Metalworking Lubricants Market Size, Trends and Insights By Product Type (Cutting Fluids, Straight Cutting Oils, Water-Miscible Cutting Fluids, Grinding Fluids, Specialty Cutting Oils, Forming Fluids, Stamping & Drawing Oils, Forging Lubricants, Rolling Oils, Wire Drawing Lubricants, Quenching Fluids, Water-Based Quenchants, Polymer Quenchants, Oil Quenchants, Rust Preventives & Cleaners, Solvent-Based Rust Preventives, Water-Based Rust Preventives, Alkaline Cleaners, Other Product Types), By Formulation (Neat Oils, Soluble Oils, Semi-Synthetic Fluids, Synthetic Fluids, Other Formulations), By Application (Turning & Milling, Drilling & Grinding, Metal Forming & Stamping, Honing & Lapping, Heat Treatment, Other Applications), By End Use Industry (Automotive, Aerospace & Defense, General Manufacturing & Engineering, Medical Devices, Energy & Power Generation, Other End Use Industries), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 5.5%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | LAMEA |

| Largest Market: | Asia Pacific |

Major Players

- Fuchs Petrolub SE

- Blaser Swisslube AG

- Henkel AG & Co. KGaA

- Castrol Limited (BP)

- Others

Reports Description

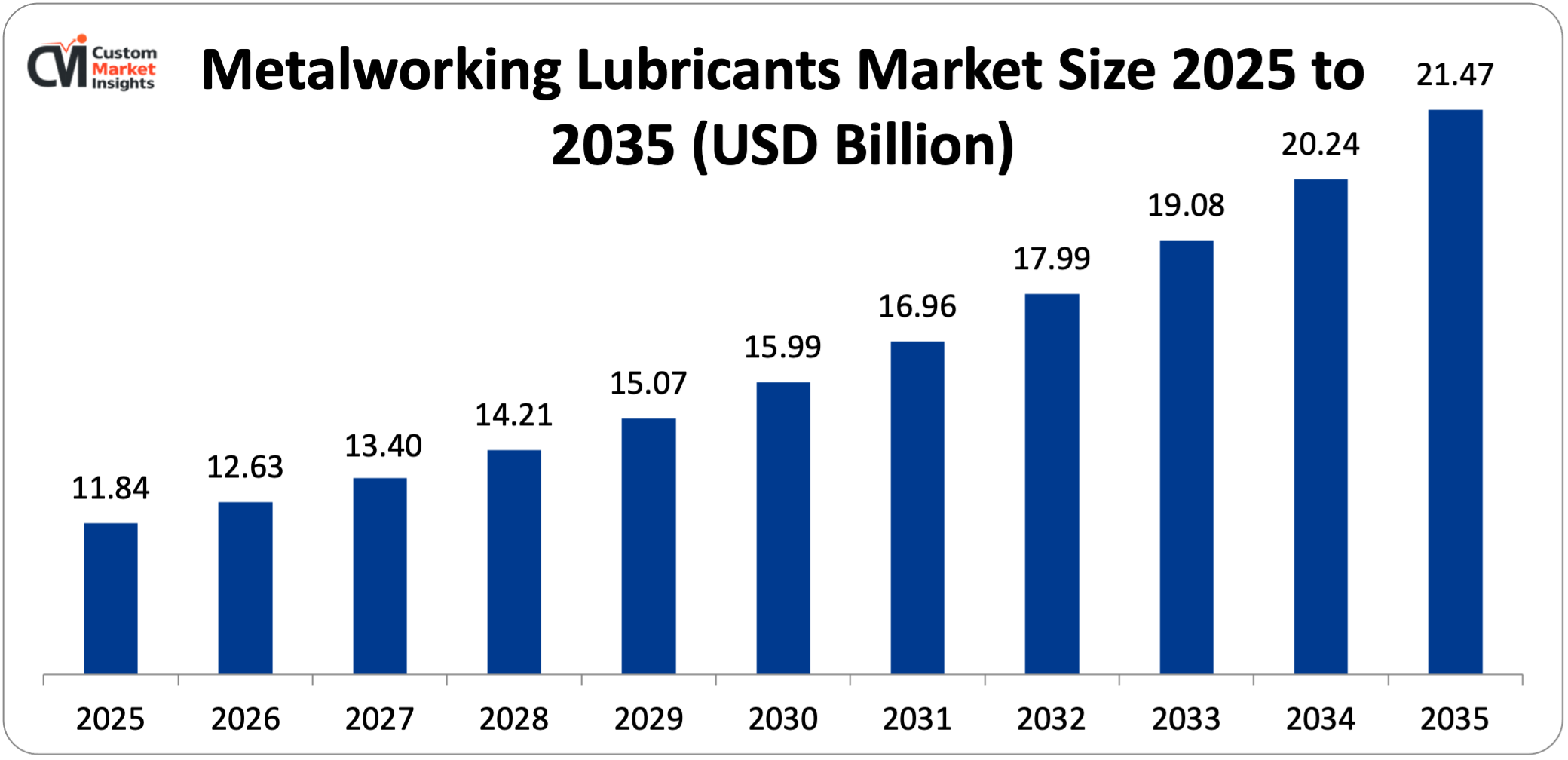

The global market for metalworking lubricants is expected to grow from USD 12.63 billion in 2026 to about USD 21.47 billion by 2035, with a compound annual growth rate (CAGR) of 5.5% from 2026 to 2035.

The market is growing because of a number of factors, including the steady growth of global manufacturing output in the automotive, aerospace, general engineering, and medical device industries the shift toward high-performance synthetic and semi-synthetic lubricant formulations driven by precision machining requirements the growing focus on worker health and environmental compliance driving reformulation away from hazardous conventional chemistries; the expansion of metalworking activity in emerging Asian and Latin American manufacturing economies; and the rising demand for specialized lubricants that work with advanced lightweight alloys like titanium, high-temperature superalloys, and aluminum-intensive vehicle architectures.

Market Highlight

- Asia Pacific had the biggest share of the metalworking lubricants market in 2025, with 43%. This was because the region is the world’s largest producer of cars, electronics, and general engineering.

- Europe is expected to keep the second-largest market share at 26% in 2025. This is because the region has a lot of precision engineering, aerospace manufacturing, and automotive production, and strict environmental and worker safety standards are pushing the use of premium lubricants.

- Cutting fluids made up about 41% of the market in 2025, showing how important they are for the most common metal removal tasks done in manufacturing around the world.

- The rust preventives and cleaners segment is growing at a CAGR of 6.2% from 2026 to 2035. This is because the need for surface preparation is growing in precision aerospace and medical device manufacturing.

- By formulation, soluble oils held about 33% of the market in 2025. This was because they were cost-effective, worked well in a variety of situations, and were already widely used in general machining.

- Synthetic fluids segment is expanding at the highest rate of 7.8% between the years 2026 and 2035. This is because it has done better in high-speed high precision machining, life benefits of longer sump, and increased preference by regulators towards oil-free formulations, which enhance the safety of workers.

- The largest market share in 2025 was in the automotive industry, which stood at 38%. This has put the production of vehicles and the giant supply chain as the primary source of the global demand for metalworking lubricants.

Significant Growth Factors

The Metalworking Lubricants Market Trends present significant growth opportunities due to several factors:

- Expanding Global Automotive Manufacturing Activity and Electrification Driven Metalworking Demand Transformation: The automotive industry’s sustained position as the dominant end use sector for metalworking lubricants — contributing approximately 38% of global market revenue in 2025 — reflects both the extraordinary scale of global vehicle production, estimated at 93.5 million units in 2024, and the exceptional metalworking intensity of automotive manufacturing, encompassing engine block and cylinder head machining, transmission gear grinding, driveshaft turning, brake component forming, body panel stamping, and hundreds of additional precision metal removal and forming operations performed across vehicle assembly. Metalworking lubricants are needed for dozens of different machining and forming operations along the component supply chain for every passenger vehicle made. For example, a typical mid-size passenger car has more than 2,000 different metal parts made through operations that use cutting, forming, quenching, or rust-preventive lubricant products. The global automotive production base is growing in Asia, especially in India, where vehicle production is expected to rise from 5.9 million units in 2024 to 10 million units per year by 2030. Southeast Asian manufacturing hubs like Thailand, Indonesia, and Vietnam are also attracting investment from OEMs and Tier 1 suppliers. This is causing a corresponding increase in the demand for metalworking lubricants in markets where lubricant penetration and formulation sophistication are currently lower than in established automotive manufacturing regions. The transition to electrification is changing the demand for automotive metalworking lubricants instead of getting rid of them. For example, battery electric vehicles get rid of the engine block, crankshaft, camshaft, and transmission gear machining operations that used to use a lot of cutting fluid, but they also create new metalworking applications like electric motor housing precision machining to tight tolerances (0.1–0.3 millimeters), battery enclosure aluminum die casting and machining, copper hairpin winding and forming for electric motor stators, and heat sink aluminum milling for power electronics thermal management. Each of these new applications needs specialized lubricant formulations that are optimized for the specific material and machining characteristics of EV-specific component manufacturing. The overall impact of vehicle electrification on metalworking lubricant demand is thought to be neutral on a per-vehicle basis at the current rate of EV adoption. This is because new EV-specific machining applications are replacing ICE powertrain operations that have been phased out. This keeps total lubricant consumption levels the same while shifting the formulation mix toward cutting fluids that work best with aluminum and forming lubricants that work best with copper.

- Rising Demand for Precision Machining Lubricants Supporting Aerospace, Medical Device, and Advanced Manufacturing Growth: Beyond automotive, sustained growth in aerospace manufacturing, medical device production, and precision engineering is generating expanding demand for the most technically demanding and highest-value metalworking lubricant formulations, as these industries machine difficult-to-cut materials, including titanium alloys, nickel-based superalloys, cobalt chrome, and hardened stainless steels that impose severe tribological challenges on cutting tools and require carefully formulated lubricant chemistry to achieve acceptable tool life, surface finish quality, and dimensional accuracy. The global aerospace manufacturing industry is in a sustained recovery and expansion phase following the COVID-19 production disruption: Airbus delivered 766 aircraft in 2024 and targets 800+ annually from 2025, while Boeing is rebuilding production rates following quality and labor challenges, with the combined commercial aircraft backlog of approximately 14,000 aircraft representing over a decade of production at current rates and providing exceptional long-term demand visibility for aerospace metalworking lubricants consumed in airframe structure machining, engine disk and blade manufacturing, landing gear component turning, and fastener forming operations. Titanium is one of the most lubricant-demanding materials to machine because it has a low thermal conductivity that causes heat to build up at the cutting zone, a high chemical reactivity that causes tool material diffusion wear, and a low elastic modulus that causes springback that lowers dimensional accuracy. To get good machining economics, you need specialized titanium-optimized cutting fluids with better extreme pressure additive systems, high lubricity ester base stocks, and effective cooling capabilities. The same goes for the demand for high-quality lubricants in the medical device industry. For example, machining cobalt-chrome and titanium alloy femoral components, spinal implants, and hip cups to surface roughness values below 0.1 μm. Ra requires ultra-clean lubricants that are free of biological contaminants and can be used in the cleaning validation processes required by FDA quality system regulations and ISO 13485 medical device quality management standards.

What are the Major Advances Changing the Metalworking Lubricants Market Today?

- Transition to Synthetic and Bio-Based Lubricant Formulations Driven by Environmental Compliance and Performance Advantages: The largest formulation-level trend that is redefining the metalworking lubricants market is the gradual replacement of traditional mineral oil-based products, neat oils and soluble oils made by refining petroleum, with synthetic and semi-synthetic and more bio-based products, which have multiple benefits of high performance, better environmental profile, improved worker health and safety aspects, and longer fluid service life, which lowers the total cost of Completely synthetic metalwork fluids – water-miscible types that do not include mineral oil and which typically are polyalkylene glycol (PAG)-based, ester-based, or organic amine-based – have numerous performance advantages in precision and high-speed machining. These advantages are improved thermal stability, thus enabling higher cutting speeds without damaging the fluid; improved biostability, thus extending sump life to 12–24 months or more in well-managed systems; reduced foaming tendency, which is significant in high-pressure coolant delivery systems that operate at pressures above 70 bar; and a cleaner machined surface finish, which makes it easier to coat and assemble parts. Synthetic fluids segment will experience the highest growth between 2026 and 2035 with the CAGR of 7.8. It will be used the most in the precision machining of automotive components, aerospace material processing, and medical device manufacturing. These three are the three areas where machining performance is of most concern and where the cost of improved sump life is most attractive. The bio-based metalworking lubricants, which are produced on the basis of vegetable oil esters or bio-based synthetic esters, are increasing at a rate of 9.3 CAGR in the wider formulation arena. This is due to regulatory pressure in Europe by REACH and, in the same way, in North America and Asia, which restricts the quantity of some mineral oil aromatic compounds that can be utilized in occupationally applied fluids. Moreover, the firms are also making investments in sustainability by incorporating bio-based content in their production consumables and the vegetable ester base stocks are biodegradable in nature, which also minimizes the environmental impact of the disposal of metalworking fluids. European regulations have been specifically effective in promoting the uptake of bio-based materials: German TRGS 611 technical regulations on hazardous substances impose restrictions on the mineral oil aromatic content of water-miscible metalworking fluids that are in effect a regulatory push towards the use of bio-based and fully synthetic base stocks across all of German manufacturing, one of the largest and most technically advanced markets in the world.

- Minimum Quantity Lubrication and Dry Machining Technologies Reshaping Cutting Fluid Market Dynamics:The emergence and progressive commercial adoption of minimum quantity lubrication (MQL) — in which metalworking lubrication is delivered as a precisely metered aerosol mist of specialized oil directly to the cutting zone at flow rates of 10–100 milliliters per hour, compared to the 10–100 liters per minute of conventional flood coolant — is fundamentally changing the economics and environmental profile of metal cutting operations, while simultaneously creating a distinct and growing market for specialized MQL lubricant formulations with unique performance requirements relative to conventional water-miscible cutting fluids. When MQL technology is used correctly, it has many operational benefits. As an example, it removes the requirement of a coolant system to cool the fluids, reducing the cost and space of machine tools. It also reduces significantly the expense of reducing fluid consumption and disposal, which is a significant expenditure in a large-volume machining setting. It also enhances the cleanliness of the workpiece because it removes the aqueous cleaning step that is typically required following flood-cooled machining and also the working environment since it eliminates the aerosol and mist that accompany the use of a flood coolant. MQL has been most advanced in the machining of powertrain parts of the automotive industry, particularly in automotive engine blocks and heads, which are of cast iron and aluminum in Germany, Japan, and South Korea. This is due to the fact that manufacturing engineers now possess sufficient experience with the process to cope with the issue of implementing MQL including how to handle evacuating the chips, how to ensure the thermal stability of the workpiece, and how to optimize the life of the tool to be used in a dry or near dry cutting environment. MQL lubricant formulations do not resemble normal cutting fluids. They are typically grounded on high-lubricity ester or polyol ester chemistry and are in use as near-dry oils as an alternative to diluted emulsions. They must also be very low in viscosity to achieve successful aerosols, have excellent lubricity in the tool-chip interface without the cooling effect of delivery systems based on flood delivery, and be compatible with either compressed air or nitrogen carrier gas delivery systems. It is predicted that the global market of MQL equipment and consumables will increase at the compound annual growth rate (CAGR) of approximately 11.2% between 2026 and 2030. It is among the most vibrant subsegments of the entire metalworking lubricants market, and the growth rates occur largely in the automotive and aerospace machining processes, where the MQL application is most economical.

- Digitalization and Industry 4.0 Integration Enabling Intelligent Fluid Management and Predictive Maintenance: The implementation of digital monitoring systems, IoT sensor networks, machine learning analytics, and automated fluid management systems to control metalworking fluid sumps using digital technologies is transforming the previously empirical and largely manual process into a data-driven operational science that optimizes fluid service life, maintains machining performance steady, reduces the number of unplanned fluid changeouts, and ensures workers are not exposed to out- The conventional metalworking fluid control involves manual sampling and laboratory analysis of the key parameters such as the fluid concentration through the refractometer, pH, microbial contamination through the dip slide, tramp oil content, and total dissolved solids. Such measurements are typically carried out weekly or monthly, which is not sufficient to detect rapid changes in fluid conditions due to microbial blooms, contamination events, or process upsets before they can cause changes in machining quality or to the health of workers. The suppliers of fluids and industrial IoT filtering companies, such as Blaser Swisslube, Fuchs Petrolub, and Quaker Houghton, have developed in-line and on-machine sensor systems via their digital service platforms. These systems can be continuously monitored in real-time to determine cutting fluid level of concentration, pH, conductivity, turbidity, and temperature. Cloud-connected data platforms send automatic alerts when parameters drift outside of defined control limits, and trend analytics can predict when fluid changes will be needed before performance starts to drop. Machine tool controllers can also adjust the fluid delivery rate based on the actual machining load conditions. Automated fluid management systems, such as centralized coolant delivery and recovery systems with in-line dosing controls that keep the target fluid concentration by continuously monitoring and adding concentrate, are becoming more popular in high-volume automotive and aerospace manufacturing settings. In these settings, consistent fluid quality directly affects machining quality and tool life consistency across large fleets of machine tools. The digital metalworking fluid management market is still in its early stages, but it is growing quickly. To stand out from the competition and keep customers, fluid suppliers are increasingly offering digital monitoring services as part of their fluid supply contracts. This helps customers get better results and gives fluid suppliers operational data streams that help them develop more targeted formulations and deliver better technical services.

Category Wise Insights

By Product Type

Why Do Cutting Fluids Lead the Metalworking Lubricants Market?

Cutting fluids will be the biggest type of product in 2025, bringing in about 41% of all market revenue. Metal cutting, which includes turning, milling, drilling, grinding, honing, and broaching, is the most common metalworking process in almost every manufacturing sector. This is why cutting fluids are used so much around the world. Cutting fluids do a lot of things at the same time during metal removal operations. They cool the tool-chip interface to keep both the cutting tool and the workpiece from getting too hot, they lubricate the tool-chip and tool-workpiece contact zones to reduce friction and wear, they flush chips and swarf from the cutting zone to keep them from getting stuck and damaging the workpiece, and they protect the machined workpiece surface from corrosion while it is being stored between operations. Because each of these functions is so important, and because cutting fluid failure can lead to premature tool wear, poor surface quality, dimensional inaccuracy, and workpiece rejection, cutting fluids are a performance-critical consumable that end users optimize for performance instead of minimum cost. The automotive industry alone uses about 2.1 billion liters of cutting fluid each year. Other industries, like aerospace, general engineering, and medical manufacturing, also use a lot of cutting fluid. This makes cutting fluids the most popular and most valuable type of metalworking lubricant.

By Formulation

Why Do Soluble Oils Lead the Formulation Segment?

Soluble oils are mineral oil-based concentrates that contain emulsifiers that make stable oil-in-water emulsions when mixed with water to typical working concentrations of 5–10%. In 2025, they will make up about 33% of the market. This is the commercial baseline formulation type that has dominated the metalworking lubricant market for decades because it is cost-effective, works well with a wide range of machining operations and workpiece materials, and manufacturing engineers have developed a lot of application knowledge and process optimization around soluble oil systems in established production environments. Soluble oils cool and lubricate at the same time in moderate-severity machining. They also have good biostability when treated with the right biocide. They come in a wide range of prices, from economy general-purpose grades to premium performance formulations with extra EP additive packages for difficult material machining. This gives purchasing and process engineering teams the freedom to find the best cost-performance balance for each machining operation. Even though more people are using synthetic and semi-synthetic alternatives in high-end applications, soluble oils still hold a large share of the market because they are cheaper in the general machining applications where performance needs don’t justify the higher cost of synthetic formulations.

By Application

Why Does Turning and Milling Lead the Application Segment?

Turning and milling operations make up the largest application segment, bringing in about 29% of market revenue in 2025. This is because these are the most common ways to remove metal in the production of automotive parts, aerospace structures, general engineering parts, and medical devices. As of 2024, there are about 4.2 million CNC machine tools in use around the world. CNC turning centers and machining centers are the most common types of metalworking machine tools. Each one needs a cutting fluid system that can hold between 100 and 2,000 liters of working solution. Drilling and grinding together make up the second-largest application, accounting for about 25% of market revenue. Grinding is especially interesting because it has very specific lubricant needs, such as high grinding fluid flow rates of 20–60 liters per minute per grinding wheel, careful thermal management to avoid grinding burn and metallurgical damage to workpiece surfaces, and effective swarf filtration to keep the fluid clean enough for precision surface generation. Metal forming and stamping make up about 22% of market revenue. These are the press shop operations that are most common in the automotive industry. The global automotive body panel stamping market uses about 380 million liters of forming lubricant each year.

By End Use Industry

Why Does Automotive Dominate the End Use Industry Segment?

Automotive manufacturing and its extended supply chain will make up about 38% of the total metalworking lubricant market revenue in 2025. This is because vehicle production involves a lot of cutting, forming, grinding, and heat treatment lubricants for engine, transmission, driveline, body, chassis, and brake components. This is the largest single industry volume of these lubricants in the world. A single automotive manufacturing complex that makes 300,000 vehicles a year usually has 800 to 1,500 CNC machine tools working on engine block machining, transmission gear machining, and component turning lines. These machines use 1 to 3 million liters of cutting fluid concentrate each year and produce an equal amount of spent fluid that needs to be managed and disposed of. The long automotive supply chain, which includes Tier 1 and Tier 2 suppliers that make precision powertrain parts, stamped body parts, forged suspension parts, and cast aluminum structural parts, increases this direct OEM consumption by a large amount. This makes automotive by far the largest end-use industry for metalworking lubricants.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 12.63 billion |

| Projected Market Size in 2035 | USD 21.47 billion |

| Market Size in 2025 | USD 11.84 billion |

| CAGR Growth Rate | 5.5% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Product Type, Formulation, Application, End Use Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

How Big is the Asia Pacific Market Size?

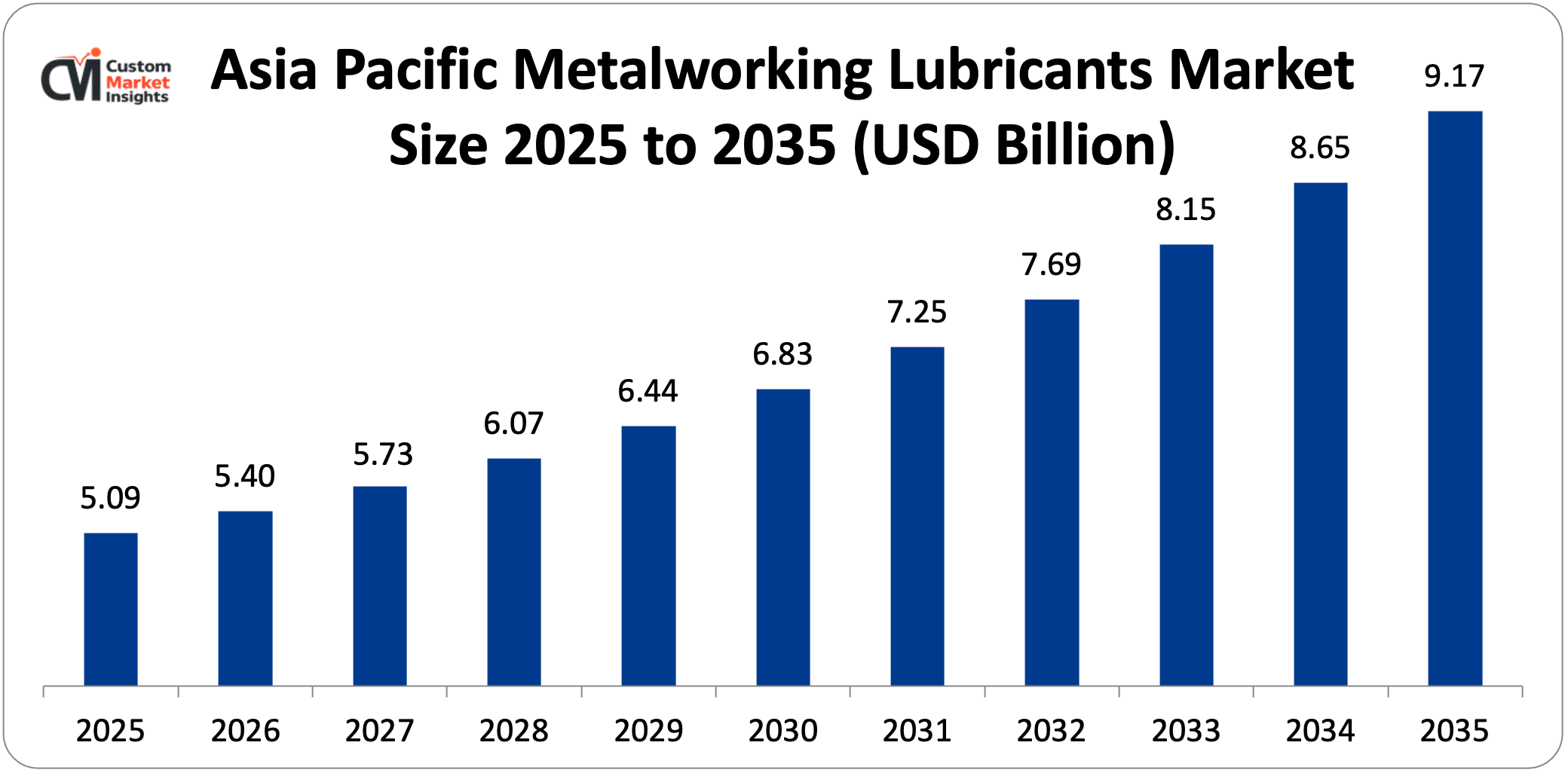

The Asia Pacific metalworking lubricants market is expected to be worth $5.09 billion in 2025 and $9.17 billion by 2035, with a compound annual growth rate (CAGR) of 6.1% from 2026 to 2035.

Why did Asia Pacific Dominate the Market in 2025?

In 2025, Asia Pacific will account for about 43% of the world’s metalworking lubricant market revenue. This is because the region is the world’s manufacturing heartland for the automotive, electronics, general engineering, and light manufacturing sectors, which are the main users of metalworking lubricants. China is the world’s largest market for metalworking lubricants by volume. This is because it is the world’s largest producer of motor vehicles, with about 30.1 million units made in 2024. It is also the world’s largest base for electronics and consumer goods manufacturing, and it has a huge general engineering and machinery manufacturing sector that uses more metalworking lubricants than any other country. Japanese metalworking lubricant demand is unique because of how advanced it is.

Japanese automotive and precision engineering manufacturers are world leaders in MQL technology adoption, high-speed machining of aluminum and cast iron, and precision grinding applications that use advanced synthetic and semi-synthetic lubricant formulations. Japanese demand is mostly for higher-value formulation segments compared to overall volume. The automotive and semiconductor equipment manufacturing industries in South Korea create a lot of demand for metalworking lubricants. The main centers of demand are Hyundai-Kia’s domestic production base and Samsung and SK Hynix’s semiconductor equipment supply chains. India is the fastest-growing market in Asia Pacific.

The automotive industry is growing quickly, the aerospace manufacturing sector is growing thanks to HAL (Hindustan Aeronautics Limited), and Tier 1 supplier investment is growing. The government’s “Make in India” initiatives are also helping domestic manufacturing in all sectors, which is increasing the demand for metalworking lubricants. This is happening as the economy-grade baseline gradually upgrades toward premium synthetic and semi-synthetic formulations as manufacturing becomes more sophisticated.

Why is Europe the Second-Largest and Most Technically Advanced Market?

In 2025, Europe will have about 26% of the world’s market revenue, worth about USD 3.08 billion. It is different from other regions because it has the most complex metalworking lubricant formulations on average, the strictest rules about lubricant composition and worker exposure, and the highest average selling price per liter of any major regional market. This is because it has a lot of aerospace, precision automotive, and medical device manufacturing that needs and justifies premium lubricant formulations.

Germany is the biggest market for metalworking lubricants in Europe. It is home to major automotive OEMs and their supply chains for precision machining, as well as world-leading machine tool manufacturers like DMG Mori (German operations), Trumpf, and Chiron, whose production facilities use specialized cutting fluids. It is also the European headquarters for major metalworking lubricant suppliers like Fuchs Petrolub, Blaser Swisslube (Switzerland), and Zeller+Gmelin.

The EU’s REACH substance restriction, the Biocidal Products Regulation that controls the use of biocides in metalworking fluids, and the EU Carcinogens and Mutagens Directive that sets occupational exposure limits for mineral oil aerosols all make metalworking lubricant formulation and use the strictest in the world. This means that all European manufacturing operations must use hydrotreated or synthetic base stocks, chlorine-free EP additive systems, and strictly controlled biocide programs.

Why is North America Experiencing Steady and Sustained Growth?

In 2025, North America will account for about 18% of global market revenue. From 2026 to 2035, it is expected to grow at a CAGR of 4.9%. This growth will be supported by continued increases in aerospace production, defense manufacturing, new manufacturing facilities built in North America due to reshoring, and the gradual shift from soluble oils to synthetic and semi-synthetic products in established manufacturing operations due to the need to comply with regulations and improve performance.

Why is the Middle East & Africa Region an Emerging Manufacturing and Lubricant Market?

By 2025, the LAMEA region will account for about 8% of global market revenue. From 2026 to 2035, it will grow at a CAGR of 6.8%, making it one of the fastest-growing regional markets. This growth is driven by Saudi Arabia’s and the UAE’s Vision 2030 and similar industrial diversification programs that are heavily investing in domestic manufacturing capacity in the petrochemical equipment, defense, and aerospace MRO sectors, which is creating demand for metalworking lubricants. Brazil’s large and diverse manufacturing base, which includes automotive, agricultural equipment, and oil and gas equipment fabrication, supports the region’s largest single national metalworking lubricant market.

South Africa’s established mining equipment and automotive manufacturing industries also contribute to this growth. Mexico is in the North America region for trade analysis, but it is also part of the larger LAMEA manufacturing growth story. The metalworking lubricant market in Mexico is growing quickly because automotive and electronics manufacturing is moving from Asia to Mexico. Major OEM manufacturing investments from Tesla, BMW, Stellantis, and many Tier 1 suppliers are increasing Mexican metalworking lubricant consumption to an estimated USD 380 million per year by 2030.

Top Players in the Market and Their Offerings

- Quaker Houghton Corporation

- Fuchs Petrolub SE

- Blaser Swisslube AG

- Henkel AG & Co. KGaA

- Castrol Limited (BP)

- TotalEnergies SE

- Chemours Company

- Buhmwoo Group

- Yushiro Chemical Industry Co. Ltd.

- Cimcool Industrial Products LLC

- Others

Key Developments

As companies in the industry try to improve their products and services and expand their capabilities, the market has changed a lot.

- In February 2025: Quaker Houghton Corporation announced the commercial launch of its QUAKERCOOL 7000 series fully synthetic cutting fluid platform specifically engineered for aluminum-intensive electric vehicle component machining, incorporating a proprietary aluminum-optimized additive system providing exceptional surface finish quality and extended sump life in high-speed CNC machining of battery enclosure housings, electric motor housings, and heat sink components manufactured from 6000 and 7000 series aluminum alloys—directly addressing the rapidly growing demand for aluminum-optimized metalworking fluid solutions driven by EV manufacturing expansion globally.

- In January 2025: Fuchs Petrolub SE announced that it was adding three new vegetable ester-based cutting fluid concentrates to its ECOCUT and PLANTOCUT bio-based metalworking fluid portfolio. These new products are aimed at European aerospace and precision engineering customers who need REACH-compliant, low-aromatic, biodegradable cutting fluid solutions. They have also achieved DIN EN ISO 9001 and AS9100D aerospace quality system certification, which means they can be used directly in Airbus and Safran Group-approved machining operations across European aerospace manufacturing facilities.

These strategic moves have helped companies strengthen their market positions, add more specialized products to their portfolios to meet new application needs, create formulations that are good for the environment and meet stricter regulatory standards, and take advantage of growth opportunities created by the growth of electric vehicle manufacturing, the ramp-up of aerospace production, and the general trend in all manufacturing sectors toward more sustainable and higher-performance metalworking lubricants.

The Metalworking Lubricants Market is segmented as follows:

By Product Type

- Cutting Fluids

- Straight Cutting Oils

- Water-Miscible Cutting Fluids

- Grinding Fluids

- Specialty Cutting Oils

- Forming Fluids

- Stamping & Drawing Oils

- Forging Lubricants

- Rolling Oils

- Wire Drawing Lubricants

- Quenching Fluids

- Water-Based Quenchants

- Polymer Quenchants

- Oil Quenchants

- Rust Preventives & Cleaners

- Solvent-Based Rust Preventives

- Water-Based Rust Preventives

- Alkaline Cleaners

- Other Product Types

By Formulation

- Neat Oils

- Soluble Oils

- Semi-Synthetic Fluids

- Synthetic Fluids

- Other Formulations

By Application

- Turning & Milling

- Drilling & Grinding

- Metal Forming & Stamping

- Honing & Lapping

- Heat Treatment

- Other Applications

By End Use Industry

- Automotive

- Aerospace & Defense

- General Manufacturing & Engineering

- Medical Devices

- Energy & Power Generation

- Other End Use Industries

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Metalworking Lubricants by Segments

- 2.1.2. Metalworking Lubricants by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Metalworking Lubricants Market Attractiveness Analysis, By Product Type

- 2.2.3. Metalworking Lubricants Market Attractiveness Analysis, By Formulation

- 2.2.4. Metalworking Lubricants Market Attractiveness Analysis, By Application

- 2.2.5. Metalworking Lubricants Market Attractiveness Analysis, By End Use Industry

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Expanding Global Automotive Manufacturing Activity and Electrification-Driven Metalworking Demand Transformation

- 3.1.2. Rising Demand for Precision Machining Lubricants Supporting Aerospace

- 3.1.3. Medical Device

- 3.1.4. and Advanced Manufacturing Growth

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Metalworking Lubricants Market – By Product Type

- 4.1. Product Type Market Overview, By Product Type Segment

- 4.1.1. Metalworking Lubricants Market Revenue Share, By Product Type, 2025 & 2035

- 4.1.2. Cutting Fluids

- 4.1.2.1. Straight Cutting Oils

- 4.1.2.2. Water-Miscible Cutting Fluids

- 4.1.2.3. Grinding Fluids

- 4.1.2.4. Specialty Cutting Oils

- 4.1.3. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Forming Fluids

- 4.1.6.1. Stamping & Drawing Oils

- 4.1.6.2. Forging Lubricants

- 4.1.6.3. Rolling Oils

- 4.1.6.4. Wire Drawing Lubricants

- 4.1.7. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1.10. Quenching Fluids

- 4.1.10.1. Water-Based Quenchants

- 4.1.10.2. Polymer Quenchants

- 4.1.10.3. Oil Quenchants

- 4.1.11. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 4.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.13. Key Market Trends, Growth Factors, & Opportunities

- 4.1.14. Rust Preventives & Cleaners

- 4.1.14.1. Solvent-Based Rust Preventives

- 4.1.14.2. Water-Based Rust Preventives

- 4.1.14.3. Alkaline Cleaners

- 4.1.15. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 4.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.17. Key Market Trends, Growth Factors, & Opportunities

- 4.1.18. Other Product Types

- 4.1.19. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 4.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.21. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Product Type Market Overview, By Product Type Segment

- Chapter 5. Metalworking Lubricants Market – By Formulation

- 5.1. Formulation Market Overview, By Formulation Segment

- 5.1.1. Metalworking Lubricants Market Revenue Share, By Formulation, 2025 & 2035

- 5.1.2. Neat Oils

- 5.1.3. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Soluble Oils

- 5.1.7. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Semi-Synthetic Fluids

- 5.1.11. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Synthetic Fluids

- 5.1.15. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1.18. Other Formulations

- 5.1.19. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 5.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.21. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Formulation Market Overview, By Formulation Segment

- Chapter 6. Metalworking Lubricants Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Metalworking Lubricants Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Turning & Milling

- 6.1.3. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Drilling & Grinding

- 6.1.7. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Metal Forming & Stamping

- 6.1.11. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Honing & Lapping

- 6.1.15. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Heat Treatment

- 6.1.19. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Other Applications

- 6.1.23. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Metalworking Lubricants Market – By End Use Industry

- 7.1. End Use Industry Market Overview, By End Use Industry Segment

- 7.1.1. Metalworking Lubricants Market Revenue Share, By End Use Industry, 2025 & 2035

- 7.1.2. Automotive

- 7.1.3. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Aerospace & Defense

- 7.1.7. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. General Manufacturing & Engineering

- 7.1.11. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1.14. Medical Devices

- 7.1.15. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 7.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.17. Key Market Trends, Growth Factors, & Opportunities

- 7.1.18. Energy & Power Generation

- 7.1.19. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 7.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.21. Key Market Trends, Growth Factors, & Opportunities

- 7.1.22. Other End Use Industries

- 7.1.23. Metalworking Lubricants Share Forecast, By Region (USD Billion)

- 7.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.25. Key Market Trends, Growth Factors, & Opportunities

- 7.1. End Use Industry Market Overview, By End Use Industry Segment

- Chapter 8. Metalworking Lubricants Market – Regional Analysis

- 8.1. Metalworking Lubricants Market Overview, By Region Segment

- 8.1.1. Global Metalworking Lubricants Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Metalworking Lubricants Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Metalworking Lubricants Market Revenue, By Product Type, 2026 – 2035

- 8.1.4. Global Metalworking Lubricants Market Revenue, By Formulation, 2026 – 2035

- 8.1.5. Global Metalworking Lubricants Market Revenue, By Application, 2026 – 2035

- 8.1.6. Global Metalworking Lubricants Market Revenue, By End Use Industry, 2026 – 2035

- 8.2. North America

- 8.2.1. North America Metalworking Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Metalworking Lubricants Market Revenue, By Product Type, 2026 – 2035

- 8.2.3. North America Metalworking Lubricants Market Revenue, By Formulation, 2026 – 2035

- 8.2.4. North America Metalworking Lubricants Market Revenue, By Application, 2026 – 2035

- 8.2.5. North America Metalworking Lubricants Market Revenue, By End Use Industry, 2026 – 2035

- 8.2.6. U.S. Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Metalworking Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Metalworking Lubricants Market Revenue, By Product Type, 2026 – 2035

- 8.3.3. Europe Metalworking Lubricants Market Revenue, By Formulation, 2026 – 2035

- 8.3.4. Europe Metalworking Lubricants Market Revenue, By Application, 2026 – 2035

- 8.3.5. Europe Metalworking Lubricants Market Revenue, By End Use Industry, 2026 – 2035

- 8.3.6. Germany Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Metalworking Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Metalworking Lubricants Market Revenue, By Product Type, 2026 – 2035

- 8.4.3. Asia Pacific Metalworking Lubricants Market Revenue, By Formulation, 2026 – 2035

- 8.4.4. Asia Pacific Metalworking Lubricants Market Revenue, By Application, 2026 – 2035

- 8.4.5. Asia Pacific Metalworking Lubricants Market Revenue, By End Use Industry, 2026 – 2035

- 8.4.6. China Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Metalworking Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Metalworking Lubricants Market Revenue, By Product Type, 2026 – 2035

- 8.5.3. The Middle-East and Africa Metalworking Lubricants Market Revenue, By Formulation, 2026 – 2035

- 8.5.4. The Middle-East and Africa Metalworking Lubricants Market Revenue, By Application, 2026 – 2035

- 8.5.5. The Middle-East and Africa Metalworking Lubricants Market Revenue, By End Use Industry, 2026 – 2035

- 8.5.6. Saudi Arabia Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Metalworking Lubricants Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Metalworking Lubricants Market Revenue, By Product Type, 2026 – 2035

- 8.6.3. Latin America Metalworking Lubricants Market Revenue, By Formulation, 2026 – 2035

- 8.6.4. Latin America Metalworking Lubricants Market Revenue, By Application, 2026 – 2035

- 8.6.5. Latin America Metalworking Lubricants Market Revenue, By End Use Industry, 2026 – 2035

- 8.6.6. Brazil Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Metalworking Lubricants Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Metalworking Lubricants Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Metalworking Lubricants Market: Company Market Share, 2025

- 9.2. Global Metalworking Lubricants Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. Quaker Houghton Corporation

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Fuchs Petrolub SE

- 10.3. Blaser Swisslube AG

- 10.4. Henkel AG & Co. KGaA

- 10.5. Castrol Limited (BP)

- 10.6. TotalEnergies SE

- 10.7. Chemours Company

- 10.8. Buhmwoo Group

- 10.9. Yushiro Chemical Industry Co. Ltd.

- 10.10. Cimcool Industrial Products LLC

- 10.11. Others.

- 10.1. Quaker Houghton Corporation

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Healthcare Foresights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

- Chapter 13. List Of Figures

- 13.1. Figures No 1 to 54

- Chapter 14. List Of Tables

- 14.1. Tables No 1 to 51

Prominent Player

- Quaker Houghton Corporation

- Fuchs Petrolub SE

- Blaser Swisslube AG

- Henkel AG & Co. KGaA

- Castrol Limited (BP)

- TotalEnergies SE

- Chemours Company

- Buhmwoo Group

- Yushiro Chemical Industry Co. Ltd.

- Cimcool Industrial Products LLC

- Others

FAQs

The key players in the market are Quaker Houghton Corporation, Fuchs Petrolub SE, Blaser Swisslube AG, Henkel AG & Co. KGaA, Castrol Limited (BP), TotalEnergies SE, Chemours Company, Buhmwoo Group, Yushiro Chemical Industry Co. Ltd., Cimcool Industrial Products LLC, Others.

Government regulations shape the metalworking lubricants market through multiple distinct mechanisms: occupational health regulations, including OSHA mineral oil mist exposure limits in the United States, the EU Carcinogens and Mutagens Directive setting occupational exposure limits for mineral oil mists in Europe, and equivalent regulations in Japan, South Korea, and Australia collectively drive manufacturers to specify lower-mist-generating synthetic and semi-synthetic formulations in preference to conventional mineral oil-based products, structurally supporting formulation upgrade trends. REACH substance restriction in the European Union — which has already restricted short-chain chlorinated paraffins and is reviewing medium-chain variants widely used as EP additives — mandates chlorine-free EP additive reformulation across European metalworking fluid products and those exported to the EU market; biocide regulations under the EU Biocidal Products Regulation impose registration requirements on all active biocide substances used in metalworking fluid preservation, creating regulatory barriers for new biocide introductions and driving the industry toward validated biocide systems with completed regulatory dossiers; environmental regulations governing metalworking fluid disposal — including wastewater discharge limits for oil content, chemical oxygen demand, and specific toxic substances — impose treatment costs that incentivize adoption of longer-life and lower-volume synthetic fluid systems that reduce disposal frequency and volume; and industrial policy incentives in India, Saudi Arabia, and Southeast Asian nations supporting domestic manufacturing investment indirectly drive metalworking lubricant demand growth by stimulating the new manufacturing capacity that consumes lubricants at operational scale.

Metalworking lubricants have a wide range of prices depending on the type of formulation and the grade of application. Fully synthetic concentrates cost USD 8–25 per liter, economy soluble oils cost USD 2–6 per liter, and semi-synthetic products cost USD 4–12 per liter. These higher prices need to be justified by lower total cost of ownership, longer sump life, less tool use, better part quality, and lower disposal costs. Aerospace-grade specialty cutting fluids for machining titanium and superalloys are the most expensive in the cutting fluid category, costing between $20 and $60 per liter of concentrate. This is because they need to be made in a way that works with exotic alloys and because there are only a few approved vendors who can get these products through strict aerospace customer approval processes. Bio-based lubricants cost 20–40% more than similar mineral oil formulations. The highest acceptance of these higher prices is in European markets, where regulatory compliance needs and corporate sustainability reporting requirements make bio-based specifications a good economic choice. Depending on the base stock and the complexity of the additive package, neat cutting oils for heavy-duty uses like broaching, gear hobbing, and tapping tough materials cost between $3 and $15 per liter. Premium sulfurized and EP-enhanced grades are at the top of this range. Long-term supply agreements of 1 to 3 years with indexed price adjustment mechanisms are common in high-volume automotive and aerospace supply relationships. These agreements give lubricant suppliers a clear picture of how much they will be supplying, while also giving customers price stability that helps them plan their production costs.

The market is expected to reach about USD 21.47 billion by 2035, based on current analysis. This is due to global manufacturing output growth in the automotive, aerospace, and industrial machinery sectors; the shift from soluble oils to synthetic and semi-synthetic products, which raises average selling prices in established manufacturing markets; manufacturing growth in India, Southeast Asia, and LAMEA, which expands the geographic demand base; digitally enabled fluid management, which extends service life and creates new service revenue streams; and the adoption of bio-based and MQL lubricants, which creates premium-priced niche segments that grow much faster than the overall market average, at a CAGR of 5.5% from 2026 to 2035.

Asia Pacific is expected to keep the biggest share of revenue throughout the forecast period, growing from 43% in 2025 to about 46% by 2035. This is because global automotive manufacturing is becoming more concentrated and expanding in China, India, and Southeast Asia. The demand for Asian metalworking lubricant formulations is also becoming more complex as quality requirements rise. At the same time, Chinese and Indian manufacturing is moving from economy-grade to semi-synthetic and synthetic formulations that increase average revenue per liter. Europe will have the highest average formulation value per liter of any region because it has strict rules about premium formulations and is home to a lot of aerospace and precision manufacturing that needs the most advanced and expensive lubricant products.

The LAMEA region is expected to grow the fastest, at a rate of 6.8% per year from 2026 to 2035. This growth will be driven by Saudi Arabia’s and the UAE’s investments in industrial diversification and manufacturing, Brazil’s large automotive and industrial manufacturing base, and the broader emerging market manufacturing expansion across the region. India has the fastest-growing individual national market in the Asia Pacific, with an estimated CAGR of 7.6%. This is because of the country’s rapidly growing automotive production, an emerging domestic aerospace manufacturing sector, and government-driven manufacturing investment under Make in India that is gradually formalizing and improving the quality of metalworking lubricant practices across Indian manufacturing industries as they move from economy to premium formulation grades to meet higher export quality standards.

The Global Metalworking Lubricants Market is predicted to experience sustained growth driven by global automotive production of 93.5 million units in 2024 and India’s vehicle production trajectory toward 10 million units annually by 2030 generating proportionate cutting and forming lubricant demand; Airbus’s 800+ annual aircraft delivery target and the combined commercial aircraft backlog of approximately 14,000 units providing exceptional long-term aerospace lubricant demand visibility; synthetic fluid adoption growing at 7.8% CAGR as precision machining performance requirements and extended sump life economics drive formulation upgrade across automotive, aerospace, and medical device manufacturing; MQL equipment and consumables market growth at approximately 11.2% CAGR creating specialized low-consumption ester-based lubricant demand; bio-based metalworking lubricant growth at approximately 9.3% CAGR driven by REACH and equivalent regulatory frameworks restricting mineral oil aromatic content in occupationally applied fluids; nanoparticle additive technology entering commercial metalworking fluid products targeting difficult-to-machine exotic alloy applications; and digital fluid management platform adoption enabling extended fluid service life and reduced operating costs that simultaneously create service revenue streams for fluid suppliers and improve total cost of ownership for manufacturing customers.