Generative AI in Chemical Market Size, Trends and Insights By Component (Software/Platforms (Generative AI Models, Chemical Informatics Platforms, Molecular Design Tools), Services (Implementation & Integration, Training & Consulting, Managed AI Services), Other Components (APIs, Data Infrastructure, Hardware Acceleration)), By Application (Molecule & Material Discovery (De Novo Molecular Design, Property Prediction, Virtual Screening), Process Optimization & Simulation (Reaction Condition Generation, Plant Optimization, Digital Twins), Predictive Maintenance (Equipment Failure Prediction, Corrosion Modeling), Supply Chain Optimization (Demand Forecasting, Procurement, Inventory), Safety & Compliance Management (QSAR Toxicology, Regulatory Intelligence, SDS Generation), Formulation Design (Coating, Adhesive, Agrochemical, Pharma Formulation), Other Applications (Patent Intelligence, Customer Engagement, Technical Service)), By Deployment Mode (Cloud-Based (Public Cloud, SaaS AI Platforms, Hybrid Cloud), On-Premise (Private AI Infrastructure, Secure Enterprise Deployment)), By End-Use Industry (Specialty Chemicals, Petrochemicals & Polymers, Agrochemicals, Pharmaceuticals & Life Sciences, Paints & Coatings, Consumer & Home Care Chemicals, Other Industries (Mining Chemicals, Electronic Chemicals, Adhesives)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 24.9%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- Schrödinger Inc.

- Insilico Medicine Ltd.

- Molecule one

- Chemify Ltd.

- Others

Reports Description

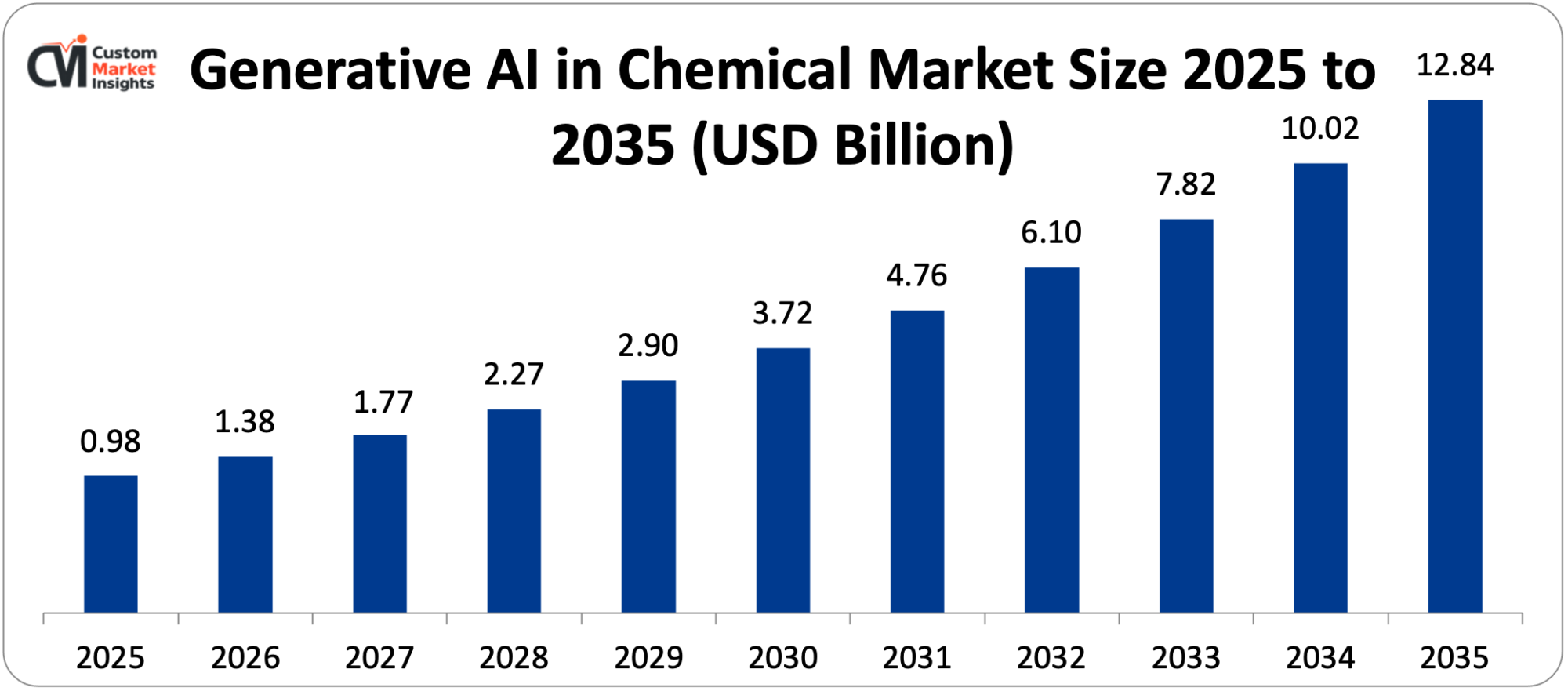

The global chemical market size for generative AI is estimated at USD 0.98 billion in 2025 and is projected to grow by USD 1.38 billion in 2026 to about USD 12.84 billion by 2035, with a CAGR of 24.9% between 2026 and 2035.

The unprecedented business momentum of generative AI technology platforms displaying transformative capacity in molecular property prediction, retrosynthesis planning, formulation optimization, and process condition generation compelling chemical industry R&D and operations leadership to invest in AI-enhanced workflows relieving decades-old experimental trial-and-error model paradigms, the increasingly swift compression of chemical discovery timelines by years to months through the generation and screening of millions of candidate molecular structures, which is contributed by increasingly competitive pressure on chemical companies to accelerate acquisition of new products and improvement of process efficiency in the face of commodity chemical cycles and screening millions of candidate molecular structures computationally before any laboratory synthesis is attempted, the accelerating deployment of large language models and multimodal foundation models fine-tuned on chemical domain data including scientific literature, patent databases, reaction databases, and materials property repositories providing chemical-specific generative intelligence unavailable from general-purpose AI systems, the rising competitive pressure on chemical companies to accelerate new product development and process efficiency improvement in the face of margin compression from commodity chemical cycles and sustainability transformation costs that makes AI-powered productivity enhancement a strategic business imperative, and the progressive maturation of chemical AI platform ecosystems with validated commercial case studies demonstrating measurable return on investment collectively drive robust and exceptional growth throughout the forecast period.

Market Highlight

- The generative AI dominated the chemical market in North America with a 42% market share in 2025.

- Asia Pacific will have the highest CAGR of 28.4% in the year 2026 to 2035.

- By component, the software/platforms segment is estimated to have taken about 64% of the market share in 2025.

- By segment, the services category has the highest CAGR of 26.8% between 2026 and 2035.

- By mode of deployment, the cloud-based segment will have the largest market share of 72% in 2025 and the cloud based segment will have the highest CAGR of 25.6% between 2026 and 2035.

- By application, the molecule and material discovery segment will add the largest market share of 31% in 2025 with the process optimization and simulation segment projected to grow by the highest CAGR of 27.2% between 2026 and 2035.

- By end-use industry, the specialty chemicals segment will also have the highest market share of 28% in 2025, and the pharmaceuticals and life sciences segment will have the highest CAGR of 26.8% between 2026 and 2035.

Significant Growth Factors

The Generative AI in Chemical Market Trends present significant growth opportunities due to several factors:

- Molecular Discovery and Materials Design Acceleration Transforming Chemical R&D Productivity:

The use of generative AI in molecular discovery and novel materials design, where generating molecular structure-based generative models trained on databases of molecular structure, property, and synthesis paths proposes novel candidate molecules with predicted target properties, is the most radical and commercially strong value proposition that drives the uptake of generative AI in the chemical industry, as the reported capability of the AI-generated molecular structures at providing target property profiles previously inaccessible by human chemist-led research strategies based on structure-activity reasoning alone creates an irreproducible competitive advantage to chemical R&D organizations adopting such solutions.

The size of the chemical space of all theoretically possible organic molecules is estimated between 1023 and 1060 distinct compounds – an astronomical number, and consequently, it is practically impossible to screen a significant fraction of this chemical space experimentally – and generative AI models can computationally explore and rank large areas of this chemical space in hours, suggesting solutions that are optimized to simultaneously satisfy multiple property goals, such as biological activity, physicochemical properties, synthetic accessibility, and regulatory safety profile, which multi-objective optimization algorithms can find in the latent space of the The application of generative AI to formulation design reportedly shortened the timelines of the formulation development process at BASF by 70%, a process that took 18–24 months using traditional laboratory screening methods, to 46 months consisting of 46 months of generative AI-assisted experimental validation, with the anticipated real-life competitive implication of shorter development cycles in new product market entry. An example of AI-proposed candidate materials being successfully demonstrated to yield gains in target barrier property profiles previously inaccessible in the existing polymer library of Dow Chemical is its collaboration with IBM in artificial intelligence-accelerated materials discovery, based on the use of IBM generative chemistry models to design polymers in packaging applications, which has resulted in AI-proposed candidate materials with the desired barrier properties not found in the existing polymer library.

The foundation model paradigm – where large transformer-based neural networks pre-trained on large collections of chemical data corpora such as the 100 million compounds in the PubChem database, the 40 million reactions in the Reaxys database, and the corpus of scientific literature of millions of chemistry publications – offers a universal chemical intelligence substrate that can be customized to particular molecular discovery tasks within a single chemical company without necessarily having each individual company build and train foundation models themselves, offering a significantly smaller AI implementation barrier to chemical R&D organizations of all sizes. Comparative studies on AI-generated molecular candidates with expert medicinal chemist proposals and published benchmarking studies have all shown AI to perform better in systematic chemical space exploration and expert chemists to do better at creative leap intuition and experimental insight (such as discovering novel molecules using known compounds), but not in complete replacement of human chemical prowess.

- Process Optimization and Digital Chemical Plant Operations Generating Operational Value:

Generative AI in chemical manufacturing process optimization, such as reaction condition optimization, separation process design, process troubleshooting, energy efficiency improvement, and plant-wide production scheduling, is producing near-term operational value that is complementary to the longer-range R&D discovery applications to create a commercial adoption driver with shorter return on investment timelines of 6–18 months that is compelling chemical companies to invest in generative AI capabilities even in the face of executive leadership skeptical of the transformative claims of molecular discovery applications. Chemical manufacturing processes – including reactions, separations, and heat integration, as well as utility systems, whose overall operating space covers thousands of variables in simultaneous interaction over their operating parameters affecting yield, energy use, product quality, and safety — have exceptionally complex optimization problems that are tackled by conventional process simulation and engineering heuristics in a sub-optimal way due to the combinatorial explosion of parameter space which grows exponentially with the complexity of the plant.

In processes with large-scale petrochemical and specialty chemical production, generative AI process optimization strategies (where operating conditions are proposed as an optimization set to a specific production goal and constraint profile by generative models trained on data of historical processes, first-principles simulations, and operator experience) can discover yield, energy usage, and off-specification product rate improvements of 2-8%, 5-15%, and 10-30%, respectively, that operate into millions or tens of millions of dollars of annual operating value. Published case studies have reported consistent yield improvement generated by the implementation of generative AI in SABIC to optimize their ethylene crackers – by training AI models using operational data on various cracker units to produce optimal feed composition, cracking severity, and heat management operating conditions based on the properties of the feedstock they use and the production objectives they need to achieve. The institutional knowledge preservation and expedient corrections proposed by the full historical experience of the plant data encapsulated in large language model-trained systems specializing in process disturbance and quality deviation hypothesis generation through the application of the generative AI process troubling logistics include the generation of hypotheses regarding the underlying cause of a process disturbance and quality deviation and suggest remedial actions based on the complete historical experience of the plant’s workforce undergoing demographic transition.

What are the Major Advances Changing the Generative AI in Chemical Market Today?

- Large Language Model Fine-Tuning on Chemical Domain Data Creating Specialized Chemical Intelligence:

The construction and commercial application of chemical domain-specific large language models that are trained or fine-tuned on chemical literature collections, on patent collections, on reaction collections, on materials property collections, and on regulatory submission collections which in aggregate encode the cumulative chemical knowledge of the chemistry discipline are developing artificial intelligence systems that have true chemical domain expertise, allowing chemical-specific reasoning, prediction of properties, synthetic planning, and analysis of regulatory submissions functions to be directly and immediately valuable to chemical R&D and regulatory affairs functions. General purpose LLMs such as GPT-4, Claude, and Gemini encode much of the chemical knowledge found in scientific publications and textbooks, offering useful though limited chemical reasoning capability limited by the fact that the LLM never saw the special databases molecular property databases, reaction condition repositories, ADMET databases, and formulation performance records that constitute the most commercially important assets in chemical knowledge.

Chemical domain-specific LLMs – such as Chemformer trained by AstraZeneca Research Group, ChemBERTa trained on SMILES molecular representations, IBM MoLFormer trained on 1.1 billion molecular structures, and Anthropic chemistry-fine-tuned models – are able to develop molecular representation knowledge, reaction prediction, and chemical property reasoning on specific chemistry problems that general-purpose LLMs cannot compete with. Chemical AI systems can use the retrieval-augmented generation approach, where chemical LLMs are linked to dynamically updated chemical databases, real-time literature repositories, and proprietary company data stores which are retrieved during inference, to access up-to-date chemical data beyond the date of cutoff on which the model was trained, respond to queries about recently published compounds and reactions and tap into proprietary company data without disclosing intellectual property information. Schrödinger, which integrates drug discovery with generative artificial intelligence, Insilico Medicine, which is an LLM-based chemistry42 engine, and Molecule.one, which is a retrosynthesis planning engine, are all commercial applications of chemistry-specific generative AI, and are already commercially deployed by pharmaceutical and specialty chemical firms, showing the commercial shift of research proof-of-concept to commercial deployment.

- Generative AI for Retrosynthesis Planning and Route Scouting:

One of the most intellectually challenging and time-intensive tasks in synthetic chemistry, reaction planning by generative AIs trained on reaction databases is proposing multi-step synthetic routes between starting materials and target molecules using commercially available starting materials, simultaneously assessing the viability of the route, cost, atom economy, waste generation, and safety hazard profile of those routes. This is being tackled by AI-generated route proposals, with synthetic chemists finding novel synthetic routes that expert chemists might not attempt to find due to their training on conventional reaction paradigms. Retrosynthesis – the disassembly of a target molecule into simpler precursor fragments by the hypothetical transformation of all its bonds through hypothetical bond-breaking reactions, recursively, until the synthesist has access to commercially available building blocks – must entail the synthesist employing knowledge of thousands of named reactions, reaction condition imperatives, protecting group strategies, stereochemical concerns, and yield and selectivity predictions that practiced synthetic chemists have gained over decades of experience in the synthesis of useful molecules. In its published experience of AI retrosynthesis planning AstraZeneca implemented AI-based retrosynthesis planning with the IBM RXN Chemistry platform where it used said system to compute AI-reported routes to a set of targets (pharmaceutical compounds) where it found novel disconnection strategies not considered by experienced synthetic chemists and where some proposed routes by the AI were proven useful as practical synthetic paths to improve upon the conventional ones based on atom economy and step count.

The recent adoption of AI retrosynthesis capability by the pharmaceutical industry is led by Synthia (formerly ICSYNTH) at Merck KGaA, the use of generative retrosynthesis platforms by Eli Lilly, and the commercial use by Pfizer in collaboration with Insilico Medicine in the field of AI synthesis planning, followed by the specialty chemical industry with applications in complex catalyst synthesis, active ingredient route optimization in agrochemicals, and specialty polymer synthesis planning. Incorporation of retrosynthesis AI with automated synthesis systems – where AI-suggested pathways are operated on robotic synthesis platforms without human input during the synthesis process, and thus the semifinal molecules are synthesized with no human input whatsoever – is the future of AI-assisted accelerated chemical discovery that major pharmaceutical and specialty chemical companies are exploring as the final realization of AI-human partnership in molecular discovery.

- Generative AI for Formulation Design and Product Performance Optimization:

- Application of generative AI to formulation design, including polymer blend formulations, coating formulations, adhesive systems, agricultural spray formulations, pharmaceutical dosage formulations, and consumer product formulations, is facilitating the systematic search of the multidimensional formulation space that cannot be efficiently explored using conventional one-variable-at-a-time experimental design and expert formulator intuition. Formulation chemistry – where the functionality of the end product is determined by the multifaceted interactions between a number of ingredients such as active ingredients, carriers, solvents, surfactants, rheology modifiers, stabilizers and functional additives — optimization problems of very high dimension where the performance response surface is non-linear, non-convex, and frequently poorly described by first-principles models, provide favorable conditions over which data-driven generative AI optimization strategies can learn the performance surface by experiment data. Specialty coatings formulation – where performance requirements such as adhesion, hardness, scratch resistance, UV resistance, gloss stability, and application viscosity have to be optimized simultaneously under regulatory VOC limits, cost constraints of available raw materials, and compatibility of manufacturing processes – is an example of a multi-objective formulation optimization problem where generative AI can suggest formulation candidates with desired property combinations that years of laboratory screening of the relevant ingredient space could find through systematic human screening of the same. According to the experience reported by the Coatings division of BASF, the use of AI in the design of formulations, i.e. machine learning and generative model, to develop automotive OEM coats found that the number of experimental steps needed to reach the desired formulation performance specification was reduced by 30%, or a significant acceleration in new coatings product development, directly translating into lower R&D costs per new product launched. The collaboration between Evonik and Nouscom on generative AI-directed design of lipid nanoparticles to deliver mRNA vaccines and gene therapies as part of the mRNA delivery applications Nouscom has developed mRNA delivery applications anchored on lipid nanoparticles, involving the use of generative AI to design lipid nanoparticles with measured nucleic acid encapsulation efficiency and in vivo delivery performance, which is the pharmaceutical formulation application of generative AI that is receiving the greatest commercial interest due to the strategic significance of lipid nanoparticle delivery.

Category Wise Insights

By Component

Why Does Software/Platforms Lead the Market?

Software and platforms are the biggest component segment with about 64% of total market share in 2025, as they represent the commercial structure of generative AI in the chemical market where cloud-deployed SaaS facilities offering computational capabilities in the form of molecular design, retrosynthesis planning, formulation optimization and process simulation dominate the entire adoption of generative AI in the chemical market by being deployed on subscription with no hardware ownership of AI infrastructure by the chemical company customers.

The software platform market is represented by a range of types of solutions, including specialized point solutions like molecular generation platforms like LiveDesign by Schrodinger, retrosynthesis planning tools like Molecule.one, and formulation AI tools like Kebotix, and provides end-to-end enterprise chemical R&D workflows with unified software packages that have integrated multiple different applications. The prevalent business model of chemical AI software, annual subscription licensing typically costing USD 50,000–USD 2,000,000 per organization (based on scope, user numbers and breadth of application), offers vendors a reliable stream of recurring revenue and subscription spending treatment to chemical company clients which avoids the capital budgeting process of large technology investments, enabling use at large and mid-size chemical companies with pre-established budgets on digital transformation. The trend in platform consolidation (where chemical companies are moving towards integrated AI platforms with unified molecular data management, generative design, property prediction, and experimental data integration) is favouring comprehensive platform providers such as Schrodinger, which is an integrated physics-based simulation platform with few machine learning generative models, and emerging integrated platform providers looking to claim the enterprise platform market leadership.

By Application

Why Does Molecule & Material Discovery Lead the Market?

The largest application segment is molecule and material discovery with an estimated market share of 31% of total market share in 2025 which portrays the chemical industry preference to invest in AI in the R&D department where the chemical space exploration capability of generative AI offers the most basic and competitively differentiating value, which consists of compressing the discovery timeline, lowering the cost of experiments per successful candidate, and achieving parts of the chemical space that cannot be accessed efficiently through traditional research methods. The market dominance of the discovery application indicates the threat concentration of generative AI value modeling in pharmaceutical and specialty chemical R&D with published case studies describing tangible time-to-market speed-up and new IP creation that warrant a high-end platform fee. The molecule and material discovery submarket includes the most valuable single deals in the generative AI chemical market, e.g. enterprise drug discovery platform subscriptions in large pharmaceutical companies are multi-million dollar-per-annum deals, and the larger market is also accessed by the mid-market specialty chemical companies implementing AI discovery platforms at more affordable purchase costs to catalyst design, polymer synthesis, and materials optimization applications.

By Deployment Mode

Why Does Cloud-Based Deployment Lead the Market?

Cloud-based deployment is the most dominant, with a market share of circa 72% in 2025, as the creation of the GPU computing infrastructure, AI model development capacity, and continuous model enhancement pipelines needed to support frontier generative AI could be impractical in terms of costs and time to build and maintain in any case and could only be commercially practicable with respect to cloud access to AI platform capabilities, available to all but the largest chemical firms with the most advanced internal digital capabilities.

The access by the cloud deployment model to frontier AI computing, with cloud AI platform vendors executing generative chemistry models on GPU clusters of thousands of accelerators, which even single chemical companies could not afford to own, offers chemical company cloud customers a scale-with-investment-in-AI-infrastructure access, as opposed to an investment in hardware per company. On-premise deployment is still relevant to the largest chemical companies globally, such as BASF, Dow, SABIC and LyondellBasell, where the confidentiality of proprietary chemical information is a concern, internal IT governance is necessary to protect chemical intellectual property, and the magnitude of AI implementation justifies dedicated infrastructure deployment to support applications of AI and molecular discovery and process optimization as the most sensitive.

By End-Use Industry

Why Does the Specialty Chemicals Segment Lead the Market?

The largest end-use segment, at about 28% of market share in 2025 is the specialty chemicals segment, as it reflects the amalgamation of the highest R&D intensity of all chemical industry segments, specialty chemical companies investing 38%-8% of revenues to R&D versus 0.5%-2% for commodity chemical producers; the most diverse product portfolio that forms the greatest cumulative new product development opportunity to accelerate AI; and the most direct competitive power of differentiated product innovation where improvement of R&D productivity directly translates to market position and market protection. Specialty chemical firms such as Evonik, Clariant, Lanxess, and Ashland are putting generative AI into use in areas like catalyst design, surfactant development, polymer additive optimization, and performance chemical formulation applications in which AI-accelerated discovery provides competitive advantages in new product introduction plans compared to their competitors, who lack similar AI capabilities. Pharmaceutical industry Pharmaceutical industry The pharmaceutical industry is early in aggressively researching and adopting AI chemistry tools at an unprecedented rate, with the pharmaceutical industry’s best-known AI sector being the drug discovery part, which directly benefits a drug by saving a year off the time-to-market timeline, which can result in billions of dollars in extra revenues and thus a faster investment payoff, and the pharmaceutical industry is broadening its use of AI chemistry tools beyond drug discovery to pharmaceutical formulation and pharmaceutical process chemistry optimization.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 1.38 billion |

| Projected Market Size in 2035 | USD 12.84 billion |

| Market Size in 2025 | USD 0.98 billion |

| CAGR Growth Rate | 24.9% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Component, Application, Deployment Mode, End-Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the North America Market Size?

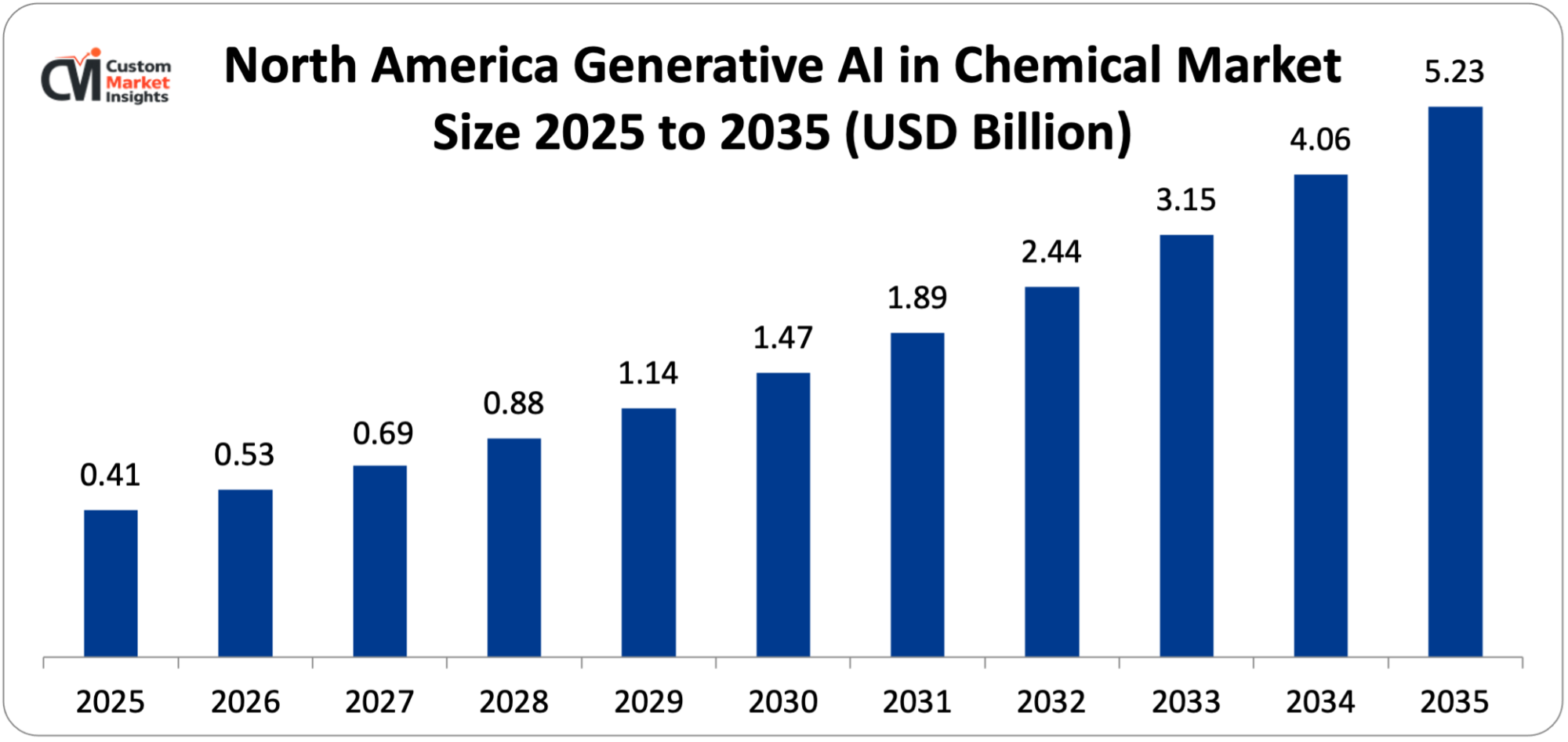

The North America generative AI in chemical market size is estimated at USD 413 million in 2025 and is projected to reach approximately USD 5.23 billion by 2035, with a CAGR of 28.8% from 2026 to 2035.

Why Did North America Dominate the Market in 2025?

In 2025, North America is estimated to have about 42% of global market share, which reflects the status of the United States as the global center of AI technology development – with most frontier generative AI models, chemical AI platforms and venture capital-funded AI chemistry startups being headquartered in the United States – and the concentration of the global investment in pharmaceutical R&D in the U.S. biopharmaceutical cluster, which provides the highest-value early adopter customers of AI, the most advanced specialty chemical industry with the highest digital investment per revenue, and The early and extensive AI chemistry use of the U.S. pharmaceutical industry, with major pharma companies such as Pfizer, Merck, Bristol-Myers Squibb, AbbVie, and Eli Lilly all having active AI chemistry platform programs and AI process chemistry platforms, giving the chemical AI platform vendor a base of the largest single-country customers and being the commercial expression of the AI chemistry value that is leading to adoption in downstream specialty chemical, agrochemical, and coatings industry segments.

The AI startup sector of Silicon Valley, which has spawned firms such as Schrodinger (now publicly traded), Insilico Medicine, Recursion Pharmaceuticals, Chemify, and dozens of other firms in the earlier-stage chemical AI development niche, has developed a cluster of commercial AI platform development that positions North America as the supplier of technology to the global chemical AI market.

Why is Europe a Strategically Important Market?

The European generative AI in the chemical market is approximated to be USD 218 million in 2025, and it is expected to grow to USD 2.74 billion in 2035 at the CAGR of 28.9. Europe is a fundamentally strategic-value market due to the clustering of the largest and most significant chemical corporations globally, including BASF, Evonik, Lanxess, Clariant, Solvay and Covestro, which creates vast potential value due to the use of AI-accelerated discovery and process optimization, the excessive investment in AI chemistry by the European pharmaceutical industry in AstraZeneca (UK), Roche (Switzerland), Novartis (Switzerland), and Bayer (Germany), and the acute sustainability transformation mandate under the EU Chemical Strategy. Germany is Europe’s largest generative AI in the chemical market – concentrated in the presence of the largest chemical company in the world, like BASF utilising AI applications in all of its molecular design, formulation and process optimization processes, the concentration of major specialty chemical firms in an industry cluster in Germany, and the academic chemical AI excellence in Germany with institutes such as the Max Planck Institute, RWTH Aachen, and TU Munich, the source of talent to feed into the German chemical industry AI adoption. The pharmaceutical AI chemistry programs of AstraZeneca, GlaxoSmithKline, and the AstraZeneca AI research center in Cambridge, which publishes leading academic AI chemistry research and commercializes AI tools internally, and AI-enabled programs of the Rosalind Franklin Institute, which are the infrastructure of government-funded chemical AI research, characterize the chemical AI market of the United Kingdom.

Why is Asia Pacific the Fastest-Growing Market?

The fastest-growing regional market with an expected CAGR of 28.4% between 2026 and 2035 is Asia Pacific, and this is due to the groundbreaking state of government investment in AI and the digital transformation of the enormous and varied Chinese chemical sector, which is the largest national chemical market by production volume, Japan with its advanced chemical and pharmaceutical industry using AI chemistry platforms at major companies such as Mitsubishi Chemical, Sumitomo Chemical, Takeda, and Daiichi Sankyo; South Korea with its Samsung SDI, LG Government-sponsored AI in chemistry initiatives in China, such as the AI-chemistry research grants of the Ministry of Science and Technology, and the development of domestic AI chemistry initiatives by firms such as SinoMab, Zhejiang Lab, and a series of AI chemistry startups funded by the technology venture ecosystem of China are generating concurrently an AI-enabled chemistry capability base and competitive adoption pressure on Chinese-based chemical firms to adopt AI or face a risk of R&D productivity disadvantage relative to AI-adopting foreign peers. The adoption of AI in Japan The methods of the Japanese chemical industry The Japanese chemical industry is adopting AI systematically and methodically, making it a faster process, and chemistry-specific features of domestic AI solutions and international platforms adapting to Japanese language and chemical regulation needs are being created.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region is exhibiting developmental trends of increasing market with Saudi Arabia having SABIC which is one of the largest petrochemical companies in the world, which has operation AI-enhanced process optimization programs in their manufacturing plants and is exploring generative AI in polymer design which will make India the largest individual country market in the South Asia region.

Top Players in the Market and Their Offerings

- NVIDIA Corporation

- IBM Corporation (IBM Research Chemistry RXN for Chemistry)

- Microsoft Corporation (Azure AI for Chemistry)

- Schrödinger Inc.

- Insilico Medicine Ltd.

- Molecule one

- Chemify Ltd.

- Kebotix Inc.

- Recursion Pharmaceuticals Inc.

- BASF SE (AI/Digital Ventures)

- Evonik Industries AG (Creavis Digital)

- Syngenta AG (Digital Agronomy)

- Others

Key Developments

The market has undergone significant developments as industry participants seek to advance chemical foundation model capabilities, expand enterprise platform deployments, and respond to the accelerating adoption of generative AI across chemical R&D and manufacturing operations globally.

- In November 2024: BASF declared the publicity of its proprietary Chemical Foundation Model a large language model that had been trained on internal chemical data collection at BASF, containing more than 5 decades of formulation research data, documentation of synthesis routes, data on process optimization, and customer application performance feedback and publicly accessible chemical databases deployed internally in the BASF R&D, formulation, and process engineering functions serve as the single AI chemistry intelligence platform adopted by the company.

- In January 2025: Schrödinger introduced a strategic collaboration with Dow Chemical integrating the physics-based generative molecular design engine with the Dow proprietary polymer performance database of more than two million experimental data points developed over 50 years of polymer research and development – to design next-generation sustainable packaging materials in support of Dow’s pledges to the New Plastics Economy Global Commitment of the Ellen MacArthur Foundation.

The Generative AI in Chemical Market is segmented as follows:

By Component

- Software/Platforms (Generative AI Models, Chemical Informatics Platforms, Molecular Design Tools)

- Services (Implementation & Integration, Training & Consulting, Managed AI Services)

- Other Components (APIs, Data Infrastructure, Hardware Acceleration)

By Application

- Molecule & Material Discovery (De Novo Molecular Design, Property Prediction, Virtual Screening)

- Process Optimization & Simulation (Reaction Condition Generation, Plant Optimization, Digital Twins)

- Predictive Maintenance (Equipment Failure Prediction, Corrosion Modeling)

- Supply Chain Optimization (Demand Forecasting, Procurement, Inventory)

- Safety & Compliance Management (QSAR Toxicology, Regulatory Intelligence, SDS Generation)

- Formulation Design (Coating, Adhesive, Agrochemical, Pharma Formulation)

- Other Applications (Patent Intelligence, Customer Engagement, Technical Service)

By Deployment Mode

- Cloud-Based (Public Cloud, SaaS AI Platforms, Hybrid Cloud)

- On-Premise (Private AI Infrastructure, Secure Enterprise Deployment)

By End-Use Industry

- Specialty Chemicals

- Petrochemicals & Polymers

- Agrochemicals

- Pharmaceuticals & Life Sciences

- Paints & Coatings

- Consumer & Home Care Chemicals

- Other Industries (Mining Chemicals, Electronic Chemicals, Adhesives)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Generative AI in Chemical by Segments

- 2.1.2. Generative AI in Chemical by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Generative AI in Chemical Market Attractiveness Analysis, By Component

- 2.2.3. Generative AI in Chemical Market Attractiveness Analysis, By Application

- 2.2.4. Generative AI in Chemical Market Attractiveness Analysis, By Deployment Mode

- 2.2.5. Generative AI in Chemical Market Attractiveness Analysis, By End-Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Molecular Discovery and Materials Design Acceleration Transforming Chemical R&D Productivity

- 3.1.2. Process Optimization and Digital Chemical Plant Operations Generating Operational Value

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Generative AI in Chemical Market – By Component

- 4.1. Component Market Overview, By Component Segment

- 4.1.1. Generative AI in Chemical Market Revenue Share, By Component, 2025 & 2035

- 4.1.2. Software/Platforms (Generative AI Models, Chemical Informatics Platforms, Molecular Design Tools)

- 4.1.3. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Services (Implementation & Integration, Training & Consulting, Managed AI Services)

- 4.1.7. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Other Components (APIs, Data Infrastructure, Hardware Acceleration)

- 4.1.11. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Component Market Overview, By Component Segment

- Chapter 5. Generative AI in Chemical Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Generative AI in Chemical Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Molecule & Material Discovery (De Novo Molecular Design, Property Prediction, Virtual Screening)

- 5.1.3. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Process Optimization & Simulation (Reaction Condition Generation, Plant Optimization, Digital Twins)

- 5.1.7. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Predictive Maintenance (Equipment Failure Prediction, Corrosion Modeling)

- 5.1.11. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Supply Chain Optimization (Demand Forecasting, Procurement, Inventory)

- 5.1.15. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Safety & Compliance Management (QSAR Toxicology, Regulatory Intelligence, SDS Generation)

- 5.1.19. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Formulation Design (Coating, Adhesive, Agrochemical, Pharma Formulation)

- 5.1.23. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1.26. Other Applications (Patent Intelligence, Customer Engagement, Technical Service)

- 5.1.27. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 5.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.29. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Generative AI in Chemical Market – By Deployment Mode

- 6.1. Deployment Mode Market Overview, By Deployment Mode Segment

- 6.1.1. Generative AI in Chemical Market Revenue Share, By Deployment Mode, 2025 & 2035

- 6.1.2. Cloud-Based (Public Cloud, SaaS AI Platforms, Hybrid Cloud)

- 6.1.3. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. On-Premise (Private AI Infrastructure, Secure Enterprise Deployment)

- 6.1.7. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Deployment Mode Market Overview, By Deployment Mode Segment

- Chapter 7. Generative AI in Chemical Market – By End-Use Industry

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 7.1.1. Generative AI in Chemical Market Revenue Share, By End-Use Industry, 2025 & 2035

- 7.1.2. Specialty Chemicals

- 7.1.3. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Petrochemicals & Polymers

- 7.1.7. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Agrochemicals

- 7.1.11. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Pharmaceuticals & Life Sciences

- 7.1.15. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Paints & Coatings

- 7.1.19. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Consumer & Home Care Chemicals

- 7.1.23. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1.26. Other Industries (Mining Chemicals, Electronic Chemicals, Adhesives)

- 7.1.27. Generative AI in Chemical Share Forecast, By Region (USD Billion)

- 7.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.29. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 8. Generative AI in Chemical Market – Regional Analysis

- 8.1. Generative AI in Chemical Market Overview, By Region Segment

- 8.1.1. Global Generative AI in Chemical Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Generative AI in Chemical Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Generative AI in Chemical Market Revenue, By Component, 2026 – 2035

- 8.1.4. Global Generative AI in Chemical Market Revenue, By Application, 2026 – 2035

- 8.1.5. Global Generative AI in Chemical Market Revenue, By Deployment Mode, 2026 – 2035

- 8.1.6. Global Generative AI in Chemical Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Generative AI in Chemical Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Generative AI in Chemical Market Revenue, By Component, 2026 – 2035

- 8.2.3. North America Generative AI in Chemical Market Revenue, By Application, 2026 – 2035

- 8.2.4. North America Generative AI in Chemical Market Revenue, By Deployment Mode, 2026 – 2035

- 8.2.5. North America Generative AI in Chemical Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2.6. U.S. Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Generative AI in Chemical Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Generative AI in Chemical Market Revenue, By Component, 2026 – 2035

- 8.3.3. Europe Generative AI in Chemical Market Revenue, By Application, 2026 – 2035

- 8.3.4. Europe Generative AI in Chemical Market Revenue, By Deployment Mode, 2026 – 2035

- 8.3.5. Europe Generative AI in Chemical Market Revenue, By End-Use Industry, 2026 – 2035

- 8.3.6. Germany Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Generative AI in Chemical Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Generative AI in Chemical Market Revenue, By Component, 2026 – 2035

- 8.4.3. Asia Pacific Generative AI in Chemical Market Revenue, By Application, 2026 – 2035

- 8.4.4. Asia Pacific Generative AI in Chemical Market Revenue, By Deployment Mode, 2026 – 2035

- 8.4.5. Asia Pacific Generative AI in Chemical Market Revenue, By End-Use Industry, 2026 – 2035

- 8.4.6. China Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Generative AI in Chemical Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Generative AI in Chemical Market Revenue, By Component, 2026 – 2035

- 8.5.3. The Middle-East and Africa Generative AI in Chemical Market Revenue, By Application, 2026 – 2035

- 8.5.4. The Middle-East and Africa Generative AI in Chemical Market Revenue, By Deployment Mode, 2026 – 2035

- 8.5.5. The Middle-East and Africa Generative AI in Chemical Market Revenue, By End-Use Industry, 2026 – 2035

- 8.5.6. Saudi Arabia Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Generative AI in Chemical Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Generative AI in Chemical Market Revenue, By Component, 2026 – 2035

- 8.6.3. Latin America Generative AI in Chemical Market Revenue, By Application, 2026 – 2035

- 8.6.4. Latin America Generative AI in Chemical Market Revenue, By Deployment Mode, 2026 – 2035

- 8.6.5. Latin America Generative AI in Chemical Market Revenue, By End-Use Industry, 2026 – 2035

- 8.6.6. Brazil Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Generative AI in Chemical Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Generative AI in Chemical Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Generative AI in Chemical Market: Company Market Share, 2025

- 9.2. Global Generative AI in Chemical Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. NVIDIA Corporation

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. IBM Corporation (IBM Research Chemistry RXN for Chemistry)

- 10.3. Microsoft Corporation (Azure AI for Chemistry)

- 10.4. Schrödinger Inc.

- 10.5. Insilico Medicine Ltd.

- 10.6. Molecule.one

- 10.7. Chemify Ltd.

- 10.8. Kebotix Inc.

- 10.9. Recursion Pharmaceuticals Inc.

- 10.10. BASF SE (AI/Digital Ventures)

- 10.11. Evonik Industries AG (Creavis Digital)

- 10.12. Syngenta AG (Digital Agronomy)

- 10.13. Others.

- 10.1. NVIDIA Corporation

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 37

List Of Tables

Tables No 1 to 51

Prominent Player

- NVIDIA Corporation

- IBM Corporation (IBM Research Chemistry RXN for Chemistry)

- Microsoft Corporation (Azure AI for Chemistry)

- Schrödinger Inc.

- Insilico Medicine Ltd.

- Molecule one

- Chemify Ltd.

- Kebotix Inc.

- Recursion Pharmaceuticals Inc.

- BASF SE (AI/Digital Ventures)

- Evonik Industries AG (Creavis Digital)

- Syngenta AG (Digital Agronomy)

- Others

FAQs

The key players in the market are NVIDIA Corporation, IBM Corporation (IBM Research Chemistry RXN for Chemistry), Microsoft Corporation (Azure AI for Chemistry), Schrödinger Inc., Insilico Medicine Ltd., Molecule.one, Chemify Ltd., Kebotix Inc., Recursion Pharmaceuticals Inc., BASF SE (AI/Digital Ventures), Evonik Industries AG (Creavis Digital), Syngenta AG (Digital Agronomy), Others.

The generative AI in the chemical market is affected by government regulations via AI governance frameworks affecting the use of AI in regulated categories of chemical products, intellectual property regulations governing AI-generated chemical inventions, chemical regulatory submission standards being updated to support AI-generated safety and efficacy data, and government investment programs that fund the research and industrial applications of AI in the chemical industries. The AI Act of the EU, which sets risk-based regulation categorization of AI systems and special demands on high-risk AI applications, provides compliance requirements on generative AI systems being applied in chemical safety assessment and regulatory-submission-supporting property prediction systems used in regulated settings prior to deployment. The changing status of AI-generated chemical inventions in patent law, where both the European Patent Office and U.S. Patent and Trademark Office have issued policies on how AI-proposed molecular structures should be treated by patent law, is bringing important implications of IP strategy to chemical companies implementing generative AI in molecular discovery, as the commercial usefulness of AI-generated intellectual property will depend on whether or not the patent protection can be secured (which current IP law frameworks are still in clear discussions about). Regulatory opportunities provided by OECD QSAR regulatory acceptance guidance and an emerging policy of the European Chemicals Agency on the use of computational methods in the submission of assessments of substances under REACH, which gradually allows validated computational toxicology predictions to be used as primary data in a chemical registration submission, create regulatory preconditions where AI-generated safety assessments can have higher commercial value when they help to reduce the number of experimental toxicology studies required. The funding of research in AI in the U.S. CHIPS and Science Act and AI in scientific discovery program by the DOE, which is funding national laboratory chemical AI research at Argonne, Oak Ridge, Lawrence Berkeley and Pacific Northwest national laboratories, is enhancing chemical foundation model capabilities and open-source chemical AI tools, which enter commercial market application by transfer of technology.

The field of generative AI in chemical market pricing is wide in terms of its application sophistication, organization size, data needs, and business model. Basic property prediction can be done at USD 0 to USD 10,000 per year by entry-level chemical AI tools accessible to individual researchers, and small chemical companies such as open-source molecular generation systems, scholarly chemical informatics systems, and entry-level SaaS systems, which have allowed the widest possible adoption of AI in chemistry departments within academia, chemical startup firms, and by individual researchers that inform the market about these technologies and open the talent pipeline to enterprise implementations. Mid-market chemical AI — used by the specialty chemical companies and those with mid-size pharmaceutical companies, and providing full molecular design, retrosynthesis, and formulation optimization solutions—is priced at USD 50,000 – USD 500,000/year in SaaS business models, which constitutes the largest market segment in number of customers and is the most rapidly expanding as mid-size chemical companies move to digital maturity and can afford AI platform investment. Enterprise chemical AI platform contracts Enterprise chemical and pharmaceutical companies with full-enterprise access to the platform, including multiple application modules, proprietary data integration, API integration with laboratory systems, and dedicated customer success services, are priced USD 500,000-USD 5,000,000/year, with the largest enterprise transactions at global pharma and major chemical firms of more than USD 10 million/year, including professional services, implementation, and custom model development. Chemical AI investment services component involved in the preparation and curation of data, platform deployment, model fine-tuning, workflow integration, and change management consulting is usually 50–150% of the value of software licensing in the case of initial enterprise deployments, with mature clients requiring less service dependence as internal AI capability builds through vendor training programs. The ROI economics of chemical AI investment, where even a 2-3 point reduction in the time taken to go through an R&D cycle or a 2-point improvement in the yield of a manufacturing process are profit-making, are leaving investment cases that pass the corporate hurdle rate at decreasing sizes of chemical companies as revenue values decrease relative to the value demonstrated to the customers passed to the customer in the forecast period, addressing the customer market increasingly but not necessarily to the limits of the forecast period, of small enterprise customers, then of mid-market customers, and eventually SME customer segments of the chemical company customer base.

According to the current analysis, the market is expected to grow to about USD 12.84 billion in 2035 due to the deep integration of generative AI into the pharmaceutical industry, resulting in sustained high-value platform demand, the incorporation of AI process optimization in hundreds of manufacturing plants worldwide, creating a vast aggregate operational AI deployment market, the democratization of the open-source foundation model embodied by IBM ChemLLM-7B, enabling chemical AI adoption by mid-size and smaller chemical companies unreachable by frontier capacity models, the development of autonomous AI discovery platforms,— combining generative molecular design, automated synthesis execution, and automated property measurement in closed-loop self-driving laboratory systems — creating premium market segments at the frontier of chemical AI capability, and the expansion of chemical AI beyond R&D and process operations to encompass supply chain intelligence, customer technical service augmentation, regulatory submission automation, and sustainability reporting that broadens the addressable market across all chemical company functions, at a CAGR of 24.9% from 2026 to 2035.

It is anticipated that North America will hold the largest market share in revenue over the forecast period, with a market share of about 42% of global market share in 2025, based on the fact that the United States has the concentration of frontier development and the greatest concentration of generation of commercial-scale AI platform capability by the use of AI in chemical manufacturing and drug discovery, has the most active investment foundation of the United States in AI, with a concentration of U.S.-based companies in the top-value early adopters of chemical AI platform customer cohorts; has an AI startup ecosystem, Silicon Valley’s AI startup ecosystem, producing the majority of commercial chemical AI platform vendors, including Schrödinger, Recursion, Insilico, and Chemify; has the U.S. DOE and DARPA investment in AI for chemical manufacturing and drug discovery providing government funding that advances commercial-stage technology, and has the concentration of global specialty chemical R&D at U.S.-headquartered companies including Dow, DuPont, Eastman, and Cabot, generating the enterprise chemical AI platform market scale that sustains North America’s regional leadership.

The highest forecasted CAGR is that of the Asia Pacific, with a total of 28.4% within the forecast timeframe, driven by generative AI in the chemical market of China with an estimated USD 64 million in current 2025 and growing at a 31.4% CAGR as Chinese chemical and pharmaceutical firms are in urgent need to outcompete using innovation and not cost the fastest growing national market, Japan, with a systematic chemical industry AI adoption acceleration that is currently estimated at Mitsubishi Chemical, Sumitomo Chemical, and other major Japanese pharmaceutical companies, South Korea’s LG Chem, Samsung SDI, and SK Innovation deploying AI for battery material and specialty chemical development, India’s specialty chemical and pharmaceutical sectors adopting AI R&D acceleration at Sun Pharma, Dr. Reddy’s, and Divi’s Laboratories, and the region’s growing AI talent base and government investment in AI for chemistry creating indigenous platform development capabilities supplementing international platform adoption.

The Global Generative AI in Chemical Market is postulated to undergo a considerable growth owing to published benchmarking studies indicating the systematic superiority of AI molecular generation over conventional experimental screening in the exploration of vast chemical space approximated at 1023 to 1060 discrete organic compounds can be sampled by either an operational ROI or high-performance computing system, BASF Chemical Foundation Model evaluation showing AI-suggested formulation candidates reaching performance targets in 68 out of 100 cases in the top-5 format compared to parity with average 14 experimental iterations for conventional approaches, SABIC’s AI cracker optimization generating annual economic benefit of tens of millions of dollars per cracker unit providing operational ROI validation compelling petrochemical industry adoption, IBM’s RXN for Chemistry enabling AstraZeneca to identify novel synthetic routes not proposed by experienced chemists demonstrating AI retrosynthesis capability in pharmaceutical applications, Schrödinger’s Dow partnership identifying 12 novel sustainable packaging polymer candidates in the first year demonstrating materials discovery acceleration timeline, the chemical AI software platform subscription model providing accessible recurring expenditure treatment bypassing capital budget barriers for chemical company AI adoption, and IBM ChemLLM-7B open-source release democratizing chemical foundation model access enabling SME and academic adoption that expands the market base beyond only large chemical company enterprise deployments.