgrimage, not as an alternative to a physical offering box. By documenting pilgrimage experiences in social media influencers and religious content creators, organic marketing appeals to younger demographics, and visually appealing posts featuring architectural beauty, cultural richness, and spiritual atmosphere attract heritage tourists and spiritual seekers outside of traditional religious demographics and the user-generated content offers authentic views, which builds trust and inspires travel decisions in digitally native millennials and Gen Z cohorts representing the growth segment of the future.

- Infrastructure Connectivity and Regional Accessibility Improvements:

Massive development of transport infrastructure such as new airports in and around pilgrimage sites, highway construction, modernization of railway networks and especially pilgrimage trains, makes access much easier cutting down travel times, making their journeys more comfortable, and making previously challenging pilgrimages possible for elderly pilgrims, family pilgrims and first time pilgrims scared of the traditional routes. The Kedarnath helicopter services can be used to illustrate a change in accessibility where the cost of accessing the shrine by helicopter has transformed the pilgrimage practices that used to require a number of days walking to reach the remote Himalayan shrine at 3,583 meters in altitude where access was limited to only the wealthy pilgrims but the cost of helicopter services (INR 5,000-8,000 per person) restricts access to the pilgrims on a tight budget but still fulfilling the role of spiritual pilgrimage by making pil The development of regional airports in the areas around major pilgrimage sites such as expanded facilities at Varanasi, a new terminal at Ayodhya, and better connectivity to pilgrimage towns allows direct flights between major cities eliminating time-consuming surface travel especially for international tourist travelers and domestic visitors of remote areas whose visits to pilgrimage sites can now be made once a week without the weeks of planning and time commitments necessary with long-range travel.

The Char Dham highway project enhancing accessibility of the four Hindu holy places in Uttarakhand shows the effect of infrastructure, wherein all-weather roads have been put in place to replace the narrow and dangerous mountain routes, reducing the time taken in the journey, increasing safety, and increasing the ability to ride comfortably by bus where only hardy travelers previously ventured onto hazardous mountain roads, with the result of the infrastructure projects set to double pilgrim numbers currently at 3-4 million to 6-8 million per year when the project is finished and pilots the pilgrimage season past the Specially designed pilgrimage trains such as the Buddhist circuit tourist train, the Ramayana Express visiting sites related to Lord Rama and the Bharat Gaurav trains with religious tours with thematic trains create an easy affordable group travelling option where pilgrims are offered tours and onboard meals and organizing visits to temples without having to worry about the logistics of traveling to religious sites which creates a feeling of unity in the community by sharing their spiritual journey.

- International Buddhist Tourism and Heritage Integration:

The Buddhist heritage sites of India are experiencing increasing international visitation especially by East and Southeast Asian countries which are predominantly Buddhist with government efforts targeting the country as the key Buddhist pilgrimage site through infrastructure development, international marketing and visa facilitation of foreign markets with the capitalization of historical ties in addition to diversifying tourism through alternatives to domestic Hindu pilgrimage markets which generate high foreign exchange earnings. The Buddhist Circuit of key sites such as Bodh Gaya where Buddha was enlightened, Sarnath where the first sermon was given, Kushinagar where Mahaparinirvana was achieved, and Lumbini where Buddha was born in neighboring Nepal, is given a special development focus with Swadesh Darshan scheme investments enhancing the development of facilities, interpretation centers and pilgrim amenities to international standards attracting high-spending foreign tourists to spend long and buy souvenirs, making them high economic contributors.

Tourism statistics also suggest that Buddhist pilgrims in Thailand and Japan, Sri Lanka, Myanmar, South Korea, and Taiwan constitute large sources of international visitor markets, with these visitors often opting to visit multiple sacred sites during 7-14 day periods, booking either mid-range or high-end accommodations, and spending on guided tours and retreats to do meditative practices as well as religious offerings that generate per-tourist income that is way beyond the average domestic pilgrim spending and now create a viable market niche that warrants further infrastructure investments and international promotion efforts. The Dalai Lama in Dharamshala is a key site that draws Tibetan Buddhist pilgrims and spiritual seekers from around the world making McLeod Ganj their international Buddhist center where they can get teachings, meditation and culture that combines religious pilgrimage with experiential tourism where visitors get an in-depth experience of Buddhist philosophy, practices and culture that they find more rewarding than superficial site visits that many wellness tourism segments globally consider as alternative and supplemental to their wellness tourism.

Category Wise Insights

By Religion Type

Why Hinduism Dominates?

With 1.1 billion followers, 94% of the global Hindu population, 68% market share, and the far-off sacred geography of 79,154 temples in Tamil Nadu alone; major pilgrimage centers like Varanasi with 72.6M visitors in 2025, and the extremely strong endemic pilgrimage practices, such as Char Dham Yatra, Kumbh Mela with 240M pilgrims, and regional temple festivals generating year-long religious tourism activity in all states, Hinduism dominated the markets.

By Sector Type

Why Organised Sector Leads?

In 2025, 54% of the market was captured by the organised sector due to the professionalization of the temple management, corporate tour operators who offer premium tours, the middle-class population that demands quality services and professional hospitality chains that entered the interest of religious tourism with branded accommodation close to pilgrimage centres to provide consistent services to pilgrims opting to visit the sacred sites due to convenience and not necessarily low-cost services.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 223.55 billion |

| Projected Market Size in 2035 | USD 441.19 billion |

| Market Size in 2025 | USD 202.85 billion |

| CAGR Growth Rate | 8.08% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Religion Type, Sector Type, Tourism Type, Booking Channel, End User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Top Players in the Market

- Thomas Cook (India) Limited

- MakeMyTrip (India) Private Limited

- Cleartrip Private Limited

- Easy Trip Planners Pvt. Ltd.

- Yatra Online Ltd.

- Indian Railway Catering and Tourism Corporation Ltd.

- Expedia Online Travel Services India Private Limited

- Le Travenues Technology Limited

- Mahindra Holidays & Resorts India Limited

- Holiday Triangle Travel Private Limited

- Others

Key Developments

- In November 2024: 46 PRASHAD projects worth USD 200 million were approved by the Ministry of Tourism to ameliorate facilities in major pilgrimage sites in the country.

- In January 2026: Kashi boasted 72.6M worshipers in 2025 after the massive expansion of infrastructure with Kashi Vishwanath Corridor.

The India Religious Tourism Market is segmented as follows:

By Religion Type

- Hinduism

- Islam

- Sikhism

- Buddhism

- Christianity

- Other Religions

By Sector Type

- Organised

- Unorganised

By Tourism Type

- Pilgrimages

- Religious & Heritage Tours

- Day Trips & Local Getaways

- Spiritual Retreats

By Booking Channel

- Online Booking

- Phone Booking

- In-Person Booking

By End User

- Domestic Pilgrims

- International Tourists

- Spiritual Seekers

- Tour Operators

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. India Religious Tourism by Segments

- 2.1.2. India Religious Tourism by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. India Religious Tourism Market Attractiveness Analysis, By Religion Type

- 2.2.3. India Religious Tourism Market Attractiveness Analysis, By Sector Type

- 2.2.4. India Religious Tourism Market Attractiveness Analysis, By Tourism Type

- 2.2.5. India Religious Tourism Market Attractiveness Analysis, By Booking Channel

- 2.2.6. India Religious Tourism Market Attractiveness Analysis, By End User

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Deep Cultural-Spiritual Roots and Diverse Religious Heritage

- 3.1.2. Deep Cultural-Spiritual Roots and Diverse Religious Heritage

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. India Religious Tourism Market – By Religion Type

- 4.1. Religion Type Market Overview, By Religion Type Segment

- 4.1.1. India Religious Tourism Market Revenue Share, By Religion Type, 2025 & 2035

- 4.1.2. Hinduism

- 4.1.3. India Religious Tourism Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Islam

- 4.1.7. India Religious Tourism Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Sikhism

- 4.1.11. India Religious Tourism Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Buddhism

- 4.1.15. India Religious Tourism Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Christianity

- 4.1.19. India Religious Tourism Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Other Religions

- 4.1.23. India Religious Tourism Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Religion Type Market Overview, By Religion Type Segment

- Chapter 5. India Religious Tourism Market – By Sector Type

- 5.1. Sector Type Market Overview, By Sector Type Segment

- 5.1.1. India Religious Tourism Market Revenue Share, By Sector Type, 2025 & 2035

- 5.1.2. Organised

- 5.1.3. India Religious Tourism Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Unorganised

- 5.1.7. India Religious Tourism Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Sector Type Market Overview, By Sector Type Segment

- Chapter 6. India Religious Tourism Market – By Tourism Type

- 6.1. Tourism Type Market Overview, By Tourism Type Segment

- 6.1.1. India Religious Tourism Market Revenue Share, By Tourism Type, 2025 & 2035

- 6.1.2. Pilgrimages

- 6.1.3. India Religious Tourism Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Religious & Heritage Tours

- 6.1.7. India Religious Tourism Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Day Trips & Local Getaways

- 6.1.11. India Religious Tourism Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Spiritual Retreats

- 6.1.15. India Religious Tourism Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Tourism Type Market Overview, By Tourism Type Segment

- Chapter 7. India Religious Tourism Market – By Booking Channel

- 7.1. Booking Channel Market Overview, By Booking Channel Segment

- 7.1.1. India Religious Tourism Market Revenue Share, By Booking Channel, 2025 & 2035

- 7.1.2. Online Booking

- 7.1.3. India Religious Tourism Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Phone Booking

- 7.1.7. India Religious Tourism Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. In-Person Booking

- 7.1.11. India Religious Tourism Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Booking Channel Market Overview, By Booking Channel Segment

- Chapter 8. India Religious Tourism Market – By End User

- 8.1. End User Market Overview, By End User Segment

- 8.1.1. India Religious Tourism Market Revenue Share, By End User, 2025 & 2035

- 8.1.2. Domestic Pilgrims

- 8.1.3. India Religious Tourism Share Forecast, By Region (USD Billion)

- 8.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.5. Key Market Trends, Growth Factors, & Opportunities

- 8.1.6. International Tourists

- 8.1.7. India Religious Tourism Share Forecast, By Region (USD Billion)

- 8.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.9. Key Market Trends, Growth Factors, & Opportunities

- 8.1.10. Spiritual Seekers

- 8.1.11. India Religious Tourism Share Forecast, By Region (USD Billion)

- 8.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.13. Key Market Trends, Growth Factors, & Opportunities

- 8.1.14. Tour Operators

- 8.1.15. India Religious Tourism Share Forecast, By Region (USD Billion)

- 8.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.17. Key Market Trends, Growth Factors, & Opportunities

- 8.1. End User Market Overview, By End User Segment

- Chapter 9. India Religious Tourism Market – Regional Analysis

- 9.1. India Religious Tourism Market Overview, By Region Segment

- 9.1.1. India Religious Tourism Market Revenue Share, By Region, 2025 & 2035

- 9.1.2. India Religious Tourism Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 9.1.3. India Religious Tourism Market Revenue, By Religion Type, 2026 – 2035

- 9.1.4. India Religious Tourism Market Revenue, By Sector Type, 2026 – 2035

- 9.1.5. India Religious Tourism Market Revenue, By Tourism Type, 2026 – 2035

- 9.1.6. India Religious Tourism Market Revenue, By Booking Channel, 2026 – 2035

- 9.1.7. India Religious Tourism Market Revenue, By End User, 2026 – 2035

- 9.1. India Religious Tourism Market Overview, By Region Segment

- Chapter 10. Competitive Landscape

- 10.1. Company Market Share Analysis – 2025

- 10.1.1. India Religious Tourism Market: Company Market Share, 2025

- 10.2. India Religious Tourism Market Company Market Share, 2024

- 10.1. Company Market Share Analysis – 2025

- Chapter 11. Company Profiles

- 11.1. Thomas Cook (India) Limited

- 11.1.1. Company Overview

- 11.1.2. Key Executives

- 11.1.3. Product Portfolio

- 11.1.4. Financial Overview

- 11.1.5. Operating Business Segments

- 11.1.6. Business Performance

- 11.1.7. Recent Developments

- 11.2. MakeMyTrip (India) Private Limited

- 11.3. Cleartrip Private Limited

- 11.4. Easy Trip Planners Pvt. Ltd.

- 11.5. Yatra Online Ltd.

- 11.6. Indian Railway Catering and Tourism Corporation Ltd.

- 11.7. Expedia Online Travel Services India Private Limited

- 11.8. Le Travenues Technology Limited

- 11.9. Mahindra Holidays & Resorts India Limited

- 11.10. Holiday Triangle Travel Private Limited

- 11.11. Others.

- 11.1. Thomas Cook (India) Limited

- Chapter 12. Research Methodology

- 12.1. Research Methodology

- 12.2. Secondary Research

- 12.3. Primary Research

- 12.3.1. Analyst Tools and Models

- 12.4. Research Limitations

- 12.5. Assumptions

- 12.6. Insights From Primary Respondents

- 12.7. Why Custom Market Insights

- Chapter 13. Standard Report Commercials & Add-Ons

- 13.1. Customization Options

- 13.2. Subscription Module For Market Research Reports

- 13.3. Client Testimonials

List Of Figures

Figures No 1 to 34

List OF Tables

Tables No 1 to 2

Prominent Player

- Thomas Cook (India) Limited

- MakeMyTrip (India) Private Limited

- Cleartrip Private Limited

- Easy Trip Planners Pvt. Ltd.

- Yatra Online Ltd.

- Indian Railway Catering and Tourism Corporation Ltd.

- Expedia Online Travel Services India Private Limited

- Le Travenues Technology Limited

- Mahindra Holidays & Resorts India Limited

- Holiday Triangle Travel Private Limited

- Others

FAQs

The key players in the market are Thomas Cook (India) Limited, MakeMyTrip (India) Private Limited, Cleartrip Private Limited, Easy Trip Planners Pvt. Ltd., Yatra Online Ltd., Indian Railway Catering and Tourism Corporation Ltd., Expedia Online Travel Services India Private Limited, Le Travenues Technology Limited, Mahindra Holidays & Resorts India Limited, Holiday Triangle Travel Private Limited, and Others.

Government projects such as the PRASHAD scheme that supports infrastructure, temple management laws that ensure transparency, heritage conservation laws that protect holy sites, visa facilitation of Buddhist pilgrims, and the tourism development policies that are prioritized to religious circuits provide an enabling environment when Digital India enhances accessibility in pilgrimage planning through a democratic way of planning.

Varied prices of budget (free temple stays), premium (helicopter services INR 5,000-8,000), and disorganized sectors can be offered at prices that the organised sector can charge higher (convenience) and the unorganized sector can charge lower (price-sensitive pilgrims), which forms a market that can support the growth.

USD 441.19B by FY2032 at 8.08% CAGR due to infrastructure development, professionalization of the organized sector, online transformation, the expansion of international tourist destinations of Buddhism, and an increase in the wealthy pilgrim segment seeking premium experiences.

Hinduism controls 68% of the market share based on 1.1B followers, 79,154 temples in Tamil Nadu alone, principal hubs such as Varanasi (72.6M visitors) and Tirupati (60,000-100,000 daily), and cultural pilgrimage customs ingrained in socioeconomic classes.

Extensive cultural-spiritual roots with 60 of domestic tourism being religious, government investment in PRASHAD (USD 200M, 46 projects) and Swadesh Darshan 2.0 (57 destinations), increased disposable incomes, adoption of digital platforms (47% online booking share), infrastructure expansion that cut down on travel times and a 1.1B Hindu population generating colossal domestic demand.