Networked Polymers Market Size, Trends and Insights By Type (Thermosetting Networked Polymers, Epoxy Resins, Phenolic Resins, Polyester Resins, Polyurethane, Vinyl Ester Resins, Cyanate Esters, Others, Thermoplastic Networked Polymers, Polyethylene (PE), Polypropylene (PP), Polyamide (PA), Polyether Ether Ketone (PEEK), Acrylonitrile Butadiene Styrene (ABS), Others, Elastomeric Networked Polymers, Silicone Rubber, Polyurethane Elastomers, Others), By Application (Automotive & Transportation, Aerospace & Defense, Electrical & Electronics, Construction, Healthcare & Medical, Coatings, Adhesives & Sealants, Others), By End-Use (Manufacturing, Consumer Goods, Industrial, Others), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 5.8%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- BASF SE

- DuPont de Nemours Inc.

- Dow Inc.

- Evonik Industries AG

- Others

Reports Description

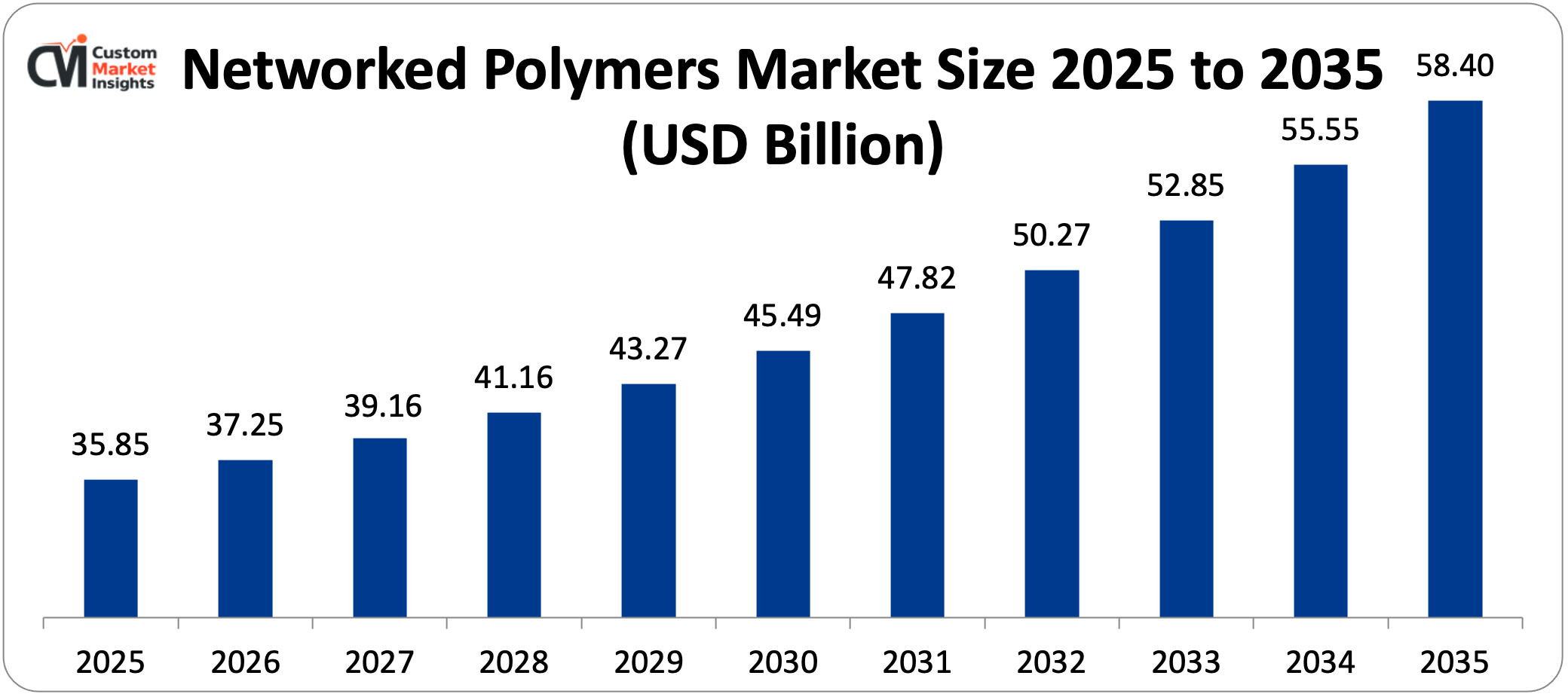

The global networked polymers market is expected to grow at a rate of 5.8% per year from 2026 to 2035, going from USD 37.25 billion in 2026 to about USD 58.40 billion by 2035. The market size is expected to be USD 35.85 billion in 2025.

The market is growing because of the rising demand for lightweight, high-performance materials in the automotive, aerospace, and electronics industries the faster adoption of electric vehicles that need advanced polymer parts the rapid growth of construction and infrastructure investment around the world; and the growing focus on developing bio-based and sustainable polymers.

Market Highlight

- The Asia Pacific region had the largest share of the networked polymers market in 2025, with 38% of the total. This was due to large-scale production in China, Japan, South Korea, and India.

- Between 2026 and 2035, North America is expected to have a steady CAGR of 5.5%, thanks to strong research and development activity and strong demand from the defense and aerospace sectors.

- By type, the thermosetting networked polymers segment made up about 57% of the total market share in 2025. This shows that it is mostly used in high-performance industrial and structural applications.

- The automotive and transportation segment had the biggest share of the market in 2025, with about 31% of it.

- The electrical and electronics segment will have the highest growth rate of 7.4% between 2026 and 2035. The reason is that an increased demand exists in 5G infrastructure, flexible electronics, and semiconductor packaging.

Significant Growth Factors

The Networked Polymers Market Trends present significant growth opportunities due to several factors:

- Rising Demand for Lightweight, High-Strength Materials in Automotive and Aerospace Industries: There are three primary causes of the high demand of networked polymers: (1) Rising Demand in Lightweight, High-Strength Materials in Automotive and Aerospace Industries: The largest causes of the high demand of networked polymers are the global requirement to make cars and planes lighter and more fuel-efficient and the structural requirements of the next-generation aircraft. Networked polymers are of great significance in the automotive industry in the production of strong and light parts. This assists cars to consume less fuel and pollute less. The shift to electric cars makes the demand for these materials even greater as they assist in reducing the weight of the car and enhance the performance of the battery. The electric car market in the world sold over 17 million vehicles in 2023. By 2030, it is expected to sell more than 40 million units a year. The amount of high-performance polymer required in each EV platform is significantly more than the amount required in a typical internal combustion engine vehicle in the form of battery housing, thermal management, high-voltage wiring insulation, and structural lightweighting. The lightweight materials market in the world is projected to be USD 250 billion in the coming years. The primary drivers will be the automotive and aerospace sectors and the networked polymers will constitute a large proportion of the value added value. The National Highway Traffic Safety Administration (NHTSA) reported that lightweight vehicles are able to achieve up to 20% of better gas mileage. This shows how important it is to use advanced polymers in vehicle design. In the aerospace industry, networked polymer composites are highly significant in the production of aircraft structures of the next generations. The thermosetting polymers are extremely significant in the aerospace industry since they produce strong yet lightweight parts such as aircraft wings and fuselages. This is because they possess high thermal resistance and mechanical properties that ensure that they can withstand the adverse conditions that are present in aerospace environments. The number of commercial aircraft in the world is projected to increase nearly by twofold within the next 20 years. The content of composite and advanced polymer, by structural weight, will be 50-55% in each new-generation aircraft, a massive increase over the 15-20% that older aircraft generations typically contain. The shift in the utilization of the materials will result in long term demand for the high-performance networked polymer systems over the forecast period.

- Expanding Electronics Applications and the 5G Technology Rollout: The growth of the networked polymers market can be attributed to the electronics industry and its increased use of these materials, as well as the implementation of 5G technology. The electronic devices that are altering rapidly include smartphones, tablets, and wearables, just to mention a few. Such devices require highly strong, flexible, and high-temperature-resistant materials. All these requirements are fulfilled by networked polymers, which provide modern electronics with the required performance. The world market of electronics was estimated at USD 3.1 trillion in 2024. Other significant sub-sectors that used networked polymers at large scale were semiconductor packaging, printed circuit board (PCB) laminates, connectors, and encapsulants. The global deployment of 5G telecommunications infrastructure is in high demand. In the year 2026, the number of 5G base stations in the world will exceed 3 million. All of them will require high-frequency circuit board laminates, antenna radome structures, and connector housings fabricated of the most sophisticated thermoset and thermoplastic networked polymer systems with high dielectric and dimensional stability. The electrical and electronics applications segment constituted 36.42% of the market share of high-performance polymers in 2025. This indicates the importance of the material to flexible printed circuits and semiconductor packaging. The revenues are continuously increasing with the addition of interconnect layers to the chiplet architectures. Foldable displays, wearable sensors, and rollable OLED panels are all examples of flexible electronics. These devices require networked polymer films that can withstand long periods without losing their electrical insulation, mechanical flexibility or chemical stability. This generates a high-demand market which is increasing at a rate of more than 10% CAGR till the end of the forecast period.

What are the Major Advances Changing the Networked Polymers Market Today?

- Bio-Based and Sustainable Networked Polymer Development: Bio-Based and Sustainable Networked Polymer Development: This developing trend of switching to materials that are more environmentally friendly is transforming the networked polymers industry in a significant way. Innovation in the networked polymers market is directed at such aspects as enhanced crosslinking strategies to enhance the mechanical properties, development of bio-based and sustainable networked polymers, and the development of materials with functionalities, such as self-healing capabilities and responsiveness to external stimuli. The development of bio-based and recyclable products is being compelled by tough environmental regulations. Both the U.S. and the European Union have chemical plans to preserve the environment. The clean manufacturing provisions of the Inflation Reduction Act and the dual carbon targets of China are both accelerating the shift to bio-derived polymer feedstocks, recyclable thermoset systems, and closed-loop polymer recovery systems. Plant-based epoxy resin made of bio-based lignin-based phenolic resin, furan-based thermoset, and bio-based epoxy resin is going through the commercial development process very fast. There are formulations where the bio-content percentages of commercial products may reach up to 30–70%. To meet global sustainability goals, companies in the industry are focusing on bio-based thermosetting polymers. At the same time, improvements in recycling technologies could help with environmental issues and make these polymers more widely used. Vitrimer chemistry is a new type of networked polymer that combines the permanence of thermosets with the reprocessability of thermoplastics through dynamic covalent bond exchange. It is one of the most promising areas of research, and several academic-industry partnerships are working to make vitrimer-based structural composites commercially viable. These materials could solve the long-standing problem of conventional thermosets not being recyclable. This could open up a lot of new market opportunities as circular economy requirements become law.

- Self-Healing Polymers and Smart Material Integration: The development of networked polymer systems that are self-healing, shape-memory, and stimulus-reactive is creating entirely new applications. Self-healing polymer networks capable of repairing microcracks and damage on surfaces independently are leaving the laboratory and finding applications in automotive finishes, aerospace structural composites, and electronic encapsulants, where field repair is too costly or impossible. By 2030, the smart polymer market in the world is projected to increase significantly. Physical stimulus-responsive polymer systems will be the most common type of smart polymer used in biomedical, automotive, and electronics applications. The smart polymers market is somewhat fragmented, with the biggest companies focusing on adopting new technologies and entering new markets to get an edge over their competitors. Notable R&D partnerships are also helping to develop materials for specific uses. Shape-memory networked polymers are becoming more popular in medical devices, deployable aerospace structures, and soft robotics. These polymers return to a pre-programmed shape when they come into contact with a trigger stimulus like heat, light, or moisture. Combining nanotechnology with polymer networks is making it possible to create single material systems with never-before-seen combinations of mechanical, electrical, thermal, and functional properties. For example, carbon nanotube-reinforced epoxies and graphene-functionalized polyurethanes have performance characteristics that can’t be achieved with traditional polymer formulation.

- Continuous and Additive Manufacturing Technologies: The new manufacturing technologies are transforming the processes of manufacturing networked polymer applications and the freedom of designers to produce new products. Additive manufacturing, which includes stereolithography, digital light processing, and continuous liquid interface production, makes it possible to make complicated three-dimensional networked polymer structures with internal architectures that can’t be made with traditional molding or casting. The additive manufacturing market in the world is projected to reach over 40 billion dollars by the year 2030. The largest material segment will be photopolymer resins and polymer composites. As more and more smart and automated technologies are used in manufacturing, networked polymers become more efficient. This makes them more appealing to businesses that want to cut costs and make their operations run more smoothly. Resin transfer molding, resin infusion, and automated fiber placement processes—all of which work well with thermoset networked polymer systems—are making it possible to make large aerospace and automotive composite structures at production levels that were only possible with metal parts before. The creation of out-of-autoclave curing systems is lowering the capital and energy costs of making high-performance thermoset composites. This makes high-quality networked polymer materials more accessible for mid-tier industrial uses.

- Growing Construction Sector Driving Thermoset Resin Demand: The growing construction sector is driving up the demand for thermoset resins. As construction activity and investment grow in emerging economies, the need for attractive and long-lasting paints and coatings is also growing. This is expected to increase the demand for thermoset resins. Thermosets are the first choice for manufacturers because they have better properties than thermoplastics, metals, and other materials. The polymer cross-linking lets them work at high temperatures, which makes them useful in many growing end-user sectors, such as aerospace, construction, and chemicals. Between 2023 and 2040, global infrastructure investment is expected to exceed USD 94 trillion. This is because developing economies in Asia, Africa, and Latin America are carrying out huge urbanization programs that are driving up demand for high-performance construction materials. Modern infrastructure construction relies heavily on networked polymer systems. These include epoxy coatings that protect steel structures from corrosion, polyurethane waterproofing membranes, fiber-reinforced polymer (FRP) rebar that replaces traditional steel reinforcement, and phenolic foam insulation systems. Green building standards are encouraging the use of eco-friendly thermosets. At the same time, strict rules are pushing for new materials that are safe for people and the environment. This is because renewable energy systems are becoming more popular. The growth of renewable energy around the world needs a lot of glass fiber-reinforced epoxy composite materials for wind turbine blades and structural mounting systems. For example, one offshore wind turbine blade can hold up to 15–20 metric tons of thermoset composite material.

Category Wise Insights

By Type

Why Do Thermosetting Networked Polymers Dominate the Market?

The thermosetting segment is the biggest contributor to revenue, with epoxy resins generating nearly USD 13.85 billion in 2024 and projected to reach USD 24.5 billion in 2032 at a CAGR of 7.25. This is due to the fact that they are highly adhesive and mechanical and chemical and can be used in bonding and coating as well as in composite matrices. The most famous resins on the market are epoxy, phenolic, and polyurethane resins since they are superior in property and can be employed in many manners. Other newer types of thermosetting polymers such as polyester, melamine, and silicone are also gaining popularity.

Phenolic resin has a big market share due to its extreme resistance to fire, minimal smoke generation, and stability in high temperatures. This qualifies them as the most suitable for aerospace interior panels, brake friction materials, and electrical insulation parts that have to comply with the stringent fire safety requirements. Thermosets of polyurethane are utilized in many different applications, such as automotive seats and dashboards, rigid building insulation, and protective coating. They are appreciated due to the power of impact, elasticity, and foaming. The thermosetting sector is well-established in that it possesses much of the manufacturing infrastructure, is familiar with processing procedures, and has decades of operating experience with regulated end-use applications. This renders competitors difficult to move to this segment.

Approximately 35% of the market is constituted of thermoplastic networked polymers. They are becoming more popular in situations where recyclability, ease of reprocessing, and design flexibility are important. Polymers of thermoplasts are meltable and can be reshaped numerous times without significant loss of most of their functional properties. This renders them quite ideal in automotive, consumer-based goods, and packaging materials that must be easy to recycle and handle. The increasing interest in producing products that are good to the environment and can be recycled is also leading to an increase in the demand for thermoplastic polymers. Tough applications that traditionally belonged to thermosets are increasingly being done in high-performance engineering thermoplastics such as PEEK, polyamides, and polyphenylene sulfide. This has been attributed to continuous enhancement of processing machinery and reinforcement technology. The last 8% of the market is made by elastomeric networked polymers. They find application in automobiles, industry, and consumer goods to seal, damp, and make parts pliable.

By Application

Why Does Automotive & Transportation Lead the Application Segment?

In 2025, the automotive and transportation segment will experience the highest number of applications with approximately 31% of the total networked polymers market. This indicates the value of the material in designing and manufacturing modern cars. Thermosetting polymers are very important in the automotive and aerospace industries because they help lower weight and increase fuel efficiency. These polymers are applied in the automotive industry in components such as bumpers, internal components, and engine components. Their strength-to-weight ratio assists in enhancing performance and conserving energy. A typical passenger car in the modern world has over 150 kg of polymer materials. Many of them consist of networked polymer systems, including epoxy composite body parts, polyurethane foam seating, NVH parts, phenolic friction materials, and engineering thermoplastic under-hood parts.

The fast transition to battery electric vehicles is structurally increasing the quantity of networked polymer per vehicle platform. To illustrate, EV battery enclosures, high-voltage cable insulation and connectors, thermal management system components, reinforced composite floor pans, etc. require special networked polymer systems, which are electrically insulated, thermally stable, flame resistant, and structurally robust. Such requirements demand material solutions of high quality and technical level.

The electrical and electronics industry has the highest projected growth rate of 7.4% between the years 2026 and 2035. This is due to the increasing demand for semiconductor packages, PCBs, 5G infrastructure development, and flexible electronics. Thermosetting polymers are ideal in circuit boards, connectors, and housings due to their superb insulation and ability to remain steady when exposed to high temperatures. The second largest segment in terms of revenue is the construction application segment due to massive infrastructure projects in Asia, the Middle East, and North America. The most valuable use per kilogram is aerospace and defense. Aerospace-grade thermoset composites as well as high-performance engineering thermoplastics are much more expensive than industrial grade due to the requirement of meeting strict qualification and certification requirements.

By End-Use

Why Does Manufacturing Lead the End-Use Segment?

The manufacturing end-use segment has the biggest share of the networked polymers market. This shows how important polymer-heavy fabrication is in making cars, electronics, aerospace parts, and industrial equipment. End users in manufacturing want consistent quality, reliable supply, technical application support, and long-term supply agreements. These are all things that established large-scale producers who can meet global supply chain needs are good at. The consumer goods sector is growing quickly because more and more appliances, sports gear, personal electronics, and packaging applications are using polymers. The industrial end-use segment includes chemical processing equipment, oil and gas infrastructure, power generation, and heavy machinery. These are all areas where thermoset networked polymer systems work well because they need to be able to handle high temperatures and chemicals.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 37.25 billion |

| Projected Market Size in 2035 | USD 58.40 billion |

| Market Size in 2025 | USD 35.85 billion |

| CAGR Growth Rate | 5.8% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Application, End-Use and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Networked Polymers Market?

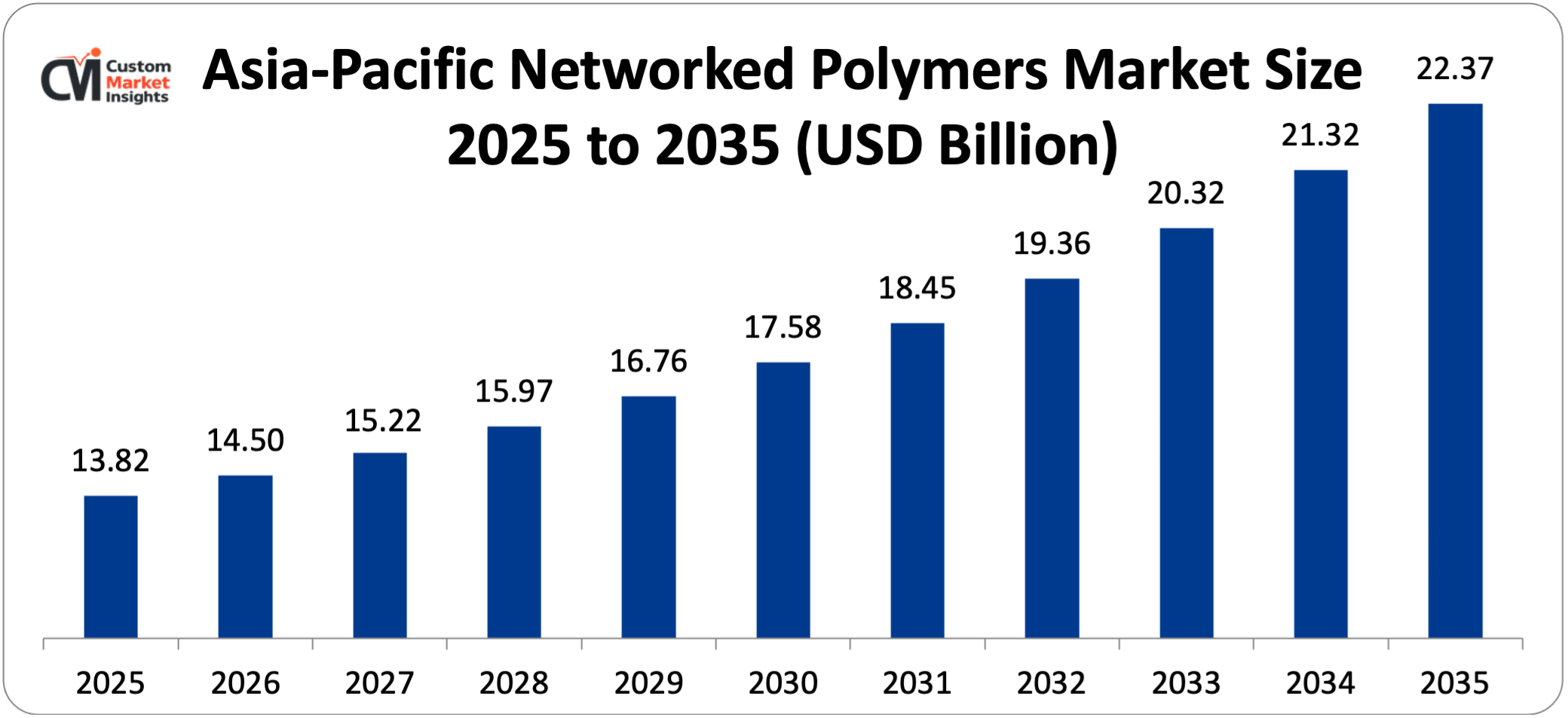

The Asia Pacific networked polymers market size is estimated at USD 13.82 billion in 2025 and is projected to reach approximately USD 22.37 billion by 2035, expanding at a CAGR of 6.2% from 2026 to 2035 — the fastest among all regions globally.

Why does Asia Pacific Dominate the Networked Polymers Market in 2025?

Asia Pacific will occupy approximately 38% of the world market in 2025. This is due to the fact that China is the largest producer and consumer of polymer materials in the globe, Japan and South Korea have developed electronic and automobile manufacturing industries, and India has an industrial and construction base that is rapidly expanding. Asia Pacific is expected to be the leader in the networked polymers market because of its fast industrialization, urbanization, and strong growth in important end-user industries like automotive, electronics, and construction.

China is the largest automotive market in the world, with a sale of over 30 million vehicles annually. It also possesses a massive electronics production base that produces a majority of consumer electronics, semiconductors, and display panels in the world. The infrastructure of the polymer industry in China comprises vertically integrated complexes of production in petrochemical clusters in the provinces of Zhejiang, Guangdong, and Shandong. These complexes contribute to low feedstock prices and manufacturing on a large scale.

What is the Size of the China Networked Polymers Market?

The market size of China’s networked polymers is estimated at USD 6.50 billion in 2025 and USD 10.90 billion years later (2035) with a CAGR of 5.6% increasing between 2026 and 2035.

China Networked Polymers Market Trends

China’s networked polymer market is changing because of government policies that support the development of advanced materials in the country, the rapid growth of its electric vehicle (EV) manufacturing industry (which produced over 9 million EVs in 2023, or nearly 60% of the world’s total EV production), and huge investments in 5G infrastructure that are driving up demand for high-performance electronic-grade polymer systems.

With a lot of government money going into polymer research and development and manufacturing technology, domestic polymer producers are slowly moving from making cheap thermoplastics to making more valuable engineering and specialty polymers. China’s stricter VOC emission standards and chemical safety rules are making it more expensive for businesses to follow the rules and encouraging the development of new low-emission, eco-friendly polymer formulations.

How Big is the North America Networked Polymers Market?

The North America networked polymers market is expected to be worth about USD 9.31 billion in 2025 and grow to USD 15.24 billion by 2035, with a compound annual growth rate (CAGR) of 5.5% from 2026 to 2035.

Why does North America Maintain a Significant Position in the Networked Polymers Market?

North America had the biggest share of the market for specialty networked polymers in 2025, accounting for more than 40% of global sales. This was due to a strong base of end-users in advanced manufacturing, aerospace, and electronics. The region benefits from having top polymer companies like BASF, Dow, DuPont, Eastman Chemical, and Celanese in the area. These companies serve both domestic and export markets in North America.

The U.S. aerospace and defense industry is one of the world’s biggest users of high-performance thermoset composite materials. It keeps up a steady demand for aerospace-grade epoxy, cyanate ester, and bismalimide resin systems. The U.S. Department of Defense’s growing use of advanced polymer composites in next-generation fighter jets, naval ships, and military ground vehicles continues to support the development of high-value applications.

What is the Size of the U.S. Networked Polymers Market?

The U.S. market for networked polymers is expected to grow at a rate of 5.4% per year from 2026 to 2035, reaching a size of about USD 7.41 billion in 2025 and almost USD 12.13 billion in 2035.

U.S. Networked Polymers Market Trends

In the U.S. market, there is a lot of sophisticated end-user demand in the aerospace, automotive, and electronics sectors. High-performance composites and electronic-grade specialty polymers are two examples of premium application segments that charge prices that are much higher than average. The CHIPS and Science Act’s $52.7 billion investment in domestic semiconductor manufacturing is expected to create more demand for high-purity electronic-grade polymer encapsulants, underfills, and substrate materials as new U.S. fabs reach full production during the forecast period. After COVID-19 disruptions, supply chain resilience became a top priority. This led to investments in domestic polymer manufacturing capacity, with several large chemical companies announcing plans to expand their capacity in the U.S. Chemical complex on the Gulf Coast.

Why is Europe Entering a New Era of Networked Polymer Market Growth?

The European networked polymers market will be worth about USD 7.53 billion in 2025, which is about 21% of the global market share. This is thanks to Germany’s world-class chemical and automotive industries, France’s and the UK’s advanced aerospace manufacturing sectors, and a focus on sustainable material innovation across the region. North America and the Asia Pacific are the main regions for thermosetting and thermoplastics, with China being the biggest buyer. Arkema, DuPont, SABIC, and other top companies shape the competitive landscape.

Europe has some of the strictest rules in the world when it comes to chemicals, thanks to REACH, the Green Deal, and the EU Chemicals Strategy for Sustainability. This means that polymer manufacturers who do business in or supply the European market must show that they fully comply with environmental regulations, safety documentation, and, more and more, lifecycle environmental performance data. This high level of regulation makes it more expensive for environmentally friendly manufacturers to follow the rules and gives them a chance to stand out from the competition.

Germany Networked Polymers Market Trends

Germany has the largest networked polymer market in Europe. This is because it has the fourth-largest chemical industry in the world, a strong automotive manufacturing sector that makes more than 4 million vehicles a year, and an advanced engineering machinery industry that needs polymers to work at high levels. BASF, Covestro, Lanxess, and Evonik Industries all have European R&D centers in Germany. Together, these centers are home to some of the world’s most important networked polymer research programs. The polymer research institutes in the Fraunhofer network add another level of collaborative applied research that links industrial producers with end-user application developers. This helps keep networked polymer formulation and processing technology up to date.

Why is the LAMEA Region Accelerating Networked Polymer Adoption?

The networked polymer market in the LAMEA region is slowly but surely growing. This is because the Gulf Cooperation Council countries are investing in infrastructure, Brazil’s automotive and industrial manufacturing base is growing, and South Africa’s technical infrastructure is getting better. Emerging economies in Latin America and the Middle East and Africa are great places to invest because they are building up their infrastructure and industrializing.

Saudi Arabia’s Vision 2030 program to diversify the economy is encouraging investment in domestic manufacturing, such as the production of specialty chemicals and polymers. This will help the region become less reliant on imported finished polymer products, which it has been for a long time. Brazil’s construction industry, consumer goods manufacturing, and oil and gas infrastructure are the biggest demand channels in Latin America. The country’s automotive cluster in São Paulo and nearby states is becoming a bigger market for automotive-grade polymer systems.

Brazil Networked Polymers Market Trends

Brazil’s networked polymer market is growing because the country is the largest car maker in Latin America, the petrochemical manufacturing infrastructure in the Rio de Janeiro and São Paulo corridors is getting bigger, and the construction industry is growing because of urbanization and infrastructure development. Brazil is one of the world’s largest producers of wind energy, with more than 28 GW of installed capacity. As the country’s wind energy capacity grows, so does the need for glass fiber-reinforced epoxy composite wind turbine blade materials. This creates a demand channel for thermoset networked polymer systems that is driven by renewable energy.

Top Players in the Networked Polymers Market and Their Offerings

- BASF SE

- DuPont de Nemours Inc.

- Dow Inc.

- Evonik Industries AG

- Arkema SA

- Mitsui Chemicals Inc.

- Covestro AG

- LANXESS AG

- Celanese Corporation

- Eastman Chemical Company

- Huntsman Corporation

- Solvay S.A.

- SABIC

- LyondellBasell Industries N.V.

- Others

Key Developments

Over the past few years, the networked polymers market has changed a lot as companies try to improve their products and services and expand their capabilities.

- In November 2021: Evonik Industries launched Trogamid myCX, a new line of networked polymers that are very clear and resistant to UV light, making them good for use in optical applications. BASF released Ultramid Endure in February 2021. This new line of networked polymers is very resistant to heat and humidity. This shows that the industry is still working to improve the performance of networked polymer systems in tough end-use situations.

- In the middle of 2024, a global polymer producer built a new continuous polymerization facility in Southeast Asia that can make 120,000 metric tons of engineering-grade thermoplastic networked polymers every year. This was done because electronics and automotive manufacturers were expanding their operations in Vietnam, Thailand, and Indonesia and needed more of these polymers.

These planned actions have helped businesses improve their market positions, grow their portfolios of sustainable materials, increase their production capacity, and take advantage of growth opportunities in the growing global networked polymers market.

The Networked Polymers Market is segmented as follows:

By Type

- Thermosetting Networked Polymers

- Epoxy Resins

- Phenolic Resins

- Polyester Resins

- Polyurethane

- Vinyl Ester Resins

- Cyanate Esters

- Others

- Thermoplastic Networked Polymers

- Polyethylene (PE)

- Polypropylene (PP)

- Polyamide (PA)

- Polyether Ether Ketone (PEEK)

- Acrylonitrile Butadiene Styrene (ABS)

- Others

- Elastomeric Networked Polymers

- Silicone Rubber

- Polyurethane Elastomers

- Others

By Application

- Automotive & Transportation

- Aerospace & Defense

- Electrical & Electronics

- Construction

- Healthcare & Medical

- Coatings, Adhesives & Sealants

- Others

By End-Use

- Manufacturing

- Consumer Goods

- Industrial

- Others

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Networked Polymers by Segments

- 2.1.2. Networked Polymers by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Networked Polymers Market Attractiveness Analysis, By Type

- 2.2.3. Networked Polymers Market Attractiveness Analysis, By Application

- 2.2.4. Networked Polymers Market Attractiveness Analysis, By End-Use

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Rising Demand for Lightweight

- 3.1.2. High-Strength Materials in Automotive and Aerospace Industries

- 3.1.3. Expanding Electronics Applications and the 5G Technology Rollout

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Networked Polymers Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Networked Polymers Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Thermosetting Networked Polymers

- 4.1.2.1. Epoxy Resins

- 4.1.2.2. Phenolic Resins

- 4.1.2.3. Polyester Resins

- 4.1.2.4. Polyurethane

- 4.1.2.5. Vinyl Ester Resins

- 4.1.2.6. Cyanate Esters

- 4.1.2.7. Others

- 4.1.3. Networked Polymers Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Thermoplastic Networked Polymers

- 4.1.6.1. Polyethylene (PE)

- 4.1.6.2. Polypropylene (PP)

- 4.1.6.3. Polyamide (PA)

- 4.1.6.4. Polyether Ether Ketone (PEEK)

- 4.1.6.5. Acrylonitrile Butadiene Styrene (ABS)

- 4.1.6.6. Others

- 4.1.7. Networked Polymers Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Elastomeric Networked Polymers

- 4.1.10.1. Silicone Rubber

- 4.1.10.2. Polyurethane Elastomers

- 4.1.10.3. Others

- 4.1.11. Networked Polymers Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Networked Polymers Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Networked Polymers Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Automotive & Transportation

- 5.1.3. Networked Polymers Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Aerospace & Defense

- 5.1.7. Networked Polymers Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Electrical & Electronics

- 5.1.11. Networked Polymers Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Construction

- 5.1.15. Networked Polymers Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Healthcare & Medical

- 5.1.19. Networked Polymers Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1.22. Coatings, Adhesives & Sealants

- 5.1.23. Networked Polymers Share Forecast, By Region (USD Billion)

- 5.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.25. Key Market Trends, Growth Factors, & Opportunities

- 5.1.26. Others

- 5.1.27. Networked Polymers Share Forecast, By Region (USD Billion)

- 5.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.29. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Networked Polymers Market – By End-Use

- 6.1. End-Use Market Overview, By End-Use Segment

- 6.1.1. Networked Polymers Market Revenue Share, By End-Use, 2025 & 2035

- 6.1.2. Manufacturing

- 6.1.3. Networked Polymers Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Consumer Goods

- 6.1.7. Networked Polymers Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Industrial

- 6.1.11. Networked Polymers Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Others

- 6.1.15. Networked Polymers Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End-Use Market Overview, By End-Use Segment

- Chapter 7. Networked Polymers Market – Regional Analysis

- 7.1. Networked Polymers Market Overview, By Region Segment

- 7.1.1. Global Networked Polymers Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Networked Polymers Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Networked Polymers Market Revenue, By Type, 2026 – 2035

- 7.1.4. Global Networked Polymers Market Revenue, By Application, 2026 – 2035

- 7.1.5. Global Networked Polymers Market Revenue, By End-Use, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Networked Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Networked Polymers Market Revenue, By Type, 2026 – 2035

- 7.2.3. North America Networked Polymers Market Revenue, By Application, 2026 – 2035

- 7.2.4. North America Networked Polymers Market Revenue, By End-Use, 2026 – 2035

- 7.2.5. U.S. Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Networked Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Networked Polymers Market Revenue, By Type, 2026 – 2035

- 7.3.3. Europe Networked Polymers Market Revenue, By Application, 2026 – 2035

- 7.3.4. Europe Networked Polymers Market Revenue, By End-Use, 2026 – 2035

- 7.3.5. Germany Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Networked Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Networked Polymers Market Revenue, By Type, 2026 – 2035

- 7.4.3. Asia Pacific Networked Polymers Market Revenue, By Application, 2026 – 2035

- 7.4.4. Asia Pacific Networked Polymers Market Revenue, By End-Use, 2026 – 2035

- 7.4.5. China Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Networked Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Networked Polymers Market Revenue, By Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Networked Polymers Market Revenue, By Application, 2026 – 2035

- 7.5.4. The Middle-East and Africa Networked Polymers Market Revenue, By End-Use, 2026 – 2035

- 7.5.5. Saudi Arabia Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Networked Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Networked Polymers Market Revenue, By Type, 2026 – 2035

- 7.6.3. Latin America Networked Polymers Market Revenue, By Application, 2026 – 2035

- 7.6.4. Latin America Networked Polymers Market Revenue, By End-Use, 2026 – 2035

- 7.6.5. Brazil Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Networked Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Networked Polymers Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Networked Polymers Market: Company Market Share, 2025

- 8.2. Global Networked Polymers Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. BASF SE

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. DuPont de Nemours Inc.

- 9.3. Dow Inc.

- 9.4. Evonik Industries AG

- 9.5. Arkema SA

- 9.6. Mitsui Chemicals Inc.

- 9.7. Covestro AG

- 9.8. LANXESS AG

- 9.9. Celanese Corporation

- 9.10. Eastman Chemical Company

- 9.11. Huntsman Corporation

- 9.12. Solvay S.A.

- 9.13. SABIC

- 9.14. LyondellBasell Industries N.V.

- 9.15. Others.

- 9.1. BASF SE

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Healthcare Foresights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

- Chapter 12. List Of Figures

- 12.1. Figures No 1 to 46

- Chapter 13. List Of Tables

- 13.1. Tables No 1 to 46

Prominent Player

- BASF SE

- DuPont de Nemours Inc.

- Dow Inc.

- Evonik Industries AG

- Arkema SA

- Mitsui Chemicals Inc.

- Covestro AG

- LANXESS AG

- Celanese Corporation

- Eastman Chemical Company

- Huntsman Corporation

- Solvay S.A.

- SABIC

- LyondellBasell Industries N.V.

- Others

FAQs

The key players in the market are BASF SE, DuPont de Nemours Inc., Dow Inc., Evonik Industries AG, Arkema SA, Mitsui Chemicals Inc., Covestro AG, LANXESS AG, Celanese Corporation, Eastman Chemical Company, Huntsman Corporation, Solvay S.A., SABIC, LyondellBasell Industries N.V., Others.

The networked polymers market is undergoing numerous transformations due to environmental regulations. As an example, the European Union regulation on REACH obliges a complete safety evaluation and registration of chemical materials in the production of polymers, increasing compliance costs of manufacturers beyond the EU. The Environmental Protection Law and the VOC emission standards in china are forcing the Chinese polymer manufacturers to upgrade their processes. The recyclability consideration in material design due to extended producer responsibility regulations is being mandated in the EU and a small number of Asian markets, which is driving investment in vitrimer and dynamic covalent chemistry research. Lastly, low-VOC environmentally certified systems of polymer coatings and adhesives are in high demand in North America and Europe as a result of green building standards. At the same time, rules that support renewable energy infrastructure, like wind turbines, solar mounting systems, and EV charging stations, are creating a lot of indirect demand for thermoset composite materials. This is a positive aspect to the industry since it helps to cover the expenses incurred in compliance with environmental regulations.

There are several issues with the networked polymers market that can slow down its development. A major issue is that it is difficult and costly to make thermosetting polymers since most of these polymers typically require special equipment and exact curing methods, which increases the cost of their production. Due to the irreversibility of the curing process, the number of possible recycling methods is limited, which has environmental implications and puts the government under pressure to do something about the waste management. An increase or decrease in the supply and cost of essential raw materials may lead to issues in the supply chain and increase the price of the products. Thermoplastic polymers are recyclable and easy to manipulate, which poses a threat to the market share of some of their uses. Moreover, strict environmental laws aimed at reducing the risk of harmful chemical emissions in the production of polymers require manufacturers to invest resources in compliance and reorganization efforts.

According to current research and predictions, the global networked polymers market will grow from USD 37.25 billion in 2026 to about USD 58.40 billion by 2035, a compound annual growth rate (CAGR) of 5.8%. Growth will come from the growing use of networked polymer systems in the automotive, electronics, construction, and renewable energy sectors, as well as the fact that advanced polymer composites are replacing metal parts in more and more industries.

Asia Pacific is expected to keep the largest share of revenue, with about 38% of the global market share during the forecast period. This is due to the size of China’s manufacturing economy, the advanced technology of Japan’s and South Korea’s industrial bases, and the rapid growth of new Asian economies. The region’s integrated petrochemical supply chain, large-scale manufacturing infrastructure, and low production costs make it even more competitive in networked polymer production and consumption.

Asia Pacific is expected to have the highest regional CAGR of 6.2% over the next five years. This is because China has a large polymer production base and a quickly growing electric vehicle (EV) manufacturing industry. Japan and South Korea have advanced electronics and semiconductor manufacturing sectors; India is quickly building up its industry and infrastructure; and Southeast Asia’s growing automotive and electronics manufacturing ecosystem is attracting a lot of foreign direct investment from global OEMs and tier-1 suppliers who want to diversify their supply chains.

The global networked polymers market is growing quickly because more and more lightweight materials are being used in the automotive and aerospace industries to meet fuel efficiency and emission reduction goals. The market of electric vehicles is developing very fast; this is why more sophisticated polymer systems are required in the fields of batteries, thermal management, and structural applications. Electronics are also in demand due to the implementation of 5G infrastructure and the development of the semiconductor industry. The world is spending a lot of money on constructing infrastructures, and this is enhancing the application of thermoset resin in the construction industry. Lastly, research and development of bio-based, self-healing, and stimulus-responsive networked polymer systems are consuming more money and are creating new high-value application frontiers. All these combined will result in a CAGR of 5.8% between 2026 and 2035.