Open Process Automation Systems Market Size, Trends and Insights By Component (Hardware, Software, Services), By Deployment Type (On-Premises, Cloud-Based), By Architecture (Open Distributed Control Systems (DCS), Modular Control Systems, Interoperable Automation Platforms), By Industry Vertical (Oil & Gas, Chemicals, Power Generation, Pharmaceuticals, Manufacturing), By Application (Process Control, Asset Management, Plant Optimization, Industrial Monitoring), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 8.5%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | North America |

| Largest Market: | Asia Pacific |

Major Players

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Emerson Electric Co.

- Others

Reports Description

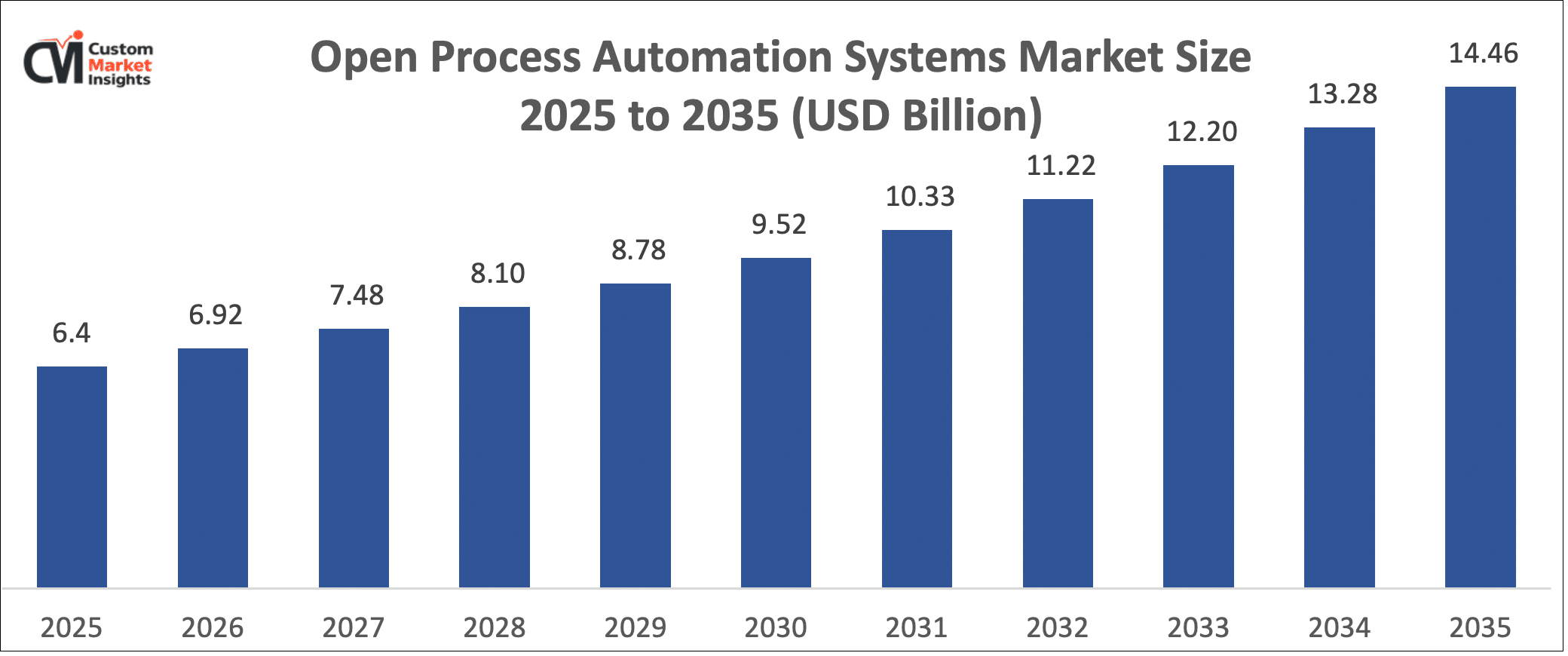

The market size of the Open Process Automation Systems is estimated to grow to USD 6.92 billion by 2026 and is intended to grow to USD 14.46 billion in the year 2035 at a CAGR of 8.5% in the 2026-2035 forecast period. The market is growing with the increasing use of open, interoperable, and vendor-neutral automation systems within industries to enhance adaptability and efficiency as well as the scalability of industrial activity. The increasing pressure to modernize control systems of the past, minimize vendor lock-in, and enhance cybersecurity in industries like oil and gas, power generation, chemicals, and manufacturing is stimulating the growth of the market. Moreover, the further development of industrial IoT (IIoT), cloud computing-based automation systems, and Industry 4.0 technologies and the investments in digital transformation and smart manufacturing will also contribute to the increased growth of the market.

Market Highlight

- In 2025, North America occupied a substantial part of the Open Process Automation Systems Market because of the early adoption of the open automation standards and the powerful investments in industrial digitalization.

- The CAGR of Asia Pacific is projected to be the highest in the period between 2026 and 2035 due to the high rates of industrialization and the growing interest in the use of Industry 4.0 technologies.

- On a Component basis, the hardware market segment prevailed in 2025 as its usage of controllers, networking equipment, and field devices is high, whereas the software market segment is projected to increase steadily with the demand for analytics and automation platforms.

- On-premises systems had the highest percentage in 2025 by Deployment Type when compared to cloud-based deployment, but the latter is expected to increase because of the need to place more value on remote monitoring and digital integration.

- Through Architecture, open distributed control systems (DCS) had a significant portion in 2025 due to the flexibility of the automation and the interoperability.

- In Industry Vertical, oil and gas conquered the market in 2025 because of strong dependence on the higher automation systems.

- Application and process control recorded the highest share in 2025 with asset management and plant optimization projected to increase in the period of forecast.

Significant Growth Factors

The emerging trend of the Open Process Automation Systems Market is tightly connected with the increasing popularity of open, interoperable automation systems, the escalating trend of the modernization of old industrial automation systems, and the rise in attention to digitalization, cybersecurity, and efficiency of operations among process industries.

- Updating Work Systems With Previous Industrial Automation: A large number of industrial systems are moving towards open, vendor-neutral automation architectures to enhance flexibility, interoperability, and lifecycle management. With open process automation, the organization is able to have multi-vendor solutions and upgrade without replacing the entire infrastructure. As an example, in March 2024, Honeywell detailed improvements in its Experion open automation platform, which is intended to assist industrial operators to modernize old control systems besides enhancing scalability and interoperability between process plants.

- Increase in the Use Of Industry 4.0 and Digital Manufacturing Technologies: fast development of industrial IoT (IIoT), cloud computing and advanced analytics is increasing the adoption pace of the open process automation systems in industries including oil and gas, chemicals, and power generation. The technologies make it possible to analyze data in real-time, predictive maintenance, and visibility in operations. By way of example, in September 2023, Siemens unveiled the improvements of its industrial automation and digitalization solutions in the interest of the manufacturing and process industries to assist in creating an open and interoperable process automation environment.

The Major Innovations That Are Transforming the Open Process Automation Systems Market Of the Modern World

- Application of Open and Interoperable Automation Platforms: Companies are also inventing open automation platforms that allow easy integration of inter-vendor equipment, software and control systems to industrial plants. These environments help to increase flexibility, scalability, and lifecycle and reduce vendor lock-in. Schneider Electric, as an example, announced in June 2023 that it had introduced enhancements to its EcoStruxure Automation Expert, an open and software-defined automation platform that supports industrial control applications and automation systems and makes it interoperable by engaging interoperable hardware.

- Process Automation using AI and Intense Analytics: AI, machine learning, and data analytics are transforming the sphere of industrial automation as they will enable predictive maintenance, process optimization, and real-time awareness of the processes. The technologies assist industries to identify something going wrong very early, minimize downtime, and increase productivity in complex manufacturing and processing settings. In October 2024, ABB declared new artificial intelligence-based features in its industrial automation systems, allowing the industry to monitor, perform predictive maintenance, and make decisions about the processes using data.

- Digital and Software-Defined Automation Architectures: The transition to digital manufacturing and Industry 4.0 is prompting business enterprises to create software-defined automation systems that decouple hardware with control software and enable more flexible and modular automation systems. Emerson launched the updates to its DeltaV distributed control system in March 2024, which is implemented to operate in the environment of modern and open automation and enhance the connectivity between industrial devices, analytics platforms, and control applications.

Category Wise Insights

By Component

Why Hardware is becoming the Market Leader?

The hardware portion will be the leading market structure of the Open Process Automation Systems Market in 2025. The primary causes of this growth are the growing use of industrial controllers, edge devices, networking devices, sensors, and field instruments, which comprise the physical base of open automation systems. The industries are replacing the legacy control infrastructure with new hardware that meets open standards and interoperability to ensure smooth communication between devices of different vendors. In the meantime, the software segment should increase at a high rate over the forecast period as industries will use the innovative analytics platform, AI-assisted automation tools, and digital control software. Services segment such as system integration, maintenance and consulting is also gaining ground since organizations need specialized services to add and operate open automation environments.

By Deployment Type

The reason why On-Premises Systems are dominating the market?

It is estimated that in 2025, on-premises deployment will take over the market since most industrial facilities choose localized control systems as a way of maintaining operation security, reliability, and adherence to stringent industrial regulations. These systems enable firms to retain complete control over essential automation systems and reduce the cybersecurity threat. Nevertheless, cloud-based implementation will experience high growth in the forecast period because of the growing need in remote monitoring solutions, platform solutions, which operate on a large scale with scalability; and real-time access to data. With the digitization transformation strategies being embraced by the industries, the cloud-based automation solutions are emerging as a promising solution in enhancing the visibility and efficiency of operations.

By Architecture

What is the significance of Open Distributed Control Systems?

It is anticipated that Open Distributed Control Systems (DCS) will be a significant portion of the market in 2025 as they offer flexible, scalable, and interoperable automation models enabling the devices and software of several vendors to interoperate. The architecture assists industries to upgrade old automation systems without necessarily overhauling the infrastructure in place. The interest towards modular control systems is also increasing due to the fact that modular control systems allow the organization to improve automation features progressively, which saves money and enhances the flexibility of the system. Moreover, interoperable automation systems are gaining more and more significance with the companies being concerned with open standards, integration of systems, and vendor-neutral automation environments.

By Industry Vertical

Why is the Oil and Gas Sector becoming the market leader?

It is projected that the oil and gas business will rule the market in 2025 because of the high dependence of advanced automation systems to operate the sophisticated exploration, refining, and production processes. Open automation systems enable an operator to be more efficient, safe, and have less downtime. Other significant adopters are the chemicals and power generation industries that need scalable and dependable automation processes to manage the large scale industrial processes. Meanwhile, the pharmaceutical and manufacturing industries are becoming more actively deployed to open automation technologies to promote smart manufacturing, regulatory compliance, and enhanced the efficiency of the processes.

By Application

Why is Process Control Ruling the Market?

The process control division is forecasted to have the highest portion in 2025 as automation systems are actually being employed to oversee and control industrial operations in real-time to maintain a steady output and efficiency. Industries use open automation systems to combine different control systems and streamline production processes. Applications in asset management and plant optimization will also have tremendous growth as companies will employ the use of data analytics, predictive maintenance, and digital monitoring tools to enhance performance and decrease downtime of their equipment. Also, the industrial monitoring applications are growing because companies are concentrating on improving the visibility of operations in large and complicated industrial sites.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 6.92 billion |

| Projected Market Size in 2035 | USD 14.46 billion |

| Market Size in 2025 | USD 6.4 billion |

| CAGR Growth Rate | 8.5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Component, Deployment Type, Architecture, Industry Vertical, Application and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

What Is the Size of the Asia Pacific Market?

The region is one of the fastest-growing markets due to industrial automation, the creation of the manufacturing sector, and an increase in investment in the Industry 4.0 technologies. The area is also migrating towards modernization of the traditional automation systems besides the introduction of the open and interoperable automation systems to improve productivity and efficiency in operations.

Why Does Asia Pacific Control the Market 2025?

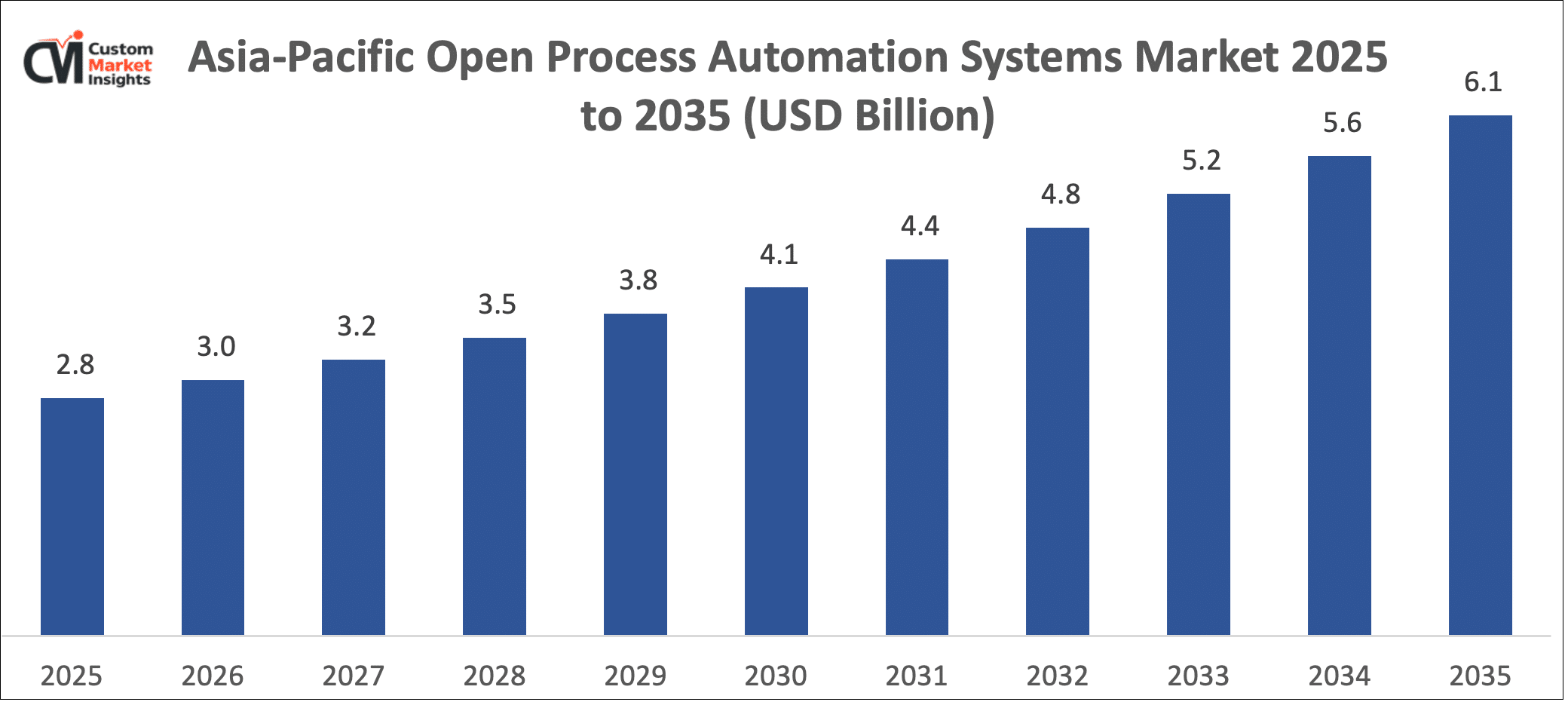

In 2025, nearly 40-45 percent of the global market share was attained in the Asia Pacific, which was made possible by strong industrialization, increasing application of smart manufacturing, and increasing demand for sophisticated automation in the oil and gas, chemicals, and power production sectors. Other emerging markets such as China, Japan, South Korea, and India are also emerging as big investors in the modern automation systems and digital manufacturing systems. In April 2024, an example is the announcement by Siemens of the expansion of its industrial automation and digital manufacturing in the Asia Pacific to play a role in the introduction of open and interoperable technologies of automation to local manufacturing processes.

China Market Trends

China conquers the Asian Pacific market because it possesses significant manufacturing experience and colossal investments into the digitalization and automation technologies of the industry. Modernizing the old factories with the open automation solutions, industrial IoT, and other high-performance process control solutions is also underway to enhance efficiency and competitiveness in the country. In October 2023, Schneider Electric also accelerated the installation of EcoStruxure automation solutions to assist manufacturers in China in integrating open and software-defined automation platforms into smart factory environments.

The Growth of North American Market: What Is It Behaved By?

The market size of the North America Open Process Automation Systems will be on an increasing trend even though it is projected that the average growth in the market will be about 6.0% CAGR in the years between 2026 and 2035 and this is because the region is showing a high interest in digital transformation of industries, cybersecurity, and modernization of the next generation control systems. There is also the presence of large automation companies and high open automation rates in most industries, such as oil and gas, power generation, and pharmaceuticals, which are the key drivers of growth. In May 2024, Honeywell declared fresh features to its Experion automation framework to help open interoperable automation landscapes to the industrial operators in North America.

U.S. Market Trends

The high demand for AI-driven automation systems, predictive maintenance, and industrial internet of things systems that enable open automation structures has been experienced in the U.S. market. The industries are adopting digital technologies to make sure that they deliver productivity and reduce the level of downtime in their operation. Rockwell Automation’s example declared the innovations to its industrial automation and digital transformation solutions in September 2023, and these solutions help manufacturers deploy the open and connected automation environments.

Top Players in the Market and Their Offerings

- ABB Ltd.

- Siemens AG

- Honeywell International Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Rockwell Automation Inc.

- Yokogawa Electric Corporation

- Mitsubishi Electric Corporation

- General Electric Company

- Hitachi Ltd.

- Bosch Rexroth AG

- FANUC Corporation

- Others

Key Developments

Open Process Automation Systems Market has grown tremendously, with large industrial automation vendors, software makers, and technology corporations investing in open and interoperable automation frameworks, digital control systems, and Industry 4.0 innovation to enhance industrial performance, adaptability, and system combination in the process industries.

- Schneider Electric has recently introduced new functions to its EcoStruxure Automation Expert, a software-defined automation platform that can support open and interoperable automation architectures of industries, allowing manufacturers to mix multi-vendor systems and enhance operational flexibility (June 2023).

- ABB In October 2024, ABB unveiled the additional capabilities of its portfolio of industrial automation and digital solutions, which focuses on AI-based monitoring, predictive maintenance, and open system integration to serve the current process automation environment.

All these reveal the growing interest of businesses in open automation systems, higher levels of digital technologies, and interoperable industrial systems in order to maximize operational efficiency, minimize the complexity of the system, and expedite the implementation of next-generation process automation systems.

The Open Process Automation Systems Market is segmented as follows:

By Component

- Hardware

- Software

- Services

By Deployment Type

- On-Premises

- Cloud-Based

By Architecture

- Open Distributed Control Systems (DCS)

- Modular Control Systems

- Interoperable Automation Platforms

By Industry Vertical

- Oil & Gas

- Chemicals

- Power Generation

- Pharmaceuticals

- Manufacturing

By Application

- Process Control

- Asset Management

- Plant Optimization

- Industrial Monitoring

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Open Process Automation Systems by Segments

- 2.1.2. Open Process Automation Systems by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Open Process Automation Systems Market Attractiveness Analysis, By Component

- 2.2.3. Open Process Automation Systems Market Attractiveness Analysis, By Deployment Type

- 2.2.4. Open Process Automation Systems Market Attractiveness Analysis, By Architecture

- 2.2.5. Open Process Automation Systems Market Attractiveness Analysis, By Industry Vertical

- 2.2.6. Open Process Automation Systems Market Attractiveness Analysis, By Application

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Updating Work Systems With Previous Industrial Automation

- 3.1.2. Increase in the Use Of Industry 4.0 and Digital Manufacturing Technologies

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Open Process Automation Systems Market – By Component

- 4.1. Component Market Overview, By Component Segment

- 4.1.1. Open Process Automation Systems Market Revenue Share, By Component, 2025 & 2035

- 4.1.2. Hardware

- 4.1.3. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Software

- 4.1.7. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Services

- 4.1.11. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Component Market Overview, By Component Segment

- Chapter 5. Open Process Automation Systems Market – By Deployment Type

- 5.1. Deployment Type Market Overview, By Deployment Type Segment

- 5.1.1. Open Process Automation Systems Market Revenue Share, By Deployment Type, 2025 & 2035

- 5.1.2. On-Premises

- 5.1.3. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Cloud-Based

- 5.1.7. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Deployment Type Market Overview, By Deployment Type Segment

- Chapter 6. Open Process Automation Systems Market – By Architecture

- 6.1. Architecture Market Overview, By Architecture Segment

- 6.1.1. Open Process Automation Systems Market Revenue Share, By Architecture, 2025 & 2035

- 6.1.2. Open Distributed Control Systems (DCS)

- 6.1.3. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Modular Control Systems

- 6.1.7. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Interoperable Automation Platforms

- 6.1.11. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Architecture Market Overview, By Architecture Segment

- Chapter 7. Open Process Automation Systems Market – By Industry Vertical

- 7.1. Industry Vertical Market Overview, By Industry Vertical Segment

- 7.1.1. Open Process Automation Systems Market Revenue Share, By Industry Vertical, 2025 & 2035

- 7.1.2. Oil & Gas

- 7.1.3. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Chemicals

- 7.1.7. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Power Generation

- 7.1.11. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Pharmaceuticals

- 7.1.15. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Manufacturing

- 7.1.19. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Industry Vertical Market Overview, By Industry Vertical Segment

- Chapter 8. Open Process Automation Systems Market – By Application

- 8.1. Application Market Overview, By Application Segment

- 8.1.1. Open Process Automation Systems Market Revenue Share, By Application, 2025 & 2035

- 8.1.2. Process Control

- 8.1.3. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 8.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.5. Key Market Trends, Growth Factors, & Opportunities

- 8.1.6. Asset Management

- 8.1.7. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 8.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.9. Key Market Trends, Growth Factors, & Opportunities

- 8.1.10. Plant Optimization

- 8.1.11. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 8.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.13. Key Market Trends, Growth Factors, & Opportunities

- 8.1.14. Industrial Monitoring

- 8.1.15. Open Process Automation Systems Share Forecast, By Region (USD Billion)

- 8.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 8.1.17. Key Market Trends, Growth Factors, & Opportunities

- 8.1. Application Market Overview, By Application Segment

- Chapter 9. Open Process Automation Systems Market – Regional Analysis

- 9.1. Open Process Automation Systems Market Overview, By Region Segment

- 9.1.1. Global Open Process Automation Systems Market Revenue Share, By Region, 2025 & 2035

- 9.1.2. Global Open Process Automation Systems Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 9.1.3. Global Open Process Automation Systems Market Revenue, By Component, 2026 – 2035

- 9.1.4. Global Open Process Automation Systems Market Revenue, By Deployment Type, 2026 – 2035

- 9.1.5. Global Open Process Automation Systems Market Revenue, By Architecture, 2026 – 2035

- 9.1.6. Global Open Process Automation Systems Market Revenue, By Industry Vertical, 2026 – 2035

- 9.1.7. Global Open Process Automation Systems Market Revenue, By Application, 2026 – 2035

- 9.2. North America

- 9.2.1. North America Open Process Automation Systems Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.2.2. North America Open Process Automation Systems Market Revenue, By Component, 2026 – 2035

- 9.2.3. North America Open Process Automation Systems Market Revenue, By Deployment Type, 2026 – 2035

- 9.2.4. North America Open Process Automation Systems Market Revenue, By Architecture, 2026 – 2035

- 9.2.5. North America Open Process Automation Systems Market Revenue, By Industry Vertical, 2026 – 2035

- 9.2.6. North America Open Process Automation Systems Market Revenue, By Application, 2026 – 2035

- 9.2.7. U.S. Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.8. Canada Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.9. Mexico Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.2.10. Rest of North America Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.3. Europe

- 9.3.1. Europe Open Process Automation Systems Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.3.2. Europe Open Process Automation Systems Market Revenue, By Component, 2026 – 2035

- 9.3.3. Europe Open Process Automation Systems Market Revenue, By Deployment Type, 2026 – 2035

- 9.3.4. Europe Open Process Automation Systems Market Revenue, By Architecture, 2026 – 2035

- 9.3.5. Europe Open Process Automation Systems Market Revenue, By Industry Vertical, 2026 – 2035

- 9.3.6. Europe Open Process Automation Systems Market Revenue, By Application, 2026 – 2035

- 9.3.7. Germany Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.8. France Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.9. U.K. Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.10. Russia Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.11. Italy Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.12. Spain Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.13. Netherlands Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.3.14. Rest of Europe Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.4. Asia Pacific

- 9.4.1. Asia Pacific Open Process Automation Systems Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.4.2. Asia Pacific Open Process Automation Systems Market Revenue, By Component, 2026 – 2035

- 9.4.3. Asia Pacific Open Process Automation Systems Market Revenue, By Deployment Type, 2026 – 2035

- 9.4.4. Asia Pacific Open Process Automation Systems Market Revenue, By Architecture, 2026 – 2035

- 9.4.5. Asia Pacific Open Process Automation Systems Market Revenue, By Industry Vertical, 2026 – 2035

- 9.4.6. Asia Pacific Open Process Automation Systems Market Revenue, By Application, 2026 – 2035

- 9.4.7. China Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.8. Japan Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.9. India Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.10. New Zealand Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.11. Australia Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.12. South Korea Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.13. Taiwan Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.4.14. Rest of Asia Pacific Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.5. The Middle-East and Africa

- 9.5.1. The Middle-East and Africa Open Process Automation Systems Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.5.2. The Middle-East and Africa Open Process Automation Systems Market Revenue, By Component, 2026 – 2035

- 9.5.3. The Middle-East and Africa Open Process Automation Systems Market Revenue, By Deployment Type, 2026 – 2035

- 9.5.4. The Middle-East and Africa Open Process Automation Systems Market Revenue, By Architecture, 2026 – 2035

- 9.5.5. The Middle-East and Africa Open Process Automation Systems Market Revenue, By Industry Vertical, 2026 – 2035

- 9.5.6. The Middle-East and Africa Open Process Automation Systems Market Revenue, By Application, 2026 – 2035

- 9.5.7. Saudi Arabia Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.8. UAE Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.9. Egypt Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.10. Kuwait Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.11. South Africa Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.5.12. Rest of the Middle East & Africa Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.6. Latin America

- 9.6.1. Latin America Open Process Automation Systems Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 9.6.2. Latin America Open Process Automation Systems Market Revenue, By Component, 2026 – 2035

- 9.6.3. Latin America Open Process Automation Systems Market Revenue, By Deployment Type, 2026 – 2035

- 9.6.4. Latin America Open Process Automation Systems Market Revenue, By Architecture, 2026 – 2035

- 9.6.5. Latin America Open Process Automation Systems Market Revenue, By Industry Vertical, 2026 – 2035

- 9.6.6. Latin America Open Process Automation Systems Market Revenue, By Application, 2026 – 2035

- 9.6.7. Brazil Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.6.8. Argentina Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.6.9. Rest of Latin America Open Process Automation Systems Market Revenue, 2026 – 2035 (USD Billion)

- 9.1. Open Process Automation Systems Market Overview, By Region Segment

- Chapter 10. Competitive Landscape

- 10.1. Company Market Share Analysis – 2025

- 10.1.1. Global Open Process Automation Systems Market: Company Market Share, 2025

- 10.2. Global Open Process Automation Systems Market Company Market Share, 2024

- 10.1. Company Market Share Analysis – 2025

- Chapter 11. Company Profiles

- 11.1. ABB Ltd.

- 11.1.1. Company Overview

- 11.1.2. Key Executives

- 11.1.3. Product Portfolio

- 11.1.4. Financial Overview

- 11.1.5. Operating Business Segments

- 11.1.6. Business Performance

- 11.1.7. Recent Developments

- 11.2. Siemens AG

- 11.3. Honeywell International Inc.

- 11.4. Schneider Electric SE

- 11.5. Emerson Electric Co.

- 11.6. Rockwell Automation Inc.

- 11.7. Yokogawa Electric Corporation

- 11.8. Mitsubishi Electric Corporation

- 11.9. General Electric Company

- 11.10. Hitachi Ltd.

- 11.11. Bosch Rexroth AG

- 11.12. FANUC Corporation

- 11.13. Others.

- 11.1. ABB Ltd.

- Chapter 12. Research Methodology

- 12.1. Research Methodology

- 12.2. Secondary Research

- 12.3. Primary Research

- 12.3.1. Analyst Tools and Models

- 12.4. Research Limitations

- 12.5. Assumptions

- 12.6. Insights From Primary Respondents

- 12.7. Why Custom Market Insights

- Chapter 13. Standard Report Commercials & Add-Ons

- 13.1. Customization Options

- 13.2. Subscription Module For Market Research Reports

- 13.3. Client Testimonials

List Of Figures

Figures No 1 to 37

List Of Tables

Tables No 1 to 56

Prominent Player

- ABB Ltd.

- Siemens AG

- Honeywell International Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Rockwell Automation Inc.

- Yokogawa Electric Corporation

- Mitsubishi Electric Corporation

- General Electric Company

- Hitachi Ltd.

- Bosch Rexroth AG

- FANUC Corporation

- Others

FAQs

The key players in the market are ABB Ltd., Siemens AG, Honeywell International Inc., Schneider Electric SE, Emerson Electric Co., Rockwell Automation Inc., Yokogawa Electric Corporation, Mitsubishi Electric Corporation, General Electric Company, Hitachi Ltd., Bosch Rexroth AG, FANUC Corporation, Others.

The open automation technologies are being promoted by government programs, which encourage the implementation of Industry 4.0, smart manufacturing, and industrial cybersecurity. In March 2024, Emerson unveiled modifications to its DeltaV distributed control system that can be used to facilitate contemporary open automation architectures and industrial digitalization endeavors.

Open automation systems have high initial investments in terms of advanced hardware and software as well as integration services. Nevertheless, they have long-term advantages of less downtime, efficiency, and lower maintenance costs. Rockwell Automation in September 2023 introduced new upgraded automation solutions aimed to assist it in flexible and open automation industrial environments.

It is estimated that the Open Process Automation Systems Market will increase to approximately USD 14.46 billion by 2035 and will grow at the rate of approximately 8.5% between the years 2026 and 2035. The increased use of AI-driven automation and digital process control technologies helps the market grow. In October 2024, ABB launched the new AI advanced capabilities in the industrial automation solutions.

The large market share is likely to be witnessed in North America owing to the high prevalence of industrial automation firms and the use of digital transformation technologies. In May 2024, Honeywell announced that it was adding some new features to its Experion automation platform to allow the integration of open and interoperable process automation systems.

It is projected that Asia Pacific will register the highest CAGR in 2026-2035 because of the fast industrialization and rising use of Industry 4.0 and smart technologies in manufacturing. China, Japan, and India are among countries that are putting a lot of money into digital manufacturing. Siemens has also developed its industrial automation systems in the Asian Pacific to facilitate the development of sophisticated digital manufacturing systems in April 2024.

The market of open process automation systems in the world is expanding with the rising demand to automate legacy industrial control systems and reduce vendor lock-in as well as to make automation platforms interoperable. The convergence of the industrial IoT, artificial intelligence, and the development of sophisticated analytics is only enhancing the uptake in the oil and gas, chemicals, and power generation sectors. As an example, in June 2023, Schneider Electric extended the EcoStruxure Automation Expert platform to accommodate open and software-defined automation systems in industries.