Polymer Functional Materials Market Size, Trends and Insights By Type (Conductive Polymers, PEDOT & PEDOT: PSS, Polyaniline (PANI), Polypyrrole (PPy), Polythiophene & Derivatives, Piezoelectric Polymers, PVDF & Copolymers (PVDF-TrFE), Polyamide-Based Piezoelectrics, Biopolymer Piezoelectrics, Shape Memory Polymers, Thermally Activated SMP, Light-Activated SMP, Magnetically Activated SMP, Self-Healing Polymers, Extrinsic Self-Healing (Microcapsule-Based), Intrinsic Self-Healing (Dynamic Bond-Based), Stimuli-Responsive Polymers, Thermoresponsive Polymers, pH-Responsive Polymers, Photoresponsive Polymers, Electroresponsive Polymers, Barrier Polymers, High-Barrier Films & Coatings, Ion-Exchange Membranes, Gas Separation Membranes, Other Types), By Application (Electronics & Semiconductors, Organic Semiconductors & OLEDs, Flexible & Printed Electronics, Dielectric & Encapsulant Layers, Antistatic & EMI Shielding, Energy Storage & Harvesting, Polymer Solid Electrolytes, Piezoelectric Energy Harvesters, Organic Photovoltaics, Supercapacitor Electrodes, Biomedical & Healthcare, Drug Delivery Systems, Tissue Engineering Scaffolds, Biosensors & Diagnostics, Medical Implants & Coatings, Automotive & Transportation, Aerospace & Defense, Packaging, Other Applications), By End Use Industry (Consumer Electronics, Automotive, Healthcare & Life Sciences, Energy & Power, Aerospace & Defense, Other End Use Industries), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

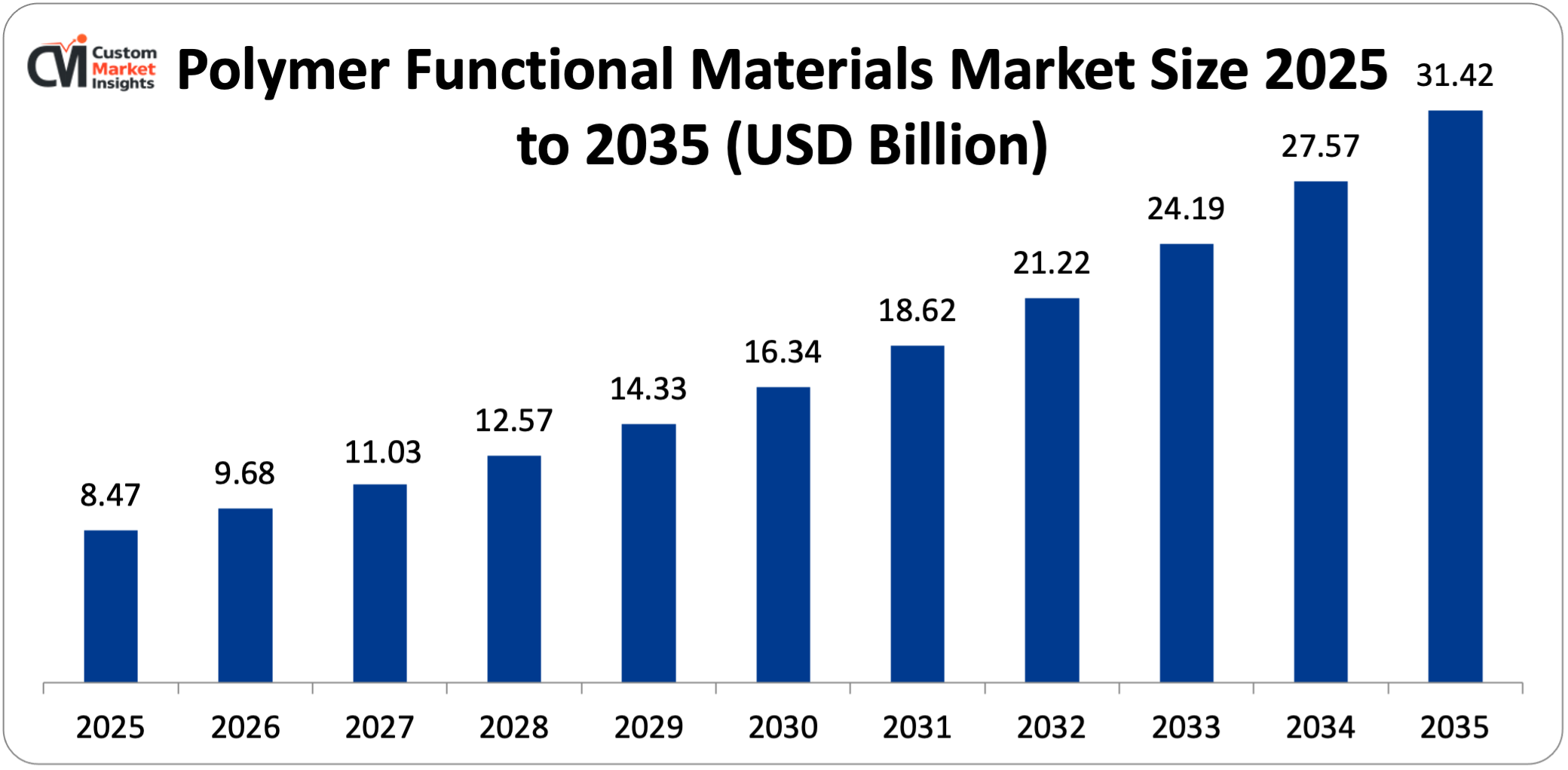

CAGR: 14.1%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- Solvay S.A.

- Arkema S.A.

- BASF SE

- Covestro AG

- Others

Reports Description

The global market for polymer functional materials is expected to grow from USD 9.68 billion in 2026 to about USD 31.42 billion by 2035, with a compound annual growth rate (CAGR) of 14.1% from 2026 to 2035. The market is growing because of the rapid progress in polymer chemistry and materials science that is creating completely new functional property profiles.

There is also a growing demand from the consumer electronics and semiconductor industries for advanced dielectric and conductive polymer materials, as well as the expansion of flexible and wearable electronics that need mechanically adaptive functional polymers. Additionally, there are more biomedical applications that need stimuli-responsive and self-healing biomaterial platforms, and the energy infrastructure is moving more quickly toward polymer-enabled energy storage and harvesting systems.

Market Highlight

- Asia Pacific had the largest share of the polymer functional materials market in 2025, with 41% of the total.

- North America is expected to keep the second-largest market share at 29% in 2025, due to its leadership in biomedical applications, aerospace and defense polymer functional material deployment, and the development of advanced energy storage technology.

- Conductive polymers took up about 28% of the market share in 2025.

- The self-healing polymers segment has the quickest growth rate with a CAGR of 19.4% between 2026 and 2035.

- Electronics and semiconductors have the largest market share in 2025 it was 34%.

- The fastest growing segment will be energy storage and harvesting, with a CAGR of 18.7% between 2026 and 2035.

Significant Growth Factors

The Polymer Functional Materials Market Trends present significant growth opportunities due to several factors:

- Flexible and Wearable Electronics Revolution Driving Transformative Demand for Mechanically Adaptive Functional Polymers:

The rise of flexible, stretchable, and wearable electronics as a commercially important and rapidly growing technology category is creating a whole new area for functional polymers that didn’t exist at a meaningful commercial scale ten years ago. This new area needs materials with combinations of electronic functionality, mechanical deformability, and biological compatibility that no existing conventional material class can provide. Flexible electronics, which include foldable smartphones, rollable display panels, flexible photovoltaic cells, electronic skin patches, smart textiles, and implantable bioelectronics, need substrate, semiconductor, conductor, and encapsulant materials that can handle repeated mechanical deformation cycles with bending radii of less than 5 millimeters, stretching strains of 50–200%, and torsional deformation without breaking or losing electrical performance.

The global flexible electronics market was worth USD36.4 billion in 2024 and is expected to grow at a rate of 15.8% per year to USD87.6 billion by 2030 Polymer functional materials, such as organic thin-film transistors on polyimide substrates, conductive polymer electrodes on PET films, and stretchable silver nanowire-polyurethane composite interconnects, are the most important materials for almost all types of flexible electronic devices. In flexible thin-film transistor architectures, conjugated polymer semiconductors like P3HT (poly(3-hexylthiophene)), PEDOT:PSS (poly(3,4-ethylenedioxythiophene) polystyrene sulfonate), and next-generation non-fullerene acceptor organic semiconductor polymers are achieving carrier mobilities close to or above 10 cm²/V·s, which is competitive with amorphous silicon. This means that polymer-based flexible electronics can meet the performance benchmarks needed for commercial display backplane, sensor array, and logic circuit applications.

Samsung’s Galaxy Z Fold series and Huawei’s Mate X series, along with new rollable display products from LG and TCL, are making flexible-form-factor electronics more popular with consumers. This is leading OEMs to invest in flexible polymer substrate and encapsulant supply chains at a commercial production scale. The wearable healthcare electronics sub-segment, which includes continuous glucose monitoring patches, cardiac monitoring wearables, sweat analysis biosensors, and neural interface devices, has very high functional polymer requirements. This is because it needs to combine the electronic functionality needs of flexible electronics with the biocompatibility, sterilizability, and long-term biostability needs that lead to the specification of advanced biocompatible functional polymer grades that cost a lot.

- Organic Electronics and Printed Electronics Platforms Creating High-Volume Polymer Semiconductor Demand:

The commercial maturation of organic light-emitting diode (OLED) display technology — now the dominant display technology in premium smartphones, growing rapidly in televisions, and entering automotive dashboard and instrument cluster applications — has established organic semiconductor polymers as commercial-scale materials with proven device performance, manufacturing reproducibility, and operational longevity. The global OLED display market was worth USD 51.3 billion in 2024 and is expected to be worth USD 104.7 billion by 2030.

The polymer light-emitting layer materials and charge transport polymer layers used in polymer OLED (PMOLED and AMOLED) displays are two important and growing demand streams for precision-synthesized conjugated polymer functional materials. Printed electronics is a quickly growing way to make money with polymer functional materials. It involves printing conductive, semiconducting, and insulating polymer inks onto flexible substrates using inkjet, gravure, screen, and aerosol jet printing processes. This method costs much less and gives designers more freedom in how they shape their products than traditional photolithographic semiconductor manufacturing.

The global market for printed electronics is expected to grow from USD 12.8 billion in 2024 to USD 43.6 billion by 2032, with a CAGR of 16.5%. Conductive polymer inks, organic semiconductor inks, and dielectric polymer inks are the three main types of functional inks. RFID antennas, smart packaging sensors, in-mold electronics, pressure-sensing arrays, and disposable biosensors are all examples of applications that are driving the adoption of printed electronics. Each of these application categories is creating more demand for the specialized conductive and semiconducting polymer formulations needed for printed devices to work reliably. Perovskite solar cell development is one of the most heavily studied photovoltaic technologies in the world. It is creating a need for polymer hole transport layers, encapsulant films, and flexible substrate materials. Leading manufacturers are expected to start making perovskite-silicon tandem cells commercially between 2026 and 2028, which will be a new high-volume application for functional polymer materials in photovoltaics beyond traditional crystalline silicon solar manufacturing.

What are the Major Advances Changing the Polymer Functional Materials Market Today?

- Self-Healing Polymer Systems Transforming Autonomous Material Damage Response Across Multiple Industries:

The development and gradual commercialization of self-healing polymer materials—systems that can automatically find and fix mechanical damage like scratches, cracks, and punctures using chemical or physical methods triggered by the damage event itself—are one of the most important material innovations of the past decade. It is significantly less expensive than conventional photolithographic semiconductor production and allows designers greater freedom in the shape of the products they create.

The printed electronics market is projected to experience growth to USD 43.6 billion by the year 2032 compared to USD 12.8 billion in 2024 with a CAGR of 16.5%. Conductive polymer inks, organic semiconductor inks, and dielectric polymer inks are the three main types of functional inks. Extrinsic systems use microencapsulated healing agents that are released when a crack breaks the capsule. These agents polymerize in the damage zone to restore mechanical integrity. Intrinsic systems, on the other hand, use reversible dynamic bonds (Diels-Alder adducts, hydrogen bonds, disulfide linkages, metal-ligand coordination bonds, or ionomeric associations) that can reform on their own after bond rupture. Self-healing polymer technology is most widely used in automotive clear coats. Self-healing polyurethane and acrylate clearcoat systems that are activated by solar heat or ambient temperature are now standard on premium vehicles from BMW, Nissan (Scratch Shield technology), and Hyundai-Kia.

The automotive refinish and OEM coating self-healing polymer market alone is expected to reach USD 1.8 billion by 2030. Aerospace structural self-healing composites are a long-term but very valuable use. They could significantly lower the cost of maintaining aircraft, which is currently estimated to be USD80 billion a year worldwide, by allowing carbon fiber reinforced polymer structures to repair themselves when micro-cracks form. Self-healing substrate and encapsulant polymers that can fix delamination and micro-crack damage caused by repeated mechanical flexing are important technologies for making flexible wearable devices last longer. In laboratory tests, self-healing polysiloxane, polyurethane, and polyimine systems have shown that they can completely restore electrical conductivity after several cutting-and-healing cycles. These tests are now moving on to commercial device integration. Combining self-healing with other useful properties, such as self-healing conductive hydrogels for biointerfacing, self-healing dielectric polymers for capacitive energy storage, and self-healing shape memory polymers, is creating multi-functional material platforms with performance capabilities that no single conventional material class can match.

- Stimuli-Responsive Polymer Systems Enabling Intelligent Material Architectures Across Biomedical and Soft Robotics Applications:

Stimuli-responsive polymers — materials that undergo reversible, controlled, and dramatic changes in physical or chemical properties in response to defined external stimuli including temperature, pH, light, electric or magnetic fields, mechanical stress, or specific chemical species — are transitioning from laboratory curiosities to commercially deployed functional material platforms across drug delivery, tissue engineering, soft robotics, smart textiles, and adaptive optical applications, creating a rapidly growing and high-value demand stream for precision-synthesized responsive polymer systems. Temperature-responsive polymers that change from hydrophilic swollen states to collapsed hydrophobic states at exactly tunable transition temperatures between 25°C and 40°C are becoming more popular in commercial applications like thermally triggered drug release systems, cell culture substrates that allow thermoresponsive cell sheet detachment for tissue engineering, and thermochromic smart window coatings.

Polymers that respond to pH, like polyacrylic acid, poly(methacrylic acid), and chitosan-based systems, are making it possible for oral drug delivery vehicles to stay collapsed at gastric pH but swell and release encapsulated therapeutics at intestinal pH. The market for pH-responsive polymer drug delivery is expected to grow at a rate of 16.8% CAGR through 2030. Photoresponsive polymers that include azobenzene, diarylethene, or spiropyran photoswitchable chromophores can change shape, switch surface wettability, and release drugs when exposed to light. They are used in optogenetics research tools, light-actuated soft robotic grippers, and photoresponsive drug delivery systems for ophthalmic and dermatological purposes. Electroresponsive conductive polymer actuators—made from PEDOT, polyaniline, or polypyrrole, which change volume when they are oxidized or reduced—are being made to work like artificial muscles for soft robotics, prosthetic limb actuation, and the development of minimally invasive surgical tools. The global soft robotics market is expected to grow from USD 1.9 billion in 2024 to USD 6.8 billion by 2030, and a large part of that growth will come from electroresponsive functional polymer actuation systems.

- Polymer Solid Electrolytes Enabling Next-Generation Solid-State Battery Commercialization:

The development of polymer solid electrolytes — ion-conducting polymer matrices capable of replacing the liquid electrolytes used in conventional lithium-ion batteries with solid-state alternatives that eliminate flammability risk, enable higher energy density through lithium metal anode compatibility, and improve long-term cycling stability — represents one of the most consequential applications of polymer functional materials in the energy storage sector, with the commercial trajectory of solid-state battery technology creating a potentially transformative demand vector for specialized ion-conducting polymer materials through the 2026–2035 forecast period. Poly(ethylene oxide) (PEO)-based solid polymer electrolytes have the longest history of development and have only been used commercially in a few niche applications, such as Bolloré’s Blue Solutions lithium-metal polymer batteries for stationary storage and electric vehicles. This shows that polymer electrolyte-based solid-state batteries can work on a large scale. Advanced polymer electrolyte systems are being worked on very hard right now. These include composite polymer electrolytes with ceramic filler particles (LLZO, LATP, LAGP) that improve ionic conductivity toward the 10⁻³ S/cm target needed for practical ambient-temperature operation and stop lithium dendrite growth; single-ion conducting polymer electrolytes that stop concentration polarization effects that limit power density in dual-ion conducting systems; and gel polymer electrolytes that are in between liquid and solid-state systems and offer better safety than liquid electrolytes while still having higher ionic conductivity than fully solid alternatives.

The global solid-state battery market is still in its early commercial stage, but it is expected to grow from USD 0.9 billion in 2024 to USD 8.1 billion by 2030 at a CAGR of 43.7%. Polymer electrolyte variants will compete with oxide ceramic and sulfide-based solid electrolyte alternatives in different application segments based on processing compatibility, mechanical flexibility, and ionic conductivity profiles. It takes about 150 to 250 tons of specialized ion-conducting polymer material to make each gigawatt-hour of solid-state battery using polymer electrolyte architecture. This means that the projected solid-state battery production volumes by 2030 would create tens of thousands of tons of annual polymer electrolyte demand. This is a structurally significant new market for functional polymer producers who can synthesize and process ion-conducting polymers that meet battery-grade purity and electrochemical performance specifications.

Category Wise Insights

By Type

Why Do Conductive Polymers Lead the Polymer Functional Materials Market?

As of 2025, conductive polymers make up the largest type segment, bringing in about 28% of all market revenue. This leadership shows how wide-ranging and commercially mature conductive polymer applications are. They range from organic electronics to electrochemical energy storage, antistatic packaging, electromagnetic interference shielding, electrochromic devices, and biosensors. These applications serve a wide range of end markets, which together create high and growing demand across many industries at the same time. PEDOT:PSS is the most popular commercial conductive polymer. It is made by companies like Heraeus (Clevios product line), Agfa-Gevaert (Orgacon), and several Asian companies. It is used in applications such as capacitor solid electrolytes, antistatic coatings, organic photovoltaics, flexible electrode films, and printed biosensors. The multilayer ceramic capacitor (MLCC) and solid tantalum capacitor markets use a lot of PEDOT:PSS as a solid electrolyte layer. This is one of the most common uses for conductive polymers in electronics, and demand for it is stable and growing as electronics get smaller and MLCCs are used more in consumer electronics, automotive electronics, and industrial control systems.

By Application

Why Do Electronics and Semiconductors Lead Polymer Functional Material Applications?

The largest segment of the market is electronics and semiconductors, which constitute approximately 34% of all sales in 2025. This leadership demonstrates the significance of polymer functional materials to virtually all the layers of the electronic devices stack today. For example, they are used in thin-film transistors and OLEDs as organic semiconductor active layers, in dielectric polymer insulation layers that separate gate electrodes from semiconductor channels, in conductive polymer electrode and interconnect layers, in piezoelectric polymer MEMS transducers, and in encapsulant polymer barriers that keep moisture and oxygen from damaging sensitive electronic structures. Functional polymer materials used in photolithographic processes, such as photoresist polymers, low-dielectric-constant (low-k) interlayer dielectric polymer films, and chemical mechanical planarization polymer slurry components, must meet parts-per-billion metallic contamination specifications and angstrom-level thickness uniformity tolerances. These requirements are the most precise and purest in the semiconductor application compared to other electronics segments.

The market size of the global semiconductor photoresist market including DUV, EUV, and i-line resist polymers is approximately USD 3.8 billion in 2024 and is increasing at the rate of 8.4% annually. The reason is that there is increased production of semiconductor wafers across the globe. Extreme ultraviolet (EUV) photoresist development is needed for sub-7nm node semiconductor patterning and is made by a small number of highly specialized suppliers, such as JSR, TOK, Shin-Etsu Chemical, and Fujifilm. This is the most valuable and technically challenging sub-segment of electronics functional polymers. The price of EUV resist is USD 3,000–8,000 per kilogram, which reflects the extraordinary synthesis, purification, and quality assurance requirements of these mission-critical materials.

By End Use Industry

Why Does Consumer Electronics Lead the End Use Industry Segment?

The highest end-use industry will be consumer electronics, which will constitute approximately 31% of the market revenue in the year 2025. The rationale is that the manufacturing of consumer electronics on a global scale is so extensive, approximately 1.4 billion smartphones, 240 million laptops and 220 million television panels every year, and the functional polymer materials are growing in display, energy storage, sensing and encapsulation functionalities in each device category.

The consumer electronics market is the most influenced by the shift in smartphone and TV display technology to OLED technology. All OLED panels employ the use of OLED organic semiconductor polymer layers, charge transport polymer interlayers and polymer encapsulant barrier films, implying that demand is increasing with the market share of OLED over LCD. The foldable smartphone market is still minuscule with an estimated sale of 15 million units annually. However, each unit uses a lot of expensive polymer functional material, such as folding mechanism hinge encapsulants, self-healing polymer outer coating layers, and flexible polymer substrate films, all of which are made to meet the devices’ extraordinary mechanical durability needs for 200,000+ folding cycles over their lifetimes. The second largest end use is healthcare and life sciences, which comprise approximately 22% of the market revenue. This is increasing at a rate of 17.3% a year, due to the increasing biomedical applications of stimuli-responsive, self-healing, conductive and piezoelectric polymer functional material in drug delivery, diagnostics, implantable devices and tissue engineering.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 9.68 billion |

| Projected Market Size in 2035 | USD 31.42 billion |

| Market Size in 2025 | USD 8.47 billion |

| CAGR Growth Rate | 14.1% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Application, End Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

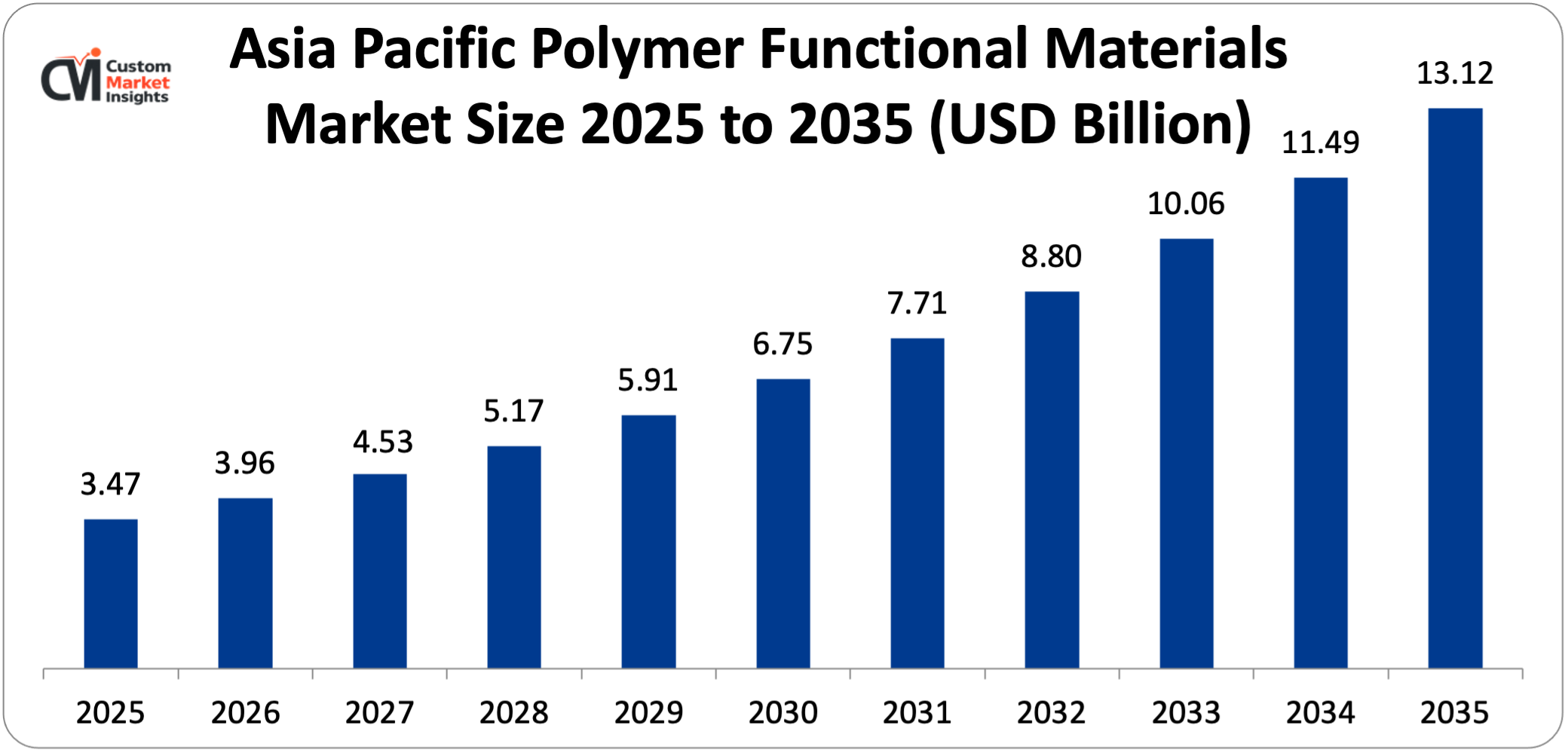

The Asia Pacific polymer functional materials market size is estimated at USD 3.47 billion in 2025 and is projected to reach approximately USD 13.12 billion by 2035, growing at a CAGR of 14.3% from 2026 to 2035.

Why did Asia Pacific Dominate the Market in 2025?

In 2025, Asia Pacific will account for about 41% of global market revenue. This is because the region is the world’s leading manufacturing center for consumer electronics, displays, and semiconductor devices, which are the main end-use applications for polymer functional materials. This is also because China, Japan, South Korea, and Taiwan are all investing heavily in research and development of advanced functional polymer materials. Japan and South Korea have the most advanced polymer functional materials markets in the region.

Japan is home to some of the world’s leading companies in electronic functional polymer materials, such as JSR Corporation, Toray Industries, Shin-Etsu Chemical, Nitto Denko, and Sumitomo Chemical. These companies supply photoresists, optical films, OLED materials, and piezoelectric polymer films to electronics manufacturers around the world from their Japanese production bases. Samsung Electronics and LG Electronics, two of the world’s largest OLED display makers, create a lot of demand for organic semiconductor polymer materials, conductive polymer electrode films, and barrier encapsulant polymers near their display panel manufacturing plants in Cheonan, Paju, and Gumi.

China’s polymer functional materials market is growing the fastest in the Asia Pacific region, at a rate of about 16.1% CAGR. This is because domestic OLED display manufacturing is growing quickly at BOE Technology, Tianma, and Visionox, domestic semiconductor fabrication capacity is increasing, which creates demand for photoresist and low-k dielectric polymers, and the government is investing a lot of money in research on functional materials through national programs like the Made in China 2025 strategy and National Key Research and Development Programs that focus on developing advanced functional polymers for use in energy, electronics, and biomedical applications.

Why is North America the Second-Largest Market with Distinct Application Leadership?

In 2025, North America will account for about 29% of the world’s market revenue, which is about USD 2.46 billion. North America is different from Asia Pacific in that it leads in biomedical and healthcare, aerospace and defense, and advanced energy storage applications, which are the three fastest-growing functional polymer application segments outside of electronics.

The United States has the world’s most active biomedical research ecosystem. The National Institutes of Health (NIH) gives out more than USD47 billion a year, and venture capital firms invest more than USD20 billion a year in biotechnology and medtech. This supports the largest and most productive academic and industrial research community working on stimuli-responsive, self-healing, and conductive polymer functional materials for drug delivery, tissue engineering, and bioelectronic medicine applications.

The U.S. aerospace and defense industry, which includes the Department of Defense’s advanced materials programs, NASA’s materials research, and the large commercial aerospace supply chains of Boeing and Lockheed Martin, is a high-value and technology-leading demand center for shape memory polymer actuators, self-healing structural composites, piezoelectric structural health monitoring sensor arrays, and conductive polymer electromagnetic shielding materials.

Why is Europe a Technologically Advanced and Regulatory-Sophisticated Market?

In 2025, Europe will have about 22% of the world’s market revenue, or about USD 1.86 billion. This is because the specialty chemicals industry, which includes companies like BASF, Covestro, Evonik, Arkema, and Solvay, will continue to be a leader in engineering polymer functional materials. The automotive industry will also be strong, driving applications for self-healing coatings and shape memory polymers. Finally, Europe will have a strong academic research base that will create the foundation for polymer functional materials science.

Germany is the biggest market in Europe. It is home to the headquarters of many major functional polymer suppliers and the engineering and automotive OEM customers who are some of the most technically demanding users of advanced polymer functional materials in the world. The EU is putting a lot of money into organic and flexible electronics through Horizon Europe research programs. It is also working to make the semiconductor material supply chain more independent by targeting domestic development.

As a result, European companies are investing in photoresist polymer and organic semiconductor material capabilities to become less reliant on Japanese suppliers for important electronics functional polymer materials. European strong rules such as REACH to register chemical materials, RoHS to restrict dangerous chemical materials in electronics, and MDR to regulate medical devices influence the functional polymer material supply chain through the requirement of material composition, safety documentation and quality systems, favoring established European specialty chemical suppliers with robust regulatory compliance systems.

Why is the Middle East & Africa Region an Emerging Opportunity?

The LAMEA region will make up about 8% of the global market revenue in 2025, but it will grow at a CAGR of 13.8% from 2026 to 2035. This is due to the fact that Saudi Arabia and the UAE are already investing in the development of new materials research and production because of their intention to diversify their economies. The Brazilian electronics manufacturing and biomedical device production is also on the rise, and South Africa is well-endowed in academic research in polymer chemistry.

The NEOM megacity project and the Vision 2030 industrial development projects in Saudi Arabia have components that target the manufacture of advanced materials. King Abdullah University of Science and Technology (KAUST) has internationally recognized research programs in polymer and materials science that are creating intellectual property and startup activity in functional polymer materials. Israel is a small market in terms of land area.

Top Players in the Market and Their Offerings

- Heraeus Holding GmbH

- Solvay S.A.

- Arkema S.A.

- BASF SE

- Covestro AG

- Evonik Industries AG

- Toray Industries Inc.

- DuPont de Nemours Inc.

- Huntsman Corporation

- 3M Company

- Others

Key Developments

The market has undergone significant developments as industry participants seek to expand capabilities and enhance product portfolios.

- In February 2025: Heraeus announced the commercial launch of its next-generation Clevios HY PEDOT:PSS formulation series specifically designed for high-conductivity flexible electrode applications in wearable biosensors and organic thermoelectric generators. This series achieves electrical conductivity greater than 3,800 S/cm while maintaining stretchability to 30% strain, solving the problem of high conductivity and mechanical deformability that have limited the use of PEDOT:PSS in stretchable electronics applications that need both properties at the same time.

- In March 2026: Arkema announced a dedicated expansion of its Kynar PVDF-TrFE piezoelectric copolymer production capacity in its China facility, citing surging demand from wearable energy harvesting, ultrasonic transducer, and flexible tactile sensor applications within the consumer electronics, medical device, and industrial IoT sectors, with the expanded capacity targeting pharmaceutical-equivalent purity grades required by implantable medical device applications consuming piezoelectric polymer films for active bone stimulation and cochlear implant transducer components.

These strategic moves have helped companies improve their market positions, grow their specialized functional polymer product lines, create next-generation material platforms that meet the needs of new applications in flexible electronics, solid-state energy storage, biomedical engineering, and autonomous self-healing material systems, and take advantage of the structural demand growth that is happening because of the convergence of digital transformation, energy transition, and healthcare innovation megatrends that are making polymer functional materials enabling technologies in the most dynamic sectors of the global economy.

The Polymer Functional Materials Market is segmented as follows:

By Type

- Conductive Polymers

- PEDOT & PEDOT: PSS

- Polyaniline (PANI)

- Polypyrrole (PPy)

- Polythiophene & Derivatives

- Piezoelectric Polymers

- PVDF & Copolymers (PVDF-TrFE)

- Polyamide-Based Piezoelectrics

- Biopolymer Piezoelectrics

- Shape Memory Polymers

- Thermally Activated SMP

- Light-Activated SMP

- Magnetically Activated SMP

- Self-Healing Polymers

- Extrinsic Self-Healing (Microcapsule-Based)

- Intrinsic Self-Healing (Dynamic Bond-Based)

- Stimuli-Responsive Polymers

- Thermoresponsive Polymers

- pH-Responsive Polymers

- Photoresponsive Polymers

- Electroresponsive Polymers

- Barrier Polymers

- High-Barrier Films & Coatings

- Ion-Exchange Membranes

- Gas Separation Membranes

- Other Types

By Application

- Electronics & Semiconductors

- Organic Semiconductors & OLEDs

- Flexible & Printed Electronics

- Dielectric & Encapsulant Layers

- Antistatic & EMI Shielding

- Energy Storage & Harvesting

- Polymer Solid Electrolytes

- Piezoelectric Energy Harvesters

- Organic Photovoltaics

- Supercapacitor Electrodes

- Biomedical & Healthcare

- Drug Delivery Systems

- Tissue Engineering Scaffolds

- Biosensors & Diagnostics

- Medical Implants & Coatings

- Automotive & Transportation

- Aerospace & Defense

- Packaging

- Other Applications

By End Use Industry

- Consumer Electronics

- Automotive

- Healthcare & Life Sciences

- Energy & Power

- Aerospace & Defense

- Other End Use Industries

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Polymer Functional Materials by Segments

- 2.1.2. Polymer Functional Materials by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Polymer Functional Materials Market Attractiveness Analysis, By Type

- 2.2.3. Polymer Functional Materials Market Attractiveness Analysis, By Application

- 2.2.4. Polymer Functional Materials Market Attractiveness Analysis, By End Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Flexible and Wearable Electronics Revolution Driving Transformative Demand for Mechanically Adaptive Functional Polymers

- 3.1.2. Organic Electronics and Printed Electronics Platforms Creating High-Volume Polymer Semiconductor Demand

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Polymer Functional Materials Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Polymer Functional Materials Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Conductive Polymers

- 4.1.2.1. PEDOT & PEDOT PSS

- 4.1.2.2. Polyaniline (PANI)

- 4.1.2.3. Polypyrrole (PPy)

- 4.1.2.4. Polythiophene & Derivatives

- 4.1.3. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Piezoelectric Polymers

- 4.1.6.1. PVDF & Copolymers (PVDF-TrFE)

- 4.1.6.2. Polyamide-Based Piezoelectrics

- 4.1.6.3. Biopolymer Piezoelectrics

- 4.1.7. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Shape Memory Polymers

- 4.1.10.1. Thermally Activated SMP

- 4.1.10.2. Light-Activated SMP

- 4.1.10.3. Magnetically Activated SMP

- 4.1.11. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Self-Healing Polymers

- 4.1.14.1. Extrinsic Self-Healing (Microcapsule-Based)

- 4.1.14.2. Intrinsic Self-Healing (Dynamic Bond-Based)

- 4.1.15. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Stimuli-Responsive Polymers

- 4.1.18.1. Thermoresponsive Polymers

- 4.1.18.2. pH-Responsive Polymers

- 4.1.18.3. Photoresponsive Polymers

- 4.1.18.4. Electroresponsive Polymers

- 4.1.19. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Barrier Polymers

- 4.1.22.1. High-Barrier Films & Coatings

- 4.1.22.2. Ion-Exchange Membranes

- 4.1.22.3. Gas Separation Membranes

- 4.1.23. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1.26. Other Types

- 4.1.27. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 4.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.29. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Polymer Functional Materials Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Polymer Functional Materials Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Electronics & Semiconductors

- 5.1.2.1. Organic Semiconductors & OLEDs

- 5.1.2.2. Flexible & Printed Electronics

- 5.1.2.3. Dielectric & Encapsulant Layers

- 5.1.2.4. Antistatic & EMI Shielding

- 5.1.3. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Energy Storage & Harvesting

- 5.1.6.1. Polymer Solid Electrolytes

- 5.1.6.2. Piezoelectric Energy Harvesters

- 5.1.6.3. Organic Photovoltaics

- 5.1.6.4. Supercapacitor Electrodes

- 5.1.7. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Biomedical & Healthcare

- 5.1.10.1. Drug Delivery Systems

- 5.1.10.2. Tissue Engineering Scaffolds

- 5.1.10.3. Biosensors & Diagnostics

- 5.1.10.4. Medical Implants & Coatings

- 5.1.11. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Automotive & Transportation

- 5.1.15. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Aerospace & Defense

- 5.1.19. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Packaging

- 5.1.23. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1.26. Other Applications

- 5.1.27. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 5.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.29. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Polymer Functional Materials Market – By End Use Industry

- 6.1. End Use Industry Market Overview, By End Use Industry Segment

- 6.1.1. Polymer Functional Materials Market Revenue Share, By End Use Industry, 2025 & 2035

- 6.1.2. Consumer Electronics

- 6.1.3. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Automotive

- 6.1.7. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Healthcare & Life Sciences

- 6.1.11. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Energy & Power

- 6.1.15. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Aerospace & Defense

- 6.1.19. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Other End Use Industries

- 6.1.23. Polymer Functional Materials Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End Use Industry Market Overview, By End Use Industry Segment

- Chapter 7. Polymer Functional Materials Market – Regional Analysis

- 7.1. Polymer Functional Materials Market Overview, By Region Segment

- 7.1.1. Global Polymer Functional Materials Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Polymer Functional Materials Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Polymer Functional Materials Market Revenue, By Type, 2026 – 2035

- 7.1.4. Global Polymer Functional Materials Market Revenue, By Application, 2026 – 2035

- 7.1.5. Global Polymer Functional Materials Market Revenue, By End Use Industry, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Polymer Functional Materials Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Polymer Functional Materials Market Revenue, By Type, 2026 – 2035

- 7.2.3. North America Polymer Functional Materials Market Revenue, By Application, 2026 – 2035

- 7.2.4. North America Polymer Functional Materials Market Revenue, By End Use Industry, 2026 – 2035

- 7.2.5. U.S. Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Polymer Functional Materials Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Polymer Functional Materials Market Revenue, By Type, 2026 – 2035

- 7.3.3. Europe Polymer Functional Materials Market Revenue, By Application, 2026 – 2035

- 7.3.4. Europe Polymer Functional Materials Market Revenue, By End Use Industry, 2026 – 2035

- 7.3.5. Germany Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Polymer Functional Materials Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Polymer Functional Materials Market Revenue, By Type, 2026 – 2035

- 7.4.3. Asia Pacific Polymer Functional Materials Market Revenue, By Application, 2026 – 2035

- 7.4.4. Asia Pacific Polymer Functional Materials Market Revenue, By End Use Industry, 2026 – 2035

- 7.4.5. China Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Polymer Functional Materials Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Polymer Functional Materials Market Revenue, By Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Polymer Functional Materials Market Revenue, By Application, 2026 – 2035

- 7.5.4. The Middle-East and Africa Polymer Functional Materials Market Revenue, By End Use Industry, 2026 – 2035

- 7.5.5. Saudi Arabia Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Polymer Functional Materials Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Polymer Functional Materials Market Revenue, By Type, 2026 – 2035

- 7.6.3. Latin America Polymer Functional Materials Market Revenue, By Application, 2026 – 2035

- 7.6.4. Latin America Polymer Functional Materials Market Revenue, By End Use Industry, 2026 – 2035

- 7.6.5. Brazil Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Polymer Functional Materials Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Polymer Functional Materials Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Polymer Functional Materials Market: Company Market Share, 2025

- 8.2. Global Polymer Functional Materials Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. Heraeus Holding GmbH

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Solvay S.A.

- 9.3. Arkema S.A.

- 9.4. BASF SE

- 9.5. Covestro AG

- 9.6. Evonik Industries AG

- 9.7. Toray Industries Inc.

- 9.8. DuPont de Nemours Inc.

- 9.9. Huntsman Corporation

- 9.10. 3M Company

- 9.11. Others.

- 9.1. Heraeus Holding GmbH

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Healthcare Foresights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

- Chapter 12. List Of Figures

- 12.1. Figures No 1 to 67

- Chapter 13. List Of Tables

- 13.1. Tables No 1 to 46

Prominent Player

- Heraeus Holding GmbH

- Solvay S.A.

- Arkema S.A.

- BASF SE

- Covestro AG

- Evonik Industries AG

- Toray Industries Inc.

- DuPont de Nemours Inc.

- Huntsman Corporation

- 3M Company

- Others

FAQs

The key players in the market are Heraeus Holding GmbH, Solvay S.A., Arkema S.A., BASF SE, Covestro AG, Evonik Industries AG, Toray Industries Inc., DuPont de Nemours Inc., Huntsman Corporation, 3M Company, Others.

Government policy influences the polymer functional materials market through three distinct mechanisms: research funding that develops the foundational materials science from which commercial applications emerge — with NIH, NSF, DARPA, Horizon Europe, and equivalent Asian national research programs collectively investing billions of dollars annually in functional polymer research across biomedical, energy, and electronics application domains; regulatory frameworks governing end-use applications that set the safety, efficacy, and performance standards that functional polymer materials must meet — FDA medical device regulations for biomedical polymer applications, semiconductor industry voluntary standards for electronic polymer materials, and aviation authority airworthiness requirements for aerospace functional composites all defining the certification pathway that commercial functional polymer materials must navigate; and strategic industrial policies targeting domestic advanced materials capability development — China’s new materials national programs, the U.S. The CHIPS Act’s provisions for domestic semiconductor materials, the EU’s Strategic Technologies for Europe Platform (STEP), and Japan’s economic security legislation aimed at semiconductor and functional materials supply chain resilience are all changing where functional polymer is made and used by encouraging major economies to develop their own capabilities at the same time.

Polymer functional materials have the most price variation of any polymer market segment. This is because the type and application spectrum has a wide range of synthesis complexity, application criticality, and production scale. EUV photoresist polymers for leading-edge semiconductor patterning cost between USD3,000 and USD8,000 per kilogram, which is one of the highest prices for any commercial polymer material. This is because this application requires very precise synthesis, high purity, and limited access to qualified suppliers. Depending on the conductivity specification and application grade, PVDF-TrFE piezoelectric copolymers for medical device applications cost between USD 200 and 600 per kilogram, self-healing polyurethane clearcoat formulations cost between USD 40 and 120 per kilogram, and PEDOT:PSS conductive polymer dispersions cost between USD 80 and 400 per kilogram. Functional polymer grades that are close to commodities, like antistatic polyamide compounds and standard barrier polymer films, cost between USD 5 and 15 per kilogram. The blended average revenue per kilogram across all polymer functional material types and applications is about 4.2 times the price of regular structural polymers. This is because most of the market revenue comes from high-specification, precision-synthesized grades that are used in electronics, biomedical, and energy applications. In these markets, functional performance is the main reason people buy, and price sensitivity is much lower than in commodity polymer markets.

The market is expected to be worth about USD 31.42 billion by 2035, with a compound annual growth rate (CAGR) of 14.1% from 2026 to 2035. This is due to the commercial use of solid-state battery polymer electrolytes in cars and consumer electronics, the widespread use of self-healing polymer coatings and composites in cars, planes, and flexible electronics, the shift of organic and printed electronics from niche to mainstream manufacturing platforms, the use of stimuli-responsive polymers in drug delivery and tissue engineering, and the growth of functional polymer demand in India, Southeast Asia, and LAMEA as the electronics manufacturing, pharmaceutical, and advanced materials industries grow.

Asia Pacific is expected to keep the biggest share of revenue throughout the forecast period, rising from 41% in 2025 to about 44% by 2035. This is because the region is still home to most of the world’s consumer electronics, display panel, and semiconductor manufacturing. North America will continue to lead in biomedical, aerospace, and energy storage functional polymer applications, which are the highest-value and fastest-growing end-use segments. This will keep North America’s revenue per unit of polymer functional material volume high, which partially makes up for its lower absolute volume share compared to Asia Pacific’s manufacturing-heavy demand base.

From 2026 to 2035, Asia Pacific is expected to grow the fastest overall, with a CAGR of 14.3%. This is because China’s rapidly growing OLED display manufacturing is creating demand for organic semiconductors and conductive polymers, South Korea’s Samsung and LG display investments are keeping the world’s highest-concentration polymer functional material consumption in display applications, Japan is the world’s leader in photoresist and electronic functional polymer supply, and India’s growing electronics manufacturing and pharmaceutical sectors are creating new demand centers for functional polymer materials in electronics and biomedical applications, respectively.

The Global Polymer Functional Materials Market is predicted to experience substantial growth driven by the global flexible electronics market projected to reach USD 87.6 billion by 2030 at a 15.8% CAGR creating transformative demand for mechanically adaptive conductive and semiconducting polymer functional materials; solid-state battery market growth at a 43.7% CAGR from 2024 to 2030 creating substantial new polymer electrolyte demand; the printed electronics market, projected to reach USD 43.6 billion by 2032 driving conductive and semiconducting polymer ink demand; self-healing polymer commercialization across automotive coatings, aerospace composites, and flexible electronics growing at the fastest type CAGR of 19.4%; stimuli-responsive polymer drug delivery systems growing at a 16.8% CAGR as precision medicine drives therapeutic payload delivery sophistication; and neuromorphic computing hardware development positioning conductive polymer memristive devices in a market projected to reach USD 6.5 billion by 2030.