Robot Fleet Management Software Market Size, Trends and Insights By Component (Software, Service), By Robot Type (Ground Robot, Aerial Robot (Drone)), By Application (Industrial/Manufacturing, Warehouse, Logistics & Delivery, Automotive, Construction & Infrastructure, Agriculture, Healthcare, Autonomous Shuttles, Others), By Device Type (Desktop/Laptop, Smartphone, Tablet), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

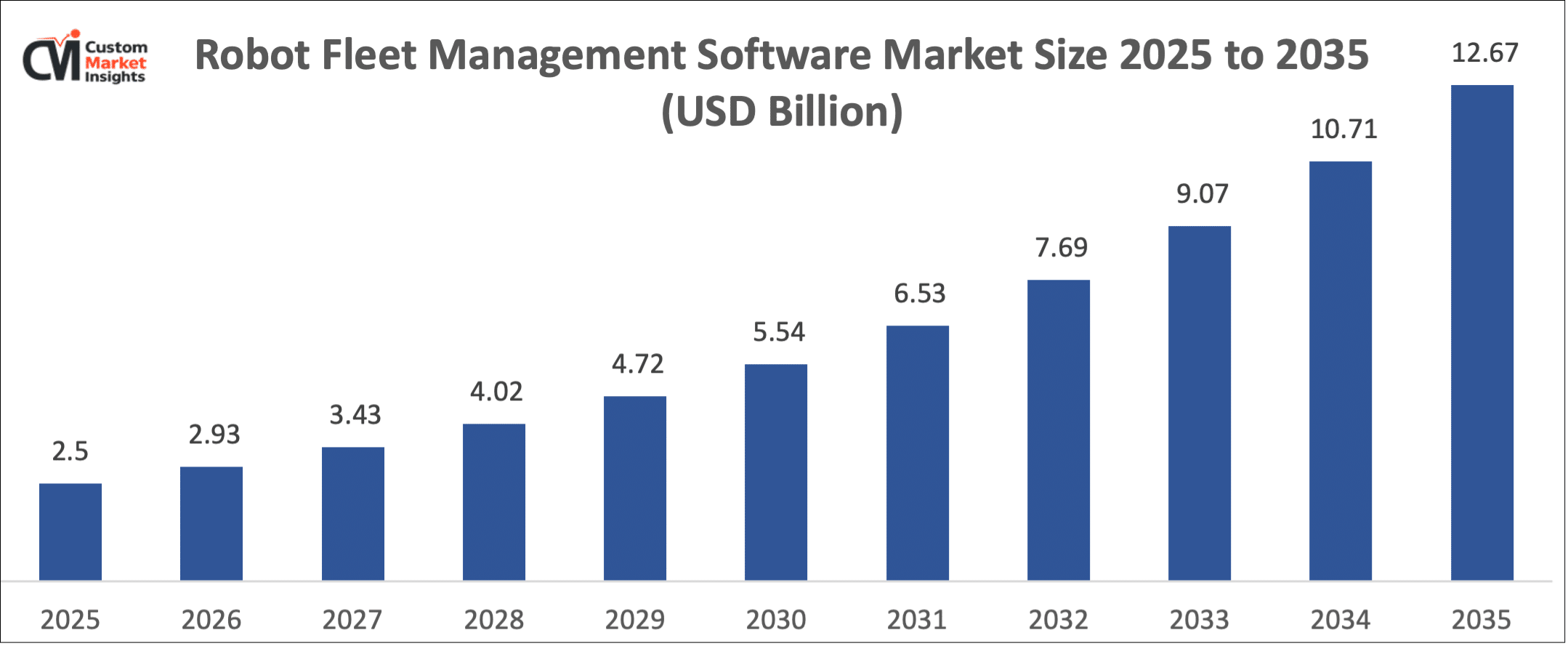

CAGR: 17.7%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | North America |

| Largest Market: | Asia Pacific |

Major Players

- ABB Ltd.

- Clearpath Robotics Inc.

- Locus Robotics

- Boston Dynamics

- Others

Reports Description

The market of robot fleet management software is estimated to reach USD 2.93 billion during the year 2026, USD 12.67 billion during the year 2035 as well as during the year 2035 with a projected CAGR of 17.7% between the years 2026 and 2035.

The growth of the market is especially related to the growing actions globally to decarbonize the environment and enhance the climate responsibility of the industrial world. Methane is regarded as one of the strongest greenhouse gases, and governments and environmental agencies implemented more stringent monitoring and reporting policies.

Market Highlight

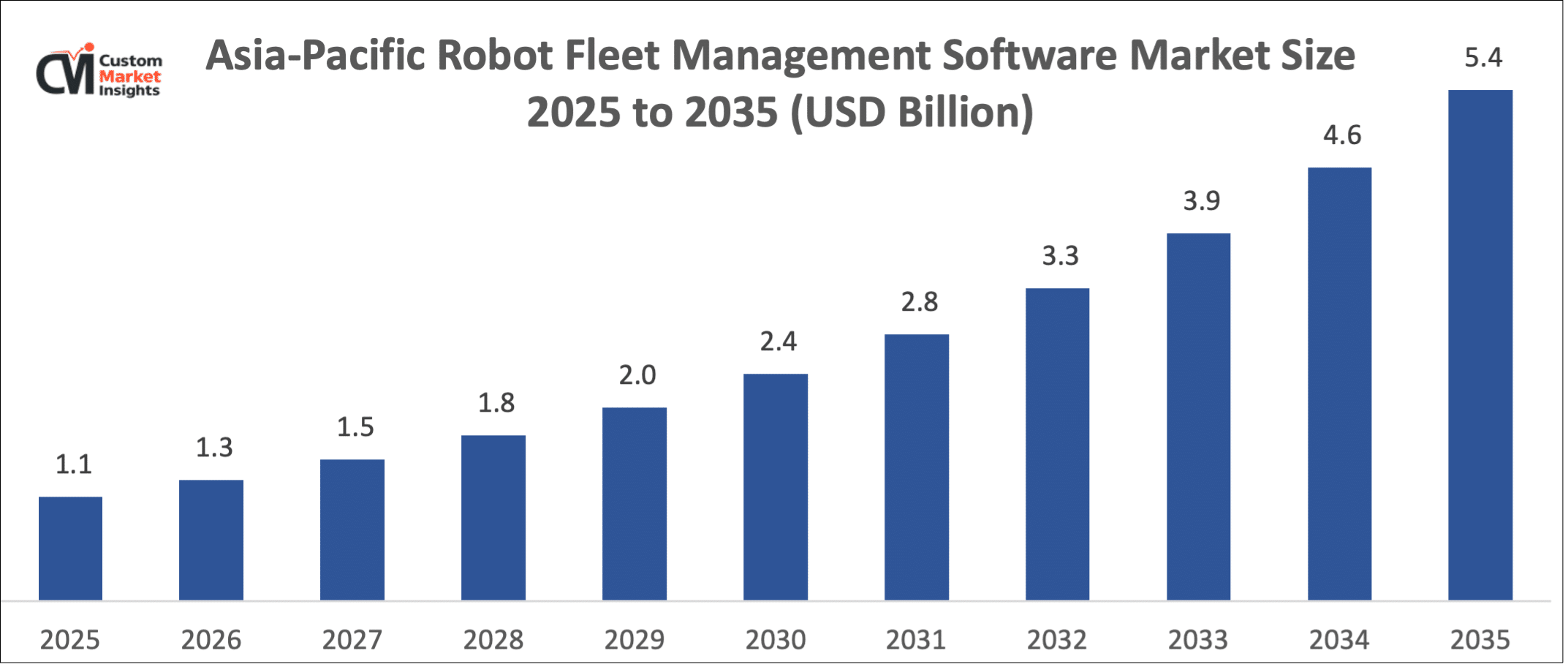

- Asia Pacific was the market leader of the robot fleet management software, holding a 45% market share in 2025.

- North America will increase by 18.1% during the years 2026 to 2035.

- The Software segment had captured 55.5% of the market share in components in 2025.

- By type of robot, the segment of Aerial Robots (Drones) will enjoy the best CAGR of 18.3% during 2026 and 2035.

- Application-wise, we will have the Warehouse market segment taking the biggest market share of 35.5% in 2025.

Significant Growth Factors

Market Trends is a software that can bring a great deal of growth to the Robot fleet management business because of the following reasons:

- Amplifying the International Climate Policies and Methane Reduction Targets: The increasing international obligations of minimizing greenhouse gas emissions are greatly increasing the application of Robot fleet management. Almost one-third of global warming has been explained by methane since the pre-industrial period, and that is why methane is a center of focus in climate mitigation policies. The International Energy Agency shows that energy processes in the world produce more than 135 million tonnes of methane emissions in 2023. Governments and global bodies are also coming up with more stringent methane reporting systems and schemes to track emissions to achieve climate goals. This has led to a trend where industries are increasingly investing in more sophisticated methods of monitoring methane, including continuous gas sensors, optical gas imaging technologies, and remote sensing technology to enhance the visibility of emissions and adherence to environmental standards.

- Increasing the demand for Continuous Emission Monitoring in the Energy Infrastructure: Energy infrastructure, including natural gas production facilities, pipeline networks and LNG terminals, is a significant contributor of methane leaks. According to the estimates of the International Energy Agency, the oil and gas industry generates more than a third of the world’s emissions of methane as a result of human activities. These are numerous emissions caused by equipment leakages, operations in venting and old age pipeline infrastructures. The regulatory authorities are thus compelling the energy firms to adopt leak detection and repair initiatives as well as installing the continuous monitoring equipment. Fixed sensor networks, laser-based detectors, and optical imaging cameras, which are part of Robot fleet management systems, are rapidly being implemented to detect the leakage, minimize the loss of the product, and promote the safety of the operations of the energy facilities.

- Quick Improvement in Satellite and Remote Methane Detection Technologies: Technological breakthroughs are revolutionizing the method of detecting methane via satellite monitoring and aircraft monitoring, as well as drone-based monitoring. It has been reported by organizations like the United Nations Environment Programme that satellite monitoring systems can sense the occurrence of the huge events of methane super-emitters in various industries across the world. The high-resolution satellites and remote sensing technologies enable the governments and companies to trace the emission in geographic regions with large territories and trace the sources of the previously untraced emissions. These technologies contribute greatly to the effectiveness of the environmental monitoring programs and allow quicker reactions to the emission incidences, which will contribute to the global strategies of reducing methane.

What are the single Biggest Developments Reshaping the Robot Fleet Management Software Market Today?

- Stricter International Methane Emission Rules and climate obligations: Governments and environmental activists across the world are establishing stricter regulations to curb the emission of such a substance as it causes climatic changes significantly. Methane causes the rise in temperature of the world by almost 30 percent since the pre-industrial days that is why it is in the attention of the environmental policy. Although, it has certain global initiatives such as the Global Methane Pledge, where nations are called upon to reduce the quantity of the gas by at least 30 percent by the year 2030. The other sectors that produce oil and gas, waste management, and agriculture will therefore need to embrace suitable systems of measurement and reporting of methane. Such policy frameworks are accelerating the use of more complex technologies in the process of monitoring methane in large industrial complexes and energy systems.

- The Creation of Satellite-based Methane Surveillance Systems: Satellite observational technologies have transformed the way of monitoring methane since they have the capability of monitoring the performance of a vast area in an environmental setup. Methane plumes in industries, pipelines, landfills, and agricultural activities can now be detected with a high level of accuracy using high end earth-observation satellites. The space agencies such as the European Space Agency and the National Aeronautics and Space Administration assist in the missions of the satellites dedicated to the observation of greenhouse gases. The systems help in the correct emission data, which in turn helps the governments and corporations to acknowledge the previously unknown leaks of methane, improves the reporting of the environment, and manages the efficiency of the emission reduction programs.

- Raising Industry Investment in the ongoing Methane Detection Solutions: Industry and players in energy firms are significantly raising investments in methane detector equipment to support emission and operational efficiency. The oil and gas industry releases their emissions (millions of tonnes of methane) into the atmosphere annually, and it is often brought about by the leakage of equipment, venting and old facilities. To address these challenges, the corporations are adopting better ways of tracking the methane such as optical gas imaging cameras, fixed systems of sensors and drone sensors. These monitoring systems allow faster detection of leakages and solutions besides guaranteeing that organizations comply with environmental demands and reduce losses of products.

- Artificial Intelligence and Data Analysis in Monitoring Platforms: The present situation of Robot fleet management platforms is the introduction of artificial intelligence (AI), machine learning, and advanced data analytics to enhance the capabilities of the systems to detect and improve functional efficiency. With the help of AI-based applications, one will be able to analyze the enormous volumes of environmental measurements and identify the patterns of emissions, identifying the abnormalities and predicting the potential leakage of methane prior to its occurrence. Such intelligent monitoring systems also have automatic reporting facilities, predictive maintenance, and remote diagnostic capabilities that reduce the manual checking. As the trend is transferred to the domain of digital infrastructure and smart-based monitoring of the industry, AI-based Robot fleet management platforms become one of the main trends that define the future of the world market development.

Category Wise Insights

By Component

What is the Reason Software is the Market Leader?

The market of robot fleet management software has the highest percentage of software since it is the platform that coordinates, controls, and optimizes the activities of a number of robots in an industrial setting. Fleet management software allows real-time tracking of autonomous robots in warehouses, manufacturing plants, and logistics facilities, optimization of routes, scheduling of tasks and performance analytics. Due to the trend of using large numbers of robots in industries, the demand to operate a centralized software platform to enable effective management of operations is rising at a high rate. The research shows that the use of automation in the world of warehouses has grown considerably, and thousands of robots work simultaneously in massive fulfillment centers. The increased level of robot density demands highly developed fleet management programs that are able to organize work and minimize the time of operation and enhance the productivity of the work.

Why is Service the Fastest-Growing Segment?

As the robotic fleet management software market is becoming more complex, services are becoming the most rapidly expanding element of the market because of the complexity of deploying and maintaining the large robot fleet. Professional services needed to help organizations in the deployment of robotic systems include system integration, software customization, training, maintenance, and technical support. With the implementation of robotics in various processes in the industries by service providers, the service providers are significant in the integration of fleet management platforms with enterprise systems like warehouse management systems (WMS) and enterprise resource planning (ERP). Besides, firms are turning to managed services and cloud-based support frameworks to preserve robotic fleets and to guarantee a constant performance of the systems.

By Robot Type

So why are Ground Robots the Leader of the Market?

The largest portion of the robot fleet management software market is composed of ground robots, as there are numerous applications of ground robots in warehousing, logistics, manufacturing, and agricultural processes. Warehouses and factories are also widely used to deploy autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) that are used to move products, handle inventory, and assist production lines. The sudden increase in e-commerce and automated logistics facilities has enhanced the use of ground robots around the globe. Huge distribution centers may have hundreds or thousands of mobile robots at the same time to sort and move materials. The more robots work in the industry setting, the more complex fleet management software should be used to organize the motion and work of robots.

What makes Aerial Robots (Drones) the Fastest-Growing Segment?

Drone robots, officially called aerial robots are rapidly emerging as the most rapidly expanding category of robot fleet management software with their usage in inspection, surveillance, mapping, and delivery services. Drones have the ability to cover vast areas within a short period of time and reach areas that ground robots might find challenging/risky. The construction industry, agriculture sector, infrastructure inspection, and logistics are the sectors that are seeing a surge in the use of drone fleets to carry out aerial inspection and data gathering. The increasing demand for real-time aerial monitoring and automated monitoring systems are contributing to the necessity of a more sophisticated fleet management platform that can coordinate a number of drones and control their routes in addition to efficiently analyzing the obtained data.

By Application

Why is Warehouse the Largest Application Segment?

The type of warehouse represents the most significant application market in the robot fleet management software industry because the growth of automated logistics and e-commerce fulfillment centers is fast. Contemporary warehouses use autonomous robots in the form of fleets to accomplish the task of order picking, transportation of inventory, and sorting. Due to the globalization of e-commerce, automated fulfillment centers have increased significantly with hundreds of robots working at the same time to ensure efficiency and less reliance on labour. The fleet management software is important in the coordination of these robots to avoid congestion in the warehouses and to streamline workflow. With online retailing becoming more popular, warehouses are putting more resources in robotics and sophisticated software systems to simplify logistics processes.

Why is the Logistics and Delivery the Rapidly Expanding Application Segment?

The quickest increase in the robot fleet management software market is in logistics and delivery apps as organizations consider autonomous solutions to optimize the last-mile delivery and supply chain. Robots of delivery and autonomous vehicles are under testing and implementation in urban settings, campuses, and business zones to deliver parcels and goods. Growing interest in the faster delivery rates and lower operational expenses is stimulating the attraction of robotic delivery services by the logistics companies. Fleet management software helps the company to trace delivery routes, control fleets of robots, and provide safe and efficient work. The use of fleet management software in the logistics systems is likely to increase substantially as autonomous delivery technologies are becoming a commonplace occurrence.

By Device Type

What is Desktop/Laptop the Largest Segment?

The market of robot fleet management software is dominated by desktop and laptop systems since they offer operators detailed control dashboards and powerful data analytics. These devices are normally utilized in the control centers by fleet managers and system administrators to track the activities of the robots, control workflows, and identify performance metrics. Desktop-based interfaces enable the connection to enterprise software systems and give an insight into all the operations, which can help organizations streamline robotic work. Desktop systems in centralized control rooms often have large industrial projects with many robots being remotely controlled, and hence desktop systems are the most typical type of device used in fleet management platforms.

Why is Smartphones the fastest-growing Segment?

Mobile applications are making smartphones the quickest expanding category of devices within the robot fleet management software industry, since it is now possible to remotely monitor and control robotic fleets. The mobile platforms enable the supervisors and technicians to monitor the status of robots, get alerts, and control operations regardless of their location. As the use of cloud-based fleet management systems is growing, there has been an influx of mobile interfaces in operations monitoring and maintenance. Real-time notifications, fast troubleshooting features, and mobile access to the operational data of the robotic system are driving the ever-increasing use of smartphones to control the robot systems in the industries.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 2.93 billion |

| Projected Market Size in 2035 | USD 12.67 billion |

| Market Size in 2025 | USD 2.5 billion |

| CAGR Growth Rate | 17.7% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Component, Robot Type, Application, Device Type and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

Why did Asia Pacific Dominate the Market in 2025?

In 2025, the Asia-Pacific region is expected to hold a major share of the Robot fleet management market due to rapid industrial expansion and rising energy demand. Countries such as China and India together represent a major portion of global industrial activity and energy consumption, which increases the need for emission monitoring technologies. The region also hosts large coal mining operations, natural gas infrastructure, and expanding waste management facilities, all of which can generate methane emissions. Governments across Asia-Pacific are strengthening environmental monitoring frameworks and launching methane reduction programs to meet climate commitments. These initiatives are encouraging industries to deploy advanced Robot fleet management technologies such as remote sensing systems, gas detection sensors, and automated emission monitoring platforms across energy infrastructure and industrial operations.

China Market Trends

China is one of the most significant markets for Robot fleet management technologies due to its large industrial base and extensive energy production activities. The country accounts for nearly 30% of global manufacturing output, creating strong demand for environmental monitoring solutions across heavy industries such as steel, chemicals, and cement production. China also operates one of the world’s largest coal mining industries, where methane emissions are a key environmental concern. To address climate challenges, the government has introduced stricter environmental policies and pledged to achieve carbon neutrality by 2060. These policy initiatives are encouraging companies to implement advanced Robot fleet management technologies, including satellite-based observation systems, automated gas sensors, and digital environmental monitoring platforms.

Why is North America Experiencing Steady Growth?

North America is witnessing steady growth in the Robot fleet management market due to strong regulatory frameworks and the presence of advanced environmental monitoring infrastructure. The region hosts one of the world’s largest oil and gas industries, with extensive pipeline networks and production facilities that require continuous emission monitoring. Regulatory agencies are implementing stricter methane leak detection and reporting requirements, prompting companies to deploy advanced monitoring technologies such as optical gas imaging cameras, drone-based inspections, and satellite monitoring systems. The growing adoption of digital environmental monitoring platforms is also helping industries improve emission transparency and regulatory compliance.

U.S. Market Trends

The United States represents a major market for Robot fleet management technologies due to strict environmental policies and extensive energy infrastructure. The country operates one of the largest natural gas production and distribution networks globally, which requires continuous monitoring to prevent methane leakage. Regulations implemented by the United States Environmental Protection Agency require companies to implement methane leak detection and repair programs across energy facilities. In addition, the United States operates thousands of power generation facilities and industrial plants, creating strong demand for Robot fleet management systems to ensure regulatory compliance and environmental transparency.

Why is Europe Focusing on Sustainability and Efficiency?

Europe represents a key region in the Robot fleet management market due to its strong climate policies and commitment to emission reduction. The region aims to reduce greenhouse gas emissions by at least 55% by 2030 compared with 1990 levels as part of its climate strategy. Thousands of industrial facilities across Europe are required to monitor and report emissions under strict environmental regulations. Growing investments in renewable energy, carbon capture technologies, and environmental monitoring infrastructure are encouraging industries to adopt advanced Robot fleet management systems that improve compliance, operational transparency, and sustainability performance.

Germany Market Trends

Germany is one of the leading Robot fleet management markets in Europe due to its strong industrial sector and strict environmental regulations. Germany accounts for nearly one-quarter of Europe’s industrial output, with major industries including automotive manufacturing, chemicals, energy production, and heavy manufacturing. Many large industrial facilities in the country are required to operate continuous emission monitoring systems to comply with environmental standards. Germany has also established ambitious climate goals aimed at achieving net-zero greenhouse gas emissions by 2045, which is encouraging industries to invest in advanced methane detection and monitoring technologies.

Why is the Middle East & Africa Region Experiencing Growth?

The Middle East and Africa region is experiencing increasing demand for Robot fleet management technologies due to expanding oil and gas production and growing environmental awareness. The Middle East accounts for a significant portion of global crude oil production, with countries such as Saudi Arabia and the United Arab Emirates operating large-scale refining and petrochemical facilities. These operations require advanced monitoring technologies to detect methane leaks and maintain environmental compliance. In addition, several African countries are expanding mining and energy projects, which are increasing the need for Robot fleet management solutions to manage industrial emissions and support sustainable development initiatives.

Top Players in the Market and Their Offerings

- ABB Ltd.

- Clearpath Robotics Inc.

- Fetch Robotics (Zebra Technologies)

- Locus Robotics

- Boston Dynamics

- Omron Corporation

- Geekplus Technology Co. Ltd.

- MiR (Mobile Industrial Robots)

- Seegrid Corporation

- KUKA AG

- GreyOrange

- Aethon Inc.

- BlueBotics SA

- RoboDK

- Vecna Robotics

- inVia Robotics

- Savioke

- Magazino GmbH

- Swisslog Holding AG

- 6 River Systems (Shopify)

- Others

Key Developments

The Robot fleet management market is undergoing radical technological shifts with the increased number of climate commitments and the need to be able to monitor emissions accurately. More is being done to identify the methane emissions to the atmosphere by the firms within the oil and gas sector, terrestrial landfills, and farmlands using satellites, aircraft-based sensors, and AI-driven emissions analysis. The rising satellites and advanced detection systems are increasing the potential of determining the source of methane emissions over a large geographical area and providing solutions to curb climate change in the world.

- Japanese satellite GOSAT-GW, which will be launched in June 2025, will contribute to monitoring all greenhouse gases like methane on the global scale. The satellite will enable the scientists and governments to see the greenhouse-gas emissions with great detail, besides better understanding the climate patterns.

- In July 2025, according to the Environmental Defense Fund, the satellite, which is designed to measure the level of methane emission to the atmosphere, MethaneSAT, lost contact with the earth after it was launched. However, the preliminary sources of missions data helped to verify the possibility of the satellite systems to trace the leaks of methane to the environment with the help of the infrastructure based on fossil fuels and also be involved in the work devoted to the minimization of the emissions.

These developments indicate a rise in the application of satellite monitoring systems, aerial detection systems, and more robust environmental analytics systems to track the emissions of methane in the world. Since remote sensing and data analytics are still being developed and improved, the Robot fleet management technologies will become an obligatory tool of the governments and other industries willing to restrict the emission of greenhouse gases and attain the climate goals.

The Robot Fleet Management Software Market is segmented as follows:

By Component

- Software

- Service

By Robot Type

- Ground Robot

- Aerial Robot (Drone)

By Application

- Industrial/Manufacturing

- Warehouse

- Logistics & Delivery

- Automotive

- Construction & Infrastructure

- Agriculture

- Healthcare

- Autonomous Shuttles

- Others

By Device Type

- Desktop/Laptop

- Smartphone

- Tablet

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Robot Fleet Management Software by Segments

- 2.1.2. Robot Fleet Management Software by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Robot Fleet Management Software Market Attractiveness Analysis, By Component

- 2.2.3. Robot Fleet Management Software Market Attractiveness Analysis, By Robot Type

- 2.2.4. Robot Fleet Management Software Market Attractiveness Analysis, By Application

- 2.2.5. Robot Fleet Management Software Market Attractiveness Analysis, By Device Type

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Amplifying the International Climate Policies and Methane Reduction Targets

- 3.1.2. Increasing the demand of Continuous Emission Monitoring in the Energy Infrastructure

- 3.1.3. Quick Improvement in Satellite and Remote Methane Detection Technologies

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Robot Fleet Management Software Market – By Component

- 4.1. Component Market Overview, By Component Segment

- 4.1.1. Robot Fleet Management Software Market Revenue Share, By Component , 2025 & 2035

- 4.1.2. Software

- 4.1.3. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Service

- 4.1.7. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Component Market Overview, By Component Segment

- Chapter 5. Robot Fleet Management Software Market – By Robot Type

- 5.1. Robot Type Market Overview, By Robot Type Segment

- 5.1.1. Robot Fleet Management Software Market Revenue Share, By Robot Type , 2025 & 2035

- 5.1.2. Ground Robot

- 5.1.3. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Aerial Robot (Drone)

- 5.1.7. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Robot Type Market Overview, By Robot Type Segment

- Chapter 6. Robot Fleet Management Software Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Robot Fleet Management Software Market Revenue Share, By Application , 2025 & 2035

- 6.1.2. Industrial/Manufacturing

- 6.1.3. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Warehouse

- 6.1.7. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Logistics & Delivery

- 6.1.11. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1.14. Automotive

- 6.1.15. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.17. Key Market Trends, Growth Factors, & Opportunities

- 6.1.18. Construction & Infrastructure

- 6.1.19. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.20. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.21. Key Market Trends, Growth Factors, & Opportunities

- 6.1.22. Agriculture

- 6.1.23. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.24. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.25. Key Market Trends, Growth Factors, & Opportunities

- 6.1.26. Healthcare

- 6.1.27. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.28. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.29. Key Market Trends, Growth Factors, & Opportunities

- 6.1.30. Autonomous Shuttles

- 6.1.31. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.32. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.33. Key Market Trends, Growth Factors, & Opportunities

- 6.1.34. Others

- 6.1.35. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 6.1.36. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.37. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Robot Fleet Management Software Market – By Device Type

- 7.1. Device Type Market Overview, By Device Type Segment

- 7.1.1. Robot Fleet Management Software Market Revenue Share, By Device Type , 2025 & 2035

- 7.1.2. Desktop/Laptop

- 7.1.3. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 7.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.5. Key Market Trends, Growth Factors, & Opportunities

- 7.1.6. Smartphone

- 7.1.7. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 7.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.9. Key Market Trends, Growth Factors, & Opportunities

- 7.1.10. Tablet

- 7.1.11. Robot Fleet Management Software Share Forecast, By Region (USD Billion)

- 7.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 7.1.13. Key Market Trends, Growth Factors, & Opportunities

- 7.1. Device Type Market Overview, By Device Type Segment

- Chapter 8. Robot Fleet Management Software Market – Regional Analysis

- 8.1. Robot Fleet Management Software Market Overview, By Region Segment

- 8.1.1. Global Robot Fleet Management Software Market Revenue Share, By Region, 2025 & 2035

- 8.1.2. Global Robot Fleet Management Software Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 8.1.3. Global Robot Fleet Management Software Market Revenue, By Component , 2026 – 2035

- 8.1.4. Global Robot Fleet Management Software Market Revenue, By Robot Type , 2026 – 2035

- 8.1.5. Global Robot Fleet Management Software Market Revenue, By Application , 2026 – 2035

- 8.1.6. Global Robot Fleet Management Software Market Revenue, By Device Type , 2026 – 2035

- 8.2. North America

- 8.2.1. North America Robot Fleet Management Software Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.2.2. North America Robot Fleet Management Software Market Revenue, By Component , 2026 – 2035

- 8.2.3. North America Robot Fleet Management Software Market Revenue, By Robot Type , 2026 – 2035

- 8.2.4. North America Robot Fleet Management Software Market Revenue, By Application , 2026 – 2035

- 8.2.5. North America Robot Fleet Management Software Market Revenue, By Device Type , 2026 – 2035

- 8.2.6. U.S. Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.7. Canada Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.8. Mexico Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.2.9. Rest of North America Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe Robot Fleet Management Software Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.3.2. Europe Robot Fleet Management Software Market Revenue, By Component , 2026 – 2035

- 8.3.3. Europe Robot Fleet Management Software Market Revenue, By Robot Type , 2026 – 2035

- 8.3.4. Europe Robot Fleet Management Software Market Revenue, By Application , 2026 – 2035

- 8.3.5. Europe Robot Fleet Management Software Market Revenue, By Device Type , 2026 – 2035

- 8.3.6. Germany Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.7. France Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.8. U.K. Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.9. Russia Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.10. Italy Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.11. Spain Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.12. Netherlands Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.3.13. Rest of Europe Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Robot Fleet Management Software Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.4.2. Asia Pacific Robot Fleet Management Software Market Revenue, By Component , 2026 – 2035

- 8.4.3. Asia Pacific Robot Fleet Management Software Market Revenue, By Robot Type , 2026 – 2035

- 8.4.4. Asia Pacific Robot Fleet Management Software Market Revenue, By Application , 2026 – 2035

- 8.4.5. Asia Pacific Robot Fleet Management Software Market Revenue, By Device Type , 2026 – 2035

- 8.4.6. China Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.7. Japan Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.8. India Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.9. New Zealand Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.10. Australia Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.11. South Korea Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.12. Taiwan Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.4.13. Rest of Asia Pacific Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.5. The Middle-East and Africa

- 8.5.1. The Middle-East and Africa Robot Fleet Management Software Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.5.2. The Middle-East and Africa Robot Fleet Management Software Market Revenue, By Component , 2026 – 2035

- 8.5.3. The Middle-East and Africa Robot Fleet Management Software Market Revenue, By Robot Type , 2026 – 2035

- 8.5.4. The Middle-East and Africa Robot Fleet Management Software Market Revenue, By Application , 2026 – 2035

- 8.5.5. The Middle-East and Africa Robot Fleet Management Software Market Revenue, By Device Type , 2026 – 2035

- 8.5.6. Saudi Arabia Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.7. UAE Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.8. Egypt Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.9. Kuwait Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.10. South Africa Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.5.11. Rest of the Middle East & Africa Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.6. Latin America

- 8.6.1. Latin America Robot Fleet Management Software Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 8.6.2. Latin America Robot Fleet Management Software Market Revenue, By Component , 2026 – 2035

- 8.6.3. Latin America Robot Fleet Management Software Market Revenue, By Robot Type , 2026 – 2035

- 8.6.4. Latin America Robot Fleet Management Software Market Revenue, By Application , 2026 – 2035

- 8.6.5. Latin America Robot Fleet Management Software Market Revenue, By Device Type , 2026 – 2035

- 8.6.6. Brazil Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.7. Argentina Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.6.8. Rest of Latin America Robot Fleet Management Software Market Revenue, 2026 – 2035 (USD Billion)

- 8.1. Robot Fleet Management Software Market Overview, By Region Segment

- Chapter 9. Competitive Landscape

- 9.1. Company Market Share Analysis – 2025

- 9.1.1. Global Robot Fleet Management Software Market: Company Market Share, 2025

- 9.2. Global Robot Fleet Management Software Market Company Market Share, 2024

- 9.1. Company Market Share Analysis – 2025

- Chapter 10. Company Profiles

- 10.1. ABB Ltd.

- 10.1.1. Company Overview

- 10.1.2. Key Executives

- 10.1.3. Product Portfolio

- 10.1.4. Financial Overview

- 10.1.5. Operating Business Segments

- 10.1.6. Business Performance

- 10.1.7. Recent Developments

- 10.2. Clearpath Robotics Inc.

- 10.3. Fetch Robotics (Zebra Technologies)

- 10.4. Locus Robotics

- 10.5. Boston Dynamics

- 10.6. Omron Corporation

- 10.7. Geekplus Technology Co. Ltd.

- 10.8. MiR (Mobile Industrial Robots)

- 10.9. Seegrid Corporation

- 10.10. KUKA AG

- 10.11. GreyOrange

- 10.12. Aethon Inc.

- 10.13. BlueBotics SA

- 10.14. RoboDK

- 10.15. Vecna Robotics

- 10.16. inVia Robotics

- 10.17. Savioke

- 10.18. Magazino GmbH

- 10.19. Swisslog Holding AG

- 10.20. 6 River Systems (Shopify)

- 10.21. Others.

- 10.1. ABB Ltd.

- Chapter 11. Research Methodology

- 11.1. Research Methodology

- 11.2. Secondary Research

- 11.3. Primary Research

- 11.3.1. Analyst Tools and Models

- 11.4. Research Limitations

- 11.5. Assumptions

- 11.6. Insights From Primary Respondents

- 11.7. Why Custom Market Insights

- Chapter 12. Standard Report Commercials & Add-Ons

- 12.1. Customization Options

- 12.2. Subscription Module For Market Research Reports

- 12.3. Client Testimonials

List Of Figures

Figures No 1 to 34

List Of Tables

Tables No 1 to 51

Prominent Player

- ABB Ltd.

- Clearpath Robotics Inc.

- Fetch Robotics (Zebra Technologies)

- Locus Robotics

- Boston Dynamics

- Omron Corporation

- Geekplus Technology Co. Ltd.

- MiR (Mobile Industrial Robots)

- Seegrid Corporation

- KUKA AG

- GreyOrange

- Aethon Inc.

- BlueBotics SA

- RoboDK

- Vecna Robotics

- inVia Robotics

- Savioke

- Magazino GmbH

- Swisslog Holding AG

- 6 River Systems (Shopify)

- Others

FAQs

The key players in the market are ABB Ltd., Clearpath Robotics Inc., Fetch Robotics (Zebra Technologies), Locus Robotics, Boston Dynamics, Omron Corporation, Geekplus Technology Co. Ltd., MiR (Mobile Industrial Robots), Seegrid Corporation, KUKA AG, GreyOrange, Aethon Inc., BlueBotics SA, RoboDK, Vecna Robotics, inVia Robotics, Savioke, Magazino GmbH, Swisslog Holding AG, 6 River Systems (Shopify), Others.

Government controls are very crucial in determining the market of methane monitoring. The policies that are to be put in place to ensure that greenhouse gas emissions are minimized demand that industries identify, quantify, and report industrial facility, landfill, and energy infrastructure methane emissions. The Global Methane Pledge is yet another international program that aims to increase the efforts of countries to improve the monitoring and reduction of emissions.

The price is an important factor in the use of Robot fleet management technologies. Major energy providers typically invest in sophisticated monitoring systems, whereas smaller industrial plants can use cheaper portable detection systems. The constant technological development of sensors, drones, and remote monitoring platforms is slowly raising the cost minimization and making Robot fleet management solutions increasingly affordable and more available in industries.

The market suggests that, by the year 2035, the market shall have reached USD 12.67 billion due to the embracing of clouds, digital health, and AI-based healthcare institutions.

There is a likelihood that North America will occupy the top position in the market of Robot fleet management because the country has solid regulatory provisions and has environmental monitoring frameworks. The United States Environmental Protection Agency has regulations that enforce industries to identify and report the emissions of methane, so many industries have adopted advanced monitoring technologies in oil and gas production plants, pipelines, and industry activities.

The Asia-Pacific market is likely to have the highest CAGR in the Robot fleet management market because of the rate at which the region is industrializing, the growth in the energy infrastructure, and the increased awareness of the environment. China and India are among other countries that are tightening their methane emission control measures and investing in high-level environmental monitoring technologies in their oil and gas sector, mining, and waste management along with manufacturing industries.

Among the factors that have contributed to the development of the Robot fleet management market, there are increased environmental regulations and various global climate commitments to ensure that greenhouse emissions are reduced. The governments and industries are adopting the system of methane detection and reporting in energy and waste management, as well as in the agricultural industries. The rise in ESG promises and sustainability ambitions are also driving more towards the implementation of new sophisticated monitoring solutions, including satellite monitoring, IoT-based gas sensors, and AI-assisted emission monitoring and analytics solutions to ensure better transparency, regulatory disposition, and environmental capability.