Polymer Casing Market Size, Trends and Insights By Material Type (Polyamide/Nylon (PA6, PA66, Co-Polyamide Multi-Layer), Polyethylene (HDPE, LDPE, LLDPE), Polypropylene (PP, Oriented PP), Polyvinylidene Chloride (PVDC, Saran-Type), Ethylene Vinyl Alcohol (EVOH, as barrier layer), Collagen-Based Polymer (Reconstituted Collagen, Collagen-Polymer Composites), Other Material Types (Cellulose-Derived, PLA, Biaxially Oriented Nylon)), By Type (Non-Edible Casings (Plastic/Polymer, Fibrous-Reinforced, Barrier Casings), Edible Casings (Collagen-Based Polymer, Cellulose Edible, Plant-Based Edible), Semi-Permeable Casings (Smoke and Moisture Permeable, Breathable Barrier)), By Application (Fresh Sausages (Bratwurst, Pork Sausage, Breakfast Links), Cooked Sausages (Frankfurters, Wieners, Bologna, Mortadella), Dry & Semi-Dry Sausages (Salami, Pepperoni, Summer Sausage, Chorizo), Deli Meats & Luncheon Products (Ham, Turkey Breast, Loaves), Specialty & Ethnic Sausages, Other Applications (Cheese Casing, Non-Meat Food Applications)), By End-User (Meat Processing Companies (Industrial Scale, Large Commercial Processors), Food Service Operators (Hotels, Restaurants, Catering, QSR), Retail Packaged Meat Producers (Supermarket Private Label, Branded Retail), Other End-Users (Artisan Producers, Export-Oriented Processors)), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

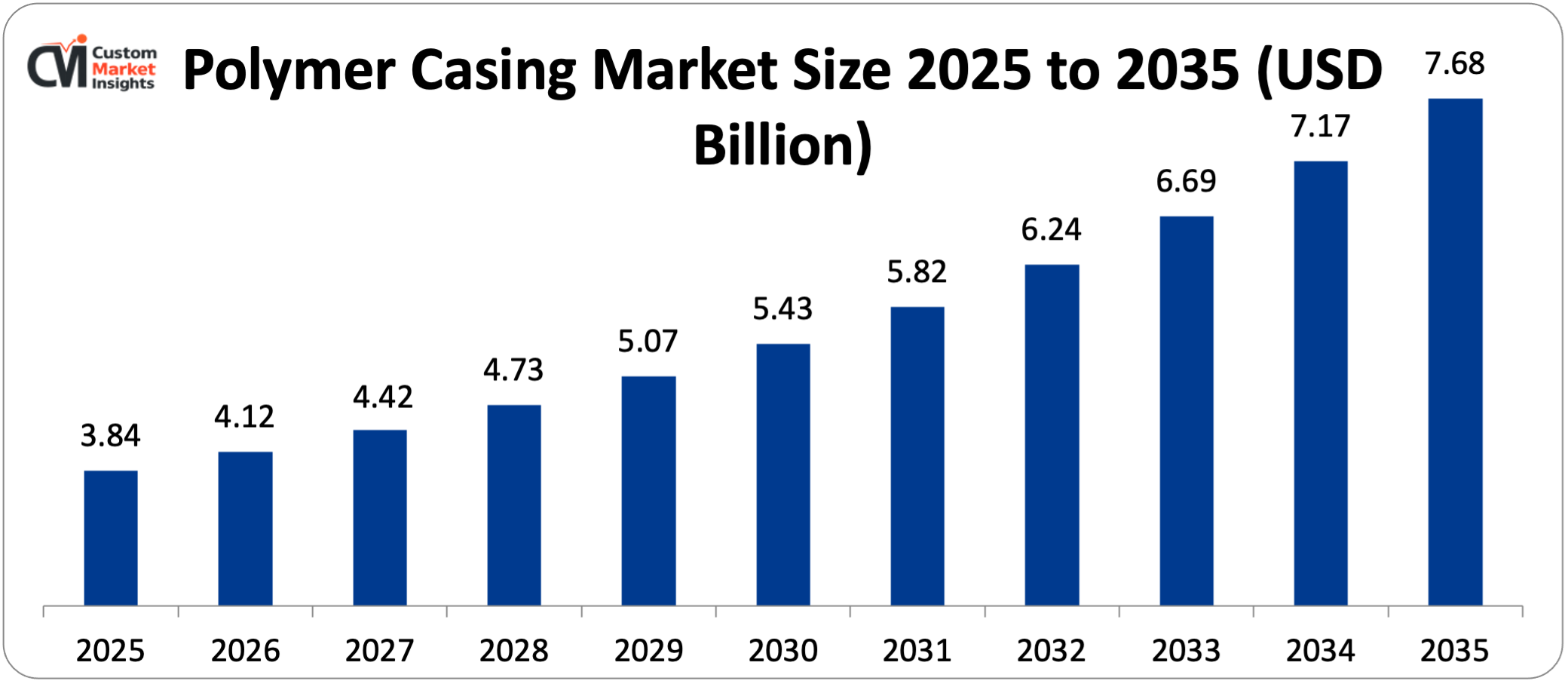

CAGR: 6.4%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | Europe |

Major Players

- Viscofan S.A.

- Viskase Companies Inc.

- Devro plc

- Kalle GmbH

- Others

Reports Description

The global polymer casing market is expected to grow from USD 4.12 billion in 2026 to about USD 7.68 billion by 2035, with a CAGR of 6.4% from 2026 to 2035. By 2025, the market size will be USD 3.84 billion.

The global meat processing industry is quickly switching to polymer casings as a better, cheaper, and cleaner alternative to natural animal-derived casings for making fresh, cooked, and processed meat products. This is because polymer casings are always the same size, have better barrier properties that protect the shelf life of the product, and don’t change in supply.

Market Highlight

- In 2025, Europe had the biggest share of the polymer casing market, with 36%.

- From 2026 to 2035, Asia Pacific is expected to grow the fastest, at a rate of 8.4% per year.

- The polyamide/nylon segment had about 34% of the market share in 2025, broken down by material type.

- The polyvinylidene chloride segment is growing the fastest, with a CAGR of 7.2% from 2026 to 2035.

- In 2025, the non-edible casings segment had the largest market share, 58%. The semi-permeable casings segment is expected to grow the fastest, at a rate of 7.8% per year, from 2026 to 2035.

- The cooked sausages segment had the largest market share in 2025, at 32%. The dry and semi-dry sausage segment is expected to grow the fastest, at a rate of 7.4% per year from 2026 to 2035.

- The meat processing companies segment had the largest market share of 62% in 2025.

Significant Growth Factors

The Polymer Casing Market Trends present significant growth opportunities due to several factors:

- Industrial Meat Processing Automation and Production Efficiency Driving Polymer Casing Adoption: The accelerating global industrialization of meat processing — driven by the labor cost, productivity, and food safety advantages of automated high-speed sausage production lines over traditional manual or semi-automated processing operations — is creating the most consequential structural demand driver for polymer casings, as automated stuffing, linking, smoking, cooking, and packaging equipment requires the dimensional precision, mechanical consistency, and controlled extensibility that polymer casings provide and that natural casings fundamentally cannot deliver at the speed and uniformity that industrial production equipment demands.

- Processed Meat Consumption Growth in Emerging Markets and Modern Retail Expansion: The accelerating global industrialization of meat processing — driven by the labor cost, productivity, and food safety advantages of automated high-speed sausage production lines over traditional manual or semi-automated processing operations — is creating the most consequential structural demand driver for polymer casings, as automated stuffing, linking, smoking, cooking, and packaging equipment requires the dimensional precision, mechanical consistency, and controlled extensibility that polymer casings provide and that natural casings fundamentally cannot deliver at the speed and uniformity that industrial production equipment demands. Modern high-speed sausage stuffing lines need casings with diameter tolerances of ±0.5 mm over continuous production runs of hours to days, consistent burst strength that prevents blowouts that stop equipment, and predictable stuffing elongation behavior that lets you control portion weight within tight specifications. Polymer casings engineered to specific processing parameters provide all of these things, while natural casings’ biological variability cannot. The total cost of ownership calculation that shows polymer casings are better than natural casings takes into account the savings in labor costs from not having to sort, soak, and inspect natural casings by hand before using them, the increase in production efficiency from not having to stop equipment and reject products because of natural casings, the increase in yield from consistent portion control made possible by the uniform dimensions of polymer casings, and the ease of managing inventory made possible by standardized polymer casing specifications compared to the quality variability of natural casings that makes processing unpredictable. Published productivity analyses of the meat processing industry show that switching from natural to polymer casings can increase throughput by 20–40% on the same production lines. This is because it cuts down on the time needed to prepare natural casings for processing, reduces the number of times equipment stops working, and works with faster automated linking speeds that natural casings can’t handle.

What are the Major Advances Changing the Polymer Casing Market Today?

- Multi-Layer Barrier Casing Technology Enabling Extended Shelf Life Performance: The expanding consumption of processed and packaged meat products across developing markets in Asia Pacific, Latin America, the Middle East, and Africa — driven by the convergence of rising per-capita incomes enabling protein-rich diet transition, rapid urbanization concentrating populations in retail-accessible urban markets, the establishment of modern supermarket and convenience store retail chains providing the refrigerated display infrastructure for packaged processed meat products, and the food service sector’s growth providing ready-to-eat sausage and luncheon meat consumption occasions — is creating a structurally growing demand base for polymer casings in geographies where natural casing-based traditional meat processing is progressively being supplemented or replaced by industrial polymer-cased meat production aligned with modern retail and food service supply chain standards. The processed meat market in China is developing rapidly due to the shift in Chinese food consumed by consumers towards higher protein diets and more convenient forms of food. This is creating much demand for the industrial polymer casings at Chinese meat processing firms such as Shuanghui (WH Group), Yurun Food, and New Hope Liuhe. Since these companies have large-scale automated production processes, they require polymer casings that are of international quality regarding barrier performance, print quality, and consistency of processing. The market size of packaged meat in India is increasing rapidly, albeit small compared to that of China. The reason behind this is that organized retail is on the rise, food delivery services are consuming more processed protein products, and urbanization is developing a consumer market of convenience foods such as packaged sausages and deli meats that require polymer casing barrier performance to achieve refrigerated and ambient shelf life. The middle-income market is increasingly favoring international food formats, such as frankfurters, mortadella, bologna, and different types of cooked sausage that were first made in European and American meat processing traditions. This is leading to growth in polymer casing demand in developing markets, which adds to the stable but mature demand for polymer casing in established Western meat processing markets.

- Sustainable and Bio-Based Polymer Casing Material Development: The commercial development and progressive market adoption of sophisticated multi-layer polymer casing architectures — in which co-extrusion technology combines multiple specialized polymer layers in a single casing wall structure, with each layer contributing specific functional properties including oxygen barrier, moisture control, mechanical strength, heat seal capability, and product contact safety — is enabling cooked and processed meat product shelf life extension beyond what single-material casings can achieve, driving market conversion from single-layer to multi-layer premium casings at meat processors whose retail customers require extended refrigerated shelf life, reduced preservative content, or modified atmosphere compatible packaging performance. The top casing manufacturers use five-layer and seven-layer co-extruded polyamide casing structures, where the layers consist of food-grade nylon, which provide contact with the product, EVOH or PVDC oxygen barrier layers, which allow less than 1 cc/m²/day of oxygen to pass through the casing, structural polyamide layers, which provide mechanical strength and heat resistance, and outer layers, which are prefer These casings have the capacity of preserving cooked sausage in the fridge for between 60 and 90 days as compared to 30 to 45 days in single layers casings. This implies that meat processors will have more time to market their products hence a better bottom line and less food wastage, as it will have more time to be sold. High-temperature barrier casings falling under the retortable polymer casing category can endure retort sterilization of 121°C over extended durations of time whilst retaining their structural integrity and excluding oxygen. This allows for shelf-stable processed meat products that don’t need to be refrigerated, which opens up new markets for ambient temperature retail channels and export markets that don’t have refrigerated distribution systems. This is the highest-performance product tier, and its technical requirements are pushing the development of polymer casing material science.

- High-Definition Printing and Branding Capability Enhancement: The progressive improvement of polymer casing surface printability — through surface treatment technologies including corona discharge, plasma activation, and primer coating systems that optimize ink adhesion on polyamide, polyethylene, and PVDC casing surfaces — combined with advances in high-definition flexographic, rotogravure, and digital printing processes applicable to tubular casing substrates, is enabling polymer casings to serve simultaneously as functional packaging and premium brand communication media whose visual impact in retail display differentiates packaged meat products and justifies the premium polymer casing cost relative to unprinted or minimally labeled natural casing alternatives. The direct-on-casing printing advantage means that the polymer casing surface carries full-color product branding, nutritional information, regulatory labeling, and origin certification through food-contact-compliant ink systems applied during casing manufacturing. This means that meat processing facilities don’t have to go through the extra step of applying printed labels to packaged meat products. This makes the production line simpler, saves money on label materials and adhesives, and reduces the need for maintenance on label application equipment, which is a big operational cost for meat processing facilities. Digital printing for polymer casings lets you print short runs, variable data, and photographic-quality images on casing surfaces without the cost of preparing plates for traditional flexographic printing. This lets you customize the packaging of premium meat products for seasonal promotions, private label retail customers, and regional market variants whose traditional printing minimum quantity requirements made too expensive to do.

Category Wise Insights

By Material Type

Why Does Polyamide/Nylon Lead the Market?

The largest material type segment consists of polyamide and nylon based casings, with approximately 34% of the overall market share in 2025. The reason is that polyamide is most suitable to be used in the industrial production of processed meat as a cooked product. It is very heat resistant so that it can be pasteurized and steamed to 130 o C; has a good oxygen barrier when combined with the appropriate barrier layer; has good mechanical strength, which enables the casing to withstand failure during high-pressure stuffing and heat treatment; has high food-contact regulatory clearance in most markets; and the casing print adheres well, which enables direct branding. The most suitable kind of polyamide casing is the co-polyamide multi-layer architecture that incorporates various polyamide layers with barrier enhancement layers of EVOH or PVDC to form five and seven layer structures. It is more expensive, as it enjoys a longer shelf life and greater oxygen barrier properties under retail packaged cooked sausage applications. The fastest-growing PVDC casings have a CAGR of 7.2% between 2026 and 2035. This is due to the fact that PVDC exhibits superior oxygen and moisture barrier properties for smoked and processed meat products which must remain stable at room temperature with the lowest possible oxygen transmission rates in order to extend shelf life during non-refrigerated display conditions. Retail outlets in emerging markets that have minimal refrigeration are more inclined to this distribution method of processed meat.

By Type

Why Do Non-Edible Casings Lead the Market?

Approximately 58% of the overall market share will comprise non-edible casings in the year 2025. It is so because the industry meat processing market requires high-performance technical casing that is geared towards production and food safety performance as opposed to consumer consumption. Non-edible polymer casings can be removed before consumption, which allows for the design freedom to include high-barrier polymer layers, antimicrobial additives, complex multi-layer architectures, and external print treatments that edible casing compositions cannot accommodate within their oral consumption safety constraints. The fastest growth is happening in semi-permeable casings, which are growing at a CAGR of 7.8% from 2026 to 2035. This is because the premium dry and fermented sausage market is growing in Asia Pacific and Latin America. Consumers there prefer traditionally smoked and naturally fermented products, which need casings that allow controlled moisture loss during maturation and smoke penetration during the smoking stage, while also providing enough mechanical support during production.

By Application

Why Do Cooked Sausages Lead the Market?

Cooked sausages make up the largest application segment, with about 32% of the total market share in 2025. This is because frankfurter, wiener, bologna, mortadella, and other similar cooked sausage formats are the most popular in industrial meat processing. They also make up the highest production volume category in the processed meat industry and are the application for which modern co-extruded polyamide and PVDC polymer casings have been most extensively engineered and qualified. The cooked sausage application’s market leadership also reflects its global geographic penetration — with frankfurter and equivalent cooked sausage formats consumed across European, North American, Latin American, Asian, and Middle Eastern markets in both premium and value product tiers — creating the broadest geographic demand base of any polymer casing application. From 2026 to 2035, the market for dry and semi-dry sausages will grow the fastest, at a rate of 7.4% per year. This is because more people around the world are interested in high-quality fermented meat products like salami, pepperoni, and European charcuterie formats. Fermented sausage snack products also fill a need for convenient protein and snack meat, and the market is starting to adopt commercially produced fermented sausage formats that were only available through specialty artisan production before.

By End-User

Why Do Meat Processing Companies Lead the Market?

In 2025, meat processing companies will make up the largest end-user group, with about 62% of the market share. This is because the industrial meat processing sector uses the most polymer casing, thanks to the large-scale automated production operations at major meat processing companies like WH Group (the world’s largest pork processor), Tyson Foods, JBS, Smithfield Foods, and other large-scale processors. These companies are the highest-value individual customers for polymer casing manufacturers because each of their facilities uses millions of meters of casing each year. Retail packaged meat producers are seeing the fastest growth in end-users, with a CAGR of 7.6% from 2026 to 2035. This is because more people are buying pre-packaged retail meat products in branded polymer-cased formats instead of traditional fresh counter service. The modern retail sector also prefers standardized packaged products that allow for self-service display and barcoded checkout. In developed markets, food safety regulations are also moving toward factory-packaged rather than retail-sliced deli meat after listeria-related regulatory action affected retail deli counter operations.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 4.12 billion |

| Projected Market Size in 2035 | USD 7.68 billion |

| Market Size in 2025 | USD 3.84 billion |

| CAGR Growth Rate | 6.4% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Material Type, Type, Application, End-User and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the European Market Size?

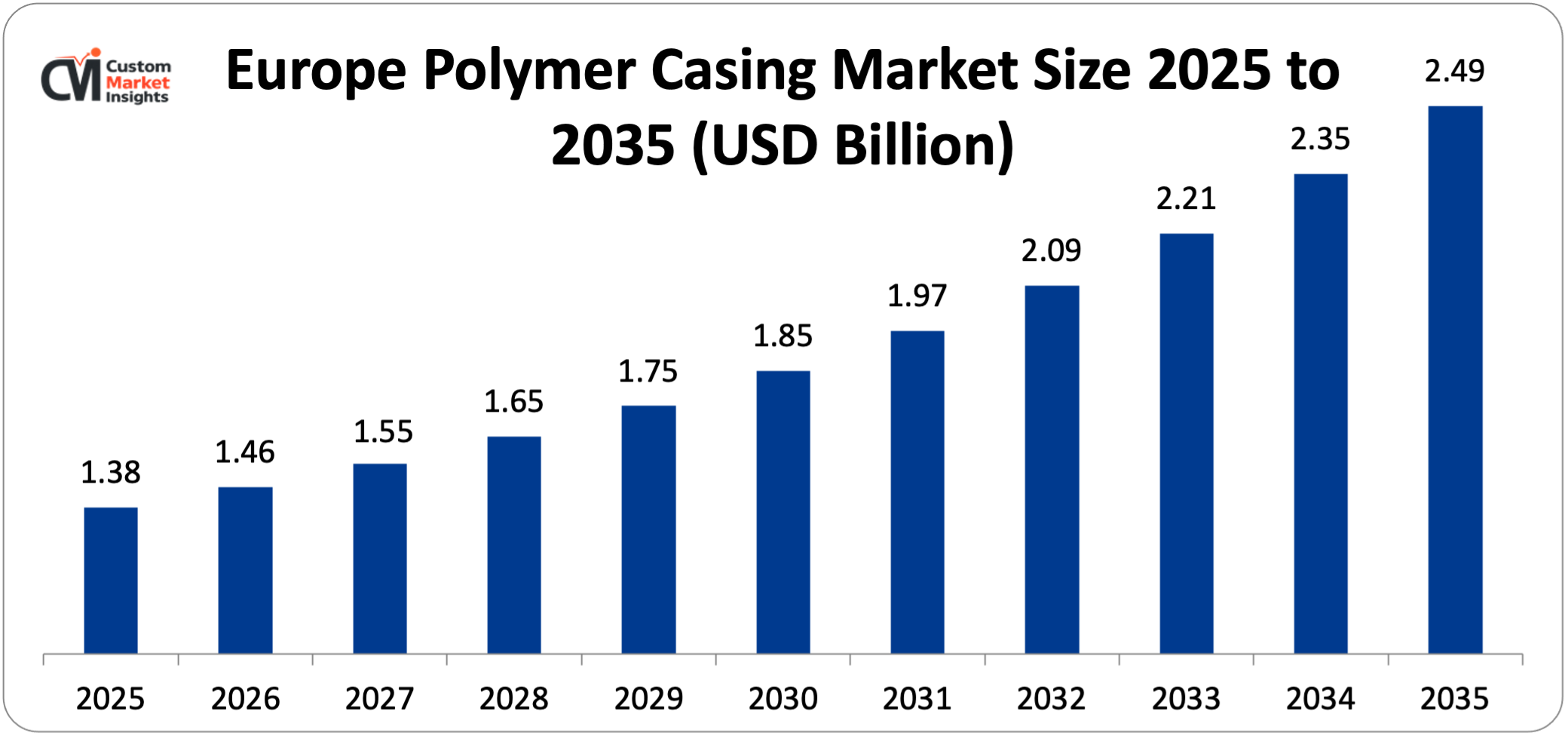

The European polymer casing market size is estimated at USD 1.38 billion in 2025 and is projected to reach approximately USD 2.49 billion by 2035, with a CAGR of 6.1% from 2026 to 2035.

Why Did Europe Dominate the Market in 2025?

By 2025, Europe will have about 36% of the world’s market share. This is because it has the highest per-capita processed meat consumption in the world, with Germany, Poland, France, Italy, and Spain being the European markets with the highest consumption. Sausage and charcuterie are deeply ingrained in food culture and dietary habits in these countries. Europe also has the highest concentration of sophisticated industrial meat processing operations that use advanced polymer casing technology.

Finally, the world’s leading polymer casing manufacturers, such as Viscofan, Kalle, ViskoTeepak, and Devro, are all based in Europe, which is where the global casing market supply is anchored. Germany is the largest meat processing market in Europe. It has some of the world’s highest per-capita sausage consumption and some of the world’s most advanced automated processing facilities, such as Tönnies, Vion, and Westfleisch.

This makes it the world’s highest-density polymer casing demand market by processing volume per unit of geographic area. The European food safety regulatory environment has pushed European meat processors toward documented, specification-controlled polymer casings. These casings are much easier to trace back to their regulatory compliance than natural casings, which makes them more likely to be used in the EU’s strict food regulatory framework.

Why is North America an Important Market?

The North American polymer casing market is expected to be worth about USD 892 million in 2025 and grow at a rate of 5.9% per year to reach about USD 1.58 billion by 2035. North America’s market is shaped by the large-scale U.S. hot dog, bologna, and luncheon meat processing industries, which produce a lot of frankfurters and cooked sausages every year. These are some of the largest single-country polymer casing consumption volumes in the world. The FDA’s listeria regulatory action has led to the gradual shift of American retail deli meat production to pre-packaged polymer-cased formats.

This is because the FDA has limited what can be done at retail deli counters. The premium and specialty sausage market is also growing, and they are using advanced multi-layer barrier casings to keep the sausages fresh for longer periods of time. The USDA’s Food Safety and Inspection Service has rules about how processed meat must be packaged. These rules say that casings used in USDA-inspected meat processing must have documented barrier performance, migration compliance, and approved food contact material status. This makes polymer casings’ documented performance look good in the U.S. regulatory environment.

Why is Asia Pacific the Fastest-Growing Market?

Asia Pacific is the fastest-growing regional market, with an expected CAGR of 8.4% from 2026 to 2035. This is because China’s processed meat market is growing so quickly, WH Group, Yurun, and New Hope Liuhe’s large-scale operations are increasing polymer casing consumption, India’s packaged meat market is growing quickly through organized retail penetration, Japan’s processed meat industry is maintaining high casing standards, South Korea’s sausage consumption culture is growing, Southeast Asia’s modern retail-serviced processed meat market is expanding, and the region’s overall protein consumption growth trajectory positions Asia Pacific as the most commercially dynamic polymer casing market globally through the forecast period.

China’s polymer casing market is expected to be worth about USD 384 million in 2025. It will grow at a CAGR of 9.2% through 2035 as Chinese processor quality standards gradually catch up with international ones and consumers prefer packaged sausage products over loose ones, which will lead to changes in retail formats. This is because China’s pork processing industry is very large and quickly industrializing, producing hundreds of thousands of tonnes of cooked and processed sausage products every year.

Why is the Middle East & Africa Region an Emerging Market?

The LAMEA region is seeing growth in the polymer casing market due to the Gulf Cooperation Council’s large halal processed meat market. Saudi Arabia, the UAE, Qatar, and Kuwait all have advanced halal meat processing operations that need polymer casings that meet halal certification standards for product contact materials. Brazil’s and Argentina’s large-scale meat export industries also need international-standard polymer casings for supply to European and Asian markets. South Africa’s developed commercial meat processing sector is also using modern polymer casing technology. Finally, the Middle East and North Africa’s growing packaged food market is driving processed protein consumption growth, which creates new polymer casing demand.

Top Players in the Market and Their Offerings

- Viscofan S.A.

- Viskase Companies Inc.

- Devro plc

- Kalle GmbH

- Nitta Casings Inc.

- ViskoTeepak

- Futamura Chemical Co. Ltd.

- Selo B.V.

- DAT-Schaub Group

- Innovia Films

- Flexopack S.A.

- Others

Key Developments

As the global demand for polymer casings in processed meat production applications grows, the market has changed a lot as companies try to improve the development of sustainable casing materials and the performance of barriers.

- In September 2024: Viscofan announced the commercial launch of its EcoVis sustainable polyamide casing series. This series has 30% post-industrial recycled polyamide content in the structural layers, but it still has the same processing performance and food contact regulatory compliance as the company’s standard polyamide casing range. It is the world’s first commercially available recycled-content polyamide meat casing to achieve EN 13430 recyclability certification through compatibility with the mechanical recycling stream for flexible polyamide films.

- In February 2025: Kalle GmbH announced a strategic investment of EUR 28 million in a new co-extrusion manufacturing line at its Wiesbaden, Germany, facility. This line will add capacity for producing seven-layer barrier polyamide casings with EVOH oxygen barrier layers that achieve oxygen transmission rates below 0.5 cc/m²/day at standard atmospheres. The goal is to target the premium extended-shelf-life retail packaged cooked sausage and deli meat market in Europe and export markets where the ultra-low oxygen transmission rate casings provide measurable commercial value in reduced markdown and waste.

The Polymer Casing Market is segmented as follows:

By Material Type

- Polyamide/Nylon (PA6, PA66, Co-Polyamide Multi-Layer)

- Polyethylene (HDPE, LDPE, LLDPE)

- Polypropylene (PP, Oriented PP)

- Polyvinylidene Chloride (PVDC, Saran-Type)

- Ethylene Vinyl Alcohol (EVOH, as barrier layer)

- Collagen-Based Polymer (Reconstituted Collagen, Collagen-Polymer Composites)

- Other Material Types (Cellulose-Derived, PLA, Biaxially Oriented Nylon)

By Type

- Non-Edible Casings (Plastic/Polymer, Fibrous-Reinforced, Barrier Casings)

- Edible Casings (Collagen-Based Polymer, Cellulose Edible, Plant-Based Edible)

- Semi-Permeable Casings (Smoke and Moisture Permeable, Breathable Barrier)

By Application

- Fresh Sausages (Bratwurst, Pork Sausage, Breakfast Links)

- Cooked Sausages (Frankfurters, Wieners, Bologna, Mortadella)

- Dry & Semi-Dry Sausages (Salami, Pepperoni, Summer Sausage, Chorizo)

- Deli Meats & Luncheon Products (Ham, Turkey Breast, Loaves)

- Specialty & Ethnic Sausages

- Other Applications (Cheese Casing, Non-Meat Food Applications)

By End-User

- Meat Processing Companies (Industrial Scale, Large Commercial Processors)

- Food Service Operators (Hotels, Restaurants, Catering, QSR)

- Retail Packaged Meat Producers (Supermarket Private Label, Branded Retail)

- Other End-Users (Artisan Producers, Export-Oriented Processors)

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Polymer Casing by Segments

- 2.1.2. Polymer Casing by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Polymer Casing Market Attractiveness Analysis, By Material Type

- 2.2.3. Polymer Casing Market Attractiveness Analysis, By Type

- 2.2.4. Polymer Casing Market Attractiveness Analysis, By Application

- 2.2.5. Polymer Casing Market Attractiveness Analysis, By End-User

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Industrial Meat Processing Automation and Production Efficiency Driving Polymer Casing Adoption

- 3.1.2. Processed Meat Consumption Growth in Emerging Markets and Modern Retail Expansion

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Polymer Casing Market – By Material Type

- 4.1. Material Type Market Overview, By Material Type Segment

- 4.1.1. Polymer Casing Market Revenue Share, By Material Type, 2025 & 2035

- 4.1.2. Polyamide/Nylon (PA6, PA66, Co-Polyamide Multi-Layer)

- 4.1.3. Polymer Casing Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Polyethylene (HDPE, LDPE, LLDPE)

- 4.1.7. Polymer Casing Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Polypropylene (PP, Oriented PP)

- 4.1.11. Polymer Casing Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Polyvinylidene Chloride (PVDC, Saran-Type)

- 4.1.15. Polymer Casing Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Ethylene Vinyl Alcohol (EVOH, as barrier layer)

- 4.1.19. Polymer Casing Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1.22. Collagen-Based Polymer (Reconstituted Collagen, Collagen-Polymer Composites)

- 4.1.23. Polymer Casing Share Forecast, By Region (USD Billion)

- 4.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.25. Key Market Trends, Growth Factors, & Opportunities

- 4.1.26. Other Material Types (Cellulose-Derived, PLA, Biaxially Oriented Nylon)

- 4.1.27. Polymer Casing Share Forecast, By Region (USD Billion)

- 4.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.29. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Material Type Market Overview, By Material Type Segment

- Chapter 5. Polymer Casing Market – By Type

- 5.1. Type Market Overview, By Type Segment

- 5.1.1. Polymer Casing Market Revenue Share, By Type, 2025 & 2035

- 5.1.2. Non-Edible Casings (Plastic/Polymer, Fibrous-Reinforced, Barrier Casings)

- 5.1.3. Polymer Casing Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Edible Casings (Collagen-Based Polymer, Cellulose Edible, Plant-Based Edible)

- 5.1.7. Polymer Casing Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Semi-Permeable Casings (Smoke and Moisture Permeable, Breathable Barrier)

- 5.1.11. Polymer Casing Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Type Market Overview, By Type Segment

- Chapter 6. Polymer Casing Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Polymer Casing Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Fresh Sausages (Bratwurst, Pork Sausage, Breakfast Links)

- 6.1.3. Polymer Casing Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Cooked Sausages (Frankfurters, Wieners, Bologna, Mortadella)

- 6.1.7. Polymer Casing Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Dry & Semi-Dry Sausages (Salami, Pepperoni, Summer Sausage, Chorizo)

- 6.1.11. Polymer Casing Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Deli Meats & Luncheon Products (Ham, Turkey Breast, Loaves)

- 6.1.15. Polymer Casing Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Specialty & Ethnic Sausages

- 6.1.19. Polymer Casing Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Other Applications (Cheese Casing, Non-Meat Food Applications)

- 6.1.23. Polymer Casing Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Polymer Casing Market – By End-User

- 7.1. End-User Market Overview, By End-User Segment

- 7.1.1. Polymer Casing Market Revenue Share, By End-User, 2025 & 2035

- 7.1.2. Meat Processing Companies (Industrial Scale, Large Commercial Processors)

- 7.1.3. Polymer Casing Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Food Service Operators (Hotels, Restaurants, Catering, QSR)

- 7.1.7. Polymer Casing Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Retail Packaged Meat Producers (Supermarket Private Label, Branded Retail)

- 7.1.11. Polymer Casing Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Other End-Users (Artisan Producers, Export-Oriented Processors)

- 7.1.15. Polymer Casing Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End-User Market Overview, By End-User Segment

- Chapter 8. Polymer Casing Market – Regional Analysis

- 8.1. Polymer Casing Market Overview, By Region Segment

- 8.1.1. Global Polymer Casing Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Polymer Casing Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Polymer Casing Market Revenue, By Material Type, 2026 – 2035

- 8.1.4. Global Polymer Casing Market Revenue, By Type, 2026 – 2035

- 8.1.5. Global Polymer Casing Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Polymer Casing Market Revenue, By End-User, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Polymer Casing Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Polymer Casing Market Revenue, By Material Type, 2026 – 2035

- 8.2.3. North America Polymer Casing Market Revenue, By Type, 2026 – 2035

- 8.2.4. North America Polymer Casing Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Polymer Casing Market Revenue, By End-User, 2026 – 2035

- 8.2.6. U.S. Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Polymer Casing Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Polymer Casing Market Revenue, By Material Type, 2026 – 2035

- 8.3.3. Europe Polymer Casing Market Revenue, By Type, 2026 – 2035

- 8.3.4. Europe Polymer Casing Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Polymer Casing Market Revenue, By End-User, 2026 – 2035

- 8.3.6. Germany Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Polymer Casing Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Polymer Casing Market Revenue, By Material Type, 2026 – 2035

- 8.4.3. Asia Pacific Polymer Casing Market Revenue, By Type, 2026 – 2035

- 8.4.4. Asia Pacific Polymer Casing Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Polymer Casing Market Revenue, By End-User, 2026 – 2035

- 8.4.6. China Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Polymer Casing Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Polymer Casing Market Revenue, By Material Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Polymer Casing Market Revenue, By Type, 2026 – 2035

- 8.5.4. The Middle-East and Africa Polymer Casing Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Polymer Casing Market Revenue, By End-User, 2026 – 2035

- 8.5.6. Saudi Arabia Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Polymer Casing Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Polymer Casing Market Revenue, By Material Type, 2026 – 2035

- 8.6.3. Latin America Polymer Casing Market Revenue, By Type, 2026 – 2035

- 8.6.4. Latin America Polymer Casing Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Polymer Casing Market Revenue, By End-User, 2026 – 2035

- 8.6.6. Brazil Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Polymer Casing Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Polymer Casing Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Polymer Casing Market: Company Market Share, 2025

- 9.2. Global Polymer Casing Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Viscofan S.A.

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Viskase Companies Inc.

- 10.3. Devro plc

- 10.4. Kalle GmbH

- 10.5. Nitta Casings Inc.

- 10.6. ViskoTeepak

- 10.7. Futamura Chemical Co. Ltd.

- 10.8. Selo B.V.

- 10.9. DAT-Schaub Group

- 10.10. Innovia Films

- 10.11. Flexopack S.A.

- 10.12. Others.

- 10.1. Viscofan S.A.

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 38

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Viscofan S. A.

- Viskase Companies Inc.

- Devro plc

- Kalle GmbH

- Nitta Casings Inc.

- ViskoTeepak

- Futamura Chemical Co. Ltd.

- Selo B.V.

- DAT-Schaub Group

- Innovia Films

- Flexopack S.A.

- Others

FAQs

The key players in the market are Viscofan S.A., Viskase Companies Inc., Devro plc, Kalle GmbH, Nitta Casings Inc., ViskoTeepak, Futamura Chemical Co. Ltd., Selo B.V., DAT-Schaub Group, Innovia Films, Flexopack S.A., Others.

Government rules have a big effect on the polymer casing market. For example, food contact material rules control the chemical makeup and migration performance of casings that come into contact with meat products. Food product labeling rules decide whether non-edible casings need to be disclosed to consumers. Food safety rules set the hygiene and process control standards that casings must meet when they are used in meat processing. The EU’s Regulation 10/2011 on plastic materials and articles intended to contact food—establishing the positive list of authorized monomers, additives, and polymer starting substances, overall migration limits of 60 mg/kg of food, and specific migration limits for individual regulated substances — provides the comprehensive food contact material regulatory framework that European polymer casing manufacturers must comply with and document for each casing composition, with compliance requiring extensive chemical characterization, migration testing, and supplier declaration documentation that represents significant regulatory compliance investment. The U.S. FDA’s food contact material framework sets the standard for polymer casings used in the U.S. Polymers are regulated under 21 CFR Parts 170–189 Food Additives, and 21 CFR Part 177 Indirect Food Additives on polymers. USDA-inspected meat processing, the USDA FSIS Review of Packaging Materials program, which requires that a manufacturer demonstrate that his or her packaging material is safe before it can be used in federally inspected meat processing. The GB standards of plastics in contact with food, such as the GB 9685 standard of permitted additives to food contact materials and the GB 4806 series standards of some types of materials are the regulations that domestic and imported polymer casings must adhere to to be used in the Chinese meat processing industry. As China’s food contact material standards get stricter, casing manufacturers are encouraged to create complete Chinese regulatory compliance documentation in addition to their existing EU and FDA compliance packages.

The price of polymer casings changes a lot depending on the type of material, the layer architecture, the functional specification, and the number of orders. Standard single-layer polyethylene fresh sausage casings are the most cost-effective polymer casing tier for fresh link sausage applications in price-sensitive markets. In commercial volumes, they cost between USD 0.80 and USD 1.80 per meter. This is the entry tier of the polymer casing market, and their prices must compete with natural hog casings with the same diameter specifications. Standard co-polyamide cooked sausage casings are the most common type of polyamide used to make frankfurters, bologna, and mortadella. They cost between $1.50 and $3.50 per meter, depending on the caliber, print requirement, and complexity of the specifications. Premium five-layer barrier polyamide casings with EVOH oxygen barrier incorporation — targeting extended shelf life retail packaged cooked sausage applications — are priced at USD 3.50–USD 7.00 per meter, with the pricing premium over standard co-polyamide justified by the documented shelf life extension value in reduced markdown, lower food waste, and extended distribution window. The premium technology tier includes seven-layer ultra-barrier casings that allow oxygen to pass through at a rate of less than 0.5 cc/m²/day. These casings cost USD 6.00 to USD 12.00 per meter because they have a 90-day shelf life that allows for retail distribution economics that standard casings can’t support. PVDC-coated high-barrier casings for ambient stable smoked products, which can be displayed without refrigeration, cost between USD 4.00 and USD 9.00 per meter. This is because PVDC barrier systems are more expensive than polyamide alternatives. The difference in price between polymer casings and natural casings (natural hog casings cost $2.00 to $5.00 per meter in calibrated form) means that premium polymer casings cost a lot more than natural casings. Meat processors are willing to pay these higher prices because they are more efficient, last longer, and are more consistent than natural casings.

Based on current analysis, the market is projected to reach approximately USD 7.68 billion by 2035, driven by Asia Pacific’s processed meat industrialization adding China’s, India’s, and Southeast Asian markets to the mainstream industrial polymer casing adoption wave progressively displacing natural casings across these large population markets, the premium multi-layer extended shelf life casing segment growing significantly as retail supply chain sustainability and waste reduction targets motivate adoption of higher-performance casings that reduce food waste, the plant-based meat alternative market generating a growing vegan-compatible edible casing segment that supplements the conventional meat casing market with a fast-growing adjacent application, active and intelligent casing functionality adoption expanding as food safety regulatory requirements and brand differentiation motivation drive premium functional casing investment, and sustainable bio-based and recyclable-content casing development achieving commercial scale as retail chain sustainability requirements create supply chain mandates that motivate meat processor casing specification updates across major European and North American markets, at a CAGR of 6.4% from 2026 to 2035.

Europe is expected to maintain the highest revenue share through the forecast period, commanding approximately 36% of global market share in 2025, based on the continent’s highest per-capita processed meat consumption establishing the largest aggregate demand base for polymer casings, the concentration of the world’s largest and most technically advanced industrial meat processing operations deploying sophisticated polymer casing technology, the headquarters location of world-leading polymer casing manufacturers, including Viscofan, Kalle, ViskoTeepak, and Devro providing both commercial operations concentration and technology development proximity, the EU’s stringent food contact material regulatory framework driving documented polymer casing compliance adoption over natural casings, and the European retail sector’s sustainability requirements driving premium recycled and recyclable casing adoption that sustains European market value leadership despite volumetric growth being fastest in Asia Pacific.

The Asia Pacific region is expected to grow the fastest, with a CAGR of 8.4% during the forecast period. This is because China’s polymer casing market is expected to grow at a CAGR of 9.2% to reach about USD 384 million in 2025. This is because Chinese processed meat industrialization is gradually adopting international quality standard polymer casings at WH Group, Yurun, and other large-scale processors. India’s emerging packaged meat market is also growing quickly through organized retail and food delivery channel expansion. Southeast Asia’s modern retail-serviced processed meat market is also expanding. Japan’s premium sausage market is also continuing to adopt polymer casings, and South Korea’s growing sausage consumption culture is also driving industrial polymer casing demand at Korean meat processors.

The Global Polymer Casing Market is predicted to experience substantial growth due to the industrial meat processing automation trend requiring dimensional precision, mechanical consistency, and controlled extensibility that polymer casings provide and that natural casings cannot match at industrial production speeds, published meat processing industry productivity analyses documenting 20–40% throughput improvement achievable through conversion from natural to polymer casings through elimination of natural casing preparation time and compatibility with faster linking speeds, the global processed meat consumption growth in Asia Pacific — particularly China and India’s rapidly expanding packaged meat markets driven by rising incomes, urbanization, and modern retail penetration — creating structurally growing demand for industrial polymer-cased production, Kalle’s seven-layer EVOH barrier casing enabling 90-day frankfurter shelf life representing a 50% extension over five-layer alternatives demonstrating the commercial value of advanced multi-layer casing technology, Viscofan’s EcoVis recycled-content casing achieving EN 13430 recyclability certification meeting retail chain sustainability supply requirements, the EU Regulation 10/2011 food contact material regulatory framework establishing documented migration compliance requirements that polymer casings satisfy more comprehensively than natural casings, Devro’s plant-based edible casing addressing the vegan sausage market’s incompatibility with animal-derived collagen casings creating a new polymer casing application category, and active antimicrobial casing functionalities providing documented Listeria control performance that food safety-conscious large retail chain meat supplier qualification programs are progressively requiring.