Smart Grid Cybersecurity Market Size, Trends and Insights By Deployment Mode (On-Premise, Cloud), By Security Type (Endpoint, Network, Application, Database), By Application (Consumption, Generation, Distribution & Control), and By Region - Global Industry Overview, Statistical Data, Competitive Analysis, Share, Outlook, and Forecast 2026 – 2035

Report Snapshot

CAGR: 28.2%

| Study Period: | 2026-2035 |

| Fastest Growing Market: | Asia Pacific |

| Largest Market: | North America |

Major Players

- IBM

- Siemens

- Cisco Systems

- BAE Systems

- Others

Reports Description

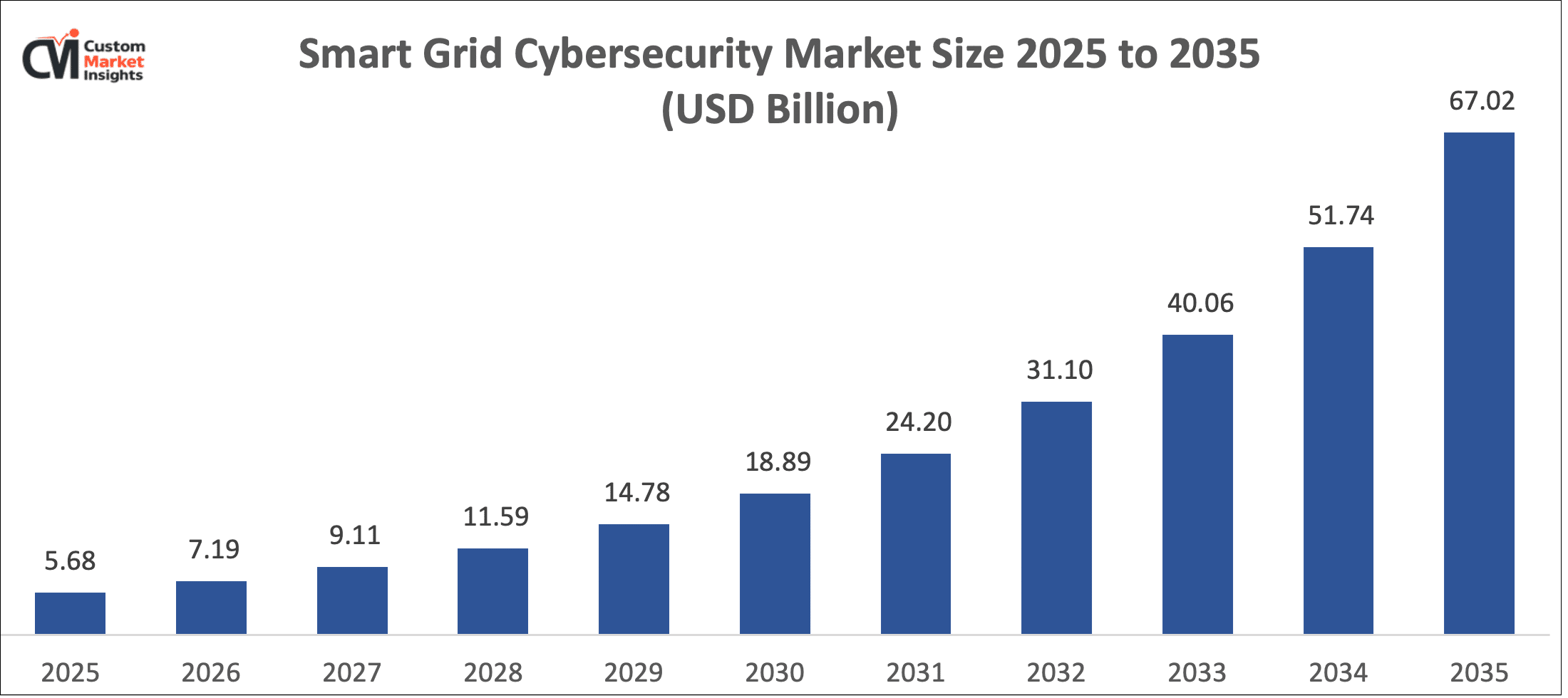

Smart grid cybersecurity market has a projected USD 7.19 billion in the year 2026, USD 67.02 billion in the year 2035 and a projected CAGR of 28.2% between the years 2026 and 2035. The rise in the market is mainly as a result of the growing international attention to decreasing the energy, waste, and agricultural activities that contribute to the emission of methane. Over a shorter time span, Methane has an extremely high global warming potential compared to carbon dioxide, which has enhanced global climate efforts and regulation. As a result, governments, environmental agencies and industries are embracing new sophisticated methane detection systems like satellite monitoring and optical gas imaging as well as sensor-based leak detection systems to enhance better transparency of the emissions and compliance with the environment.

Market Highlight

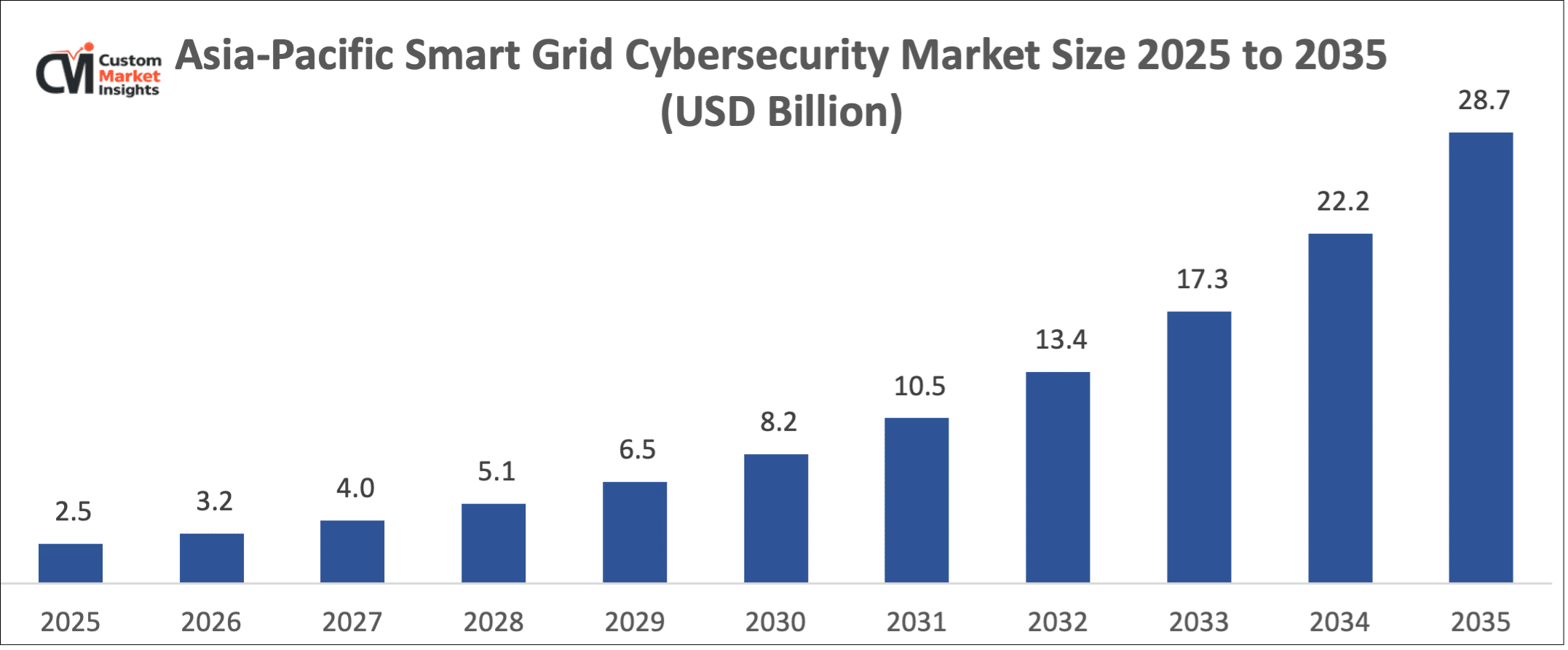

- Asia Pacific is the leader and had a market share of 45% in 2025.

- The growth of North America in the years 2026 to 2035 will be by 28.6%.

- 5% of the market share had been occupied by the On-Premise segment by deployment mode in 2025.

- By Security type, the Endpoint Security segment shall demonstrate the greatest CAGR of 28.8% of 2026-2035.

- Application-wise, 60.5% of the market share of the Distribution and Control segment will be the largest in 2025.

Significant Growth Factors

The Smart grid cybersecurity Market Trends have great growth potential because of the following factors:

- Expanding Methane Emission Regulations Across Industrial Sectors: Governments all over the world are tightening their belts regarding the regulation of the emission of methane by the oil and gas industry, mining, waste management, and agricultural sectors. The global warming potential of methane is greater than that of carbon dioxide by more than 25 times in 100 years and this has placed it at the center of climate policy. Strict monitoring, reporting and verification to follow the methane emissions in industrial plants are being introduced by the environmental authorities. Consequently, businesses are implementing methane detection tools that include infrared gas imaging cameras and fixed gas sensors, in addition to automated monitoring systems to make sure that organizations comply with the environmental laws and to enhance operational transparency.

- Growing the use of Leak Detection Technology in the Oil and Gas Industry: The oil and gas industry has been one of the biggest emitters of man-made methane gases, with leaks in production, processing, storage, and transportation processes. Methane leakages are especially susceptible in the pipeline networks, compressor stations and storage facilities because of equipment wear and inefficiency in the work. In response to such concerns, energy companies are now adopting Leak Detection and Repair (LDAR) programs that have been backed up with sophisticated methane monitoring systems. Laser-based analyzers, portable gas detectors, and drone-based inspection systems among others are solutions that are being implemented to detect leaks faster and mitigate gas loss and enhance safety in energy infrastructure.

- Increased Adoption of Solutions to Monitor Methane Through Advanced Analytics and Remote Monitoring Tools: Digital technologies are radically changing the process of monitoring methane due to the capabilities of artificial intelligence, cloud-based analytics, and remote sensors. The contemporary monitoring systems gather data through various sources, which are ground sensors, drones, satellites, and industrial monitoring systems. These datasets are analyzed using advanced analytics to identify abnormal emission patterns and sales and automatically report the environment. These technologies enable the companies to track the emission level in real time and react to the possible threats to the environment. With the continued adoption of electronic environmental management systems by industries, there has been an increasing demand for intelligent methane monitoring platforms in the global industries.

What are the Single Biggest Developments Reshaping the Smart Grid Cybersecurity Market Today?

- Global Methane Transparency and Reporting Initiatives: Global climate systems and other environmental partnerships are radically altering the market of methane monitoring by promoting open reporting of emissions. The governments are also imposing tougher standards in measurement and verification of methane emissions in various industries like the energy sector, agriculture, and waste management. It is estimated that the global emission of methane goes beyond 600 million tonnes in a year, and most of this is caused by human activity. In the quest to enhance transparency, the regulatory bodies are compelling firms to install continuous methane monitoring systems and high-technology leakage detecting technology throughout the production sites, pipeline systems, and industrial plants.

- Introduction of the High-Resolution Remote Sensing and Airborne Detection Systems: The technological advances in platforms of remote sensing, such as aircraft-mounted spectrometers and drone-based detection systems, are changing the ability to monitor methane. The technologies enable the quick detection of methane leakages at large energy facilities as well as in remote infrastructure where manual inspections are not feasible. Methane awareness campaigns have shown that a few large sources of emissions- commonly known as “super-emitters- can be involved in the overall emissions disproportionately. These emissions can be identified and their quantity can be measured, which is making industries resort to the use of high-precision monitoring systems in order to manage the environment better.

- Increasing Implementation of Long-term Monitoring Systems in Industry Plants: Continuous monitoring of the emissions is being done through permanent methane monitoring systems installed by industries. There is an implementation of fixed gas sensors, laser-based sensors, and real-time monitoring platforms in oil and gas production sites, petrochemical plants, landfills and coal mines. Constant monitoring will enable operators to identify the leaks of methane in question promptly and make the fixes much faster, minimizing the operational losses. These monitoring mechanisms also assist in meeting the environmental reporting requirement as well as enhancing safety and reliability in the industrial infrastructure.

- Further Adoption of Integrated Environmental Data Platforms: Current methane monitoring solutions are shifting towards integrated digital platforms where both satellite, ground sensor, drone and industrial monitoring equipment data are visible. Environmental management systems based on the cloud enable organizations to store the emission data in the same place, conduct sophisticated analytics, and automatically generate regulatory reports. These platforms will offer a unified perspective of the methane emission across operations by combining several sources of data on the activities. This move towards data based environmental management is assisting industries to develop better emission responsibility and enhance long-term mitigation plans on climate.

Category Wise Insights

By Deployment Mode

What is the reason why On-Premise is the Leader in the market?

The smart grid cybersecurity market is mostly on-premise deployment, as utility operators are more interested in having maximum control of critical infrastructure systems. The power grids are based on industrial control systems and SCADA networks to control electricity transmission and distribution on a spot basis. The International energy Agency indicates that the world is steadily accelerating its electricity needs, which implies that it requires a stable grid infrastructure. Most utilities use legacy operating technology environments that necessitate on-site cybersecurity systems in order to provide reliability, data privacy, and cyberattack protection for energy infrastructure.

Why is Cloud the Fastest-Growing Segment?

The most rapidly developing segment is cloud deployment because the area of power infrastructure gets more and more digitalized and the technologies of smart grids are introduced. Cybersecurity cloud solutions enable utilities to patrol grid networks, perform threat intelligence analysis, and update systems security across multiple sites on a real-time basis. There is the emergence of smart meters, distributed energy resources, and connected grid devices that are producing huge amounts of operation data. Cloud solutions allow scalable security monitoring and quicker threat detection to assist energy providers in securing more and more complex grid ecosystems at a lower cost of infrastructure management.

By Security Type

What is the reason why Network Security is the Leader of the Market?

The major part of the smart grid cybersecurity market is network security since the electric grid systems are based on large networks of communication between the control centers and substations and the power generation plants. Such networks have sensitive working information and instructions that regulate power circulation. Any cyberspace attack on grid communication infrastructure can destabilize the energy supply and undermine grid security. The utilities thus implement firewalls, intrusion detection systems, and network monitoring tools to ensure that they protect data transmission as well as ensure that data is not accessed illegally by unauthorized parties in grid communication networks.

What is the fastest-growing Segment and why is Endpoint Security?

The area of endpoint security is the quickest expanding because the quantity of connected devices in the smart grid infrastructure grows fast. Heavy use of smart meters, sensors, intelligent electronic devices, and remote terminal units has become common in the current power networks. Every linked endpoint will be a potential entry point of cyber threats. The utilities are hence investing in endpoint protection systems monitoring device activity, spyware, and unauthorized access of the system to ensure reliability and security of the distributed grid infrastructure.

By Application

Why is Distribution and Control the Largest Application Segment?

The most significant market share in the smart grid cybersecurity market belongs to the distribution and control systems since they are the working basis of power systems. These control substations, transformers, and grid automation systems that control the movement of power throughout the electricity systems in regions. With the advanced distribution management system and automated grid control platforms developed by utilities, the digital communication channels grow exponentially. Cybersecurity solutions will therefore be required to ensure that grid control systems are against cyber threats that might interfere with the supply of power or operations of vital infrastructure.

What Generation Is the Fastest-Growing Segment?

The most rapidly expanding segment of usage is power generation because of the high growth rates of renewable energy sources and distributed power generation systems. Contemporary power plants are dominated by digital monitoring systems, industrial control, and remote management systems. Cybersecurity is becoming a bigger threat with more and more connectivity of the generation assets and the grid networks. Power producers are hence investing in high-tech security systems in order to ensure that the turbines, control systems, and plant management networks are not subjected to cyberattacks that may cripple the production of electricity or destroy critical infrastructure.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 7.19 billion |

| Projected Market Size in 2035 | USD 67.02 billion |

| Market Size in 2025 | USD 5.68 billion |

| CAGR Growth Rate | 28.2% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Deployment Mode, Security Type, Application and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Regional Analysis

Asia Pacific -Why did Asia Pacific Dominate the Market in 2025?

Over the next decade, the Asia-Pacific region had the highest share of the smart grid cybersecurity market as a result of the fast growth of the smart grid infrastructure and increasing electricity demand. The region is being transformed with the digitalization of power grids in countries through smart meters, automated substations, and a sophisticated network of grid communication. Massive investments in renewable energy integration and grid modernization projects are also being experienced in the region. With the further digitization of electricity networks, there is a higher threat of cyber-attacks against power infrastructure, which is why, to secure grid operations and maintain energy security, utilities and governments implement the latest cybersecurity systems.

China Market Trends

China is one of the biggest markets for smart grid cybersecurity since its electricity infrastructure is huge and there are current grid modernization projects. The nation has the biggest power transmission system in the world and is still growing the renewable power systems like wind and solar energy. Cyber threats to grid communication systems are now being given priority due to the millions of smart meters and digital grid devices across the country. The government spends a lot of money on cybersecurity technologies to protect energy infrastructure and facilitate the growth of smart grids and reliable provision of electricity in the industrial and residential sectors.

Why is North America Undergoing a Consistent Growth?

The smart grid cybersecurity market is gradually growing in North America because of a robust regulatory environment and the developed power grid infrastructure. Smart grid technologies have been extensively embraced in the region that encompasses intelligent substations, sophisticated metering infrastructure, and automated systems of grid control. Together with the rise in grid connectivity, utilities are exposed to rising cyber threats to the operation technology networks. The energy providers are thus spending on better cybersecurity measures like the network monitoring systems, threat detection systems, and security of the industrial control systems to safeguard the key energy infrastructure.

How Large is the American Market?

The United States continues to be one of the significant markets in smart grid cybersecurity because of the high level of digitalization of the electricity systems and effective regulation standards. The federal authorities like the North American Electric Reliability Corporation have adopted stringent cybersecurity requirements for the power grid operators. Thousands of power plants, substations, and transmission networks in the country are based on the use of digital control systems. With the utilities incorporating renewable and distributed energy resources into the grid, the need to have sophisticated cybersecurity platforms to secure the operational technology networks is on the increase.

The question is why Europe is emphasizing on Sustainability and Efficiency?

Europe is a market with significant promise to the smart grid cybersecurity market because of its great interest in energy transition and digital grid infrastructure. European nations are putting a lot into renewable energy, combining intelligent metering and automated grid platforms. The technologies make the grids more connected and data-sharing in and between the electricity networks, posing new cybersecurity challenges. To mitigate these threats, utilities in Europe are putting in place cybersecurity systems and improved threat detection systems in order to safeguard the energy infrastructure as they strive to facilitate the process of moving towards sustainable and efficient electricity systems.

Germany Market Trends

Germany has one of the most developed cybersecurity markets for smart grids in Europe because it has a high technology industrial system and a good policy on the energy transition. The nation is increasing production of renewable energy and upgrading grid infrastructure to facilitate decentralized generation of power. In Germany as well, there are numerous automated substations and digital systems of grid control, which need a strong level of cybersecurity. The energy policies of countries and stringent cybersecurity policies are pushing utilities towards adopting sophisticated network security, endpoint security and real-time threat monitoring systems.

What is the Reason behind the Growth of the Middle East and Africa Region?

The regions of the Middle East and Africa are booming markets for smart grid cybersecurity technologies because of the development of the power infrastructure and increasing energy demand. A large number of the nations in the area are undertaking smart grid modernization efforts in an attempt to enhance energy efficiency and grid reliability. The power plants, transmission systems, and renewable energy systems are becoming more and more interrelated with the help of digital monitoring systems. With such a rise in grid connectivity, utilities are implementing cybersecurity solutions to prevent cyberattacks on critical power infrastructure and maintain a consistent supply of power across the fast growing energy markets.

Top Players in the Market and Their Offerings

- IBM

- Siemens

- Cisco Systems

- BAE Systems

- Schneider Electric

- Honeywell International

- General Electric

- Lockheed Martin

- Palo Alto Networks

- Fortinet

- Others

Key Developments

Technological improvement is being experienced fast in the smart grid cybersecurity market, with governments and utilities developing and enhancing security of critical power infrastructure against cyberattacks. The growth of smart meters, computerized substations, and automated systems of grid control has heightened the demand for highly developed cybersecurity systems. The energy companies and technology providers are thus investing in threat detection systems, protection of industrial control systems, and security monitoring using AI to protect the modern electricity networks.

- In February 2025, Siemens has increased its utility operator cybersecurity by adding to the capabilities of its grid automation solutions. The upgrade centers on securing technology networks of operations in substations and control centers against cyber intrusions and unauthorized access.

- In April 2025, Schneider Electric released the new cybersecurity solutions that are specifically targeting the smart grid infrastructure. The platform is in use to enable utilities to track threats on grid communication networks, enhance endpoint defenses on the connected devices, and enhance the resilience of power distribution systems.

- Cisco Systems declared a further boost in its industrial cybersecurity architecture in March 2025, which would protect digital power networks. The solution combines network observation, secure connection, and threat intelligence to assist the energy providers to safeguard grid communication infrastructure and identify cyber threats in real time.

These trends outline the increased significance of cybersecurity frameworks, real-time threat monitoring, and industrial network protection in the current power systems. With continued digitization and interconnection of electricity networks, utilities are likely to speed up investments in cybersecurity technologies in smart grids to guarantee the reliability of operations and secure critical energy infrastructure.

The Smart Grid Cybersecurity Market is segmented as follows:

By Deployment Mode

- On-Premise

- Cloud

By Security Type

- Endpoint

- Network

- Application

- Database

By Application

- Consumption

- Generation

- Distribution & Control

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Contents

- Chapter 1. Report Introduction

- 1.1. Report Description

- 1.1.1. Purpose of the Report

- 1.1.2. USP & Key Offerings

- 1.2. Key Benefits For Stakeholders

- 1.3. Target Audience

- 1.4. Report Scope

- 1.1. Report Description

- Chapter 2. Market Overview

- 2.1. Report Scope (Segments And Key Players)

- 2.1.1. Smart Grid Cybersecurity by Segments

- 2.1.2. Smart Grid Cybersecurity by Region

- 2.2. Executive Summary

- 2.2.1. Market Size & Forecast

- 2.2.2. Smart Grid Cybersecurity Market Attractiveness Analysis, By Deployment Mode

- 2.2.3. Smart Grid Cybersecurity Market Attractiveness Analysis, By Security Type

- 2.2.4. Smart Grid Cybersecurity Market Attractiveness Analysis, By Application

- 2.1. Report Scope (Segments And Key Players)

- Chapter 3. Market Dynamics (DRO)

- 3.1. Market Drivers

- 3.1.1. Expanding Methane Emission Regulations Across Industrial Sectors

- 3.1.2. Growing the use of Leak Detection Technology in the Oil and Gas Industry

- 3.1.3. Increased Adoption of Solutions to Monitor Methane Through Advanced Analytics and Remote Monitoring Tools

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.5. Pestle Analysis

- 3.6. Porter Forces Analysis

- 3.7. Technology Roadmap

- 3.8. Value Chain Analysis

- 3.9. Government Policy Impact Analysis

- 3.10. Pricing Analysis

- 3.1. Market Drivers

- Chapter 4. Smart Grid Cybersecurity Market – By Deployment Mode

- 4.1. Deployment Mode Market Overview, By Deployment Mode Segment

- 4.1.1. Smart Grid Cybersecurity Market Revenue Share, By Deployment Mode , 2025 & 2035

- 4.1.2. On-Premise

- 4.1.3. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 4.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.5. Key Market Trends, Growth Factors, & Opportunities

- 4.1.6. Cloud

- 4.1.7. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 4.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 4.1.9. Key Market Trends, Growth Factors, & Opportunities

- 4.1. Deployment Mode Market Overview, By Deployment Mode Segment

- Chapter 5. Smart Grid Cybersecurity Market – By Security Type

- 5.1. Security Type Market Overview, By Security Type Segment

- 5.1.1. Smart Grid Cybersecurity Market Revenue Share, By Security Type, 2025 & 2035

- 5.1.2. Endpoint

- 5.1.3. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 5.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.5. Key Market Trends, Growth Factors, & Opportunities

- 5.1.6. Network

- 5.1.7. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 5.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.9. Key Market Trends, Growth Factors, & Opportunities

- 5.1.10. Application

- 5.1.11. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 5.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.13. Key Market Trends, Growth Factors, & Opportunities

- 5.1.14. Database

- 5.1.15. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 5.1.16. Comparative Revenue Analysis, By Country, 2025 & 2035

- 5.1.17. Key Market Trends, Growth Factors, & Opportunities

- 5.1. Security Type Market Overview, By Security Type Segment

- Chapter 6. Smart Grid Cybersecurity Market – By Application

- 6.1. Application Market Overview, By Application Segment

- 6.1.1. Smart Grid Cybersecurity Market Revenue Share, By Application, 2025 & 2035

- 6.1.2. Consumption

- 6.1.3. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 6.1.4. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.5. Key Market Trends, Growth Factors, & Opportunities

- 6.1.6. Generation

- 6.1.7. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 6.1.8. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.9. Key Market Trends, Growth Factors, & Opportunities

- 6.1.10. Distribution & Control

- 6.1.11. Smart Grid Cybersecurity Share Forecast, By Region (USD Billion)

- 6.1.12. Comparative Revenue Analysis, By Country, 2025 & 2035

- 6.1.13. Key Market Trends, Growth Factors, & Opportunities

- 6.1. Application Market Overview, By Application Segment

- Chapter 7. Smart Grid Cybersecurity Market – Regional Analysis

- 7.1. Smart Grid Cybersecurity Market Overview, By Region Segment

- 7.1.1. Global Smart Grid Cybersecurity Market Revenue Share, By Region, 2025 & 2035

- 7.1.2. Global Smart Grid Cybersecurity Market Revenue, By Region, 2026 – 2035 (USD Billion)

- 7.1.3. Global Smart Grid Cybersecurity Market Revenue, By Deployment Mode , 2026 – 2035

- 7.1.4. Global Smart Grid Cybersecurity Market Revenue, By Security Type, 2026 – 2035

- 7.1.5. Global Smart Grid Cybersecurity Market Revenue, By Application, 2026 – 2035

- 7.2. North America

- 7.2.1. North America Smart Grid Cybersecurity Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.2.2. North America Smart Grid Cybersecurity Market Revenue, By Deployment Mode , 2026 – 2035

- 7.2.3. North America Smart Grid Cybersecurity Market Revenue, By Security Type, 2026 – 2035

- 7.2.4. North America Smart Grid Cybersecurity Market Revenue, By Application, 2026 – 2035

- 7.2.5. U.S. Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.6. Canada Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.7. Mexico Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.2.8. Rest of North America Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe Smart Grid Cybersecurity Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.3.2. Europe Smart Grid Cybersecurity Market Revenue, By Deployment Mode , 2026 – 2035

- 7.3.3. Europe Smart Grid Cybersecurity Market Revenue, By Security Type, 2026 – 2035

- 7.3.4. Europe Smart Grid Cybersecurity Market Revenue, By Application, 2026 – 2035

- 7.3.5. Germany Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.6. France Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.7. U.K. Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.8. Russia Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.9. Italy Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.10. Spain Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.11. Netherlands Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.3.12. Rest of Europe Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Smart Grid Cybersecurity Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.4.2. Asia Pacific Smart Grid Cybersecurity Market Revenue, By Deployment Mode , 2026 – 2035

- 7.4.3. Asia Pacific Smart Grid Cybersecurity Market Revenue, By Security Type, 2026 – 2035

- 7.4.4. Asia Pacific Smart Grid Cybersecurity Market Revenue, By Application, 2026 – 2035

- 7.4.5. China Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.6. Japan Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.7. India Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.8. New Zealand Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.9. Australia Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.10. South Korea Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.11. Taiwan Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.4.12. Rest of Asia Pacific Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.5. The Middle-East and Africa

- 7.5.1. The Middle-East and Africa Smart Grid Cybersecurity Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.5.2. The Middle-East and Africa Smart Grid Cybersecurity Market Revenue, By Deployment Mode , 2026 – 2035

- 7.5.3. The Middle-East and Africa Smart Grid Cybersecurity Market Revenue, By Security Type, 2026 – 2035

- 7.5.4. The Middle-East and Africa Smart Grid Cybersecurity Market Revenue, By Application, 2026 – 2035

- 7.5.5. Saudi Arabia Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.6. UAE Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.7. Egypt Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.8. Kuwait Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.9. South Africa Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.5.10. Rest of the Middle East & Africa Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.6. Latin America

- 7.6.1. Latin America Smart Grid Cybersecurity Market Revenue, By Country, 2026 – 2035 (USD Billion)

- 7.6.2. Latin America Smart Grid Cybersecurity Market Revenue, By Deployment Mode , 2026 – 2035

- 7.6.3. Latin America Smart Grid Cybersecurity Market Revenue, By Security Type, 2026 – 2035

- 7.6.4. Latin America Smart Grid Cybersecurity Market Revenue, By Application, 2026 – 2035

- 7.6.5. Brazil Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.6. Argentina Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.6.7. Rest of Latin America Smart Grid Cybersecurity Market Revenue, 2026 – 2035 (USD Billion)

- 7.1. Smart Grid Cybersecurity Market Overview, By Region Segment

- Chapter 8. Competitive Landscape

- 8.1. Company Market Share Analysis – 2025

- 8.1.1. Global Smart Grid Cybersecurity Market: Company Market Share, 2025

- 8.2. Global Smart Grid Cybersecurity Market Company Market Share, 2024

- 8.1. Company Market Share Analysis – 2025

- Chapter 9. Company Profiles

- 9.1. IBM

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Product Portfolio

- 9.1.4. Financial Overview

- 9.1.5. Operating Business Segments

- 9.1.6. Business Performance

- 9.1.7. Recent Developments

- 9.2. Siemens

- 9.3. Cisco Systems

- 9.4. BAE Systems

- 9.5. Schneider Electric

- 9.6. Honeywell International

- 9.7. General Electric

- 9.8. Lockheed Martin

- 9.9. Palo Alto Networks

- 9.10. Fortinet

- 9.11. Others.

- 9.1. IBM

- Chapter 10. Research Methodology

- 10.1. Research Methodology

- 10.2. Secondary Research

- 10.3. Primary Research

- 10.3.1. Analyst Tools and Models

- 10.4. Research Limitations

- 10.5. Assumptions

- 10.6. Insights From Primary Respondents

- 10.7. Why Custom Market Insights

- Chapter 11. Standard Report Commercials & Add-Ons

- 11.1. Customization Options

- 11.2. Subscription Module For Market Research Reports

- 11.3. Client Testimonials

List Of Figures

Figures No 1 to 25

List Of Tables

Tables No 1 to 46

Prominent Player

- IBM

- Siemens

- Cisco Systems

- BAE Systems

- Schneider Electric

- Honeywell International

- General Electric

- Lockheed Martin

- Palo Alto Networks

- Fortinet

- Others

FAQs

The key players in the market are IBM, Siemens, Cisco Systems, BAE Systems, Schneider Electric, Honeywell International, General Electric, Lockheed Martin, Palo Alto Networks, Fortinet, Others.

Regulations by the government contribute significantly to the market of the smart grid cybersecurity. Strict cybersecurity standards are being proposed by regulatory authorities to ensure that critical power infrastructure is not exposed to cyberattacks. Institutions like North American Electric Reliability Corporation implement security compliance systems of utilities that handle power grids. Such policies make utilities adopt superior cybersecurity systems to protect grid communication networks and ensure stable electricity supply.

Cybersecurity technologies of the smart grid have a significant role in pricing in adoption. Endpoint protection, threat monitoring systems and network security are common across large utility operators who deploy comprehensive cybersecurity platforms. Smaller energy providers, however, can first apply more affordable security solutions. With the maturity of cybersecurity technologies and their higher scalability, the costs of implementation are slowly dropping, allowing their use by more power utilities.

By 2035, the market, according to the market, will have reached USD 67.02 billion, due to the adoption of the clouds, digital health, and AI-based healthcare facilities.

The smart grid cybersecurity market is projected to be dominated by North America because it is the place where smart grid technologies are widely implemented and where the activity of the regulators is high. In the United States and Canada, electricity networks of energy companies are highly digitalized. The high security requirements regarding the security of critical infrastructure is urging utilities to invest in more sophisticated cybersecurity systems to protect the power grid infrastructure against cyber-attacks.

Asia-Pacific will experience the greatest CAGR in the market of smart grid cybersecurity because the modernization of a grid and the growth of electricity infrastructure is very rapid. Smart meters, renewable energy integration and digital grid systems are some of the areas that countries like China and India are investing a lot in. Such advances raise the cost of modern technology needed to secure grid communications networks and energy management systems.

The high pace of digitalization of electricity networks and the growth of cyber threats to critical energy infrastructure are the two main factors that drive the smart grid cybersecurity market. Smart meters, automated substations, and grid communication networks are being installed by utilities and need an advanced security protection. Governments and power operators are thus investing in cybersecurity platforms to protect the work technology infrastructure, interruption of services and to make sure that there is reliable power supply through the contemporary electricity grids.