Wood Plastic Composite (WPC) Decking Market Size, Trends and Insights By Product Type (Hollow WPC Decking (Lightweight, Structural Hollow Core Profiles), Solid WPC Decking (Dense Core, Heavy-Duty Profiles), Other Product Types (Grooved WPC for Hidden Fastening, Specialty Profiles)), By Polymer Type (Polyethylene-Based WPC (HDPE, LDPE, Post-Consumer PE Film), Polypropylene-Based WPC (Virgin PP, Recycled PP), Polyvinyl Chloride-Based WPC (PVC-Wood Composite), Other Polymer Types (Mixed Polymer, Biopolymer Blends)), By Application (Residential Decking (Private Homes, Apartments, Balconies), Commercial Decking (Hotels, Restaurants, Office Buildings, Retail), Industrial & Infrastructure Decking (Marinas, Boardwalks, Parks, Transit), Other Applications (Rooftop Decking, Pool Surrounds, Garden Pathways)), By Distribution Channel (Retail Stores (Home Improvement Centers, Specialist Decking Retailers), Direct Sales (Contractor Direct, Builder Programs), Online Channels (E-Commerce, Manufacturer Direct-to-Consumer), Other Distribution Channels (Distributor Networks, Export Trade)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 7.8%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- Trex Company Inc.

- AZEK Building Products Inc.

- Fiberon LLC (Fortune Brands)

- TimberTech (AZEK)

- Others

Reports Description

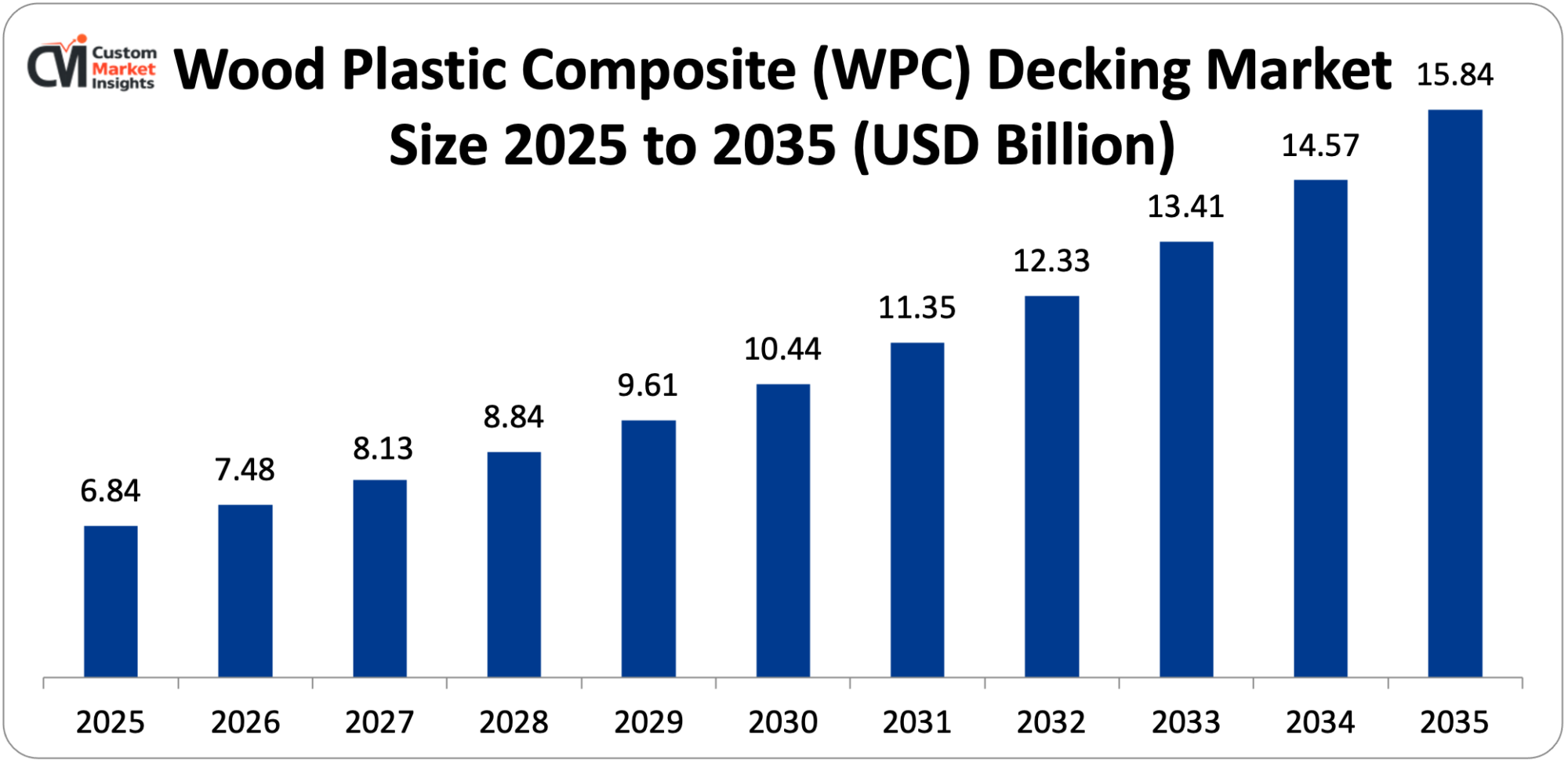

The wood plastic composite decking market is expected to reach USD 15.84 billion by 2035 at a CAGR of 7.8% from 2026 to 2035, with the global market value projected to be USD 6.84 billion in 2025.

Market Highlight

- In 2025, North America held the largest share in the WPC decking market with 42% of the market.

- Asia Pacific is projected to show the highest CAGR at 10.8% during the forecast period (2026-2035).

- Based on product type, the hollow WPC decking accounted for around 54% market share in 2025.

- The solid WPC decking market is expanding the fastest at a CAGR of 8.6% during the forecast period (2026–2035).

- By polymer type, the polyethylene-based WPC dominated the market in 2025 accounting for 52% of the market share, while the polypropylene-based WPC is projected to grow at the fastest CAGR of 9.4% over the forecast period from 2026 to 2035.

- In terms of market share, the residential decking accounted for the highest share of 62% in 2025, while the commercial decking segment is projected to grow at the highest CAGR of 8.8% during 2026–35.

- On a distribution channel basis, the retail stores accounted for the largest market share in 2025, and the online channels segment is projected to grow at the fastest CAGR of 11.4% during 2026-35.

Impact of Middle East war on Wood Plastic Composite (WPC) Decking Market

The supply chain of raw materials, including plastics, resins, and wood additives required to produce WPC decking has been impacted by the Middle East war. The increasing prices of crude oil have caused the increase in costs associated with WPC decking production and shipping, thus affecting its pricing. There has been a reduction in construction activities in regions experiencing the effects of conflict, hence decreased demand for WPC decking products.

Significant Growth Factors

The Wood Plastic Composite (WPC) Decking Market Trends present significant growth opportunities due to several factors:

- Outdoor Living Space Investment Boom and Premium Deck Specification Driving Residential Demand: The most significant consumer market demand for WPC decking is being generated by the high value of decking projects, combined with the homeowner’s high quality and longevity expectations, leading to the highest possible specification of the decking material in accordance with the value of the project. The value escalation of the outdoor living market, as average U.S. residential project values for outdoor decking increase exponentially due to the increasing complexity of deck project combinations (multiple levels, multiple deck/cover combinations, premium composite decking material specifications), leads to an increase in the demand for premium WPC decking products, where the higher material cost is only a fraction of the total project value at elevated project values. Data from the North American Deck and Railing Association (NADRA) demonstrates that the consumer has been gradually accepting the value that composite decking offers when compared to pressure-treated lumber, as composite decking’s 25-year warranty, low maintenance needs, and consistent appearance over time prove to be more valuable in the long term than the low initial cost of pressure-treated lumber that is offset by the cost of annual maintenance and the eventual need to replace the deck structure due to rot and insect damage and the consumer’s realization that pressure-treated lumber is losing its aesthetic value over time. The value return on deck investment, which invariably shows a homeowner a 65-80% ROI on the professionally built outdoor deck, is the financial argument that can be made in how much value return a home can reap on deck investment beyond the lifestyle benefit equation.

- Sustainability Imperatives and Tropical Timber Substitution Driving Commercial Specification: The convergence of tightening regulatory controls on tropical timber harvesting and trade (EU Timber Regulation/EU Deforestation Regulation requiring documented legal harvesting origin and deforestation-free supply chain documentation for all wood products placed on the EU market, U.S. Lacey Act provisions prohibiting the import of illegally harvested timber and progressive tightening of FSC certification requirements that reduce commercially available certified tropical hardwood supply) with the construction industry’s increasing environmental specification requirements for building material sustainability credentials is driving strong regulatory and commercial momentum toward WPC decking specification as a verified sustainable alternative to tropical hardwood decking, whose supply chain documentation requirements are creating significant procurement risk and compliance burden for architects, contractors and facility managers. The EU Deforestation Regulation (EUTR) due diligence rules, which will apply to timber products from tropical areas entering the EU from December 2024, impose compliance documentation requirements on manufacturers of imported tropical hardwood decking, introducing complexity in procurement, audit costs, and supply security risk that is completely avoided through the WPC decking supply chain structure. Leading WPC products with verified EPD documentation to demonstrate the embodied carbon content are starting to be used as a standard requirement for the specification in commercial buildings and are creating green building certification motivation.

What are the Major Advances Changing the WPC Decking Market Today?

- Advanced Capping Technology and Four-Sided Cap Protection Transforming Product Performance: Four-sided full encapsulation significantly expanded the performance envelope of WPC decking as well as its value proposition to consumers compared to the first-generation uncapped WPC products that held the early market for composite decking, because those early products were constrained by water absorption, surface staining, mold growth, and fading of colors that limited consumer acceptance of the category. First generation WPCs made by extrusion of wood fibre and polymer blends without surface capping exposed the wood fiber component at the deck surface and exposed edges to moisture, allowing it to absorb moisture through exposed wood fibre which produced surface swelling and growth of mould, which would provide a nutrient substrate for biofilm development in the wood fibre matrix; and surface staining due to tannin release and iron reaction that was difficult to clean away without using aggressive chemical cleaning that was incompatible with the integrity of the plastic component. The co-extruded polymer cap, which is applied as a thin 1-3 mm thick layer of mineral filled HDPE, ASA or acrylic modified polymer during the extrusion process to cover the composite core, provides a moisture impermeable surface layer that prevents interaction of the wood fiber with moisture, resists the surface staining mechanisms that affected uncapped products, has an inherent mold resistance surface character due to the elimination of organic fiber substrate at the exposed surface, and can be embossed with the high definition wood grain texture and consistency of color that is far better accommodated by the smooth surface character of the cap as opposed to the rougher composite surface. Leading WPC manufacturers have been able to offer 25 years of fade and stain warranty coverage, an achievement impossible without the cap polymer’s UV stability; the warranty differentiation has enabled them to charge and sell premium prices and gain consumer confidence.

- Recycled Content Integration and Circular Economy Material Development: The innovative and progressive increase in post-consumer recycled plastic (PCR) in the formulations of WPC decking, ranging from 10–20% PCR to 95–100% PCR, represents a significant improvement in the environmental sustainability profile of this material and also has the potential to create material narratives that play to the very environmentally conscious consumer segment that is driving the specification decisions for premium WPC. Post-consumer recycled plastic integration challenge, with the post-consumer HDPE film streams from grocery bags, agricultural film, or industrial packaging collection programs, all contaminated, coloured and rheologically unpredictable, has been gradually overcome by better sorting and washing technology at plastic reclaim facilities and by the development of WPCs, which allow for variability in recycled content within the parameters of the extrusion process required to ensure dimensional and structural uniformity in decking profiles. The manufacturing of Trex’s composite decking products using nearly 95% post-consumer content, including 1.5 billion pounds of polyethylene film per year from major U.S. grocery retailer chain grocery bag collection programs, is the largest-scale commercial implementation of a circular economy WPC material flow, positioning Trex as the market volume leader and the sustainability credential standard for which competing WPC manufacturers are benchmarked by consumers and commercial specifiers who are aware of the environment. The reclaimed wood fiber dimension of WPC’s recycled content is consistent with responsible forest resource utilization principles which are understood as preferred sourcing of wood fiber in wood containing building products in FSC certification frameworks, where sawmill residuals, planer shavings and recovered wood fiber from demolished wood products are used as a functional replacement for virgin wood fiber in the manufacture of WPCs.

- Surface Texture and Aesthetic Innovation Closing the Visual Gap with Natural Wood: This marked significant progression in the aesthetics of the WPC decking surface, with the deepening and more 3-D embossing die technology allowing a deeper and more varied wood grain reproduction; the multi-tone color variegation systems, which are achieved by introducing a colour variation within each board, which loosely replicates the figure variation of natural wood grain, and the ability to be brushed to produce a surface texture differentiation from smooth composite surfaces; and the commercial use of wider board profiles, up to 200 mm face width, has reduced the aesthetic gap with natural wood decking boards in prestige residential and commercial applications where close inspection of the surface is a determining factor in material selection. The multi-tone variegated colour system, using proprietary co-extrusion die technology to produce multiple streams of color, is the biggest aesthetic breakthrough that has put WPC boards on par with the visual appearance of close inspection of premium hardwood decking that brings a complex surface character to the board. The reversible decking board development with two different surface patterns on either side of the same board that allows the installer or homeowner to choose the preferred pattern on the underside of the board and reverse the board for use as the top face after several years of service is a unique service life extension process that no wood decking can offer and offers a tangible service benefit to consumers that goes beyond aesthetics alone, justifying a premium price.

Category Wise Insights

By Product Type

Why Does Hollow WPC Decking Lead the Market?

At around 54% of the total product type segment, hollow WPC decking is the preferred specification for the majority of residential and commercial deck applications where the key evaluation criteria are commercial and technical advantages of hollow profile construction (lower material content per linear meter of decking, making it cost competitive when compared with solid profiles, reduced weight per board for easier installation by deck installer, and internal drainage channel function that allows moisture trapped on decking surface beneath fastener penetrations to drain through the hollow center of the profile instead of accumulating within it); and therefore it is the most dominant product type segment. The market dominance of the hollow WPC segment is the result of the most prevalent application volume category, residential deck replacement and new construction, in which homeowners and contractors seek to maximize structure, material cost, and installation efficiency, all of which hollow profiles provide. The solid specification is the fastest growing with a CAGR of 8.6% from 2026 to 2035, reflecting the rising specification of solid sections in heavy duty commercial, marina and public infrastructure applications where the improved compressive strength, superior fastener pull-out resistance, and increased span capability of solid sections are considered to justify the higher material cost, as well as the growing premium residential specification of solid decking at feature deck projects where structural robustness and premium feel underfoot is differentiating the installation quality.

By Polymer Type

Why Does Polyethylene-Based WPC Lead the Market?

Polyethylene-based WPCs will be the largest polymer type in 2025, accounting for about 52% of market share, as polyethylene has been the primary polymer matrix material for the WPC decking market for 20 years, making it the most optimized polymer-wood fiber composite currently available for the decking market and specification requirements. Nearly all decking boards are made with a 100% recycled content of post-consumer (PC) HDPE film from leading manufacturers of PE-WPC, resulting from the recycled-content supply chain developed for grocery bag and agricultural film collection programs, with its flexibility and impact resistance properties, PE-WPC is the dominant market product type. Polypropylene based WPC is expected to see the highest growth rate at 9.4% CAGR from 2026 to 2035, as polypropylene based WPC offers a higher stiffness-to-weight ratio, which in turn allows a longer span capacity and reduces board deflection underfoot, giving it better resistance to elevated temperature softening under intense summer sun exposure than HDPE based products; and a higher rate of adoption by WPC manufacturers in Europe for use in the commercial and infrastructure application segment where structural performance requirements favor PP’s superior mechanical stiffness.

By Application

Why Does Residential Decking Lead the Market?

The homeowner market is the foundation and most commercially developed user base of decking, at about 62% of the total decking market, and with the U.S. residential deck construction and replacement market being the world’s largest single application market for WPC decking by installation volume, as the outdoor living investment trend has continued after the pandemic due to the growing consumer education about WPC’s maintenance free life cycle advantages, and as the documented property value return from the investment of deck construction continues to propel decking project specification away from pressure-treated lumber toward composite across the deck project spectrum. Commercial decks are growing at the fastest rate at 8.8% CAGR 2026-35, as outdoor dining, terrace and pool decks are increasingly being constructed in hospitality applications, while WPC’s commercial durability and slip resistance compliance for public area specifications and low maintenance needs across high traffic public areas offer operational and lifecycle cost benefits, and the public infrastructure specification of WPC at urban parks, waterfront boardwalks, and transit station platforms where durability and maintenance minimization are prime procurement considerations.

By Distribution Channel

Why Do Retail Stores Lead the Market?

Retail stores lead the pack at about 44%, as the home improvement retail channel is the most important consumer touchpoint for decking purchases, with the major home improvement stores in North America (such as The Home Depot and Lowe’s) and equivalent national home improvement retail chains in Europe providing the homeowner with the physical display, sample selection, and convenience of purchase that homeowners planning deck projects leverage as their primary product discovery and specification source point. The online segment is on track for the highest growth with a CAGR of 11.4% between 2026 and 2035, enabled by the rollout of AR visualization tools, online deck configurators and the full e-commerce capability for materials, which are increasingly making it possible to sell composite decking projects online without the involvement of the physical retail store, especially to the design-engaged homeowner market segment who are most at ease with a digital sales journey for major home improvement investments.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 7.48 billion |

| Projected Market Size in 2035 | USD 15.84 billion |

| Market Size in 2025 | USD 6.84 billion |

| CAGR Growth Rate | 7.8% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Product Type, Polymer Type, Application, Distribution Channel and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the North America Market Size?

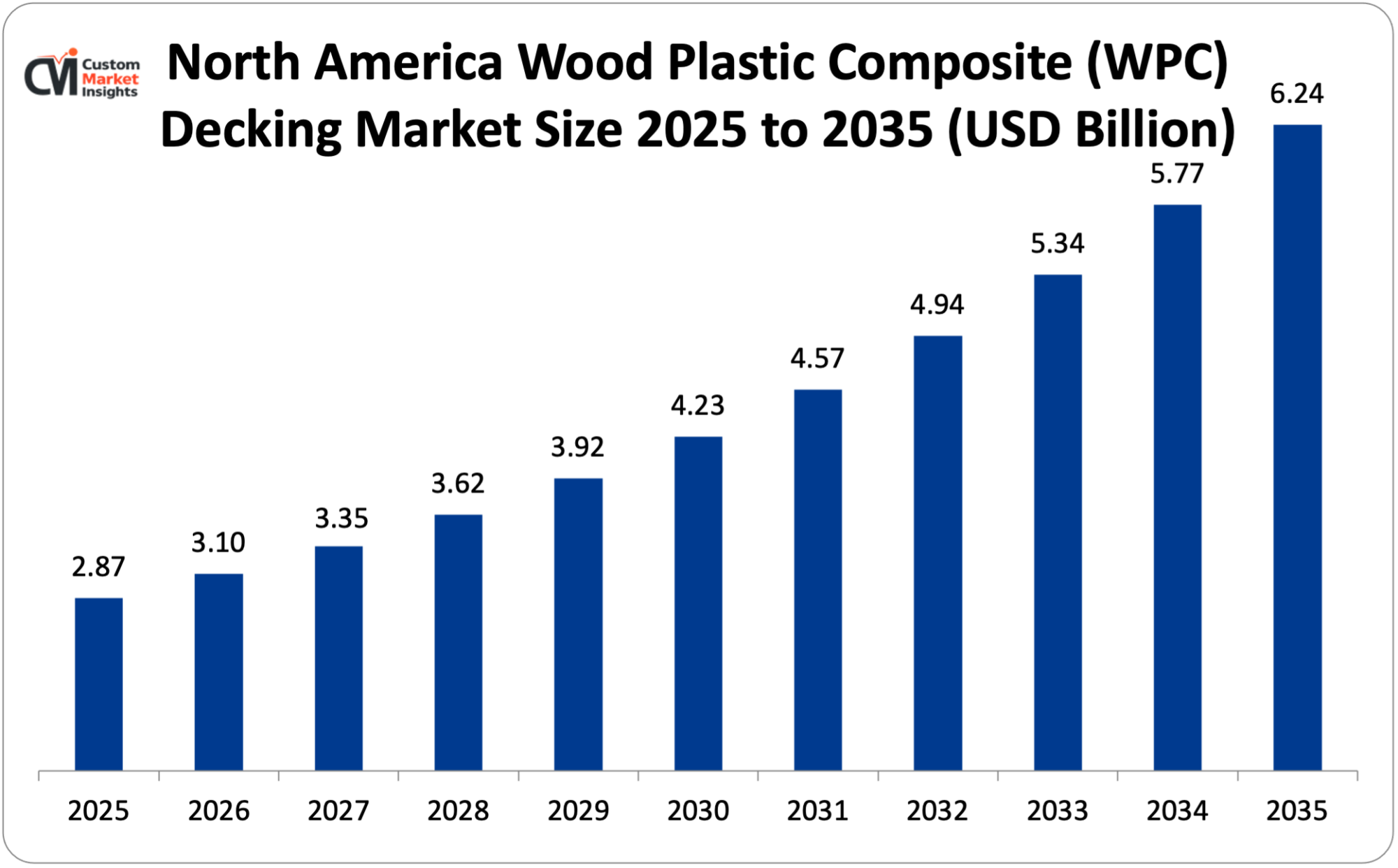

The North American WPC decking market size is estimated at USD 2.87 billion in 2025 and is projected to reach approximately USD 6.24 billion by 2035, with a CAGR of 8.1% from 2026 to 2035.

Why Did North America Dominate the Market in 2025?

North America has roughly 42% of the world’s decking market in 2025, and the United States’ residential decking application is the largest single market application in the world, benefiting from having the most single-family homes with deck building potential, the most advanced awareness and acceptance of composite decking technology, and the most advanced retail distribution infrastructure, in which composite decking technology is a prominent part of the home improvement merchandising strategy for major retail chains, combined with the highest per capita investment in deck projects that justifies the premium price of composite decking.

The U.S. market has been the biggest contributor to the deck market through renovation and replacement projects, as the large installed base of pressure-treated wood decks built in the ’80s to ’00s nears end-of-service life and creates replacement projects where the primary specification for upgrade is composite decking. Canadian homeowners, who invest more heavily in their decks than most in the world, including the many countries without winters, make up a major portion of the Canadian market, especially for premium composites.

Why is Europe a Strategically Important Market?

The European WPC decking market is estimated to be around USD 1.64 billion in 2025 and is expected to grow further to USD 3.38 billion by 2035 with a CAGR of 7.5%. Europe is a strategically important and growing market where the market dynamics are driven by distinctly European factors, such as the EU Deforestation Regulation creating compliance risk for the decking industry from tropical hardwoods, the European construction industry’s progressive adoption of Environmental Product Declaration as a specification requirement, where WPC’s documented recycled content and reduced embodied carbon is a key differentiator and advantage, and the strong Northern European outdoor living culture in Germany, the Netherlands, Scandinavia and the UK, where the decking industry is investing heavily in outdoor homes.

Germany is the biggest market for WPC decking in Europe, supported by the country’s wide garden and outdoor culture, high prevalence of single-family homes and progressive building specification preferences for the environment, which has led to a surge in the adoption of WPCs in Europe. The UK’s high proportion of single-family homes, its progressive building specification preference for the environment, and its large residential renovation market combined with the investment trend for outdoor living makes the UK’s second largest national WPC market in Europe.

Why is Asia Pacific the Fastest-Growing Market?

The growing market in Asia Pacific is expected to have the highest CAGR of 10.8% during the forecast period, assisted by China’s rapidly expanding middle-class consumer demand for investment in their terrace space in residential dwellings as villa and apartment terrace construction is becoming more widespread and popular as an aspirational lifestyle feature.

The establishment of Chinese manufacturing capacity for WPC products, both for local consumption and international export markets, the large and familiar WPC residential decking market in Australia where investment in outdoor living space is a core national lifestyle feature, and the growing market for investment in outdoor living space in the commercial hospitality sector in Southeast Asia, with WPC being specified for terrace applications in resorts, hotels and restaurants. China’s manufacturing base for WPC — with many Chinese manufacturers developing technically superior capped composite products, both for export to established markets and for increased domestic demand.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region shows constant growth in WPC decking market development as the considerable luxury residential and hospitality construction in the region creates specifications for high-end outdoor decking in villas, hotels, resorts and waterfront projects where WPC’s heat resistance, UV color stability, and low maintenance in the harsh Gulf climate give decking performance benefits over that offered by timber or concrete solutions. Saudi Arabia’s NEOM and Vision 2030 construction is driving a major new commercial landscape that demands a specification of outdoor decking, and Australia’s and New Zealand’s well-developed outdoor living culture is adding to the market’s development, alongside the luxury resort and hospitality industry construction within the UAE.

Top Players in the Market and Their Offerings

- Trex Company Inc.

- AZEK Building Products Inc.

- Fiberon LLC (Fortune Brands)

- TimberTech (AZEK)

- Deckorators (UFP Technologies)

- Cali Bamboo

- Boise Cascade

- Zuri Premium Decking (Royal Building Products)

- EverGrain Composite Decking (TAMKO)

- Duralife Decking & Railing

- Universal Forest Products

- Others

Key Developments

Driven by the demand for sustainable, high-quality outdoor decking materials worldwide, the market has seen remarkable advancements, with manufacturers continuously innovating their capping technology, increasing recycled content in products, and meeting the rising demand for eco-friendly options.

- In September 2024: Trex Company launched its Trex Transcend Lineage collection of decking products, claiming that the new four-sided cap formulation delivers a 30% greater surface hardness and scratch resistance compared to the previous generation of Transcend products, while a new die tooling system has increased the pattern depth by 40% to meet homeowner expectations for surface durability and authenticity in the premium residential specification segment.

- In February 2025: AZEK Building Products announced a USD 200 million investment in a new manufacturing facility in Wilmington, Ohio, that will leverage a closed-loop water system to eliminate discharge from the manufacturing process, a dedicated solar power purchase agreement (PPA) for 100% renewable electricity supply, and post-consumer plastic reclaim processing onsite that will allow direct collection of grocery bag film materials to be used in the production of TimberTech composite decking products without the need for middlemen processing the recycled film at reclaim facilities.

The Wood Plastic Composite (WPC) Decking Market is segmented as follows:

By Product Type

- Hollow WPC Decking (Lightweight, Structural Hollow Core Profiles)

- Solid WPC Decking (Dense Core, Heavy-Duty Profiles)

- Other Product Types (Grooved WPC for Hidden Fastening, Specialty Profiles)

By Polymer Type

- Polyethylene-Based WPC (HDPE, LDPE, Post-Consumer PE Film)

- Polypropylene-Based WPC (Virgin PP, Recycled PP)

- Polyvinyl Chloride-Based WPC (PVC-Wood Composite)

- Other Polymer Types (Mixed Polymer, Biopolymer Blends)

By Application

- Residential Decking (Private Homes, Apartments, Balconies)

- Commercial Decking (Hotels, Restaurants, Office Buildings, Retail)

- Industrial & Infrastructure Decking (Marinas, Boardwalks, Parks, Transit)

- Other Applications (Rooftop Decking, Pool Surrounds, Garden Pathways)

By Distribution Channel

- Retail Stores (Home Improvement Centers, Specialist Decking Retailers)

- Direct Sales (Contractor Direct, Builder Programs)

- Online Channels (E-Commerce, Manufacturer Direct-to-Consumer)

- Other Distribution Channels (Distributor Networks, Export Trade)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Wood Plastic Composite (WPC) Decking by Segments

- 2.1.2. Wood Plastic Composite (WPC) Decking by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Wood Plastic Composite (WPC) Decking Market Attractiveness Analysis, By Product Type

- 2.2.3. Wood Plastic Composite (WPC) Decking Market Attractiveness Analysis, By Polymer Type

- 2.2.4. Wood Plastic Composite (WPC) Decking Market Attractiveness Analysis, By Application

- 2.2.5. Wood Plastic Composite (WPC) Decking Market Attractiveness Analysis, By Distribution Channel

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Outdoor Living Space Investment Boom and Premium Deck Specification Driving Residential Demand

- 3.1.2. Sustainability Imperatives and Tropical Timber Substitution Driving Commercial Specification

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Wood Plastic Composite (WPC) Decking Market – By Product Type

- 4.1. Product Type Market Overview, By Product Type Segment

- 4.1.1. Wood Plastic Composite (WPC) Decking Market Revenue Share, By Product Type, 2025 & 2035

- 4.1.2. Hollow WPC Decking (Lightweight, Structural Hollow Core Profiles)

- 4.1.3. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Solid WPC Decking (Dense Core, Heavy-Duty Profiles)

- 4.1.7. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Other Product Types (Grooved WPC for Hidden Fastening, Specialty Profiles)

- 4.1.11. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Product Type Market Overview, By Product Type Segment

- Chapter 5. Wood Plastic Composite (WPC) Decking Market – By Polymer Type

- 5.1. Polymer Type Market Overview, By Polymer Type Segment

- 5.1.1. Wood Plastic Composite (WPC) Decking Market Revenue Share, By Polymer Type, 2025 & 2035

- 5.1.2. Polyethylene-Based WPC (HDPE, LDPE, Post-Consumer PE Film)

- 5.1.3. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Polypropylene-Based WPC (Virgin PP, Recycled PP)

- 5.1.7. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Polyvinyl Chloride-Based WPC (PVC-Wood Composite)

- 5.1.11. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Other Polymer Types (Mixed Polymer, Biopolymer Blends)

- 5.1.15. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Polymer Type Market Overview, By Polymer Type Segment

- Chapter 6. Wood Plastic Composite (WPC) Decking Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Wood Plastic Composite (WPC) Decking Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Residential Decking (Private Homes, Apartments, Balconies)

- 6.1.3. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Commercial Decking (Hotels, Restaurants, Office Buildings, Retail)

- 6.1.7. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Industrial & Infrastructure Decking (Marinas, Boardwalks, Parks, Transit)

- 6.1.11. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Other Applications (Rooftop Decking, Pool Surrounds, Garden Pathways)

- 6.1.15. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Wood Plastic Composite (WPC) Decking Market – By Distribution Channel

- 7.1. Distribution Channel Market Overview, By Distribution Channel Segment

- 7.1.1. Wood Plastic Composite (WPC) Decking Market Revenue Share, By Distribution Channel, 2025 & 2035

- 7.1.2. Retail Stores (Home Improvement Centers, Specialist Decking Retailers)

- 7.1.3. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Direct Sales (Contractor Direct, Builder Programs)

- 7.1.7. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Online Channels (E-Commerce, Manufacturer Direct-to-Consumer)

- 7.1.11. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Other Distribution Channels (Distributor Networks, Export Trade)

- 7.1.15. Wood Plastic Composite (WPC) Decking Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Distribution Channel Market Overview, By Distribution Channel Segment

- Chapter 8. Wood Plastic Composite (WPC) Decking Market – Regional Analysis

- 8.1. Wood Plastic Composite (WPC) Decking Market Overview, By Region Segment

- 8.1.1. Global Wood Plastic Composite (WPC) Decking Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Wood Plastic Composite (WPC) Decking Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Wood Plastic Composite (WPC) Decking Market Revenue, By Product Type, 2026 – 2035

- 8.1.4. Global Wood Plastic Composite (WPC) Decking Market Revenue, By Polymer Type, 2026 – 2035

- 8.1.5. Global Wood Plastic Composite (WPC) Decking Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Wood Plastic Composite (WPC) Decking Market Revenue, By Distribution Channel, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Wood Plastic Composite (WPC) Decking Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Wood Plastic Composite (WPC) Decking Market Revenue, By Product Type, 2026 – 2035

- 8.2.3. North America Wood Plastic Composite (WPC) Decking Market Revenue, By Polymer Type, 2026 – 2035

- 8.2.4. North America Wood Plastic Composite (WPC) Decking Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Wood Plastic Composite (WPC) Decking Market Revenue, By Distribution Channel, 2026 – 2035

- 8.2.6. U.S. Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Wood Plastic Composite (WPC) Decking Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Wood Plastic Composite (WPC) Decking Market Revenue, By Product Type, 2026 – 2035

- 8.3.3. Europe Wood Plastic Composite (WPC) Decking Market Revenue, By Polymer Type, 2026 – 2035

- 8.3.4. Europe Wood Plastic Composite (WPC) Decking Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Wood Plastic Composite (WPC) Decking Market Revenue, By Distribution Channel, 2026 – 2035

- 8.3.6. Germany Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Wood Plastic Composite (WPC) Decking Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Wood Plastic Composite (WPC) Decking Market Revenue, By Product Type, 2026 – 2035

- 8.4.3. Asia Pacific Wood Plastic Composite (WPC) Decking Market Revenue, By Polymer Type, 2026 – 2035

- 8.4.4. Asia Pacific Wood Plastic Composite (WPC) Decking Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Wood Plastic Composite (WPC) Decking Market Revenue, By Distribution Channel, 2026 – 2035

- 8.4.6. China Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Wood Plastic Composite (WPC) Decking Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Wood Plastic Composite (WPC) Decking Market Revenue, By Product Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Wood Plastic Composite (WPC) Decking Market Revenue, By Polymer Type, 2026 – 2035

- 8.5.4. The Middle-East and Africa Wood Plastic Composite (WPC) Decking Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Wood Plastic Composite (WPC) Decking Market Revenue, By Distribution Channel, 2026 – 2035

- 8.5.6. Saudi Arabia Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Wood Plastic Composite (WPC) Decking Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Wood Plastic Composite (WPC) Decking Market Revenue, By Product Type, 2026 – 2035

- 8.6.3. Latin America Wood Plastic Composite (WPC) Decking Market Revenue, By Polymer Type, 2026 – 2035

- 8.6.4. Latin America Wood Plastic Composite (WPC) Decking Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Wood Plastic Composite (WPC) Decking Market Revenue, By Distribution Channel, 2026 – 2035

- 8.6.6. Brazil Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Wood Plastic Composite (WPC) Decking Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Wood Plastic Composite (WPC) Decking Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Wood Plastic Composite (WPC) Decking Market: Company Market Share, 2025

- 9.2. Global Wood Plastic Composite (WPC) Decking Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Trex Company Inc.

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. AZEK Building Products Inc.

- 10.3. Fiberon LLC (Fortune Brands)

- 10.4. TimberTech (AZEK)

- 10.5. Deckorators (UFP Technologies)

- 10.6. Cali Bamboo

- 10.7. Boise Cascade

- 10.8. Zuri Premium Decking (Royal Building Products)

- 10.9. EverGrain Composite Decking (TAMKO)

- 10.10. Duralife Decking & Railing

- 10.11. Universal Forest Products

- 10.12. Others.

- 10.1. Trex Company Inc.

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 33

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Trex Company Inc.

- AZEK Building Products Inc.

- Fiberon LLC (Fortune Brands)

- TimberTech (AZEK)

- Deckorators (UFP Technologies)

- Cali Bamboo

- Boise Cascade

- Zuri Premium Decking (Royal Building Products)

- EverGrain Composite Decking (TAMKO)

- Duralife Decking & Railing

- Universal Forest Products

- Others

FAQs

The key players in the market are Trex Company Inc., AZEK Building Products Inc., Fiberon LLC (Fortune Brands), TimberTech (AZEK), Deckorators (UFP Technologies), Cali Bamboo, Boise Cascade, Zuri Premium Decking (Royal Building Products), EverGrain Composite Decking (TAMKO), Duralife Decking & Railing, Universal Forest Products, Others.

The WPC decking market is affected by government regulations in the following ways: Timber trade regulations that impact the competitive natural wood products market; Building code regulations that set structural performance requirements for decking products, Green building certification frameworks that encourage specification of sustainable material inputs; and, Regulations that limit chemical content in construction products. Whereas WPC products with recycled wood fiber or FSC certified wood fiber are inherently deforestation-free, the EU Deforestation Regulation places compliance obligations on any timber and timber derived products placed on the EU market, which impacts the demand for WPC products in the most significant way, especially for tropical hardwood decking products. The U.S. Lacey Act, which bans imports, exports, transport, and acquisition of illegally harvested timber, imposes competing compliance regulations on tropical hardwoods in the U.S. market that also compromise (and would compromise further) imported timber products compared to domestically manufactured WPC products. The technical performance documentation requirements of building code are the requirements that WPC manufacturers invest in testing and certification programs to meet; these requirements are established by prescriptive structural requirements in the International Residential Code (IRC) for decking spans, specifications for fasteners, and requirements for guardrail attachments, and these requirements are documented in an ICC Evaluation Report that is accepted by the building official and enables WPC decking to be specified in code-compliant residential and commercial deck construction. The added motivation to specify WPC in commercial projects where certification point achievement affects architects and developers’ material selection comes from LEED v4.1 and BREEAM materials credits, which include recycled content certification and responsible sourcing verification that the recycled content levels and EPD documentation that leading manufacturers have developed for WPCs are increasingly available.

The price of WPC decking can differ widely based on the type of product, cap technology, and geographic market it is sold in. Rental, value composite, or basic-capped WPC products — such as products from the domestic manufacturers that target price-conscious homeowners — are priced into the lowest level of WPC, USD 2.50–USD 4.50 per linear foot of board, and compete most closely with pressure treated lumber in terms of cost on the installed surface. Mid-range capped composite decking — which encompasses the mainstream product tier of established brands with full warranty coverage on four sides and a 25-year fade and stain guarantee — costs USD 4.50–USD 8.00 per linear foot and targets the broad new construction and renovation market where warranty coverage, quality and brand recognition build consumer confidence in purchase. Premium capped composite decking, which includes the highest specification products with deep wood grain embossing, multi-tone color variegating, and enhanced cap formulations for superior scratch protection, is sold at USD 8.00–USD 15.00 per linear foot and is directed to the feature residential deck and commercial specification market where the highest possible aesthetic authenticity and capability of the material are to be expected. The first price objection that the WPC salesperson has to overcome is the price of the pressure-treated lumber ($0.80-$2.00 per linear foot). Commercial and public infrastructure WPC decking is priced at USD 10.00–USD 25.00 per linear foot, reflecting the extra investment in specification, testing and documentation of the product that is necessary for commercial and public use.

The market will grow to approximately USD 15.84 billion by 2035 at a CAGR of 7.8% from 2026 to 2035, based on current analysis, as the market will be driven by the continued residential renovation conversion from pressure-treated wood to composite decking, the extraordinary growth in the market in Asia Pacific as the region’s market is growing in tandem with the Chinese market’s own growth, faster adoption in Europe as the EU tropical timber import regulations and sustainability requirements for the green building certification programme drive the growth, the market is expanding beyond only specifiers in the contractor market by increasing the market’s total addressable market through online channels, which allow decks to be sold directly to consumers, the increased specification of WPC decking as its whole-life cost benefits over concrete and other timber options becomes better documented through specifier literature, and its progressive penetration in the LAMEA region, as the market in the Gulf region is scaling with its massive consumer base and outdoor decking specification at green building projects is going to be motivated by the market’s sustainability credentials and the superior performance and aesthetic quality of WPC that justifies its selection for best value.

Based on the United States being the most commercially advanced WPC decking market with the most developed market awareness with consumers, the most advanced retail distribution infrastructure, the highest per-capita residential deck investment, the largest established composite decking installed base, and the concentration of the world’s leading WPC decking manufacturers that have invested in innovation that has sustained North America’s product quality leadership, the structural advantage of decades of consumer market development has established composite as the expected premium specification for residential deck projects across the most commercially active U.S. residential renovation market, which will result in North America maintaining the highest revenue share throughout the forecast period.

The WPC decking market in Asia Pacific is expected to witness the highest CAGR of 10.8% during the forecast period, as the market is experiencing simultaneous growth in several key sectors including the middle class residential outdoor space investment, commercial hospitality specification market and public infrastructure decking market; Australia’s large outdoor living culture creating established demand for WPC in the country; the progressive improvement of the quality of Asian WPC manufacture and the resulting growth of the domestic market; and the export of competitive products, driven by cost advantage, from Asia Pacific, expanding market growth across the global market where premium North American brands compete technologically and branded, versus on cost.

WPC’s market share of decking, the EU Deforestation Regulation due diligence requirements, is creating compliance risk for tropical hardwood decking imports that WPC completely avoids through its domestic material supply chain. Trex Company’s 95% recycled content achievement from 1.5 billion pounds of annual polyethylene film establishes the circular economy credential benchmark that consumers in the decking specification market compare when evaluating decking specification options, Fiberon’s biopolymer cap layer is achieving a 32% embodied carbon reduction and is qualified for LEED v4.1 Material Ingredients credits in projects that are being specified for their sustainability, and the AR deck visualization tool deployment is creating a 40-60% conversion rate improvement over sample-based selection, giving a financial justification for premium WPC material specification for residential projects of meaningful size, as people around the world become more educated on the benefits of a circular economy and are increasingly buying products based on sustainability credentials.