Medical Devices Market Size, Trends and Insights By Type (Orthopedic Devices, Diagnostic Imaging Devices, Cardiovascular Devices, In-vitro Diagnostic (IVD), Minimally Invasive Surgery Devices, Diabetes Care Devices, Wound Management, Ophthalmic Devices, Dental Devices, Nephrology Devices, General Surgery, Others), By End User (Hospitals & ASCs, Clinics, Others), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 7.1%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- Medtronic

- Abbott Laboratories

- Siemens Healthineers

- Stryker Corporation

- others

Reports Description

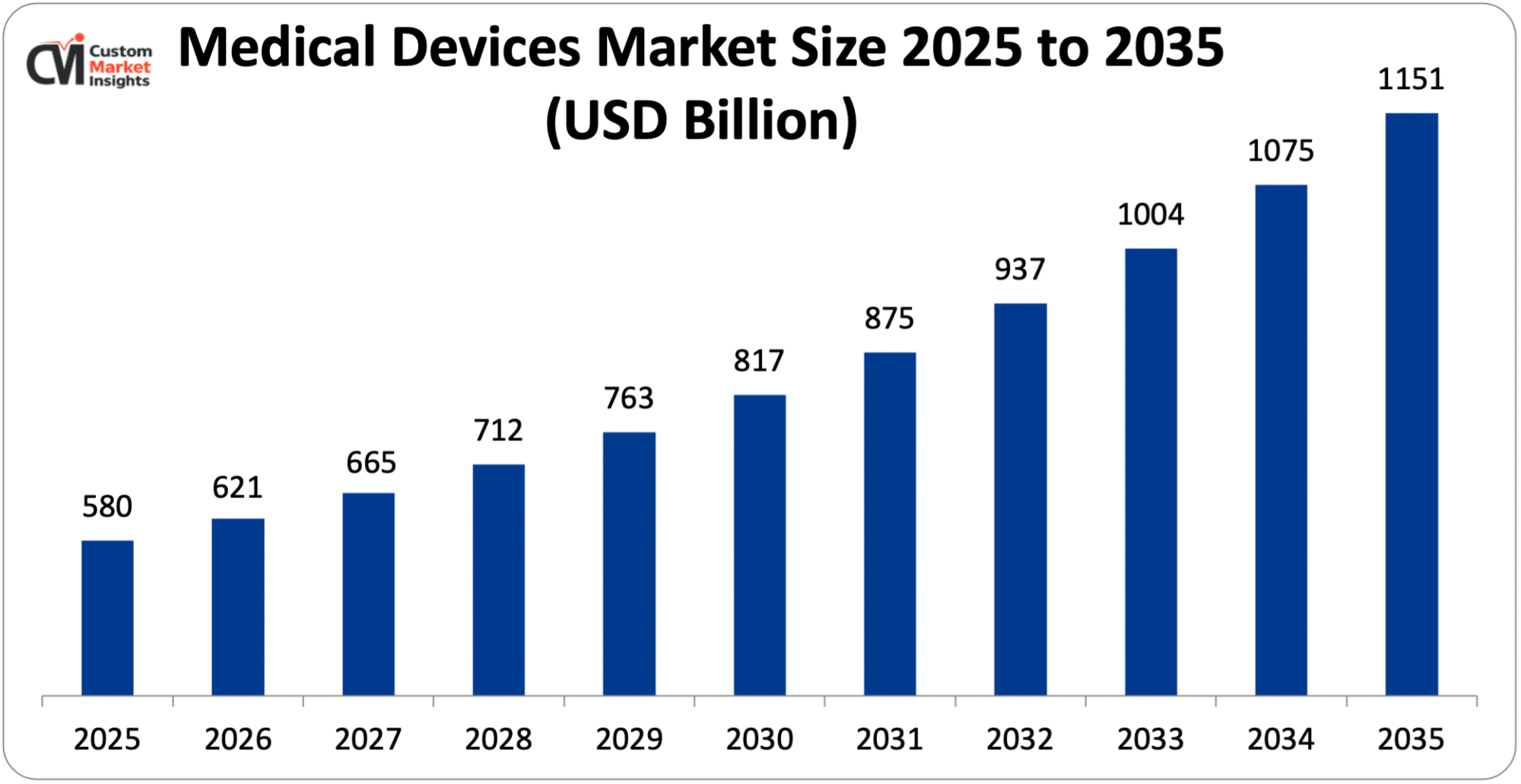

The market size of global medical devices will be estimated at USD 580 billion in 2025 and is expected to grow to between USD 621 billion in 2026 and about USD 1151 billion by 2035, with a current CAGR (compound annual growth rate) of 7.1% during the period of 2026 to 2035. Medical devices include instruments, apparatuses, machines, implants, and associated products that medical professionals use for diagnosing, preventing, monitoring, and treating human diseases and medical conditions. Medical devices achieve their main function through their physical and mechanical properties because these devices do not depend on chemical processes or metabolic functions like pharmaceuticals do.

The medical device category includes both basic equipment which consists of thermometers and syringes, and sophisticated equipment which includes MRIs, CT scanning systems, robotic surgical equipment, pacemakers, and artificial joint implantable devices. The devices serve a vital function in the healthcare process because they assist doctors with decision-making, they help patients achieve better health results, they allow procedures to be conducted with minimal body intrusion and they improve the effectiveness of medical facilities.

Market Highlight

- In 2025, North America will dominate the global market with an estimated market share of 42%. This growth is driven by the region’s increasing prevalence of CVD.

- The Asia Pacific is growing at the highest CAGR over the analysis period. Increasing investment in healthcare infrastructure drives industry growth.

- By type, the In vitro Diagnostic (IVD) segment accounted for the highest revenue share of over 12% in 2025.

- By end user, the hospitals & ASCs segment would have the highest share of the market in 2025.

Significant Growth Factors

The medical devices market trends present significant growth opportunities due to several factors:

- Rising Prevalence of Chronic Disease: An increased prevalence of chronic diseases is one of the most prominent factors responsible for the trend of growth in the medical devices industry. Chronic diseases such as heart diseases, diabetes, cancer, and respiratory diseases are increasing across the globe as a response to aging populations but also due to longer life expectancy, poor lifestyles, inadequate eating habits, and environmental situations. Most of these issues require continuous and instant treatment and constant check-ups, which is further increasing the demand for medical devices specifically focused on diagnosis and monitoring. For instance, those who are diabetic require glucose monitoring and administration devices, and those who are suffering from cardiac diseases require implanted devices like pacemakers, stents, blood pressure monitors, and others. A similar trend is emerging in the case of cancer, where the popularity of sophisticated imaging systems is rapidly rising. Therefore, the constant requirement of healthcare and examination of such chronic diseases tends to promote the demand for a variety of medical devices in the industry. For instance, according to the International Diabetes Federation (IDF), in 2045, 783 million people are expected to be diabetic.

- Expansion of Healthcare Infrastructure: Development of healthcare infrastructure is an important factor in the growth of the medical devices industry. Public and private sector investors based in developed and developing countries are investing substantially in building healthcare infrastructure in the form of hospitals, clinics, diagnostic centers, operating suites, and other specialized units to provide enhanced healthcare services. For instance, government initiatives in India and China have led to increased health spending and urbanization, which are leading to an upsurge in building healthcare facilities; these pathways to better health are predominantly opening in poorer, more rural places, and these require advanced medical devices to be installed. Every new hospital or construction of a modernized hospital will also require a slew of ancillary devices, from computer-aided diagnostics to patient monitoring systems, high-end surgical devices, and ICU devices. Modernizing existing infrastructure to adopt innovations like digital health management or smart hospitals will also lead to a higher use of more innovative and connected medical devices.

What are the Major Advances Changing the Medical Devices Market Today?

- AI & Machine Learning Integration: AI & Machine Learning (ML) is one of the most disruptive applications to the medical devices market to date and has the potential to change the way that healthcare is delivered, diagnosed, and managed. Many applications of AI algorithms are already present in many medical devices, where they can be used to process large sums of patient data simultaneously and give clinicians enhanced insight into the condition of their patients, allowing them to react faster and more accurately in a more tailored approach to healthcare. For imaging hardware, AI can facilitate the faster detection of pathologies, whether tumors, strokes, or broken bones, than traditional techniques can. In the hospital environment, ML can also be used to identify high-risk patients in other locations and anticipate outcomes for the future to enable tailored therapies and decrease rates of readmission. investment in combining AI with existing imaging systems, patient monitors, and clinical systems from companies such as Siemens Healthineers, GE HealthCare, and Philips Healthcare is indicative of this trend. Additionally, AI will play a large role in the automation of hospitals and relieving the burden placed on staff with currently high workloads. As healthcare shifts to a more data-driven and precision way of working, AI & ML in the medical devices industry will be a key fuel to its growth.

- Minimally Invasive & Robotic Surgery: Minimally invasive and robotic surgery is one of the most exciting value-added segments of the medical devices market and has revolutionized conventional surgical procedures by providing a more effective, efficient, and patient-friendly intervention. Minimally invasive techniques have transformed the entire concept of surgery through the use of small incisions, highly specialized instruments, and the application of imaging technology, such as endoscopy and laparoscopy, to perform the intervention with reduced trauma to the tissues when compared to open surgery or other traditional techniques. These benefits include shorter hospital stays, faster recovery, and lower risk of complications, thereby ultimately translating into lower costs of care. Robotic or computer-assisted surgery provides further enhancement of technologies for minimally invasive procedures through the incorporation of advanced robotic systems, which have increased precision, control, and flexibility. These systems offer high-definition 3D visualization, tremor filtration, and enhanced instrumentation control for surgeons and consist of a surgeon’s console, patient-side manipulator, and vision cart. Intuitive surgical is one of the leaders in this segment of the market and has pioneered the da Vinci robotic systems, and other players are also gaining ground with Stryker Corporation and Medtronic strengthening their robotics portfolios. The reasons attributed to increased demand for the segment include patient and physician preference for surgical robots over other conventional procedures and the influx of novel technologies related to the segment. Thus, the minimally invasive and robotics segment is growing at a rapid pace.

Category Wise Insights

By Type

Why In-vitro Diagnostic (IVD) Hold a Prominent Position in the Market?

The In vitro Diagnostic (IVD) segment accounted for the highest revenue share of over 12% in 2025. The growth is attributed to factors such as the increasing occurrence of infectious diseases among the population, the growing number of tests conducted among the population, and others. The abovementioned factors, along with the increasing research and development activities among the major players to develop and launch new and innovative test kits and products to meet the rising demand of the people, are expected to support the segmental growth in the market. For example, in Nov 2023, Newland EMEA launched a new range of in vitro diagnostics products for the healthcare industry.

The diabetes care devices segment is growing at the highest CAGR during the forecast period. The increasing prevalence of diabetes along with a rising aging population drives the segment expansion.

By End User

Why Hospitals & ASCs Capture the Highest Market Share in the Medical Devices Market?

The hospitals & ASCs segment would have the highest share of the market in 2025. This growth can be attributed to overall increases in surgical caseloads, facility scope of practice, and patient hospital admissions, as well as an increased preference for high-end venues for patient care. Hospitals will remain a dominant source of demand for medical devices because high-end venues require a high number of medical devices (imaging, monitoring, surgical, and life-support) to perform complex procedures and critical care services. However, ASCs are experiencing a rapid rate of growth because they provide high-volume, cost-effective, efficient, one-day, specialty, minimally invasive surgical care, which has experienced exponential growth in the recent decade. This has increased Uom demand for small, mobile, in-room, high-end medical devices.

The clinics segment is growing at a rapid rate over the projected period. A continued move towards decentralization and outpatient medicine will drive growth. Clinics are the first point of call for many patients and are more and more often being equipped with smaller, high-tech equipment for diagnostics, monitoring, and minor surgery. Chronic diseases are increasing, and the need for their early detection, coupled with a demand for accessible and cheap healthcare, will promote the expansion of clinics in both rural and urban areas.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 621 billion |

| Projected Market Size in 2035 | USD 1151 billion |

| Market Size in 2025 | USD 580 billion |

| CAGR Growth Rate | 7.1% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, End User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is North America Medical Devices Market Size?

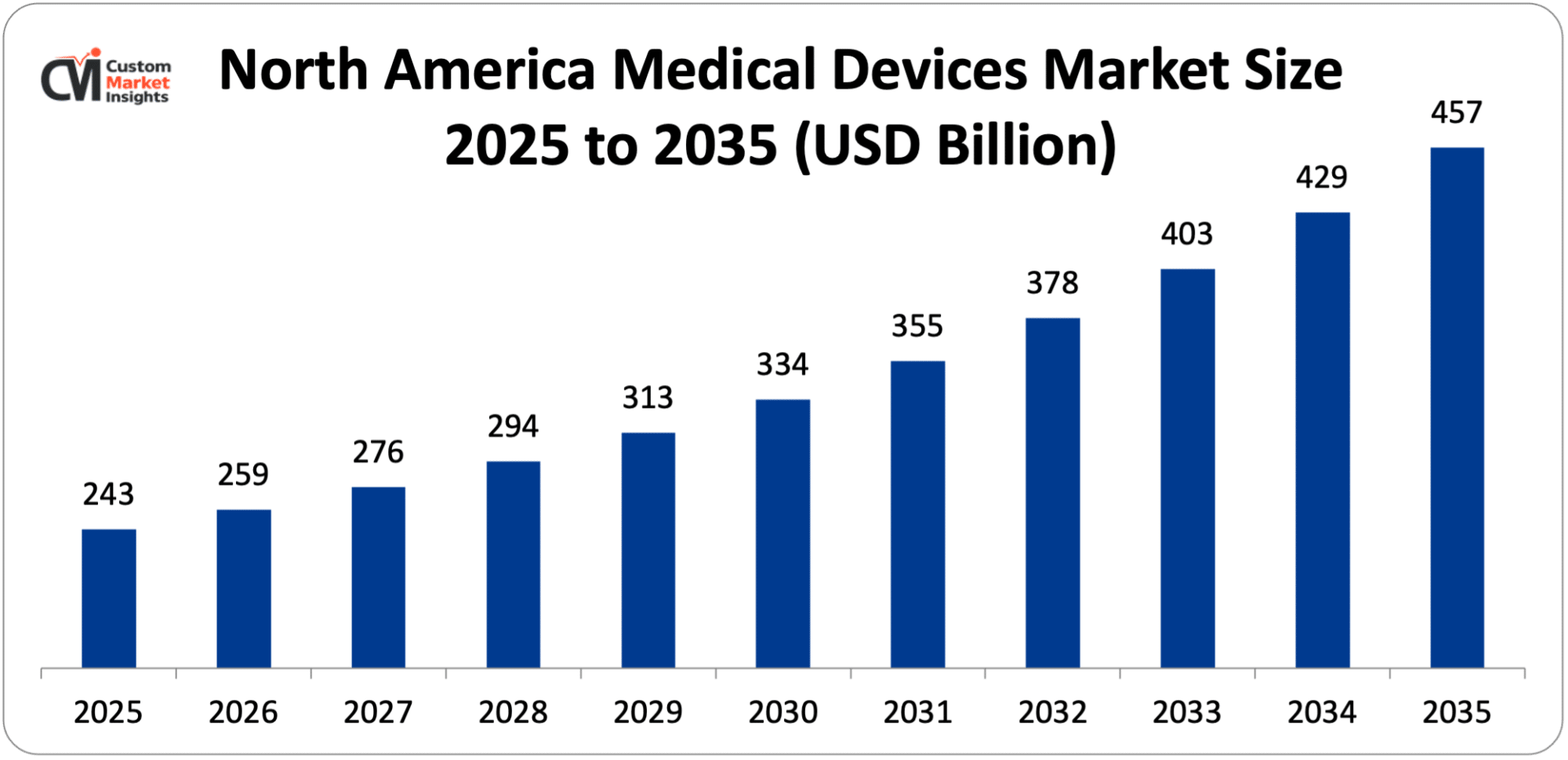

Its market size, in terms of North American medical devices, is projected to be USD 243 billion in 2025 with a growth to about USD 457 billion in 2035 with a CAGR of 6.5% between 2026 and 2035.

Why did North America Dominate the Medical Devices Market in 2025?

In 2025, North America will dominate the global market with an estimated market share of 42%. The market is driven by the presence of sophisticated health care infrastructure, investment in health care expenditures, and the high rate of adoption of new-age technologies. The strong health care base consisting of hospitals, diagnostic centers, and research institutes, among others, that are based in the region and are investing heavily in state-of-the-art devices—robotic surgical systems, AI-based imaging systems, and remote monitoring systems. The increasing occurrence of chronic diseases, including cardiovascular disorders, cancer, and diabetes, is also one of the important trends.

US Medical Devices Market Trends

In the North American region, the US is expected to dominate the market over the projected period. The growth in the region is owing to the rising prevalence of chronic disease. For instance, according to the American Heart Association Journals, Cardiovascular disease (CVD) prevalence is rising in the U.S., with over 940,000 deaths annually and over 72% of adults having an unhealthy weight.

Why is Europe Experiencing Significant Growth in the Medical Devices Market?

Europe holds a significant market share in 2025. The region is supported by mature healthcare systems, increasing healthcare expenditure and focus on innovation. Germany, France, and the United Kingdom are the major regions contributing to the growth owing to established hospital infrastructure and high adoption of recent technologies such as diagnostic imaging systems, minimally invasive surgical devices, and digital health. An aging population in developed regions is also a major factor for the increased demand of medical devices in orthopedics, cardiology, and home healthcare segments.

UK Medical Devices Market Trends

The UK held the dominant position in the market in 2025. Aging in the UK has increased the use of implants for orthopedics and healthcare appliances in the home. Medical device innovation in the UK is driven by centers of research excellence, government investment, and initiatives on digital health and AI.

Why is the Asia Pacific Growing at the Highest CAGR in the Medical Devices Market?

The Asia Pacific is expected to grow at a significant rate over the projected period. The region is growing healthcare expenditures and increasing the prevalence of chronic disease.

India Medical Devices Market Trends

India holds the prominent market share in the industry. Increasing number of surgical procedures and growing prevalence of chronic disease are driving the market for medical devices in India. There is an increasing trend in various surgical procedures like resection of tumors, organ transplants, and cardiovascular interventions owing to increased incidence of diabetes, cardiovascular diseases, cancer, and others. Medical devices play an important role in all of the above procedures, thereby driving industry growth.

Why is the Middle East & Africa Region is growing rapidly in the Medical Devices?

The MEA region is growing at a steady rate over the projected period. The growth is mainly driven by enhanced health care infrastructure, surging health care costs, and the widening reach of quality health services. The growth in the region is led by nations like the United Arab Emirates, Saudi Arabia, and South Africa, with governments pumping money into the healthcare infrastructure, like building hospitals, promoting medical tourism, and upgrading the health care setup. Growing incidences of lifestyle-related ailments such as cancer, diabetes, and cardiovascular disease have translated into equal growth in demand for diagnostic and therapeutic devices.

UAE Medical Devices Market Trends

The UAE is growing at the highest CAGR during the forecast period. The expanding private healthcare sectors and growing awareness about early diagnosis and preventive care are supporting device adoption.

Top Players in the Medical Devices Market and Their Offerings

- Medtronic

- Johnson & Johnson MedTech

- Abbott Laboratories

- Siemens Healthineers

- Stryker Corporation

- BD

- GE HealthCare

- Philips Healthcare

- Boston Scientific

- Medline Industries

- Cardinal Health

- Baxter International

- Fresenius Medical Care

- Danaher Corporation

- Roche Diagnostics

- Terumo Corporation

- Olympus Corporation

- Smith & Nephew

- Zimmer Biomet

- Alcon

- Others

Key Developments

Medical devices market has experienced considerable changes in the last two years as the market players are trying to diversify their technological aspects and develop product portfolios using strategic approaches.

- In March 2025, Johnson & Johnson MedTech, a global leader in orthopedic technologies and solutions, is highlighting its latest advancements in digital orthopedics at the American Academy of Orthopaedic Surgeons (AAOS) 2025 Annual Meeting in San Diego, California, from March 10-14. Expanding on last year’s innovations, Johnson & Johnson MedTech is introducing cutting-edge implants, advanced techniques, and data-driven technologies across orthopedic specialties, including joint reconstruction, trauma, extremities, and spine. These developments are grounded in the company’s commitment to deliver innovative, impactful solutions that address the evolving needs of surgeons and patients.

- In April 2025, Bausch Health Companies Inc., a global, diversified pharmaceutical company, and its aesthetics business, Solta Medical, announced today Fraxel FTX™ will launch at the American Society for Laser Medicine & Surgery, Inc. (ASLMS) 2025 Annual Conference on April 25 in Orlando, FL. This event begins the rollout of Fraxel FTX™ to dermatologists, plastic surgeons, and other licensed aesthetic professionals across the United States, with plans to expand globally in the coming months.

These strategic measures have enabled the companies to reinforce their competitive positions, increase the product line, boost their technological competencies and also seize growth opportunities in the fast-growing medical devices market.

The Medical Devices Market is segmented as follows:

By Type

- Orthopedic Devices

- Diagnostic Imaging Devices

- Cardiovascular Devices

- In-vitro Diagnostic (IVD)

- Minimally Invasive Surgery Devices

- Diabetes Care Devices

- Wound Management

- Ophthalmic Devices

- Dental Devices

- Nephrology Devices

- General Surgery

- Others

By End User

- Hospitals & ASCs

- Clinics

- Others

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Medical Devices by Segments

- 2.1.2. Medical Devices by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Medical Devices Market Attractiveness Analysis, By Type

- 2.2.3. Medical Devices Market Attractiveness Analysis, By End User

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Rising Prevalence of Chronic Disease

- 3.1.2. Expansion of Healthcare Infrastructure

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Medical Devices Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Medical Devices Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Orthopedic Devices

- 4.1.3. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Diagnostic Imaging Devices

- 4.1.7. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Cardiovascular Devices

- 4.1.11. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. In-vitro Diagnostic (IVD)

- 4.1.15. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Minimally Invasive Surgery Devices

- 4.1.19. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Diabetes Care Devices

- 4.1.23. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1.26. Wound Management

- 4.1.27. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.29. Key Market Trends, Growth Factors, & Opportunities

- 4.1.30. Ophthalmic Devices

- 4.1.31. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.33. Key Market Trends, Growth Factors, & Opportunities

- 4.1.34. Dental Devices

- 4.1.35. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.36. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.37. Key Market Trends, Growth Factors, & Opportunities

- 4.1.38. Nephrology Devices

- 4.1.39. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.40. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.41. Key Market Trends, Growth Factors, & Opportunities

- 4.1.42. General Surgery

- 4.1.43. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.44. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.45. Key Market Trends, Growth Factors, & Opportunities

- 4.1.46. Others

- 4.1.47. Medical Devices Share Forecast, By Region (USD Billion)

- 4.1.48. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.49. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Medical Devices Market – By End User

- 5.1. End User Market Overview, By End User Segment

- 5.1.1. Medical Devices Market Revenue Share, By End User, 2025 & 2035

- 5.1.2. Hospitals & ASCs

- 5.1.3. Medical Devices Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Clinics

- 5.1.7. Medical Devices Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Others

- 5.1.11. Medical Devices Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1. End User Market Overview, By End User Segment

- Chapter 6. Medical Devices Market – Regional Analysis

- 6.1. Medical Devices Market Overview, By Region Segment

- 6.1.1. Global Medical Devices Market Revenue Share, By Region, 2025 & 2035

- 6.1.2. Global Medical Devices Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 6.1.3. Global Medical Devices Market Revenue, By Type, 2026 – 2035

- 6.1.4. Global Medical Devices Market Revenue, By End User, 2026 – 2035

- 6.2. North America

- 6.2.1. North America Medical Devices Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 6.2.2. North America Medical Devices Market Revenue, By Type, 2026 – 2035

- 6.2.3. North America Medical Devices Market Revenue, By End User, 2026 – 2035

- 6.2.4. U.S. Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.2.5. Canada Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.2.6. Mexico Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.2.7. Rest of North America Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.3. Europe

- 6.3.1. Europe Medical Devices Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 6.3.2. Europe Medical Devices Market Revenue, By Type, 2026 – 2035

- 6.3.3. Europe Medical Devices Market Revenue, By End User, 2026 – 2035

- 6.3.4. Germany Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.3.5. France Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.3.6. U.K. Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.3.7. Russia Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.3.8. Italy Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.3.9. Spain Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.3.10. Netherlands Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.3.11. Rest of Europe Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.4. Asia Pacific

- 6.4.1. Asia Pacific Medical Devices Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 6.4.2. Asia Pacific Medical Devices Market Revenue, By Type, 2026 – 2035

- 6.4.3. Asia Pacific Medical Devices Market Revenue, By End User, 2026 – 2035

- 6.4.4. China Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.4.5. Japan Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.4.6. India Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.4.7. New Zealand Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.4.8. Australia Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.4.9. South Korea Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.4.10. Taiwan Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.4.11. Rest of Asia Pacific Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.5. The Middle-East and Africa

- 6.5.1. The Middle-East and Africa Medical Devices Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 6.5.2. The Middle-East and Africa Medical Devices Market Revenue, By Type, 2026 – 2035

- 6.5.3. The Middle-East and Africa Medical Devices Market Revenue, By End User, 2026 – 2035

- 6.5.4. Saudi Arabia Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.5.5. UAE Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.5.6. Egypt Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.5.7. Kuwait Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.5.8. South Africa Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.5.9. Rest of the Middle East & Africa Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.6. Latin America

- 6.6.1. Latin America Medical Devices Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 6.6.2. Latin America Medical Devices Market Revenue, By Type, 2026 – 2035

- 6.6.3. Latin America Medical Devices Market Revenue, By End User, 2026 – 2035

- 6.6.4. Brazil Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.6.5. Argentina Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.6.6. Rest of Latin America Medical Devices Market Revenue, 2026 – 2035 (USD Billion)

- 6.1. Medical Devices Market Overview, By Region Segment

- Chapter 7. Competitive Landscape

- 7.1. Company Market Share Analysis – 2025

- 7.1.1. Global Medical Devices Market: Company Market Share, 2025

- 7.2. Global Medical Devices Market Company Market Share, 2024

- 7.1. Company Market Share Analysis – 2025

- Chapter 8. Company Profiles

- 8.1. Medtronic

- 8.1.1. Company Overview

- 8.1.2. Key Executives

- 8.1.3. Product Portfolio

- 8.1.4. Financial Overview

- 8.1.5. Operating Business Segments

- 8.1.6. Business Performance

- 8.1.7. Recent Developments

- 8.2. Johnson & Johnson MedTech

- 8.3. Abbott Laboratories

- 8.4. Siemens Healthineers

- 8.5. Stryker Corporation

- 8.6. BD

- 8.7. GE HealthCare

- 8.8. Philips Healthcare

- 8.9. Boston Scientific

- 8.10. Medline Industries

- 8.11. Cardinal Health

- 8.12. Baxter International

- 8.13. Fresenius Medical Care

- 8.14. Danaher Corporation

- 8.15. Roche Diagnostics

- 8.16. Terumo Corporation

- 8.17. Olympus Corporation

- 8.18. Smith & Nephew

- 8.19. Zimmer Biomet

- 8.20. Alcon

- 8.21. Others.

- 8.1. Medtronic

- Chapter 9. Research Methodology

- 9.1. Research Methodology

- 9.2. Secondary Research

- 9.3. Primary Research

- 9.3.1. Analyst Tools and Models

- 9.4. Research Limitations

- 9.5. Assumptions

- 9.6. Insights From Primary Respondents

- 9.7. Why Custom Market Insights

- Chapter 10. Standard Report Commercials & Add-Ons

- 10.1. Customization Options

- 10.2. Subscription Module For Market Research Reports

- 10.3. Client Testimonials

List Of Figures

Figures No 1 to 29

List Of Tables

Tables No 1 to 41

Prominent Players

- Medtronic

- Johnson & Johnson MedTech

- Abbott Laboratories

- Siemens Healthineers

- Stryker Corporation

- BD

- GE HealthCare

- Philips Healthcare

- Boston Scientific

- Medline Industries

- Cardinal Health

- Baxter International

- Fresenius Medical Care

- Danaher Corporation

- Roche Diagnostics

- Terumo Corporation

- Olympus Corporation

- Smith & Nephew

- Zimmer Biomet

- Alcon

- Others

FAQs

The key players in the market are Medtronic, Johnson & Johnson MedTech, Abbott Laboratories, Siemens Healthineers, Stryker Corporation, BD, GE HealthCare, Philips Healthcare, Boston Scientific, Medline Industries, Cardinal Health, Baxter International, Fresenius Medical Care, Danaher Corporation, Roche Diagnostics, Terumo Corporation, Olympus Corporation, Smith & Nephew, Zimmer Biomet, Alcon, Others.

Government regulations play a crucial role in shaping the development of the medical devices market by ensuring product safety, quality, and efficacy while also influencing the speed of innovation and market entry, as stringent approval processes, compliance standards, and reimbursement policies can either facilitate growth through trust and standardization or slow it down by increasing time-to-market and development costs.

The price point significantly impacts market growth and adoption by influencing affordability, accessibility, and purchasing decisions, where higher costs can limit adoption in price-sensitive regions while cost-effective and value-based pricing accelerates penetration across hospitals, clinics, and homecare settings.

According to the present analysis and forecast modeling, the market of medical devices will witness a significant growth of about USD 1151 billion in the year 2035 with the growing innovative product launch, increasing collaboration, and increasing prevalence of CVD with a CAGR of 7.1% between the years 2026 and 2035.

It is projected that North America will hold the largest market share in the medical devices market in the forecast period, with a share of about 42% of the global market share, which is owing to the growing prevalence of CVD along with an ageing population.

The Asia Pacific is expected to grow at the highest rate during the forecast period. The increasing investment in healthcare infrastructure drives the market growth.

The growth of the medical devices market is primarily driven by the rising prevalence of chronic diseases, an increasing aging population, rapid technological advancements, expanding healthcare infrastructure, and growing demand for minimally invasive and home-based care solutions.