Multi-layer Film Recycling Market Size, Trends and Insights By Technology (Mechanical Recycling, Sorting and Washing, Extrusion and Pelletizing, Compatibilization, Chemical Recycling, Pyrolysis, Gasification, Depolymerization, Solvent-Based Recycling, Other Technologies), By Film Type (Polyethylene-based Films, Polypropylene-based Films, Polyamide-based Films, EVOH-based Films, Other Film Types), By Application (Food Packaging, Pharmaceutical Packaging, Industrial Packaging, Agriculture Films, Other Applications), By End-Use Industry (Food & Beverage, Healthcare, Retail, Agriculture, Other Industries), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 9.2%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- SUEZ SA

- Poly-America L.P.

- Republic Services Inc.

- Waste Management Inc.

- Others

Reports Description

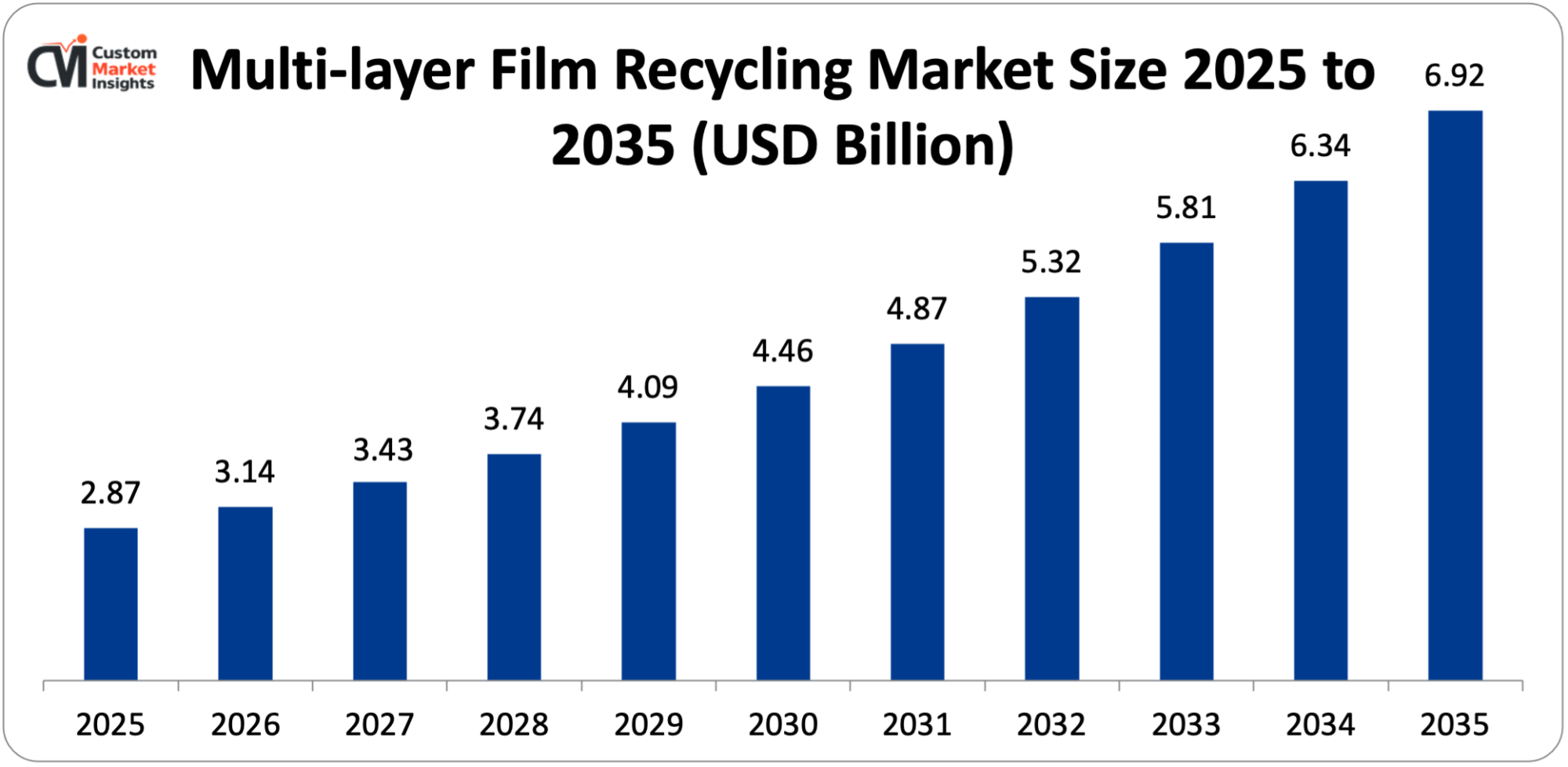

The size of the global multi-layer film recycling market is estimated at USD 2.87 billion in 2025 and is projected to grow to between USD 3.14 billion in 2026 and approximately USD 6.92 billion by 2035 with a CAGR of 9.2% between 2026 and 2035.

The strengthening of environmental policies and circular economy requirements, the growing consumer concern about plastic waste, the increasing use of sophisticated recycling technologies facilitating the extraction of materials that make up complex packaging systems, the rising investment in chemical recycling complexes and the need to allocate sustainability through corporate-related sustainability policies contribute to market growth.

Market Highlight

- The multi-layer film recycling market was dominated by Europe, which held a 42% market share in 2025.

- Asia Pacific will increase at the quickest CAGR of 11.3% between the period 2026 and 2035.

- Technology: The mechanical recycling segment is projected to have taken approximately 48% of the market share by 2025.

- With technology, the chemical recycling segment is expanding at the highest CAGR of 14.6% between 2026 and 2035.

- By application, the food packaging segment will have the highest market share of 56% in 2025, and the pharmaceutical packaging segment will grow with the highest CAGR of 10.8% during the expected period of between 2026 and 2035.

- By type of film, the polyethylene-based film market gained 52% of the market share in 2025.

- Multi-layer films constitute about 35% of the total flexible packaging production worldwide with the current level of recycling of 14%; however, it is expected to increase to 35% by 2030.

Significant Growth Factors

The Multi-layer Film Recycling Market Trends present significant growth opportunities due to several factors:

- Stringent Environmental Regulations and Extended Producer Responsibility (EPR) Schemes:

The growing introduction of extensive environmental laws to the global market is the major trigger of the extensive growth of the multi-layered film recycling market where governments have established mandatory recycling quotas, taxes on plastic and extended producer responsibility schemes, which are compelling the manufacturers of packaging and brand owners to make their products recyclable and add recycled content.

The Packaging and Packaging Waste Regulation (PPWR) of the European Union stipulates that all packaging should be recyclable by 2030 with plastic packaging containing a minimum percentage of recycled content stipulated at 30% of PET bottle packaging by 2030 and 65% of all contact sensitive plastic packaging by 2040. The European commission estimates the amount of plastic waste generated in the EU to be 26 million tons per annum, only 30% of which is collected to be recycled, which is a phenomenal unexploited potential in terms of growth of multi-layer film recycling infrastructure. In January 2019, France introduced the world’s first plastic tax of EUR 0.50 per kilogram of non-recycled plastic packaging, followed by a plastic packaging tax of GBP 200 per ton on packaging with less than 30% of recycled content introduced in the UK in April 2022, which provides strong economic incentives to adopt recycling. Throughout the period 2021 to 2025, 35 states in the US have introduced EPR laws for packaging, including several comprehensive EPR laws in California, Oregon, Colorado, and Maine, requiring manufacturers to fund collection and recycling facilities, which are expected to drive USD 5bn of investment throughout the country.

Single use plastic bans have been enacted in more than 75 countries around the world, including shopping bags, food service packaging, and agricultural films, but currently India has banned single use plastic items and this ban has extended to multi-layer sachets and films used widely in packaging of the FMCG sector. It is reported that about 400 million tons of plastic waste are produced every year all over the world, with the packaging representing 36% of the total amount of 400 million, and the flexible packaging such as multi-layer films occupies about 140 million tons per year. Recycling rate of multi-layer films is still very low relative to other packaging styles because of the technical difficulty of separating the various polymer layers, glues and barrier materials, with an average of 1214% worldwide compared to 29% for rigid plastic packages and 41% for PET bottles. This regulatory pressure and low recycling levels of multi-layer film waste result in a large market potential for technologies that can operate effectively in processing multi-layer film waste, and it is estimated that the advanced recycling facilities will generate over USD 15 billion of investment in recycling facilities around the world by 2025-2030.

- Corporate Sustainability Commitments and Circular Economy Initiatives:

The expansion of the market has increased significantly in response to the large consumer goods firms, retailers and packaging producers making bold sustainability commitments requiring the use of recycled material in packaging and meeting certain recyclability targets, which stimulate the demand for recycled multi-layer film materials and investment in recycling facilities.

The New Plastics Economy Global Commitment by the Ellen MacArthur Foundation, which has been signed by over 500 entities representing a fifth of all plastic packaging in the world, has targets to remove problematic or unnecessary plastic packaging, innovate to have 100% of all plastic packaging easily and safely reused, recycled, or composted by 2025, and have 25% of all plastic packaging with recycled content used by 2025. Large companies such as Unilever vowed to cut the use of virgin plastic by 50% by the year 2025 and have 100% of plastic packaging recyclable or reusable by the year 2025.

Nestlé pledged that by 2025 it would have 100% of packaging recycled or reused and cut virgin plastic use by a third, PepsiCo stated that it will achieve 50% recycled content in plastic packaging by 2030 and Procter and Gamble decided Industry analysis shows in 2024 that the top 100 world consumer goods firms produce more than 30 million tons of plastic packaging each year, of which about 40% are flexible packaging types such as multi-layered films utilized in both food and beverage and personal care and household product packaging. Such corporate commitments generate a high volume of demand through recycled multi-layer film content and according to the market research, demand for food-grade recycled polyethylene and polypropylene of multi-layer film sources will increase to 8-12 million tons per year by 2030, which is 600 times higher than at present. An example of a brand owner investing in recycling infrastructure is the case of Danone investing to support chemical recycling through a EUR 30 million deal with several chemical recycling technology partners, or the case of Mondelēz International colluding with various recycling technology experts to develop solutions to flexible snack packaging, or the involvement of Henkel in consortium projects that support the development of multi-layered film recycling in Europe.

The Circular Economy of Flexible Packaging (CEFLEX) consortium is a group of more than 180 European companies, associations, and organisations within the flexible packaging value chain, which is working on the design principles, collection systems and recycling solutions with the efforts yielding recyclability-assessment tools used to evaluate over 5,000 flexible packaging formats. Retailers are also introducing policies that necessitate suppliers to achieve packaging sustainability requirements, with Walmart in its project Gigaton involving more than 4,500 suppliers to aid in reducing greenhouse gas emissions by means of sustainable packaging, Target intending to have in place 100% recyclable, compostable or reusable owned-brand packaging by 2025 and Tesco having removed hard to recycle materials in own-brand packaging that affects over 2,000 product lines.

What are the Major Advances Changing the Multi-layer Film Recycling Market Today?

- Chemical Recycling Technologies Breaking Down Polymer Barriers:

The most radical innovation in multi-layer film recycling is the development and subsequent large-scale commercialization of advanced chemical recycling technologies, also known as advanced recycling or molecular recycling, allowing disaggregation of complex polymer structures into their molecular building blocks by means of pyrolysis, gasification, solvolysis, and depolymerization, overcoming inherent limitations of mechanical recycling which finds it difficult to handle contaminated and mixed-material waste streams and multi-layers of film.

Multi-layer films that multi-layer technology cannot process using conventional mechanical techniques are processed using chemical recycling methods, producing pyrolysis oil, syngas, or monomers that can be recycled into new virgin-quality polymers, which can be used in food-contact applications. In the United States, the 2024 capacity in chemical recycling reached about 350,000 tons per year according to the American Chemistry Council and planned projects are projected to reach over 3 million tons per year by 2027, a factor of close to 10 times the current capacity, which is due mainly to the multi-layer and mixed plastic waste processing capacity. Large petrochemicals are developing massive chemical recycling plants, among which ExxonMobil has planned to recycle 500,000 metric tons of plastic waste each year by 2026 with its Exxtend technology consisting of combining advanced recycling and certified circular polymers, SABIC has commercial-scale chemical recycling facilities in the Netherlands that generate certified circular polymers using mixed plastic waste, and LyondellBasel is advancing its MoReTec molecular recycling technology by building a 50,000-ton demonstration plant in Germany.

The most commercially developed chemical recycling technology of films is pyrolysis, which converts plastic waste into smaller hydrocarbon molecules such as oils, which can be further refined to produce naphtha feedstock that goes into ethylene and propylene monomers in steam crackers at temperatures of 300-900°C in the absence of oxygen, under oxy-free conditions. Technology suppliers of films such as Plastic Energy, Brightmark, and Agilyx have commercial facilities that process multi-layer film wastes. With the development of technology, pyrolysis has become a much more efficient process, and the yield of the liquid oil on the multi-layer polyolefin films has increased to 70-85% (as opposed to 50-60% on the previous generation technologies).

The heat recovery and the process optimization have also helped to cut the energy usage by 30-40%. Recycling technologies Solvent-based technologies Solvent-based recycling technologies reuse selective solvents to dissolve particular polymers contained within a multi-layer structure and can extract and recycle individual polymer types and remove impurities such as inks, adhesives, and barrier layers, with examples such as the APK AG Newcycling process to recover high-purity polyolefins in multi-layer films and the purification process by PureCycle Technologies to produce ultra-pure recycled polypropylene out of heavily contaminated feedstock. The mass balance certification models allow recycling producers of chemicals to commercialize certified circular polymers to which recycled content allocation has been made even in instances where recycled feedstock has been mixed with virgin materials during processing, and certification schemes such as ISCC PLUS and RSB allow tracking of the chain of custody and allow the brand owner to claim recycled content use on packaging.

- Advanced Sorting and Separation Technologies Enabling Material Recovery:

The economics and the quality of materials in multi-layer film recycling are being radically transformed by the technological development of automated sorting, separation, and decontamination systems that allow the effective identification, segregation, and cleaning of a vast array of film materials that would otherwise have been discarded at a landfill or burnt. This has been achieved through the use of near-infrared (NIR) spectroscopy with artificial intelligence and machine learning algorithms, which means that optical sorting systems can sort and identify various polymer types and colors and even distinguish between multi-layered structures at processing rates over 3-4 tons per hour with an accuracy rate of more than 95% compared to the 70-80% accuracy of previous sorting solutions. State-of-the-art sorting systems combine several technologies used to detect different materials, such as visible cameras to sort by color, NIR to detect polymer, laser-induced breakdown spectroscopy (LIBS) to process elemental data, X-ray fluorescence (XRF) to identify heavy metals and contaminants, and hyperspectral imaging systems to process broader wavelength repositories to better characterize materials.

According to a report by TOMRA Sorting Recycling, one of the world leaders in sensor-based sorting technology, its AUTOSORT systems, which use the flying beam technology and SHARP EYE sensor technology, produce polymer purity of output fractions at over 98% and target material recovery at over 90% of the mixed plastic waste streams including multi-layered films. Modern material recovery facilities (MRFs) capable of sorting 8-12 distinct plastic film fractions in mixed waste streams with sophisticated optical sorting equipment can now sort these fractions economically, which is 2-3 fractions of mixed waste streams with manual or rudimentary sorting equipment, allowing higher-value recycled materials to be produced that can be used in more demanding applications. Washing and decontamination technologies have improved, and the present day multistage washing systems that combine dry cleaning, wet washing with special surrogates and detergents, friction washing, and density separation can remove printing inks, adhesives, product residues, and odors of post-consumer multi-layer films to manufacture recycled materials that meet the food safety standards. The compatibility technologies are becoming vital facilitators of mechanical recycling of multi-layered films based on the application of reactive additives or compatibilizing agents that enhance adhesion and compatibility between the various types of polymers in the recycled blends that allow the production of mechanically recycled material sources based on multi-layered sources without complete delamination and separation.

Category Wise Insights

By Technology

Why Mechanical Recycling Leads the Market?

The biggest part in 2025 will be mechanical recycling, with about 48% of total market share. This pre-eminence indicates the fixed infrastructure of mechanical recycling, less capital needed than the capital requirements of chemical recycling, a good track record of processing polyethylene and polypropylene films and pre-existing compatibility with current waste collection. The Association of Plastic Recyclers jointly reports that in the US, the total yearly plastic films recycled in North America have a significant capacity of more than 2 million tons at mechanical recycling plants and the European recycling facility has a capacity of 2.8 million tons each year. Mechanical recycling involves the majestic amassing, sorting, washing, and reprocessing of the multi-layer films by shredding, melting and extrusion into recycled plastic pellets which may be used in the making of new packaging or other plastic articles, and which attains material recovery at a lower cost and consumes less energy than the other technologies.

The popularity of the mechanical recycling segment is due to several major strengths such as well-developed recycling processing technology and decades of operation experience, a cheaper capital cost of USD 2-8 million in comparison with USD 50-150 million in a chemical recycling plant, a higher processing rate of up to 3-5 tons per hour and recycled pellets that are directly convertible for manufacturing purposes. Also, the International Solid Waste Association emphasizes that mechanical recycling consumes 40-60% less energy than chemical recycling, which lowers the costs of operation and carbon footprint, which supports their significance in the market. Newer mechanical recycling also employs technological improvements such as optical sorting with AI reaching purity of 95%+, advanced washing systems that remove 99% of contaminants and compatibilization additives that allow processing of mixed polymer streams.

Chemical recycling is growing at the quickest rate with a forecasted CAGR of 14.6% in the period 2026-2035 owing to the capability to recycle highly contaminated and multi-layered films that cannot be recycled by mechanical recycling. Chemical Recycling reduces polymer to the molecule level resulting in virgin quality output that can be used for food-contact purposes. Chemical recycling of plastics can be projected to expand between USD 385 million in 2025 and USD 1.2 billion in 2030 indicating enormous industry uptake. Pyrolysis at 400-800 o C to convert the films into oils, gasification at 700-1500 o C to produce a syngas, and solvolysis using solvents are all types of recycling processes to selectively dissolve and separate the types of polymer in producing recycled materials that have the same properties as virgin plastics.

By Application

Why Food Packaging Dominates Multi-layer Film Recycling Applications?

The biggest segment is the food packaging applications which contribute about 56% of total markets in 2025. This management is representative of the vast amounts of multi-layer films that are utilized in food packaging all over the world with barrier properties being necessary to ensure that the contents have a long shelf life and food safety. Multi-layer constructions such as polyethylene, polypropylene, polyamide and EVOH allow packaging of a variety of different products such as fresh meat, cheese, snacks, and coffee as well as ready meals, with global food packaging estimated at about 78 million tons of plastic per year, comprising about 45-50 million tons of multi-layer flexible films. The dominance of the food packaging segment is informed by the brand owner’s sustainability promises of adding recycled content, consumer preference for sustainable packaging, regulatory pressure necessitating recyclability, and the sheer scale of the food industry creating stable waste streams that could be recycled to develop recycling infrastructures.

Recycling of food packaging is a special concern due to such factors as strict food safety standards that require food to be processed through decontamination, product residue contamination that necessitates high-quality washing and regulation that restricts the content of recycled material in direct contact with food which has induced innovation of super-clean recycling procedures. Recycling of food packaging today uses multi-stage washing for 99.9% contaminant removal and chemical recycling to virgin-equivalent material to pass through food contact and mass balance certification allowing them to claim recycled content. In 2023, the food packaging industry worldwide was estimated to be USD 359.6 billion, which is expected to increase to USD 426.7 billion in 2025, with a 6.2% CAGR, and through the use of sustainable packaging, the industry is expected to have a sustained demand requiring the capabilities of recycling to support the food packaging sector.

The pharmaceutical packaging is recording the greatest growth with the foreseen CAGR of 10.8% between 2026 and 2035 due to rising pharmaceutical production, rising packaging volumes as a result of the trend in personalized medicine and unit dose packaging and sustainability in the pharmaceutical industry. Pharmaceutical applications Multi-layer films Multi-layer films used in pharmaceuticals include blister packs, sachet packaging, pouches, and protective films that must have stringent barrier properties, and pharmaceutical packaging produces about 12 million tons a year worldwide. Recycling pharmaceutical packaging with modern recycling strategies focuses on special purposes of high-purity demands, controlled substance regulations and serialization which will assist the industry in the transition to circular packaging systems.

By Film Type

Why Polyethylene-based Films Dominate the Market?

Polyethylene-related films form the biggest market share comprising about half of the market in 2025. Such hegemony is seen in the dominance of polyethylene as the most used polymer in flexible packaging because of its good processing properties, great heat sealing, ability to create moisture barriers, and affordability. In the world, polyethylene films are manufactured at a rate of over 45 million tons each year with LDPE, LLDPE and HDPE grades finding much use in multi-layer constructions in food packaging, industry, and agricultural films. Polyethylene materials are easily recycled by mechanical methods, the collection and processing facilities are well in place, and hence they offer an appealing target to recycling activities. The segment has the advantage of having a large quantity of waste with assured availability of feedstock, available technologies to recycle waste over time with high proportionality, and the market demand of recycled polyethylene in garbage bags, construction film, and non-food packaging.

Modern recycling of polyethylene can recover the material at a 75-85% rate of recovery, and recycled pellets with properties close to those of virgin material can be obtained through automated sorting, efficient washing to get high rates of recovery, and optimized extrusion. Large consumer goods companies are moving towards a significant increase in the use of recycled polyethylene, with a goal of 25-50% of the content of the packaging being recycled by 2025-2030, generating strong demand to sustain the growth of the market. In 2024, the prices of recycled LDPE were USD 800-1,100 per ton on average as compared to virgin material at USD 1,200-1,400, which is an economic incentive to adopt recycling, and the growth in demand of recycled content continues to push the price upward, enhancing the economics of recycling.

The growth in polypropylene-based films is high owing to the growing use of polypropylene in flexible packaging such as snack foods, labels, and industrial packaging, where recycling is problematic due to degradation in the reprocessing of the material necessitating virgin material mixing or chemical recycling methods to maintain quality. Polypropylene recovery processes are developing using technologies of chemical recycling, and solvent-based methods are able to separate by high purity by using multi-layer structures, which promotes the development of markets.

The growth in polypropylene-based films is high owing to the growing use of polypropylene in flexible packaging such as snack foods, labels, and industrial packaging, where recycling is problematic due to degradation in the reprocessing of the material necessitating virgin material mixing or chemical recycling methods to maintain quality. Polypropylene recovery processes are developing using technologies of chemical recycling, and solvent-based methods are able to separate by high purity by using multi-layer structures, which promotes the development of markets.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 3.14 billion |

| Projected Market Size in 2035 | USD 6.92 billion |

| Market Size in 2025 | USD 2.87 billion |

| CAGR Growth Rate | 9.2% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Technology, Film Type, Application, End-Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

Which Region Dominates the Multi-layer Film Recycling Market?

The current situation in the multi-layer film recycling market is that it is dominated by Europe, which will have more than 42% of the global market share in 2025 through the strictest environmental rules and regulations making it compulsory to use recycled and recyclable content, the waste collection infrastructure with high rates of capture of flexible packaging, heavy investment in high-tech recycling facilities, progressive policies on the circular economy and high demand for sustainable packaging solutions to provide good market conditions for the growth of the recycling industry.

Europe Market Analysis

European dominance in multi-layer film recycling is an effect of extensive regulatory frameworks such as the EU Packaging and Packaging Waste Directive obliging member states to attain minimum recycling rates, with targets set at 65% recycling of all packaging waste by 2025 and 70% by 2030, plastic specific targets of 50% recycling of all packaging waste by 2025 and 55% by 2030 and proposed revisions of 100% recycled content requirements. Germany has the best recycling system with the Dual System (Der Grue Punkt), which collects more than 1.7 million tons of lightweight packaging every year of flexible films, with a recovery rate of plastic packaging of more than 63% obtained by an extensive collection network, state-of-the-art sorting plants and compulsory producer responsibility charges as an incentive to design items that are recyclable.

Investment in European chemical recycling is unprecedented with more than EUR 7 billion invested in high-technology recycling projects in 202025, including a 33,000-ton chemical recycling plant in Seville, Spain converting mixed plastic waste to TACOIL feedstock, a 16,000-ton pyrolysis facility in Skive, Denmark reworking end-of-life plastic to synthetic oil and wax; and several more planned facilities by Neste, Borealis and other petrochemical manufacturers incorporating recycled In 2020, France enacted the landmark anti-waste law (Loi AGEC), requiring 20% plastic packaging recycled content by 2025, 30% by 2030, specific measures on single-use plastics reduction, and producer responsibility schemes that require payment by recycling by packaging companies of 80% of the cost of collection and recycling, which, with the income this generates, has seen an estimated investment in recycling infrastructure of EUR 500 million/year.

The United Kingdom has set the Resources and Waste Strategy, which aims to reduce the amount of unwanted plastic waste by 2042, introduce deposit return schemes on beverage containers, and ensure uniformity in the collection of both business and household recycling as well as plastic packaging tax, which provides an economic incentive for the use of recycled content which may cover over 1.2 million tons of plastic packaging in the UK each year. Film producers and converters in Europe are putting significant effort into enhancing their recyclability, and associations such as CEFLEX, Flexible Packaging Europe, and European Bioplastics are working on design-for-recyclability guidelines that have been applied to over 15,000 packaging designs to enhance their suitability to existing and future recycling systems. According to the statistics provided by Plastics Europe, the volume of the European plastic film production amounts to 8.4 million tons in 2023, with post-consumer film collection rates rising from 18% in 2015 to 32% in 2024, which is a positive result but still requires work to achieve the targets of the green economy.

Which Region Holds the Fastest Growth Potential?

On the one hand, the Asia Pacific region is expected to have the greatest growth rate of 11.3% between 2026 and 2035 due to the high rate of urbanization and growing middle class increasing packaged goods consumption, mounting environmental consciousness and policy measures to address the plastic waste crisis, intensive foreign investments in recycling systems, developing export markets of recycled material and government activities promoting the creation of the circular economy, which creates favorable circumstances for packaged goods to expand the market.

Asia Pacific Market Dynamics

The rapidly expanding market growth of Asia Pacific is due to the fact that the region is the largest plastic consumer and producer in the world whereby China, India, Southeast Asian countries and Japan together contribute more than half of the world’s plastic production and consumption generating huge volumes of multi-layered film waste that needs to be processed. The domestic recycling industry growth was triggered by the introduction of domestic policy on plastic waste recycling in China in 2018, the National Sword policy, followed by the Green Fence and Blue Sky plans, which led to the establishment of more than USD 12 billion worth of modern sorting, washing, and recycling facilities within 2018-2024, significantly increasing domestic recycling capacity.

The Ministry of Ecology and Environment in China reported that in 2023 the country produced 63 million tons of plastic waste, with multilayer flexible packaging making up to 28% of that volume, and recycling of plastic film rates increased to 22% in 2024 after investing in infrastructure and implementing the policy. In 2016, India adopted Plastic Waste Management Rules, which were amended in 2021, and that is that single-use plastics should be phased out and that plastic packaging producers should have extended producer responsibility, which stipulates that plastic packaging waste must be collected and recycled in the same quantity produced by their products.

The Japanese packaging has shown the best practices in sustainability with a voluntary agreement between the industry and the government to achieve 85% effective use of plastic containers and packaging by the year 2030, an increase over the 86% in 2020, with major companies such as Mitsubishi Chemical and Mitsui Chemicals investing in multi-layer film waste chemical recycling technologies to convert the waste into a feedstock material to produce another polymer. Some countries in Southeast Asia such as Thailand, Vietnam, the Philippines, Indonesia, and Malaysia are adopting policies aimed at managing plastic waste and are inviting foreign investors to invest in recycling infrastructure with Thailand aiming to achieve 100% recycling or reuse of plastic waste by 2027, banning single-use plastics in tourist destinations in Vietnam and Indonesia promising to eliminate marine plastic waste by 70% by 2025 through the adoption of better waste management systems such as increased recycling. In the same report, Asia Pacific Recycling Industry records show that by 2024, the regional investment in mechanical and chemical recycling plants was USD 4.2 billion, and it is projected to reach USD 8 billion and above in 2028 because governments, corporations, and development organizations currently plan to emphasize the infrastructure of the circular economy as a way of managing the plastic pollution crisis in coastal areas and oceans.

North America Market Overview

North America is estimated to have about 26% of the total multi-layered film recycling market share with the regulatory pressure at the state and municipal level pushing towards EPR implementation, corporate investment in recycling technology and infrastructure being high, the packaging industry shifting to recyclable designs, a new chemical recycling industry drawing billion-dollar investment, and consumers putting pressure on the brands leading to sustainability creating market growth dynamics. As a result of the data provided by the EPA, the United States produces in a year about 42 million tons of plastic waste, of which 45% is packaging, and the multi-layer films of flexible packaging constitute around 19 million tons, leaving the existing rates of plastic film recycling at about 13%, which means that there is a lot of room to expand the infrastructure.

EPR laws on the state level are revolutionizing the U.S. recycling landscape, as SB 54 in California mandates 65% recycling of single-use plastic packaging by 2032 and a 25% decrease in plastic packaging waste, HB 22-1355 in Colorado introduces a producer responsibility program for recycling packaging, Maine’s LD 1541 becomes the first state law to create an EPR system in the country to recycle packaging, and SB 582 in Oregon requires comprehensive producer financing of recycling systems. all of Investment in chemical recycling in North America has now gone on a rocket ship, with projects announced like Eastman Chemical with its USD 1 billion molecular recycling plant in Texas that processes 250,000 tons of plastic waste per annum, Braskem and Valero with their renewable chemicals plant in Texas, Nexus Circular with its USD 500 million advanced recycling complex in Pennsylvania, and smaller-scale projects announced by Brightmark, Agilyx, Encina, and others who operate in technology provision.

Canada introduced federal and provincial policies that aim to eliminate plastic waste, the Federal Plastics Registry that requires brand owners and producers to report the data on packaging, the comprehensive EPR program in British Columbia that regulates the packaging and paper products, and the producer responsibility framework in Ontario that forms the basis of the development of collection and recycling facilities. North American flexible packaging manufacturing according to the industry statistics of the Flexible Packaging Association shows that production was at 7.8 million tons in 2024, and recycled content use is at 18% CAGR due to promises by brand owners, regulatory demands, and the rising availability of recycled materials through advanced recycling plants.

What is Driving Growth in the LAMEA Region?

The LAMEA region is where the market is developing at a rapid rate due to the growing urbanization which raises the consumption of packaged goods; international development aid sources supporting the waste management infrastructure; the rising awareness of plastic contamination issues impacting tourism and ecosystems; multinationals practicing global sustainability policies in the region; and government efforts in waste management issues to improve the collection and recycling of waste, which are building the base for the growth of the market.

Middle East & Africa Regional Dynamics

The countries of the Middle East also combat plastic waste by policy measures such as the national policy of the UAE to reduce by 75% the municipal solid waste in landfills by 2021, the Saudi Vision 2030 sustainability objectives of recycling of waste, and the Qatari National Vision 2030 with its focus on environmental sustainability. The African countries are experiencing significant problems with domination of the informal waste sector but are establishing formal recycling systems with international financial support, and South Africa has the most developed recycling industries, with about 350,000 tons of plastic packaging recycled each year under industry-funded schemes such as PETCO and Polyco. The Latin American markets demonstrate an increase in regulatory activity, as Brazil has a policy on Solid Waste Nationwide that creates a shared responsibility to achieve waste management, Chile has a ban on single-use plastic bags in the country, Mexico City has a plastics policy that restricts plastics use, and Argentina has been developing an extended producer responsibility system, which stimulates the gradual development of recycling infrastructure.

Latin America Market Development

The international recycling market of multi-layer film is growing with the rising level of environmental regulation, the introduction of a circular economy as part of regional governments, the development of modern retail that creates uniform packaging waste flows, and the international brands introducing global commitments on packaging sustainability in regional marketing. As per the industry data of the region, Latin America produces about 17 million tons of plastic waste per year, with recycling rates ranging widely between 5% in Central American countries and higher than 20% in other countries such as Chile, Uruguay, and Costa Rica that have well-developed systems. Recycling infrastructure is relatively small in comparison to other regions but growing faster, and in 2023-25, pilot projects in chemical recycling in Brazil, Mexico, and Colombia were drawing venture capital and corporate investment larger than USD 200 million.

Top Players in the Market and Their Offerings

- Veolia Environnement S.A.

- SUEZ SA

- Poly-America L.P.

- Republic Services Inc.

- Waste Management Inc.

- Aduro Clean Technologies Inc.

- APR2 Plast

- Plastic Energy Ltd.

- Brightmark LLC

- Agilyx Corporation

- PureCycle Technologies Inc.

- Others

Key Developments

The market has been experiencing tremendous developments, with the players in the industry trying to increase possibilities and technological solutions.

- In February 2025: Veolia stated that it had opened an advanced multi-layer film recycling plant in France with a capacity of 25,000 tons per year using proprietary mechanical separation to make food grade recycled polyethylene from post-consumer flexible packaging. (Source: Veolia)

- In January 2025: PureCycle Technologies reported successful processing trials for multi-layer polypropylene films through its solvent-based purification technology, demonstrating the ability to remove barrier layers, adhesives, and contaminants to produce ultra-pure recycled polypropylene meeting virgin material specifications for food packaging applications. (Source: PureCycle)

Such strategic initiatives have enabled the firms to consolidate market shares, develop processing capacities, improve technological applications to complex multi-layered packages and tap expanding demands of recycled materials by brand owners and packaging producers.

The Multi-layer Film Recycling Market is segmented as follows:

By Technology

- Mechanical Recycling

- Sorting and Washing

- Extrusion and Pelletizing

- Compatibilization

- Chemical Recycling

- Pyrolysis

- Gasification

- Depolymerization

- Solvent-Based Recycling

- Other Technologies

By Film Type

- Polyethylene-based Films

- Polypropylene-based Films

- Polyamide-based Films

- EVOH-based Films

- Other Film Types

By Application

- Food Packaging

- Pharmaceutical Packaging

- Industrial Packaging

- Agriculture Films

- Other Applications

By End-Use Industry

- Food & Beverage

- Healthcare

- Retail

- Agriculture

- Other Industries

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Multi-layer Film Recycling by Segments

- 2.1.2. Multi-layer Film Recycling by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Multi-layer Film Recycling Market Attractiveness Analysis, By Technology

- 2.2.3. Multi-layer Film Recycling Market Attractiveness Analysis, By Film Type

- 2.2.4. Multi-layer Film Recycling Market Attractiveness Analysis, By Application

- 2.2.5. Multi-layer Film Recycling Market Attractiveness Analysis, By End-Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Stringent Environmental Regulations and Extended Producer Responsibility (EPR) Schemes

- 3.1.2. Corporate Sustainability Commitments and Circular Economy Initiatives

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter’s Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Multi-layer Film Recycling Market – By Technology

- 4.1. Technology Market Overview, By Technology Segment

- 4.1.1. Multi-layer Film Recycling Market Revenue Share, By Technology, 2025 & 2035

- 4.1.2. Mechanical Recycling

- 4.1.2.1. Sorting and Washing

- 4.1.2.2. Extrusion and Pelletizing

- 4.1.2.3. Compatibilization

- 4.1.3. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Chemical Recycling

- 4.1.6.1. Pyrolysis

- 4.1.6.2. Gasification

- 4.1.6.3. Depolymerization

- 4.1.7. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Solvent-Based Recycling

- 4.1.11. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Other Technologies

- 4.1.15. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Technology Market Overview, By Technology Segment

- Chapter 5. Multi-layer Film Recycling Market – By Film Type

- 5.1. Film Type Market Overview, By Film Type Segment

- 5.1.1. Multi-layer Film Recycling Market Revenue Share, By Film Type, 2025 & 2035

- 5.1.2. Polyethylene-based Films

- 5.1.3. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Polypropylene-based Films

- 5.1.7. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Polyamide-based Films

- 5.1.11. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. EVOH-based Films

- 5.1.15. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Other Film Types

- 5.1.19. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Film Type Market Overview, By Film Type Segment

- Chapter 6. Multi-layer Film Recycling Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Multi-layer Film Recycling Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Food Packaging

- 6.1.3. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Pharmaceutical Packaging

- 6.1.7. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Industrial Packaging

- 6.1.11. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Agriculture Films

- 6.1.15. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Other Applications

- 6.1.19. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Multi-layer Film Recycling Market – By End-Use Industry

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 7.1.1. Multi-layer Film Recycling Market Revenue Share, By End-Use Industry, 2025 & 2035

- 7.1.2. Food & Beverage

- 7.1.3. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Healthcare

- 7.1.7. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Retail

- 7.1.11. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Agriculture

- 7.1.15. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Other Industries

- 7.1.19. Multi-layer Film Recycling Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 8. Multi-layer Film Recycling Market – Regional Analysis

- 8.1. Multi-layer Film Recycling Market Overview, By Region Segment

- 8.1.1. Global Multi-layer Film Recycling Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Multi-layer Film Recycling Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Multi-layer Film Recycling Market Revenue, By Technology, 2026 – 2035

- 8.1.4. Global Multi-layer Film Recycling Market Revenue, By Film Type, 2026 – 2035

- 8.1.5. Global Multi-layer Film Recycling Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Multi-layer Film Recycling Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Multi-layer Film Recycling Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Multi-layer Film Recycling Market Revenue, By Technology, 2026 – 2035

- 8.2.3. North America Multi-layer Film Recycling Market Revenue, By Film Type, 2026 – 2035

- 8.2.4. North America Multi-layer Film Recycling Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Multi-layer Film Recycling Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2.6. U.S. Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Multi-layer Film Recycling Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Multi-layer Film Recycling Market Revenue, By Technology, 2026 – 2035

- 8.3.3. Europe Multi-layer Film Recycling Market Revenue, By Film Type, 2026 – 2035

- 8.3.4. Europe Multi-layer Film Recycling Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Multi-layer Film Recycling Market Revenue, By End-Use Industry, 2026 – 2035

- 8.3.6. Germany Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Multi-layer Film Recycling Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Multi-layer Film Recycling Market Revenue, By Technology, 2026 – 2035

- 8.4.3. Asia Pacific Multi-layer Film Recycling Market Revenue, By Film Type, 2026 – 2035

- 8.4.4. Asia Pacific Multi-layer Film Recycling Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Multi-layer Film Recycling Market Revenue, By End-Use Industry, 2026 – 2035

- 8.4.6. China Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Multi-layer Film Recycling Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Multi-layer Film Recycling Market Revenue, By Technology, 2026 – 2035

- 8.5.3. The Middle-East and Africa Multi-layer Film Recycling Market Revenue, By Film Type, 2026 – 2035

- 8.5.4. The Middle-East and Africa Multi-layer Film Recycling Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Multi-layer Film Recycling Market Revenue, By End-Use Industry, 2026 – 2035

- 8.5.6. Saudi Arabia Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Multi-layer Film Recycling Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Multi-layer Film Recycling Market Revenue, By Technology, 2026 – 2035

- 8.6.3. Latin America Multi-layer Film Recycling Market Revenue, By Film Type, 2026 – 2035

- 8.6.4. Latin America Multi-layer Film Recycling Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Multi-layer Film Recycling Market Revenue, By End-Use Industry, 2026 – 2035

- 8.6.6. Brazil Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Multi-layer Film Recycling Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Multi-layer Film Recycling Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Multi-layer Film Recycling Market: Company Market Share, 2025

- 9.2. Global Multi-layer Film Recycling Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Veolia Environnement S.A.

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. SUEZ SA

- 10.3. Poly-America L.P.

- 10.4. Republic Services Inc.

- 10.5. Waste Management Inc.

- 10.6. Aduro Clean Technologies Inc.

- 10.7. APR2 Plast

- 10.8. Plastic Energy Ltd.

- 10.9. Brightmark LLC

- 10.10. Agilyx Corporation

- 10.11. PureCycle Technologies Inc.

- 10.12. Others.

- 10.1. Veolia Environnement S.A.

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 43

List Of Tables

Tables No 1 to 51

Prominent Player

- Veolia Environnement S.A.

- SUEZ SA

- Poly-America L.P.

- Republic Services Inc.

- Waste Management Inc.

- Aduro Clean Technologies Inc.

- APR2 Plast

- Plastic Energy Ltd.

- Brightmark LLC

- Agilyx Corporation

- PureCycle Technologies Inc.

- Others

FAQs

The key players in the market are Veolia Environnement S.A., SUEZ SA, Poly-America L.P., Republic Services Inc., Waste Management Inc., Aduro Clean Technologies Inc., APR2 Plast, Plastic Energy Ltd., Brightmark LLC, Agilyx Corporation, PureCycle Technologies Inc., Others.

Large brand owners and packaging manufacturers are growing their markets with ambitious sustainability commitments, with the Ellen MacArthur Foundation’s New Plastics Economy Global Commitment with more than 500 organizations representing 20% of global plastic packaging production committed to 100% recyclable packaging by 2025 and 25% recycled content use, with major corporations such as Unilever committing to a 50% reduction of virgin plastic, Nestle pledging 100% of packaging recyclable or reusable, PepsiCo setting a 50% recycled content goal by 2030, and Procter & Gamble targeting 50% recycled content in packaging, collectively creating demand for 8-12 million tons of recycled polyethylene and polypropylene annually by 2030, with direct investments including Danone’s EUR 30 million in chemical recycling partnerships and retailer requirements affecting thousands of product lines driving recyclability improvements and recycled content sourcing.

Advanced technologies in recycling are shifting market potential, with chemical recycling processes such as pyrolysis getting liquid oil yields of 70-85% out of multi-layer polyolefin film and using less energy through process optimization, near-infrared spectroscopy coupled with AI allowing automated sorting at 3-4 times the current rate of 30-40% with 95%+ accuracy compared to 2-3 in earlier systems, modern material recovery plants that are capable of separating 8-12 different film fractions of plastic samples versus 2-3 with basic sorting, compatibilization technologies enabling mechanical recycling of mixed polymer streams without complete separation, and mass balance certification enabling certified circular polymers production meeting food-contact standards, collectively expanding addressable waste streams from approximately 14% currently recyclable to a projected 35% by 2030.

According to the existing analysis, the market is expected to reach some USD 6.92 billion in 2035, with a strong growth rate due to the increasing regulatory demands to recycle and use recycled material, the development of chemical recycling facilities to process previously indefeasible multi-layer structures, corporate commitments to sustainable packaging, the advances in technology to enhance separation efficiency and material quality, and the implementation of the circular economy opportunities to the closed-loop system, at the CAGR of 9.2% between 2026 and 2035.

There is a projected high growth rate of 11.3 of CAGR in the Asia Pacific region due to the fact that the region is also the largest plastic consumer in the world with an importation of more than 50% of the global production and consumption of plastics. China has invested more than USD 12 billion in domestic recycling investments between 2018 and 2024 and its policies on plastic waste management requirements with Thailand are targeting 100% plastic waste recycling by 2027, and the investment towards recycling infrastructure in the region is USD 4.

There is a projected high growth rate of 11.3 of CAGR in the Asia Pacific region due to the fact that the region is also the largest plastic consumer in the world, with an importation of more than 50% of the global production and consumption of plastics. China has invested more than USD 12 billion in domestic recycling investments between 2018 and 2024 and its policies on plastic waste management requirements with Thailand are are targeting 100% plastic waste recycling by 2027, with the investment towards recycling infrastructure in the region of USD 4.2 billion in 2024 with projections exceeding USD 8 billion by 2028.

Global Multi-layer Film Recycling Market is estimated to grow significantly because of the strict environmental policies where the EU requires 100% recyclable packaging by 2030 and a minimum recycled content of 30% to 65% annually with the top 100 consumer goods companies producing over 30 million tons of plastic packaging and with 50-100% usage of recycled content capacity in 2024 of 350,000 tons, which will rise to over 3 million tons by 2027 in the United States alone, and demand for recycling capacity expanding from 350,000 tons in 2024 to over 3 million tons by 2027 in the United States alone, and demand for recycled polyethylene and polypropylene projected to reach 8-12 million tons annually by 2030 representing 600% increase.