Centrifugal High-Speed Separators Market Size, Trends and Insights By Type (Disc Stack Separators (Self-Cleaning and Manual Discharge), Decanter Centrifuges (2-Phase and 3-Phase), Tubular Bowl Centrifuges, Basket Centrifuges, Other Types (Nozzle Centrifuges, Scroll Centrifuges)), By Application (Liquid-Solid Separation, Liquid-Liquid Separation, Liquid-Liquid-Solid Separation (Three-Phase), Clarification, Other Applications (Concentration, Washing)), By End-Use Industry (Food & Beverage (Dairy, Edible Oils, Beverages, Starch), Pharmaceutical & Biotechnology, Oil & Gas (Upstream, Midstream, Downstream), Chemical Processing, Wastewater Treatment & Environmental, Marine (Fuel Oil Treatment, Bilge Water), Other Industries (Mining, Pulp & Paper)), By Operation Mode (Continuous, Batch), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Europe |

Major Players

- Alfa Laval AB

- GEA Group AG

- Andritz AG

- Flottweg SE

- Others

Reports Description

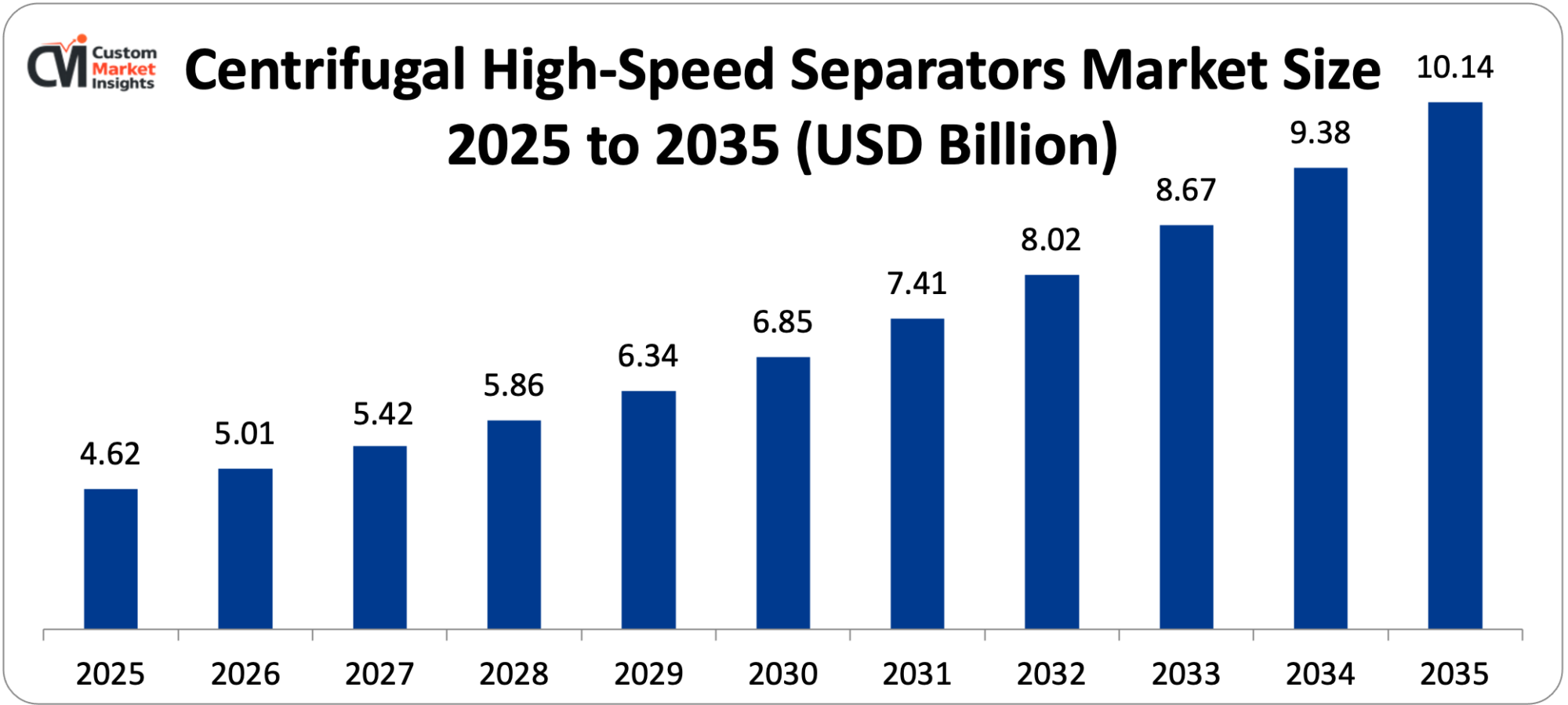

The market size of the global centrifugal high-speed separators is estimated at USD 4.62 billion in 2025 and is expected to grow between USD 5.01 billion in 2026 and about USD 10.14 billion in 2035 at a rate of CAGR of 7.3%. The increase in demand for high-efficiency separation technologies in the food and beverage processing and pharmaceutical manufacturing industries and the industrial wastewater treatment industry, as well as the increasing use of continuous separation processes in place of batch operations to enhance production throughput and consistency in product quality, are driving sustained and robust growth in the market over the forecast period.

Market Highlight

- Europe was the largest market shareholder in centrifugal high-speed separators with a market share of 34% in 2025.

- Asia-Pacific will grow with the highest CAGR of 9.6% in 2026-2035.

- By type, the disc stack separators are capturing about 44% of the market share in 2025.

- By type, the decanter centrifuge segment is increasing at the highest CAGR of 8.8% between 2026 and 2035.

- By category, the greatest market share of 47% in 2025 was attributed to the liquid-solid separation segment, and the liquid-liquid-solid separation segment is projected to have the fastest CAGR of 9.4% throughout the forecasted years 2026 to 2035.

- By end-use industry, the food and beverage segment had the greatest market share of 32% in 2025 with the pharmaceutical and biotechnology segment projected to have the highest CAGR between 2026 and 2035.

- By operation mode, the continuous segment had gained 68% market share in 2025.

Significant Growth Factors

The Centrifugal High-Speed Separators Market Trends present significant growth opportunities due to several factors:

- Food and Beverage Processing Industry Expansion Driving High-Throughput Separation Demand:

The ever-growing globalization of the food and beverage processing sector, with the increasing human population, the accelerating urbanization process that shifts food preparation to packaged and processed food items, the premiumization of food and beverage categories that necessitate more technologically advanced processing equipment, and the widening of the global dairy trade that links production regions with consumption markets across the intercontinental supply chains are all structural causal antecedents of centrifugal high-speed separator demand as virtually every major food and beverage processing category requires centrifugal separation as a processing step.

The greatest application of centrifugal separators to the food industry, with dairy processing, where high-speed disc stack centrifuges are used to separate cream and skim milk at flow rates of 20,000-100,000 liters per hour, being one of the earliest and most established industrial centrifuge applications, is dairy processing, where large-scale dairy production and modernisation of dairy processing facilities are driving considerable equipment demand. Published market research estimates the global dairy market was estimated to be USD 718 billion in 2023 and the production and processing capacity of dairy is growing at an exceptionally high rate especially in emerging market economies such as India, the largest milk producer in the world, China and Southeast Asia as the growing incomes increase consumption of dairy products. Another food preparation application involving large volumes of centrifugal separators and thus a large-volume food application is edible oil processing which involves centrifugal separators to remove impurities, water, and fine solids of crude vegetable oils such as palm, soybean, sunflower, and canola oils with multiple refining processes yielding a sustained demand on high-capacity centrifugal separation equipment at an oil processing facility.

The craft beverage revolution – which has seen the explosive growth of craft beer, high-end spirits, cold-pressed juice, and specialty coffee production around the world – has led to the need for smaller, application-specific centrifugal separators with the capacity to handle the broad range of raw materials and process demands presented by the artisanal beverage production at throughputs less than those typified by conventional industrial-scale centrifugal transport units. Fruit juice clarification Fruit juice clarification (where centrifugal separators are used to remove pulp, pectin and fine suspended solids in fresh-pressed juice to gain the desired clarity and stability necessary to commercially pack the juice product) is another developing application area due to the expansion of the health beverage market across the world and the need to replace the concentrate based production of juice with a not-from-concentrate based production method that demands more advanced processing facilities.

- Biopharmaceutical Manufacturing Expansion Creating Premium Separator Demand:

Even though the characteristics of the biopharmaceutical manufacturing industry have played a role in the tremendous increase in centrifugal high-speed separator demand in recent years, biopharmaceutical manufacturing may be seen as an emerging market offering the greatest utility of centrifugal high-speed separators, as operations within both biosimilar and recombinant biologic manufacturing sectors (such as cell harvesting, cell debris clarification, and continuous downstream processing) demand centrifugal separation equipment meeting pharmaceutical grade construction, cleanability, and performance requirements. Monoclonal antibody production, which is the most common type of biopharmaceutical product with an annual global market in the range of USD 200 billion, involves centrifugal separation in two major unit operations, namely cell harvesting at the end of the bioreactor culture phase to separate viable cells and culture broth and clarification of the harvested cell culture fluid to eliminate cellular debris and fine particles prior to chromatographic purification.

The combination of high throughput and high cell and debris removal efficiency demanded by industrial-scale production of monoclonal antibodies at bioreactor volumes of 2,000-25,000 liters is achieved by high speed disc stack centrifuges where centrifugal forces of 5,000 -14,000 xG are produced by centrifugal force acting upon the disc stack centrifuge at velocities of 8,000-12,000 RPM. Large biopharmaceutical manufacturers such as Roche, AbbVie, Amgen, Regeneron, and Samsung Biologics have several manufacturing sites worldwide whose centrifuge capacity is tailored to their production volumes, and with every new suite of bioreactors, a centrifugal separator capital investment of USD 500,000-USD 3 million per separation train is required based on equipment scale and configuration.

The increasing use of continuous bioprocessing where traditional batch bioreactor processes are substituted with continuous perfusion bioreactors and integrated continuous downstream processing is placing pressure on continuous cell retention centrifuges and high-performance clarification separators that can handle continuous streams of generated culture fluids, a technically more challenging and high value separator application than the conventionally used batch cell harvesting. New biosimilar manufacturing facilities are under construction around the world due to the biosimilar manufacturing market, which is expanding as a result of the expiry of patents on original biologic drugs, creating commercial opportunities for the production of inexpensive biosimilar versions, and the sector of bioreactor and downstream processing capacity is being constructed which requires high levels of centrifugal separator purchase.

What are the Major Advances Changing the Centrifugal High-Speed Separators Market Today?

- Digital Integration and Intelligent Separator Control Systems:

The digital monitoring technologies, high-speed separator operation, and predictive maintenance analytics transformation are enabling separator operators to attain higher separation efficiency, less energy use, decreased product loss, and elimination of unplanned equipment downtime — transforming separator management from an operator intervention dependent process to an automated, data-driven process optimization that keeps the separator performing optimally at any feed condition. Existing high-speed separators by major manufacturers such as Alfa Laval, GEA Group, Andritz, and Flottweg are also set up with increased digital control systems and sensor suites that track the parameters of bowl speed, vibration signatures, bearing temperature, and changes in motor current and outlet flow quality parameters as the feed composition and feed rate change, becoming standard provisions to ensure that optimum separation performance is maintained. Predictive maintenance capability Predictive maintenance capability in which AI algorithms based on the historical data on the operation of a separator and history of failures detect developing indicators of bearer wear, imbalance, and seal deterioration using vibration and temperature sensor data prior to causing separator failure is under implementation into separator monitoring platforms by larger equipment manufacturers, with published implementation experience with food and beverage processing customers showing 30% to 50% rates of reduction in unplanned separator downtime following the introduction of predictive maintenance system usage.

The combination of separator control systems and plant-level distributed control systems (DCS) and manufacturing execution systems (MES) allows separator operation to be synchronized with upstream and downstream process equipment through automated production processes. — is promoting centrifugal separator application in highly automated continuous food processing, pharmaceutical manufacturing, and chemical production processes where the use of manual equipment arbitrarily limits the scope of process automation. The Separator Monitoring Service of Alfa Laval, a remote monitoring system that provides real-time visibility of separator performance, automated alarm handling, and remote diagnostic assistance to engineers with Alfa Laval service, is the most commercially developed version of the digital separator monitoring services, whereby the platform allows proactive service intervention before the quality of products or the continuity of the process is adversely impacted by separator performance.

- Hygienic Design Advancement for Pharmaceutical and Food Grade Applications:

The ongoing development of hygienic centrifugal separator design, which includes the development of internal surface finish, the removal of crevices and dead areas in products, greater clean-in-place/sterilize in place capabilities, and mechanical seal system development that avoids contamination of the product, is in areas of pharma and food where the last generation of centrifugal separator design was not able to meet regulatory requirements in hygiene. Pharmaceutical grade centrifugal separators verified to meet ASME standards of BPE (Bioprocessing Equipment) and GMP manufacturing standards and USP 1116 standards of cleanroom compatibility – internal product contact surfaces with electropolished finish of Ra less than 0.5m that reduces microbial adhesion and enables easy verification of complete cleaning, with all product contact materials being 316L stainless steel or pharmaceutical grade equivalent alloys, and with certified material traceability documentation.

The creation of fully hermetically sealed centrifuge designs, whereby the product-contacting bowl and feed systems are fully enclosed in an inert atmosphere, resulting in zero contact with oxygen of delicate biological or specialty chemical products that would otherwise be destroyed by oxidation, is increasing the use of centrifugal separators in pharmaceutical and specialty chemical applications where contact with oxygen would have caused oxidative degradation of the product. Increased CIP/SIP capacity – allowing all product contact surfaces to be in-place cleaned and steam sterilized without product separator dismantling – is shortening the separator turnaround time between product lots in pharmaceutical manufacturing operations, improving equipment utilization and decreasing the manual labor input into separator cleaning validation, which is a considerable operating cost in GMP operations. The separator standards of the 3-A Sanitary Standards organization, commonly used in U.S. regulatory compliance in dairy and food processing as an element of regulatory compliance, and the EHEDG (European Hygienic Engineering and Design Group) certification requirements in the European food processing industries are increasing the continuous improvement of the hygienic design through the provision of measurable standards against which compliance must be demonstrated to major food processing purchasers having mandatory hygienic design procurement specifications.

- Energy Efficiency Optimization and Sustainable Separator Operation:

The increased focus on energy efficiency in industrial processing due to the increasing energy costs, corporate net-zero-emission policies, and the demand by regulatory bodies to reduce the specific energy consumption of centrifugal high-speed separators, which constitute some of the most energy-intensive unit operations in food and chemical processing due to the high rotational rates and continuous operation typical of high-speed centrifuge applications, is driving significant engineering investment into lowering the specific energy consumption of centrifugal high-speed separators Energy consumption due to centrifugal separators

The motor powering rotations in the bowl is a dominant source of energy consumption – large industrial disc stack separators (1575 kW continuous electrical power) are used depending on the bowl diameter and rotational rate – making adjustment of motor frequency and power consumption a primary source of energy efficiency improvement leverage, with VFD-controlled separators functioning dynamically at the current actual feed flow rate and with varying power consumption depending on the actual separation requirement. The most technically sophisticated centrifuge models are adopting magnetic bearing technology, where traditional rolling element bearings are being replaced with frictionless electromagnetic bearing systems, which hold the rotating bowl assembly in suspension without mechanical contact and do not need any lubrication oil, which introduces a risk of product contamination and results in servicing costs, or allows faster rotation speeds, which do not increase energy consumption in the separator in direct relationship with that rotation rate.

The introduction of better bowl geometry and internal feed distribution system designs based on a computational fluid dynamics model to optimize the flow patterns in the rotating bowl and reduce the turbulent energy dissipation, which decreases the separation efficiency, is permitting new separator designs to operate at lower rotational speeds and with the resulting lower energy consumption than the previous designs. The published energy benchmarking data of GEA Group on its dairy separator product line records energy consumption savings of 20-35% of its current generation separators amongst the same customers as the previous product generation, which shows that sustained engineering investment into the energy efficiency of its centrifugal separators is enhancing the lifecycle economics of centrifugal separator investment in the energy-sensitive customers of food and industrial processing.

Category Wise Insights

By Type

Why Do Disc Stack Separators Lead the Market?

The disc stack separators are the largest type segment with an approximate market share of 44% of total market share in 2025, which is indicative of their dominant role across the entire range of centrifugal separation applications of the highest volume and the highest value, such as dairy processing, edible oil refining, pharmaceutical clarification, and marine fuel oil cleaning – applications where the disc stack design combination of extraordinarily high separation efficiency at very high volumetric throughput, continuous self-cleaning operation through automated desludging and lower physical footprint in relation to separation capacity makes The principle of operation of the disc stack separator – where a stack of conical discs rotating at 4,000-12,000 RPM forms a stack of thin separation channels that significantly decreases the settling distance that particles need to travel prior to contacting a solid surface and enhances the ability to separate particles as small as 0.5 micrometers and liquid phases with small density differences, such as 10 kg/m³, at continuous feed flow rates of 1,000-100,000 liters per hour depending on the size of the self-cleaning disc stack separator- where built up solids are automatically removed via the release of a hydraulically controlled valve at the bowl periphery- allows uninterrupted 24-hour liquid solids separation without operator action, and this type of arrangement is the default of large-scale continuous industrial solids processing applications. Additional installed base products, Alfa Laval and GEA Group combined, control most of the market share in the disc stack separators industry, and their global service networks offer the aftermarket parts and maintenance services that establish customer retention benefits that installed base leadership.

By Application

Why Does Liquid-Solid Separation Lead the Market?

Liquid-solid separation is the largest segment of the market with the greatest market share of about 47% in 2025 due to the intrinsic presence of solid liquid separation needs in fundamentally all industrial processing segments – such as the elimination of cell biomass in fermentation culture broth in pharmaceutical bioprocessing and the dewatering of mineral slurries in mining processes, clarifying of fruit juice of suspended pulp and pectin and starch separation in process water in starch manufacturing as well as the removal of suspended solids in industrial wastewater before dis The fact that liquid-solid separation is applicable to all industrial processes, and the proven superiority of centrifugal separation over other technologies such as filtration, gravity settling, and flocculation in terms of separation efficiency, throughput capacity, ability to operate continuously, and more minimal dependency of chemical addition, makes this application the primary application platform of the centrifugal separator market. The pharmaceutical and biotechnology use of liquid-solid separation – cell harvesting and clarification in the manufacturing process of biopharmaceuticals – generates the highest per-unit revenue of the liquid-solid separation segment due to the pharmaceutical grade construction specifications, sterilizable design requirements, and the documentation of the process performance that would require premium prices of the pharmaceutical grade separators at 2-4 times the cost of an equal grade product in industrial application.

By End-Use Industry

Why Does Food & Beverage Lead the Market?

Food and beverage processing is the largest end-use market with about 32% of total market share in 2025 as it is a combination of the highest installed base of centrifugal separators worldwide – accrued during the more than a century of centrifuge use in dairy and beer processing and edible oil refining – the constant replacement requirements of equipment, and the greatest diversity of centrifuge applications within a single industry segment. Dairy processing, including milk standardization, cream separation, concentration of whey proteins, cheese production, and infant formula production, results in the highest food industry food processing demand of high-speed disc stack separators with milk separation lines at larger dairy plant facilities having multiple high-speed disc stack separators operating in parallel to meet the demand required. The dairy processing equipment, including centrifugal separators, pilots its overall market growth with the growth in dairy capacity in Asia and the Middle East and with equipment modernization at developed dairy plants in Europe, North America, and Oceania. Brewing and fermentation uses – such as decanting beer of yeast, processing wort, sedimentation of fermentation byproducts, and so on – create large-scale demand from the world brewing sector, and the rise of craft breweries creates smaller-scale demand on separators, as well as the large industrial brewing markets previously served by high-capacity disc stack systems.

By Operation Mode

Why Does Continuous Operation Lead the Market?

Continuous operation is the widest mode with about 68% market share in 2025 due to an inherent inclination towards continuous separation processes in large-scale industrial operations where the throughput needs, consistency of product quality goals and economics of operation are highly favoured to continuous rather than batch processing. The continuous centrifugal separation, which introduces feed continuously and discharges separator phases continuously as long as the process continues, has a higher production throughput per unit of installed separator capacity, eliminates the variability in product quality between batches that comes with batch separation, and decreases the number of operators required because it eliminates the batch cycle loading/unloading process and thus can be integrated into fully continuous production systems in food, chemical, and pharmaceutical production facilities where batch processing is a bottleneck that cannot be used with continuously running upstream and downstream operations.

The adoption of continuous centrifugal separation in pharmaceutical bioprocessing is particularly being driven by the trend towards continuous pharmaceutical manufacturing: actively facilitated by the emerging technology program of the FDA and supported by the awareness of quality, cost, and throughput benefits of continuous centrifugal separation by the pharmaceutical industry, the perfusion bioreactor format characteristic of continuous upstream bioprocessing is being adopted.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 5.01 billion |

| Projected Market Size in 2035 | USD 10.14 billion |

| Market Size in 2025 | USD 4.62 billion |

| CAGR Growth Rate | 7.3% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Application, End-Use Industry, Operation Mode and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

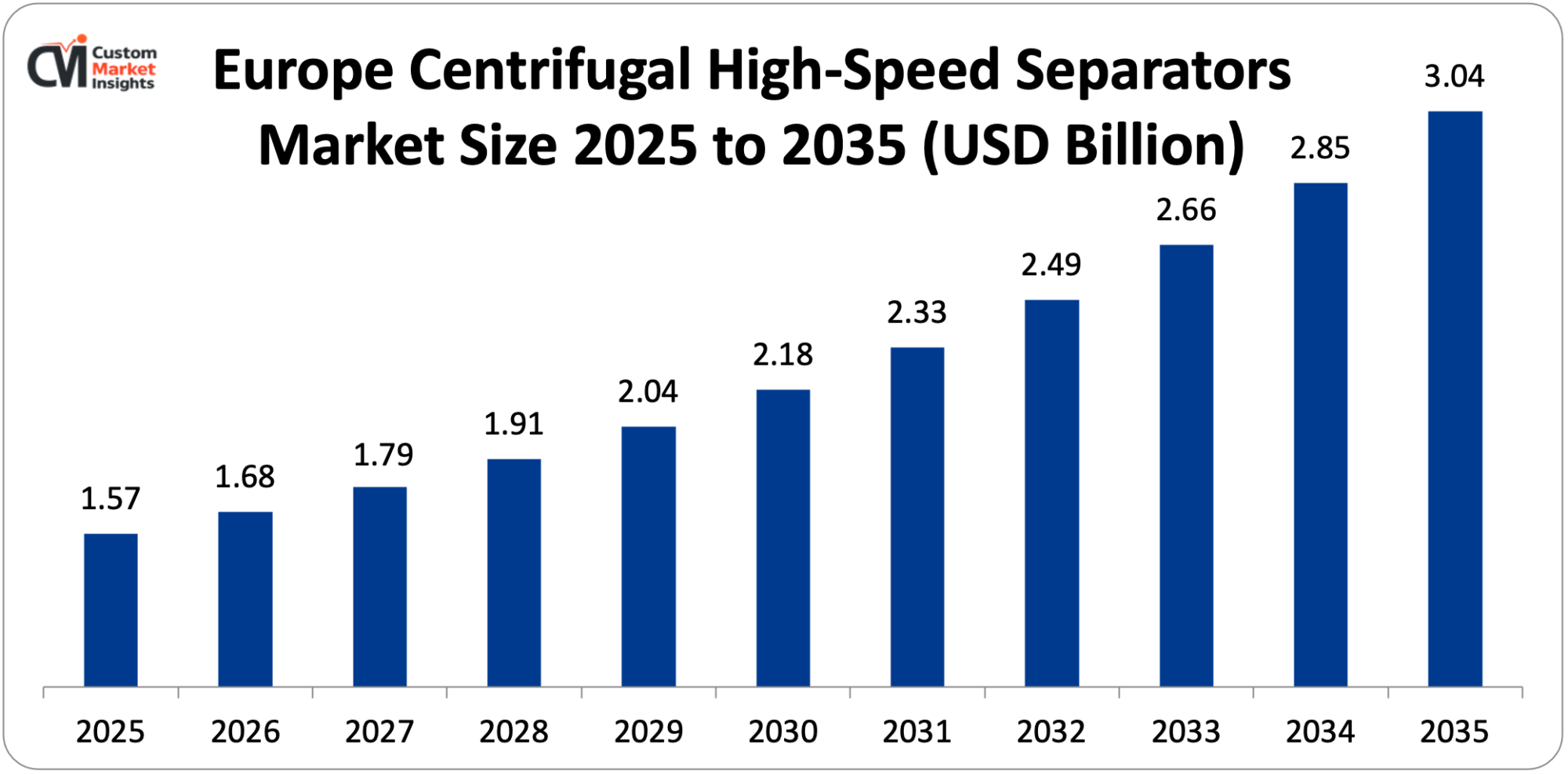

How Big is the Europe Market Size?

The European centrifugal high-speed separators market size is estimated at USD 1.57 billion in 2025 and is projected to reach approximately USD 3.04 billion by 2035, with a CAGR of 6.8% from 2026 to 2035.

Why Did Europe Dominate the Market in 2025?

Europe controls nearly 34% of world markets in 2025, because it has historically been the location of the industrial centrifugal separation technology and the world leaders in separator manufacturing (Alfa Laval, Sweden; GEA Group, Germany; Andritz, Austria; Flottweg, Germany; and Pieralisi, Italy), whose presence in the world market, knowledge in application engineering, and extensive global aftermarket service systems position the European manufacturers as the competitive force in the global market of high-speed separators.

The manufacturing capacity of separators is so concentrated in Germany that the GEA Group, including the separator division in Oelde, the manufacturing facility of Flottweg in Vilsbiburg, and dozens of specialist centrifuge component and service firms in the larger German industrial machinery system, the German manufacturing center is the most significant single national centrifuge manufacturing space in the world, with German-manufactured separators being exported to all end-use markets. The high and mature food and beverage processing sector of Europe, encompassing the most advanced dairy processing sectors in the world, the largest consumer of three-phase decanter centrifuges of which is situated in the Mediterranean olive oil processing industry, and the high-end brewing and beverage processing sector of Europe are the source of the largest concentration of installed separator capacity and the resultant aftermarket parts, maintenance, and equipment replacement demand worldwide.

The pharmaceutical production facilities of the European pharmaceutical and biotechnology industry, headquartered in Germany, Switzerland, Ireland, the UK, and Denmark, command some of the most sophisticated biopharmaceutical manufacturing plants in the world and provide a huge demand on the region’s established separator manufacturers with specific pharmaceutical product lines.

Why is Asia Pacific the Fastest-Growing Market?

Asia Pacific is the quickest expanding regional market with a predicted CAGR of 9.6% in the next 2026-2035 due to the rapid increase in food and beverage processing capacity in China, India, Southeast Asia and Australia to cater to a growing and increasingly wealthy consumer base; the build-up of biopharmaceutical manufacturing capacity in South Korea, China, India, and Singapore to position Asia Pacific as a global manufacturing contract manufacturing center in biologics, the increasing investment in wastewater treatment infrastructure development in urbanizing Asian economies, which implement increasingly strict industrial effluent standards, and the growth of marine separator demand driven by Asia Pacific’s dominant position in global shipbuilding — along with South Korean, Chinese and Japanese shipyards as the largest producers of new commercial ships that need the fuel oil treatment and bilge water separating systems. Modernization of the food processing industry in China is creating significant investment in modern centrifugal separation equipment in dairy, edible oil, starch, and beverage processing industries as a result of modernization of their food processing industry weighed down by government food safety improvement programs and the high growth in organized food retail supply chains bridging centralized food processing plants into urban supermarket chains. The growing dairy industry in India, India being the largest producer of annual milk in the world, and domestic dairy processing capacity is rapidly modernizing with the pressure of cooperative dairy organizations such as Amul and the National Dairy Development Board, resulting in increasing demand of modern high-speed dairy separators, as the traditional open-pan forms of processing are being superseded by continuous automated processing facilities.

Why is North America Experiencing Steady Growth?

The steady growth of the United States (estimated CAGR of 6.4% between 2026 and 2035) is also driven by the large installed base of centrifugal separators used in dairy processing, ethanol production, mining and pharmaceutical manufacturing in North America, which creates consistent demand in centrifuge replacements and upgrade demand, the growing U.S. biofuel manufacturing consumption in biopharmaceutical manufacturing, which is introducing new biologics manufacturing facilities that necessitate the need to procure pharmaceutical grade centrifuges, the expansion of U.S. renewable fuel production — including corn ethanol, soybean biodiesel, and emerging cellulosic biofuel — generating centrifuge demand for stillage dewatering, oil extraction, and process water clarification, and the continued investment in municipal wastewater treatment infrastructure upgrades mandated by EPA effluent quality requirements.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region is characterized by the emerging market growth due to the increasing investment of Gulf Cooperation Council in food processing and the dairy industry in favor of import substitution through increasing investments in the oil and gas sector in the Middle East in support of food security programs, pharmaceutical manufacturing development aspirations proposed by Saudi Arabia and the UAE in support of its oil and gas industry, the high level of centrifuge demand generated by the large oil and gas sector in the Middle East, the urbanization process in Sub-Saharan Africa with the resulting need to provide centrifuge services to large cities such as Lagos, Nairobi, and Johannesburg, and Brazil’s large food processing, sugarcane ethanol, and mining industries generating centrifuge demand across multiple application categories.

Top Players in the Market and Their Offerings

- Alfa Laval AB

- GEA Group AG

- Andritz AG

- Flottweg SE

- Pieralisi Group

- Tomoe Engineering Co. Ltd.

- Mitsubishi Kakoki Kaisha Ltd.

- IHI Corporation

- HAUS Centrifuge Technologies

- Hiller GmbH

- Rousselet Robatel

- Others

Key Developments

The market has undergone significant developments as industry participants seek to advance digital separator capabilities, expand pharmaceutical grade product lines, and respond to growing demand from biopharmaceutical manufacturing and sustainable processing applications.

- In October 2024: Alfa Laval declared the launch of its ALDEC G3 line of decanter centrifuges with a new high-torque gearbox design and improved variable frequency drive motor control system that was 22% lower in specific energy consumption per tonne of handled material than the predecessor ALDEC G2 series over the standard wastewater biosolids dewatering process.

- In February 2025: GEA Group declared the commercial introduction of its Westfalia Separator pharma disc centrifuge series with improved continuous sterilization-in-place functionality – allowing entire SIP cycles to be completed in less than 45 minutes (instead of 90 to 120 minutes) by the earlier designs – in particular, the biopharmaceutical cell harvesting and clarification market, where the efficiency of manufacturing campaign schedules directly depends on the turnaround time of the separator between manufacture batches.

The Centrifugal High-Speed Separators Market is segmented as follows:

By Type

- Disc Stack Separators (Self-Cleaning and Manual Discharge)

- Decanter Centrifuges (2-Phase and 3-Phase)

- Tubular Bowl Centrifuges

- Basket Centrifuges

- Other Types (Nozzle Centrifuges, Scroll Centrifuges)

By Application

- Liquid-Solid Separation

- Liquid-Liquid Separation

- Liquid-Liquid-Solid Separation (Three-Phase)

- Clarification

- Other Applications (Concentration, Washing)

By End-Use Industry

- Food & Beverage (Dairy, Edible Oils, Beverages, Starch)

- Pharmaceutical & Biotechnology

- Oil & Gas (Upstream, Midstream, Downstream)

- Chemical Processing

- Wastewater Treatment & Environmental

- Marine (Fuel Oil Treatment, Bilge Water)

- Other Industries (Mining, Pulp & Paper)

By Operation Mode

- Continuous

- Batch

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Centrifugal High-Speed Separators by Segments

- 2.1.2. Centrifugal High-Speed Separators by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Centrifugal High-Speed Separators Market Attractiveness Analysis, By Type

- 2.2.3. Centrifugal High-Speed Separators Market Attractiveness Analysis, By Application

- 2.2.4. Centrifugal High-Speed Separators Market Attractiveness Analysis, By End-Use Industry

- 2.2.5. Centrifugal High-Speed Separators Market Attractiveness Analysis, By Operation Mode

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Food and Beverage Processing Industry Expansion Driving High-Throughput Separation Demand

- 3.1.2. Biopharmaceutical Manufacturing Expansion Creating Premium Separator Demand

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Centrifugal High-Speed Separators Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Centrifugal High-Speed Separators Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Disc Stack Separators (Self-Cleaning and Manual Discharge)

- 4.1.3. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Decanter Centrifuges (2-Phase and 3-Phase)

- 4.1.7. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Tubular Bowl Centrifuges

- 4.1.11. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Basket Centrifuges

- 4.1.15. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Other Types (Nozzle Centrifuges, Scroll Centrifuges)

- 4.1.19. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Centrifugal High-Speed Separators Market – By Application

- 5.1. Application Market Overview, By Application Segment

- 5.1.1. Centrifugal High-Speed Separators Market Revenue Share, By Application, 2025 & 2035

- 5.1.2. Liquid-Solid Separation

- 5.1.3. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Liquid-Liquid Separation

- 5.1.7. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Liquid-Liquid-Solid Separation (Three-Phase)

- 5.1.11. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Clarification

- 5.1.15. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Other Applications (Concentration, Washing)

- 5.1.19. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Application Market Overview, By Application Segment

- Chapter 6. Centrifugal High-Speed Separators Market – By End-Use Industry

- 6.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 6.1.1. Centrifugal High-Speed Separators Market Revenue Share, By End-Use Industry, 2025 & 2035

- 6.1.2. Food & Beverage (Dairy, Edible Oils, Beverages, Starch)

- 6.1.3. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Pharmaceutical & Biotechnology

- 6.1.7. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Oil & Gas (Upstream, Midstream, Downstream)

- 6.1.11. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Chemical Processing

- 6.1.15. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Wastewater Treatment & Environmental

- 6.1.19. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Marine (Fuel Oil Treatment, Bilge Water)

- 6.1.23. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1.26. Other Industries (Mining, Pulp & Paper)

- 6.1.27. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 6.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.29. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 7. Centrifugal High-Speed Separators Market – By Operation Mode

- 7.1. Operation Mode Market Overview, By Operation Mode Segment

- 7.1.1. Centrifugal High-Speed Separators Market Revenue Share, By Operation Mode, 2025 & 2035

- 7.1.2. Continuous

- 7.1.3. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Batch

- 7.1.7. Centrifugal High-Speed Separators Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Operation Mode Market Overview, By Operation Mode Segment

- Chapter 8. Centrifugal High-Speed Separators Market – Regional Analysis

- 8.1. Centrifugal High-Speed Separators Market Overview, By Region Segment

- 8.1.1. Global Centrifugal High-Speed Separators Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Centrifugal High-Speed Separators Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Centrifugal High-Speed Separators Market Revenue, By Type, 2026 – 2035

- 8.1.4. Global Centrifugal High-Speed Separators Market Revenue, By Application, 2026 – 2035

- 8.1.5. Global Centrifugal High-Speed Separators Market Revenue, By End-Use Industry, 2026 – 2035

- 8.1.6. Global Centrifugal High-Speed Separators Market Revenue, By Operation Mode, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Centrifugal High-Speed Separators Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Centrifugal High-Speed Separators Market Revenue, By Type, 2026 – 2035

- 8.2.3. North America Centrifugal High-Speed Separators Market Revenue, By Application, 2026 – 2035

- 8.2.4. North America Centrifugal High-Speed Separators Market Revenue, By End-Use Industry, 2026 – 2035

- 8.2.5. North America Centrifugal High-Speed Separators Market Revenue, By Operation Mode, 2026 – 2035

- 8.2.6. U.S. Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Centrifugal High-Speed Separators Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Centrifugal High-Speed Separators Market Revenue, By Type, 2026 – 2035

- 8.3.3. Europe Centrifugal High-Speed Separators Market Revenue, By Application, 2026 – 2035

- 8.3.4. Europe Centrifugal High-Speed Separators Market Revenue, By End-Use Industry, 2026 – 2035

- 8.3.5. Europe Centrifugal High-Speed Separators Market Revenue, By Operation Mode, 2026 – 2035

- 8.3.6. Germany Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Centrifugal High-Speed Separators Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Centrifugal High-Speed Separators Market Revenue, By Type, 2026 – 2035

- 8.4.3. Asia Pacific Centrifugal High-Speed Separators Market Revenue, By Application, 2026 – 2035

- 8.4.4. Asia Pacific Centrifugal High-Speed Separators Market Revenue, By End-Use Industry, 2026 – 2035

- 8.4.5. Asia Pacific Centrifugal High-Speed Separators Market Revenue, By Operation Mode, 2026 – 2035

- 8.4.6. China Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Centrifugal High-Speed Separators Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Centrifugal High-Speed Separators Market Revenue, By Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Centrifugal High-Speed Separators Market Revenue, By Application, 2026 – 2035

- 8.5.4. The Middle-East and Africa Centrifugal High-Speed Separators Market Revenue, By End-Use Industry, 2026 – 2035

- 8.5.5. The Middle-East and Africa Centrifugal High-Speed Separators Market Revenue, By Operation Mode, 2026 – 2035

- 8.5.6. Saudi Arabia Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Centrifugal High-Speed Separators Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Centrifugal High-Speed Separators Market Revenue, By Type, 2026 – 2035

- 8.6.3. Latin America Centrifugal High-Speed Separators Market Revenue, By Application, 2026 – 2035

- 8.6.4. Latin America Centrifugal High-Speed Separators Market Revenue, By End-Use Industry, 2026 – 2035

- 8.6.5. Latin America Centrifugal High-Speed Separators Market Revenue, By Operation Mode, 2026 – 2035

- 8.6.6. Brazil Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Centrifugal High-Speed Separators Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Centrifugal High-Speed Separators Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Centrifugal High-Speed Separators Market: Company Market Share, 2025

- 9.2. Global Centrifugal High-Speed Separators Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Alfa Laval AB

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. GEA Group AG

- 10.3. Andritz AG

- 10.4. Flottweg SE

- 10.5. Pieralisi Group

- 10.6. Tomoe Engineering Co. Ltd.

- 10.7. Mitsubishi Kakoki Kaisha Ltd.

- 10.8. IHI Corporation

- 10.9. HAUS Centrifuge Technologies

- 10.10. Hiller GmbH

- 10.11. Rousselet Robatel

- 10.12. Others.

- 10.1. Alfa Laval AB

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 37

List Of Tables

Tables No 1 to 51

Prominent Player

- Alfa Laval AB

- GEA Group AG

- Andritz AG

- Flottweg SE

- Pieralisi Group

- Tomoe Engineering Co. Ltd.

- Mitsubishi Kakoki Kaisha Ltd.

- IHI Corporation

- HAUS Centrifuge Technologies

- Hiller GmbH

- Rousselet Robatel

- Others

FAQs

The key players in the market are Alfa Laval AB, GEA Group AG, Andritz AG, Flottweg SE, Pieralisi Group, Tomoe Engineering Co. Ltd., Mitsubishi Kakoki Kaisha Ltd., IHI Corporation, HAUS Centrifuge Technologies, Hiller GmbH, Rousselet Robatel, Others.

The government regulations have a pervasive impact throughout the centrifugal high-speed separators market by food safety standards that govern the hygienic design of separators, pharmaceutical GMP standards that dictate the construction of the separator, the environmental regulations that force the demand of wastewater treatment separators, and the marine regulations that require the fuel oil treatment in commercial vessels and the bilge water separation equipment. The equipment design, material of construction, and cleaning requirements of the centrifugal separators, as specified by the U.S. FDA Current Good Manufacturing Practice regulations, i.e., 21 CFR Part 110 in respect of food processing and 21 CFR Parts 210 and 211 in respect of pharmaceutical manufacturing, provide compliance motivation to the operators to invest in contemporary hygienic centrifugal separator designs in accordance with the prevailing regulatory standards. Equivalent European food safety standards on food processing equipment such as centrifugal separators are set under the Food Hygiene Regulation 852/2004 of the EU and companion animal-origin food product Regulation 853/2004, which is administered by national food safety authorities such as the UK FSA, German BVL, and French ANSES, which identify the European market source of documentation of hygienic design compliance, which major food processor procurement specifications demand. The international maritime organization in their MARPOL Annex I rules – which forbids the discharge of an oily water mix with an oil content of above 15 ppm in machinery spaces of the ships – requires the oily water separating equipment to be installed on a commercial vessel with the IMO in their resolution MEPC.107(49) outlining the standards of performance that the bilge water treatment systems such as centrifugal separators should meet in order to have the ship certified under MARPOL rules.

The centrifugal high speed separator pricing has a wide range covering the difference in the equipment type, size, construction standard, and performance requirements in the market. Food processing Industrial disc stack separators Standard industrial disc stack separators, such as dairy cream separators, edible oil centrifuges, etc., in mid-range bowl sizes commonly cost USD 80,000 – USD 400,000 individually depending on throughput capacity and automation additions. Separators with large capacities and repeated high volumes: disc stack industrial separators with high-volume continuous processing applications such as the largest Alfa Laval and GEA dairy separators (100,000 liters per hour) cost USD 500,000-USD 1.2 million per unit. Pharmaceutical grade disc stack centrifuges to harvest and clarify biopharmaceutical cells — meets ASME BPE, GMP, and 3-A sanitary standards with full validation documentation support, costing USD 3 million per facility, depending on the size of the bowl used and the features that are included with each design — cost 2-4 times more than comparable industrial grade equipment that construction pharmaceutical requirements demand. Decanter centrifuges, which dewater biosolids in wastewater employing decanter centrifuges range between USD 100,000 and USD 600,000 per unit, and the acquisition of the biosolids to municipal wastewater treatment plants is normally competitive tender-based between a number of suppliers that moderate biosolids prices at the lower end of the range. The aftermarket parts and service market, including replacement wear parts (such as disc stacks, scroll conveyor flights, and mechanical seals) and preventive maintenance services (service contracts) and emergency service market, consists of about 35-45% of total market revenue across the installed bases of the major separator manufacturers, which provides a robust cycle of recurring market revenues partly counterbalancing the capital equipment revenue cyclicity during industrial investment cycles.

Existing analysis shows that the market is expected to grow to about USD 10.14 billion by 2035 due to the expansion of biopharmaceutical manufacturing capacity to maintain a decade-long growth cycle in the pharmaceutical segment of the segmentation of purchasing new centrifugal separators, with a CAGR of 7.3% between 2026 and 2035.

It is predicted that Europe will retain the largest revenue share of the rest of the world in the next five years with an estimated market share of about 34% of the global market share in 2025, based on the concentration of the world market leading centrifugal separator companies, including Alfa Laval, GEA Group, Andritz, and Flottweg, in the Swedish, German, Austrian, and Bavarian regions that form the global dairy, edible oil, and pharmaceutical processing industries with the largest number of centrifugal separator units installed with centrifugal separators at food, pharmaceutical, and industrial processing facilities, European manufacturers’ dominant global export position supplying high-performance separators to customers across all world regions, and the continued investment in new pharmaceutical grade and food grade separator product development concentrated at European R&D centers that maintains European technology leadership.

Asia Pacific is expected to achieve the highest CAGR of 9.6% over the forecast period due to the food processing modernization of China that is creating significant demand for dairy, edible oil, and beverage separators; India with the world’s largest milk production industry in the process of modernizing its processing infrastructure with modern high-speed separator equipment; South Korea with the biopharmaceutical contract manufacturing industry that is growing and necessitating pharmaceutical grade separator equipment procurement and tightening industrial wastewater discharge regulations that are increasing across the urbanizing Asian economies; and industrial centrifuge investment at new and expanding manufacturing facilities.

Growth in the Global Centrifugal High-Speed Separators Market is forecasted to be high mainly due to the world-wide dairy market of USD 718 billion in 2023 supporting the largest established centrifuge application that will have continued capacity expansion in India, China, and Southeast Asia, biopharmaceutical global sales approaching USD 200 billion annually with monoclonal antibody production necessitating centrifugal cell harvesting and fermentation broth clarification at each production facility, GEA Group and Alfa Laval documented improved energy consumption in 20–35% energy consumption improvements in current generation separator designs improving lifecycle economics for energy-cost-sensitive customers, the expanding alternative protein and precision fermentation industry creating new high-volume centrifuge demand for microalgae harvesting and fermentation broth processing, tightening industrial wastewater effluent standards across Asia, Europe, and North America driving decanter centrifuge investment for biosolids dewatering and industrial effluent treatment, the FDA’s continuous manufacturing initiative promoting continuous bioprocessing that requires continuous cell retention centrifuges, and digital predictive maintenance integration reducing unplanned separator downtime by 30–50% delivering compelling operational ROI that accelerates technology adoption decisions.