Bio-Based Cosmetics and Personal Care Ingredients Market Size, Trends and Insights By Ingredient Type (Emollients & Moisturizers, Plant-Derived Oils & Butters, Bio-Based Squalane, Fermentation-Derived Emollients, Natural Waxes, Surfactants, Sugar-Based Surfactants (APG, SPE), Amino Acid-Based Surfactants, Fatty Acid-Derived Surfactants, Emulsifiers, Lecithin & Phospholipids, Sucrose Esters, Plant Sterol Esters, Preservatives, Fermentation-Derived Preservatives, Natural Antimicrobial Extracts, Organic Acid-Based Systems, Active Ingredients, Botanical Extracts & Phytoactives, Fermentation-Derived Bioactives, Marine-Derived Actives, Upcycled & Circular Actives, Colorants & Pigments, Plant-Derived Colorants, Fermentation-Derived Pigments, Mineral Colorants, Other Ingredient Types), By Source (Plant-Derived, Seed & Fruit Oils, Root & Bark Extracts, Leaf & Flower Extracts, Upcycled Agricultural Byproducts, Algae & Marine-Derived, Microalgae, Macroalgae & Seaweed, Marine Biotechnology Derivatives, Fermentation-Derived, Bacterial Fermentation, Yeast Fermentation, Fungal Fermentation, Other Sources), By Application (Skin Care, Facial Moisturizers & Serums, Anti-Aging & Treatment, Sun Care, Body Care, Hair Care, Shampoos & Conditioners, Scalp Treatments, Styling Products, Color Cosmetics, Foundation & Complexion, Lip Products, Eye Cosmetics, Fragrances, Oral Care, Other Applications), By End Use (Mass Market, Premium & Prestige, Professional, Other End Uses), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 11.1%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Europe |

Major Players

- Givaudan SA

- Symrise AG

- Croda International Plc

- Evonik Industries AG

- Others

Reports Description

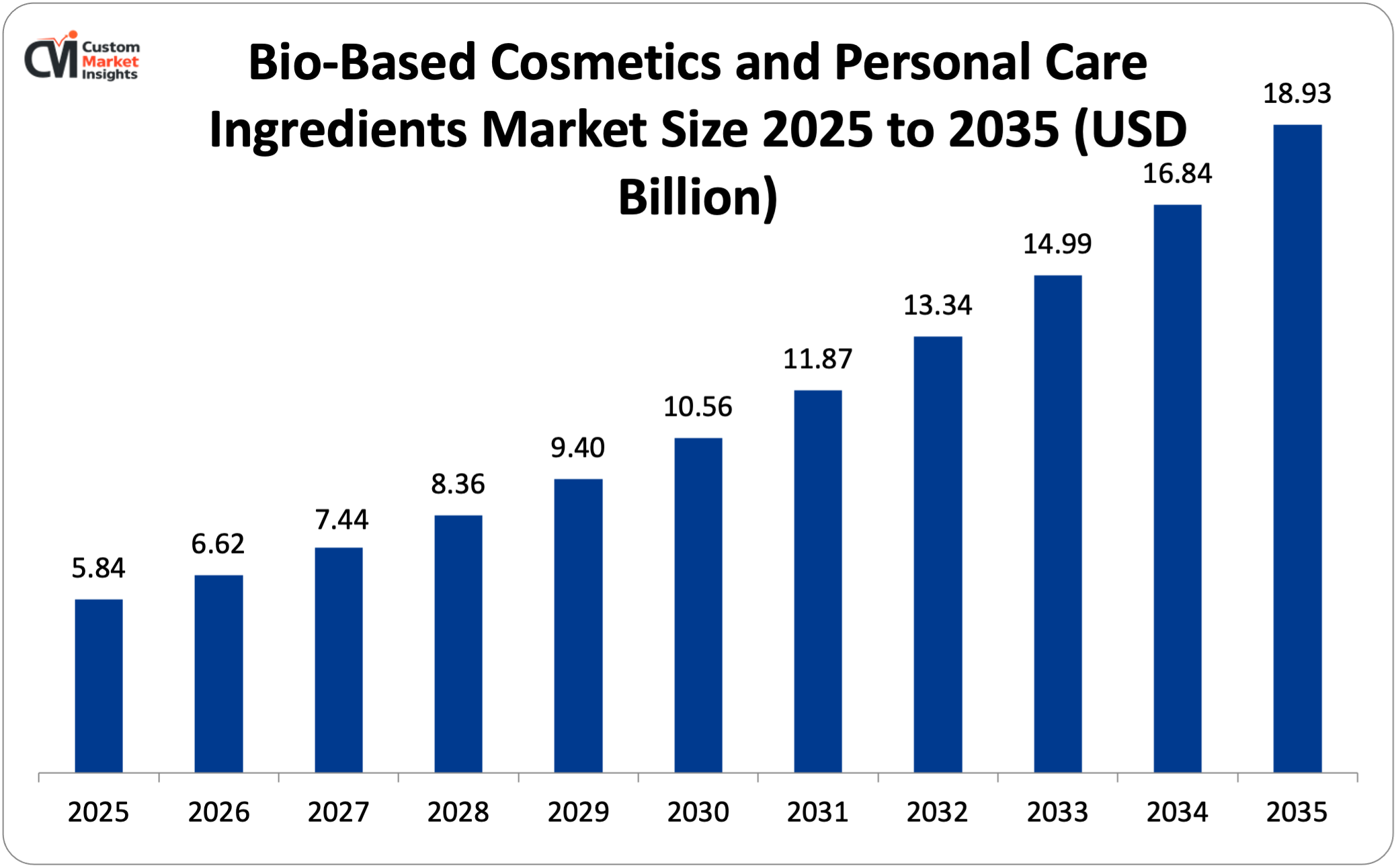

The market size of the global bio-based cosmetics and personal care ingredients is estimated to be USD 5.84 billion in 2025 and is expected to rise from USD 6.62 billion in 2026 to about USD 18.93 billion in 2035 with a CAGR of 11.1% between 2026 and 2035.

The growing market is being driven by the accelerating consumer demand towards clean beauty and natural formulations due to the increasing ingredient transparency pressures, the increasing regulatory constraints on synthetic and petrochemical-based ingredients across key markets, the rapid development of fermentation biotechnology and green chemistry technologies to develop bio-based alternatives to the functional superiority of synthetic and petrochemical ingredients, and the growing brand promises of sustainable sourcing and biodegradability.

Market Highlight

- Europe had the largest market share and was the market leader in bio-based cosmetics and personal care ingredients with a 34% market share in 2025 due to the most developed regulatory framework of clean beauty in the region, the greatest level of consumer awareness of bio-based ingredients, and the highest density of natural cosmetic certification agencies and bio-ingredient manufacturers.

- Asia Pacific is projected to grow with the highest CAGR of 13.6% in the 2026-2035 period owing to the phenomenal growth of the prestige skin care market in China, South Korea, Japan and India where consumers are highly inclined to botanical and fermentation-based skin care components.

- By ingredient type, emollients and moisturizers had an estimated market share of about 29% in 2025 with this being the largest volume bio-based ingredient group used in skin care, hair care and color cosmetic formulations across the world.

- By ingredient type, the active ingredients segment has the highest CAGR at 14.2% between 2026 and 2035, due to the unprecedented premiumization of skin care and the rapid rise in the consumer desire for scientifically proven bio-active compounds such as bio-retinol substitutes, plant-based peptides, and fermentation derived growth factors.

- Application By application, skin care had the largest market share of 43% in 2025 making facial moisturizers, serums, sunscreens, and anti-aging treatments the primary bio-based ingredient application by revenue.

- By application, the color cosmetics segment is forecasted to grow with a 12.8% CAGR of the next five years, 2026-2035, due to the clean beauty movement in the makeup industry and the gradual substitution of synthetic dyes, petroleum waxes, and petrochemical emollients with certified bio-based and natural compounds.

Significant Growth Factors

The Bio-Based Cosmetics and Personal Care Ingredients Market Trends present significant growth opportunities due to several factors:

- Clean Beauty Movement and Ingredient Transparency Demands Fundamentally Reshaping Formulation Priorities Across All Market Segments: The clean beauty movement, as a paradigm shift in consumption that requires formulations without particular synthetic and petrochemical-derived ingredients that are considered harmful, damaging to the environment, or ethically questionable has become the most influential structural demand driver of bio-based cosmetics ingredients of all types and of all geographies. The trend is marked by the active research of ingredient lists by consumers, the rejection of the compositions including certain synthetic substances such as parabens, sulfates, phthalates, silicones, mineral oil, and synthetic fragrances, and orientation towards the brands with ingredient philosophies toward transparency, natural origin, and environmental responsibility. A 2024 survey of global consumers showed that 71% of beauty consumers around the world now read ingredient labels before they buy, compared with 48% in 2019 a behavioral change that has far reaching consequences on the cosmetic formulators whose product development choices are now limited by consumer ingredients’ acceptability rather than by technical and cost optimization factors only. The imperative of clean beauty ingredient substitution is creating direct and increasing demand on bio-based substitutes of virtually all cosmetic ingredient functions: plant-derived squalene or amaranth as an emollient instead of petrochemical squalene and mineral oil; bio-based surfactants, such as coconut, corn, or sugar-derived, instead The first and most aggressively adopted bio-based ingredient platforms have been the premium and prestige segments of the skin care category, with such brands as Tata Harper, Beautycounter, Tatcha, Drunk Elephant, and Herbivore Botanicals building complete product portfolios and brand identities around bio-based, naturally-derived formulations – and securing a premium price and a strong brand identity that has become an acquisition target. Mass-market brands such as L’Oréal, Procter and Gamble, and Beiersdorf have reacted to the clean beauty demand by introducing dedicated natural ingredient sub-brands L’Oréal Seed Phytonutrients, P&G Herbal Essences Bio:Renew, and NIVEA Naturally Good and at the same time reformulated the existing flagship products to eliminate consumer-banned synthetic ingredients and replace them with.

- Regulatory Expansion Restricting Synthetic Cosmetic Ingredients Creating Mandatory Bio-Based Substitution Demand Across Major Markets: Irrelevant and mutually reinforcing of the evolution of consumer preferences, the global regulatory context that manages the safety of cosmetic ingredients and environmental impact is being subjected to tightening in the major markets, which impose mandatory reformulation requirements directly translating to bio-based ingredient demand even where the consumers of the brands in question are not at the level of ingredient consciousness that drives voluntary adoption of clean beauty. The cosmetics regulatory framework of the European Union is regulated under the EU Cosmetics Regulation (EC) No. 1223/2009 and its constantly updated restricted substances. Annex II list has banned the use of over 1,400 chemical substances in cosmetics, with the restriction list actively growing as the European Chemicals Agency (ECHA) conducts safety appraisals of further synthetic cosmetic ingredients through The Chemicals Strategy of the European Green Deal, which the EU adopted and has an express goal of further expanding such restrictions on cosmetic ingredients against endocrine-disrupting chemicals, substances of very high concern, and environmentally persistent synthetic compounds that are overrepresented among traditional cosmetic ingredient chemistries. The most notable change in U.S. cosmetics regulation since 1938 was the Modernization of Cosmetics Regulation Act of 2022 (MoCRA), which gave the FDA significantly greater authority to substantiate the safety of cosmetic ingredients, require good manufacturing practices, and possibly restrict or prohibit certain ingredients, taking the regulatory landscape towards European-equivalent levels of ingredient restriction, which will gradually reduce the range of acceptables. The Toxic-Free Cosmetics Act of California, which barred 24 specific cosmetic ingredients as of January 2025, and the ingredient reporting database of the California Safe Cosmetics Program are also further expediting the process of formulation changes in the largest U.S. state market, with national brands generally acquiring the most restrictive standard that applies to all lines. Under renewed cosmetic regulation in China, the National Medical Products Administration (NMPA) has introduced more stringent cosmetic ingredient safety and efficacy evaluation standards under revised cosmetic regulations that become effective in 2021, and at the same time, has designated certain natural botanical extract and fermentation-derived ingredients as traditional Chinese medicine-adjacent materials with expedited approval approaches that provide regulatory benefit to bio-based ingredients.

What are the Major Advances Changing the Bio-Based Cosmetics and Personal Care Ingredients Market Today?

- Fermentation Biotechnology Enabling Unprecedented Bioactive Ingredient Innovation and Performance Parity With Synthetic Compounds: Unparalleled Bioactive Ingredient Novelty and Performance Equity to Synthetic Compounds The most disruptive technological advancement transforming the bio-based cosmetics ingredient category is the use of precision fermentation where engineered microorganisms, such as bacteria, yeast, and fungi, are programmed to synthesize specific high-value cosmetic active compounds. The most commercially important bio-fermentation product in cosmetics, hyaluronic acid, which is consumed worldwide in skin care formulations at an estimated 6,500 tonnes each year due to its extraordinary humectant and skin plumping properties, is produced only by fermentation of Streptococcus equi or related bacterial strains, and its commercial manufacturers include Bloomage Biotechnology. Squalane derived by fermentation of sugarcane-derived farnesene, via yeast fermentation of Amyris Inc., then converted to squalane has dominated the market over traditional squalane derived by shark finning, and is gradually replacing petrochemical squalane in high end skin care formulations, which is better compatible with human skin, has the same molecular structure as squalane produced by plants, and presents more Next-generation fermentation platforms are also facilitating bio-production of some hitherto synthetically-only compounds such as retinol. Companies such as Genomatica and Eurekam are developing fermentation routes to bio-retinol which would replace the petrochemical synthesis route to retinol that currently supplies nearly all commercial retinol production, niacinamide fermentation routes to bio-nic The de novo production of bio-novel compounds, peptides, proteins, polysaccharides, and secondary metabolites, which are simply not found in accessible amounts in nature and are practically unavailable to extract but can be designed in silico using computational protein engineering and produced in large amounts by fermentation, is also being facilitated by the precision fermentation approach, providing a completely new frontier of bio-active cosmetics.

- Marine and Algae-Derived Ingredients Establishing New Sustainability-Differentiated Ingredient Categories: Marine biotechnology is proving to be one of the most dynamically innovative sectors in bio-based cosmetic ingredients, and algae, seaweed, marine microorganisms, and marine-derived compounds have been shown to have unique bioactive profiles, due to evolutionary adaptation to extreme ocean environments, With both the scientifically proven efficacy of marine bioactives such as astaxanthin, fucoidans, carrageenan, marine collagen peptides, and alguronic acid, and the strong sustainability message of marine ingredients sourced by controlled aquaculture or cultivating in photobioreactors without land use, pesticides, and the susceptibility of traditional botanical ingredient sourcing to land use, pestic Commercial scale Microalgae cultivation – e.g. Haematococcus pluvialis (producing astaxanthin) under open raceway pond and closed photobioreactor production systems, Nannochloropsis (producing EPA), and Arthrospira (Spirulina) (producing protein and phycocyanin pigments)—is now commercially viable, with manufacturers such as Algatech, Bio-based alternatives to synthetic polymer thickeners, emulsifiers, and film-forming agents such as carrageenan in red seaweeds, sodium alginate in brown kelp, and agar in Gracilaria are being developed as macroalgae, and are being used as multifunctional bio-based rheology modifiers in personal care formulations as substitutes to synthetic carbomers, PEG derivatives Brands with sustainability credentials of marine-derived ingredients, especially those grown with seaweed aquaculture that captures carbon, offer marine habitat complexity, and do not require freshwater or synthetic fertilizer interventions are drawing premium pricing and sustainability certification assistance in the increasingly competitive clean beauty marketplace, which is the most differentiated and scientifically supported claim of sustainability.

- Upcycled and Circular Economy Ingredient Sourcing Creating New Bio-Based Raw Material Platforms: The implementation of the principles of the circular economy to cosmetic ingredient sourcing – whereby by-products and waste streams of food processing, agricultural production, beverage manufacturing, and pharmaceutical fermentation are valorized into high-performing cosmetic active and functional ingredients – is producing a completely new form of cosmetic ingredients bio Coffee cherry extract, a high-antioxidant skin care active extracted using the pulp and husks left behind in the processing of coffee beans, a waste stream of about 10 million tonnes a year, is being developed as a high-antioxidant skin care active by such companies as Volcán Azul (collaborating with Starbucks) and used in product lines by Biossance and Saie. Wine production byproducts that contain grape seed and grape skin extracts, which are also rich in polyphenolic antioxidants such as resveratrol, oligomeric proanthocyanidins, and quercetin, are also established commercial bio-based actives, such as Natex and Nexira, based on the large quantities of pomace left by European wine production. Rice bran, a byproduct of white rice milling, was also a source of rice bran oil, ceramides, ferulic acid, phytic acid, and gamma-oryzanol – various different cosmetically active compounds that can be extracted simultaneously using the same stream of agricultural byproducts, making rice bran one of the highest value-dense upcycled ingredient raw materials in cosmetics. The idea of upcycled beauty ingredients is being commercialized with certification and transparency schemes: the Upcycled Beauty Standard, created by the Upcycled Food Association and applied to cosmetics, and Origin claims verification systems offered by certification organizations such as Ecocert and NSF International are offering verifiable upcycled ingredient credentials that brands can use on-pack and in digital marketing with provenance documentation. According to consumer research, the story of upcycled ingredients (especially the use of familiar food-industry byproducts and effluents such as fruit peels, coffee grounds, and olive mill effluent) into high-value cosmetic actives has produced high purchase intent and brand affinity scores among clean beauty shoppers who view waste valorization as an authentically meaningful sustainability practice instead of a form of greenwashing.

Category Wise Insights

By Ingredient Type

Why Do Emollients and Moisturizers Lead the Bio-Based Cosmetics Ingredients Market?

Emollients and moisturizers will constitute the biggest type of ingredient segment in 2025, and this segment will contribute about 29% of the total market revenue. This superiority is indicative of the primary position of emollient and moisturizing ingredients as the most volumetric functional components in skin care, body care, lip care, and color cosmetics formulations – delivering the sensory skin feel, occlusiveness of moisture retention, and skin conditioning functionality that consumers physically experience and relate to product efficacy. The shift to bio-based emollients in place of petrochemical ones like mineral oil, petrolatum, dimethicone, and isopropyl myristate is coinciding with both consumer-driven rejection of petroleum-based emollient ingredients and regulatory bans on the use of particular synthetic emollient chemistries in the European marketplace. The most commercially developed category of bio-based emollient oils and butters are plant-derived, and some of the established premium skin care ingredients that are available commercially as per-kg products include argan oil, rosehip seed oil, jojoba oil, marula oil, sea buckthorn oil, shea butter, mango butter, and kokum butter with price ranges of USD 15-500 One of the most commercially successful bio-based emollient transitions of the last 10 years is bio-based squalane, whether produced via the fermentation of sugarcane or the byproducts of upcycled olive oil processing, which has been widely adopted in high-end skin care in high concentrations as a lightweight, non-comedogenic, skin-identical emollient and has successfully replaced shark-der Bio-based substitutes to petroleum-derived paraffin and microcrystalline waxes in lip products, mascara, and anhydrous formulations are natural waxes such as carnauba, candelilla, beeswax, and rice bran wax, which are also vegan natural waxes, have increasing demand, especially fast as color cosmetics brands switch beeswax to plant-based carnauba and candelilla alternatives.

By Source

Why Do Plant-Derived Ingredients Lead the Source Segment?

The commercial maturity, the breadth of supply chains, regulatory acceptance, and consumer familiarity of botanical ingredient platforms, which have underpinned the natural cosmetics category since the first commercial development of the category, mean that 54% of all market revenue in 2025 will be taken by plant-derived ingredients. The vegetable segment is the broadest source of ingredient portfolio of any source category, including high-volume commodity ingredients of coconut-derived surfactants and emulsifiers, consumed in thousands of tonnes per year, mid-volume specialty oils, such as argan, rosehip, and marula, which are consumed in tens of tonnes per year, and rare exotic extracts, such as oud, neroli, and Bak. Organic botanical ingredient certification is increasing especially fast, with the Cosmos Organic and USDA Organic certification systems offering credible third party credentialing assurance to the consumer and retailer that the additional brand natural claims are in demand. The most rapidly growing segment of source is fermentation-derived ingredients with a CAGR of 15.1% between 2026 and 2035 with precision fermentation capabilities that allow bio-identical and bio-novel active ingredients to be produced at large scale with a purity and consistency unattainable by plant extraction processes, which are subject to crop variability. The second-fastest-growing source with a 14.8% CAGR is algae and marine-derived ingredients, with the growth difference and sustainability attributes of marine bioactives and the commercialization of the microalgae and seaweed farming infrastructure.

By Application

Why Does Skin Care Dominate the Bio-Based Cosmetics Ingredients Application Landscape?

The biggest area of application is the skin care segment which is expected to contribute nearly 43% of all market revenue in 2025. This preeminence is a reflection of the point of congruence between the greatest consumer activity in any personal care category skin care users are the most likely category user group to research ingredient lists, seek clinical substantiation, and pay premiums based on bio-active credentials – and the most profoundly extensive and diverse functional ingredients to form the broadest addressable market to bio-based ingredient substitution. The worldwide skin care market is estimated to be USD 162.7 billion in 2024 and is set to rise to USD 240.8 billion by 2030, with the sub-sector that is adopting bio-based ingredient formulations in its products the most aggressively being premium and prestige skin care, growing disproportionately faster than mass market skin care with an estimated CAGR The facial serum applications show the highest value of the bio-active ingredient unit application in the skin care sector, since serums are designed at a higher level of active ingredient and are positioned as high-efficacy treatment products where the premium bio-active ingredient can be priced the most easily based on the consumer being willing to pay more to get a demonstrable skin benefit. The anti-aging skin care sub-segment is especially bio-active ingredient intensive with botanical retinoic acid analogs such as Bakuchiol extracted out of Psoralea corylifera seeds, trans-retinoic acid analogs found in rosehip, and retinaldehyde precursors in fermentation-derived all moving quickly into commercial growth as clean beauty-committed consumers seek clinically substantiated alternatives to conventional retinol that are compatible with pregnancy, sensitive skin, and clean beauty formulation philosophies.

By End Use

Why Does Premium and Prestige Lead the End Use Segment?

The high-end use and premium segment of the market is in the range of about 44% of total market revenue, yet the segment is a smaller percentage of the unit volume, due to the high premium prices charged by bio-based cosmetic ingredients and the concentration of bio-based formulation adoption into those market segments where brand storytelling on natural origin, sustainability, and bio-active efficacy have the greatest impact on consumer purchasing decisions and willingness to The premium and prestige brands have been the first movers in the bio-based ingredient adoption since the launch of the category, with brands like La Mer, La Prairie, Tatcha, Tata Harper and Aesop all basing competitive differentiation on bio-derived ingredient platforms of marine fermentation, Japanese botanical extracts, certified organic farming and Australian plant actives, respectively, that retail at USD 50-500 The professional end use market – which includes salon professional hair care, dermatologist – prescribed skin care, and spa treatment products—is projected to grow at a 12.1% CAGR between 2026 and 2035 owing to the authority of the professional channel as a consumer trust and brand education channel of the bioactive ingredient concepts, which are later transferred to a retail channel. Although at present the adoption of bio-based ingredients in the mass market is around 28% of market revenue, the adoption is increasing at the rate of 9.8% CAGR as the cost of formulation is reduced through mass production of bio-based ingredients, especially bio-surfactants, bio-emulsifiers, and standard botanical extracts, which allows mass market price positioning of bio-based formulations.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 6.62 billion |

| Projected Market Size in 2035 | USD 18.93 billion |

| Market Size in 2025 | USD 5.84 billion |

| CAGR Growth Rate | 11.1% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Ingredient Type, Source, Application, End Use and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Europe Market Size?

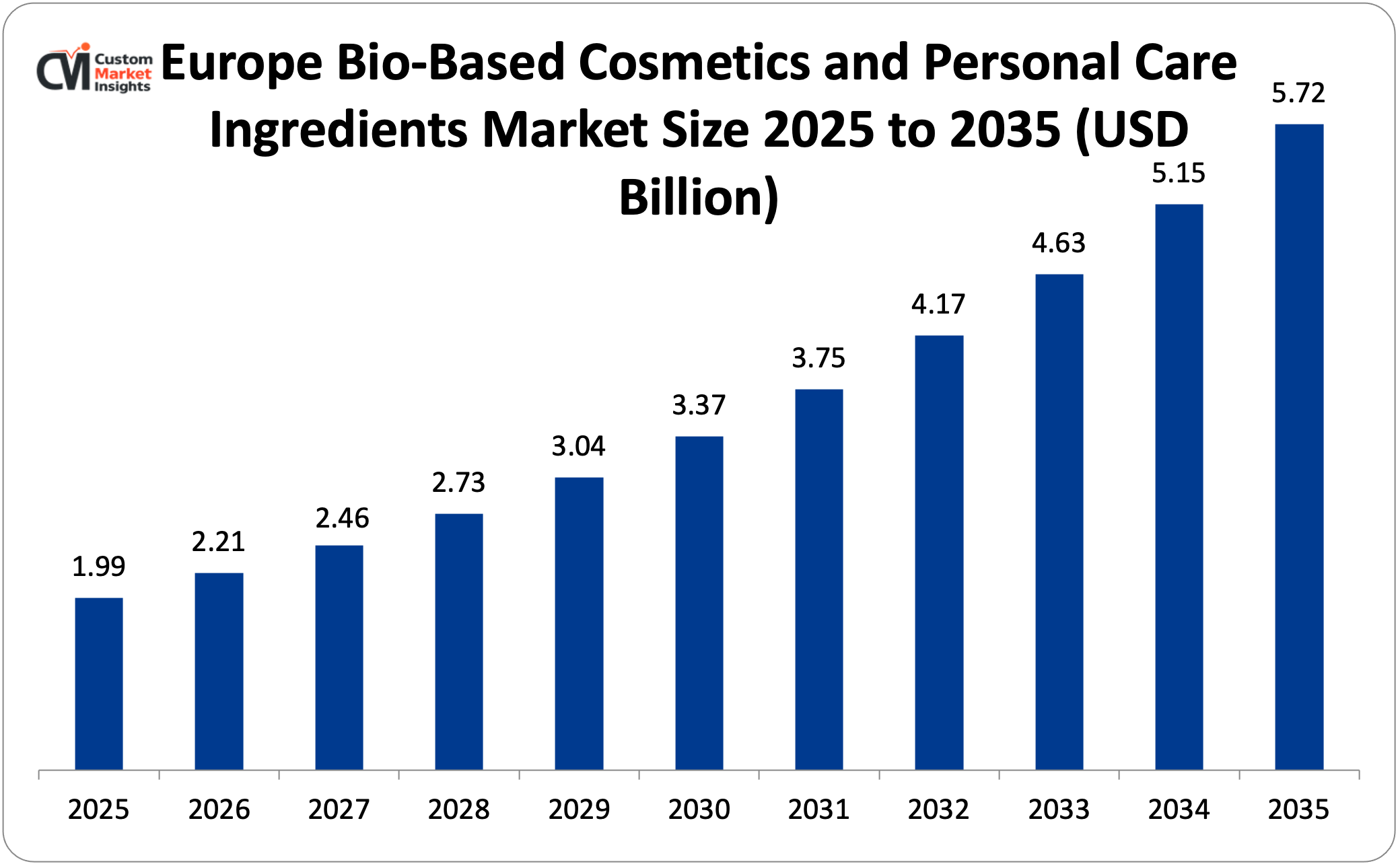

The European bio-based cosmetics and personal care ingredients market size is estimated at USD 1.99 billion in 2025 and is projected to reach approximately USD 5.72 billion by 2035, growing at a CAGR of 11.1% from 2026 to 2035.

Why did Europe Dominate the Market in 2025?

In the year 2025, Europe leads the global market revenue in the natural cosmetics industry at some 34%, a position earned through the most developed system of natural cosmetic ingredient regulatory and certification worldwide, the highest density of certified natural and organic cosmetic consumers in the world, the concentration of natural cosmetic ingredient manufacturing headquarters in countries such as France, Germany, Switzerland and Italy, and a long history of historical experience with botanicals. This long varied restricted substances list of the EU Cosmetics Regulation, which is the most comprehensive in the world with a list of over 1,400 prohibited ingredients, has structurally required bio-based ingredient replacement of a wider selection of cosmetic uses than any other regulatory framework, gradually widening the list of uses to which bio-based alternatives are not just desirable but necessary to access the EU market. European-based natural cosmetics certification organizations such as COSMOS Standard (managed by BDIH, Cosmebio, Ecocert, ICEA, and Soil Association) have set the current world standard certification models defining bio-based and natural ingredient standards followed by brands and consumers in more than 70 countries, providing the European certification framework with a disproportionate international platform over bio-based ingredient market standards.

The world’s fragrance and premium cosmetics ingredient centers are in France, respectively, as the fragrance tradition of Grasse, as well as the concentration of the headquarters of prestige and luxury brands of beauty, creates the most discerning and powerful market in the world in terms of highly sought-after premium natural and bio-based cosmetic active ingredients. The historical natural and organic cosmetics market in Germany, supported by the standard of BDIH natural cosmetics and a highly developed ecological consumer culture, keeps the market as the highest ratio of certified natural cosmetics use per capita in the world, with Weleda, Dr. Hauschka, Lavera, and LOGANA, each representing one of the most well-established certified natural cosmetic brands and high consumers of bio-based ingredient consumers.

Why is Asia Pacific the Fastest-Growing Regional Market?

Asia Pacific, though, possesses some of the most promising market revenue of about 28% in the world market with estimated value of USD 1.63 billion and a CAGR of a whopping 13.6% between 2026 and 2035 due to the exceptional growth of premium skin care consumption in China, South Korea, Japan and India with strong consumer demand on botanical, fermented and The K-beauty phenomena of South Korea, that has over the past decade exported Korean beauty culture, formulation innovation, and ingredient trends to the rest of the world, is a particularly influential source of bio-based ingredient adoption, with the adoption of fermentation-based ingredients (fermented rice water, sake fermentation filtrate and probiotic ferments) and botanical extracts (green tea). Shortly, with the presence of technical sophistication of the Japanese fermentation technology on cosmetic efforts applied to cosmetics, the market of these bio-based cosmetic ingredients in Japan is characterized by the fact that Japanese have an advanced, well-established, and sophisticated consumer of beauty products, which is prepared to spend large sums of money on fermentation-based, science-backed innovations in skin care products. The Chinese market of bio-based cosmetic ingredients is forecasted to increase at a rate of about 15.2% CAGR between 2026 and 2035 due to the unprecedented growth of the Chinese prestige beauty market and a favorable regulatory environment created by the government that promotes the use of traditional Chinese medicine-related ingredients in cosmetic formulations, providing regulatory pathways and benefits to some types of bio-based and fermentation-derived active ingredients.

Why is North America Showing Strong Sustained Growth?

In 2025, the North American market serves around 22% of the global market revenue and is projected to grow at a CAGR of 10.8% between the years 2026 and 2035, sustained by the expanding regulatory demands under the MoCRA, the accelerating retailer clean beauty requirements, and the eye-opening expansion of direct-to-consumer clean beauty brands, which in turn have.

Why is the Middle East & Africa Region an Emerging High-Growth Market?

The LAMEA region constitutes about 8% of the global market revenue in the year 2025 but with a projected CAGR of 12.3% between two decades, 2025 and 2035, prompted by a number of different demand vectors in its makeup markets. The Middle East and the UAE, specifically, are fast-expanding premium cosmetics consumer markets with the greatest cultural interest in botanical fragrance compounds such as oud, rose, and frankincense as part of the regional botanical heritage and a highly developed luxury customer base that is becoming more involved in clean beauty branding resources aligned with the cultures of wellness and halal cosmetics. The botanical biodiversity of Brazil, including the Amazon basin, cerrado, and Atlantic forest, which together contributes thousands of species of singular botanical species with cosmetic bioactive potential, makes the country not only a significant consumer but also a bio-producer of seemingly unique Amazon-based bio-based cosmetic ingredients, with cupuaçu butter, açaí extract, murumuru butter, andiroba oil, and Brazil nut oil establishing a global commercial presence as unique Amazon-origin bio-based cosmetic ingredients.

Top Players in the Market and Their Offerings

- Givaudan SA

- Firmenich SA (dsm-firmenich)

- Symrise AG

- Croda International Plc

- Evonik Industries AG

- BASF SE

- Clariant AG

- Ashland Global Holdings Inc.

- Elementis plc

- Innospec Inc.

- Others

Key Developments

The market has undergone significant developments as industry participants seek to expand capabilities and enhance product portfolios.

- In March 2025: Croda International Plc declared the commercial introduction of its Crodamol™ SFX bio-based emollient system, a new generation of 100% bio-based, COSMOS-approved emollient esters made of upcycled agricultural byproduct fatty acids and bio-based polyols that obtained the same sensory ingredient efficiency and equivalent sensory performance to conventional synthetic isopropyl myristate and C12-15 alkyl benzoate emollients while offering fully biodegradable, palm-free, and certified bio-based content above 95%—directly addressing the formulation challenge of replacing petroleum-derived emollient esters in premium skin care and color cosmetics applications without compromising the sensory elegance that prestige consumers demand.

- In February 2025: Givaudan SA stated a strategic relationship with biotechnology company Ginkgo Bioworks to partner in the creation of precision fermentation-derived perfume and active cosmetic ingredients based on Ginkgo’s organism engineering platform, beginning with the synthesis of rare botanical fragrance compounds reliant on geographically constrained and climate-exposed plant harvests such as sandalwood, ambergris, and orris root derivatives — through scalable yeast fermentation, with the first joint fermentation-derived ingredient launches targeted for commercial introduction by 2027 across Givaudan’s Active Beauty and Fragrance divisions serving premium cosmetics and fine fragrance brand customers globally.

These strategic activities have allowed companies to strengthen market positions, expand bio-based ingredient portfolios addressing evolving formulator and consumer requirements, develop next-generation fermentation and biotechnology-derived ingredient platforms, and capitalize on the structural demand growth being generated by the clean beauty revolution, regulatory tightening of synthetic ingredient acceptability, and the progressive global adoption of bio-based cosmetic formulation standards across mass market, premium, and prestige beauty segments.

The Bio-Based Cosmetics and Personal Care Ingredients Market is segmented as follows:

By Ingredient Type

- Emollients & Moisturizers

- Plant-Derived Oils & Butters

- Bio-Based Squalane

- Fermentation-Derived Emollients

- Natural Waxes

- Surfactants

- Sugar-Based Surfactants (APG, SPE)

- Amino Acid-Based Surfactants

- Fatty Acid-Derived Surfactants

- Emulsifiers

- Lecithin & Phospholipids

- Sucrose Esters

- Plant Sterol Esters

- Preservatives

- Fermentation-Derived Preservatives

- Natural Antimicrobial Extracts

- Organic Acid-Based Systems

- Active Ingredients

- Botanical Extracts & Phytoactives

- Fermentation-Derived Bioactives

- Marine-Derived Actives

- Upcycled & Circular Actives

- Colorants & Pigments

- Plant-Derived Colorants

- Fermentation-Derived Pigments

- Mineral Colorants

- Other Ingredient Types

By Source

- Plant-Derived

- Seed & Fruit Oils

- Root & Bark Extracts

- Leaf & Flower Extracts

- Upcycled Agricultural Byproducts

- Algae & Marine-Derived

- Microalgae

- Macroalgae & Seaweed

- Marine Biotechnology Derivatives

- Fermentation-Derived

- Bacterial Fermentation

- Yeast Fermentation

- Fungal Fermentation

- Other Sources

By Application

- Skin Care

- Facial Moisturizers & Serums

- Anti-Aging & Treatment

- Sun Care

- Body Care

- Hair Care

- Shampoos & Conditioners

- Scalp Treatments

- Styling Products

- Color Cosmetics

- Foundation & Complexion

- Lip Products

- Eye Cosmetics

- Fragrances

- Oral Care

- Other Applications

By End Use

- Mass Market

- Premium & Prestige

- Professional

- Other End Uses

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Bio-Based Cosmetics and Personal Care Ingredients by Segments

- 2.1.2. Bio-Based Cosmetics and Personal Care Ingredients by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Bio-Based Cosmetics and Personal Care Ingredients Market Attractiveness Analysis, By Ingredient Type

- 2.2.3. Bio-Based Cosmetics and Personal Care Ingredients Market Attractiveness Analysis, By Source

- 2.2.4. Bio-Based Cosmetics and Personal Care Ingredients Market Attractiveness Analysis, By Application

- 2.2.5. Bio-Based Cosmetics and Personal Care Ingredients Market Attractiveness Analysis, By End Use

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Clean Beauty Movement and Ingredient Transparency Demands Fundamentally Reshaping Formulation Priorities Across All Market Segments

- 3.1.2. Regulatory Expansion Restricting Synthetic Cosmetic Ingredients Creating Mandatory Bio-Based Substitution Demand Across Major Markets

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Bio-Based Cosmetics and Personal Care Ingredients Market – By Ingredient Type

- 4.1. Ingredient Type Market Overview, By Ingredient Type Segment

- 4.1.1. Bio-Based Cosmetics and Personal Care Ingredients Market Revenue Share, By Ingredient Type, 2025 & 2035

- 4.1.2. Emollients & Moisturizers

- 4.1.2.1. Plant-Derived Oils & Butters

- 4.1.2.2. Bio-Based Squalane

- 4.1.2.3. Fermentation-Derived Emollients

- 4.1.2.4. Natural Waxes

- 4.1.3. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Surfactants

- 4.1.6.1. Sugar-Based Surfactants (APG, SPE)

- 4.1.6.2. Amino Acid-Based Surfactants

- 4.1.6.3. Fatty Acid-Derived Surfactants

- 4.1.7. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Emulsifiers

- 4.1.10.1. Lecithin & Phospholipids

- 4.1.10.2. Sucrose Esters

- 4.1.10.3. Plant Sterol Esters

- 4.1.11. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Preservatives

- 4.1.14.1. Fermentation-Derived Preservatives

- 4.1.14.2. Natural Antimicrobial Extracts

- 4.1.14.3. Organic Acid-Based Systems

- 4.1.15. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Active Ingredients

- 4.1.18.1. Botanical Extracts & Phytoactives

- 4.1.18.2. Fermentation-Derived Bioactives

- 4.1.18.3. Marine-Derived Actives

- 4.1.18.4. Upcycled & Circular Actives

- 4.1.19. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Colorants & Pigments

- 4.1.22.1. Plant-Derived Colorants

- 4.1.22.2. Fermentation-Derived Pigments

- 4.1.22.3. Mineral Colorants

- 4.1.23. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1.26. Other Ingredient Types

- 4.1.27. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 4.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.29. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Ingredient Type Market Overview, By Ingredient Type Segment

- Chapter 5. Bio-Based Cosmetics and Personal Care Ingredients Market – By Source

- 5.1. Source Market Overview, By Source Segment

- 5.1.1. Bio-Based Cosmetics and Personal Care Ingredients Market Revenue Share, By Source, 2025 & 2035

- 5.1.2. Plant-Derived

- 5.1.2.1. Seed & Fruit Oils

- 5.1.2.2. Root & Bark Extracts

- 5.1.2.3. Leaf & Flower Extracts

- 5.1.2.4. Upcycled Agricultural Byproducts

- 5.1.3. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Algae & Marine-Derived

- 5.1.6.1. Microalgae

- 5.1.6.2. Macroalgae & Seaweed

- 5.1.6.3. Marine Biotechnology Derivatives

- 5.1.7. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Fermentation-Derived

- 5.1.10.1. Bacterial Fermentation

- 5.1.10.2. Yeast Fermentation

- 5.1.10.3. Fungal Fermentation

- 5.1.11. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Other Sources

- 5.1.15. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Source Market Overview, By Source Segment

- Chapter 6. Bio-Based Cosmetics and Personal Care Ingredients Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Bio-Based Cosmetics and Personal Care Ingredients Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Skin Care

- 6.1.2.1. Facial Moisturizers & Serums

- 6.1.2.2. Anti-Aging & Treatment

- 6.1.2.3. Sun Care

- 6.1.2.4. Body Care

- 6.1.3. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Hair Care

- 6.1.6.1. Shampoos & Conditioners

- 6.1.6.2. Scalp Treatments

- 6.1.6.3. Styling Products

- 6.1.7. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Color Cosmetics

- 6.1.10.1. Foundation & Complexion

- 6.1.10.2. Lip Products

- 6.1.10.3. Eye Cosmetics

- 6.1.11. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Fragrances

- 6.1.15. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Oral Care

- 6.1.19. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Other Applications

- 6.1.23. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Bio-Based Cosmetics and Personal Care Ingredients Market – By End Use

- 7.1. End Use Market Overview, By End Use Segment

- 7.1.1. Bio-Based Cosmetics and Personal Care Ingredients Market Revenue Share, By End Use, 2025 & 2035

- 7.1.2. Mass Market

- 7.1.3. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Premium & Prestige

- 7.1.7. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Professional

- 7.1.11. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Other End Uses

- 7.1.15. Bio-Based Cosmetics and Personal Care Ingredients Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End Use Market Overview, By End Use Segment

- Chapter 8. Bio-Based Cosmetics and Personal Care Ingredients Market – Regional Analysis

- 8.1. Bio-Based Cosmetics and Personal Care Ingredients Market Overview, By Region Segment

- 8.1.1. Global Bio-Based Cosmetics and Personal Care Ingredients Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Ingredient Type, 2026 – 2035

- 8.1.4. Global Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Source, 2026 – 2035

- 8.1.5. Global Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By End Use, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Ingredient Type, 2026 – 2035

- 8.2.3. North America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Source, 2026 – 2035

- 8.2.4. North America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By End Use, 2026 – 2035

- 8.2.6. U.S. Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Ingredient Type, 2026 – 2035

- 8.3.3. Europe Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Source, 2026 – 2035

- 8.3.4. Europe Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By End Use, 2026 – 2035

- 8.3.6. Germany Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Ingredient Type, 2026 – 2035

- 8.4.3. Asia Pacific Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Source, 2026 – 2035

- 8.4.4. Asia Pacific Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By End Use, 2026 – 2035

- 8.4.6. China Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Ingredient Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Source, 2026 – 2035

- 8.5.4. The Middle-East and Africa Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By End Use, 2026 – 2035

- 8.5.6. Saudi Arabia Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Ingredient Type, 2026 – 2035

- 8.6.3. Latin America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Source, 2026 – 2035

- 8.6.4. Latin America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, By End Use, 2026 – 2035

- 8.6.6. Brazil Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Bio-Based Cosmetics and Personal Care Ingredients Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Bio-Based Cosmetics and Personal Care Ingredients Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Bio-Based Cosmetics and Personal Care Ingredients Market: Company Market Share, 2025

- 9.2. Global Bio-Based Cosmetics and Personal Care Ingredients Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Givaudan SA

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Firmenich SA (dsm-firmenich)

- 10.3. Symrise AG

- 10.4. Croda International Plc

- 10.5. Evonik Industries AG

- 10.6. BASF SE

- 10.7. Clariant AG

- 10.8. Ashland Global Holdings Inc.

- 10.9. Elementis plc

- 10.10. Innospec Inc.

- 10.11. Others.

- 10.1. Givaudan SA

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 79

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Givaudan SA

- Firmenich SA (dsm-firmenich)

- Symrise AG

- Croda International Plc

- Evonik Industries AG

- BASF SE

- Clariant AG

- Ashland Global Holdings Inc.

- Elementis plc

- Innospec Inc.

- Others

FAQs

The key players in the market are Givaudan SA, Firmenich SA (dsm-firmenich), Symrise AG, Croda International Plc, Evonik Industries AG, BASF SE, Clariant AG, Ashland Global Holdings Inc., Elementis plc, Innospec Inc., Others.

Government regulations and independent certification frameworks constitute dual complementary forces shaping the bio-based cosmetics ingredient market through distinct but mutually reinforcing mechanisms. Regulatory restriction—through the EU Cosmetics Regulation restricted substances list, MoCRA-enabled FDA ingredient authority, California Toxic-Free Cosmetics Act, and equivalent national frameworks—creates mandatory bio-based ingredient adoption floors by prohibiting specific synthetic alternatives, with the regulatory list of restricted cosmetic ingredients expected to expand progressively through the forecast period as safety assessment frameworks, including the EU’s SCCS (Scientific Committee on Consumer Safety), complete evaluations of additional synthetic cosmetic ingredient categories. Certification frameworks including COSMOS Organic and Natural, NaTrue, USDA Organic, Ecocert, and the NSF Certified for Sport program for sports nutrition crossover products provide voluntary but commercially powerful market access credentials that enable brands to command price premiums, achieve retail shelf placement in clean beauty zones, and substantiate natural ingredient claims with third-party verification that reduces greenwashing litigation risk and builds consumer trust. The interplay between regulatory minimum requirements and certification premium positioning creates a tiered market structure in which compliance with regulatory restrictions is the cost of market access while certification achieves the brand premium positioning and retail channel access that generates the margin to justify continued bio-based ingredient investment — a structure that sustainably drives both market breadth and market value growth simultaneously across the forecast period.

Bio-based cosmetic ingredients exhibit extraordinary price range diversity — from commodity bio-surfactants including coconut-derived sodium lauryl sulfate at USD 1.50–3.00 per kilogram to ultra-premium rare botanical extracts including Bulgarian rose otto at USD 4,000–8,000 per kilogram — with price stratification reflecting both the scarcity and complexity of bio-based ingredient sourcing and production and the premium willingness-to-pay of cosmetics consumers for bio-derived active credential narratives. Certified organic versions of commodity botanical ingredients command 30–80% premiums over non-certified equivalents, while Cosmos Organic certified status enables an additional 15–25% pricing advantage in European retail channels where certification is increasingly expected as a baseline standard for natural claims substantiation. Fermentation-derived premium actives including cosmetic-grade hyaluronic acid trade at USD 80–400 per kilogram depending on molecular weight specification and purity, representing substantial premiums over synthetic humectants they replace but economically justified by the clinical efficacy data and consumer demand for bio-derived hyaluronic acid specifically. The price premium for bio-based over synthetic ingredients is gradually compressing in commodity ingredient categories as bio-based production scales—bio-surfactants from sugar fermentation are approaching price parity with petroleum-derived equivalents in several product categories—while maintaining or expanding in premium active ingredient categories where bio-derived origin and fermentation-derived precision remain sustained sources of formulation differentiation and consumer value.

Based on current analysis, the market is projected to reach approximately USD 18.93 billion by 2035, driven by regulatory tightening of synthetic ingredient acceptability across major markets progressively mandating bio-based substitution, precision fermentation scaling enabling bio-identical active ingredient production at cost-competitive pricing, the K-beauty and J-beauty global influence expanding fermentation and botanical ingredient adoption into North American and European mass market formulations, marine biotechnology commercialization providing novel bioactive ingredient categories, upcycled ingredient platforms expanding the raw material base and sustainability credential portfolio for bio-based ingredient innovation, and the geographic expansion of premium and prestige beauty consumption into China, India, and Southeast Asia creating new large-scale bio-based ingredient demand centers, at a CAGR of 11.1% from 2026 to 2035.

Europe is expected to maintain the highest revenue share through the early forecast years, holding approximately 31% of global market revenue by 2030, before Asia Pacific progressively narrows the gap and potentially surpasses European market value by approximately 2033 given the significant differential in regional growth rates. Europe’s sustained leadership reflects its position as the global benchmark for natural cosmetics certification, the most comprehensive regulatory mandate for bio-based ingredient adoption, and the concentration of both leading bio-based ingredient producers and the world’s most sophisticated natural beauty brands in the region, sustaining premium pricing and high-value formulation adoption that maintain European per capita bio-based ingredient revenue well above any other regional market.

Asia Pacific is expected to grow at the fastest CAGR of 13.6% from 2026 to 2035, driven by China’s bio-based cosmetics ingredient market growing at approximately 15.2% CAGR from extraordinary prestige beauty market growth and regulatory facilitation of traditional botanical ingredients, South Korea’s K-beauty-driven global influence on fermentation and botanical ingredient adoption, Japan’s fermentation technology leadership in cosmetic bio-actives, and India’s rapidly growing organized beauty retail market expanding consumer access to premium bio-based formulated products. The combination of deep cultural heritage aligning with bio-based ingredient narratives across traditional Asian beauty philosophies and rapidly modernizing consumer markets creates a uniquely powerful demand environment for bio-based cosmetic ingredient growth unmatched in any other regional market.

The Global Bio-Based Cosmetics and Personal Care Ingredients Market is predicted to experience substantial growth driven by 71% of global beauty consumers reading ingredient labels in 2024 versus 48% in 2019 representing a structural clean beauty behavioral shift; bio-based ingredients growing from 26% to 38% of total cosmetics ingredient market value between 2020 and 2025 demonstrating accelerating market share gains; the EU Cosmetics Regulation’s restriction list of over 1,400 prohibited synthetic ingredients creating mandatory reformulation demand; MoCRA’s expanded FDA authority representing the most significant U.S. cosmetics regulatory reform since 1938 with progressive synthetic ingredient restriction implications; the global skin care market projected to reach USD 240.8 billion by 2030 growing at 8.4% CAGR in premium segments where bio-based formulation adoption is most concentrated; precision fermentation enabling bio-identical and bio-novel active ingredient production at commercial scale including hyaluronic acid at 6,500 tonnes annually and bio-based squalane displacing shark-derived and petrochemical alternatives; marine cosmetics ingredients growing at 15.8% CAGR from unique bioactive compound profiles and compelling aquaculture sustainability credentials; and upcycled beauty ingredient certification frameworks creating verifiable sustainability claims that generate strong consumer purchase intent.