Linear Polymers Market Size, Trends and Insights By Type (Polyethylene (PE), High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), Linear Low-Density Polyethylene (LLDPE), Ultra-High Molecular Weight Polyethylene (UHMWPE), Polypropylene (PP), Homopolymer PP, Copolymer PP, Polyvinyl Chloride (PVC), Rigid PVC, Flexible PVC, Polystyrene (PS), General Purpose Polystyrene (GPPS), High Impact Polystyrene (HIPS), Expanded Polystyrene (EPS), Polyamides (PA / Nylon), PA 6, PA 6,6, Others, Others (PET, Polycarbonate, ABS, etc.)), By Manufacturing Process (Addition Polymerization, Condensation Polymerization, Ring-Opening Polymerization, Emulsion Polymerization), By End-Use Industry (Packaging, Flexible Packaging, Rigid Packaging, Automotive & Transportation, Construction, Electrical & Electronics, Healthcare & Medical Devices, Agriculture, Consumer Goods & Textiles, Others), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 4.7%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Asia Pacific |

Major Players

- BASF SE

- LyondellBasell Industries N.V.

- ExxonMobil Corporation

- Dow Inc.

- Others

Reports Description

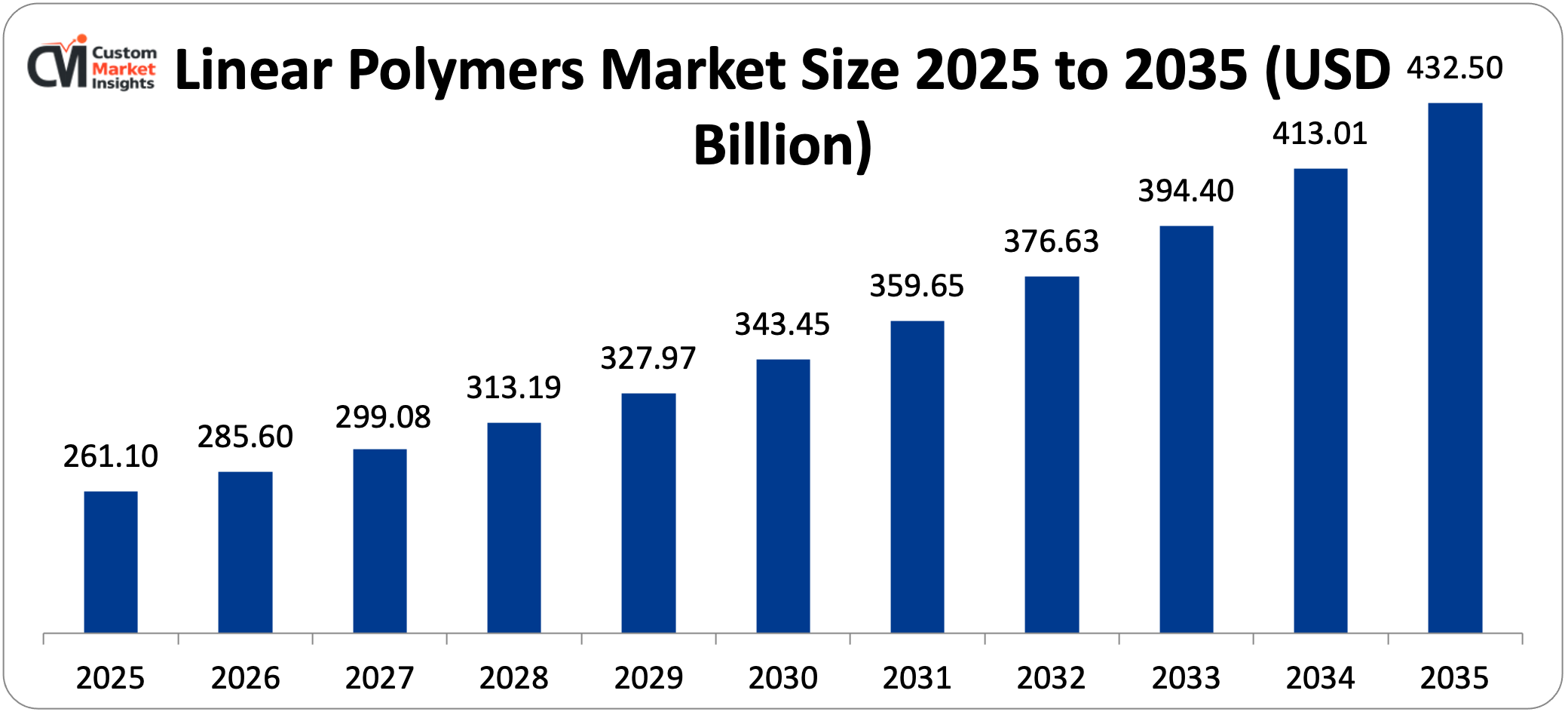

The worldwide market in linear polymers is valued at USD 261.1 billion in 2025. By 2030, it is expected to be worth USD 343.45 billion, growing at a rate of 4.4% per year from 2024 to 2030. On a bigger timeframe, the market will have expanded to USD 285.6 billion in 2026 and USD 432.5 billion in 2035 at a CAGR of 4.7% between the years 2026 and 2035. Market is expanding due to increased use of light and durable materials in packaging, automobiles, buildings, electronics, and medicine. Asia Pacific and LAMEA are also experiencing an increase in urbanization and investment in infrastructure. There is increased use of bio-based and recyclable polymer solutions, and there is also continuous improvement of the polymer synthesis and processing technologies.

Market Highlight

- The largest market was in the Asia Pacific, which held over two-fifths of the market in linear polymers around the world. The rapid industrialization of China, India, and Southeast Asia is expected to give it the highest CAGR in the forecast period.

- North America had the largest market share, with over 40% of global revenue. By 2025, the market size had reached USD 104.86 billion due to the high demand in the automotive, healthcare, and packaging sectors.

- The segment that generated the largest amount of money was the segment of polyethylene, and it will continue to increase at a CAGR of 4.5% throughout the forecast period. The reason is that it finds extensive application in flexible packaging, construction pipes, and industries.

- The addition polymerization segment was the largest manufacturing process money earner. It is predicted to increase at a CAGR of 4.4% over the forecast period since this process enables the polymer chains to continue increasing through the formation of strong covalent bonds.

- The largest share based on end-use industry was the packaging segment which is projected to increase at the highest rate (5.0%) within the forecast period. This is due to the evolving consumer pattern, increase in online purchases, and the necessity of having convenient packaging solutions.

- Polyethylene- Polyethylene is the most widespread form of polymer, comprising 28.4% in the world market. Polypropylene constitutes 23.7%, polyvinyl chloride constitutes 18.2%, and polystyrene constitutes 12.9%.

Significant Growth Factors

The Linear Polymers Market Trends present significant growth opportunities due to several factors:

- Surging Demand from the Packaging Industry and E-Commerce Expansion: The largest and most consistent demand in linear polymers globally is the packaging sector, which comprises approximately two-fifths of the entire market consumption. Linear polymers possess numerous diverse features and may be adapted to meet some packaging requirements. They can be made in various degrees of strength, flexibility, barrier and transparency. This flexibility allows the packaging makers to produce packaging suitable to a great variety of products and customer needs. The world packaging market exceeded 1.1 trillion in 2024, and of the total amount of materials utilized, polymer-based packaging items constituted over 40% by weight. The structural boom of e-commerce, with global online retail sales projected to exceed USD8 trillion by 2027, has raised the demand of protective packaging films, stretch wraps, courier bags, and cushioning materials (primarily of linear polyethylene and polypropylene). The packaging sector should demand environmentally friendly and effective packaging solutions. This is the key cause of the linear polymer market expansion. Linear polymers are the best in packaging as they are inexpensive, lightweight and possess excellent barrier properties. The increasing popularity of convenience food, beverages, and online shopping is also increasing the demand for the packaging materials which is favorable to the market. The applications of flexible packaging such as multilayer barrier films, stand up pouches and lidding films are increasing at an above average rate. The reason is that humans are more likely to choose packaging that is readily available, lightweight and improves the duration of freshness of food as well as reduces the weight of transportation and carbon footprint. Blow molding and extrusion molding have introduced new concepts that have resulted in multilayer films with excellent barrier properties that can increase the lifespan of products by over 20%. Also, there are new polymer blends and multi-layer co-extrusion technologies that allow the formation of monomaterial packaging architectures, wherein all the layers are composed of the same polymer family. These designs are far simpler to recycle compared to the conventional mixed-material laminate designs, a reaction to the growing call by brands and regulators to use environmentally friendly packaging alternatives.

- Rising Demand for Lightweight Materials in Automotive and Aerospace Applications: The market of linear polymers is expanding due to the increased need for lightweight and high-performance materials in more industries, such as automotive, aerospace, and construction. Linear polymers are excellent when it comes to reducing the weight of products, increasing their fuel efficiency, and reducing carbon footprints because they possess a superior strength-to-weight ratio. The global automotive sector produces over 90 million vehicles annually. The average amount of polymer materials in the interior trim, exterior body panels, under-hood components and seating systems of each new passenger car is 150 to 200 kg. The automotive industry, particularly the rising markets, has contributed to the demand for linear polymers such as polypropylene and polyethylene. The metals are also lighter and can be used to substitute the heavier metal parts in cars, hence being fuel-efficient and reducing emissions. The most widely used polymer in cars is polypropylene; it has low density (0.9 g/cm³), is very impact resistant, remains stable at temperatures up to 130°C when used under the hood, and is compatible with a large variety of reinforcing agents and additive systems. Polypropylene in the bumper systems, instrument panels, door claddings, and wheel arch liners of a single mid-size passenger car is approximately 30 to 40 kg. The demand for automotive polymers is also being altered by the rapid proliferation of electric vehicles across the globe. To take one example, battery electric vehicles require high voltage cable insulation using special linear polymer solutions, battery module housings, thermal management system components, and lightweight structural components that enable them to travel as far as possible. In February 2025, Hyundai Motor Group and Kolon Group declared a strategic partnership in materials to develop advanced polymer composite materials to be utilized in the next generation of electric vehicles. This indicates that the car industry is yet to be dedicated to using polymers to be electrified.

What are the Major Advances Changing the Linear Polymers Market Today?

- Circular Economy Transition and Advanced Recycling Technologies: Circular Economy Transition and High-tech Recycling Technologies The shift between a linear economic system that is based on a take-make-dispose economic model and a circular economy is the most significant structural force altering the linear polymers industry. Policies such as the European Union’s Packaging and Packaging Waste Regulation that became effective in February 2025 and defines minimum requirements regarding the quantity of recycled material used in packaging are compelling polymer producers, converters, and brand owners to invest a significant sum in supply chains based on recycled materials. LyondellBasell made and sold more than 200,000 tonnes of recycled and renewable-based polymers in 2024, which is a 65% increase from the year before. The company plans to make and sell 2 million tonnes of circular polymers every year by 2030. An example of how the molecular recycling technology can be applied on a large scale to transform mixed polyolefin waste into circular feedstocks that can be utilized in producing food-contact-grade virgin-equivalent polymers is the MoReTec-1 chemical recycling plant in Cologne, Germany, which will be opened in 2026. It is an example of how molecular recycling technology can be used on a large scale to turn mixed polyolefin waste into circular feedstocks that can be used to make food-contact-grade virgin-equivalent polymers. ExxonMobil’s Baytown, Texas, facility has recycled more than 80 million pounds of plastic that was at the end of its life using advanced recycling technology. The company is also working on more advanced recycling projects at manufacturing sites in North America, Europe, and Asia, with the goal of reaching 1 billion pounds per year of advanced recycling capacity around the world. BASF wants to use 250,000 metric tons of recycled and waste-based raw materials in its production plants every year starting in 2025. These materials could be pyrolysis oil from mixed plastic waste or end-of-life tires. By 2030, the company wants to double sales of circular economy solutions to €17 billion. These investments in the industry are making certified circular linear polymers more widely available in the polyethylene, polypropylene, and polyamide product families. This means that brand owners and converters can meet recycled content requirements without sacrificing the performance of the materials.

- Bio-Based Linear Polymers and Renewable Feedstock Adoption: The growth of bio-based alternatives to petroleum-based linear polymers is picking up speed in the business world, thanks to brand owners’ commitments to sustainability and government incentives for using low-carbon materials. Bio-based polyethylene, which is made from sugarcane ethanol, works the same way as fossil-based HDPE and LDPE but has a much lower carbon footprint from cradle to gate. More and more people are making biopolymers like polylactic acid (PLA) and polyhydroxyalkanoates (PHA), which are better for the environment than regular linear polymers. More and more, these biopolymers are being used in packaging, farming, and consumer goods. The global bioplastics market is expected to grow from about 2.5 million tons in 2024 to more than 7.5 million tons by 2030. Bio-based drop-in polymers, which work the same way as their petrochemical counterparts, will take up more and more of the market as production increases and costs go down. Polylactic acid (PLA), which is a ring-opened condensation polymer, is driving a lot of growth in compostable and bio-based packaging. Global PLA production capacity will grow a lot during the forecast period. Mass balance certification schemes, which assign bio-based or recycled feedstock inputs to specific product volumes at complex cracker-integrated production sites, are allowing major companies like SABIC, BASF, and LyondellBasell to sell certified renewable-content polymers to customers without having to build separate bio-feedstock production lines.

- Metallocene and Single-Site Catalyst Innovations: It is now possible to prepare linear polymer grades with molecular weight distributions, comonomer incorporation, and chain architecture far superior to those produced with conventional Ziegler-Natta catalyzed systems, due to advances in catalyst technology, particularly the continued improvement and commercial availability of metallocene and single-site catalyst systems. The continuous studies and technological advancement in the technique of polymer synthesis and modification have enabled the linear polymers to be more effective and have transformed their characteristics which has provided new applications of the polymers in a broad spectrum of activities such as packaging, construction, and electronics, among others. The market is growing, and new opportunities are presented by new polymer blends and formulations of additives. Linear low density polyethylene (mLLDPE) produced using metallocene catalysts is highly puncture resistant and is highly optical in nature and can be downgauged, whereby manufacturers of the film can achieve the same or better performance at 10-25% lower gauge. This makes it more economical in packaging application. It is also possible to make ultra-high molecular weight polyethylene (UHMWPE) in single-site catalyst systems to produce tough engineering products, such as orthopedic implants, ballistic protection panels, and high-performance fibers. They also produce ethylene based elastomers and plastomers which are similar to thermoplastics but have rubber-like mechanical properties. These new catalysts are continuously stretching the boundaries of linear polymer systems enabling them to be deployed into markets that previously were only accessible to more costly engineering polymers.

- Healthcare and Medical Device Applications Expansion: Linear polymers are increasing in medical device applications, drug delivery systems, and medical packaging due to their biocompatibility and their versatility. These polymers, like polyethylene and polypropylene, are very important for making syringes, implants, and prosthetics, which helps the market grow even more. By 2030, the global market for medical devices is expected to be worth USD800 billion. As medical products use more complex polymer structures for both functional and structural purposes, the value of these materials will make up a larger and larger part of the total value of devices. Ultra-high molecular weight polyethylene (UHMWPE) is the best material for hip and knee replacement implants. There are over 2 million total joint replacement surgeries done around the world each year. Gamma-irradiation-crosslinked variants make the implants even more resistant to wear, which makes them last longer. Polypropylene that is medical-grade is very important for syringe barrels, intravenous medication containers, diagnostic test devices, and a lot of other disposable tools where clarity, chemical resistance, steam sterilization compatibility, and following the rules are very important. The COVID-19 pandemic showed how important polymer-based medical supplies are and how easily supply chains can be broken. This led to a lot of money being put into making medical polymers in North America, Europe, and Asia.

Category Wise Insights

By Type

Why Does Polyethylene Dominate the Linear Polymers Market?

Polyethylene is the most popular linear polymer. Low-density PE and linear low-density PE are commonly used for flexible packaging, while high-density PE is better for pipes, containers, and industrial uses. Polyethylene is the most popular polymer because it has a unique set of properties that make it the best choice for a wide range of applications. These properties include excellent chemical resistance, moisture barrier performance, ease of processing with all major thermoplastic conversion techniques, and industry-leading cost competitiveness. The global linear low-density polyethylene market is expected to grow from USD 66.3 billion in 2025 to USD 118.7 billion by 2035, which is a compound annual growth rate (CAGR) of 6.0%. This growth is due to its increasing use in packaging films, containers, and flexible piping systems because it is strong, flexible, and cost-effective.

HDPE is the best material for blow-molded containers like milk jugs, detergent bottles, and industrial drums, as well as for pressure pipes in water and natural gas distribution systems. This is because it is rigid, resistant to chemicals, and easy to work with. It also lasts more than 50 years and doesn’t corrode, which makes it much cheaper to use than metal alternatives. LLDPE is replacing LDPE in demanding flexible film applications because it is better at resisting punctures, stretching when it breaks, and withstanding dart impacts. Polyethylene is used a lot in the packaging industry. Changes in people’s lives, the rise of online shopping, and the need for convenience have all led to an increase in the demand for flexible packaging like films, bags, and pouches. Polyethylene is a great material for packaging because it is flexible, has great barrier properties, and is cheap.

Polypropylene has a large market share because it can be used in a wide range of products, such as automotive parts, packaging films, and textiles. PVC is still important in building for pipes, profiles, and electrical fittings. Polypropylene is the best material for packaging closures, automotive interior systems, appliance housings, and nonwoven fibers for hygiene applications because it has the best balance of stiffness, impact resistance, chemical resistance, and thermal stability. Its density of only 0.9 g/cm³ is the lowest among commodity polymers. The global market for polypropylene is expected to grow from about USD100 billion in 2024 to about USD155 billion by 2033. PVC is still very important in construction around the world because it is very fire-resistant, stable in size, and cheap for window profiles, pipe systems, and cable insulation. PVC pipes, window frames, and insulation materials are now considered essential in construction. As more people move to cities, the demand for these materials is growing, making plastics more popular than metals and glass.

By Manufacturing Process

Why Does Addition Polymerization Lead the Manufacturing Process Segment?

Addition polymerization lets polymer chains keep growing. Monomers with unsaturated bonds can react with each other to make strong covalent bonds and make the polymer chain longer in a straight line. This process is what makes polyethylene, polypropylene, polystyrene, and polyvinyl chloride. Together, these four types of plastic make up most of the world’s linear polymer volume. The process is the basis for the industry’s largest production volumes because it can be used in gas-phase, slurry, and solution reactor configurations, and there are many different catalyst systems that allow for precise control of molecular architecture. Addition polymerization works well with continuous large-scale reactor designs, which lets modern world-scale polyolefin facilities handle more than 500,000 tonnes of material per year in a single train. This is what makes commodity polymers so competitive in terms of cost.

To make polyamides, polyesters, and polycarbonates, condensation polymerization is necessary. The global market for polyamides is expected to reach more than USD 60 billion by 2030. Ring-opening polymerization is the main way to make nylon-6 from caprolactam and polylactic acid from lactide monomers. PLA is becoming more important in eco-friendly packaging, which is why more money is being put into ring-opening polymerization capacity around the world. Emulsion polymerization makes it possible to make water-based polymer dispersions that can be used in coatings, adhesives, and binders.

By End-Use Industry

Why Does Packaging Lead the End-Use Industry Segment?

In 2022, the packaging segment was the biggest part of the global market and is expected to grow the fastest, at a rate of 5.0% per year. Linear polymers have a lot of different properties and can be made to fit certain packaging needs. Packaging is the most important material in modern supply chains because it provides food safety, protects products, and makes things easier for consumers in ways that no other material can do at the same cost and performance level. The food and drink industry uses more than 60% of all flexible packaging polymers. Linear polymers are the most common type of polymer used in fresh produce films, meat packaging, dairy containers, and beverage closures because they are good at keeping moisture out, can be heat-sealed, and meet FDA standards for food contact.

The largest segment of the linear polymer market is packaging where the need for lightweight, long-lasting, and low-cost solutions in food, drinks, and medicines is increasing. Linear polymers are also important in the production of electronics since they can be employed in the insulation, circuit protection, and powerful casing. Construction materials are still in demand since they are applied in building structures, pipes, and cables. In the case of pharmaceutical packaging and disposable devices, the healthcare industry requires resistant, sterile and safe polymers. Linear polymers are applied in agriculture in films and irrigation systems and also for protective purposes.

The second-largest segment is the automotive end-use segment, which is expanding at a faster rate compared to the market as a whole due to the trends of light and more electric vehicles. Polypropylene (PP) type is likely to increase fast due to the fact that the automotive sector requires it. This is due to the fact that manufacturers are producing cars with reduced weight in order to make them more efficient and reduce their carbon emissions. The construction segment experiences consistent high and massive demand due to infrastructure investment in every region, particularly on PVC pipe systems and polyethylene geomembranes. The most useful application in terms of per-kilogram value is the healthcare segment. The medical-grade polymer certification with its rigorous purity, sterility, and regulatory documentation is much more expensive.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 285.6 billion |

| Projected Market Size in 2035 | USD 432.5 billion |

| Market Size in 2025 | USD 261.1 billion |

| CAGR Growth Rate | 4.7% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Type, Manufacturing Process, End-Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Linear Polymers Market?

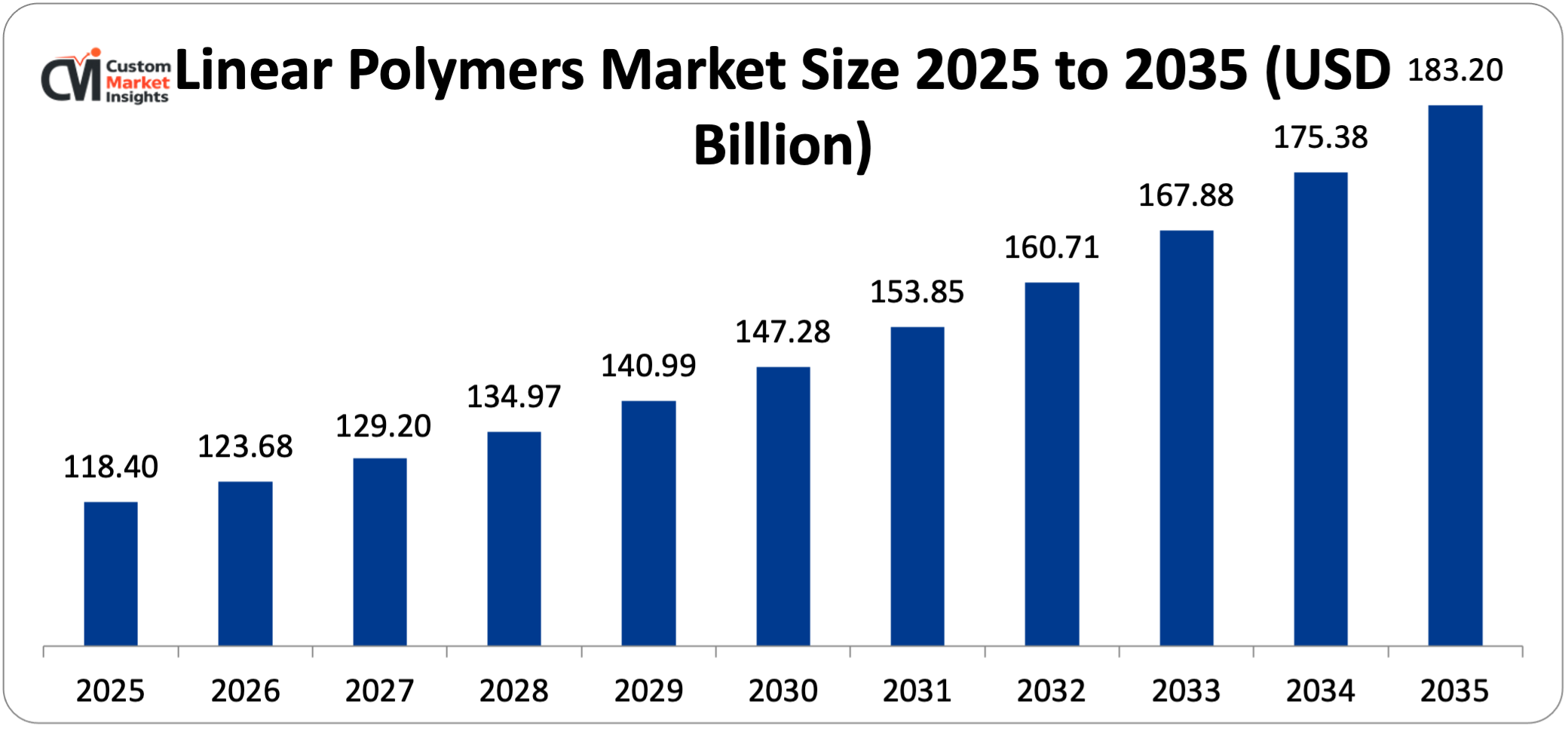

Asia Pacific had the biggest market share, making up more than two-fifths of the global linear polymers market. The regional market was worth about USD 118.4 billion in 2025 and is expected to grow at a CAGR of 5.0% from 2026 to 2035, making it the fastest-growing region. By 2035, it is expected to be worth about USD 183.2 billion.

Why Does Asia Pacific Dominate the Linear Polymers Market in 2025?

Asia Pacific is an important market for linear polymers, both in terms of making and using them. The market is growing steadily because Asia-Pacific is quickly becoming more industrialized, especially in China, India, and Southeast Asian countries. This growth in industry increases the need for linear polymers in many fields, such as automotive, packaging, construction, electronics, and consumer goods. China’s dominant position is based on the fact that it has the world’s largest infrastructure for making and using polymers. The country’s petrochemical industry is also growing quickly. China’s packaging industry uses more than 25 million tons of polyethylene and polypropylene every year. This is possible because China has the world’s largest e-commerce market, a huge food processing industry, and the highest output of consumer goods manufacturing in the world. India’s linear polymer market is one of the fastest-growing in the Asia Pacific region. This is because the country has a population of 1.4 billion people, a rapidly growing middle class, and a lot of construction demand due to urbanization. The government’s Production Linked Incentive schemes are also encouraging domestic manufacturing in the packaging, electronics, and automotive sectors.

What is the Size of the China Linear Polymers Market?

The China linear polymers market is expected to grow at a rate of 5.1% per year from 2026 to 2035, reaching almost USD 107.2 billion by 2035.

China Linear Polymers Market Trends

China has a market that is characterized by a massive volume of production, rapid capacity building, and an increasing domestic demand in all major fields of application. It consumes the PVC more than any other nation in the world because its large construction sector requires pipe systems, window profiles and cable insulation on over 1 billion square meters of new construction annually. It is also the country that packages the largest quantity of polyethylene. Sinopec Group and PetroChina are two of the largest polymer producers in the world, based in China. Big manufacturing is also present in China by foreign companies such as BASF, Dow, SABIC, and LyondellBasell to satisfy local demand. More strict environmental rules are making smaller domestic producers upgrade their efficiency and combine their production capacity. Meanwhile, the policies promoting the development of the circular economy by the government encourage investment in infrastructure development related to the recycling of polymers.

How Big is the North America Linear Polymers Market?

North America represented the largest market share in 2025 with over 40% of the revenue around the world. The market size was USD 104.86 billion and will continue to expand at a compound annual growth rate (CAGR) of 3.2% to about USD 148.7 billion by 2035.

Why Does North America Maintain a Leading Position in the Linear Polymers Market?

The U.S. helps North America stay on top. The Gulf Coast has a world-class petrochemical manufacturing complex that gets competitive natural gas liquid feedstocks, especially ethane from shale gas production. This gives it a big cost advantage over naphtha-cracker-based competitors in Europe and Asia when making polyethylene and polypropylene. The shale gas revolution changed the structure of the U.S. economy, making it a major exporter of polyethylene and polypropylene. The U.S. exports more than 10 million tonnes of polyethylene every year. The high volume of polymer use is supported by North American manufacturing facilities’ advanced production capabilities and the growing demand for medical plastics, especially in the healthcare and home healthcare markets. Also, people will use more advanced specialty polymers because they are more aware of how important sustainability is and because the government requires more recycling.

U.S. Linear Polymers Market Trends

The U.S. market benefits from the simultaneous advantages of cost-competitive shale-derived feedstocks for commodity polyolefin production, world-leading innovation capability in specialty and engineering polymer development, and the world’s largest and most sophisticated end-user industries across packaging, automotive, medical devices, and construction. ExxonMobil, Chevron Phillips Chemical, and LyondellBasell have all made big investments in capacity in the Gulf Coast region. This has greatly increased the U.S. polyethylene production capacity, which has helped meet growing domestic demand and open up new export markets in Latin America, Asia, and Europe.

Why is Europe Entering a New Era of Linear Polymers Market Development?

The European linear polymers market will be worth about USD 78.6 billion in 2025, and it will grow at a rate of 3.5% per year through the end of the forecast period. The European polymers market is expected to grow steadily until 2035. This is because there is a growing focus on sustainable materials, the need for more cars to be made, and new developments in chemical technology. Germany will still be the leader in the regional market in 2025, with a 31.2% share. This is due to the country’s strong chemical industry, high demand from the automotive sector, and strong growth in environmental technology. The Packaging and Packaging Waste Regulation, the EU Plastics Strategy, and national extended producer responsibility schemes all require more recycled content, recyclability by design, and less use of single-use plastics. This makes Europe’s regulatory environment the most strict in the world for polymer sustainability performance. At the same time, these rules are making it more expensive to comply and creating high-end markets for certified sustainable polymer products.

Why is the LAMEA Region Accelerating Linear Polymer Adoption?

The LAMEA polymer market was worth USD71 billion in 2025 and is expected to be worth about USD118.16 billion by 2035. The LAMEA region is growing because of more infrastructure development, more people moving to cities, more demand for consumer goods, and more manufacturing jobs. Saudi Arabia’s Jubail Industrial City is home to the Kingdom’s integrated petrochemical complex, which includes SABIC’s world-scale crackers and polymer plants. This makes Saudi Arabia one of the world’s largest producers and exporters of linear polymers. The Kingdom has access to very cheap ethane feedstocks, which gives it an edge in the global commodity polyethylene and polypropylene markets.

Brazil Linear Polymers Market Trends

Brazil has the biggest linear polymer market in Latin America because of its large packaging, automotive, construction, and agriculture industries. Braskem is the largest producer of petrochemicals and polymers in Latin America. Its headquarters is in São Paulo. The company has polyethylene, polypropylene, and PVC facilities all over Brazil and sells its products to both domestic and international markets. Brazil has one of the largest agriculture sectors in the world, which creates a lot of demand for polyethylene films used in greenhouses, silage storage, and mulch. The country’s rapidly growing population also drives demand for PVC pipe systems and PE geomembranes in the construction sector.

Top Players in the Linear Polymers Market and Their Offerings

- BASF SE

- LyondellBasell Industries N.V.

- ExxonMobil Corporation

- Dow Inc.

- SABIC (Saudi Arabian Oil Company)

- INEOS Group Holdings S.A.

- Chevron Phillips Chemical Company LLC

- LG Chem Ltd.

- Formosa Plastics Group

- TotalEnergies SE

- Braskem S.A.

- Reliance Industries Limited

- Sinopec Group

- Borealis AG

- Others

Key Developments

The linear polymers market has undergone significant developments over the past couple of years as industry participants seek to expand capabilities and enhance product portfolios.

- In November 2023: LyondellBasell’s MoReTec-1 chemical recycling plant in Cologne, Germany, is expected to start up in 2026. It will be the company’s first commercial-scale chemical recycling operation and will turn end-of-life plastic waste into circular feedstocks. The company also said that it would work with joint venture partners to build a second Cyclyx Circularity Center in the Dallas-Fort Worth area. This center will open in 2026 and be used to prepare feedstock for advanced recycling.

- In June 2023: LyondellBasell Industries and AFA Nord formed a 50:50 joint venture called LMF Nord GmbH to recycle post-commercial flexible secondary packaging waste. They built a recycling plant in Northern Germany to turn LLDPE and LDPE waste into high-quality recycled plastic for flexible packaging. Production will start in early 2025, and the company will be able to offer more circular products.

These strategic actions have helped businesses improve their market positions, move forward with their circular economy capabilities, increase their production capacity in areas with high growth, and take advantage of opportunities in the growing global linear polymers market.

The Linear Polymers Market is segmented as follows:

By Type

- Polyethylene (PE)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Linear Low-Density Polyethylene (LLDPE)

- Ultra-High Molecular Weight Polyethylene (UHMWPE)

- Polypropylene (PP)

- Homopolymer PP

- Copolymer PP

- Polyvinyl Chloride (PVC)

- Rigid PVC

- Flexible PVC

- Polystyrene (PS)

- General Purpose Polystyrene (GPPS)

- High Impact Polystyrene (HIPS)

- Expanded Polystyrene (EPS)

- Polyamides (PA / Nylon)

- PA 6

- PA 6,6

- Others

- Others (PET, Polycarbonate, ABS, etc.)

By Manufacturing Process

- Addition Polymerization

- Condensation Polymerization

- Ring-Opening Polymerization

- Emulsion Polymerization

By End-Use Industry

- Packaging

- Flexible Packaging

- Rigid Packaging

- Automotive & Transportation

- Construction

- Electrical & Electronics

- Healthcare & Medical Devices

- Agriculture

- Consumer Goods & Textiles

- Others

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Linear Polymers by Segments

- 2.1.2. Linear Polymers by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Linear Polymers Market Attractiveness Analysis, By Type

- 2.2.3. Linear Polymers Market Attractiveness Analysis, By Manufacturing Process

- 2.2.4. Linear Polymers Market Attractiveness Analysis, By End-Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Surging Demand from the Packaging Industry and E-Commerce Expansion

- 3.1.2. Rising Demand for Lightweight Materials in Automotive and Aerospace Applications

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Linear Polymers Market – By Type

- 4.1. Type Market Overview, By Type Segment

- 4.1.1. Linear Polymers Market Revenue Share, By Type, 2025 & 2035

- 4.1.2. Polyethylene (PE)

- 4.1.2.1. High-Density Polyethylene (HDPE)

- 4.1.2.2. Low-Density Polyethylene (LDPE)

- 4.1.2.3. Linear Low-Density Polyethylene (LLDPE)

- 4.1.2.4. Ultra-High Molecular Weight Polyethylene (UHMWPE)

- 4.1.3. Linear Polymers Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Polypropylene (PP)

- 4.1.6.1. Homopolymer PP

- 4.1.6.2. Copolymer PP

- 4.1.7. Linear Polymers Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Polyvinyl Chloride (PVC)

- 4.1.10.1. Rigid PVC

- 4.1.10.2. Flexible PVC

- 4.1.11. Linear Polymers Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Polystyrene (PS)

- 4.1.14.1. General Purpose Polystyrene (GPPS)

- 4.1.14.2. High Impact Polystyrene (HIPS)

- 4.1.14.3. Expanded Polystyrene (EPS)

- 4.1.15. Linear Polymers Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Polyamides (PA / Nylon)

- 4.1.18.1. PA 6

- 4.1.18.2. PA 6,6

- 4.1.18.3. Others

- 4.1.19. Linear Polymers Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Others (PET, Polycarbonate, ABS, etc.)

- 4.1.23. Linear Polymers Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Type Market Overview, By Type Segment

- Chapter 5. Linear Polymers Market – By Manufacturing Process

- 5.1. Manufacturing Process Market Overview, By Manufacturing Process Segment

- 5.1.1. Linear Polymers Market Revenue Share, By Manufacturing Process, 2025 & 2035

- 5.1.2. Addition Polymerization

- 5.1.3. Linear Polymers Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Condensation Polymerization

- 5.1.7. Linear Polymers Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Ring-Opening Polymerization

- 5.1.11. Linear Polymers Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Emulsion Polymerization

- 5.1.15. Linear Polymers Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Manufacturing Process Market Overview, By Manufacturing Process Segment

- Chapter 6. Linear Polymers Market – By End-Use Industry

- 6.1. End-Use Industry Market Overview, By End-Use Industry Segment

- 6.1.1. Linear Polymers Market Revenue Share, By End-Use Industry, 2025 & 2035

- 6.1.2. Packaging

- 6.1.2.1. Flexible Packaging

- 6.1.2.2. Rigid Packaging

- 6.1.3. Linear Polymers Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Automotive & Transportation

- 6.1.7. Linear Polymers Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Construction

- 6.1.11. Linear Polymers Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Electrical & Electronics

- 6.1.15. Linear Polymers Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Healthcare & Medical Devices

- 6.1.19. Linear Polymers Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Agriculture

- 6.1.23. Linear Polymers Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1.26. Consumer Goods & Textiles

- 6.1.27. Linear Polymers Share Forecast, By Region (USD Billion)

- 6.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.29. Key Market Trends, Growth Factors, & Opportunities

- 6.1.30. Others

- 6.1.31. Linear Polymers Share Forecast, By Region (USD Billion)

- 6.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.33. Key Market Trends, Growth Factors, & Opportunities

- 6.1. End-Use Industry Market Overview, By End-Use Industry Segment

- Chapter 7. Linear Polymers Market – Regional Analysis

- 7.1. Linear Polymers Market Overview, By Region Segment

- 7.1.1. Global Linear Polymers Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Linear Polymers Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Linear Polymers Market Revenue, By Type, 2026 – 2035

- 7.1.4. Global Linear Polymers Market Revenue, By Manufacturing Process, 2026 – 2035

- 7.1.5. Global Linear Polymers Market Revenue, By End-Use Industry, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Linear Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Linear Polymers Market Revenue, By Type, 2026 – 2035

- 7.2.3. North America Linear Polymers Market Revenue, By Manufacturing Process, 2026 – 2035

- 7.2.4. North America Linear Polymers Market Revenue, By End-Use Industry, 2026 – 2035

- 7.2.5. U.S. Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Linear Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Linear Polymers Market Revenue, By Type, 2026 – 2035

- 7.3.3. Europe Linear Polymers Market Revenue, By Manufacturing Process, 2026 – 2035

- 7.3.4. Europe Linear Polymers Market Revenue, By End-Use Industry, 2026 – 2035

- 7.3.5. Germany Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Linear Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Linear Polymers Market Revenue, By Type, 2026 – 2035

- 7.4.3. Asia Pacific Linear Polymers Market Revenue, By Manufacturing Process, 2026 – 2035

- 7.4.4. Asia Pacific Linear Polymers Market Revenue, By End-Use Industry, 2026 – 2035

- 7.4.5. China Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Linear Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Linear Polymers Market Revenue, By Type, 2026 – 2035

- 7.5.3. The Middle-East and Africa Linear Polymers Market Revenue, By Manufacturing Process, 2026 – 2035

- 7.5.4. The Middle-East and Africa Linear Polymers Market Revenue, By End-Use Industry, 2026 – 2035

- 7.5.5. Saudi Arabia Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Linear Polymers Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Linear Polymers Market Revenue, By Type, 2026 – 2035

- 7.6.3. Latin America Linear Polymers Market Revenue, By Manufacturing Process, 2026 – 2035

- 7.6.4. Latin America Linear Polymers Market Revenue, By End-Use Industry, 2026 – 2035

- 7.6.5. Brazil Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Linear Polymers Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Linear Polymers Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Linear Polymers Market: Company Market Share, 2025

- 8.2. Global Linear Polymers Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. BASF SE

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. LyondellBasell Industries N.V.

- 9.3. ExxonMobil Corporation

- 9.4. Dow Inc.

- 9.5. SABIC (Saudi Arabian Oil Company)

- 9.6. INEOS Group Holdings S.A.

- 9.7. Chevron Phillips Chemical Company LLC

- 9.8. LG Chem Ltd.

- 9.9. Formosa Plastics Group

- 9.10. TotalEnergies SE

- 9.11. Braskem S.A.

- 9.12. Reliance Industries Limited

- 9.13. Sinopec Group

- 9.14. Borealis AG

- 9.15. Others.

- 9.1. BASF SE

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Healthcare Foresights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

- Chapter 12. List Of Figures

- 12.1. Figures No 1 to 50

- Chapter 13. List Of Tables

- 13.1. Tables No 1 to 46

Prominent Player

- BASF SE

- LyondellBasell Industries N.V.

- ExxonMobil Corporation

- Dow Inc.

- SABIC (Saudi Arabian Oil Company)

- INEOS Group Holdings S.A.

- Chevron Phillips Chemical Company LLC

- LG Chem Ltd.

- Formosa Plastics Group

- TotalEnergies SE

- Braskem S.A.

- Reliance Industries Limited

- Sinopec Group

- Borealis AG

- Others

FAQs

The key players in the market are BASF SE, LyondellBasell Industries N.V., ExxonMobil Corporation, Dow Inc., SABIC (Saudi Arabian Oil Company), INEOS Group Holdings S.A., Chevron Phillips Chemical Company LLC, LG Chem Ltd., Formosa Plastics Group, TotalEnergies SE, Braskem S.A., Reliance Industries Limited, Sinopec Group, Borealis AG, Others.

Environmental rules are changing the linear polymers market in many ways at the same time. The EU’s Packaging and Packaging Waste Regulation, which went into effect in February 2025, requires polymer packaging to have a certain amount of recycled content. This creates a structural demand for certified recycled polyethylene and polypropylene. Rules in the EU, UK, India, and many other places are limiting the use of single-use plastics in certain products, such as straws, plates, and cutlery. This means that materials must be replaced or products must be redesigned. Extended producer responsibility programs in Europe, Canada, and growing Asian markets are adding the costs of managing products at the end of their lives to the price of polymers. This makes it more profitable to design products that can be recycled. At the same time, rules that require vehicles to be more fuel-efficient and produce less CO₂ indirectly increase the demand for polymers in automotive lightweighting applications. These changing rules are speeding up the industry’s move toward sustainable, circular polymer systems and giving producers with advanced environmental performance capabilities unique business opportunities.

Changes in the prices of raw materials, especially crude oil, have a direct effect on production costs and profits. Strict rules about the environment that have to do with making and getting rid of polymers are also getting in the way. Even though these are problems, ongoing research and development efforts focused on linear polymers that are biodegradable and sustainable are expected to ease these worries and open up new growth opportunities in the next few years. Other problems include the quick growth of bio-based and biodegradable alternatives that could replace traditional linear polymers in applications that care about sustainability, higher costs of compliance due to stricter recycled content requirements, and more competition from producers in areas with low-cost feedstock advantages that put pressure on margins in global commodity polymer markets.

The global linear polymers market is expected to grow from USD 285.6 billion in 2026 to about USD 432.5 billion by 2035, with a compound annual growth rate (CAGR) of 4.7%. Growth will be driven by more applications in packaging, automotive, construction, and healthcare, more use of bio-based and recycled-content polymer grades, more polymer-for-metal substitution in structural and functional applications, and population growth and rising living standards in emerging economies, which will lead to more polymer consumption per person.

The share of the revenue is anticipated to remain the highest in the Asia Pacific as the region is projected to have over two-fifths of all the market share worldwide during the forecast period. This can be attributed to the fact that China has the largest scale of production and consumption, the region is the foremost producer of electronics and consumer goods, and the demand for packaging and construction is increasing at a very high rate in the developing economies in Asia. The largest portion of the world market is in North America, where estimates indicate that more than 40% of all revenue is in North America. This is due to the fact that the U.S. polymer sector is so large, and the region is likely to retain a large portion of it due to its competitive standpoint in terms of feedstock and advanced end-user needs.

During the forecast period, Asia Pacific is expected to have the highest CAGR. This is because China, India, and Southeast Asian countries are industrializing quickly, which is driving demand in the automotive, packaging, construction, electronics, and consumer goods industries. India and Southeast Asian countries like Vietnam, Thailand, and Indonesia are expected to have the fastest growth rates in Asia Pacific. This is because their manufacturing sectors are growing quickly and their domestic consumption is improving as incomes rise and cities grow.

Technological improvements, more industrial uses, and a growing need for lightweight, high-performance materials are all important factors that are driving the growth of the linear polymers market. Because they can be easily molded and shaped, linear polymers are especially useful in industries that need to make things quickly and accurately. Their use in packaging, consumer goods, and even high-tech medical devices shows how flexible they are. More drivers include the fast growth of e-commerce, which increases the need for packaging; the fast growth of electric vehicle production, which increases the amount of automotive polymers; the growth of the construction industry in Asia and LAMEA due to urbanization; the growth of the healthcare industry, which increases the use of polymers; and government rules that require recycled content, which encourages circular polymer investment.