Phosphor Bronze Market Size, Trends and Insights By Product Form (Strips & Sheets, Ultra-Thin Precision Strip (< 0.15 mm), Standard Strip (0.15–1.0 mm), Heavy Gauge Sheet (> 1.0 mm), Wires & Rods, Fine Wire (< 1.0 mm diameter), Standard Wire (1.0–5.0 mm diameter), Rods & Bars (> 5.0 mm diameter), Tubes & Pipes, Seamless Phosphor Bronze Tubes, Drawn Phosphor Bronze Tubes, Castings, Sand Castings, Centrifugal Castings, Continuous Castings, Powder, Atomized Phosphor Bronze Powder, Sintered Bronze Powder, Other Product Forms), By Grade (C51000 (5% Sn, Standard Grade), C52100 (6% Sn, High Strength), C52400 (8% Sn, Extra High Strength), C54400 (Phosphor Bronze B, Free-Cutting), Other Grades, C50500 (1.3% Sn, Low Tin), C53400 (Medium Tin, Enhanced Machinability), Specialty and Custom Grades), By Application (Electrical & Electronic Components, Connector Terminals & Contacts, Lead Frames, Spring Contacts & Switch Components, PCB Test Sockets, Bearings & Bushings, Plain Bearings, Flanged Bushings, Thrust Washers, Springs & Connectors, Precision Springs, Electrical Connectors, Relay Components, Marine Hardware, Propeller Shaft Bearings, Marine Fasteners & Fittings, Valve Components, Industrial Fasteners, Musical Instruments, Guitar & Bass Strings, Wind Instrument Components, Other Applications), By End Use Industry (Electrical & Electronics, Consumer Electronics, Telecommunications, Industrial Electronics, Automotive, ICE Powertrain Components, EV High-Voltage Connectors, Body & Chassis Electronics, Industrial Machinery, Bearings & Power Transmission, Hydraulic & Pneumatic Components, Marine, Commercial Shipping, Naval Defense, Offshore Energy, Aerospace & Defense, Consumer Goods, Other End Use Industries), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 5%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | LAMEA |

| Largest Market: | Asia Pacific |

Major Players

- Wieland-Werke AG

- KME Group

- Aurubis AG

- Mitsubishi Shindoh Co. Ltd.

- Others

Reports Description

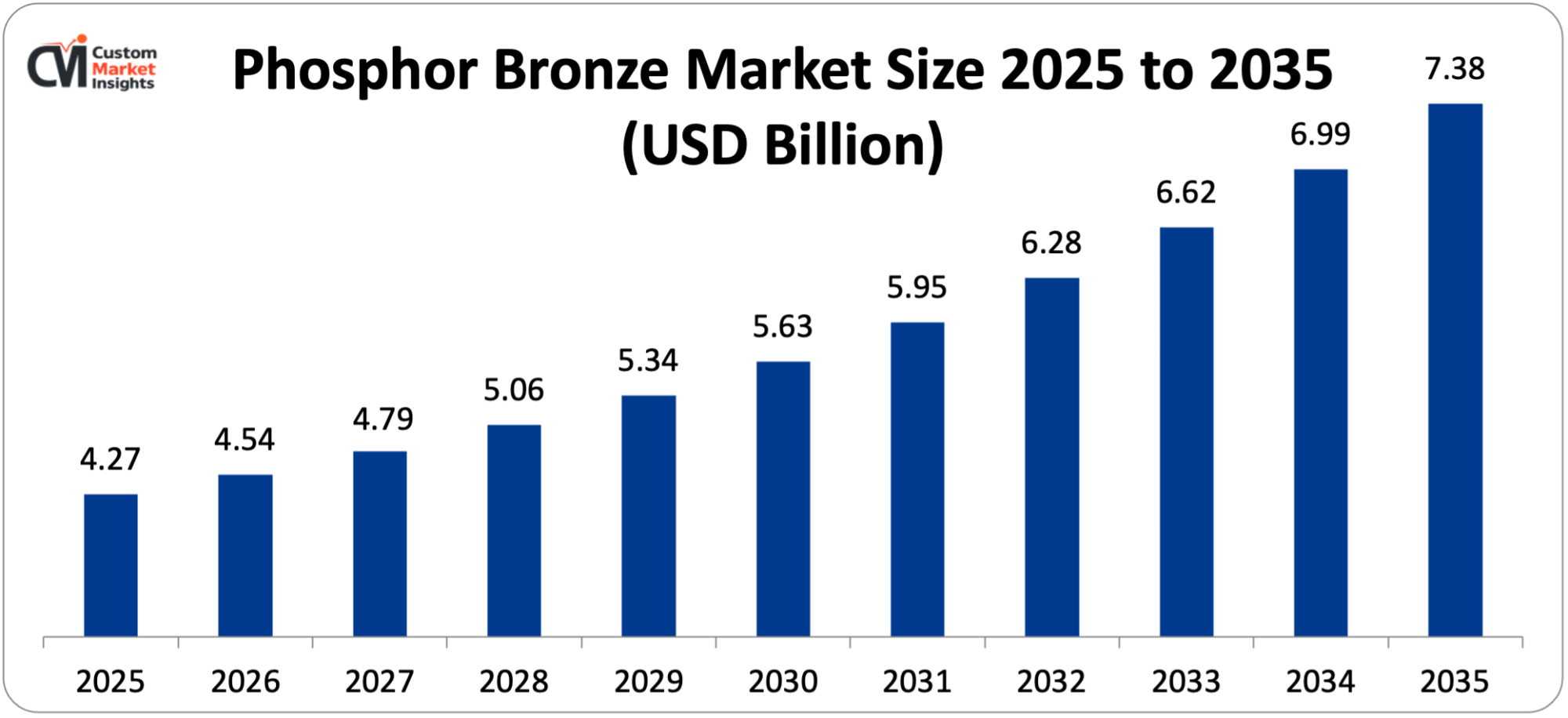

The global phosphor bronze market is estimated at USD 4.27 billion in 2025 and is expected to grow from USD 4.54 billion in 2026 to USD 7.38 billion by 2035, growing at 5% CAGR from 2026 to 2035.

Market Highlight

- Asia Pacific held the largest market share in the phosphor bronze market in 2025, accounting for 52% of the market, owing to the presence of the world’s largest electrical and electronics manufacturing base, the biggest automotive production base, and the largest strip and wire processing industry for phosphor bronze in China, Japan, South Korea, and Taiwan.

- Europe will retain the second highest market share of 21% in 2025, as the automotive component manufacturing, precision engineering and marine equipment sectors are the largest consumers of phosphor bronze in technically challenging applications where certified material specifications are critical.

- In 2025, the strips and sheets accounted for nearly 38% of the market share by product form, which shows that the dominant end markets that consumed the maximum phosphor bronze alloy worldwide were electrical connector manufacturing, lead frame manufacturing, spring contact manufacturing, and precision stamped components manufacturing.

- By form, the wires and rods segment is growing at the highest CAGR (2026–2035) at 5.8%, owing to the increasing end uses of electrical winding wire and telecommunications cable components, as well as the increasing medical device industry demand for precision instruments and components for surgical tools using phosphor bronze wire.

- Electrical and electronic components accounted for the largest market share of 43% in 2025, in application, as connector terminals, lead frames, spring contacts, and precision stamped electrical components were the key application areas for phosphor bronze globally.

- The electrical and electronics industry accounted for the largest share of total market revenue at 46% in 2025, while the automotive industry had the highest CAGR of 6.4% between 2026 and 2035 as a result of the surge in the number of connectors in battery electric and hybrid electric vehicles fueled by electrification.

Impact of Middle East War on Phosphor Bronze Market

There have been increased risks of supply volatility of metals such as copper and tin that are used in the production of phosphor bronze due to the war in the Middle East region. Increased prices of energy and transport have increased the manufacturing expenses of metal alloy producers. Both defense and electronic industries will likely face volatility in the demand for phosphor bronze alloy because of the political uncertainties and slow economies.

Significant Growth Factors

The Phosphor Bronze Market Trends present significant growth opportunities due to several factors:

- Expanding Global Electrical Connector and Electronic Component Manufacturing Driving Structural Phosphor Bronze Demand: The largest aggregate use of phosphor bronze strip and sheet worldwide and the most structurally significant market force pushing growth in the phosphor bronze industry is the steady growth of the manufacture of electrical connectors and electronic components by global manufacturers across all industry sectors, ranging from consumer electronics and automotive to industrial automation, medical devices, and telecommunications infrastructure, driven by the inexorable spread of electronic content in every sector of the global economy. In 2024, the global electrical connector market was valued at nearly USD 88.4 billion and is expected to grow at a 6.1% CAGR, reaching USD 141.7 billion by 2032; phosphor bronze strip is the largest consumed metallic substrate in precision-stamped electrical connector terminals and contact springs in almost all connector formats, from mini board-to-board connectors for smartphones to heavy duty, power connectors for factory automation systems. The combination of these properties (electrical conductivity: 15–20% IACS (International Annealed Copper Standard) – enough to meet the current-carrying requirements for connectors; spring temper (0.2% proof stress 600–800 MPa) – reliable generation of contact force over millions of mating cycles; excellent resistance to atmospheric and industrial corrosion – no atmospheric corrosion and no corrosion in industrial environments; and outstanding formability – precision stamping of complex 3D connector geometries at high production speeds) makes phosphor bronze effectively irreplaceable by alternative materials in most electrical connector terminal applications. As the precision and functional demands of miniaturized contact geometries continue to rise, the transition toward miniaturization in the connector industry has made phosphor bronze stampings increasingly complex but has also provided this industry with a way to continue to use more phosphor bronze per connector. The phone industry alone uses an estimated 10,000-18,000 metric tons of phosphor bronze strip each year for the estimated 1.25 billion smartphones produced globally in 2024, which includes a wide variety of connector and contact components used across the board-to-board, USB, SIM, memory card and speaker connector components. The Internet of Things (IoT) device market – which includes smart home devices, industrial IoT sensors, wearable technology and connected automotive modules – is seeing fast growth in the number of connected devices, estimated at 18.8 billion by 2024 and reaching more than 32 billion by 2030, with each device featuring multiple phosphor bronze connector and spring contact components, driving significant and accelerating growth and incremental demand above the traditional connector market.

- Electric Vehicle Electrification Creating New High-Performance Phosphor Bronze Connector and Busbar Applications: With the rapid global shift toward all-electric and hybrid electric powertrains, a large amount of new demand is being created for phosphor bronze components in high-voltage electrical connectors, battery management system interconnects, charging port contacts, and current-carrying busbar and terminal components, which are unique to electrified vehicles and that require the higher current carrying capacity, vibration resistance, and high-temperature performance that phosphor bronze’s superior mechanical and electrical properties enable when compared to traditional electrical connector materials. A conventional internal combustion engine vehicle has about 2-3 kilometers of low voltage wiring, 400-600 positions of connectors, and a battery management system interconnection array of hundreds of cell level voltage sensing and temperature monitoring contacts, each of which uses relatively small amounts of phosphor bronze, resulting in a total of about 2.8 times more than an equivalent conventional ICE vehicle. High current systems for the charging of electric vehicles, such as Level 2 AC charging stations and 22-350 kilowatt DC fast chargers, have high thermal and mechanical performance requirements for the contact materials in their high-current connectors, which is why the superior fatigue resistance, high-temperature strength retention and reliable contact spring force of phosphor bronze contact materials are especially useful when compared to lower quality alternatives. Beyond the demand for phosphor bronze in electric vehicles, demand will also grow at the charging infrastructure level due to the use of this material in the connector interface, busbar connections, and current-carrying terminal components of individual charging stations, which is expected to rise from current global levels of about USD 22.4 billion to more than USD 100 billion by 2032. Underhood/body connector environments and battery enclosure connector applications are environments where higher grade, premium phosphor bronze components are being increasingly adopted because these environments impose requirements for higher contact force due to larger gauge body and connector geometry and higher temperature cycling due to the battery or body enclosure environment.

What are the Major Advances Changing the Phosphor Bronze Market Today?

- Advanced Alloy Development and Microstructural Engineering Extending Phosphor Bronze Performance Frontiers: The most technically significant advancement in the capabilities of phosphor bronze products is the systematic development of next-generation phosphor bronze strip and wire products with superior combinations of properties, especially the historically difficult electrical and mechanical balance that limits the electrical performance of conventional phosphor bronze alloys, so that these products are able to compete with and in many applications outperform the higher-cost specialty copper alloys such as beryllium copper and titanium copper in critical electrical connector applications. Conventional phosphor bronze alloys are mechanically strong because of the tin that is solid solution strengthened in the copper matrix, but with each increment of tin content, the electrical conductivity is decreased by about 1–2% IACS; thus, there is a fundamental design trade-off between mechanical and electrical strength, eliminating acceptable use of phosphor bronze in high-frequency and high-current applications where higher electrical conductivity is required, while simultaneously making it acceptable for connector applications where 15–20% IACS conductivity can be tolerated. Variants of precipitation hardened phosphor bronze — with controlled additions of zirconium, chromium, iron and nickel that produce fine coherent precipitate dispersions during precipitation heat-treatment — are being developed to achieve 0.2% proof stress from 900 to 1,100 MPa and electrical conductivity from 25 to 35% IACS, approaching the performance envelope of beryllium copper, at material costs much lower and without health and safety concerns associated with beryllium processing. Optimization of the reduction ratios in the cold rolling process and intermediate annealing cycles, which allow production of ultra-fine grain phosphor bronze strip with average grain diameters below 5 micrometers, is a multi-functional solution that simultaneously enhances the fatigue resistance and surface finish quality of the strip, necessary for miniaturized connector applications where the strip is required to have complex bend shapes without intergranular cracking and must be electroplated with precious metals to ensure reliable adhesion to the plating. Advanced surface finishing, hot rolling, and cold rolling processes offered by the top manufacturers like Wieland-Werke, KME and Aurubis are meeting the surface quality standards demanded by top connector manufacturers such as Molex, TE Connectivity, and Aurubis with surface roughness below 0.1 μm Ra and the freedom of surface oxide inclusions that cause electroplating defects, as connector miniaturization pushes stamping tolerances below 0.05 millimeters and precious metal plating thickness below 0.2 micrometers.

- Tin Sourcing and Recycled Content Strategy Reshaping Phosphor Bronze Supply Chain Economics and Sustainability: The concentration risks of tin supply, with about 50% of the world’s refined tin currently sourced from China and Indonesia, and the increased focus on recycled copper and tin in the production of phosphor bronze as a circular economy solution that aims to reduce dependency on primary materials, decrease the carbon footprint of phosphor bronze production and fulfil customer and regulatory demands for transparency on the origin of materials, are creating a strategic transformation in the global phosphor bronze supply chain. The EU Critical Raw Materials Act 2024 lists tin as a critical raw material, and EU commercial uncertainty in phosphor bronze production is caused by the usage risk in the supply chain as well as the strategic importance of tin, which is used at between 4 and 9% by weight in commercial phosphor bronze alloys and is the main alloying cost premium over pure copper. For key producers of phosphor bronze, the development and qualification of high-recycled-content production routes are commercially and sustainability driven, and all three companies (Aurubis, Wieland-Werke, and KME) have announced stepped up targets for the recycled content of their copper alloy strip production, with end-of-life electronic scrap recovery supplying the bulk of the copper and tin needed. Phosphor bronze scrap recycling is commercially proven to be a business for the clean and composition-known scrap stream, with stamping turnings from precision connector manufacturers being the highest quality secondary phosphor bronze raw material available with prices very close to the new alloy value minus processing cost. For copper alloy scrap with an “unknown” composition (such as blends of phosphor bronze with brass, copper-nickel, or other copper alloys that cannot be distinguished without composition analysis), the challenge is being solved by laser-induced breakdown spectroscopy (LIBS) sorting systems being installed at large copper scrap processors, which enable sorting of the copper alloy scrap into alloy classes to provide a defined copper alloy input stream for secondary copper alloy production, and in this case, to provide a defined input stream of phosphor bronze.

- Precision Cold Rolling and Strip Processing Technology Advances Improving Dimensional Consistency for Miniaturized Connector Applications: The technical requirements of modern electrical connector manufacturing, imposed by the continuing demand in the consumer electronics industry for thinner, lighter, and denser electronic assemblies, are driving ever tighter dimensional tolerances on electrical connector phosphor bronze strip for ultra-thin strip ranging from 0.05-0.30 millimeters thickness at production speeds from 200-600 meters per minute, in addition to increasing the investment in advanced cold rolling mill technology and in-line dimensional monitoring infrastructure to maintain the strip thickness tolerance of ±0.002-0.005 millimeters and width tolerance of ±0.05 millimeters. The ultra-thin phosphor bronze strip, which is manufactured at 0.05–0.15mm thickness for the most cutting-edge miniaturized connector applications in wearables, smartphones and ultra-compact industrial electronics — The most technically demanding and highest value phosphor bronze product form, these premium prices (40-80% above standard thickness strip) are due to the additional rolling passes required, the precision tension control and the surface quality management needed to produce commercially acceptable ultra thin material without thickness variation, shape defects or surface quality issues that would cause connector stamping die failures or plating defects. Japanese and Korean electronics manufacturers whose connector designs push the limit of miniaturization are able to obtain ultra-thin precision strip in thicknesses as small as ±0.001 millimeters and maintain thickness uniformity with the aid of computer-controlled roll gap and tension control systems that are compatible with multi-stand Sendzimir cold rolling mills, which are built by leading phosphor bronze strip manufacturers such as Nippon Mining & Metals, Mitsubishi Shindoh and Wieland-Werke, are capable of operating at production speeds competitive with conventional thickness precision strip rolling. New tools such as electromagnetic strip flatness measurement and feedback controlled leveling systems, which measure the flatness of the strip at spatial resolution below 10 mm with arrays of eddy current sensors, are enabling the real-time correction of strip shape defects during cold rolling and roller leveling operations, thus producing the flatness value below 0.5 I-units that is required for reliable high-speed progressive die stamping of miniaturized connector terminals at production rates of over 1,000 strokes per minute.

Category Wise Insights

By Product Form

Why Do Strips and Sheets Lead the Phosphor Bronze Market?

Strips and sheets are the leading product form category in 2025, with revenue expected to be around 38% of the total market. The application of this highest-volume phosphor bronze is in the production of precision-stamped parts, specifically in electrical connector and electronic component manufacturing, all of which are concentrated in the cold-rolled phosphor bronze strip processed in coiled strip material using progressive die stamping operations at 200 – 1,500 strokes per minute.

In 2024, estimated consumption of phosphor bronze strip amounted to 280,000–320,000 metric tons globally, with most of this coming from Asian Pacific processing facilities for the consumer electronics, automotive connector, and telecommunications equipment markets. The Standard thickness strip market ($15–1000/million) is the main group of strip cases, with applications in most electrical connector, lead frame, spring contact and precision instrument component uses.

The fastest-growing and highest-single value sub-segment of strips is ultra-thin precision strips under 0.15mm, which are expected to see a CAGR of ~7.3% between 2026 and 2035, as the miniaturization trend of smartphones and wearable electronics continues to make connector terminal thicknesses thinner, while at the same time standards for the generation of contact forces remain the same or increase. C51000 is the dominant grade for commercial phosphor bronze strip, accounting for about 64% of strip segment revenue, due to its optimal combination of electrical conductivity, mechanical properties and material cost for the widest range of electrical connector applications, with C52100 and C52400 higher-tin grades accounting for 26% of strip revenue in the most demanding applications where the extra spring temper and fatigue resistance are compensated by the higher alloy costs.

By Grade

Why Does C51000 Lead the Grade Segment?

The standard 5% tin phosphor bronze grade (C51000) is the most commonly used alloy composition in the electrical connector and electronic component market and will account for around 58% of market revenue in 2025, as it is the alloy most optimized for commercial use for a wide range of applications that benefit from a balance of 15–18% IACS electrical conductivity, spring temper proof stress of 550–700 MPa, and material cost.

C51000’s dominance is strengthened by its extensive use in the global electrical connector industry specification of materials, with most of the industry’s well-established designs having been qualified and production-tooled for the use of C51000 strip, which creates switching costs that will support continued use of the C51000 specification over alternative grades when performance-driven reformulation requirements do not exist.

C52100 at approximately 19% of market revenue is used in applications where extra mechanical strength and fatigue resistance are warranted by the higher tin content and cost premium, such as high-insertion-force automotive connectors, precision test socket contacts and relay spring components that need to provide dependable contact force in high temperature cycling environments.

The free-cutting phosphor bronze grade, C54400, with the addition of lead to the C51000 standard to increase its machinability to approximately 80% compared to 20%, is used in the bearing, bushing and precision machining component application sector which represents about 11% of the market revenue with benefits in the form of reduced machining time and tool wear related to the turned and milled precision machining of the phosphor bronze components compared to the standard non-leaded grades. Specialty and custom grade, which is expected to expand at around 6.8% CAGR between 2026 and 2035, is driven by the increasing demand for alloy variants with a range of specific properties that are not available in standard commercial grades, including precision medical device applications, high-frequency telecommunications components, and EV high-voltage connector applications.

By Application

Why Do Electrical and Electronic Components Lead the Phosphor Bronze Application Segment?

That’s about 46% of the total market revenue for electrical and electronics in 2025, and the precision connector and electronic component stamping application is the absolute leader for the electrical and electronics manufacturing industry, the world’s biggest individual consumer of phosphor bronze strip material. Within the electrical and electronics sector, consumer electronics makes up the largest sub-sector, with the smartphone, laptop, tablet and wearable device sectors all producing billions of individual units of consumer electronics and using millions of individual units of phosphor bronze connectors each year.

Global networks are rolling out 5G base station equipment and fiber optic terminal boxes, and data center interconnect hardware is expanding at about 7.8% CAGR in the electrical and electronics end use, as a significant amount of new connector hardware is being demanded by the densely connected antenna arrays and massive MIMO radio systems that are integral to 5G networks. At 6.4%, the automotive end use is the quickest to grow between 2026 and 2035, according to market revenue, owing to the proliferation of EV high-voltage connectors, growth in advanced driver assistance system (ADAS) radar and camera module connectors, and the rising trend of increasing electronic content per vehicle in both conventional and EV architectures.

By End Use Industry

Why Does the Electrical and Electronics Industry Lead the End Use Segment?

Electrical and electronics currently generate some 46% of the total market revenue in 2025, and the absolute focus of the highest-volume application for phosphor bronze strip — precision connector and electronic component stamping — is within this industry, the world’s biggest single market for phosphor bronze strip. The largest sub-sector is consumer electronics in the electrical and electronics sector where billions of devices such as smartphones, laptops, tablets and wearables are being manufactured which use millions of individual phosphor bronze connectors per year.

The global 5G network deployment is generating significant new demand for connector hardware from the densely connected antenna arrays and massive MIMO radio equipment comprising 5G base station technology, which is growing at ~7.8% CAGR in the telecommunications infrastructure sub-sector of the electrical and electronics end use. The automotive end use will see the highest CAGR of 6.4% between 2026 and 2035 due to the proliferation of EV high-voltage connectors, the growth of advanced driver assistance system (ADAS) radar and camera module connectors, and the progressive increase in electronic content per vehicle in both traditional and electrified architectures, which will generate market revenue of around 19%.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 4.54 billion |

| Projected Market Size in 2035 | USD 7.38 billion |

| Market Size in 2025 | USD 4.27 billion |

| CAGR Growth Rate | 5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Product Form, Grade, Application, End Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

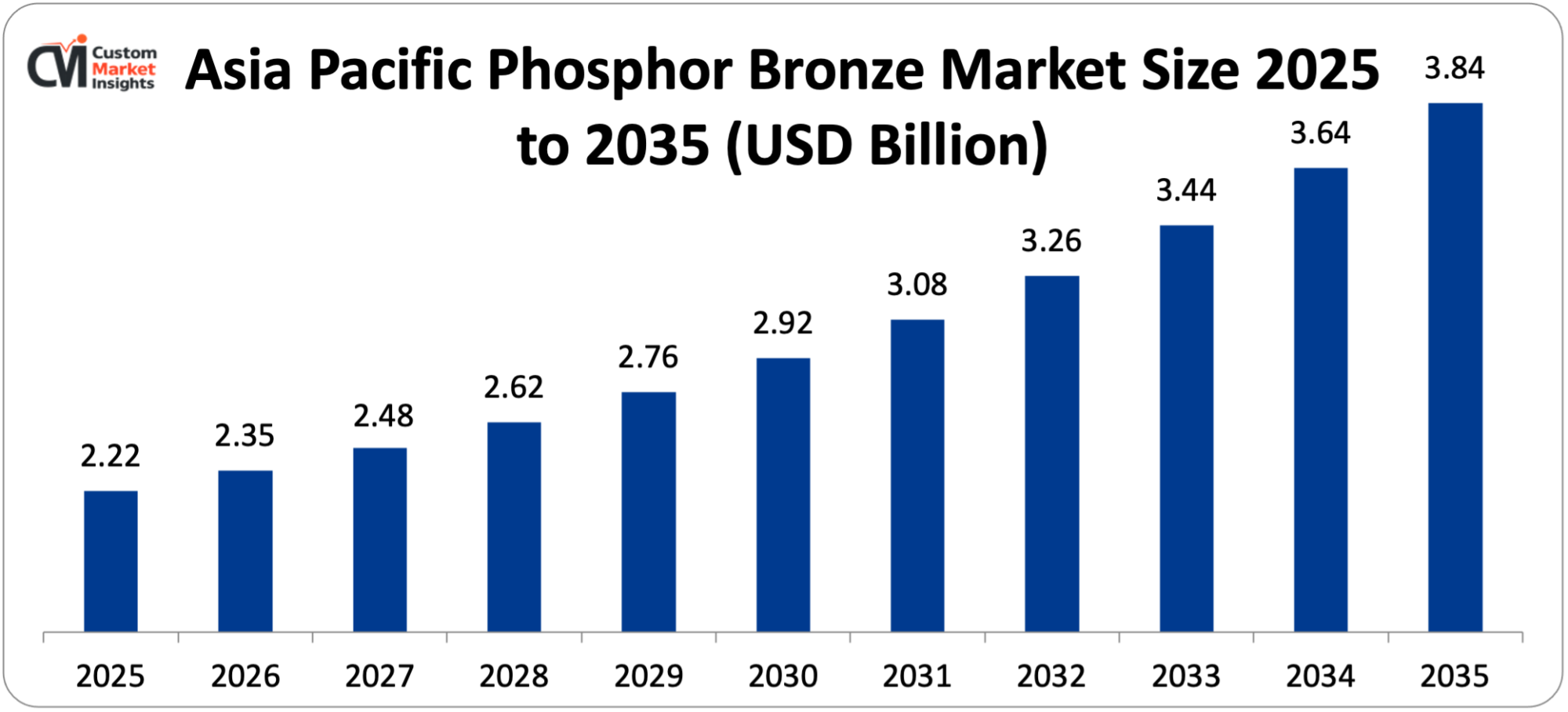

The Asia Pacific phosphor bronze market size is estimated at USD 2.22 billion in 2025 and is projected to reach approximately USD 3.84 billion by 2035, growing at a CAGR of 5.6% from 2026 to 2035.

Why is Europe the Second-Largest and Most Technically Demanding Market?

In 2025, Europe captures about 21% of the global market revenue, valued at around USD 897 million, with the industry focus of precision engineering, automotive manufacturing, marine equipment, and industrial machinery industries, which are among the most technically advanced consumers of phosphor bronze in the world. The European largest market for phosphor bronze is Germany, where the automotive OEMs, such as Volkswagen, BMW, and Mercedes-Benz, have their headquarters and their electrical system complexity makes Germany one of the largest markets for connectors, with substantial consumption of associated electrical components as well, with Bosch and Continental being prominent automotive electronics manufacturers that consume connector terminals in significant quantities, and the precision engineering industry in Germany, with its wide use of phosphor bronze bearings, bushings, and spring components, consuming a significant amount of phosphor bronze in industrial equipment.

The European market leader is Wieland-Werke, with its headquarters in Ulm, Germany and one of the world’s most technically advanced copper alloy strip rolling plants, along with KME Group and Aurubis, who combine to manufacture the bulk of European-origin premium precision phosphor bronze strip used in the automotive, industrial and electronics sectors. Northern Europe’s marine equipment and offshore energy sectors, which are mainly centred on Germany, the Netherlands, Norway and the United Kingdom, are a unique European demand driver for the marine grade phosphor bronze castings, fastenings and valve components that are needed for offshore wind foundation hardware, North Sea platform equipment, and commercial shipbuilding applications that demand the highest standards of seawater corrosion resistance.

Why is North America Showing Steady and Sustained Growth?

In 2025, the market revenue share for North America is about 18%; it is projected to grow at a CAGR of 4.6% from 2026 to 2035, driven by increased market demand for EV manufacturing, growth in the aerospace and defense electronics industry, reshoring manufacturing investments, and the offshore wind energy industry development along the U.S. coasts, which will drive market demand for marine grade phosphor bronze in offshore foundation and electrical infrastructure.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region, estimated to grow at the fastest rate in the region at 5.8% CAGR from 2026 to 2035, will account for around 6% of worldwide market revenue in 2025, due to the development of the manufacturing sector in the Gulf Cooperation Council under Vision 2030 initiatives that is generating new electrical and industrial component manufacturing requirements, the expanding offshore energy infrastructure in the Gulf and West Africa that is driving the demand for marine-grade phosphor bronze hardware, and the fact that Brazil’s large electronics and automotive manufacturing base is the leading Latin American user of phosphor bronze.

The industrial diversification investment, which comprises the expansion of downstream petrochemical complexes, the expansion of desalination facilities, and the growth of the emerging electrical connector hardware and electronics assembly industry, is driving new phosphor bronze demand from industrial equipment bearings, valve components, and electrical connector hardware in new industrial manufacturing facilities in Saudi Arabia. The Brazilian phosphor bronze market is fueled by a large domestic automotive and electronics manufacturing base that utilizes connector and bearing components and by Brazilian copper and bronze producers, such as Eluma and Celta Bronze, that produce from domestic processing that meets domestic demand.

Top Players in the Market and Their Offerings

- Wieland-Werke AG

- KME Group

- Aurubis AG

- Mitsubishi Shindoh Co. Ltd.

- Nippon Mining & Metals Co. Ltd.

- Materion Corporation

- Lebronze Alloys

- Ningbo Jintian Copper Group Co. Ltd.

- Aviva Metals Inc.

- National Bronze Mfg. Co.

- Others

Key Developments

The market has undergone significant developments as industry participants seek to expand capabilities and enhance product portfolios.

- In March 2025: Wieland-Werke AG announced the commercial launch of its W-Alloy PB72 advanced precipitation-hardened phosphor bronze strip — a next-generation alloy incorporating precisely controlled zirconium and chromium microadditions achieving 0.2% proof stress of 950 MPa combined with electrical conductivity of 28% IACS — specifically targeting electric vehicle high-voltage connector applications requiring the superior fatigue resistance and elevated temperature strength retention needed for 800-volt automotive connector systems operating under underhood thermal cycling conditions, with the product qualifying under major automotive connector manufacturer material specifications and receiving IATF 16949 quality management system certification for automotive supply chain use.

- In February 2025: The expanded precision phosphor bronze strip production site with 35,000 metric tonnes per year of C51000 and C52100 precision strip production capacity equipped with the latest generation Sendzimir cold rolling mills with laser thickness control and electromagnetic flatness measurement systems are aimed at the rapidly expanding Chinese domestic and export market demand for precision phosphor bronze strip products from consumer electronics connector manufacturers and automotive electrical system component manufacturers, and the site has been certified to meet the IATF 16949 standard for automotive quality management and ISO 9001 standard for quality management.

During the forecast period, these strategic activities enabled companies to reinforce market positions, broaden precision strip product portfolios to meet the most technologically challenging connector applications in the EV and miniaturized electronics industry, create next-generation alloy compositions with improved property combinations that are not found in traditional phosphor bronze grades, and benefit from structural demand growth that has been driven by growth in global EV fleets, smartphone and IoT device manufacturing, 5G infrastructure rollout, and offshore energy development.

The Phosphor Bronze Market is segmented as follows:

By Product Form

- Strips & Sheets

- Ultra-Thin Precision Strip (< 0.15 mm)

- Standard Strip (0.15–1.0 mm)

- Heavy Gauge Sheet (> 1.0 mm)

- Wires & Rods

- Fine Wire (< 1.0 mm diameter)

- Standard Wire (1.0–5.0 mm diameter)

- Rods & Bars (> 5.0 mm diameter)

- Tubes & Pipes

- Seamless Phosphor Bronze Tubes

- Drawn Phosphor Bronze Tubes

- Castings

- Sand Castings

- Centrifugal Castings

- Continuous Castings

- Powder

- Atomized Phosphor Bronze Powder

- Sintered Bronze Powder

- Other Product Forms

By Grade

- C51000 (5% Sn, Standard Grade)

- C52100 (6% Sn, High Strength)

- C52400 (8% Sn, Extra High Strength)

- C54400 (Phosphor Bronze B, Free-Cutting)

- Other Grades

- C50500 (1.3% Sn, Low Tin)

- C53400 (Medium Tin, Enhanced Machinability)

- Specialty and Custom Grades

By Application

- Electrical & Electronic Components

- Connector Terminals & Contacts

- Lead Frames

- Spring Contacts & Switch Components

- PCB Test Sockets

- Bearings & Bushings

- Plain Bearings

- Flanged Bushings

- Thrust Washers

- Springs & Connectors

- Precision Springs

- Electrical Connectors

- Relay Components

- Marine Hardware

- Propeller Shaft Bearings

- Marine Fasteners & Fittings

- Valve Components

- Industrial Fasteners

- Musical Instruments

- Guitar & Bass Strings

- Wind Instrument Components

- Other Applications

By End Use Industry

- Electrical & Electronics

- Consumer Electronics

- Telecommunications

- Industrial Electronics

- Automotive

- ICE Powertrain Components

- EV High-Voltage Connectors

- Body & Chassis Electronics

- Industrial Machinery

- Bearings & Power Transmission

- Hydraulic & Pneumatic Components

- Marine

- Commercial Shipping

- Naval Defense

- Offshore Energy

- Aerospace & Defense

- Consumer Goods

- Other End Use Industries

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Phosphor Bronze by Segments

- 2.1.2. Phosphor Bronze by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Phosphor Bronze Market Attractiveness Analysis, By Product Form

- 2.2.3. Phosphor Bronze Market Attractiveness Analysis, By Grade

- 2.2.4. Phosphor Bronze Market Attractiveness Analysis, By Application

- 2.2.5. Phosphor Bronze Market Attractiveness Analysis, By End Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Expanding Global Electrical Connector and Electronic Component Manufacturing Driving Structural Phosphor Bronze Demand

- 3.1.2. Electric Vehicle Electrification Creating New High-Performance Phosphor Bronze Connector and Busbar Applications

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Phosphor Bronze Market – By Product Form

- 4.1. Product Form Market Overview, By Product Form Segment

- 4.1.1. Phosphor Bronze Market Revenue Share, By Product Form, 2025 & 2035

- 4.1.2. Strips & Sheets

- 4.1.2.1. Ultra-Thin Precision Strip (< 0.15 mm)

- 4.1.2.2. Standard Strip (0.15–1.0 mm)

- 4.1.2.3. Heavy Gauge Sheet (> 1.0 mm)

- 4.1.3. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Wires & Rods

- 4.1.6.1. Fine Wire (< 1.0 mm diameter)

- 4.1.6.2. Standard Wire (1.0–5.0 mm diameter)

- 4.1.6.3. Rods & Bars (> 5.0 mm diameter)

- 4.1.7. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Tubes & Pipes

- 4.1.10.1. Seamless Phosphor Bronze Tubes

- 4.1.10.2. Drawn Phosphor Bronze Tubes

- 4.1.11. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Castings

- 4.1.14.1. Sand Castings

- 4.1.14.2. Centrifugal Castings

- 4.1.14.3. Continuous Castings

- 4.1.15. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Powder

- 4.1.18.1. Atomized Phosphor Bronze Powder

- 4.1.18.2. Sintered Bronze Powder

- 4.1.19. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Other Product Forms

- 4.1.23. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Product Form Market Overview, By Product Form Segment

- Chapter 5. Phosphor Bronze Market – By Grade

- 5.1. Grade Market Overview, By Grade Segment

- 5.1.1. Phosphor Bronze Market Revenue Share, By Grade, 2025 & 2035

- 5.1.2. C51000 (5% Sn, Standard Grade)

- 5.1.3. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. C52100 (6% Sn, High Strength)

- 5.1.7. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. C52400 (8% Sn, Extra High Strength)

- 5.1.11. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. C54400 (Phosphor Bronze B, Free-Cutting)

- 5.1.15. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Other Grades

- 5.1.18.1. C50500 (1.3% Sn, Low Tin)

- 5.1.18.2. C53400 (Medium Tin, Enhanced Machinability)

- 5.1.18.3. Specialty and Custom Grades

- 5.1.19. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Grade Market Overview, By Grade Segment

- Chapter 6. Phosphor Bronze Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Phosphor Bronze Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Electrical & Electronic Components

- 6.1.2.1. Connector Terminals & Contacts

- 6.1.2.2. Lead Frames

- 6.1.2.3. Spring Contacts & Switch Components

- 6.1.2.4. PCB Test Sockets

- 6.1.3. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Bearings & Bushings

- 6.1.6.1. Plain Bearings

- 6.1.6.2. Flanged Bushings

- 6.1.6.3. Thrust Washers

- 6.1.7. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Springs & Connectors

- 6.1.10.1. Precision Springs

- 6.1.10.2. Electrical Connectors

- 6.1.10.3. Relay Components

- 6.1.11. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Marine Hardware

- 6.1.14.1. Propeller Shaft Bearings

- 6.1.14.2. Marine Fasteners & Fittings

- 6.1.14.3. Valve Components

- 6.1.15. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Industrial Fasteners

- 6.1.19. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Musical Instruments

- 6.1.22.1. Guitar & Bass Strings

- 6.1.22.2. Wind Instrument Components

- 6.1.23. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1.26. Other Applications

- 6.1.27. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 6.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.29. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Phosphor Bronze Market – By End Use Industry

- 7.1. End Use Industry Market Overview, By End Use Industry Segment

- 7.1.1. Phosphor Bronze Market Revenue Share, By End Use Industry, 2025 & 2035

- 7.1.2. Electrical & Electronics

- 7.1.2.1. Consumer Electronics

- 7.1.2.2. Telecommunications

- 7.1.2.3. Industrial Electronics

- 7.1.3. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Automotive

- 7.1.6.1. ICE Powertrain Components

- 7.1.6.2. EV High-Voltage Connectors

- 7.1.6.3. Body & Chassis Electronics

- 7.1.7. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Industrial Machinery

- 7.1.10.1. Bearings & Power Transmission

- 7.1.10.2. Hydraulic & Pneumatic Components

- 7.1.11. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Marine

- 7.1.14.1. Commercial Shipping

- 7.1.14.2. Naval Defense

- 7.1.14.3. Offshore Energy

- 7.1.15. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Aerospace & Defense

- 7.1.19. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Consumer Goods

- 7.1.23. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1.26. Other End Use Industries

- 7.1.27. Phosphor Bronze Share Forecast, By Region (USD Billion)

- 7.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.29. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End Use Industry Market Overview, By End Use Industry Segment

- Chapter 8. Phosphor Bronze Market – Regional Analysis

- 8.1. Phosphor Bronze Market Overview, By Region Segment

- 8.1.1. Global Phosphor Bronze Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Phosphor Bronze Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Phosphor Bronze Market Revenue, By Product Form, 2026 – 2035

- 8.1.4. Global Phosphor Bronze Market Revenue, By Grade, 2026 – 2035

- 8.1.5. Global Phosphor Bronze Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Phosphor Bronze Market Revenue, By End Use Industry, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Phosphor Bronze Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Phosphor Bronze Market Revenue, By Product Form, 2026 – 2035

- 8.2.3. North America Phosphor Bronze Market Revenue, By Grade, 2026 – 2035

- 8.2.4. North America Phosphor Bronze Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Phosphor Bronze Market Revenue, By End Use Industry, 2026 – 2035

- 8.2.6. U.S. Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Phosphor Bronze Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Phosphor Bronze Market Revenue, By Product Form, 2026 – 2035

- 8.3.3. Europe Phosphor Bronze Market Revenue, By Grade, 2026 – 2035

- 8.3.4. Europe Phosphor Bronze Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Phosphor Bronze Market Revenue, By End Use Industry, 2026 – 2035

- 8.3.6. Germany Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Phosphor Bronze Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Phosphor Bronze Market Revenue, By Product Form, 2026 – 2035

- 8.4.3. Asia Pacific Phosphor Bronze Market Revenue, By Grade, 2026 – 2035

- 8.4.4. Asia Pacific Phosphor Bronze Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Phosphor Bronze Market Revenue, By End Use Industry, 2026 – 2035

- 8.4.6. China Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Phosphor Bronze Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Phosphor Bronze Market Revenue, By Product Form, 2026 – 2035

- 8.5.3. The Middle-East and Africa Phosphor Bronze Market Revenue, By Grade, 2026 – 2035

- 8.5.4. The Middle-East and Africa Phosphor Bronze Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Phosphor Bronze Market Revenue, By End Use Industry, 2026 – 2035

- 8.5.6. Saudi Arabia Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Phosphor Bronze Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Phosphor Bronze Market Revenue, By Product Form, 2026 – 2035

- 8.6.3. Latin America Phosphor Bronze Market Revenue, By Grade, 2026 – 2035

- 8.6.4. Latin America Phosphor Bronze Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Phosphor Bronze Market Revenue, By End Use Industry, 2026 – 2035

- 8.6.6. Brazil Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Phosphor Bronze Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Phosphor Bronze Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Phosphor Bronze Market: Company Market Share, 2025

- 9.2. Global Phosphor Bronze Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Wieland-Werke AG

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. KME Group

- 10.3. Aurubis AG

- 10.4. Mitsubishi Shindoh Co. Ltd.

- 10.5. Nippon Mining & Metals Co. Ltd.

- 10.6. Materion Corporation

- 10.7. Lebronze Alloys

- 10.8. Ningbo Jintian Copper Group Co. Ltd.

- 10.9. Aviva Metals Inc.

- 10.10. National Bronze Mfg. Co.

- 10.11. Others.

- 10.1. Wieland-Werke AG

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 85

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Wieland-Werke AG

- KME Group

- Aurubis AG

- Mitsubishi Shindoh Co. Ltd.

- Nippon Mining & Metals Co. Ltd.

- Materion Corporation

- Lebronze Alloys

- Ningbo Jintian Copper Group Co. Ltd.

- Aviva Metals Inc.

- National Bronze Mfg. Co.

- Others

FAQs

The key players in the market are Wieland-Werke AG, KME Group, Aurubis AG, Mitsubishi Shindoh Co. Ltd., Nippon Mining & Metals Co. Ltd., Materion Corporation, Lebronze Alloys, Ningbo Jintian Copper Group Co. Ltd., Aviva Metals Inc., National Bronze Mfg. Co., Others.

The regulation and technical standard of the phosphor bronze market affect the market in various ways and have an impact on the specification of the product and the drivers of demand in key end use markets. The EU RoHS Directive prohibiting the use of lead and other hazardous materials in electrical and electronic equipment — along with the global equivalents in China (RoHS), Korea (RoHS), and elsewhere — has made significant strides toward phasing out the use of leaded phosphor bronze grades such as C54400 in electrical and electronic applications and has encouraged the development of grades that offer comparable machinability without the lead content. The documentation requirements set in the REACH regulation substance restriction in Europe are applicable to producers and distributors of copper alloys where the substance of very high concern content is present in products and for specialty grades of phosphor bronze, the documentation requirements are applicable to cobalt and other alloying elements, thus imposing regulation compliance management requirements on the supply chain. Automotive industry quality standards such as IATF 16949 (ISO 26999) quality management system certification and OEM-specific material approval requirements from key automotive connector specification bodies like USCAR standards published by the U.S. Council for Automotive Research pose certification barriers for producers of automotive phosphor bronze, with IATF 16949 now a market access requirement for automotive phosphor bronze producers. The EU Battery Regulation’s due diligence provisions on material traceability of battery materials, including copper, will increasingly drive producers of phosphor bronze to provide product documentation and certifications for EV battery and charging system manufacturers to comply with supply chain transparency obligations, resulting in additional documentation and certification requirements that create compliance infrastructure investment for copper producers that supply the EV industry.

The London Metal Exchange copper price is the fundamental price in the pricing of phosphor bronze and as it is literally the foundation of the raw material price in most phosphor bronze alloys, it means there is considerable base metal price volatility that trickles through to the pricing of phosphor bronze products and makes commercial planning difficult for both producers and customers. The LME copper price movements correspond directly to the movements in the raw material cost of standard C51000 phosphor bronze, as the copper content is 94.5%–96% by weight, and copper price movements are reflected in the raw material cost of the copper through monthly/quarterly raw material price changes based on LME copper average prices in the long-term supply contracts with the major connector and electronics manufacturer customers. Fabrication premium varies depending on the thickness of the strip, tolerance class, surface quality grade, and annual quantity of precision phosphor bronze strip, ranging from around USD 1,200 to USD 3,500 per metric ton, with the thicker the strip, the tighter the tolerance, the higher the surface quality grade, and the smaller the annual quantity, the higher the fabrication premium. China and Indonesia are the geographic supply concentration of tin, which adds a second price risk factor for producers of phosphor bronze and increases the volatility of the price of tin on the London Metal Exchange (LME) in recent years, creating phosphor bronze production cost uncertainty, which producers deal with through tin hedging programs and inventory management. These premium alloy grades, such as C52100, C52400 and specialty precipitation-hardened alloys, are fabricated at a premium and have properties that are superior—cost of the alloy, processing complexity, and premium markets in which the superior properties justify premium connector manufacturer specifications—in 20–60% higher than that of the standard C51000.

Global electrical connector market growth will proportionately boost phosphor bronze strip consumption, EV fleet growth will drive the growth of high-voltage connectors and charging stations hardware demand, offshore wind energy capacity growth will generate the growth of associated marine hardware demand, the proliferation of IoT and 5G technology will fuel the growth of electronic connector component demand, and the geographic expansion of the market across India, Southeast Asia, and LAMEA will create new centers of phosphor bronze materials demand from the industry and electronics manufacturing sectors at 5.0% CAGR from 2026 to 2035.

Asia Pacific is projected to hold the largest revenue share over the forecast period, rising from 52% in 2025 to an estimated 54% in 2035, as the region’s electronics sector consumes the bulk of global precision strip phosphor bronze production, the region’s domestic capacity to manufacture phosphor bronze steadily increases, and India’s automotive manufacturing sector is driving incremental demand for electronics. European producers Wieland-Werke and KME will continue to establish the technical standards for precision strip quality and the allocation of the necessary alloy performance that lays the foundations for the market.

The region of LAMEA is projected to show the highest CAGR of 5.8% between 2026 and 2035 owing to the industrial manufacturing development in the Gulf Cooperation Council countries, the expansion of offshore energy infrastructure in the Gulf and West Africa countries, which will demand more marine grade phosphor bronze, and the industrialization of the emerging markets, which will lead to an increase in the demand for electrical equipment and industrial machinery. Asia Pacific is the largest growth market individually at around 7.4% CAGR, with rapid domestic electronics manufacturing growth under the Production Linked Incentive scheme, automotive sector growth – high voltage connectors demand growth in this market due to EV transitions in the region—and industrial machinery sector growth – phosphor bronze bearings and bushing components demand growth in this market.

The Global Phosphor Bronze Market is predicted to experience sustained growth driven by the global electrical connector market valued at approximately USD 88.4 billion in 2024 projected to reach USD 141.7 billion by 2032 at 6.1% CAGR creating structural phosphor bronze strip demand growth; BEVs consuming 1.8–2.8 times more phosphor bronze per vehicle than ICE equivalents from high-voltage connector proliferation driving automotive segment growth at the fastest CAGR of 6.4%; the global EV charging infrastructure market projected to grow from USD 22.4 billion in 2024 to over USD 100 billion by 2032 creating infrastructure-level phosphor bronze demand from high-current connector and terminal components; the global IoT device population growing from 18.8 billion in 2024 to over 32 billion by 2030 generating growing electronic connector component demand; offshore wind capacity growing from approximately 75 GW to 380 GW by 2035 generating marine-grade phosphor bronze hardware demand; 5G infrastructure deployment growing at 7.8% CAGR within electrical and electronics end use consuming precision connector components; ultra-thin precision strip growing at 7.3% CAGR from smartphone and wearable miniaturization; and advanced precipitation-hardened phosphor bronze grade development enabling penetration of premium connector applications previously served exclusively by more expensive beryllium copper alloys.