Plant-based Milk Market Size, Trends and Insights By Product (Almond Milk, Soy Milk, Oat Milk, Coconut Milk, Pea Milk, Rice Milk, Others), By Nature (Organic, Conventional), By Flavor (Flavored Milk, Non-Flavored Milk), By Sales Channel (Hypermarkets & Supermarkets, Online, Specialty Stores, Others), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Europe |

| Largest Market: | Asia Pacific |

Major Players

- Alpro (Danone)

- Blue Diamond Growers

- Califia Farms LLC

- Daiya Foods Inc.

- Others

Reports Description

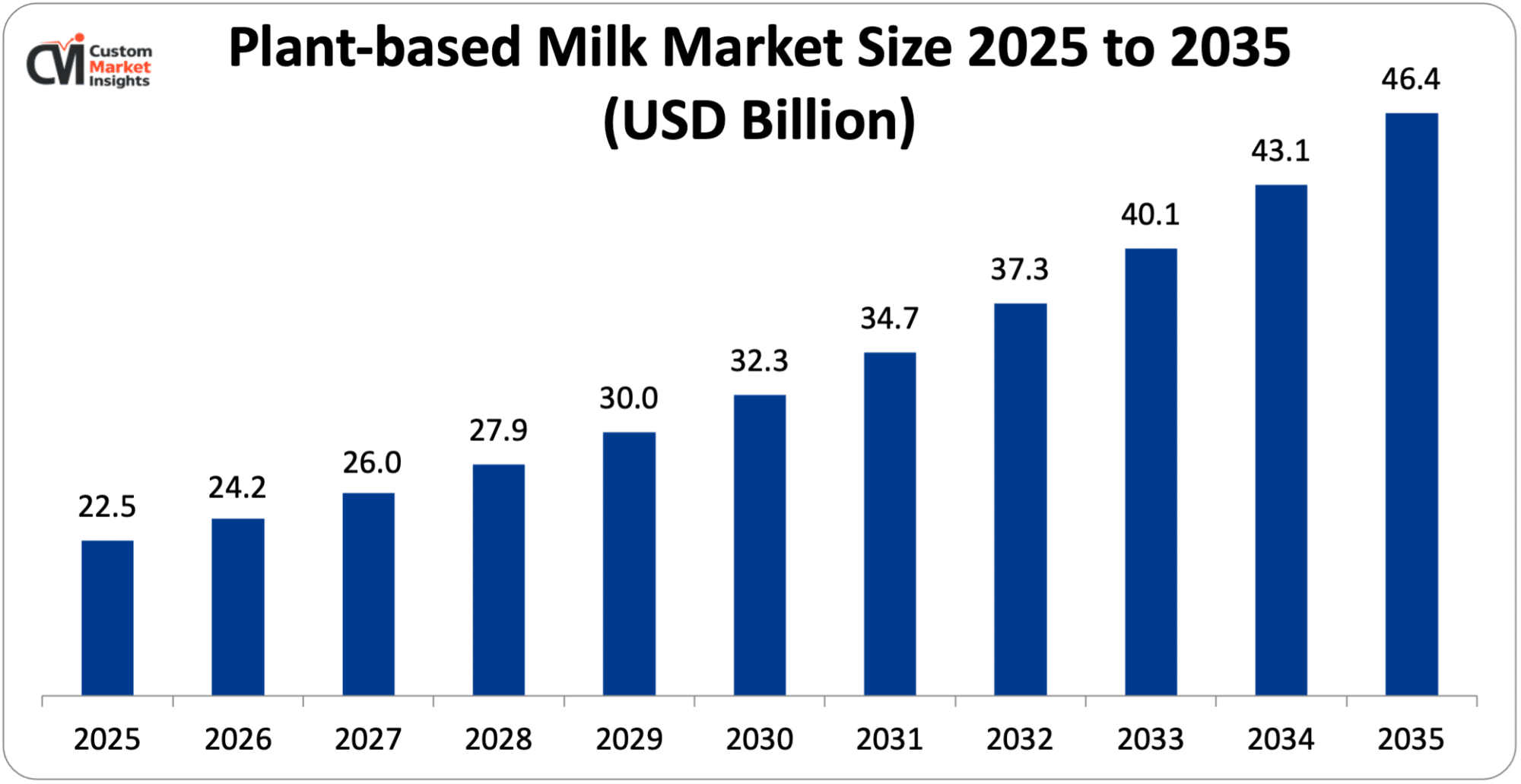

The market size of global plant-based milk will be estimated at USD 22.5 billion in 2025 and is expected to grow to between USD 24.2 billion in 2026 and about USD 46.4 billion by 2035, with a current CAGR (compound annual growth rate) of 7.5% during the period of 2026 to 2035. “Plant milk” can be a naturally integral term used to scan the production and manufacture of a wide set of various varieties of non-dairy drinks that could be made from the extraction and blending of different plant foods/ingredients: almonds, cereals, seeds, tubers, and pulses.

The ingredients are rinsed and processed to imitate sensory qualities of dairy milk in color and mouthfeel, and also at some points it refers to nutritional values as well. Among non-dairy alternatives, nut/legume milk appears the most common, but rice, soy, and oat milk are also employed as substitutes. Whether the journey into buying by consumers is now primarily fuelled by health or sustainability concerns or from lactose intolerance, hay fever or dairy allergies, the purchase is simply initiated.

Market Highlight

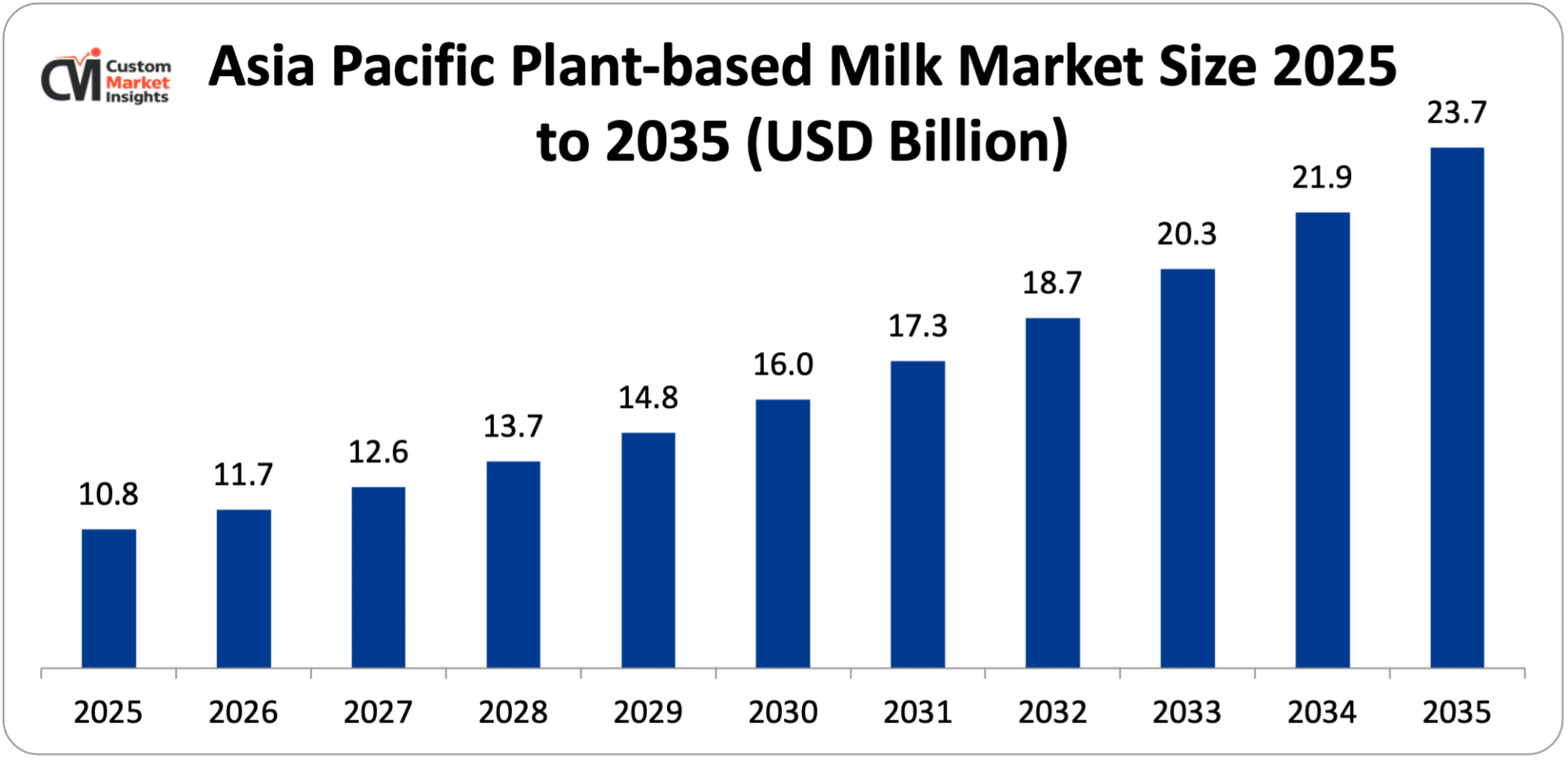

- In 2025, the Asia Pacific will dominate the global market with an estimated market share of 48%. Increasing disposable income and product launches drive the regional expansion.

- Europe is growing at the highest CAGR over the analysis period. The increasing focus towards sustainability drives the industry growth.

- By product, the almond milk segment accounted for the highest revenue share of 58% in 2025.

- By nature, the conventional segment would have the highest share of the market in 2025 of over 80%.

- By flavor, the non-flavored milk segment dominated the market with a revenue share of 65%.

- By sales channel, the hypermarkets & supermarkets segment dominated the market with a share of 42% in 2025.

Significant Growth Factors

The plant-based milk market trends present significant growth opportunities due to several factors:

- Rising Lactose Intolerance & Dairy Allergies: Increasing cases of lactose intolerance and dairy allergy are key biological factors that are fueling plant-based milk market growth at a robust CAGR and are supported by scientific grounds. Lactose intolerance—the inability to digest lactose or milk sugar—is caused by a lack of the enzyme ‘lactase’ in the small intestine that converts or causes digestion of lactose into a digestible form, resulting in symptoms like loose stool and diarrhea, bloating, and stomach pain. As per global health survey reports, around 65-68% of the world suffers from varying degrees of lactose malabsorption; 70-100% of the population in Asia and Africa—including a significant share of the Indian population—is affected. Further, cow‘s milk allergy, an immune system response to milk proteins (casein, whey), can affect 0.5-3% of infants worldwide, and some studies have reported it to be as high as 2-7.5% in children—resulting in total dairy avoidance due to severe allergic reactions. This provides a ready consumer base that cannot or will not consume market in traditional milk, resulting in bountiful opportunities for plant-based milk substitutes.

- Growing Health Consciousness: The rising health consciousness of consumers is another main reason for the fast growth of plant-based milk, as consumers surely agree that they focus on the health benefits, nutrition education, and disease prevention of their foods. As evidenced by science and nutrition research, plant-based milk contains less saturated fat and zero cholesterol, contributing to cardiovascular health and the goal set up by health authorities for everyone to keep animal fat or its derivative to a minimum. Furthermore, some milk, which is made from plants, is enriched with a greater amount of nutrients, e.g. Calcium, vitamin D, and B12, to compete with or surpass the nutritional quality of milk. In addition to the efficiency of nutrition quality, the health concern also enables young and middle-aged consumers’ populations to be more willing to choose low-calorie, plant-based drinks, especially in urban areas, as the drinks can help consumers to keep fit and healthy weight with a stable blood sugar. In addition to the positive connection, the health trend has been further strengthened by the increased awareness of more natural “clean-label” products, non-dairy milk, lactose-free products, or functional products.

What are the Major Advances Changing the Plant-based Milk Market Today?

- Next-generation Ingredient Innovation: The next generation ingredient innovation is an advancement in the field of plant-based milk, where the industry is moving beyond traditional soy and almond-based milk to create high protein, multi-ingredient, and functionally superior products. Ripple Foods is an example where an advanced plant-based milk product was developed by the company in 2026 based on yellow pea protein, which is much higher in protein and creaminess than traditional plant-based milk. This is an advancement over one of the major scientific challenges with traditional plant-based milk products, where the protein content was very low. This is an advancement over traditional milk from an environmental point of view, where the product is much lower in water usage than traditional dairy-based milk. Another example is Califia Farms, where a multi-plant protein-based milk product was developed by the company in 2024 based on a blend of pea protein, chickpea protein, and fava bean protein, which provides all the essential amino acids and other nutritional benefits. This is an advancement over traditional plant-based milk products, where the industry is moving towards composite ingredient-based products where several plants are blended to provide the best taste, texture, and nutritional benefits. In addition, this innovation is now moving beyond traditional soy and pea-based products to include pistachio, chia, and oats, where the industry is working to provide much better taste and texture, which were some of the major issues with traditional plant-based milk products. Industry reports suggest that this is now an advancement over traditional product development, where the industry is working to provide protein standardization, taste masking, and other improvements to ensure repeat consumer acceptability. These product launches suggest that next-generation ingredient innovation is not just incremental but structural, where plant-based milk is now much closer to traditional dairy milk and is much faster than traditional milk.

- Sustainability & Low-impact Processing: Sustainability and low impact processing have been two important developments in the world of plant-based milk products, which have been fueled by the increasing environmental issues in the world and the need for sustainability in food processing. Several studies have confirmed the low impact processing of plant-based milk products on greenhouse emissions, land use, and water usage compared to traditional dairy milk. Several studies have confirmed that dairy milk is responsible for three times more greenhouse emissions compared to oat milk or soy milk. Moreover, plant-based milk products have been confirmed to have lower land use compared to traditional dairy milk. Moreover, plant-based milk products, such as oat milk, have been confirmed to have lower water usage compared to traditional dairy milk. These trends have been supported by the development of low impact processing technology and innovation in the supply chain for the reduction of waste and energy consumption in processing plant-based milk products. In addition, sustainability has been considered a key parameter in plant milk processing with companies selecting crops to be used for processing plant-based milk products based on their sustainability. Another important factor is the innovation in plant-based milk cartons, as several companies have started using recyclable plant-based milk cartons or plant-based milk cartons in order to reduce plastic usage in packaging plant-based milk products. Moreover, plant-based milk products have been confirmed to be a means of sustainability and environmental conservation while aligning with the global fight against climate change.

Category Wise Insights

By Product

Why Almond Milk Hold a Prominent Position in the Market?

The almond milk segment accounted for the highest revenue share of 58% in 2025. Almond milk is targeted to be a more attractive product among other plant milk drinks, as it is lower in calories. Almond milk offers nutrients, as it is loaded with vitamin E content that contributes to its status as a popular drink among consumers. Also, Almond Breeze and Silk are some of the pioneers that take almond milk to new heights through their aggressive marketing for the benefits of such products and their uses. They influence consumers and give them a convenient and speedy shopping experience and make the product a familiar and trusted choice among consumers. This led to almond milk‘s substantial growth and acceptance worldwide during the forecast period.

The oat milk segment is growing at a high CAGR of 9.8% during the forecast period. Consumers can also gain essential nutrients from oat milk. It is known for having a high level of dietary fiber, especially beta-glucan, which has been found to be effective in reducing the level of cholesterol. As well as this, it can contain a higher level of protein compared to other plant-based milks. In addition, new advances in the processing of oat milk are reaching the market to ensure that high-quality products are being used to address the demand from customers for flavored oat milk, added oat milk, and oat-based creamers, so it is predicted that this factor will drive the oat milk market growth in the forecast period.

By Nature

Why Conventional Capture the Highest Market Share in the Plant-based Milk Market?

The conventional segment would have the highest share of the market in 2025 of over 80%. Conventional plant-based milk has a slightly complex distribution network. It is easily available in supermarkets, grocery stores, and even in convenience stores. Many people prefer easily available options for their ease of purchase. Conventional plant-based milk is also cheaper than its organic counterpart, which makes it more economical for the consumers, thus easily accessible. Due to easy accessibility, conventional plant-based milk is expected to maintain its dominance during the forecast period.

The organic segment is growing at a rapid rate over the projected period. There is an increasing consumer trend toward organic products because of the health benefits they perceive. Organic plant-based milk does not contain any synthetic fertilizers and pesticides, which attract health-conscious consumers. The rising consciousness over the health hazards of synthetic additives also boosts its demand. Moreover, the rising number of launches of organic plant-based milk by manufacturers is estimated to increase its growth during the forecast period. For instance, in June 2024, Milkadamia launched the first USDA organic range of premium plant-based milks containing shelf‐stable Macadamia Nut Milk in the United States.

By Flavor

Why does the Non-Flavored Milk Dominates the Plant-based Milk Market?

The non-flavored milk segment dominated the market with a revenue share of 65%. In the plant-based milk market. Non-flavored plant-based milks are expected to be highly versatile and can be used for a wide range of purposes, from culinary applications to blending with different ingredients. Such features are further expected to support the high market presence of non-flavored milk. Additionally, a large number of consumers believe that no-flavor plant-based milks are as healthy as compared to flavored plant-based milks, which mainly contain additional sugar and flavor additives. Flavored plant-based milks are not appreciated by health-conscious people as non-flavored plant-based milks are considered much healthier and are preferred for preventing intake of excess sugars, which is further estimated to drive their market demand during the forecast period.

The flavored milk segment is growing at a prominent rate over the projected period. Flavored plant-based milk offers consumers diverse tastes and preferences, such as chocolate, vanilla, strawberry, and so on. Flavored plant-based milk provides more taste for consumers. Flavored plant-based milk can attract children as well as those who think unflavored plant-based milk is tasteless. Furthermore, different flavors introduced by manufacturers can get consumers’ attention, and people would be keen on more unique tastes in different seasons and limited-edition flavors. These factors are expected to give a boost to sales growth of the plant-based milk in the forecast period.

By Sales Channel

How Does the Hypermarkets & Supermarkets Sales Channel Capture a Prominent Market Share in the Plant-based Milk Market?

The hypermarkets & supermarkets segment dominated the market with a share of 42% in 2025. Hypermarkets and supermarkets have very extensive coverage and are accessible to many consumers. They are located conveniently and attract a large number of customers; therefore, these are the favorite shopping places for most of the consumers. As they stock a large number of plant-based milk products from various brands, they offer a multitude of products for consumers to choose and compare. This falls under the best-selling channel for any product.

The online segment is growing at a moderate rate over the projected period. The growing smartphone adoption along with internet penetration drives the industry growth.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 24.2 billion |

| Projected Market Size in 2035 | USD 46.4 billion |

| Market Size in 2025 | USD 22.5 billion |

| CAGR Growth Rate | 7.5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Product, Nature, Flavor, Sales Channel and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Plant-based Milk Market Size?

Its market size, in terms of the Asia Pacific Plant-based Milk, is projected to be USD 10.8 billion in 2025 with a growth of about USD 23.7 billion in 2035 with a CAGR of 8.2% between 2026 and 2035.

Why did the Asia Pacific Dominate the Plant-based Milk Market in 2025?

In 2025, the Asia Pacific will dominate the global market with an estimated market share of 48%. Vegetarianism and veganism are on the rise, and there are increasing concerns of animal cruelty. These are likely to further lead to demand for Plant based milks (PBM). Similarly, many traditional country-specific diets, which are similar to that of India, such as vegetarian diets, will further fuel the demand of PBM. The influence of western diets is also rising, with plant based diets gaining popularity across the world. Younger generations (who are more accepting of changes in diets) are the key drivers of demand during the forecast period.

India Plant-based Milk Market Trends

In the Asia Pacific region, India is growing at a significant rate over the projected period. The increasing health awareness among the population and rising disposable income drive the country’s market growth.

Why is Europe Experiencing a Significant Growth in the Plant-based Milk Market?

Europe holds a significant market share in 2025. The policies implemented by the European Union, promoting sustainable agriculture and decreasing its impact on the environment, are indirectly aiding the growth of the plant-based milk market. Through subsidies and incentives to farmers for planting crops that go into plant-based milks, as well as labeling policies that ensure transparency, these are also aiding in the growth of the market. In addition, as the popularity in the European region for veganism and vegetarianism increases, the market grows, as there are a number of benefits for flexitarians.

UK Plant-based Milk Market Trends

The UK held the dominant position in the market in 2025. The increasing adoption of plant-based diets and increasing emphasis on sustainable agriculture drives the market growth.

Why is North America Growing at the Moderate Rate in the Plant-based Milk Market?

North America is expected to grow at a moderate rate over the projected period. The growth is owing to the presence of big players, and rising health consciousness among individuals drives the industry growth.

US Plant-based Milk Market Trends

The US holds the prominent market share in the industry. The growing prevalence of type 2 diabetes and increasing emphasis on preventive healthcare among the population drives the industry growth in the area.

Why is the Middle East & Africa Region is growing rapidly in the Plant-based Milk?

The MEA region is growing at a steady rate over the projected period. A large one driving market growth is increasing disposable income and premiumization in certain parts of the region, particularly the Gulf states. Although Plant-based milk products remain discounted, well-off consumers are making themselves willing to spend on the health and eco benefits.

UAE Plant-based Milk Market Trends

The UAE is growing at the highest CAGR during the forecast period. The expansion of online retailing is driving the industry growth.

Top Players in the Plant-based Milk Market and Their Offerings

- Alpro (Danone)

- Blue Diamond Growers

- Califia Farms LLC

- Daiya Foods Inc.

- Danone S.A.

- Earth’s Own Food Company Inc.

- Eden Foods Inc.

- Elmhurst Milked Direct LLC

- Forager Project

- Freedom Foods Group Limited

- Good Karma Foods

- MALK Organics

- Oatly AB

- Pacific Foods of Oregon LLC

- Plenish

- Ripple Foods

- Others

Key Developments

Plant-based milk market has experienced considerable changes in the last two years as the market players are trying to diversify their technological aspects and develop product portfolios using strategic approaches.

- In June 2025, HRX, a fitness and lifestyle brand, has launched plant-based oat milk protein shakes, expanding into the nutrition sector. Using oat milk as its base, this plant-powered shake delivers 25g of protein per 200ml serving, making it a clean and effective option for daily protein intake. It contains no processed sugar, making it an ideal choice for those seeking a natural, nutritious boost. HRX’s oat milk protein shake is a 100 percent dairy-free and lactose-free beverage, specially crafted for today’s health-conscious and active individuals. (https://dairybusinessmea.com/2025/06/17/hrx-expands-into-indias-nutrition-market-with-launch-of-plant-based-oat-milk-protein-shakes/)

- In November 2025, Danone has announced the launch of Silk Protein, a range of plant-based milks with 13g of complete protein and 3g of fibre per serving. (https://www.greenqueen.com.hk/danone-silk-high-protein-milk-plant-based-dairy-glp-1/)

These strategic measures have enabled the companies to reinforce their competitive positions, increase the product line, boost their technological competencies and also seize growth opportunities in the fast-growing plant-based milk market.

The Plant-based Milk Market is segmented as follows:

By Product

- Almond Milk

- Soy Milk

- Oat Milk

- Coconut Milk

- Pea Milk

- Rice Milk

- Others

By Nature

- Organic

- Conventional

By Flavor

- Flavored Milk

- Non-Flavored Milk

By Sales Channel

- Hypermarkets & Supermarkets

- Online

- Specialty Stores

- Others

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Plant-based Milk by Segments

- 2.1.2. Plant-based Milk by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Plant-based Milk Market Attractiveness Analysis, By Product

- 2.2.3. Plant-based Milk Market Attractiveness Analysis, By Nature

- 2.2.4. Plant-based Milk Market Attractiveness Analysis, By Flavor

- 2.2.5. Plant-based Milk Market Attractiveness Analysis, By Sales Channel

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Rising Lactose Intolerance & Dairy Allergies

- 3.1.2. Growing Health Consciousness

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Plant-based Milk Market – By Product

- 4.1. Product Market Overview, By Product Segment

- 4.1.1. Plant-based Milk Market Revenue Share, By Product, 2025 & 2035

- 4.1.2. Almond Milk

- 4.1.3. Plant-based Milk Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Soy Milk

- 4.1.7. Plant-based Milk Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Oat Milk

- 4.1.11. Plant-based Milk Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Coconut Milk

- 4.1.15. Plant-based Milk Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Pea Milk

- 4.1.19. Plant-based Milk Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Rice Milk

- 4.1.23. Plant-based Milk Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1.26. Others

- 4.1.27. Plant-based Milk Share Forecast, By Region (USD Billion)

- 4.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.29. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Product Market Overview, By Product Segment

- Chapter 5. Plant-based Milk Market – By Nature

- 5.1. Nature Market Overview, By Nature Segment

- 5.1.1. Plant-based Milk Market Revenue Share, By Nature, 2025 & 2035

- 5.1.2. Organic

- 5.1.3. Plant-based Milk Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Conventional

- 5.1.7. Plant-based Milk Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Nature Market Overview, By Nature Segment

- Chapter 6. Plant-based Milk Market – By Flavor

- 6.1. Flavor Market Overview, By Flavor Segment

- 6.1.1. Plant-based Milk Market Revenue Share, By Flavor, 2025 & 2035

- 6.1.2. Flavored Milk

- 6.1.3. Plant-based Milk Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Non-Flavored Milk

- 6.1.7. Plant-based Milk Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Flavor Market Overview, By Flavor Segment

- Chapter 7. Plant-based Milk Market – By Sales Channel

- 7.1. Sales Channel Market Overview, By Sales Channel Segment

- 7.1.1. Plant-based Milk Market Revenue Share, By Sales Channel, 2025 & 2035

- 7.1.2. Hypermarkets & Supermarkets

- 7.1.3. Plant-based Milk Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Online

- 7.1.7. Plant-based Milk Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Specialty Stores

- 7.1.11. Plant-based Milk Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Others

- 7.1.15. Plant-based Milk Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Sales Channel Market Overview, By Sales Channel Segment

- Chapter 8. Plant-based Milk Market – Regional Analysis

- 8.1. Plant-based Milk Market Overview, By Region Segment

- 8.1.1. Global Plant-based Milk Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Plant-based Milk Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Plant-based Milk Market Revenue, By Product, 2026 – 2035

- 8.1.4. Global Plant-based Milk Market Revenue, By Nature, 2026 – 2035

- 8.1.5. Global Plant-based Milk Market Revenue, By Flavor, 2026 – 2035

- 8.1.6. Global Plant-based Milk Market Revenue, By Sales Channel, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Plant-based Milk Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Plant-based Milk Market Revenue, By Product, 2026 – 2035

- 8.2.3. North America Plant-based Milk Market Revenue, By Nature, 2026 – 2035

- 8.2.4. North America Plant-based Milk Market Revenue, By Flavor, 2026 – 2035

- 8.2.5. North America Plant-based Milk Market Revenue, By Sales Channel, 2026 – 2035

- 8.2.6. U.S. Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Plant-based Milk Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Plant-based Milk Market Revenue, By Product, 2026 – 2035

- 8.3.3. Europe Plant-based Milk Market Revenue, By Nature, 2026 – 2035

- 8.3.4. Europe Plant-based Milk Market Revenue, By Flavor, 2026 – 2035

- 8.3.5. Europe Plant-based Milk Market Revenue, By Sales Channel, 2026 – 2035

- 8.3.6. Germany Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Plant-based Milk Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Plant-based Milk Market Revenue, By Product, 2026 – 2035

- 8.4.3. Asia Pacific Plant-based Milk Market Revenue, By Nature, 2026 – 2035

- 8.4.4. Asia Pacific Plant-based Milk Market Revenue, By Flavor, 2026 – 2035

- 8.4.5. Asia Pacific Plant-based Milk Market Revenue, By Sales Channel, 2026 – 2035

- 8.4.6. China Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Plant-based Milk Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Plant-based Milk Market Revenue, By Product, 2026 – 2035

- 8.5.3. The Middle-East and Africa Plant-based Milk Market Revenue, By Nature, 2026 – 2035

- 8.5.4. The Middle-East and Africa Plant-based Milk Market Revenue, By Flavor, 2026 – 2035

- 8.5.5. The Middle-East and Africa Plant-based Milk Market Revenue, By Sales Channel, 2026 – 2035

- 8.5.6. Saudi Arabia Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Plant-based Milk Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Plant-based Milk Market Revenue, By Product, 2026 – 2035

- 8.6.3. Latin America Plant-based Milk Market Revenue, By Nature, 2026 – 2035

- 8.6.4. Latin America Plant-based Milk Market Revenue, By Flavor, 2026 – 2035

- 8.6.5. Latin America Plant-based Milk Market Revenue, By Sales Channel, 2026 – 2035

- 8.6.6. Brazil Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Plant-based Milk Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Plant-based Milk Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Plant-based Milk Market: Company Market Share, 2025

- 9.2. Global Plant-based Milk Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Alpro (Danone)

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Blue Diamond Growers

- 10.3. Califia Farms LLC

- 10.4. Daiya Foods Inc.

- 10.5. Danone S.A.

- 10.6. Earth’s Own Food Company Inc.

- 10.7. Eden Foods Inc.

- 10.8. Elmhurst Milked Direct LLC

- 10.9. Forager Project

- 10.10. Freedom Foods Group Limited

- 10.11. Good Karma Foods

- 10.12. MALK Organics

- 10.13. Oatly AB

- 10.14. Pacific Foods of Oregon LLC

- 10.15. Plenish

- 10.16. Ripple Foods

- 10.17. Others.

- 10.1. Alpro (Danone)

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 33

List Of Tables

Tables No 1 to 51

Prominent Player

- Alpro (Danone)

- Blue Diamond Growers

- Califia Farms LLC

- Daiya Foods Inc.

- Danone S.A.

- Earth’s Own Food Company Inc.

- Eden Foods Inc.

- Elmhurst Milked Direct LLC

- Forager Project

- Freedom Foods Group Limited

- Good Karma Foods

- MALK Organics

- Oatly AB

- Pacific Foods of Oregon LLC

- Plenish

- Ripple Foods

- Others

FAQs

The key players in the market are Alpro (Danone), Blue Diamond Growers, Califia Farms LLC, Daiya Foods Inc., Danone S.A., Earth’s Own Food Company Inc., Eden Foods Inc., Elmhurst Milked Direct LLC, Forager Project, Freedom Foods Group Limited, Good Karma Foods, MALK Organics, Oatly AB, Pacific Foods of Oregon LLC, Plenish, Ripple Foods, Others.

Government regulations shape the market by setting labeling standards, safety requirements, and subsidy policies, which can either encourage growth through support and clarity or slow adoption through restrictions and compliance costs.

Higher prices tend to slow adoption by limiting accessibility, while competitive pricing accelerates market growth by making plant-based milk affordable to a broader consumer base.

According to the present analysis and forecast modeling, the market of plant-based milk will witness a significant growth of about USD 46.4 billion in the year 2035 with the growing innovative product launch, increasing collaboration, and rising disposable income with a CAGR of 7.5% between the years 2026 and 2035.

It is projected that the Asia Pacific will hold the largest market share in the plant-based milk market in the forecast period, with a share of about 48% of the global market share, which is attributed to the increasing disposable income of the population and key player expansion in the developing market.

Europe is expected to grow at the highest rate during the forecast period. The growth in the region is owing to the growing demand for sustainability.

The key factors driving the market are health and wellness trends, environmental sustainability concerns, a rising vegan and vegetarian population, product innovation and diversification, global market expansion, and partnerships and collaborations.